UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

(MARK ONE)

FOR

THE QUARTERLY PERIOD ENDED

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission

File Number

(Exact name of Registrant as specified in its charter)

| (State of or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

| (Address of principal executive offices) | (Zip code) |

(Registrant’s

telephone number, including area code) (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports),

and (2) has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant

to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large

accelerated filer ☐ Accelerated filer ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

As of November 8, 2021, the registrant had common units outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None.

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Table of Contents

2

NAMES OF ENTITIES

Unless the context otherwise requires, references in this Form 10-Q to “Cypress Environmental Partners, L.P.,” “the partnership,” “we,” “our,” “us,” or like terms, refer to Cypress Environmental Partners, L.P. and its subsidiaries.

References to:

| ● | “CBI” refers to Cypress Brown Integrity, LLC, a 51% owned subsidiary of CEP LLC; |

| ● | “CEP LLC” refers to Cypress Environmental Partners, LLC, a wholly-owned subsidiary of the Partnership; |

| ● | “CF Inspection” refers to a nationally certified women-owned business, CF Inspection Management, LLC, owned 49% by TIR-PUC and consolidated under generally accepted accounting principles by TIR-PUC. CF Inspection is 51% owned, managed and controlled by Cynthia A. Field, an affiliate of Holdings and a Director of our General Partner; |

| ● | “General Partner” refers to Cypress Environmental Partners GP, LLC, a subsidiary of Cypress Energy GP Holdings, LLC; |

| ● | “Holdings” refers to Cypress Environmental Holdings, LLC, the owner of Holdings II; |

| ● | “Holdings II” refers to Cypress Energy Holdings II, LLC, the owner of 5,610,549 common units representing 45% of our outstanding common units as of November 8, 2021; |

| ● | “Partnership” refers to the registrant, Cypress Environmental Partners, L.P.; |

| ● | “TIR Entities” refers collectively to TIR LLC, TIR-Canada, TIR-PUC and CF Inspection; |

| ● | “TIR-Canada” refers to Tulsa Inspection Resources – Canada, ULC, a wholly-owned subsidiary of TIR LLC; |

| ● | “TIR LLC” refers to Tulsa Inspection Resources, LLC, a wholly-owned subsidiary of CEP LLC; and |

| ● | “TIR-PUC” refers to Tulsa Inspection Resources – PUC, LLC, a subsidiary of TIR LLC that has elected to be treated as a corporation for U.S. federal income tax purposes. |

3

CAUTIONARY REMARKS REGARDING FORWARD-LOOKING STATEMENTS

The information discussed in this Quarterly Report on Form 10-Q includes “forward-looking statements.” These forward-looking statements are identified by their use of terms and phrases such as “may,” “expect,” “estimate,” “project,” “plan,” “believe,” “intend,” “achievable,” “anticipate,” “continue,” “potential,” “should,” “could,” and similar terms and phrases. Although we believe that the expectations reflected in these forward-looking statements are reasonable, they do involve certain assumptions, risks, and uncertainties, and we can give no assurance that such expectations or assumptions will be achieved. Important factors that could cause actual results to differ materially from those in the forward-looking statements are described under “Item 1A – Risk Factors” and “Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report on Form 10-K for the year ended December 31, 2020, filed with the U.S. Securities and Exchange Commission (the “SEC”) on March 23, 2021, and in this report. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements in this paragraph and elsewhere in this Quarterly Report on Form 10-Q and speak only as of the date of this Quarterly Report on Form 10-Q. Other than as required under the securities laws, we do not assume a duty to update these forward-looking statements, whether as a result of new information, subsequent events or circumstances, changes in expectations or otherwise.

4

PART I. FINANCIAL INFORMATION

ITEM 1. Unaudited Condensed Consolidated Financial Statements

| CYPRESS ENVIRONMENTAL PARTNERS, L.P. |

| Unaudited Condensed Consolidated Balance Sheets |

| As of September 30, 2021 and December 31, 2020 |

| (in thousands) |

| September

30, 2021 | December

31, 2020 | |||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Trade accounts receivable, net | ||||||||

| Accounts receivable - affiliates | ||||||||

| Assets of discontinued operations | ||||||||

| Prepaid expenses and other | ||||||||

| Total current assets | ||||||||

| Property and equipment: | ||||||||

| Property and equipment, at cost | ||||||||

| Less: Accumulated depreciation | ||||||||

| Total property and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Goodwill | ||||||||

| Finance lease right-of-use assets, net | ||||||||

| Operating lease right-of-use assets | ||||||||

| Debt issuance costs, net | ||||||||

| Assets of discontinued operations | ||||||||

| Other assets | ||||||||

| Total assets | $ | $ | ||||||

| LIABILITIES AND OWNERS’ EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | $ | ||||||

| Accounts payable - affiliates | ||||||||

| Accrued payroll and other | ||||||||

| Income taxes payable | ||||||||

| Finance lease obligations | ||||||||

| Operating lease obligations | ||||||||

| Current portion of long-term debt | ||||||||

| Liabilities of discontinued operations | ||||||||

| Total current liabilities | ||||||||

| Long-term debt | ||||||||

| Finance lease obligations | ||||||||

| Operating lease obligations | ||||||||

| Liabilities of discontinued operations | ||||||||

| Other noncurrent liabilities | ||||||||

| Total liabilities | ||||||||

| Commitments and contingencies - Note 7 | ||||||||

| Owners’ equity: | ||||||||

| Partners’ capital: | ||||||||

| Common units

( | ||||||||

| September 30, 2021 and December 31, 2020, respectively) | ||||||||

| Preferred units

( | ||||||||

| General partner | ( | ) | ( | ) | ||||

| Accumulated other comprehensive loss | ( | ( | ) | |||||

| Total partners’ capital | ||||||||

| Noncontrolling interests | ||||||||

| Total owners’ equity | ||||||||

| Total liabilities and owners’ equity | $ | $ | ||||||

See accompanying notes.

5

| CYPRESS ENVIRONMENTAL PARTNERS, L.P. |

| Unaudited Condensed Consolidated Statements of Operations |

| For the Three and Nine Months Ended September 30, 2021 and 2020 |

| (in thousands, except per unit data) |

| Three

Months Ended September 30, | Nine

Months Ended September 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Revenue | $ | $ | $ | $ | ||||||||||||

| Costs of services | ||||||||||||||||

| Gross margin | ||||||||||||||||

| Operating costs and expense: | ||||||||||||||||

| General and administrative | ||||||||||||||||

| Depreciation, amortization and accretion | ||||||||||||||||

| Loss (gain) on asset disposals, net | ( | ) | ||||||||||||||

| Operating (loss) income | ( | ) | ( | ) | ||||||||||||

| Other (expense) income: | ||||||||||||||||

| Interest expense | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Foreign currency (losses) gains | ( | ) | ( | ) | ||||||||||||

| Other, net | ||||||||||||||||

| Net (loss) income before income tax expense | ( | ) | ( | ) | ( | ) | ||||||||||

| Income tax expense | ||||||||||||||||

| Net (loss) income from continuing operations | ( | ) | ( | ) | ( | ) | ||||||||||

| Net (loss) income from discontinued operations, net of tax | ( | ) | ( | ) | ||||||||||||

| Net (loss) income | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| Net (loss) income from continuing operations | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | ||||||

| Net income attributable to noncontrolling interests - continuing operations | ||||||||||||||||

| Net (loss) income attributable to limited partners - continuing operations | ( | ) | ( | ) | ( | ) | ||||||||||

| Net (loss) income attributable to limited partners - discontinued operations | ( | ) | ( | ) | ||||||||||||

| Net (loss) income attributable to limited partners | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | ||||||

| Net (loss) income attributable to limited partners - continuing operations | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | ||||||

| Net income attributable to preferred unitholder | ||||||||||||||||

| Net loss attributable to common unitholders - continuing operations | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net (loss) income attributable to common unitholders - discontinued operations | ( | ) | ( | ) | ||||||||||||

| Net loss attributable to common unitholders | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Net (loss) income per common limited partner unit: | ||||||||||||||||

| Basic and diluted - continuing operations | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Basic and diluted - discontinued operations | ( | ) | ( | ) | ||||||||||||

| Basic and diluted | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Weighted average common units outstanding: | ||||||||||||||||

| Basic and diluted | ||||||||||||||||

See accompanying notes.

6

| CYPRESS ENVIRONMENTAL PARTNERS, L.P. |

| Unaudited Condensed Consolidated Statements of Comprehensive (Loss) Income |

| For the Three and Nine Months Ended September 30, 2021 and 2020 |

| (in thousands) |

| Three

Months Ended September 30, | Nine

Months Ended September 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Net (loss) income | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| Other comprehensive income (loss) | ||||||||||||||||

| foreign currency translation | ( | ) | ( | ) | ||||||||||||

| Comprehensive (loss) income | $ | ( | ) | $ | $ | ( | ) | $ | ||||||||

| Comprehensive income attributable to preferred unitholders | ||||||||||||||||

| Comprehensive (loss) income attributable to noncontrolling interests | ( | ) | ( | ) | ||||||||||||

| Comprehensive loss attributable to common unitholders | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

See accompanying notes.

7

| CYPRESS ENVIRONMENTAL PARTNERS, L.P. |

| Unaudited Condensed Consolidated Statement of Owners’ Equity |

| For the Nine Months Ended September 30, 2021 and 2020 |

| (in thousands) |

| Nine Months Ended September 30, 2021 | ||||||||||||||||||||||||

| Common Units | Preferred Units | General Partner | Accumulated Other Comprehensive Income (Loss) | Noncontrolling Interests | Total Owners’ Equity | |||||||||||||||||||

| Owners’ equity at December 31, 2020 | $ | $ | $ | ( | ) | $ | ( | ) | $ | $ | ||||||||||||||

| Net (loss) income for the period January 1, 2021 through March 31, 2021 | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Foreign currency translation adjustment | ( | ) | ( | ) | ||||||||||||||||||||

| Distributions | ( | ) | ( | ) | ||||||||||||||||||||

| Equity-based compensation expense | ||||||||||||||||||||||||

| Unit-based compensation reclassified to liabilities | ( | ) | ( | ) | ||||||||||||||||||||

| Taxes paid related to net share settlement of equity-based compensation | ( | ) | ( | ) | ||||||||||||||||||||

| Owners’ equity at March 31, 2021 | ( | ) | ( | ) | ||||||||||||||||||||

| Net (loss) income for the period April 1, 2021 through June 30, 2021 | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Foreign currency translation adjustment | ( | ) | ( | ) | ||||||||||||||||||||

| Equity-based compensation expense | ||||||||||||||||||||||||

| Unit-based compensation reclassified to liabilities | ( | ) | ( | ) | ||||||||||||||||||||

| Taxes paid related to net share settlement of equity-based compensation | ( | ) | ( | ) | ||||||||||||||||||||

| Owners’ equity at June 30, 2021 | ( | ) | ( | ) | ||||||||||||||||||||

| Net (loss) income for the period July 1, 2021 through September 30, 2021 | ( | ) | ( | ) | ( | ) | ||||||||||||||||||

| Foreign currency translation adjustment | ||||||||||||||||||||||||

| Distributions | ( | ) | ( | ) | ||||||||||||||||||||

| Equity-based compensation expense | ||||||||||||||||||||||||

| Unit-based compensation reclassified to equity | ||||||||||||||||||||||||

| Owners’ equity at September 30, 2021 | $ | $ | $ | ( | ) | $ | ( | ) | $ | $ | ||||||||||||||

See accompanying notes.

8

| Nine Months Ended September 30, 2020 | |||||||||||||||||||

| Common Units | Preferred Units | General Partner | Accumulated Other Comprehensive Loss | Noncontrolling Interests | Total Owners’ Equity | ||||||||||||||

| Owners’ equity at December 31, 2019 | $ | $ | $ | ( | ) | $ | ( | ) | $ | $ | |||||||||

| Net (loss) income for the period January 1, 2020 through March 31, 2020 | ( | ) | ( | ) | ( | ) | |||||||||||||

| Foreign currency translation adjustment | |||||||||||||||||||

| Distributions | ( | ) | ( | ) | ( | ) | ( | ) | |||||||||||

| Equity-based compensation expense | |||||||||||||||||||

| Taxes paid related to net share settlement of equity-based compensation | ( | ) | ( | ) | |||||||||||||||

| Owners’ equity at March 31, 2020 | ( | ) | ( | ) | |||||||||||||||

| Net (loss) income for the period April 1, 2020 through June 30, 2020 | ( | ) | |||||||||||||||||

| Foreign currency translation adjustment | ( | ) | ( | ) | |||||||||||||||

| Distributions | ( | ) | ( | ) | ( | ) | ( | ) | |||||||||||

| Equity-based compensation expense | |||||||||||||||||||

| Owners’ equity at June 30, 2020 | ( | ) | ( | ) | |||||||||||||||

| Net (loss) income for the period July 1, 2020 through September 30, 2020 | ( | ) | |||||||||||||||||

| Foreign currency translation adjustment | ( | ) | ( | ) | |||||||||||||||

| Distributions | ( | ) | ( | ) | ( | ) | |||||||||||||

| Equity-based compensation expense | |||||||||||||||||||

| Owners’ equity at September 30, 2020 | $ | $ | $ | ( | ) | $ | ( | ) | $ | $ | |||||||||

| See accompanying notes. |

9

| CYPRESS ENVIRONMENTAL PARTNERS, L.P. |

| Unaudited Condensed Consolidated Statements of Cash Flows |

| For the Nine Months Ended September 30, 2021 and 2020 |

(in thousands) |

| Nine

Months Ended September 30, | ||||||||

| 2021 | 2020 | |||||||

| Operating activities: | ||||||||

| Net (loss) income | $ | ( | ) | $ | ||||

| Net (loss) income from discontinued operations, net of tax | ( | ) | ||||||

| Net loss from continuing operations | ( | ) | ( | ) | ||||

| Adjustments to reconcile net (loss) income to net cash (used in) provided by operating activities: | ||||||||

| Depreciation, amortization and accretion | ||||||||

| Loss on asset disposals, net | ||||||||

| Interest expense from debt issuance cost amortization | ||||||||

| Equity-based compensation expense | ||||||||

| Equity in earnings of investee | ( | ) | ( | ) | ||||

| Distributions from investee | ||||||||

| Foreign currency (gains) losses | ( | ) | ||||||

| Changes in assets and liabilities: | ||||||||

| Trade accounts receivable | ( | ) | ||||||

| Prepaid expenses and other | ( | ) | ||||||

| Accounts payable, accounts payable - affiliates and accounts receivable - affiliates | ( | ) | ( | ) | ||||

| Accrued payroll and other | ( | ) | ( | ) | ||||

| Income taxes payable | ( | ) | ( | ) | ||||

| Net cash (used in) provided by operating activities - continuing operations | ( | ) | ||||||

| Net cash (used in) provided by operating activities - discontinued operations | ( | ) | ||||||

| Net cash (used in) provided by operating activities | ( | ) | ||||||

| Investing activities: | ||||||||

| Proceeds from fixed asset disposals | ||||||||

| Purchases of property and equipment, excluding finance leases | ( | ) | ( | ) | ||||

| Net cash used in investing activities - continuing operations | ( | ) | ( | ) | ||||

| Net cash used in investing activities - discontinued operations | ( | ) | ( | ) | ||||

| Net cash used in investing activities | ( | ) | ( | ) | ||||

| Financing activities: | ||||||||

| Borrowings on credit facility | ||||||||

| Repayments on credit facility | ( | ) | ( | ) | ||||

| Repayments on finance lease obligations | ( | ) | ( | ) | ||||

| Debt issuance cost payments | ( | ) | ( | ) | ||||

| Taxes paid related to net share settlement of equity-based compensation | ( | ) | ( | ) | ||||

| Distributions | ( | ) | ( | ) | ||||

| Net cash used in financing activities - continuing operations | ( | ) | ( | ) | ||||

| Net cash used in financing activities - discontinued operations | ( | ) | ( | ) | ||||

| Net cash used in financing activities | ( | ) | ( | ) | ||||

| Effect of exchange rates on cash | ( | ) | ||||||

| Net decrease in cash and cash equivalents | ( | ) | ( | ) | ||||

| Cash and cash equivalents, beginning

of period (includes restricted cash equivalents of $ | (a) | (c) | ||||||

| Cash

and cash equivalents, end of period (includes restricted cash equivalents of $ | $ | (b) | $ | (d) | ||||

| Non-cash items: | ||||||||

| Accounts payable and accrued liabilities excluded from capital expenditures | $ | $ | ||||||

| Acquisitions of finance leases included in liabilities | $ | $ | ||||||

| Debt issuance costs included in accrued payroll and other | $ |

|

$ | |||||

| (a) | Amount

includes $ |

| (b) | Amount

includes $ |

| (c) | Amount

includes $ |

| (d) | Amount

includes $ |

See accompanying notes.

10

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Notes to the Unaudited Condensed Consolidated Financial Statements

| 1. | Organization and Operations |

Cypress Environmental Partners, L.P. (“we”, “us”, “our”, or the “Partnership”) is a Delaware limited partnership formed in 2013. We offer essential services that help protect the environment and ensure sustainability. We provide a wide range of environmental services including independent inspection, integrity, and support services for pipeline and energy infrastructure owners and operators and public utilities. We also provide water pipelines, hydrocarbon recovery, disposal, and water treatment services. Trading of our common units began January 15, 2014 on the New York Stock Exchange under the symbol “CELP”. Our business is organized into the Inspection Services (“Inspection Services”) and Water and Environmental Services (“Environmental Services”) segments.

The Inspection Services segment generates revenue by providing essential environmental services including inspection and integrity services on a variety of infrastructure assets including midstream pipelines, gathering systems, and distribution systems. Services include nondestructive examination, in-line inspection support, pig tracking, data gathering, and supervision of third-party contractors. We typically charge our customers a daily or hourly fee for our services, in addition to per diem, mileage, and other reimbursable items. Revenue and costs are subject to seasonal variations and interim activity may not be indicative of yearly activity, considering that many of our customers develop yearly operating budgets and enter into contracts with us during the winter season for work to be performed during the remainder of the year. Additionally, inspection work throughout the United States during the winter months (especially in the northern states) may be hampered or delayed due to inclement weather.

The

Environmental Services segment owns and operates

| 2. | Basis of Presentation and Summary of Significant Accounting Policies |

Basis of Presentation

The Unaudited Condensed Consolidated Financial Statements as of September 30, 2021 and for the three and nine months ended September 30, 2021 and 2020 include our accounts and those of our controlled subsidiaries. All intercompany transactions and account balances have been eliminated in consolidation. Investments over which we exercise significant influence, but do not control, are accounted for using the equity method of accounting. The Unaudited Condensed Consolidated Balance Sheet at December 31, 2020 is derived from our audited financial statements.

The accompanying Unaudited Condensed Consolidated Financial Statements have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim consolidated financial information and in accordance with the rules and regulations of the Securities and Exchange Commission (the “SEC”). The Unaudited Condensed Consolidated Financial Statements include all adjustments considered necessary for a fair presentation of the consolidated financial position and consolidated results of operations for the interim periods presented. Such adjustments consist only of normal recurring items, unless otherwise disclosed herein. Accordingly, the Unaudited Condensed Consolidated Financial Statements do not include all of the information and notes required by GAAP for complete consolidated financial statements. However, we believe that the disclosures made are adequate to make the information not misleading. These interim Unaudited Condensed Consolidated Financial Statements should be read in conjunction with our audited financial statements as of and for the year ended December 31, 2020 included in our Form 10-K. The results of operations for interim periods are not necessarily indicative of the results to be expected for a full year.

Use of Estimates in the Preparation of Financial Statements

The preparation of our Unaudited Condensed Consolidated Financial Statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in these financial statements and accompanying notes. Actual results could differ from those estimates.

The COVID-19 pandemic and the volatility in the price of crude oil have created and may continue to create significant uncertainty in macroeconomic conditions, which may continue to cause decreased demand for our services and adversely impact our results of operations. In addition, limitations on the availability of borrowing capacity under our current credit facility and any future credit facilities may lead us to sell assets and/or discontinue certain service lines. We consider these changing conditions as we develop accounting estimates, such as our annual effective tax rate, allowance for bad debts, and long-lived asset impairment assessments. We expect our accounting estimates to continue to evolve as new events and circumstances arise.

Significant Accounting Policies

Our significant accounting policies are consistent with those described in Note 2 to our audited consolidated financial statements as of and for the year ended December 31, 2020.

Discontinued Operations

In September 2021, we discontinued the operations of Cypress Brown Integrity, LLC (“CBI”), which previously represented our Pipeline & Process Services segment. CBI provided customers with hydrotesting, chemical cleaning, drying, water treatment, nitrogen and other related services. CBI was located in Giddings, Texas and a plan of termination impacted approximately 18 employees. Our reasons for exiting the business included the decline in new pipeline construction projects and the inability to obtain more work directly with pipeline owners on maintenance projects, which led to operating losses in 2021. We have recast the financial information for all periods presented in these Unaudited Condensed Consolidated Financial Statements to report the assets, liabilities, revenues, and expenses of CBI within discontinued operations.

In the third quarter of 2021, we recorded a loss of $

11

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Notes to the Unaudited Condensed Consolidated Financial Statements

These assets and liabilities of discontinued operations on the Unaudited Condensed Consolidated Balance Sheets are summarized below:

| September 30, | December 31, | |||||||

| 2021 | 2020 | |||||||

| ASSETS OF DISCONTINUED OPERATIONS | (in thousands) | |||||||

| Current assets of discontinued operations: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Trade accounts receivable, net | ||||||||

| Prepaid expenses and other | ||||||||

| Property and equipment, net | ||||||||

| Finance lease right-of-use assets, net | ||||||||

Total current assets of discontinued operations | ||||||||

| Property and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Finance lease right-of-use assets, net | ||||||||

| Total assets of discontinued operations | $ | $ | ||||||

| LIABILITIES OF DISCONTINUED OPERATIONS | ||||||||

| Current liabilities of discontinued operations: | ||||||||

| Accounts payable | $ | $ | ||||||

| Accrued payroll and other |

| |||||||

| Income taxes payable | ||||||||

| Finance lease obligations | ||||||||

| Total current liabilities of discontinued operations | ||||||||

| Finance lease obligations | ||||||||

| Total liabilities of discontinued operations | $ | $ | ||||||

The revenues and expenses of discontinued operations in our Unaudited Condensed Consolidated Statements of Operations are summarized below:

| Three

Months Ended September 30, | Nine

Months Ended September 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| (in thousands) | ||||||||||||||||

| Revenue | $ | $ | $ | $ | ||||||||||||

| Costs of services | ||||||||||||||||

| Gross margin | ( | ) | ( | ) | ||||||||||||

| Operating costs and expense: | ||||||||||||||||

| General and administrative | ||||||||||||||||

| Depreciation, amortization and accretion | ||||||||||||||||

| Loss (gain) on asset disposals, net | ( | ) | ( | ) | ||||||||||||

| Operating (loss) income | ( | ) | ( | ) | ||||||||||||

| Other (expense) income: | ||||||||||||||||

| Interest expense | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other, net | ||||||||||||||||

| Net (loss) income before income tax expense | ( | ) | ( | ) | ||||||||||||

| Income tax expense | ||||||||||||||||

| Net (loss) income from discontinued operations, net of tax | ( | ) | ( | ) | ||||||||||||

| Net (loss) income attributable to noncontrolling interests - discontinued operations | ( |

) | ( |

) | ||||||||||||

| Net (loss) income attributable to common unitholders - discontinued operations | $ | ( |

) | $ |

|

$ | ( |

) | $ | |||||||

General and administrative expenses that are directly attributable to CBI are reported within net

(loss) income from discontinued operations, net of tax

whereas general and administrative that are indirectly allocable to CBI are not reported within

net (loss) income from discontinued operations, net of tax.

Interest expense associated with $

Subsequent to September 30, 2021, the following events occurred:

| ● | CBI

sold certain vehicles which were accounted for as finance leases for $ |

| ● | CBI

sold certain fully-depreciated equipment for $ |

Goodwill

We

have $ of goodwill on our Unaudited Condensed Consolidated Balance Sheet at September 30, 2021. Of this amount, $

To perform a goodwill impairment assessment, we first evaluate qualitative factors to determine whether it is more likely than not that the fair value of a reporting unit exceeds its carrying value. If this assessment reveals that it is more likely than not that the carrying value of a reporting unit exceeds its fair value, we then determine the estimated fair market value of the reporting unit. If the carrying amount exceeds the reporting unit’s fair value, we record a goodwill impairment charge for the excess (not exceeding the carrying value of the reporting unit’s goodwill).

12

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Notes to the Unaudited Condensed Consolidated Financial Statements

For our Inspection Services and Environmental Services segments, we performed goodwill impairment analyses at November 1, 2020 and concluded that the fair values of the reporting units were more likely than not greater than their carrying values. Our evaluation included various factors, including current and projected earnings, current customer relationships and projects, and the impact of commodity prices on our earnings. The use of different assumptions and estimates from the assumptions and estimates we used in our analyses could have resulted in the requirement to record a goodwill impairment. It is reasonably possible that changes could occur that would require a goodwill impairment charge in the future. For the Inspection Services segment, such changes could include, among others, a slower than expected recovery in demand for inspection and integrity services and increased pessimism among market participants, which could increase the discount rate on (and therefore reduce the value of) estimated future cash flows. For the Environmental Services segment, such changes could include, among others, a slower than expected recovery in demand for petroleum products, an increase in supply from other areas (or other factors) that result in reduced production in North Dakota, an increase in costs reducing our profitability, and increased pessimism among market participants, which could increase the discount rate on (and therefore reduce the value of) estimated future cash flows. Our goodwill impairment assessment for both the Inspection Services and Environmental Services segments included an assumption that our revenues will increase in future years. If this assumption proves to be incorrect, we could be required to record a goodwill impairment in a future period.

Accounts Receivable and Allowance for Bad Debts

We

grant unsecured credit to customers under normal industry standards and terms and have established policies and procedures that

allow for an evaluation of the creditworthiness of each of our customers. We typically receive payment from our customers 45 to

75 days after the services have been performed. We determine allowances for bad debts based on management’s assessment of

the creditworthiness of our customers. Trade receivables are written off against the allowance when deemed uncollectible. Recoveries

of trade receivables previously written off are recorded when cash is received. As of both September 30, 2021 and December 31,

2020, we had an allowance for doubtful accounts of $

Accrued Payroll and Other

Accrued payroll and other on our Unaudited Condensed Consolidated Balance Sheets includes the following:

| September 30, 2021 | December 31, 2020 | |||||||

| (in thousands) | ||||||||

| Accrued payroll | $ | $ | ||||||

| Customer deposits and accruals | ||||||||

| Other | ||||||||

| $ | $ | |||||||

Revenue Recognition

Under Accounting Standards Codification (“ASC”) 606 - Revenue from Contracts with Customers, an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. Based on this accounting guidance, our revenue is earned and recognized through the service offerings of our reportable business segments. Our sales contracts have terms of less than one year. As such, we have used the practical expedient contained within the accounting guidance, which exempts us from the requirement to disclose the transaction price allocated to remaining performance obligations if the performance obligation is part of a contract with an original expected duration of one year or less. We apply judgment in determining whether we are the principal or the agent in instances where we utilize subcontractors to perform all or a portion of the work under our contracts. Based on the criteria in ASC 606, we have determined we are principal in all such circumstances, with the exception of $

As

of September 30, 2021, and December 31, 2020, we recognized a refund liability of less than $

During

the three months ended September 30, 2021, we received a signed contract modification from one of our customers for a price increase

that is retroactive to June 2021. We recorded $

Foreign Currency Translation

Our Unaudited Condensed Consolidated Financial Statements are reported in U.S. dollars. We translate our Canadian-dollar-denominated assets and liabilities into U.S. dollars at the exchange rate in effect at the balance sheet date. We translate our Canadian-dollar-denominated revenues and expenses into U.S. dollars at the average exchange rate in effect during the period in which the applicable revenues and expenses were recorded.

Our Unaudited Condensed Consolidated Balance Sheet at September 30, 2021 includes $ of accumulated other comprehensive loss associated with accumulated currency translation adjustments, all of which relate to our Canadian operations. If at some point in the future we were to sell or substantially liquidate our Canadian operations, we would reclassify the balance in accumulated other comprehensive loss to other accounts within partners’ capital, which would be reported in the Unaudited Condensed Consolidated Statement of Operations as a reduction to net (loss) income. Our Canadian subsidiary has certain payables to our U.S.-based subsidiaries. These intercompany payables and receivables among our consolidated subsidiaries are eliminated on our Unaudited Condensed Consolidated Balance Sheets. We report currency translation adjustments on these intercompany payables and receivables within foreign currency (losses) gains in our Unaudited Condensed Consolidated Statements of Operations.

New Accounting Standards

Accounting guidance proposed by the Financial Accounting Standards Board (“FASB”) that may impact our Unaudited Condensed Consolidated Financial Statements, which we have not yet adopted, includes:

The FASB issued Accounting Standards Update (“ASU”) 2016-13 – Financial Instruments – Credit Losses in September 2016, which replaces the current “incurred loss” methodology for recognizing credit losses with an “expected loss” methodology. This guidance affects trade receivables, financial assets and certain other instruments that are not measured at fair value through net income. In November 2019, the FASB issued final guidance to delay the implementation of this new guidance for smaller reporting companies until fiscal years beginning after December 15, 2022, including interim periods within those fiscal years. We are currently evaluating the impact this ASU will have on our Unaudited Condensed Consolidated Financial Statements.

The FASB issued ASU 2020-06 – Debt – Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40)—Accounting For Convertible Instruments and Contracts in an Entity’s Own Equity in August 2020. The ASU simplifies accounting for convertible instruments by removing major separation models required under current GAAP. Consequently, more convertible debt instruments will be reported as a single liability instrument with no separate accounting for embedded conversion features. The ASU removes certain settlement conditions that are required for equity contracts to qualify for the derivative scope exception, which will permit more equity contracts to qualify for it. The ASU also simplifies the diluted net income per share calculation in certain areas. The new guidance is effective for annual and interim periods for smaller reporting companies beginning after December 15, 2023, and early adoption is permitted for fiscal years beginning after December 15, 2020, and interim periods within those fiscal years. We are currently evaluating the impact this ASU will have on our Unaudited Condensed Consolidated Financial Statements.

13

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Notes to the Unaudited Condensed Consolidated Financial Statements

| 3. | Debt |

We

are party to a credit agreement (the “Credit Agreement”) with a syndicate of seven banks, with Deutsche Bank Trust

Company Americas serving as the Administrative Agent. The obligations under the Credit Agreement are secured by a first priority

lien on substantially all of our assets. The Credit Agreement was amended in March 2021 and in August 2021. As amended, the Credit

Agreement has a total capacity of $

Outstanding

borrowings at September 30, 2021 and December 31, 2020 were $

All

borrowings under the Credit Agreement bear interest, at our option, on a leveraged based grid pricing at (i) a base rate plus

a margin of

The

Credit Agreement contains various customary covenants and restrictive provisions. Prior to the August 2021 amendment, the Credit

Agreement also required us to maintain certain financial covenants, including a leverage ratio and an interest coverage ratio.

After the August 2021 amendment, these financial ratio covenant requirements have been removed. As amended in August 2021, the

Credit Agreement requires that we maintain liquidity in excess of $

As amended in August 2021, the Credit Agreement contains significant limitations on our ability to pay cash distributions. We may only pay the following cash distributions:

| ● | distributions to common and preferred unitholders, to the extent of income taxes estimated to be payable by these unitholders resulting from allocations of our earnings; and |

| ● | distributions to the noncontrolling interest owners of CBI and CF Inspection. |

The

Credit Agreement, as amended, restricts our ability to redeem or repurchase our equity interests and requires us to use the proceeds

from asset sales in excess of $

Debt

issuance costs are reported as debt issuance costs, net on the Unaudited Condensed Consolidated Balance Sheets and total

$

The carrying value of our long-term debt approximates fair value, as the borrowings under the Credit Agreement are considered to be priced at market for debt instruments having similar terms and conditions (Level 2 of the fair value hierarchy).

| 4. | Income Taxes |

As a limited partnership, we are generally not subject to U.S. federal or state income taxes. Our income tax provision relates primarily to (1) our U.S. corporate subsidiaries that provide services to public utility customers, which may not fit within the definition of qualified income as it is defined in the Internal Revenue Code, Regulations, and other guidance, which subjects this income to U.S. federal and state income taxes, (2) our Canadian subsidiary, which is subject to Canadian federal and provincial income taxes, and (3) certain other state income taxes, including the Texas franchise tax.

As

a publicly-traded partnership, we are subject to a statutory requirement that

| 5. | Equity |

Series A Preferred Units

On

May 29, 2018 (the “Closing Date”), we sold

The

Purchaser has the option to convert the Preferred Units into common units on a one-for-one basis. If certain conditions are met,

we will have the option to cause the Preferred Units to convert to common units. We also have the option to redeem the Preferred

Units. We may redeem the Preferred Units (a) at any time or prior to the fourth anniversary of the Closing Date at a redemption

price equal to

At-the-Market Equity Program

In

April 2018, we established an at-the-market equity program (“ATM Program”), which allows us to offer and sell common

units from time to time, to or through the sales agent under the ATM Program, up to an aggregate offering amount of $

14

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Notes to the Unaudited Condensed Consolidated Financial Statements

Employee Unit Purchase Plan

In

November 2019, we established an employee unit purchase plan (“EUPP”), which allows us to offer and sell up to

common units. Employees could elect to have up to

Net Loss per Unit

Our

net loss (income) is attributable and allocable to three ownership groups: (1) our preferred unitholder, (2) the noncontrolling

interests in certain subsidiaries, and (3) our common unitholders. Income attributable to preferred unitholder represents the

Basic and diluted net loss per common limited partner unit - continuing operations is calculated as net loss attributable to common unitholders - continuing operations divided by the basic weighted average common units outstanding. Basic and diluted net (loss) income per common limited partner unit - discontinued operations is calculated as net (loss) income attributable to common unitholders - discontinued operations divided by the basic weighted average common units outstanding.

| Three

Months Ended September 30, | Nine

Months Ended September 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| (in thousands, except per unit data) | ||||||||||||||||

| Net loss attributable to common unitholders - continuing operations | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Net (loss) income attributable to common unitholders - discontinued operations | ( | ) | ( | ) | ||||||||||||

| Net loss attributable to common unitholders | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Weighted average common units outstanding | ||||||||||||||||

| Basic and diluted net loss per common limited partner unit - continuing operations | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Basic and diluted net (loss) income per common limited partner unit - discontinued operations | ( | ) | ( | ) | ||||||||||||

| Basic and diluted net loss per common limited partner unit | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

For the three and nine months ended September 30, 2021 and 2020, the preferred units and the long-term incentive plan unvested units would have been antidilutive, and therefore diluted net loss per common limited partner unit and basic net loss per common limited partner unit are the same amount.

Distributions

We

paid common unit distributions of $

We

paid

CBI’s

company agreement generally requires CBI to make an annual distribution to its members equal to or greater than the amount of

CBI’s taxable income multiplied by the maximum federal income tax rate. In March 2021, CBI declared and paid a distribution

of $

Long-Term Incentive Plan (“LTIP”)

During

March 2021, four members of our Board of Directors (“Directors”) elected to have certain of their LTIP units net settled

upon vesting for tax withholding purposes. As the Directors are not considered employees under the IRS statutory withholding requirements,

any unit withholding upon settlement is considered an excess withholding, resulting in liability accounting treatment for the

entire award. The modification of these awards from equity awards to liability awards did not result in the recognition of any

additional compensation cost. As of September 30, 2021, we recorded $

In May 2021, we granted Unit Appreciation Rights (“UARs”) and phantom restricted units (“Units”) to certain employees and directors. The UARs will vest in three equal tranches in May 2024, May 2025, and May 2026, respectively, contingent only on the continued service of the recipients through the vesting dates. The UARs have an exercise price of $ and terminate from the grant date. The Units will vest in three equal tranches in May 2022, May 2023, and May 2024, respectively, contingent only on the continued service of the recipients through the vesting dates.

| 6. | Related-Party Transactions |

Holdings

We are party to an omnibus agreement with Holdings and other related parties. The omnibus agreement provides for, among other things, our right of first offer on Holdings’ and its subsidiaries’ assets used in, and entities primarily engaged in, providing water treatment and other water and environmental services. So long as Holdings controls our General Partner, the omnibus agreement will remain in full force and effect, unless we and Holdings agree to terminate it sooner. If Holdings ceases to control our General Partner, either party may terminate the omnibus agreement. We and Holdings may agree to further amend the omnibus agreement; however, amendments that the General Partner determines are adverse to our unitholders will also require the approval of the Conflicts Committee of our Board of Directors. Prior to June 30, 2021, all of the employees who conduct our business were employed by affiliates of Holdings, although we often refer to these individuals in this report as our employees. We generally reimbursed Holdings for the compensation costs associated with these employees. Effective June 30, 2021, all of our employees are employed by subsidiaries of the Partnership.

Alati Arnegard, LLC

The

Partnership provides management services to a

15

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Notes to the Unaudited Condensed Consolidated Financial Statements

CF Inspection Management, LLC

We

have also entered into a joint venture with CF Inspection, a nationally-qualified woman-owned business. CF Inspection allows us

to offer various services to clients that require the services of an approved Women’s Business Enterprise, as CF Inspection

is certified as a Women’s Business Enterprise by the Supplier Clearinghouse in California and as a National Women’s

Business Enterprise by the Women’s Business Enterprise National Council. We own

CBI

Entities

owned by Holdings provided contract labor support to CBI during 2021 and 2020. During the nine months ended September 30, 2021 and

2020, CBI incurred costs less than $

Continental Resources, Inc.

A

Director of our General Partner is the President and Chief Operating Officer of Continental Resources, Inc. (“Continental”).

Our Environmental Services segment began providing water treatment services to Continental at the end of 2020. Revenues from Continental

during the nine months ended September 30, 2021 were $

| 7. | Commitments and Contingencies |

Security Deposits

We

have various obligations that are secured with security deposits totaling $

Compliance Audit Contingencies

Certain

agreements with customers offer our customers the right to perform periodic compliance audits, which include the examination of

the accuracy of our invoices. Should our invoices be determined to be inconsistent with the agreements, the agreements may provide

the customer the right to receive a credit or refund for overcharges identified. At any given time, we may have multiple audits

ongoing. As of September 30, 2021 and December 31, 2020, we established reserves of $

Legal Proceedings

We are and may in the future be subject to litigation and binding arbitration involving allegations of violations of the Fair Labor Standards Act and state wage and hour laws. In addition, we generally indemnify our customers for claims related to the services we provide and actions we take under our contracts, including claims regarding the Fair Labor Standards Act and state wage and hour laws, and have received indemnification demands from some of our customers in regard to such claims, and, in some instances, we may be allocated risk through our contract terms for actions by our customers or other third parties. Claims related to the Fair Labor Standards Act are generally not covered by insurance. From time to time, we are subject to various claims, lawsuits and other legal proceedings brought or threatened against us in the ordinary course of our business. These actions and proceedings may seek, among other things, compensation for alleged personal injury, workers’ compensation, employment discrimination and other employment-related damages, breach of contract, property damage, environmental liabilities, punitive damages and civil penalties or other losses, liquidated damages, consequential damages, or injunctive or declaratory relief. The outcome of related litigation is unknown at this time but could be material to our financial statements in future periods. As of September 30, 2021 we have accrued $0.3 million for certain claims on which we have offered a settlement.

Gain on Settlement of Dispute

In November 2021, we settled a dispute with another party. We and the other party agreed to fully and finally resolve our differences without any admission of liability. We received proceeds of $

16

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Notes to the Unaudited Condensed Consolidated Financial Statements

| 8. | Reportable Segments |

Our operations consist of two reportable segments: (i) Inspection Services and (ii) Water and Environmental Services (“Environmental Services”). The amounts within “Other” represent corporate and overhead items not specifically allocable to the other reportable segments. As described in Note 2, we have reclassified our former Pipeline & Process Services segment to discontinued operations for all periods presented.

| Inspection | Environmental | |||||||||||||||

| Services | Services | Other | Total | |||||||||||||

| (in thousands) | ||||||||||||||||

| Three months ended September 30, 2021 | ||||||||||||||||

| Revenue | $ | $ | $ | $ | ||||||||||||

| Costs of services | ||||||||||||||||

| Gross margin | ||||||||||||||||

| General and administrative | (a) | |||||||||||||||

| Depreciation, amortization and accretion | ||||||||||||||||

| Loss on asset disposals, net | ||||||||||||||||

| Operating income (loss) | $ | $ | ( | ) | $ | ( | ) | ( | ) | |||||||

| Interest expense | ( | ) | ||||||||||||||

| Foreign currency losses | ( | ) | ||||||||||||||

| Other, net | ||||||||||||||||

| Net loss before income tax expense | $ | ( | ) | |||||||||||||

| Three months ended September 30, 2020 | ||||||||||||||||

| Revenue | $ | $ | $ | $ | ||||||||||||

| Costs of services | ||||||||||||||||

| Gross margin | ||||||||||||||||

| General and administrative | (b) | |||||||||||||||

| Depreciation, amortization and accretion | ||||||||||||||||

| Gain on asset disposals, net | ( | ) | ( | ) | ||||||||||||

| Operating income (loss) | $ | $ | $ | ( | ) | |||||||||||

| Interest expense | ( | ) | ||||||||||||||

| Foreign currency gains | ||||||||||||||||

| Other, net | ||||||||||||||||

| Net income before income tax expense | $ | |||||||||||||||

| (a) | Amount

includes $ |

| (b) | Amount

includes $ |

17

CYPRESS ENVIRONMENTAL PARTNERS, L.P.

Notes to the Unaudited Condensed Consolidated Financial Statements

| Inspection | Environmental | |||||||||||||||

| Services | Services | Other | Total | |||||||||||||

| (in thousands) | ||||||||||||||||

| Nine months ended September 30, 2021 | ||||||||||||||||

| Revenue | $ | $ | $ | $ | ||||||||||||

| Costs of services | ||||||||||||||||

| Gross margin | ||||||||||||||||

| General and administrative | (c) | |||||||||||||||

| Depreciation, amortization and accretion | ||||||||||||||||

| Loss on asset disposals, net | ||||||||||||||||

| Operating loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | ( | ) | |||||

| Interest expense | ( | ) | ||||||||||||||

| Foreign currency gains | ||||||||||||||||

| Other, net | ||||||||||||||||

| Net loss before income tax expense | $ | ( | ) | |||||||||||||

| Nine months ended September 30, 2020 | ||||||||||||||||

| Revenue | $ | $ | $ | $ | ||||||||||||

| Costs of services | ||||||||||||||||

| Gross margin | ||||||||||||||||

| General and administrative | (d) | |||||||||||||||

| Depreciation, amortization and accretion | ||||||||||||||||

| Loss on asset disposals, net | ||||||||||||||||

| Operating income (loss) | $ | $ | $ | ( | ) | |||||||||||

| Interest expense | ( | ) | ||||||||||||||

| Foreign currency losses | ( | ) | ||||||||||||||

| Other, net | ||||||||||||||||

| Net loss before income tax expense | $ | ( | ) | |||||||||||||

| Total Assets | ||||||||||||||||

| September 30, 2021 | $ | $ | $ | $ | ||||||||||||

| December 31, 2020 | $ | $ | $ | $ | ||||||||||||

| (c) | Amount

includes $ |

| (d) | Amount

includes $ |

18

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion contains forward-looking statements that reflect our future plans, estimates, beliefs and expected performance. The forward-looking statements are dependent upon events, risks and uncertainties that may be outside our control, including, among other things, the risk factors discussed in “Item 1A. Risk Factors” of our Annual Report on Form 10-K for the year ended December 31, 2020 and this Quarterly Report on Form 10-Q. Our actual results could differ materially from those discussed in these forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, market prices for oil and natural gas, production volumes, capital expenditures, weather, economic and competitive conditions, regulatory changes and other uncertainties, as well as those factors discussed below and elsewhere in our Annual Report on Form 10-K for the year ended December 31, 2020 and this Quarterly Report on Form 10-Q, all of which are difficult to predict. In light of these risks, uncertainties, and assumptions, the forward-looking events discussed may or may not occur. See “Cautionary Remarks Regarding Forward-Looking Statements” in the front of this Quarterly Report on Form 10-Q.

This Management’s Discussion and Analysis of Financial Condition and Results of Operations contains a discussion of our business, including a general overview of our properties, our results of operations, our liquidity and capital resources, and our quantitative and qualitative disclosures about market risk broken down into two segments: (1) our Inspection Services (“Inspection Services”) segment comprises the TIR Entities and; (2) our Water and Environmental Services (“Environmental Services”) segment comprises our water treatment facilities. The financial information for the Inspection Services and Environmental Services segments is included in “Item 2 – Management’s Discussion and Analysis of Financial Condition and Results of Operations” should be read in conjunction with the interim financial statements and related notes included elsewhere in this report and prepared in accordance with accounting principles generally accepted in the United States of America and in our Consolidated Financial Statements for the year ended December 31, 2020 included in our Annual Report on Form 10-K for the year ended December 31, 2020.

Overview

We are a growth-oriented master limited partnership formed in September 2013. We offer essential services that help protect the environment and ensure sustainability. We provide a wide range of environmental services including independent inspection, integrity, and support services for pipeline and energy infrastructure owners and operators and public utilities. We also provide water pipelines, hydrocarbon recovery, disposal, and water treatment services. The Inspection Services segment comprises the operations of our TIR Entities. We also provide water treatment and other water and environmental services to U.S. onshore oil and natural gas producers and trucking companies through our Environmental Services segment.

In September 2021 we discontinued the operations of Cypress Brown Integrity, LLC (“CBI”), which previously represented our Pipeline & Process Services segment. We have classified the accounts of CBI within discontinued operations in the accompanying Unaudited Condensed Consolidated Financial Statements.

Ownership

As of September 30, 2021, Holdings and its affiliates own 64% of our common units. Holdings’ ownership group also owns 100% of the General Partner and certain incentive distribution rights (although no such incentive distributions have been paid to date), and an affiliate of Holdings owns 100% of the preferred units.

Omnibus Agreement

We are party to an omnibus agreement with Holdings and other related parties. The omnibus agreement provides for, among other things, our right of first offer on Holdings’ and its subsidiaries’ assets used in, and entities primarily engaged in, providing water treatment and other water and environmental services. So long as Holdings controls our General Partner, the omnibus agreement will remain in full force and effect, unless we and Holdings agree to terminate it sooner. If Holdings ceases to control our General Partner, either party may terminate the omnibus agreement. We and Holdings may agree to further amend the omnibus agreement; however, amendments that the General Partner determines are adverse to our unitholders will also require the approval of the Conflicts Committee of our Board of Directors.

Inspection Services

The Inspection Services segment generates revenue by providing essential environmental services, including inspection and integrity services on a variety of infrastructure assets, such as midstream pipelines, gathering systems, and distribution systems. Services include nondestructive examination, in-line inspection support, pig tracking, data gathering, and supervision of third-party contractors. Our revenues in this segment are driven by the number of inspectors who perform services for our customers and the fees that we charge for those services, which depend on the type, skills, technology, equipment, and number of inspectors used on a particular project, the nature of the project, and the duration of the project. The number of inspectors engaged on projects is driven by the type of project, the age and condition of customers’ assets including pipelines, gas plants, compression stations, storage facilities, and gathering and distribution systems including the legal and regulatory requirements relating to the inspection and maintenance of those assets. We also bill our customers for per diem charges, mileage, and other reimbursement items. Revenue and costs in this segment are subject to seasonal variations and interim activity may not be indicative of yearly activity, considering many of our customers develop yearly operating budgets and enter into contracts with us during the winter season for work to be performed during the remainder of the year. Additionally, inspection work throughout the United States during the winter months (especially in the northern states) may be hampered or delayed due to inclement weather. The first and fourth quarters of each year are typically slower than the second and third quarters, due to weather conditions and customers’ budgeting cycles.

Environmental Services

The Environmental Services segment owns and operates nine water treatment facilities with ten EPA Class II injection wells in the Bakken shale region of the Williston Basin in North Dakota. We wholly-own eight of these water treatment facilities and we own a 25% interest in the other facility. These water treatment facilities are connected to thirteen pipeline gathering systems, including two that we developed and own. We specialize in the treatment, recovery, separation, and disposal of waste byproducts generated during the lifecycle of an oil and natural gas well to protect the environment and our drinking water. All of the water treatment facilities utilize specialized equipment and remote monitoring to minimize the facilities’ downtime and increase the facilities’ efficiency for peak utilization. Revenue is generated on a fixed-fee per barrel basis for receiving, separating, filtering, recovering, processing, and injecting produced and flowback water. We also sell recovered oil, receive fees for pipeline transportation of water, and receive fees from a partially-owned water treatment facility for management and staffing services.

Outlook

Overall

Our 2020 results were the worst in our short history following our best year in 2019. The financial results in 2020 were adversely affected by a significant decline in oil prices, which was driven in part by increased supply from Russia, Saudi Arabia, and other oil-producing nations as a result of a price war and in part by a significant decrease in demand as a result of the COVID-19 pandemic. The combination of these events led many of our customers to cancel planned construction projects and to defer regular maintenance projects whenever possible. The effects of these events placed significant financial pressures on the vast majority of our customers to reduce costs, which led some of our customers to aggressively pursue pricing concessions. We value our long-term customer relationships and worked closely with them to address this reality, which in turn required us to modify what pay we could offer to our valued inspectors. Despite the COVID-19 pandemic, we continued our field operations without any significant disruption in our service to our customers.

19

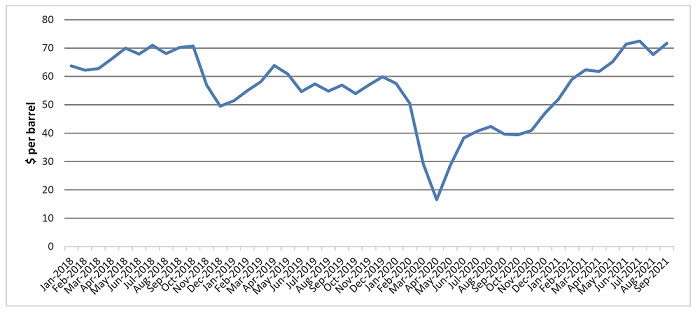

Previously, OPEC started a price war for market share in November 2014 that led to a downturn that lasted through 2017. The industry, our customers, and we benefitted from a rebound in 2018 and 2019. In the years leading into 2020, many companies had been active in constructing new energy infrastructure, such as pipelines, gas plants, compression stations, pumping stations, and storage facilities, which afforded us the opportunity to provide our inspection and integrity services on these projects. The commodity price decline in 2020 led our customers to change their budgets and plans, and to decrease their spending on capital expenditures. This, in turn, had an impact on regular maintenance work and the construction of new pipelines, gathering systems, and related energy infrastructure. Lower exploration and production activity also affected the midstream industry and led to delays and cancellations of projects. The volatility in crude oil prices is illustrated in the chart below, which shows the average monthly spot price for West Texas Intermediate crude oil from 2018 through September 2021:

Recognizing the impact of the COVID-19 pandemic, we took swift and decisive actions in 2020 to reduce overhead and other costs through a combination of salary reductions, reductions in workforce, and other cost-cutting measures. We elected to defer some discretionary capital expenditures and we remained focused on opportunities to reduce our working capital needs. In early 2021, we took additional actions to further reduce our costs with some additional reductions in workforce and furloughs. These actions have significantly lowered our general and administrative costs. While reducing certain costs, we have also made investments in personnel in our account management and business development teams, to position ourselves to take advantage of the market’s eventual recovery. In addition, the challenging market conditions notwithstanding, in May 2021 we prospectively restored the salaries of certain key employees that had accepted temporary salary reductions in 2020.

In light of the adverse market conditions, we made the difficult decision in July 2020 to temporarily suspend payment of common unit distributions. This has enabled us to retain more cash to manage our working capital and financing requirements during these challenging market conditions. Our credit facility, as amended in 2021, contains significant restrictions on our ability to pay cash distributions to common and preferred unitholders. As a result, we expect to use cash generated from operations for working capital to support revenue growth and to pay down debt.

The vaccination process for COVID-19 has progressed, which has likely been a leading factor in the recent recovery in demand for crude oil. The price of crude oil has increased in 2021, with the average daily spot price for West Texas Intermediate crude oil increasing from $48.35 per barrel at December 31, 2020 to $81.96 per barrel at November 8, 2021. We expect that a sustained increase in crude oil prices would lead customers to increase their maintenance and capital spending plans, although to this point, customers have been slow to increase activity. We continue to focus on winning new customers while supporting our existing customers.

Sales and business development continue to be among our top priorities, and we are bidding on many projects with both existing and prospective new customers. The near-term recovery remains fragile, as market participants evaluate the risks associated with new variants of the coronavirus. Our customers continue to evaluate these changing circumstances. Historically, as commodity prices increase, customers begin to increase their spending, which increases our opportunities to provide services. Although higher commodity prices typically benefit our business, we typically experience a lag between when commodity prices increase and when our customers begin to increase their spending for our services. We believe there will be significant long-term demand for our services, and we continue our efforts to diversify our customer base. We have continued to invest in talent in the areas of account management and business development. We strive to position ourselves as a stable and reliable provider of high-quality services to our customer base.

In 2020 we made the strategic decision to pursue new inspection markets to diversify our inspection business to markets not tied to commodity prices. We have the expertise and systems to offer inspection services into new markets such as municipal water, sewer, bridges, electrical transmission, marine coatings, wind, solar, and hydroelectric. We have been bidding inspection jobs in these new markets and many of our inspectors and employees have the skills to offer services to these new markets. Over the long term, we hope to have the majority of our inspection revenue coming from these new services.

20

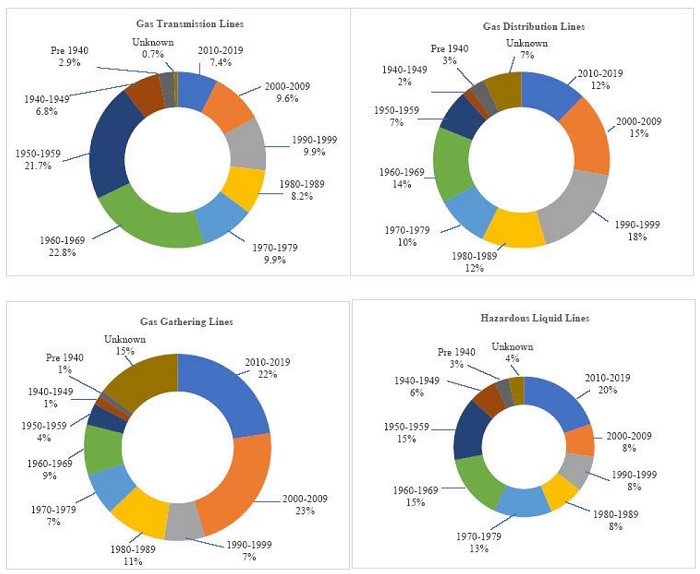

We believe government regulation under the new administration will continue to grow with a focus on protecting the environment. The U.S. Pipeline and Hazardous Materials Safety Administration (“PHMSA”) recently issued new rules that impose several new requirements on operators of onshore gas transmission systems and hazardous liquids pipelines. The new rules expand requirements to address risks to pipelines outside of environmentally sensitive and populated areas. In addition, the rules make changes to integrity management requirements, including emphasizing the use of in-line inspection technology. The new rules took effect on July 1, 2020 with various implementation phases over a period of years. We remain optimistic about the long-term demand for environmental services such as inspection services, integrity services, and water solutions, due to our nation’s aging pipeline infrastructure, and we believe we continue to be well-positioned to capitalize on these opportunities. The following charts summarize the age of pipelines in the United States, as developed from independent research and government data:

In 2018, Holdings completed an acquisition to further broaden our collective suite of environmental services. This acquisition provided entry into the municipal water industry, whereby we can offer our traditional inspection services, including corrosion and nondestructive testing services, as well as in-line inspection (“ILI”). Holdings’ next generation 5G ultra high-resolution magnetic flux leakage (“MFL”) ILI technology called EcoVision™ UHD, is capable of helping pipeline owners and operators better manage the integrity of their pipeline assets in both the municipal water and energy industries. We believe Holdings is the only technology provider today capable of offering this service to the large and diverse municipal water industry that provides drinking water to our communities. Holdings has been investing in building tools to serve pipelines of various sizes. At some point in the future, this business may be offered to the Partnership when appropriate. We do not expect to acquire this business in the near term, although we continue to use our affiliation with this business as a cross-selling opportunity for our services.

Our parent company’s ownership interests continue to remain fully aligned with our unitholders, as our General Partner and insiders collectively own 76% of our total common and preferred units.

In March 2021, we entered into an amendment to our credit facility that extended the maturity date of the facility to May 2022, reduced the total borrowing capacity under the facility from $110.0 million to $75.0 million, and made the leverage ratio covenant temporarily less restrictive. In August 2021, we entered into another amendment to the credit facility that, among other things, removed certain financial statement ratio covenants for the remaining term of the facility and reduced the total capacity under the facility from $75.0 million to $70.0 million. We continue to have discussions with our lenders regarding our financing options beyond the May 2022 maturity date of our credit facility. It is possible that any future amendments, extensions, or replacements of the credit facility could further reduce the borrowing capacity under the credit facility, further limit our payment of distributions or add other new restrictions, which could further limit our ability to borrow for working capital to fund revenue growth and could also restrict our ability to borrow to fund capital expenditures. Future amendments, extensions, or replacements of the credit facility could also result in increased interest rates and bank fees. We have incurred and expect to continue to incur additional advisory fees in developing our financing plans. We can make no assurances that we will be able to successfully extend the credit facility beyond the May 2022 maturity date. As part of our efforts to reduce our outstanding debt and working capital needs, we will consider asset sales, which could result in impairments to long-lived assets in future periods. In September 2021, we discontinued the operations of our Pipeline & Process Services segment, which is now reported within discontinued operations in the accompanying Unaudited Condensed Consolidated Financial Statements. In October 2021, we decided to wind down our survey service line, which represented less than 1% of the total revenues of the Inspection Services segment during the nine months ended September 30, 2021.

Inspection Services

Revenues of our Inspection Services segment decreased from $41.9 million during the three months ended September 30, 2020 to $31.5 million during the three months ended September 30, 2021, a decrease of 25%. Gross margins in this segment decreased from $5.1 million during the three months ended September 30, 2020 to $3.9 million during the three months ended September 30, 2021, a decrease of 24%. At the end of the first quarter of 2020, the outbreak of the COVID-19 pandemic, combined with a significant decrease in crude oil prices resulting from reduced demand and an anticipated increase in supply from Saudi Arabia and Russia, led many of our customers to reduce their spending on capital expenditures and maintenance projects. Most projects that were already in process continued, despite the COVID-19 pandemic. However, many customers announced reductions in their capital expansion budgets and deferrals of planned construction projects, which significantly reduced our opportunities to generate revenue from inspection services. The lower level of activity continued into 2021, and many of our customers have not yet resumed significant spending on capital expansion. We are beginning to see signs of a market upcycle driven by much higher commodity prices, which we expect to benefit many of our customers in the energy industry.

The macroeconomic fundamentals have strengthened recently with a recovery in demand for oil, natural gas, and refined products. Absent a recession or pandemic-related economic setback, these positive dynamics are expected to benefit our industry. The development by our customers of large expansion projects typically lags behind increases in commodity prices, due to the time required to plan, permit, and initiate large-scale projects.

In 2021, a large majority of our revenues have been generated from services to utility customers and maintenance services to our customers in the energy industry, rather than from new construction projects. Services to public utility customers have represented over 50% of the Inspection Services segment’s revenues in 2021. We have seen modest improvement during 2021, as our average monthly inspector headcount increased from 436 in January 2021 to 462 in September 2021.

We expect customers to continue to conduct maintenance activities, many of which are government-mandated. However, many clients are deferring maintenance work whenever possible if they have the option. We believe our reputation developed over 18 years will give us a competitive advantage during this challenging industry downturn when some of our competitors may not survive.

21

We continue to bid on new inspection opportunities, including in new markets such as electrical transmission and municipal water. We operate in a very large market, with more than 3,000 customer prospects who require federally and/or state-mandated inspection and integrity services. Our focus remains on maintenance and integrity work on existing pipelines, as well as work on new projects. The majority of our clients are large public companies with long planning cycles that lead to healthy backlogs of new long-term projects when market conditions warrant and existing pipeline networks that also require inspection and integrity services. We believe that regulatory requirements, coupled with the aging pipeline infrastructure, mean that our customers will require our inspection services regardless of commodity prices. However, any prolonged downturn in oil and natural gas prices could lead to reduced demand for our services.

We are currently reviewing our inspector remuneration programs to address a longstanding industry practice whereby inspectors are provided with fixed reimbursements based on estimates of their out-of-pocket expenditures. We plan to reduce these reimbursements to our inspectors and to make corresponding increases in their wages and benefits. We have also continued our process of converting inspector compensation from day rates to hourly rates. We believe these changes should be welcomed by our customers and inspectors; however, these changes could lead to the loss of inspectors who prefer the historical practices, as inspectors could choose to switch to competitors that maintain such historical remuneration practices.

Occupational Safety and Health Administration (“OSHA”) released federal regulations implementing a workplace COVID-19 vaccination mandate, effective January 4, 2022. Employers with 100 or more employees would be required to establish, implement, and enforce a policy that either ensures their workers are fully vaccinated or requires all unvaccinated workers to wear a mask and submit to weekly COVID-19 testing. We are still evaluating the potential impact of these new regulations on our field personnel and inspectors. Additionally, various state employment laws may impact us. These policies could lead to the departure of inspectors, to the extent that inspectors refuse to accept the mandates of such policies, and these departures could result in the loss of revenue and/or additional cost to find new inspectors.