|

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-275898

|

||

|

The information in this preliminary terms supplement is not complete and may be changed.

|

|||

|

Preliminary Terms Supplement

Subject to Completion:

Dated April 24, 2024

Pricing Supplement Dated April __, 2024, to the Product Prospectus Supplement ERN-EI-1, the Prospectus Supplement and the Prospectus, Each Dated December 20, 2023

|

$

Auto-Callable Geared Buffered Notes Linked

to the Lesser Performing of Two Equity

Indices, due October 28, 2025

Royal Bank of Canada

|

||

Royal Bank of Canada is offering Auto-Callable Geared Buffered Notes (the “Notes”) linked to the lesser performing of two equity indices (each, a “Reference Asset,” and

collectively, the “Reference Assets”). The Notes are our senior unsecured obligations, will pay a semi-annual coupon at the interest rate specified below, and will have the terms described in the documents

set forth above, as supplemented or modified by this terms supplement.

|

Reference Assets

|

Initial Levels*

|

Buffer Levels**

|

||

|

Nasdaq-100 Index® ("NDX")

|

17,471.47

|

13,977.18, which is 80% of its Initial Level

|

||

|

Russell 2000® Index ("RTY")

|

2,002.643

|

1,602.114, which is 80% of its Initial Level

|

* The Initial Level of each Reference Asset is its closing level on April 23, 2024 (the "Strike Date").

** Rounded to two decimal places in the case of the NDX and three decimal places in the case of the RTY.

The Notes do not guarantee any return of principal at maturity. All payments on the Notes are subject to our credit risk.

Investing in the Notes involves a number of risks. See “Selected Risk Considerations” beginning on page P-8 of this terms supplement, and “Risk Factors” beginning on page S-3 of

the prospectus supplement, on page PS-4 of the product prospectus supplement, each dated December 20, 2023.

The Notes will not constitute deposits insured by the Canada Deposit Insurance Corporation, the U.S. Federal Deposit Insurance

Corporation or any other Canadian or U.S. government agency or instrumentality. The Notes are not subject to conversion into our common shares under subsection 39.2(2.3) of the Canada Deposit Insurance Corporation Act.

Neither the Securities and Exchange Commission (the "SEC") nor any state securities commission has approved or disapproved of the Notes or determined that this terms

supplement is truthful or complete. Any representation to the contrary is a criminal offense.

|

Issuer:

|

Royal Bank of Canada

|

Stock Exchange

Listing:

|

None

|

|

Trade Date:

|

April 25, 2024

|

Principal Amount:

|

$1,000 per Note

|

|

Issue Date:

|

April 30, 2024

|

Coupon Payments:

|

The Coupon Payments will be paid in equal semi-annual installments at the rate of 8.45% per annum.

|

|

Observation Dates:

|

Semi-annual, as set forth below

|

Final Level:

|

For each Reference Asset, its closing level on the Valuation Date.

|

|

Maturity Date:

|

October 28, 2025

|

||

|

Payment at Maturity (if

not previously called

and held to maturity):

|

If the Notes are not previously called, we will pay you at maturity an amount in cash based on the Final Level of the Lesser Performing Reference Asset:

For each $1,000 in principal amount of the Notes, $1,000 plus the final Coupon Payment, unless the Final Level of either Reference Asset is less than

its respective Buffer Level.

If the Final Level of either Reference Asset is less than its Buffer Level, then the investor will receive at maturity, in addition to the final Coupon

Payment, an amount in cash equal to, for each $1,000 in principal amount, the sum of:

$1,000 + [$1,000 x (Percentage Change of the Lesser Performing Reference Asset + 20%) x (100/80)]

In this case, investors could lose some or all of their investment at maturity.

|

||

|

Lesser Performing

Reference Asset:

|

The Reference Asset with the lowest Percentage Change.

|

||

|

Call Feature:

|

If the closing level of each Reference Asset is greater than or equal to its Initial Level starting on October 23, 2024 or on any semi-annual Observation Date thereafter, the Notes will be

automatically called for 100% of their principal amount, plus the Coupon applicable to that Observation Date.

|

||

|

CUSIP:

|

78017FVN0

|

||

|

Per Note

|

Total

|

||

|

Price to public

|

100.00%

|

||

|

Underwriting discounts and commissions(1)

|

1.00%

|

||

|

Proceeds to Royal Bank of Canada

|

99.00%

|

(1) We or one of our affiliates may pay varying selling concessions of up to $10.00 per $1,000 in principal amount of the Notes in connection with

the distribution of the Notes to other registered broker-dealers. Certain dealers who purchase the Notes for sale to certain fee-based advisory accounts may forego some or all of their underwriting discount or selling concessions. The public

offering price for investors purchasing the Notes in these accounts may be between $990 and $1,000 per $1,000 in principal amount of the Notes. In addition, RBCCM or one of its affiliates may pay a referral fee to a broker-dealer that is not

affiliated with us in an amount of up to 0.55% of the principal amount of the Notes. See “Supplemental Plan of Distribution (Conflicts of Interest)” below.

The initial estimated value of the Notes as of the Trade Date is expected to be between $942.50 and $992.50 per $1,000 in principal amount of the Notes, and will be less than the

price to public. The final pricing supplement relating to the Notes will set forth our estimate of the initial value of the Notes as of the Trade Date. The actual value of the Notes at any time will reflect many factors, cannot be predicted

with accuracy, and may be less than this amount. We describe our determination of the initial estimated value in more detail below.

RBC Capital Markets, LLC

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

SUMMARY

The information in this “Summary” section is qualified by the more detailed information set forth in this terms supplement, the product prospectus supplement, the prospectus

supplement, and the prospectus.

|

General:

|

This terms supplement relates to an offering of Auto-Callable Geared Buffered Notes (the “Notes”) linked to the lesser performing

of the Reference Assets listed on the cover page of this document.

|

|

Issuer:

|

Royal Bank of Canada (the “Bank”)

|

|

Strike Date:

|

April 23, 2024

|

|

Trade Date (Pricing

Date):

|

April 25, 2024

|

|

Issue Date:

|

April 30, 2024

|

|

Valuation Date:

|

October 23, 2025

|

|

Maturity Date:

|

October 28, 2025

|

|

Denominations:

|

Minimum denomination of $1,000, and integral multiples of $1,000 thereafter.

|

|

Coupon Rate:

|

8.45% per annum. The Coupon Payments will be paid in equal semi-annual installments of $42.25 per $1,000 in principal amount of

the Notes on the applicable Coupon Payment Date.

|

|

Key Dates:

|

The Observation Dates and Coupon Payment Dates will occur semi-annually, as set forth below:

|

|

Observation Dates

|

Coupon Payment Dates

|

||||

|

October 23, 2024

|

October 28, 2024

|

||||

|

April 23, 2025

|

April 28, 2025

|

||||

|

October 23, 2025

(the Valuation Date)

|

October 28, 2025

(the Maturity Date)

|

|

The Observation Dates and Coupon Payment Dates are subject to postponement as set forth in the product supplement and the prospectus supplement.

|

|

|

Record Dates:

|

The record date for each Coupon Payment Date will be one business day prior to that scheduled Coupon Payment Date; provided,

however, that any Coupon payable at maturity or upon a call will be payable to the person to whom the payment at maturity or upon the call, as the case may be, will be payable.

|

|

Call Feature:

|

If, starting on October 23, 2024 and on any semi-annual Observation Date thereafter, the

closing level of each Reference Asset is greater than or equal to its Initial Level, then the Notes will be automatically called.

|

|

Payment if Called:

|

If the Notes are automatically called, then, on the applicable Coupon Payment Date, for each $1,000 in principal amount of the

Notes, you will receive $1,000 plus the Coupon otherwise due on that Coupon Payment Date.

|

|

Percentage Change:

|

With respect to each Reference Asset, and expressed as a percentage:

|

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

|

Lesser Performing

Reference Asset:

|

The Reference Asset which has the lowest Percentage Change.

|

|

Initial Levels:

|

For each Reference Asset, its closing level on the Strike Date, as set forth on the cover page of this document.

|

|

Buffer Levels:

|

For each Reference Asset, 80% of its Initial Level, as set forth on the cover page of this document.

|

|

Final Levels:

|

For each Reference Asset, its closing level on the Valuation Date.

|

|

Downside Multiplier:

|

100/80, which is 1.25.

|

|

Payment at Maturity (if

not previously called

and held to maturity):

|

If the Notes are not previously called, for each $1,000 in principal amount of the Notes, we will pay you at maturity an amount

in cash based on the Final Level of the Lesser Performing Reference Asset:

• If the Final Level of the Lesser Performing Reference Asset is greater than or equal to its Buffer Level, we will pay

you a cash payment equal to the principal amount plus the Coupon Payment otherwise due on the Maturity Date.

• If the Final Level of the Lesser Performing Reference Asset is less than its Buffer Level, you will receive at maturity, in addition to the final

Coupon Payment, an amount in cash equal to:

$1,000 + [$1,000 x (Percentage Change of the Lesser Performing Reference Asset + 20%) x (100/80)]

In this case, investors in the Notes could lose some or all of their investment at maturity.

|

|

Monitoring Period:

|

The Valuation Date. The closing levels of the Reference Assets between the Strike Date and the Valuation Date will not impact the Payment at Maturity.

|

|

Monitoring Method:

|

Close of Trading Day

|

|

Market Disruption

Events:

|

The occurrence of a market disruption event (or a non-trading day) as to either of the Reference Assets will result in the postponement of an

Observation Date or the Valuation Date as to that Reference Asset, as described in the product prospectus supplement, but not to any non-affected Reference Asset.

|

|

Calculation Agent:

|

RBC Capital Markets, LLC (“RBCCM”)

|

|

U.S. Tax Treatment:

|

By purchasing a Note, each holder agrees (in the absence of a change in law, an administrative determination or a judicial ruling to the contrary) to

treat the Note as an investment unit consisting of (i) a non-contingent debt instrument issued by us to you and (ii) a put option with respect to the Reference Assets written by you and purchased by us.

However, the U.S. federal income tax consequences of your investment in the Notes are uncertain and the Internal Revenue Service could assert that the

Notes should be taxed in a manner that is different from that described in the preceding sentence. Please see the section below, “Supplemental Discussion of U.S. Federal Income Tax Consequences” including the opinion of Ashurst LLP, our

special U.S. tax counsel).

|

|

Secondary Market:

|

RBCCM (or one of its affiliates), though not obligated to do so, may maintain a secondary market in the Notes after the issue date. The amount that an

investor may receive upon sale of the Notes prior to maturity may be less than the principal amount.

|

|

Listing:

|

The Notes will not be listed on any securities exchange.

|

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

|

Settlement:

|

DTC global (including through its indirect participants Euroclear and Clearstream Luxembourg as described under “Ownership and

Book Entry Issuance” in the prospectus)

|

|

Terms Incorporated in

the Master Note:

|

All of the terms appearing on the cover page and above the item captioned “Secondary Market” in this section and the applicable

terms appearing under the caption “General Terms of the Notes” in the product prospectus supplement, as modified by this terms supplement.

|

The Trade Date, issue date and other dates set forth above are subject to change, and will be set forth in the final pricing supplement relating to the Notes.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

ADDITIONAL TERMS OF YOUR NOTES

You should read this terms supplement together with the prospectus dated December 20, 2023, as supplemented by the prospectus supplement dated December 20, 2023 and the

product prospectus supplement dated December 20, 2023, relating to our Senior Global Medium-Term Notes, Series J, of which these Notes are a part. Capitalized terms used but not defined in this terms supplement will have the meanings given to

them in the product prospectus supplement. In the event of any conflict, this terms supplement will control. The Notes vary from the terms described in the product prospectus supplement in

several important ways. You should read this terms supplement carefully.

This terms supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any

other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among

other things, the matters set forth in “Risk Factors” in the prospectus supplement and in the product prospectus supplement, each dated December 20, 2023, as the Notes involve risks not associated with conventional debt securities. We urge you

to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes. You may access these documents on the Securities and Exchange Commission (the “SEC”) website at www.sec.gov as follows (or if that address has

changed, by reviewing our filings for the relevant date on the SEC website):

Prospectus dated December 20, 2023:

Prospectus Supplement dated December 20, 2023:

Product Prospectus Supplement ERN-EI-1 dated December 20, 2023:

Our Central Index Key, or CIK, on the SEC website is 1000275. As used in this terms supplement, “we,” “us,” or “our” refers to Royal Bank of Canada.

Royal Bank of Canada has filed a registration statement (including a product prospectus supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to

which this terms supplement relates. Before you invest, you should read those documents and the other documents relating to this offering that we have filed with the SEC for more complete information about us and this offering. You may obtain

these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Royal Bank of Canada, any agent or any dealer participating in this offering will arrange to send you the product prospectus supplement, the

prospectus supplement and the prospectus if you so request by calling toll-free at 1-877-688-2301.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

HYPOTHETICAL EXAMPLES

The examples set forth below are provided for illustration purposes only. The assumptions in each of the examples are purely hypothetical

and do not relate to the actual performance of either Reference Asset. The hypothetical terms do not purport to be representative of every possible scenario concerning increases or decreases in the Final Level of each Reference Asset relative

to its Initial Level. We cannot predict the actual performance of each Reference Asset.

The table below illustrates the Payment at Maturity of the Notes (excluding the final Coupon Payment) for a hypothetical range of performance for the Lesser Performing

Reference Asset, assuming an Initial Level of 100, a Buffer Level of 80 and an initial investment of $1,000. For this purpose, we have assumed that there will be no market disruption events and that the Notes have not been called. Hypothetical

Final Levels of the Lesser Performing Reference Asset are shown in the first column on the left. The second column shows the hypothetical Percentage Change for the Lesser Performing Reference Asset. The third column shows the hypothetical

Payment at Maturity and the final Coupon Payment, as a percentage of the principal amount. The last column shows the Payment at Maturity including the final Coupon Payment of $42.25 per $1,000 in principal amount of the Notes. The amounts in

the table have been rounded for ease of analysis.

If the Notes are automatically called prior to maturity, the table below will not be relevant, and you will receive the principal amount plus the Coupon Payment due on the

applicable payment date.

We make no representation or warranty as to which of the Reference Assets will be the Lesser Performing Reference Asset for purposes of

calculating the payment, if any, we will deliver or pay on the Maturity Date.

|

Hypothetical Final

Level of the Lesser

Performing

Reference Asset

|

Percentage Change

|

Payment at Maturity as

Percentage of

Principal Amount*

|

Hypothetical

Payment at Maturity*

|

|

150.00

|

50.00%

|

104.225%

|

$1,042.25

|

|

130.00

|

30.00%

|

104.225%

|

$1,042.25

|

|

120.00

|

20.00%

|

104.225%

|

$1,042.25

|

|

110.00

|

10.00%

|

104.225%

|

$1,042.25

|

|

100.00

|

0.00%

|

104.225%

|

$1,042.25

|

|

90.00

|

-10.00%

|

104.225%

|

$1,042.25

|

|

85.00

|

-15.00%

|

104.225%

|

$1,042.25

|

|

80.00

|

-20.00%

|

104.225%

|

$1,042.25

|

|

75.00

|

-25.00%

|

97.975%

|

$979.75

|

|

70.00

|

-30.00%

|

91.725%

|

$917.25

|

|

60.00

|

-40.00%

|

79.225%

|

$792.25

|

|

50.00

|

-50.00%

|

66.725%

|

$667.25

|

|

30.00

|

-70.00%

|

41.725%

|

$417.25

|

|

0.00

|

-100.00%

|

4.225%

|

$42.25

|

* Includes the final Coupon Payment

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

Hypothetical Examples of Amounts Payable at Maturity

The following hypothetical examples illustrate how the payments at maturity set forth in the table above are calculated, assuming the Notes have not been

called. In addition to the hypothetical payment at maturity, an investor would have received the periodic Coupon Payments over the term of the Notes.

Example 1: The level of the Lesser Performing Reference Asset increases by 25% from the Initial Level of 100.00 to a Final

Level of 125.00. Because the Final Level of the Lesser Performing Reference Asset is greater than its Buffer Level, the investor receives at maturity, in addition to the final Coupon Payment, a cash payment of $1,000 per Note, despite

the 25% appreciation in the level of the Lesser Performing Reference Asset.

Example 2: The level of the Lesser Performing Reference Asset decreases by 10% from the Initial Level of 100.00 to a Final

Level of 90.00. Because the Final Level of the Lesser Performing Reference Asset is greater than its Buffer Level, the investor receives at maturity, in addition to the final Coupon Payment, a cash payment of $1,000 per Note, despite

the 10% decline in the level of the Lesser Performing Reference Asset.

Example 3: The level of the Lesser Performing Reference Asset decreases by 50% from the Initial Level of $100.00 to a Final Level of 50.00. Because

the Final Level of the Lesser Performing Reference Asset is less than the Buffer Level, we will pay an amount in cash that will be calculated as follows:

$1,000 + [$1,000 x (-50% + 20%) x (100/80)] = $625.00

In addition, we will pay the final Coupon Payment of $42.25, for a total payment of $667.25

* * *

The Payments at Maturity shown above are entirely hypothetical; they are based on values of the Reference Assets that may not be achieved on the Valuation Date and on

assumptions that may prove to be erroneous. The actual market value of your Notes on the Maturity Date or at any other time, including any time you may wish to sell your Notes, may bear little relation to the hypothetical Payments at Maturity

shown above, and those amounts should not be viewed as an indication of the financial return on an investment in the Notes or on an investment linked to either Reference Asset.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

SELECTED RISK CONSIDERATIONS

An investment in the Notes involves significant risks. Investing in the Notes is not equivalent to investing directly in the Reference Assets. These risks are explained in

more detail in the section “Risk Factors” in the product prospectus supplement. In addition to the risks described in the prospectus supplement and the product prospectus supplement, you should consider the following:

Risks Relating to the Terms and Structure of the Notes

| • |

You May Lose Some or All of the Principal Amount at Maturity — Investors in the Notes could lose some or all of their principal amount if there is a decline in the

level in either Reference Asset between the Strike Date and the Valuation Date. If the Notes are not automatically called and the Final Level of the Lesser Performing Reference Asset is less than its Buffer Level, you will lose 1.25% of

the principal amount for each 1% that the Final Level is less than the Buffer Level. The rate of interest payable on the Notes may not be sufficient to compensate for any such loss.

|

| • |

The Notes Are Subject to an Automatic Call — If on any Observation Date, beginning in October 2024, the closing level of the Lesser Performing Reference Asset is

greater than or equal to its Initial Level, then the Notes will be automatically called. If the Notes are automatically called, then, on the applicable Coupon Payment Date, for each $1,000 in principal amount of the Notes, you will

receive $1,000 plus the Coupon otherwise due on the applicable Coupon Payment Date. You will not receive any Coupons after that payment. You may be unable to reinvest your proceeds from the automatic call in an investment with a return

that is as high as the return on the Notes would have been if they had not been called.

|

| • |

The Payments on the Notes Are Limited — The payments on the Notes will be limited to the Coupon Payments. Accordingly, your

return on the Notes may be less than your return would be if you made an investment in the Reference Assets, the securities included in the Reference Assets, or in a security directly linked to the positive performance of the Reference

Assets.

|

| • |

The Amount Payable at Maturity Will Be Determined Solely by Reference to the Lesser Performing Reference Asset Even if the Other Reference Asset Performs Better — The

Payment at Maturity will be determined solely by reference to the performance of the Lesser Performing Reference Asset. Even if the Final Level of the other Reference Asset has increased compared to its Initial Level, or has experienced

a decrease that is less than that of the Lesser Performing Reference Asset, your return will only be determined by reference to the performance of the Lesser Performing Reference Asset, regardless of the performance of the other

Reference Asset. The Notes are not linked to a weighted basket, in which the risk may be mitigated and diversified among each of the basket components. For example, in the case of notes linked to a weighted basket, the return would

depend on the weighted aggregate performance of the basket components reflected as the basket return. As a result, the depreciation of one basket component could be mitigated by the appreciation of the other basket component, as scaled

by the weighting of that basket component. However, in the case of the Notes, the individual performance of each of the Reference Assets would not be combined, and the depreciation of one Reference Asset would not be mitigated by any

appreciation of the other Reference Asset. Instead, your return will depend solely on the Final Level of the Lesser Performing Reference Asset. Because each Reference Asset tracks a different segment of the U.S. equities market, they

may both decrease in a comparable manner.

|

| • |

Your Return on the Notes May Be Lower than the Return on a Conventional Debt Security of Comparable Maturity — The return that you will receive on the Notes, which

could be negative, may be less than the return you could earn on other investments. Even if your return is positive, your return may be less than the return you would earn if you purchased one of our conventional senior interest bearing

debt securities.

|

| • |

Owning the Notes Is Not the Same as Owning the Securities Represented by the Reference Assets — The return on your Notes is unlikely to reflect the return you would

realize if you actually owned the securities represented by the Reference Assets. For instance, you will not receive or be entitled to receive any dividend payments or other distributions on those securities during the term of your

Notes. As an owner of the Notes, you will not have voting rights or any other rights that holders of the Reference Assets may have. Further, the level of one or both of the Reference Assets may increase substantially during the term of

the Notes, while your return on the Notes is limited to the Coupon Payments.

|

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

| • |

Payments on the Notes Are Subject to Our Credit Risk, and Changes in Our Credit Ratings Are Expected to Affect the Market Value of the Notes — The Notes are our senior

unsecured debt securities. As a result, your receipt of each Coupon Payment and the amount due on any relevant payment date is dependent upon our ability to repay our obligations on the applicable payment dates. This will be the case

even if the levels of the Reference Assets increase after the Strike Date. No assurance can be given as to what our financial condition will be at any time during the term of the Notes.

|

| • |

The Payments on the Notes Are Subject to Postponement Due to Market Disruption Events and Adjustments — The payment at maturity, each Observation Date, each Coupon

Payment Date and the Valuation Date are subject to adjustment as described in the product prospectus supplement. For a description of what constitutes a market disruption event as well as the consequences of that market disruption

event, see “General Terms of the Notes—Market Disruption Events” in the product prospectus supplement.

|

| • |

The Tax Treatment of the Notes Is Uncertain — The U.S. federal income tax treatment of an investment in the Notes is uncertain. We do not plan to request a ruling from

the Internal Revenue Service (the "IRS") regarding the tax treatment of an investment in the Notes, and the IRS or a court may not agree with the tax treatment described in this document.

|

Risks Relating to the Secondary Market for the Notes

| • |

There May Not Be an Active Trading Market for the Notes-Sales in the Secondary Market May Result in Significant Losses — There may be little or no secondary market for

the Notes. The Notes will not be listed on any securities exchange. RBCCM and our other affiliates may make a market for the Notes; however, they are not required to do so. RBCCM or any of our other affiliates may stop any market-making

activities at any time. Even if a secondary market for the Notes develops, it may not provide significant liquidity or trade at prices advantageous to you. We expect that transaction costs in any secondary market would be high. As a

result, the difference between bid and ask prices for your Notes in any secondary market could be substantial.

|

Risks Relating to the Initial Estimated Value of the Notes

| • |

The Initial Estimated Value of the Notes Will Be Less than the Price to the Public — The initial estimated value that will be set forth on the cover page of the final

pricing supplement for the Notes will not represent a minimum price at which we, RBCCM or any of our affiliates would be willing to purchase the Notes in any secondary market (if any exists) at any time. If you attempt to sell the Notes

prior to maturity, their market value may be lower than the price you paid for them and the initial estimated value. This is due to, among other things, changes in the levels of the Reference Assets, the borrowing rate we pay to issue

securities of this kind, and the inclusion in the price to the public of the underwriting discount, the referral fee, and estimated costs relating to our hedging of the Notes. These factors, together with various credit, market and

economic factors over the term of the Notes, are expected to reduce the price at which you may be able to sell the Notes in any secondary market and will affect the value of the Notes in complex and unpredictable ways. Assuming no

change in market conditions or any other relevant factors, the price, if any, at which you may be able to sell your Notes prior to maturity may be less than your original purchase price, as any such sale price would not be expected to

include the underwriting discount, the referral fee, or hedging costs relating to the Notes. In addition to bid-ask spreads, the value of the Notes determined by RBCCM for any secondary market price is expected to be based on the

secondary rate rather than the internal funding rate used to price the Notes and determine the initial estimated value. As a result, the secondary price will be less than if the internal funding rate was used. The Notes are not designed

to be short-term trading instruments. Accordingly, you should be able and willing to hold your Notes to maturity.

|

| • |

The Initial Estimated Value of the Notes that We Will Provide in the Final Pricing Supplement Will Be an Estimate Only, Calculated as of the Time the Terms of the Notes Are

Set — The initial estimated value of the Notes will be based on the value of our obligation to make the payments on the Notes, together with the mid-market value of the derivative embedded in the terms of the Notes. See

“Structuring the Notes” below. Our estimate will be based on a variety of assumptions, including our credit spreads, expectations as to dividends, interest rates and volatility, and the expected term of the Notes. These assumptions are

based on certain

|

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

forecasts about future events, which may prove to be incorrect. Other entities may value the Notes or similar securities at a price that is significantly

different than we do.

The value of the Notes at any time after the Trade Date will vary based on many factors, including changes in market conditions, and cannot

be predicted with accuracy. As a result, the actual value you would receive if you sold the Notes in any secondary market, if any, should be expected to differ materially from the initial estimated value of your Notes.

Risks Relating to Conflicts of Interest and Our Trading Activities

| • |

Our Business Activities May Create Conflicts of Interest — We and our affiliates expect to engage in trading activities related to the Notes or to the securities

represented by the Reference Assets that are not for the account of holders of the Notes or on their behalf. These trading activities may present a conflict between the holders’ interests in the Notes and the interests we and our

affiliates will have in their proprietary accounts, in facilitating transactions, including options and other derivatives transactions, for their customers and in accounts under their management. These trading activities, if they

influence the levels of the Reference Assets, could be adverse to the interests of the holders of the Notes. We and one or more of our affiliates may, at present or in the future, engage in business with the issuers of the securities

represented by the Reference Assets, including making loans to or providing advisory services. These services could include investment banking and merger and acquisition advisory services. These activities may present a conflict between

our or one or more of our affiliates’ obligations and your interests as a holder of the Notes. Moreover, we, and our affiliates may have published, and in the future expect to publish, research reports with respect to the Reference

Assets or securities represented by the Reference Assets. This research is modified from time to time without notice and may express opinions or provide recommendations that are inconsistent with purchasing or holding the Notes. Any of

these activities by us or one or more of our affiliates may affect the values of the Reference Assets, and, therefore, the market value of the Notes.

|

| • |

You Must Rely on Your Own Evaluation of the Merits of an Investment Linked to the Reference Assets — In the ordinary course of their business, our affiliates may have

expressed views on expected movements in the Reference Assets or the equity securities that they represent, and may do so in the future. These views or reports may be communicated to our clients and clients of our affiliates. However,

these views are subject to change from time to time. Moreover, other professionals who transact business in markets relating to any Reference Asset may at any time have significantly different views from those of our affiliates. For

these reasons, you are encouraged to derive information concerning the Reference Assets from multiple sources, and you should not rely solely on views expressed by our affiliates.

|

Risks Relating to the Reference Assets

| • |

An Investment in the Notes Is Subject to Risks Associated in Investing in Stocks With a Small Market Capitalization — The RTY consists of stocks issued by companies

with relatively small market capitalizations. These companies often have greater stock price volatility, lower trading volume and less liquidity than large-capitalization companies. As a result, the level of the RTY may be more

volatile than that of a market measure that does not track solely small-capitalization stocks. Stock prices of small-capitalization companies are also generally more vulnerable than those of large-capitalization companies to adverse

business and economic developments, and the stocks of small-capitalization companies may be thinly traded, and be less attractive to many investors if they do not pay dividends. In addition, small capitalization companies are often less

well-established and less stable financially than large-capitalization companies and may depend on a small number of key personnel, making them more vulnerable to loss of those individuals. Small capitalization companies tend to have

lower revenues, less diverse product lines, smaller shares of their target markets, fewer financial resources and fewer competitive strengths than large-capitalization companies. These companies may also be more susceptible to adverse

developments related to their products or services.

|

| • |

An Investment in the Notes Is Subject to Risks Relating to Non-U.S. Securities Markets — Because certain securities included in the NDX are issued by non-U.S. issuers

and/or are traded outside of the U.S., an investment in the Notes involves particular risks. For example, the relevant non-U.S. securities markets may be more volatile

|

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

than the U.S. securities markets, and market developments may affect these markets differently from the U.S. or other securities markets.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

INFORMATION REGARDING THE REFERENCE ASSETS

All disclosures contained in this document regarding the Reference Assets, including, without limitation, their make-up, method of calculation, and changes in

their components, have been derived from publicly available sources, without independent investigation. Neither we nor RBCCM accepts any responsibility for the calculation, maintenance or publication of any Reference Asset.

Nasdaq-100 Index® (“NDX”)

The Nasdaq-100 Index® ("NDX") is a modified market capitalization-weighted index of the 100 largest non-financial stocks that have their

primary U.S. listing on the Nasdaq Global Select Market or the Nasdaq Global Market. The NDX excludes securities of companies assigned to the Financials industry according to the Industry Classification Benchmark. The NDX was launched on

January 31, 1985, with a base index value of 250.00. On January 1, 1994, the base index value was reset to 125.00. The Nasdaq, Inc. (“index sponsor”) publishes the NDX.

Security Eligibility Criteria

To be eligible for initial inclusion in the NDX, a security must meet the following criteria:

| • |

the security must generally be a common stock, ordinary share, American Depositary Receipt ("ADR"), or tracking stock. Companies organized as real estate investment trusts are not eligible for index

inclusion. If the security is an ADR, then references to the “issuer” are references to the underlying security and the total shares outstanding is the actual ADRs outstanding as reported by the depositary banks. If an issuer has listed

multiple security classes, all security classes are eligible, subject to meeting all other security eligibility criteria;

|

| • |

the security’s primary U.S. listing must exclusively be listed on the Nasdaq Global Select Market or the Nasdaq Global Market;

|

| • |

if the security is issued by an issuer organized under the laws of a jurisdiction outside the United States, it must have listed options on a registered options market in the United States or be eligible for

listed-options trading on a registered options market in the United States;

|

| • |

the security must be issued by a non-financial company (any industry other than Financials) according to the Industry Classification Benchmark;

|

| • |

the security must have a minimum average daily trading volume of 200,000 shares s (measured over the three calendar months ending with the month that includes the reconstitution reference date);

|

| • |

the security must have traded for at least three full calendar months, not including the month of initial listing, on an “eligible exchange,” which includes Nasdaq (Nasdaq Global Select Market, Nasdaq Global

Market, or Nasdaq Capital Market), NYSE, NYSE American or CBOE BZX. Eligibility is determined as of the constituent selection reference date, and includes that month. A security that was added to the NDX as a result of a spin-off event

will be exempt from this requirement;

|

| • |

the security may not be issued by an issuer currently in bankruptcy proceedings; and

|

| • |

the issuer of the security generally may not have entered into a definitive agreement or other arrangement that would make it ineligible for NDX inclusion and where the transaction is imminent as determined

by the Index Management Committee.

|

There is no market capitalization eligibility or float eligibility criterion.

Constituent Selection Process

The index sponsor selects constituents once annually in December. The security eligibility criteria are applied using market data as of the end of October and total shares outstanding as of the

end of November. All eligible issuers, ranked by market capitalization, are considered for the NDX inclusion based on the following order of criteria.

| • |

The top 75 ranked issuers will be selected for inclusion in the NDX.

|

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

| • |

Any other issuers that were already members of the NDX as of the reconstitution reference date and are ranked within the top 100 are also selected for inclusion in the NDX.

|

| • |

In the event that fewer than 100 issuers pass the first two criteria, the remaining positions will first be filled, in rank order, by issuers currently in the index ranked in positions 101-125 that were

ranked in the top 100 at the previous reconstitution or replacement-or spin-off-issuers added since the previous reconstitution. In the event that fewer than 100 issuers pass the first three criteria, the remaining positions will be

filled, in rank order, by any issuers ranked in the top 100 that were not already members of the NDX as of the reconstitution reference date.

|

Index reconstitutions are announced in early December and become effective after the close of trading on the third Friday in December.

Constituent Weighting

The NDX is rebalanced on a quarterly basis in March, June, September and December and index weights are announced in early March, June, September and December.

Quarterly weight adjustment

The NDX’s quarterly weight adjustment employs a two-stage weight adjustment scheme according to issuer-level constraints.

Index securities’ initial weights are determined using up to two calculations of market capitalization: Total shares outstanding-derived market capitalization and index share-derived market

capitalization. Total shares outstanding-derived market capitalization is defined as a security’s last sale price times its total shares outstanding. Index share-derived market capitalization is defined as a security’s last sale price times its

updated index shares as of the prior month end. Both total shares outstanding-derived market capitalization and index share-derived market capitalization can be used to calculate total shares outstanding-derived index weights and index

share-derived initial weights by dividing each index security’s total shares outstanding-derived market capitalization or index share-derived market capitalization by the aggregate total shares outstanding-derived market capitalization or index

share-derived market capitalization of all index securities.

When the rebalance coincides with the reconstitution, only total shares outstanding-derived initial weights are used. When the rebalance does not coincide with the reconstitution, index

share-derived initial weights are used when doing so results in no weight adjustment; otherwise, total shares outstanding-derived initial weights are used in both stages of the weight adjustment procedure. Issuer weights are the aggregated

weights of the issuers’ respective index securities.

Stage 1

If no initial issuer weight exceeds 24%, initial weights are used as Stage 1 weights; otherwise, initial weights are adjusted to meet the following Stage 1 constraint, producing the Stage 1

weights:

| • |

No issuer weight may exceed 20% of the index.

|

Stage 2

If the aggregate weight of the subset of issuers whose Stage 1 weights exceed 4.5% does not exceed 48%, Stage 1 weights are used as final weights; otherwise, Stage 1 weights are adjusted to meet

the following Stage 2 constraint, producing the final weights:

| • |

The aggregate weight of the subset of issuers whose Stage 1 weights exceed 4.5% is set to 40%.

|

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

Annual weight adjustment

The NDX’s annual weight adjustment employs a two-stage weight adjustment scheme according to security-level constraints.

Index securities’ initial weights are determined via the quarterly weight adjustment procedure.

Stage 1

If no initial security weight exceeds 15%, initial weights are used as Stage 1 weights; otherwise, initial weights are adjusted to meet the following Stage 1 constraint, producing the Stage 1

weights:

| • |

No security weight may exceed 14% of the index.

|

Stage 2

If the aggregate weight of the subset of index securities with the five largest market capitalizations is less than 40%, Stage 1 weights are used as final weights; otherwise, Stage 1 weights are

adjusted to meet the following constraints, producing the final weights:

| • |

The aggregate weight of the subset of index securities with the five largest market capitalizations is set to 38.5%.

|

| • |

No security with a market capitalization outside the largest five may have a final index weight exceeding the lesser of 4.4% or the final index weight of the index security ranked fifth by market

capitalization.

|

Special rebalance schedule

A special rebalance may be conducted at any time based on the weighting restrictions described above if it is determined to be necessary to maintain the integrity of the NDX.

Index Calculation

The NDX is a modified market capitalization-weighted index. The level of the NDX equals the index market value divided by the divisor. The index market value is the sum of each index security's

market value, as may be adjusted for any corporate actions. An index security’s market value is determined by multiplying the last sale price by the number of shares of the index security represented in the NDX. The NDX is a price return index,

which means that the NDX reflects changes in market value of the index securities and does not reflect regular cash dividends paid on those index securities.

If an index security does not trade on the relevant Nasdaq exchange on a given day or the relevant Nasdaq exchange has not opened for trading, the previous index calculation day’s closing price

for the index security (adjusted for corporate actions occurring prior to market open on the current day, if any) is used. If an index security is halted during the trading day, the most recent last sale price is used until trading resumes. For

securities where the Nasdaq Stock Market is the relevant Nasdaq exchange, the last sale price may be the Nasdaq Official Closing Price when it is closed.

The divisor is calculated as the ratio of (i) the start of day market value of the NDX divided by (ii) the previous day market value of the NDX. The index divisor is adjusted to ensure that

changes in an index security’s price or shares either by corporate actions or index participation which occur outside of trading hours do not affect the index level. An index divisor change occurs after the close of the NDX.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

Index Maintenance

Deletion Policy

If, at any time other than an index reconstitution, the index sponsor determines that an index security is ineligible for index inclusion, the index security is removed as

soon as practicable. This may include:

| • |

Listing on an ineligible index exchange;

|

| • |

Merger, acquisition, or other major corporate event that would adversely impact the integrity of the NDX;

|

| • |

If a company is organized as a real estate investment trust;

|

| • |

If an index security is classified as a financial company (Financials industry) according to the Industry Classification Benchmark;

|

| • |

if the issuer has an adjusted market capitalization below 0.10% of the aggregate adjusted market capitalization of the NDX for two consecutive month ends; and

|

| • |

If a security that was added to the NDX as the result of a spin-off event has an adjusted market capitalization below 0.10% of the aggregate adjusted market capitalization of the NDX at the end of its second

day of regular way trading as an index member.

|

In the case of mergers and acquisitions, the effective date for the removal of an index issuer or security will be largely event-based, with the goal to remove the issuer or

security as soon as completion of the acquisition or merger has been deemed highly probable. Notable events include, but are not limited to, completion of various regulatory reviews, the conclusion of material lawsuits and/or shareholder and

board approvals.

If at the time of the removal of the index issuer or security there is not sufficient time to provide advance notification of the replacement issuer or security so that both

the removal and replacement can be effective on the same day, the index issuer or security being removed will be retained and persisted in the NDX calculations at its last sale price until the effective date of the replacement issuer or

security’s entry to the NDX.

Securities that are added as a result of a spin-off may be deleted as soon as practicable after being added to the NDX. This may occur when the index sponsor determines that a

security is ineligible for inclusion because of reasons such as ineligible exchange, security type, industry, or adjusted market capitalization. Securities that are added as a result of a spin-off may be maintained in the NDX until a later date

and then removed, for example, if a spin-off security has liquidity characteristics that diverge materially from the security eligibility criteria and could affect the integrity of the NDX.

Replacement policy

Securities may be added to the NDX outside of the index reconstitution when there is a deletion. The index security (or all index securities under the same issuer, if

appropriate) is replaced as soon as practicable if the issuer in its entirety is being deleted from the NDX. The issuer with the largest market capitalization and that meets all eligibility criteria as of the prior month end which is not in the

NDX will replace the deleted Issuer. Issuers that are added as a result of a spin-off are not replaced until after they have been included in an index reconstitution.

For pending deletions set to occur soon after an index reconstitution and/or index rebalance effective date, the index sponsor may decide to remove the index security from the

NDX in conjunction with the index reconstitution and/or index rebalance effective date.

Corporate actions

In the periods between scheduled index reconstitution and rebalancing events, individual index securities may be the subject to a variety of corporate actions and

events that require maintenance and adjustments to the NDX, including special cash dividends, stock splits, stock dividends, bonus issues, reverse stock splits, rights offerings/issues, stock distributions of another security and

spin-offs/de-mergers. Adjustments for corporate actions are made prior to market

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

open on the effective date, ex-date, ex-dividend date or ex-distribution date of a given corporate action/event. In absence of one of those dates, there

will be no adjustment to the NDX for such corporate action.

At the quarterly rebalancing, no changes are made to the NDX from the previous month end until the quarterly share change effective date, with the

exception of corporate actions with an ex-date.

Index share adjustments

If a change in total shares outstanding arising from other corporate events is greater than or equal to 10%, an adjustment to index shares is made as soon as practicable after

being sufficiently verified. If the change in total shares outstanding is less than 10%, then all such changes are accumulated and made effective at one time on a quarterly basis after the close of trading on the third Friday in each of March,

June, September and December. The index shares are adjusted by the same percentage amount by which the total shares outstanding has changed.

License Agreement

The Notes are not sponsored, endorsed, sold or promoted by Nasdaq, Inc. or its affiliates (collectively, “Nasdaq”). Nasdaq has not passed on the legality or suitability of, or

the accuracy or adequacy of descriptions and disclosures relating to, the Notes. Nasdaq makes no representation or warranty, express or implied to the owners of the Notes, or any member of the public regarding the advisability of investing in

securities generally or in the Notes particularly, or the ability of the NDX to track general stock market performance. Nasdaq’s only relationship to us is in the licensing of the Nasdaq®, NDX trademarks or service marks, and certain

trade names of Nasdaq and the use of the NDX which are determined, composed and calculated by Nasdaq without regard to us or the securities. Nasdaq has no obligation to take the needs of us or the owners of the Notes into consideration in

determining, composing or calculating the NDX. Nasdaq is not responsible for and has not participated in the determination of the timing of, prices at, or quantities of the Notes to be issued or in the determination or calculation of the

equation by which the Notes are to be converted into cash. Nasdaq has no liability in connection with the administration, marketing or trading of the Notes.

NASDAQ DOES NOT GUARANTEE THE ACCURACY AND/OR UNINTERRUPTED CALCULATION OF THE NDX OR ANY DATA INCLUDED THEREIN. NASDAQ MAKES NO WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY

LICENSEE, OWNERS OF THE NOTES, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE NDX OR ANY DATA INCLUDED THEREIN. NASDAQ MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A

PARTICULAR PURPOSE OR USE WITH RESPECT TO THE NDX OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL NASDAQ HAVE ANY LIABILITY FOR ANY LOST PROFITS OR SPECIAL, INCIDENTAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL

DAMAGES, EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES. NASDAQ®, NASDAQ 100® AND NASDAQ 100 INDEX® ARE TRADE OR SERVICE MARKS OF NASDAQ AND ARE INCENSED FOR USE BY US. THE NOTES HAVE NOT BEEN PASSED ON BY

NASDAQ AS TO THEIR LEGALITY OR SUITABILITY. THE NOTES ARE NOT ISSUED, ENDORSED, SOLD OR PROMOTED BY NASDAQ. NASDAQ MAKES NO WARRANTIES AND BEARS NO LIABILITY WITH RESPECT TO THE NOTES.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

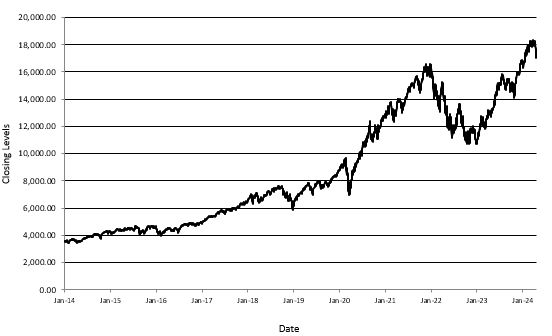

Historical Information

The graph below sets forth information relating to the historical performance of the NDX for the period from January 1, 2014 through April 23, 2024.

We obtained the information regarding the historical performance of the NDX in the graph below from Bloomberg Financial Markets, without independent verification.

Nasdaq-100 Index® (“NDX”)

|

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

Russell 2000® Index (“RTY”)

The RTY was developed by Russell Investments (“Russell”) before FTSE International Limited and Russell combined in 2015 to create FTSE Russell, which is wholly owned by London

Stock Exchange Group. Russell began dissemination of the RTY (Bloomberg L.P. index symbol “RTY”) on January 1, 1984. FTSE Russell calculates and publishes the RTY. The RTY was set to 135 as of the close of business on December 31, 1986. The RTY

is designed to track the performance of the small capitalization segment of the U.S. equity market. As a subset of the Russell 3000® Index, the RTY consists of the smallest 2,000 companies included in the Russell 3000®

Index. The Russell 3000® Index measures the performance of the largest 3,000 U.S. companies, representing approximately 96% of the investable U.S. equity market. The RTY is determined, comprised, and calculated by FTSE Russell

without regard to the Notes.

Selection of Stocks Underlying the RTY

All companies eligible for inclusion in the RTY must be classified as a U.S. company under FTSE Russell’s country-assignment methodology. If a company is incorporated, has a

stated headquarters location, and trades on a standard exchange in the same country (American Depositary Receipts and American Depositary Shares are not eligible), then the company is assigned to its country of incorporation. If any of the

three factors are not the same, FTSE Russell defines three Home Country Indicators (“HCIs”): country of incorporation, country of headquarters, and country of the most liquid exchange (as defined by a two-year average daily dollar trading

volume) from all exchanges within a country. Using the HCIs, FTSE Russell compares the primary location of the company’s assets with the three HCIs. If the primary location of its assets matches any of the HCIs, then the company is assigned to

the primary location of its assets. If there is insufficient information to determine the country in which the company’s assets are primarily located, FTSE Russell will use the country from which the company’s revenues are primarily derived for

the comparison with the three HCIs in a similar manner. FTSE Russell uses the average of two years of assets or revenues data to reduce potential turnover. If conclusive country details cannot be derived from assets or revenues data, FTSE

Russell will assign the company to the country of its headquarters, which is defined as the address of the company’s principal executive offices, unless that country is a Benefit Driven Incorporation “BDI” country, in which case the company

will be assigned to the country of its most liquid stock exchange. BDI countries include: Anguilla, Antigua and Barbuda, Aruba, Bahamas, Barbados, Belize, Bermuda, Bonaire, British Virgin Islands, Cayman Islands, Channel Islands, Cook Islands,

Curacao, Faroe Islands, Gibraltar, Guernsey, Isle of Man, Jersey, Liberia, Marshall Islands, Panama, Saba, Sint Eustatius, Sint Maarten, and Turks and Caicos Islands. For any companies incorporated or headquartered in a U.S. territory,

including Puerto Rico, Guam, and U.S. Virgin Islands, a U.S. HCI is assigned. If a company is designated as a Chinese N share, it will not be considered eligible for inclusion.

All securities eligible for inclusion in the RTY must trade on a major U.S. exchange. Stocks must have a closing price at or above $1.00 on their primary exchange on the “rank

day”, which is the last business day of April. However, in order to reduce unnecessary turnover, if an existing member’s closing price is less than $1.00 on the rank day, it will be considered eligible if the average of the daily closing prices

(from its primary exchange) during the 30 days prior to the rank date is equal to or greater than $1.00. Initial public offerings are added each quarter and must have a closing price at or above $1.00 on the last day of their eligibility period

in order to qualify for index inclusion. If an existing stock does not trade on the rank day, it must have a closing price at or above $1.00 on another eligible U.S. exchange to remain eligible for inclusion.

An important criterion used to determine the list of securities eligible for the RTY is total market capitalization, which is defined as the market price as of the rank day

for those securities being considered at annual reconstitution times the total number of shares outstanding. Where applicable, common stock, non-restricted exchangeable shares and partnership units/membership interests are used to determine

market capitalization. Any other form of shares such as preferred stock, convertible preferred stock, redeemable shares, participating preferred stock, warrants, rights, installment receipts or trust receipts, are excluded from the calculation.

If multiple share classes of common stock exist, they are combined to determine total shares outstanding. If multiple classes of common stock exist, they are combined to determine total shares outstanding. In cases where the common stock share

classes act independently of each other (e.g., tracking stocks), each class is considered for inclusion separately.

Companies with a total market capitalization of less than $30 million are not eligible for the RTY. Similarly, companies with only 5% or less of their shares available in the marketplace are not

eligible for the RTY. Royalty trusts, U.S. limited liability companies, closed-end investment companies (companies that are required to report acquired fund fees and expenses, as defined by the SEC, including business development companies),

blank check companies, special purpose

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

acquisition companies, and limited partnerships are also ineligible for inclusion. Exchange traded funds and mutual funds are also excluded. Bulletin board, pink sheets, and

over-the-counter traded securities are not eligible for inclusion.

Annual reconstitution is a process by which the RTY is completely rebuilt. Based on closing levels of the company’s common stock on its primary exchange on the rank day, all

eligible securities are ranked by their total market capitalization. Reconstitution of the RTY occurs on the fourth Friday in June. In addition, FTSE Russell adds initial public offerings to the RTY on a quarterly basis based on total market

capitalization ranking within the market-adjusted capitalization breaks established during the most recent reconstitution.

After membership is determined, a security’s shares are adjusted to include only those shares available to the public. This is often referred to as “free float.” The purpose

of the adjustment is to exclude from market calculations the capitalization that is not available for purchase and is not part of the investable opportunity set.

License Agreement

FTSE Russell and the Bank have entered into a non-exclusive license agreement providing for the license to the Bank, and certain of its affiliates, in exchange for a fee, of

the right to use indices owned and published by FTSE Russell in connection with some securities, including the Notes. The license agreement provides that the following language must be stated in this document.

FTSE Russell does not guarantee the accuracy and/or the completeness of the RTY or any data included in the RTY and has no liability for any errors, omissions, or

interruptions in the RTY. FTSE Russell makes no warranty, express or implied, as to results to be obtained by the calculation agent, holders of the Notes, or any other person or entity from the use of the RTY or any data included in the RTY in

connection with the rights licensed under the license agreement described in this document or for any other use. FTSE Russell makes no express or implied warranties, and hereby expressly disclaims all warranties of merchantability or fitness

for a particular purpose with respect to the RTY or any data included in the RTY. Without limiting any of the above information, in no event will FTSE Russell have any liability for any special, punitive, indirect or consequential damages,

including lost profits, even if notified of the possibility of these damages.

The Notes are not sponsored, endorsed, sold or promoted by FTSE Russell. FTSE Russell makes no representation or warranty, express or implied, to the owners of the Notes or

any member of the public regarding the advisability of investing in securities generally or in the Notes particularly or the ability of the RTY to track general stock market performance or a segment of the same. FTSE Russell’s publication of

the RTY in no way suggests or implies an opinion by FTSE Russell as to the advisability of investment in any or all of the stocks upon which the RTY is based. FTSE Russell's only relationship to the Bank is the licensing of certain trademarks

and trade names of FTSE Russell and of the RTY, which is determined, composed and calculated by FTSE Russell without regard to the Bank or the Notes. FTSE Russell is not responsible for and has not reviewed the Notes nor any associated

literature or publications and FTSE Russell makes no representation or warranty express or implied as to their accuracy or completeness, or otherwise. FTSE Russell reserves the right, at any time and without notice, to alter, amend, terminate

or in any way change the RTY. FTSE Russell has no obligation or liability in connection with the administration, marketing or trading of the Notes.

“Russell 2000®” and “Russell 3000®” are registered trademarks of FTSE Russell in the U.S. and other countries.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

Historical Information

The graph below sets forth information relating to the historical performance of the RTY for the period from January 1, 2014 through April 23, 2024.

We obtained the information regarding the historical performance of the RTY in the graph below from Bloomberg Financial Markets, without independent verification.

Russell 2000® Index (“RTY”)

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

U.S. FEDERAL TAX INFORMATION

The following section supplements the discussion of U.S. federal income taxation in the accompanying prospectus and prospectus supplement, and supersedes

the discussion in the product supplement under the caption “Supplemental Discussion of U.S. Federal Income Tax Consequences.” It applies only to those holders who are not excluded from the discussion of U.S. federal income taxation in the

accompanying prospectus. This discussion applies only to U.S. holders and non-U.S. holders that will purchase the Notes upon original issuance and will hold the Notes as capital assets for U.S. federal income tax purposes. This discussion does

not apply to holders subject to special rules including accrual method taxpayers subject to special tax accounting rules under Section 451(b) of the Code.

You should consult your tax advisor concerning the U.S. federal income tax and other tax consequences of your investment in the Notes in your particular

circumstances, including the application of state, local or other tax laws and the possible effects of changes in federal or other tax laws.

We will not attempt to ascertain whether the issuer of any of the component stocks included in the Reference Assets would be treated as a “passive

foreign investment company” within the meaning of Section 1297 of the Internal Revenue Code of 1986, as amended (the “Code”), or a “U.S. real property holding corporation” within the meaning of Section 897 of the Code. If the issuer of one or

more of such stocks were so treated, certain adverse U.S. federal income tax consequences could possibly apply to a holder. You should refer to any available information filed with the SEC and other authorities by the issuers of the component

stock included in the Reference Assets and consult your tax advisor regarding the possible consequences to you in this regard, if any.

NO STATUTORY, JUDICIAL OR ADMINISTRATIVE AUTHORITY DIRECTLY DISCUSSES HOW THE NOTES SHOULD BE TREATED FOR U.S. FEDERAL INCOME TAX PURPOSES. AS A RESULT,

THE U.S. FEDERAL INCOME TAX CONSEQUENCES OF AN INVESTMENT IN THE NOTES ARE UNCERTAIN. BECAUSE OF THE UNCERTAINTY, YOU SHOULD CONSULT YOUR TAX ADVISOR IN DETERMINING THE U.S. FEDERAL INCOME TAX AND OTHER TAX CONSEQUENCES OF YOUR INVESTMENT IN

THE NOTES, INCLUDING THE APPLICATION OF STATE, LOCAL OR OTHER TAX LAWS AND THE POSSIBLE EFFECTS OF CHANGES IN FEDERAL OR OTHER TAX LAWS.

In the opinion of our counsel, Ashurst LLP, it would

generally be reasonable to treat your Notes as an investment unit consisting of (i) a non-contingent debt instrument issued by us to you (the “Debt Portion”) and (ii) a put option with respect to the Reference Assets written by you and

purchased by us (the “Put Option”). The balance of this disclosure assumes this treatment is proper and will be respected for U.S. federal income tax purposes. Pursuant to this treatment, ___% of each 8.45% Coupon Payment will be treated as

an interest payment and ___% of each 8.45% Coupon Payment will be treated as payment for the Put Option for U.S. federal income tax purposes.

Treatment as an Investment Unit

If your Notes are properly treated as an investment unit consisting of a Debt Portion and Put Option, it is likely that the Debt Portion of your Notes

would be treated as having been issued for the principal amount of the Notes (if you are an initial purchaser) and that Coupon Payments on the Notes would be treated in part as payments of interest and in part as payments for the Put Option.

Amounts treated as interest would be included in income in accordance with your regular method of accounting for interest for U.S. federal income tax purposes (as described under “Tax Consequences—United States Taxation—Payments of Interest” in

the accompanying prospectus). Amounts treated as payment for the Put Option would be deferred and accounted for upon the call, sale or maturity of the Notes, as discussed below.

If you were to receive a cash payment of the full principal amount of your Notes upon the call or maturity of your Notes, such payment would likely be treated as (i) payment

in full of the principal amount of the Debt Portion (which would not result in the recognition of gain or loss if you are an initial purchaser of your Notes) and (ii) the lapse of the Put Option which would likely result in your recognition of

short-term capital gain in an amount equal to the amount paid to you for the Put Option and deferred as described above. If you were to receive a cash payment upon the maturity of your Notes (excluding cash received as a Coupon Payment) of less

than the full principal amount of your Notes, such payment would likely be treated as (i) payment in full of the principal amount of the Debt Portion (which would not result in the recognition of gain or loss if you are an initial purchaser of

your Notes) and (ii) the cash settlement of the Put Option pursuant to which you paid to us an amount equal to the excess of the principal amount of your Notes over the amount that you

|

|

|

Auto-Callable Geared Buffered Notes

Royal Bank of Canada

|

received upon the maturity of your Notes (excluding cash received as a Coupon Payment) in order to settle the Put Option. If the aggregate amount paid to

you for the Put Option and deferred as described above is greater than the amount you are deemed to have paid to us to settle the Put Option, you will likely recognize short-term capital gain in an amount that is equal to such excess.

Conversely, if the amount paid to you for the Put Option and deferred as described above is less than the amount you are deemed to have paid to us to settle the Put Option, you will likely recognize short-term capital loss in an amount that is

equal to such difference. The deductibility of capital losses is subject to limitations.

Upon the sale of your Notes, you would be required to apportion the value of the amount you receive between the Debt Portion and Put Option on the basis

of the values thereof on the date of the sale. You would recognize gain or loss with respect to the Debt Portion in an amount equal to the difference between (i) the amount apportioned to the Debt Portion and (ii) your adjusted U.S. federal

income tax basis in the Debt Portion (which would generally be equal to the principal amount of your Notes if you are an initial purchaser of your Notes). Except to the extent attributable to accrued but unpaid interest with respect to the Debt

Portion, such gain or loss would be long-term capital gain or loss if your holding period is greater than one year. The amount of cash that you receive that is apportioned to the Put Option (together with any amount of premium received in

respect thereof and deferred as described above) would be treated as short-term capital gain. If the value of the Debt Portion on the date of the sale of your Notes is in excess of the amount you receive upon such sale, you would likely be

treated as having made a payment (to the purchaser in the case of a sale) equal to the amount of such excess in order to extinguish your rights and obligations under the Put Option. In such a case, you would likely recognize short-term capital

gain or loss in an amount equal to the difference between the premium you previously received in respect of the Put Option and the amount of the deemed payment made by you to extinguish the Put Option. The deductibility of capital losses is

subject to limitations.

If you are a secondary purchaser of your Notes, you would be required to allocate your purchase price for your Notes between the Debt Portion and Put

Option based on the respective fair market values of each on the date of purchase. If, however, the portion of your purchase price allocated to the Debt Portion is at a discount from, or is in excess of, the principal amount of your Notes, you

may be subject to the market discount or amortizable bond premium rules described in the accompanying prospectus under “Tax Consequences—United States Taxation—Market Discount” and “Tax Consequences—United States Taxation—Debt Securities

Purchased at a Premium” with respect to the Debt Portion. The portion of your purchase price that is allocated to the Put Option would likely be offset for tax purposes against amounts you subsequently receive with respect to the Put Option

(including amounts received upon a sale of the Notes that are attributable to the Put Option), thereby reducing the amount of gain or increasing the amount of loss you would recognize with respect to the Put Option or with respect to the sale

of any Reference Assets you receive upon the exercise of the Put Option. If, however, the portion of your purchase price allocated to the Debt Portion as described above is in excess of your purchase price for your Notes, you would likely be

treated for tax purposes as having received a payment for the Put Option (which will be deferred as described above) in an amount equal to such excess.

Alternative Characterizations

There is no judicial or administrative authority discussing how your Notes should be treated for U.S. federal income tax purposes. Therefore, other

treatments would also be reasonable and the Internal Revenue Service might assert that treatment other than that described above is more appropriate.

For example, it is possible that your Note could be treated as a single debt instrument subject to the special tax rules governing contingent payment

debt instruments. If your Note is so treated, you would be required to accrue interest income over the term of your Note based upon the yield at which we would issue a non-contingent fixed-rate debt instrument with other terms and conditions

similar to your Note. You would recognize gain or loss upon the call, sale or maturity of your Note in an amount equal to the difference, if any, between the amount you receive at such time and your adjusted basis in your Note. In general, your