U.S. Equity Market Structure: Making Our Markets Work Better for Investors

Commissioner Luis A. Aguilar

U.S. Securities and Exchange Commission[1]

I. Introduction

It is well known that the Commission needs to undertake a holistic review of our current equity market structure. In fact, the Commission has formed an advisory committee to assist that review.[2] In furtherance of that process, the following is intended to focus on certain issues that any serious review should consider—such as the various issues that have arisen from our markets’ increasingly fragmented structure, including market quality, and various market participants’ responses to the intensified competition for order flow.

In areas where there appears to be a compelling need for action—and where the benefits of a particular course of action are clear—there is a call for action. In areas where there may be a need for action, but where the best course is not readily apparent, recommendations will be made as to areas that require further study, including empirical research. Finally, in areas where there is no convincing evidence that change is warranted, or where it may appear that suggested reforms might even worsen matters, caution will be urged.[3]

II. Background

The United States’ equity markets present a paradox. Our markets are routinely lauded as being the most “liquid, transparent, efficient, and competitive . . . in the world.”[4] And, by many measures of market quality, this appears to be true. Quoted bid-ask spreads for the largest stocks remain pegged at the minimum level of one cent,[5] and overall spreads, including those for smaller stocks, are near historic lows.[6] Displayed market depth for the median stock has, according to one study, grown nearly 300% in the past eight years,[7] average daily trading volumes have returned to pre-financial crisis levels,[8] and intraday volatility is near its lowest levels in decades.[9] Competition has directly benefitted retail investors in a number of ways, including by making prices generally more efficient[10] and driving commission rates to historically low levels.[11] Institutional investors also appear to be faring well. One study estimates that average costs for block trade transactions have fallen by approximately 66% since 2001.[12] Another study shows that institutional trading costs for U.S. large cap stocks are among the lowest in the world, and that these costs have fallen more than 19% since 2010 alone.[13] And, while small cap stocks continue to face serious challenges,[14] there is some good news here, as well: displayed market depth for these securities has nearly doubled in the last ten years.[15] Taken together, these figures portray a vibrant equities market that is working well for many market participants.

At the same time, our equities markets have arguably never been subject to more strident and widespread criticism. Our markets have variously been described as “broken,”[16] a “complete mess,”[17] or, perhaps most alarming of all, “rigged.”[18] What is especially troubling about these criticisms is that they come not from uninformed outsiders, but from sophisticated industry participants. For example, Thomas Peterffy, one of the pioneers of electronic trading,[19] has said our markets are in a “crisis,” and that “order, fair dealing, and trust” need to be restored.[20] Charles Schwab, founder of the eponymal brokerage, has characterized high-frequency trading as “a growing cancer” that is “corrupting our capital market system by creating an unleveled [sic] playing field for individual investors and driving the wrong incentives for our commodity and equities exchanges.”[21] Even a former CEO of the New York Stock Exchange has remarked that “nobody rational would look at this [market] and say it isn’t broken.”[22] These opinions cannot be simply dismissed as the gripes of industry veterans who have found themselves on the wrong side of the transformational changes our markets have witnessed in recent years: a recent poll found that a majority of “financial industry participants” believe “markets are not fair for all participants.”[23]

One overarching aspect of our market structure that has been singled out for criticism by many market participants is its highly decentralized nature. Specifically, many market participants have claimed that, while Regulation NMS has enhanced competition, it has also fostered an overly “fragmented” market structure that raises trading costs[24] and renders our markets unduly fragile.[25] There are also claims that the large and rising proportion of trading that takes place away from exchanges—whether in so-called dark pools[26] or through the processes of preferencing[27] and internalization[28]—has reduced displayed liquidity, and greatly hampered the price discovery process.[29] Still others contend that incentives like the maker-taker pricing model[30] and payment for order flow arrangements[31] pose irreconcilable conflicts of interest for broker-dealers that deprive investors of their right to best execution.[32]

How can these competing narratives about the state of our equity markets be reconciled? There are no easy answers. But the intensity of the ongoing debate makes clear that it is well past time for an objective and dispassionate review of our equity market structure. This review must be fearless and searching. Too much is at stake for the Commission simply to accept the assumptions that underlie the status quo—or the justifications some have offered to defend it. For this review to be principled, however, it must be an informed one. To proceed in the absence of reliable data invites policy decisions to be made on the basis of the Commission’s authority rather than on the basis of evidence, which leaves the rulemaking process vulnerable to vested interests. In other words, whenever the Commission exercises its rulemaking powers, it must do so prudently and, whenever possible, with the benefit of accurate and comprehensive information.

Furthermore, any potential revisions to our market structure must be pursued in a careful and measured way. Past experience shows that even small changes can profoundly alter our equity markets in unforeseen ways.[33] That said, the Commission cannot delay action when there is an obvious need for it. To do so unacceptably jeopardizes the safety of investors and the orderly functioning of our equities markets.

III. A framework for Assessing the Quality of Our Equity Markets

Any thoughtful analysis of market structure must begin with a simple realization: no market structure is optimal for all market participants. A structure that is ideal for one group must, at least to some degree, leave others less well off than they could be.[34] As a result, today’s market structure embodies a series of trade-offs that elevate certain policy goals above others, and which benefit certain participants more than others.[35]

Given that trade-offs are an unavoidable consequence of any market structure, it is important to identify the policy goals that should be prioritized. Here is the appropriate hierarchy:

- First, there is no doubt whose interests should be paramount: those of investors and issuers who utilize the equity markets to meet underlying economic goals, rather than to profit from continual trading.[36] These investors and issuers are the very reason the equities markets exist,[37] and their interests should come first.

- The next priority should be to structure our equity markets to maximize the public benefits that derive from highly liquid markets, which produce the most accurate prices.[38] Deep, efficient, and liquid capital markets are the engine that drives our country’s economic growth,[39] and our policies should favor them whenever possible.

- The third priority should be to support the interests of the market participants that support our markets, such as registered dealers and market makers, because they are an indispensable part of an efficient and liquid market.[40] The interests of these market participants, however, are subject to an important limitation: they should be supported only to the extent that they further the first two policy goals listed above.[41] This approach follows from the Commission’s mission, which is to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.[42]

- Finally, the Commission’s policies should generally disfavor the interests of traders that seek to take unfair advantage of other traders.[43] For example, the Commission should consider the impact of algorithmic traders that rely on cutting edge technology to exploit fleeting price discrepancies that exist only for milliseconds. It has been argued that such trading merely raises trading costs for legitimate traders, and generally does not provide the benefits of arbitrage.[44] But, it should be recognized that a nuanced analysis is often required. As discussed below, there are some activities that may not appear to benefit ordinary investors, such as the maker-taker pricing model, that may in fact provide some benefits.[45]

In undertaking a review of our equity market structure, the Commission needs to consider the factors in the Securities and Exchange Act that establish the Commission’s mandate with respect to the national market system. Specifically, the Commission is to be guided by five objectives as it seeks to fashion rules to govern equity market structure. These objectives include: (i) economically efficient execution of securities transactions; (ii) fair competition among brokers and dealers, among exchange markets, and between exchange markets and markets other than exchange markets; (iii) the availability to brokers, dealers, and investors of information with respect to quotations and transactions in securities; (iv) the practicability of brokers executing investors’ orders in the best market; and (v) an opportunity, consistent with efficiency and best execution, for investors’ orders to be executed without the participation of a dealer.[46]

As the Commission has noted, however, these goals can be in tension at times, and “there clearly is room for reasonable disagreement as to whether the market structure at any particular time is, in fact, achieving an appropriate balance of these multiple objectives.”[47] To the extent that the objectives outlined in the Exchange Act come into conflict, the Commission should look to the priorities outlined above, as well as to the Commission’s overarching mission to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.[48]

IV. The Proliferation of Trading Venues

Our equity markets have witnessed a profound transformation in recent years. A structure that was dominated by a handful of exchanges just a few decades ago has given way to a far more decentralized system, in which trading activity is dispersed across 11 exchanges,[49] approximately 44 alternative trading systems,[50] and more than 200 broker-dealers that internalize their customers’ trades by executing them against their own inventory (“internalizers”).[51]

In many ways, this structure has been keenly influenced by a number of regulatory initiatives the Commission implemented over the past 20 years in an effort to encourage competition.[52] In pursuing these regulatory initiatives, particularly Regulation NMS (“Reg NMS”), the Commission sought to balance two “vital” but potentially conflicting forms of competition: competition among market centers and competition among individual orders. [53] The Commission attempted to navigate the tension between these goals by allowing trading centers to compete vigorously, while also mandating competition among orders through Regulation NMS’s order protection rule—also known as the trade-through rule. The order protection rule essentially requires all trading centers[54] to ensure that trades are executed at the best publicly quoted prices, even if it means routing an order to a competitor that is publicly displaying a superior price.[55] This rule weaves the various trading centers together into a unified marketplace, forcing them to compete for order flow.[56] It is thought that this competition has benefitted retail and institutional investors through lower trade costs, quicker executions, and better execution quality.[57]

But the burgeoning number of trading venues carries a number trade-offs, as well. First, the dilution of liquidity among multiple trading centers can impair market quality, in particular the price discovery process, which is one of the markets’ most critical functions. Second, multiple trading centers can give rise to added costs and complexity, and make our markets more susceptible to disruptions, whether technical or otherwise. Finally, multiple trading centers can lead to transparency issues for investors, who may struggle to identify the venues to which their orders were routed in an effort to secure the best price. Each of these issues is discussed below.

a. Market Quality and Price Discovery

The proliferation of trading venues can threaten the markets’ ability to price equities accurately in two discrete ways. First, when trading interest is spread across a multitude of lit venues,[58] traders may find it more difficult and expensive to locate liquidity and execute trades in a timely manner, particularly when larger trades are involved.[59] Second, approximately 35.85% of all trades are now executed by dark pools and internalizers.[60] As these two venues do not display their quotations to the public, a significant portion of the market’s trading interest is now shielded from the pre-trade price discovery process.[61]

A number of recent academic studies have sought to examine the possibility that market quality may suffer when liquidity is spread across a growing number of lit and dark trading venues.[62] These studies are subject to numerous limitations in terms of the quality and availability of data, and while their findings are far from uniform, they generally suggest that the advent of new exchanges and dark trading venues can lead to better price discovery, tighter spreads, lower transaction costs, and possibly even greater displayed depth.[63]

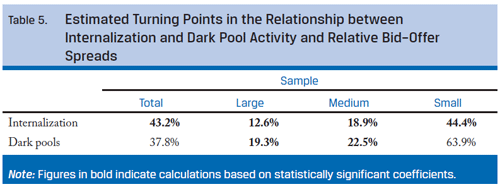

Yet, this appears to be true only up to a point. Several studies have found that there may be a threshold beyond which additional fragmentation and dark trading can impair price discovery and overall market quality, and that this threshold can vary depending upon a stock’s market capitalization.[64] One study even attempted to estimate the threshold beyond which additional dark trading could impair market quality. This study found that 46.7% could be the tipping point for all stocks, and, furthermore, that stocks at each level of market capitalization could have their own tipping points, depending upon the trading venue at issue.[65]

As noted above, today’s markets enjoy historically narrow spreads, low transaction costs, and increased displayed liquidity.[66] This suggests that the proliferation of lit exchanges and dark trading venues in recent years has not harmed investors, at least not to any measurable degree. In addition, while there may come a point when dark venues capture too much order flow, the evidence currently available to us suggests that we have not yet crossed that threshold.[67]

Nevertheless, this is an issue that deserves attention. The academic literature identifies very real and acute risks that could arise if trading activity continues to be dispersed across a growing web of trading centers. This requires that the Commission closely monitor the levels of dark trading in our markets and their potential consequences for market quality. This surveillance must be sufficiently granular to assess the effects of dark trading on stocks with different market capitalization levels, and across different venues, as studies suggest that different thresholds could apply to each.[68] This monitoring is essential so that the Commission will not be taken by surprise—we need to neutralize problems before they occur, not react to them.

Furthermore, while the market quality metrics described above suggest that markets are functioning well, the Commission cannot grow complacent. There is always room for improvement. The Commission must proactively explore ways to make our markets work still better for investors. To that end, the Commission should consider a number of steps to address the trend of increased dark trading.

- First, while the Commission has taken the important step of asking trading centers to clarify how their numerous order types operate in practice,[69] the Commission should also study how the use of non-displayed order types by exchanges may affect the price discovery process. These so-called “hidden” order types represent another form of dark liquidity that is not often discussed. One study has found that non-displayed order types are the most commonly used order types on exchanges,[70] and these order types may account for as much as 11% to 14% of exchange-based volume.[71] The Commission should study what effect this phenomenon may be having on the price discovery process and incentives for investors to post displayed limit orders.

- Second, the Commission should explore ways of exposing off-exchange trades to more competition. One possibility is to require trades negotiated in dark pools and with internalizers to be exposed to the exchanges for potential price improvement.[72] This would essentially set up an auction process that would directly benefit investors, and could potentially enhance displayed liquidity.

- Third, the Commission should dust off the Regulation of Non-Public Trading Interest proposal issued in 2009,[73] and examine whether price discovery could also be enhanced by enacting the provisions proposed in that release. These provisions include: (i) requiring ATSs to publicly display smaller-sized actionable indications of interest,[74] (ii) reducing the 5% volume threshold for ATSs to publicly display their best-priced orders,[75] and (iii) requiring ATSs to disclose their identities when they report executed trades to the consolidated tape, with an appropriate exception or delay for block trades.[76] These actions have already been subject to public notice and comment, and the Commission could proceed to adoption right away, subject to such improvements as may be warranted by the comments and data received.

b. Complexity and Fragility

It has been noted that, to comply with the order protection rule of Reg NMS,[77] trading venues and broker-dealers have developed elaborate IT systems to monitor the prices of all NMS stocks[78] on all lit exchanges, and to route orders accordingly.[79] These entities claim that this tangle of data connections adds needless complexity and cost,[80] and makes our markets overly fragile.[81] They also contend that the order protection rule props up exchanges that are otherwise not economically viable by giving them a share of market data revenues.[82] Furthermore, at least one market participant has contended that the requirement to interact with smaller exchanges exposes broker-dealers to toxic order flows in a way that leads them to violate their best execution obligations.[83] A number of exchanges and broker-dealers have accordingly called for the Commission to revise the order protection rule to limit its reach to exchanges that meet a certain market share threshold, such as 1 percent.[84]

The order protection rule has proven to be a vital investor protection, and it should not be weakened lightly. Indeed, the continuing importance of the order protection rule has been underscored by recent enforcement actions. For example, the Financial Industry Regulatory Authority (FINRA) fined one dark pool operator last year for violations of the rule,[85] and just two years ago three exchanges admitted they had failed to obtain the best available price for their customers.[86]

Moreover, it appears that only two exchanges, the Chicago Stock Exchange and NYSE’s MKT exchange, currently fall below the suggested 1 percent threshold.[87] Thus, it would seem that the cost savings from excluding these two exchanges from the order protection rule would likely be negligible. Furthermore, with Regulation Systems Compliance and Integrity (Regulation “SCI”)[88] becoming effective next year, concerns about market fragility should abate.

More importantly, the suggested 1 percent threshold could needlessly stifle competition and innovation. The order protection rule appears to have encouraged innovation by helping fledgling exchanges overcome significant barriers to entry. For example, to address the problem of shrinking order sizes,[89] Nasdaq’s PSX exchange has implemented a novel approach of replacing the traditional price-time priority scheme with a price-size priority scheme.[90] Similarly, IEX has developed innovations that may help attract more liquidity to lit venues, and that may nullify the speed advantages enjoyed by high frequency traders.[91] The initial response to these innovations appears to be positive. Nasdaq, which had a market share of only half a percent just one year ago, has now achieved a full 1 percent market share.[92] Similarly, IEX, which reportedly had only half a percent of market share just a year ago,[93] now claims to have approximately 1.134% of the market,[94] and is attempting to register as an exchange.[95] Furthermore, the claim that the order protection rule sustains unprofitable exchanges appears to be undermined by recent events. For example, last year, the National Stock Exchange and the CBOE Stock Exchange—two exchanges that failed to achieve a 1 percent of market share—were both shuttered.[96] Apparently, the order protection rule did not sustain them.

Nevertheless, if market forces fail to address the situation of an exchange that has failed to reach a reasonable market share over an extended period, market participants have other avenues through which they can seek relief. Specifically, if market participants can demonstrate that linking to a small exchange poses unnecessary costs, and makes the national market system measurably less stable, then market participants could petition the Commission for limited exemptive relief from the order protection rule on the ground that such an exemption is in the public interest.[97]

c. Transparency

Finally, the growth in trading venues has created transparency issues, as investors generally do not know which of the multitude of exchanges, ATSs, and internalizers their orders are routed to in an effort to obtain the best price.[98] This hampers both retail and institutional investors’ ability to monitor the quality of their trade executions. Anecdotal evidence suggests that this is not an idle concern. A study by one buy-side firm found that a small purchase order for just 1,000 shares was sent to 18 different exchanges and dark pools before it was entirely filled.[99] Another firm was shocked to learn that its order to purchase 2.5 million shares of a highly liquid stock led its broker to place and cancel bids for a total of 750 million shares across a number of venues, all in an effort to conceal the order from high frequency traders.[100]

To address these issues, there is general agreement that investors need better information about order execution quality and routing practices.[101] The information that investors receive pursuant to Rules 605 and 606 of Regulation NMS is designed to support competition by enhancing the transparency of order execution and routing practices.[102] Yet, these rules have badly lagged technological advances, and are in need of modernization. Just last summer, Chair White asked the staff to prepare a recommendation for the Commission on this issue,[103] and these changes should be pursued as quickly as possible.

The required updates are too numerous and detailed to list here, but key changes include the following: (i) adding new order types to the disclosure requirement, including dark and reserve orders; (ii) capturing the entire life cycle of an order, such as all routers and venues through which an order passes prior to execution, including all routers and venues owned by the same entity; (iii) recalibrating the parameters for measuring the speed of execution; (iv) adding odd lot orders; (v) including information for the market open; (vi) including statistics regarding the average time cancelled orders were displayed, as well as the overall number of cancellations for intermarket sweep orders, immediate-or-cancel orders, and indications of interest; and (vii) the inclusion of the options markets.[104] Other important revisions that are needed to these disclosures are discussed elsewhere in this statement.

V. Competition for Order Flow

As noted above, one of the principal goals of Reg NMS was to foster competition among trading venues.[105] One consequence of this intensified competition is that trading centers have developed various strategies to attract order flow. For example, exchanges have widely adopted the so-called maker-taker pricing model (“maker-taker”), in which they impose a fee on traders that remove, or take, liquidity from the exchange by crossing the spread; the exchanges then use a portion of that fee to pay a rebate to traders who furnish liquidity.[106] Similarly, internalizers attract order flow by purchasing the orders retail brokers receive from their customers, a practice known as “payment for order flow.”[107] The fierce competition among trading centers for order flow has manifested itself in other ways, as well, such as through the development of exotic order types that cater to certain trading strategies, particularly those used by high frequency traders.[108]

Critics have argued that the competition for order flow has introduced conflicts of interest that give brokers a strong incentive to route customer orders in ways that place brokers’ financial interests ahead of those of their customers.[109] Advocates, by contrast, have argued that payments for order flow keep retail customers’ commissions low, and that retail customers’ orders receive better execution than if they were routed directly to an exchange.[110] Although there are often many sides to any discussion, the Commission’s role is to subject the parties’ competing claims to an objective and rigorous review.

a. The Maker-Taker Payment Model

No issue in the market structure debate has proven more polarizing than the maker-taker pricing model—with the possible exception of high frequency trading. Critics decry the maker-taker model for engendering all manner of evils. For example, some claim that it has “distorted order routing decisions, aggravated agency problems among brokers and their clients, unleveled the playing field among dealers and exchange trading systems, produced fraudulent trades, and produced quoted spreads that do not represent actual trading costs.”[111] Critics of the maker-taker model include Jeffrey Sprecher, Chairman and CEO of the Intercontinental Exchange (ICE) and the Chairman of the NYSE, who has said that the maker-taker pricing model should not be “legal” because it “puts wrong incentives in the market.”[112] Sprecher’s critique carries significant weight because it subverts his company’s own financial interests—in fact, it has been reported that fully 6% of ICE’s revenues come from maker-taker fees.[113] Moreover, even one of the individuals responsible for developing the maker-taker pricing model has suggested that it is no longer relevant in today’s highly automated markets.[114]

Defenders of the model,[115] however, contend that the maker-taker pricing model facilitates competition,[116] “provides advantages to both sides” of a trade, and has helped reduce the “frictional costs of trading to their lowest levels in history.”[117] Their argument is that maker-taker fees encourage liquidity on exchanges and narrow bid-ask spreads by compensating liquidity providers for the risks associated with posting limit orders, including the risk of adverse selection.[118]

What follows is a brief summation of the competing viewpoints on the key issues, followed by suggestions for a path forward.

i. Liquidity

Some commenters believe that the high access fees exchanges must charge in order to pay maker-taker rebates have diverted marketable orders[119] away from the exchanges, reducing market quality and impairing the price discovery process. Specifically, these commenters have observed that, when possible, brokers will either internalize their customers’ marketable orders or sell them to over-the-counter (“OTC”) market makers, in order to avoid paying the access fees that exchanges must charge in order to pay the maker-taker rebates.[120] These same commenters have further observed that “many” brokers will first route marketable limit orders to dark pools, which charge lower transaction fees.[121]

Yet, recent events appear to have confirmed the critical role that the maker-taker model plays in attracting liquidity to exchanges. On February 2, 2015, Nasdaq instituted a pilot program in which it reduced access fees and rebates for 14 highly liquid stocks, including both NYSE- and Nasdaq-listed stocks.[122] The stated purpose of this program was “to attract more investor orders to the public markets” by “respon[ding] to claims that public markets are too expensive.”[123] Nevertheless, the program does not appear to have achieved the intended result. Instead, it has been reported that this program has led Nasdaq to lose substantial market share, with no measurable improvement in market quality.[124] Clearly, any proposed modifications to the maker-taker pricing model will require careful thought.

ii. Conflicts of Interest

One study (the “Battalio Study”) appears to confirm that the maker-taker model has led some brokers to place their financial interests ahead of their clients’ interests. The Battalio Study found that four “well-known national brokerages” almost consistently routed their non-retail clients’ standing limit orders to the exchanges that paid the highest maker-taker rebate.[125] The study concluded that this practice is “inconsistent with maximizing limit order execution quality” because limit orders sent to exchanges with lower maker-taker fees were executed faster and more frequently.[126]

The Battalio Study, however, was apparently based exclusively on data from “a major investment bank,” and thus did not directly examine orders placed by retail investors.[127] The President and CEO of one of the brokers cited in the Battalio Study has said that the “institutional, proprietary algorithmic trading” that formed the basis of the Battalio Study is “very different” from retail orders.[128] The President and CEO also said his firm did its own analysis of the non-marketable limit orders placed by its retail investors.[129] Specifically, this analysis examined the non-marketable limit orders that were routed to the exchange that paid the highest rebates. According to the President and CEO, this analysis showed that “approximately 93% of [retail customers’ non-marketable limit] orders were executed . . . provided there was a trade on any exchange at the limit price.”[130] This suggests that the conflicts of interest identified by the Battalio Study may not arise in connection with retail investors’ orders.

iii. Spreads

Commenters have also argued that the maker-taker pricing model appears to have distorted markets by artificially narrowing quoted spreads.[131] This distortion appears to occur because the quoted spreads do not reflect the fees paid by takers of liquidity or the rebates received by providers of liquidity. Thus, if the quoted spread on a stock is one cent, the true spread, assuming the take fee is 0.3 cents (the maximum permitted under Rule 610), is 1.6 cents, or 60% higher than the quoted spread.[132] In the absence of the maker-taker pricing model, then, quoted spreads on some stocks would likely rise to reflect the true degree of risk traders incur when they post liquidity.[133]

To date, it does not appear that any empirical study of this issue has been conducted. Nasdaq’s pilot program, however, suggests that the maker-taker pricing model’s impact on spreads could be minimal, at least with respect to certain stocks. Initial results from Nasdaq’s pilot program suggest that spreads on the affected stocks have generally remained unchanged.[134] The apparent absence of an effect on spreads, however, must be viewed with caution. Only highly liquid stocks were selected for the Nasdaq pilot program, and it is possible that the competitive environment for these stocks, combined with the continued availability of rebates on other exchanges, kept spreads tight despite the reduction in access fees.

iv. Other Factors to Consider

Certain additional factors complicate the analysis of the maker-taker model. First, what has gone largely unnoticed in the broader debate is that the maker-taker model may represent an implicit subsidy for retail investors. According to various observers, the reason for this is that virtually none of the marketable orders placed by retail investors ever reach an exchange; instead, these orders are internalized by their broker or sold to an OTC market maker that executes the orders against its own inventory.[135] Internalizers and OTC market makers typically execute these marketable retail customer orders at the spread quoted on the exchange, not the true spread.[136] Under the current maker-taker regime, therefore, it appears that retail investors are generally not required to pay the access fee that exchanges charge. If the maker-taker model were abolished, however, quoted spreads on at least some stocks could widen to accurately reflect the risks undertaken by liquidity providers, which could potentially harm retail investors.[137]

In addition, one possible explanation for the proliferation of exchanges in recent years is that it has allowed exchanges to offer different maker-taker pricing schemes.[138] For example, NYSE and Nasdaq each operate three separate equities exchanges, while BATS operates four.[139] Each of these exchanges offers unique fee and rebate schedules.[140] Consequently, reducing or eliminating the maker-taker pricing model could potentially affect the prevailing dynamic, either by mitigating incentives to create new exchanges, or by alleviating some of the competitive pressures that have encouraged the proliferation of trading centers in our equities markets.

v. A Path Forward

Concerns about the maker-taker pricing model have led some to call for the Commission to ban it altogether.[141] The factors listed above, however, argue for a careful and nuanced approach to this issue, one that takes into account the possibility of unintended consequences, and one that is firmly rooted in an evidence-based review. And while the three principal exchange groups have all proposed eliminating or reducing maker-taker rebates,[142] Nasdaq’s recent experience may suggest that the maker-taker model presents a prisoner’s dilemma,[143] where each exchange’s decision to act in its own best interests leads to an outcome that leaves all exchanges worse off than if they had cooperated.[144] Such situations could be resolved through appropriate regulatory action.

One option for the Commission to consider, as recommended by certain market participants and as proposed in a recent House bill,[145] is a carefully constructed pilot program.[146] This pilot program should apply a tiered approach, as was suggested by BATS earlier this year.[147] Under this approach, maker-taker fees could be eliminated entirely for the most liquid stocks, as public trading in these stocks appears to be sufficiently robust that rebates are not required to attract liquidity to exchanges. And, as the results of the Nasdaq pilot appear to confirm, rebates do not seem necessary in order to maintain spreads on these stocks at their current levels. The proposed pilot’s impact on retail investors whose orders are internalized should therefore be muted. The rebates could remain in place for less liquid securities, and could be tiered so that they rise as a given stock’s liquidity falls. The reductions in the rebates should be accompanied by a reduction in the access fee cap imposed by Rule 610 of Regulation NMS.[148] The reduction of the cap should help ease the intense competitive pressures exchanges face in today’s markets.

Nasdaq’s experience earlier this year might suggest that any maker-taker pilot program should include a trade-at rule. A trade-at rule would presumably help prevent liquidity from migrating away from exchanges by forcing brokers and dark pools to route trades to public exchanges, unless they can execute the trades at a price that is meaningfully better than the ones available on an exchange.[149] But here’s the rub: this presumption may not prove correct. According to preliminary data, Nasdaq did not lose market share to dark pools. Instead, it lost market share to other exchanges that were still paying full rebates.[150] This suggests that the liquidity providers who fled Nasdaq were those who place a substantial premium on receiving maker-taker rebates.[151] Therefore, if all exchanges are forced to eliminate or reduce rebates, it does not necessarily follow that liquidity providers will migrate to dark venues.[152] But since such a migration is at least a possibility, the pilot program proposed above should take this into account.

Given the uncertainty as to the potential impact of eliminating or reducing maker-taker fees, the proposed pilot program should have two phases. The first phase would eliminate or reduce rebates, with a corresponding reduction of the access fee cap. At that stage, the pilot would not include a trade-at requirement. At the end of the first phase, the Commission would evaluate whether the exchanges lost market share and, if so, to which venues. In the second phase of the program, the Commission could reevaluate the level of the access fee cap, and, if appropriate, include a trade-at restriction to encourage the posting of liquidity on exchanges. Importantly, the Commission should consider proceeding with the second phase of the program regardless of the results of the first. It is advisable to test whether a general trade-at provision would improve market quality, particularly given that at least one study has concluded that “investors [are] paying $3,890,624 more per stock per year due to internalization,” and that a trade-at rule could have a “measureable” impact on bid-ask spreads.[153] Moreover, a pilot program would help to identify any unintended consequences a trade-at provision could create.[154]

In fact, recent experience suggests that trade-at rules can have unexpected effects. For example, both Canada and Australia recently implemented robust trade-at rules that failed to increase the amount of liquidity posted on their exchanges. Worse yet, the imposition of a trade-at rule in both countries was followed by a widening of both quoted and effective spreads.[155] Various justifications for these somewhat counterintuitive results have been offered, including certain aspects of each nation’s regulatory and market environments.[156] Another possible explanation is that minimum tick size requirements in those countries prevented their exchanges from matching dark venues’ ability to offer mid-point price improvements.[157] According to Commission staff, yet another possible explanation for the unexpected results in Canada and Australia is that these jurisdictions did not allow exchanges to reduce their access fees in connection with the trade-at rule, which may have dissuaded liquidity providers from posting limit orders on the lit exchanges. In developing any pilot programs, the Commission would need to carefully weigh these issues, among others.[158]

In addition, the Commission should use the pilot program to assess the validity of claims that a trade-at rule could harm both institutional and retail investors.[159] For example, some believe that a trade-at rule would hurt institutional investors by limiting their ability to access liquidity in dark venues.[160] As for retail investors, some commenters have asserted that a trade-at rule could deprive them of the price improvement and low commissions they currently enjoy when their trades are internalized or sold to OTC market makers.[161] Indeed, there is some evidence suggesting that this is correct. It has been reported that retail investors in Canada saw their average price improvement fall by 70% following implementation of the trade-at rule.[162] Furthermore, commentators have noted that a trade-at rule could harm retail investors by forcing them to trade on exchanges, where they might be taken advantage of by more informed professional traders, such as high frequency traders.[163] The proposed pilot program would offer an opportunity to test these concerns.

Nonetheless, since maker-taker rebates remain very much a part of the current market structure, the Commission must promptly take steps to address the conflict-of-interest issues that these rebates create. One step the Commission needs to pursue immediately, together with FINRA, is to provide additional guidance on brokers’ best execution obligations as they relate to maker-taker rebates and routing decisions. Some have argued that existing guidance on best execution is out of date, and has not kept pace with changes in market structure and automated trading.[164]

Furthermore, the Commission should move promptly to revise the order routing rule, Rule 606, to require brokers to provide additional information that will help investors gauge the quality of the executions they receive. For example, in addition to the updates discussed in Section IV.c above, Rule 606 could also be revised to require firms to disclose within their 606 reports information from their 605 reports concerning the overall quality of execution delivered by executing market centers.[165] Additionally, Rule 606 should split the reporting of routed and executed orders into categories that facilitate a statistical comparison of execution quality and fee disclosure metrics.[166] Such disclosures would be helpful, and these changes do not need to wait for a pilot program.

Additionally, the Commission should create a page on its website where investors could access all brokers’ Rule 606 reports in one place, so they could make apples-to-apples comparisons regarding brokers’ execution quality.[167]

Finally, to address the claim that retail customers’ limit orders are not susceptible to the types of conflicts of interest that were identified in the Battalio Study, the Commission should consider making a formal information request to brokers for any data and analyses that would substantiate—or refute—this claim. This will enable the Commission to better assess the quality of execution that brokers are delivering for retail investors’ limit orders.

b. Payments for Order Flow

Payments for order flow implicate the same conflict-of-interest and market quality issues raised by market fragmentation and the maker-taker pricing model, and the measures outlined above should serve to illuminate the effects of this practice, as well. Yet, the payment for order flow regime presents additional concerns that also need to be specifically examined.

For instance, some detractors have expressed concerns that the conflict-of-interest issue is particularly acute in the payment for order flow context because of the sheer amount of money at stake for some brokers.[168] In addition, some commenters have expressed concern that retail investors would fare better if their orders were executed on exchanges, rather than by the OTC market makers that purchase their orders and provide a small degree of price improvement.[169] These commenters believe that payments for order flow may lead to higher costs and wider spreads.[170] Finally, the Commission’s report on the May 6, 2010 flash crash noted that the payment for order flow regime exacerbated market instability that day when the OTC market makers that typically purchase and internalize the vast majority of retail investors’ trades suddenly reversed this practice, and flooded the exchanges with a massive influx of sell orders.[171]

Some experts, however, believe that the payment for order flow regime has benefitted retail investors. Robust competition, they claim, has forced brokers to pass along to their customers most of the benefits of these payments.[172] This may well be true, and it is certainly possible that retail investors’ situation would not measurably improve if the status quo were altered. But in light of the controversy surrounding this issue, the Commission should look into whether customers could be made better off.

For example, what would happen if brokers were forced to pass all payments for order flow along to their customers? This would eliminate the existing conflicts of interest, which should go a long way to rebuilding trust in market intermediaries. And although brokers could potentially raise commission rates as a result, retail investors would, in theory, be compensated for this loss by receiving the payments for order flow their orders generate. Although it is possible that this approach would also lead brokers to charge for additional services, such as online investment tools, this could be a far more efficient result, as it would allocate the costs of these services to the customers that actually use them, rather than compelling all customers to bear these costs. This would certainly be a more transparent approach, and the value of transparency cannot be overstated.

In addition, the justifications that underpin the payment for order flow regime should be put to the test. For instance, brokers claim that retail customers benefit from the price improvement they receive when their orders are sold to OTC market makers.[173] But there is evidence suggesting that retail investors could do better. For example, one broker that sends approximately 95% of its customers’ orders to exchanges claims that, for the past 8 years, it has consistently provided better price improvement than firms that sell their customers’ orders to OTC market makers.[174] Although the level of this price improvement varied, an independent assessment[175] reveals that it has been as high as 53 cents per 100 shares, and has been at least 30 cents per 100 shares two-thirds of the time.[176]

These facts demand that the Commission study the economic consequences of payments for order flow more closely. In addition, this information suggests that the Commission needs to carefully evaluate the consequences of trade-at rules that may form part of any pilot programs in the near future. For instance, just last week, the Commission approved the tick size pilot program, which includes a limited trade-at rule.[177] The Commission should carefully study the effects of that program to determine what lessons, if any, can be gleaned about the consequences of the payment for order flow regime.

The need for future studies, however, should not be a reason for delay. It is clear that, in the near term, the Commission needs to take prompt steps to ensure that payments for order flow do not impair brokers’ ability to deliver best execution. Of course, this is currently difficult as brokers presently do not provide sufficient disclosure about payments for order flow. This should not be acceptable.

Rule 606 should promptly be revised to require brokers to disclose to customers the total amount of payments for order flow the broker receives, as well as the average amount of price improvement customers receive on orders sold to OTC market makers. The rule should also be revised to require brokers to disclose the total execution costs of their clients’ trades, so investors can see how payments for order flow and other factors affect their trading costs. For example, brokers should report not only direct costs, such as commissions and fees paid, but also all benefits that may have reduced those costs, such as price improvement, liquidity rebates, and payments for order flow.[178]

In addition, the Commission should monitor the experience of other jurisdictions, such as the United Kingdom, that have prohibited payments for order flow entirely.[179] In particular, the Commission should determine whether the pervasive deficiencies that led the UK’s Financial Conduct Authority (FCA) to ban these payments outright also exist in this country.[180] Further, the Commission should work with the FCA to monitor how brokers respond to the ban. For example, the ban is an opportunity to test brokers’ claims that payments for order flow are vital to keeping retail customers’ commissions low. The ban also offers an opportunity to determine whether, as some have claimed, market participants will react to the ban by merely seeking alternative ways of providing compensation to those who send them business.

Finally, the Commission needs to evaluate the role that the payment for order flow regime could play in making markets less stable, particularly in times of market stress. The Commission should consider the benefits of a rule recommended by the “Flash Crash” committee that would require internalizers and OTC market makers to be subject to market maker obligations that require them to execute some material portion of their order flow internally during periods of extreme market volatility.[181]

None of this is to say with certainty that the payment for order flow regime could or should be abolished. For example, one study indicated that the execution quality delivered by OTC market makers hit an “all-time high” in the final quarter of 2014, suggesting that retail investors are faring well, or at least better than in the past.[182] In fact, some experts believe that banning payments for order flow could magnify conflicts of interest, and could create even more difficult challenges, as market participants might respond by finding more opaque ways to pay for order flow.[183]

In light of the serious concerns discussed above, however, it is important for the Commission to examine the payment for order flow regime carefully. Knowledge is always better than speculation.

VI. Conclusion

No one can question that our equity markets have undergone a period of transformational change in recent years, and that the structure that has emerged is far more complex and diverse than in the past. There are many indications that this new structure has yielded measurable benefits for investors, both large and small. Yet, it has also come at a price, in the form of palpable conflicts of interest, and an intensely competitive environment that has led, at least in some instances, to less than ideal outcomes for certain market participants.

The Commission must work proactively to ensure that our markets are fair and orderly, and that investor protections keep pace with a rapidly evolving marketplace. Hopefully, the concepts, suggestions, and proposals outlined above can help move the process forward.

The issues that exist are very complex and I make no claim to having identified any ideal solutions. My hope has been to provide an informed perspective on issues that the Commission must address. Obviously, there are more areas that need examination, including the possibility of excessive intermediation in our markets, the reasons institutional investors’ trading costs have failed to see any meaningful improvement in the last 13 years,[184] possible avenues to incentivize market makers to provide liquidity during periods of market volatility, the propriety of the fees that exchanges charge for data and ancillary services and, of course, an in-depth study of the practices employed by high-frequency traders and the quality of the liquidity they provide.

[1] The views I express are my own, and do not necessarily reflect the views of the U.S. Securities and Exchange Commission (the “SEC” or “Commission”), my fellow Commissioners, or members of the staff.

[2] Securities Exchange Act Release No. 74092, Equity Market Structure Advisory Committee (Jan. 20, 2015), available at https://www.sec.gov/rules/other/2015/34-74092.pdf.

[3] This analytical framework follows that employed by Professors Fox, Glosten, and Rauterberg in their recent article. See Merritt B. Fox, Lawrence R. Glosten, and Gabriel V. Rauterberg, The New Stock Market: Sense and Nonsense, 3 (Mar. 17, 2015), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2580002.

[4] Testimony of Joe Ratterman, CEO, BATS Global Markets, Inc., before the U.S. Senate Banking Committee (July 8, 2014), available at http://www.banking.senate.gov/public/index.cfm?FuseAction=Files.View&FileStore_id=e629a146-0ee1-4ebc-940b-b3289ef77118.

[5] James J. Angel, Lawrence E. Harris, and Chester S. Spatt, Equity Trading in the 21st Century: An Update, 5 (June 21, 2013), available at http://www.q-group.org/wp-content/uploads/2014/01/Equity-Trading-in-the-21st-Century-An-Update-FINAL1.pdf; US Securities and Exchange Commission Market Structure Website, Data, Spreads and Depth by Individual Security, Spreads by Individual Security, 2013 (noting that, for 2013, the bid-ask spread for the most liquid 126 stocks was 1 cent), available at http://www.sec.gov/data/market-structure/spreads-and-depth-by-individual-security.html.

[6] Id.; see also Peter Haslag and Matthew C. Ringgenberg, The Causal Impact of Market Fragmentation on Liquidity, 11, 29 (Apr. 6, 2015) (utilizing a data set that represents “the true cross-sectional average of tradeable [sic] securities in the U.S. marketplace” to show that “bid-ask spreads have generally decreased” since 2004, and are near their lowest levels since that time)(working paper), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2591715.

[7] James J. Angel, Lawrence E. Harris, and Chester S. Spatt, Equity Trading in the 21st Century: An Update, 8 (June 21, 2013), available at http://www.q-group.org/wp-content/uploads/2014/01/Equity-Trading-in-the-21st-Century-An-Update-FINAL1.pdf.

[8] Id. at 4; see also Larry Tabb, CEO, TABB Group, Written Testimony to the United States Senate Committee on Banking, Housing, and Urban Affairs, 5 (Sept. 20, 2012), available at http://www.banking.senate.gov/public/index.cfm?FuseAction=Files.View&FileStore_id=268afb1b-4c5e-4ec0-8028-fc840b973843. These statistics should not be read to suggest that our equity markets do not face challenges. For example, some analyses demonstrate a downward trend in average trade volume since the financial crisis. A number of explanations for this phenomenon have been offered, including a decline in high frequency trading, a decline in investment banks’ proprietary trading, and a general shift by investors to passive index funds, options, and futures. See Victor Reklaitis and Anora Mahmudova, Why trading volume is tumbling, explained in 5 charts, MarketWatch (July 7, 2014), available at http://www.marketwatch.com/story/why-trading-volume-is-tumbling-explained-in-5-charts-2014-07-07.

[9] Id. at 12; Ed Easterling, Volatility in Perspective, Crestmont Research, 2 (Jan. 6, 2015)(noting that the S&P 500’s rolling volatility is currently at 8%, and that “volatility tends to average near 15%”), available at http://www.crestmontresearch.com/docs/Stock-Volatility-Perspective.pdf; see also Peter Haslag and Matthew C. Ringgenberg, The Causal Impact of Market Fragmentation on Liquidity, 11, 29 (Apr. 6, 2015) (covering only the period from 2004 until January 1, 2013, but confirming that volatility is near its lowest levels during that period) (working paper), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2591715.

[10] Peter Haslag and Matthew C. Ringgenberg, The Causal Impact of Market Fragmentation on Liquidity, 11, 29 (Apr. 6, 2015) (utilizing a data set that represents “the true cross-sectional average of tradeable securities in the U.S. marketplace” to show that “bid-ask spreads have generally decreased” since 2004, and are near their lowest levels since that time)(working paper), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2591715.

[11] James J. Angel, Lawrence E. Harris, and Chester S. Spatt, Equity Trading in the 21st Century: An Update, 14 (June 21, 2013), available at http://www.q-group.org/wp-content/uploads/2014/01/Equity-Trading-in-the-21st-Century-An-Update-FINAL1.pdf; Barron’s Online Broker Survey 2015: How they Stack Up, Barron’s (Mar. 9, 2015)(listing the top 10 online brokers and noting that none of them charges more than $9.99 for online stock trades, and that all but two charge less), available at http://online.barrons.com/articles/SB51367578116875004693704580500193983582362; see also, e.g., TD Ameritrade, Pricing (May 6, 2015) (offering “$9.99 Flat-rate online equity trades), available at https://www.tdameritrade.com/pricing.page; E*Trade, Commissions & Fees (May 6, 2015) (offering $9.99 flat-rate commissions for up to 149 online stock and options trades per quarter), available at https://us.etrade.com/e/t/estation/pricing?id=1206010000; Charles Schwab, Fees and Minimums (May 6, 2015) (offering a flat $8.95 rate for online stock and ETF trades), available at http://www.schwab.com/public/schwab/investing/pricing_services/fees_minimums.

[12] Id. at 23-24.

[13] Investment Technology Group’s Global Cost Review Q3/2014, 8 (reporting total costs of trading U.S. large cap stocks as 32.9 basis points) (Jan. 14, 2015), available at http://www.itg.com/marketing/ITG_GlobalCostReview_Q3_2014_20150205.pdf; Investment Technology Group’s Global Cost Review 2010/Q2, 6 (reporting total costs of trading U.S. large cap stocks as 40.8 basis points (Oct. 27, 2010), available at http://www.itg.com/wp-content/uploads/2009/12/ITGGlobalCostReview_2010Q2_Final.pdf.

[14] Charles Collver, A characterization of market quality for small capitalization US equities, U.S. Securities and Exchange Commission, 1 (2014) (noting that “[s]mall cap stocks had larger quoted and effective spreads and traded much lower volumes than mid cap stocks. They also showed lower depth at the inside quotes and beyond.”), available at http://www.sec.gov/marketstructure/research/small_cap_liquidity.pdf; Larry Tabb, CEO, TABB Group, Written Testimony to the United States Senate Committee on Banking, Housing, and Urban Affairs, 5 (Sept. 20, 2012), available at http://www.banking.senate.gov/public/index.cfm?FuseAction=Files.View&FileStore_id=268afb1b-4c5e-4ec0-8028-fc840b973843.

[15] James J. Angel, Lawrence E. Harris, and Chester S. Spatt, Equity Trading in the 21st Century: An Update, 9 (June 21, 2013), available at http://www.q-group.org/wp-content/uploads/2014/01/Equity-Trading-in-the-21st-Century-An-Update-FINAL1.pdf.

[16] Sal Arnuk and Joseph Saluzzi, Broken Markets: How High Frequency Trading and Predatory Practices on Wall Street Are Destroying Investor Confidence and Your Portfolio, 219 (2012).

[17] Thomas Peterffy, Chairman and CEO of Interactive Brokers Group, Comments Before the 2010 General Assembly of the World Federation of Exchanges, 1 (Oct. 11, 2010), available at https://www.interactivebrokers.com/download/worldFederationOfExchanges.pdf.

[18] Michael Lewis, Flash Boys, 40 (2014); see also Max Ehrenfreund, A veteran programmer explains how the stock market became “rigged,” The Washington Post (Apr. 4, 2014)(quoting Eric Scott Hunsader, founder of Nanex, as saying “[s]o when Michael Lewis used the word ‘rigged,’ he’s right. [The stock market is] rigged . . . .”), available at http://www.washingtonpost.com/blogs/wonkblog/wp/2014/04/04/a-veteran-programmer-explains-how-the-stock-market-became-rigged/.

[19] Abram Brown, Billionaire Thomas Peterffy Practically Invented Digital Trading. Now He Wants To Be Your Broker, Forbes (Nov. 5, 2014), available at http://www.forbes.com/sites/abrambrown/2014/11/05/billionaire-thomas-peterffy-practically-invented-digital-trading-now-he-wants-to-be-your-broker/.

[20] Thomas Peterffy, Chairman and CEO of Interactive Brokers Group, Comments Before the 2010 General Assembly of the World Federation of Exchanges, 2 (Oct. 11, 2010), available at https://www.interactivebrokers.com/download/worldFederationOfExchanges.pdf.

[21] Charles Schwab and Walt Bettinger, Schwab Statement on High-Frequency Trading (Apr. 3, 2014), available at http://pressroom.aboutschwab.com/press-release/corporate-and-financial-news/schwab-statement-high-frequency-trading; but see Kathleen Pender, Charles Schwab CEO clarifies high-frequency trading remarks, San Francisco Chronicle (Apr. 25, 2014) (noting that Walt Bettinger, CEO of Charles Schwab, later said that "intelligent people can make sound arguments on either side of the issues around high-frequency trading."), available at http://www.sfchronicle.com/business/networth/article/Charles-Schwab-CEO-clarifies-high-frequency-5430935.php.

[22] Deal Journal, NYSE CEO: Knight Capital Another Reason for Reform (Aug. 3, 2012)(speaking in the wake of the Knight Capital debacle), available at http://blogs.wsj.com/deals/2012/08/03/nyse-ceo-knight-capital-another-reason-for-reform/.

[23] Eric Noll, U.S. Equity Market Structure “Flashback” Survey Results (Mar. 26, 2015), available at http://convergex.tumblr.com/post/114674985559/u-s-equity-market-structure-flashback-survey.

[24] BlackRock, US Equity Market Structure: An Investor Perspective, 2 (Apr. 2014) (noting that, “while investors have benefitted from [rules like Reg NMS], it is also important to recognize that these regulations have fostered a complex and highly fragmented market where trade order flow must navigate 13 exchanges, 40+ dark pools, and a handful of Electronic Communication Networks (ECNs). . . . , [t]he ability to place orders in all venues comes at a cost . . . .”), available at https://www.blackrock.com/corporate/en-us/literature/whitepaper/viewpoint-us-equity-market-structure-april-2014.pdf.

[25] Nina Mehta, Fragmentation of U.S. Equities Market Criticized in SEC Panels, BloombergBusiness (June 23, 2010)(quoting Matt Schrecengost, chief operating officer at Jump Trading LLC, a proprietary trading firm in Chicago, as saying “[t]he U.S. equities market is so complex normally that when you add in a situation like [the May 6 flash crash] the complexity turns into confusion”), available at http://www.bloomberg.com/news/articles/2010-06-23/fragmentation-of-u-s-stock-market-criticized-at-sec-panels-in-washington.

[26] “The term ‘dark pools’ generally refers to electronic stock trading platforms in which pre-trade bids and offers are not published and price information about the trade is only made public after the trade has been executed.” Gary Shorter and Rena S. Miller, Dark Pools in Equity Trading: Policy Concerns and Recent Developments, i (Sept. 26, 2014), available at http://www.fas.org/sgp/crs/misc/R43739.pdf.

[27] “Brokers preference orders when they route their clients’ marketable orders to dealers in exchange for various monetary and nonpecuniary payments for order flow.” Larry Harris, Trading and Exchanges: Market Microstructure for Practitioners, (2003).

[28] “When you place an order to buy or sell a stock, your broker has choices on where to execute your order. Instead of routing your order to a market or market-makers for execution, your broker may fill the order from the firm's own inventory. This is called ‘internalization.’" U.S. Securities and Exchange Commission, Fast Answers, available at http://www.sec.gov/answers/internalization.htm.

[29] See, e.g., Daniel Weaver, The Trade-At Rule, Internalization, and Market Quality, 3 (Apr. 17, 2014)(finding “strong support for the existence of a negative relationship between the degree of internalization and market quality,” and concluding that “investors [are] paying $3,890,624 more per stock per year due to internalization.”), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1846470.

[30] Under the maker-taker pricing model, the traders whose orders “make” or furnish liquidity to a trading venue by posting new bids or offers receive a rebate, whereas traders who “take” or remove liquidity by hitting an existing bid or lifting an existing offer pay a take fee. See Stanislav Dolgopolov, The Maker-Taker Pricing Model and Its Impact on Securities Market Structure, 8 Va. L. & Bus. Rev. 234-35 (June 27, 2014), available at http://bit.ly/1mfme9M.

[31] “As a way to attract orders from brokers, some exchanges or market-makers will pay your broker's firm for routing your order to them . . . . This is called ‘payment for order flow.’" U.S. Securities and Exchange Commission, Fast Answers, available at http://www.sec.gov/answers/payordf.htm.

[32] Testimony of Robert Battalio, Professor of Finance, Mendoza College of Business, University of Notre Dame, before the U.S. Senate Permanent Subcommittee on Investigations (June 17, 2014), available at http://www.hsgac.senate.gov/download/?id=83e63371-7a55-4eb4-99e8-d5973a5456b3; Editorial, The Hidden Cost of Trading Stocks, N.Y. Times (June 22, 2014) (suggesting that maker-taker fees are “corrupting” brokers, who “under the guise of making subjective judgments about best execution, [] were routinely sending orders to venues that paid the highest rebates,” and concluded by calling for greater regulation or elimination of maker-taker fees), available at http://www.nytimes.com/2014/06/23/opinion/best-execution-and-rebates-for-brokers.html?_r=0.

[33] Jennifer Victoria Christine Deana, Paradigm Shifts & Unintended Consequences: The Death Of The Specialist, The Rise Of High Frequency Trading, & The Problem Of Duty-Free Liquidity In Equity Markets, FIU Law Review, 218, 235 (Fall 2012)(noting that “Reg. NMS was fairly successful” because “the rise of electronic markets increased competition and reduced transaction costs,” but that the resulting “explosion of venues also had unintended consequences—consequences that run contrary to the good intentions of the national market system mandate.”), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2249294.

[34] Larry Tabb, Can Reg NMS Be Fixed?, Tabb Forum (Oct. 2, 2013) (noting that “[f]ixing Reg NMS to solve all of the industry’s problems together is next to impossible. Depending on your role in the market, the rules can swing from significantly beneficial to very detrimental. Where you stand on the issues depends on where you sit.”), available at http://tabbforum.com/opinions/can-reg-nms-be-fixed.

[35] Id.

[36] Lawrence Harris, Trading and Exchanges: Market Microstructure for Practitioners, 216-17 (2003). Professor Harris refers to these traders as “utilitarian traders.” See id. at 192-94. They include, among others, the following: (i) investors who seek to save current income for future consumption, while obtaining a reasonable rate of return; (ii) borrowers who rely on the promise of future revenues to borrow money to finance current investment; (iii) asset exchangers, who obtain an asset of greater immediate value than the one they tender; and (iv) hedgers, who trade in equities to reduce risk. Id.

[37] Id. at 216.

[38] Id. Professor Harris notes that “[l]iquid markets benefit the public through the externalities that utilitarian traders produce when they use markets to conduct their businesses more efficiently. These externalities generally result from production efficiencies that traders can realize by using markets to exchanges assets, hedge, or share risks.” Id. at 214.

[39] Ross Levine and Sara Zervos, Stock Markets, Banks, and Economic Growth, 88 Am. Econ. Rev., 537-58 (1998)(finding a significant positive correlation between stock market liquidity and current and future rates of economic growth, after controlling for economic and political factors.).

[40] Id. at 216-17; see also Committee on the Global Financial System, Market-making and proprietary trading: Industry trends, drivers and policy implications, 1 (Nov. 2014)(noting that “[m]arket-makers serve a crucial role in financial markets by providing liquidity to facilitate market efficiency and functioning.”), available at http://www.bis.org/publ/cgfs52.pdf. Of course, the interests of profit-motivated traders and investors and issuers are all sometimes aligned. See Securities Exchange Act Release No. 61358 (Jan. 14, 2010), 75 FR 3593, 3603 (Jan. 21, 2010), available at http://www.gpo.gov/fdsys/pkg/FR-2010-01-21/pdf/2010-1045.pdf.

[41] Id. at 216-17.

[42] See, e.g., U.S. Securities and Exchange Commission, The Investor's Advocate: How the SEC Protects Investors, Maintains Market Integrity, and Facilitates Capital Formation, (June 10, 2013)(noting that “[t]he mission of the U.S. Securities and Exchange Commission is to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.”), available at http://www.sec.gov/about/whatwedo.shtml; see also, e.g., 15 U.S.C. § 78k(a)(2).

[43] Id. at 217.

[44] Merritt B. Fox, Lawrence R. Glosten, and Gabriel V. Rauterberg, The New Stock Market: Sense and Nonsense, 31-34 (Mar. 17, 2015), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2580002&download=yes.

[45] Id. at 23-31.

[46] 15 U.S.C. § 78k-1(a)(1)(C).

[47] Securities Exchange Act Release No. 61358 (Jan. 14, 2010), 75 FR 3593, 3597 (Jan. 21, 2010)(noting that “the five objectives set forth in Section 11A can, at times, be difficult to reconcile.”), available at http://www.gpo.gov/fdsys/pkg/FR-2010-01-21/pdf/2010-1045.pdf. For example, the goal of matching investor orders “can be difficult to reconcile with the objective of promoting competition among markets. Order interaction promotes a system that maximizes the opportunities for the most willing seller to meet the most willing buyer. When many trading centers compete for order flow in the same stock, however, such competition can lead to the fragmentation of order flow in that stock. Fragmentation can inhibit the interaction of investor orders and thereby impair certain efficiencies and the best execution of investors’ orders.” Id. (internal citation and quotation marks omitted).

[48] See, e.g., U.S. Securities and Exchange Commission, The Investor's Advocate: How the SEC Protects Investors, Maintains Market Integrity, and Facilitates Capital Formation, (June 10, 2013)(noting that “[t]he mission of the U.S. Securities and Exchange Commission is to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.”), available at http://www.sec.gov/about/whatwedo.shtml; see also, e.g., 15 U.S.C. § 78k(a)(2).

[49] See BATS Market Volume Summary, U.S. Stock Exchanges (Apr. 29, 2015), available at http://www.batstrading.com/market_summary/. Of the eleven exchanges, three are operated by the New York Stock Exchange, three are operated by NASDAQ, four are operated by BATS, and the final one is CHX.

[50] See FINRA ATS Transparency Data (Apr. 6, 2015), available at https://ats.finra.org/TradingParticipants. Although 85 alternative trading systems were registered with the Commission as of April 6, 2015, only 36 are currently trading . A list of alternative trading systems registered with the Commission is available at http://www.sec.gov/foia/ats/atslist0415.pdf.

[51] Testimony of Stephen Luparello, Director of the Division of Trading and Markets, before the United States Senate Subcommittee on Securities, Insurance, and Investment, Committee on Banking, Housing, and Urban Affairs (Mar. 10, 2015), available at http://www.sec.gov/news/testimony/testimony-venture-exchanges.html.

[52] Testimony of Joe Ratterman, CEO, BATS Global Markets, Inc., before the U.S. Senate Banking Committee (July 8, 2014), available at http://www.banking.senate.gov/public/index.cfm?FuseAction=Files.View&FileStore_id=e629a146-0ee1-4ebc-940b-b3289ef77118.

[53] Securities Exchange Act Release No. 51808 (June 9, 2005), 70 FR 37496, 37499 (June 29, 2005)(noting that “[t]he [national market system] . . . incorporates two distinct types of competition — competition among individual markets and competition among individual orders — that together contribute to efficient markets. Vigorous competition among markets promotes more efficient and innovative trading services, while integrated competition among orders promotes more efficient pricing of individual stocks for all types of orders, large and small. Together, they produce markets that offer the greatest benefits for investors and listed companies), available at http://www.gpo.gov/fdsys/pkg/FR-2005-06-29/pdf/05-11802.pdf#page=125; see also 15 U.S.C. 78k-1(a)(1)(C)(ii).

[54] For purposes of the order protection rule, trading centers include not only the lit exchanges, but also dark pools, electronic communication networks, off-exchange market makers, and broker-dealers that internalize customer orders.

[55] Rule 611 of Regulation NMS, 17 CFR 242.611, available at https://www.law.cornell.edu/cfr/text/17/242.611. The order protection rule extends only to the national best bid or offer, and not to inferior quotes that comprise an exchange’s depth of book. Further, the rule includes the best bid or offer on FINRA’s alternative display facility, but that facility currently has no active participants. See FINRA, Alternative Display Facility, Participants, available at http://www.finra.org/industry/adf/participants.

[56] Haim Bodek, The Problem of HFT: Collected Writings on High Frequency Trading & Stock Market Reform, 37 (2012).

[57] Larry Tabb, CEO, TABB Group, Written Testimony to the United States Senate Committee on Banking, Housing, and Urban Affairs, 5 (Sept. 20, 2012), available at http://www.banking.senate.gov/public/index.cfm?FuseAction=Files.View&FileStore_id=268afb1b-4c5e-4ec0-8028-fc840b973843. Tabb notes that:

[W]hen the NYSE had the dominant share of NYSE-listed market activity, the NYSE acted like a monopoly. Execution times were long, costs were high, and institutional investors were not happy with their execution quality. . . . The implementation of Reg NMS changed this. It forced the NYSE to compete against other exchanges for market share. This caused the NYSE to lower cost, streamline their technologies, and expedite their average execution time from approximately 11 seconds, circa 2005, to under a millisecond today.

[58] A “lit” trading center is one where a limit order “is immediately visible to all market participants and thus has an immediate price impact as market participants revise their beliefs about the fundamental value. In contrast, if the limit order instead rests in a dark market, no one except the order submitter can observe the order and none of the information contained in the limit order can be impounded into prices until a trade occurs. If the limit order does not execute, the market will never know about the order.” Carole Comerton-Forde and Ta-lis J. Putnin,š, Dark trading and price discovery, 6 (Jan 6, 2015), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2183392&download=yes; see also Irene Aldridge, High Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems, 221 (2013)(defining a “lit” venue as “a traditional exchange-like trading venue, where the limit order book is observable by all engaged market participants.”).

[59] Michael A. Goldstein, Andriy V. Shkilko, Bonnie F. Van Ness, and Robert A. Van Ness, Competition in the Market for NASDAQ-listed Securities, 1 (Oct. 16, 2005), available at http://faculty.babson.edu/goldstein/research/Nasdaq-Competition28.pdf; Gary Shorter and Rena S. Miller, Dark Pools in Equity Trading: Policy Concerns and Recent Developments, 8 (Sept. 26, 2014), available at http://www.fas.org/sgp/crs/misc/R43739.pdf.

[60] BATS, U.S. Stock Exchanges Market Volume Summary (Apr. 30, 2015)(five-day average percentage of market), available at http://www.batstrading.com/market_summary/.

[61] See Amy Kwan, Ronald Masulis, and Thomas McInish, Trading Rules, Competition for Order Flow and Market Fragmentation, 7 ECGI Working Paper Series in Law (2014)(“There is widespread concern that dark trading may be harming market quality.”), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2365603&download=yes. Although dark pools and internalizers do not transmit their best quotations to the consolidated tape, they do transmit their completed trades to the tape. Thus, they provide post-trade price transparency.

[62] See generally U.S. Securities and Exchange Commission, Equity Market Structure Literature Review Part I: Market Fragmentation (Oct. 7, 2013), available at https://www.sec.gov/marketstructure/research/fragmentation-lit-review-100713.pdf.