EXHIBIT 13.1

TransCanada Corporation

2018 Annual information form

February 13, 2019

TED

TransCanada Annual information form 2018 | 2 | |

Contents

12 | ||

14 | ||

16 | ||

16 | ||

16 | ||

16 | ||

18 | ||

18 | ||

18 | ||

18 | ||

Health, safety, sustainability and environmental protection and social policies | 19 | |

20 | ||

21 | ||

21 | ||

21 | ||

24 | ||

24 | ||

25 | ||

Fitch | 25 | |

25 | ||

26 | ||

26 | ||

27 | ||

28 | ||

28 | ||

30 | ||

31 | ||

32 | ||

32 | ||

33 | ||

33 | ||

34 | ||

34 | ||

35 | ||

35 | ||

35 | ||

35 | ||

35 | ||

36 | ||

37 | ||

38 | ||

TransCanada Annual information form 2018 | 1 | |

Presentation of information

Throughout this Annual information form (AIF), the terms, we, us, our, the Company and TransCanada mean TransCanada Corporation and its subsidiaries. In particular, TransCanada includes references to TransCanada PipeLines Limited (TCPL). Where TransCanada is referred to with respect to actions that occurred prior to its 2003 plan of arrangement (Arrangement) with TCPL, which is described in the TransCanada Corporation – Corporate structure section below, such actions were taken by TCPL or its subsidiaries. The term subsidiary, when referred to in this AIF, with reference to TransCanada means direct and indirect wholly owned subsidiaries of, and legal entities controlled by, TransCanada or TCPL, as applicable.

Unless otherwise noted, the information contained in this AIF is given at or for the year ended December 31, 2018 (Year End). Amounts are expressed in Canadian dollars unless otherwise indicated. Information in relation to metric conversion can be found at Schedule A to this AIF. The Glossary found at the end of this AIF contains certain terms defined throughout this AIF and abbreviations and acronyms that may not otherwise be defined in this document.

Certain portions of TransCanada's management's discussion and analysis dated February 13, 2019 (MD&A) are incorporated by reference into this AIF as stated below. The MD&A can be found on SEDAR (www.sedar.com) under TransCanada's profile.

Financial information is presented in accordance with United States (U.S.) generally accepted accounting principles (GAAP). We use certain financial measures that do not have a standardized meaning under GAAP and therefore they may not be comparable to similar measures presented by other entities. Refer to the About this document – Non-GAAP measures section of the MD&A for more information about the non-GAAP measures we use and a reconciliation to their GAAP equivalents, which section of the MD&A is incorporated by reference herein.

Forward-looking information

This AIF, including the MD&A disclosure incorporated by reference herein, contains certain information that is forward-looking and is subject to important risks and uncertainties. We disclose forward-looking information to help current and potential investors understand management’s assessment of our future plans and financial outlook, and our future prospects overall.

Statements that are forward-looking are based on certain assumptions and on what we know and expect today and generally include words like anticipate, expect, believe, may, will, should, estimate or other similar words.

Forward-looking statements included or incorporated by reference in this AIF include information about the following, among other things:

• | our financial and operational performance, including the performance of our subsidiaries |

• | expectations about strategies and goals for growth and expansion |

• | expected cash flows and future financing options available, including portfolio management |

• | expected dividend growth |

• | expected future credit ratings |

• | expected costs and schedules for planned projects, including projects under construction and in development |

• | expected capital expenditures and contractual obligations |

• | expected regulatory processes and outcomes, including the impact of recent Federal Energy Regulatory Commission (FERC) policy changes (2018 FERC Actions) |

• | expected outcomes with respect to legal proceedings, including arbitration and insurance claims |

• | the expected impact of future accounting changes, commitments and contingent liabilities |

• | expected industry, market and economic conditions. |

Forward-looking statements do not guarantee future performance. Actual events and results could be significantly different because of assumptions, risks or uncertainties related to our business or events that happen after the date of this AIF.

2 | TransCanada Annual information form 2018 | |

Our forward-looking information is based on the following key assumptions, and subject to the following risks and uncertainties:

Assumptions

• | regulatory decisions and outcomes, including final outcomes of the 2018 FERC Actions |

• | planned and unplanned outages and the use of our pipeline and energy assets |

• | integrity and reliability of our assets |

• | anticipated construction costs, schedules and completion dates |

• | access to capital markets, including portfolio management |

• | expected industry, market and economic conditions |

• | inflation rates and commodity prices |

• | interest, tax and foreign exchange rates |

• | nature and scope of hedging. |

Risks and uncertainties

• | our ability to successfully implement our strategic priorities and whether they will yield the expected benefits |

• | our ability to implement a capital allocation strategy aligned with maximizing shareholder value |

• | the operating performance of our pipeline and energy assets |

• | amount of capacity sold and rates achieved in our pipeline businesses |

• | the amount of capacity payments and revenues from our energy business due to plant availability |

• | production levels within supply basins |

• | construction and completion of capital projects |

• | costs for labour, equipment and materials |

• | the availability and market prices of commodities |

• | access to capital markets on competitive terms |

• | interest, tax and foreign exchange rates |

• | performance and credit risk of our counterparties |

• | regulatory decisions and outcomes of legal proceedings, including arbitration and insurance claims |

• | changes in environmental and other laws and regulations |

• | competition in the pipeline and energy sectors |

• | unexpected or unusual weather |

• | acts of civil disobedience |

• | cyber security and technological developments |

• | economic conditions in North America as well as globally |

• | our ability to effectively anticipate and assess changes to government policies and regulations. |

You can read more about these factors and others in the MD&A and other reports we have filed with Canadian securities regulators and the U.S. Securities and Exchange Commission (SEC).

As actual results could vary significantly from the forward-looking information, you should not put undue reliance on forward-looking information and should not use future-oriented financial information or financial outlooks for anything other than their intended purpose. We do not update our forward-looking statements due to new information or future events, unless we are required to by law.

TransCanada Annual information form 2018 | 3 | |

TransCanada Corporation

CORPORATE STRUCTURE

Our head office and registered office are located at 450 – 1 Street S.W., Calgary, Alberta, T2P 5H1. TransCanada was incorporated pursuant to the provisions of the Canada Business Corporations Act (CBCA) on February 25, 2003 in connection with the Arrangement, which established TransCanada as the parent company of TCPL. The Arrangement was approved by TCPL common shareholders on April 25, 2003 and, following court approval and the filing of Articles of Arrangement, the Arrangement became effective May 15, 2003. Pursuant to the Arrangement, the common shareholders of TCPL exchanged each of their TCPL common shares for one common share of TransCanada. The debt securities and preferred shares of TCPL remained obligations and securities of TCPL (the preferred shares of TCPL have been subsequently redeemed). TCPL continues to carry on business as the principal operating subsidiary of TransCanada. TransCanada does not hold any material assets directly other than the common shares of TCPL and receivables from certain of TransCanada's subsidiaries.

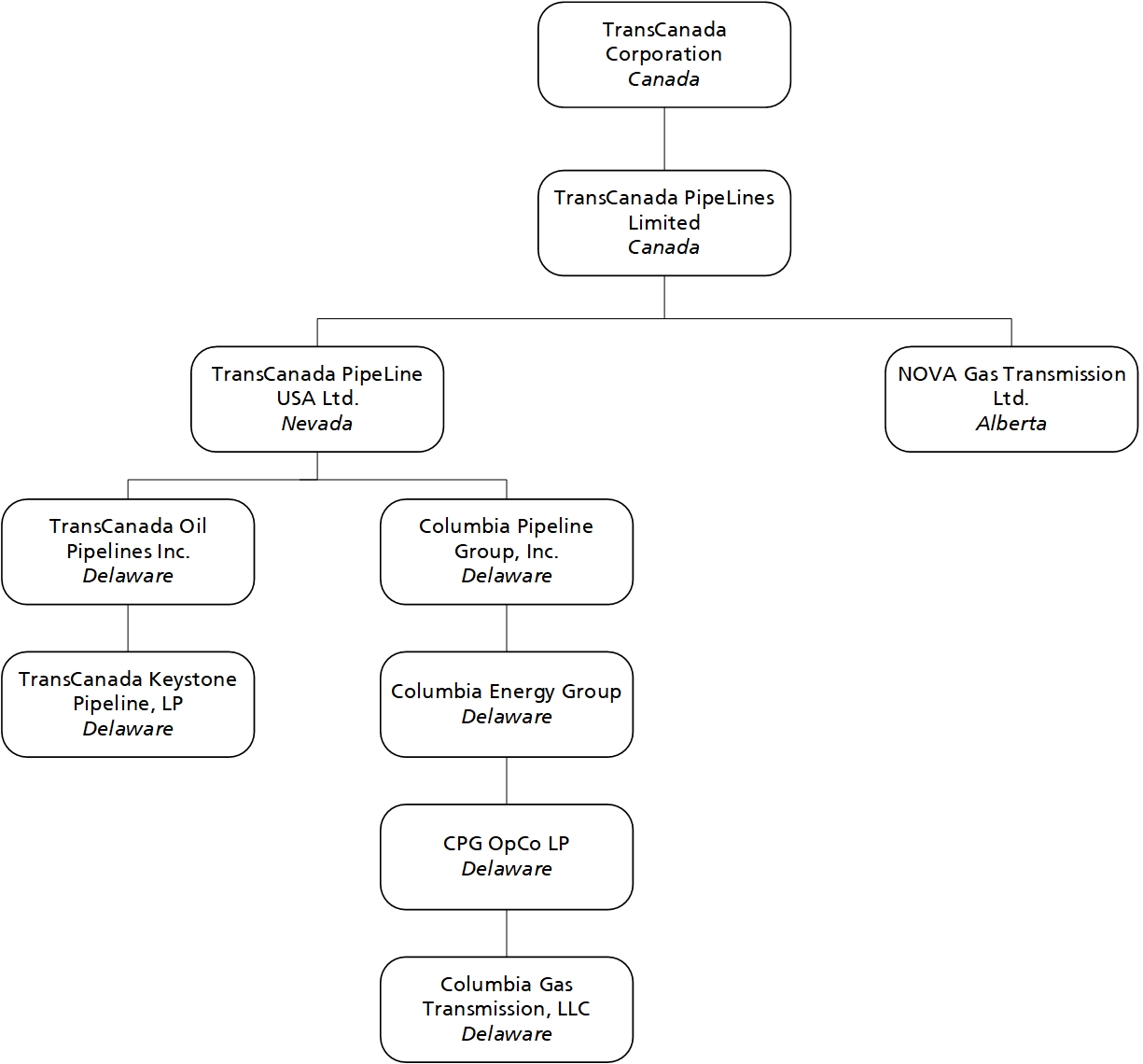

INTERCORPORATE RELATIONSHIPS

The following diagram presents the name and jurisdiction of incorporation, continuance or formation of TransCanada’s principal subsidiaries as at Year End. Each of the subsidiaries shown has total assets that exceeded ten per cent of the total consolidated assets of TransCanada as at Year End or revenues that exceeded ten per cent of the total consolidated revenues of TransCanada as at Year End. TransCanada beneficially owns, controls or directs, directly or indirectly, 100 per cent of the voting shares or units in each of these subsidiaries.

TransCanada Corporation Canada TransCanada PipeLines Limited Canada TransCanada PipeLine USA Ltd. Nevada TransCanada Oil Pipelines Inc. Delaware TransCanada Keystone Pipeline, LP Delaware Columbia Pipeline Group, Inc. Delaware Columbia Energy Group Delaware CPG OpCo LP Delaware Columbia Gas Transmission, LLC Delaware NOVA Gas Transmission Ltd. Alberta |

The above diagram does not include all of the subsidiaries of TransCanada. The assets and revenues of excluded subsidiaries in the aggregate did not exceed 20 per cent of the total consolidated assets of TransCanada as at Year End or total consolidated revenues of TransCanada for the year then ended.

4 | TransCanada Annual information form 2018 | |

General development of the business

We operate in three core businesses – Natural Gas Pipelines, Liquids Pipelines and Energy. In order to provide information that is aligned with how management decisions about our businesses are made and how performance of our businesses is assessed, our results are reflected in five operating segments: Canadian Natural Gas Pipelines, U.S. Natural Gas Pipelines, Mexico Natural Gas Pipelines, Liquids Pipelines and Energy. We also have a Corporate segment, consisting of corporate and administrative functions that provide governance, financing and other support to the Company's business segments.

Natural Gas Pipelines and Liquids Pipelines are principally comprised of our respective natural gas and liquids pipelines in Canada, the U.S. and Mexico, as well as our regulated natural gas storage operations in the U.S. Energy includes our power operations and our unregulated natural gas storage business in Canada.

Summarized below are significant developments that have occurred in our Natural Gas Pipelines, Liquids Pipelines and Energy businesses, respectively, and certain acquisitions, dispositions, events or conditions which have had an influence on those developments, during the last three financial years and year to date in 2019. Further information about changes in our business that we expect to occur during the current financial year can be found in the Canadian Natural Gas Pipelines, U.S. Natural Gas Pipelines, Mexico Natural Gas Pipelines, Liquids Pipelines and Energy sections of the MD&A, which sections of the MD&A are incorporated by reference herein.

NATURAL GAS PIPELINES

Developments in the Canadian Natural Gas Pipelines Segment

Date | Description of development |

CANADIAN REGULATED PIPELINES | |

NGTL System - Expansion Programs | |

2016 | In 2016, we had approximately $2.3 billion of facilities that received regulatory approval and approximately $0.45 billion under construction. In October 2016, the Government of Canada approved our application for a $1.3 billion NGTL System expansion program. This NGTL System expansion program consists of five pipeline loops ranging in size from 24 to 48-inch pipe of approximately 230 km (143 miles) in length, and two compressor station unit additions of approximately 46.5 MW (62,360 hp). In 2016, we placed approximately $0.5 billion of new facilities in service. |

2017 | In June 2017, we announced a $2.0 billion expansion program on our NGTL System based on contracted customer demand for approximately 3.2 PJ/d (3 Bcf/d) of incremental firm receipt and delivery services, subject to regulatory approvals. Construction is expected to start in early 2019, with initial projects expected to be in service in fourth quarter 2019 and final projects in service in 2021. In 2017, we placed approximately $1.7 billion of new facilities in service. |

2018 | In February 2018, we announced the NGTL System 2021 Expansion Program with an estimated capital cost of $2.3 billion and an anticipated in-service date in the first half of 2021. This program consists of approximately 375 km (233 miles) of new pipeline, three compressor units, a control valve and associated facilities. The expansion is required to connect incremental supply and expand basin export capacity by 1.1 PJ/d (1 Bcf/d) to the Empress export delivery point at the interconnection of the NGTL System and the Canadian Mainline. An application to construct and operate the NGTL System 2021 Expansion Program was filed with the NEB in June 2018 and will proceed through a public hearing in third quarter 2019. In October 2018, we announced the NGTL System 2022 Expansion Program to meet capacity requirements for incremental firm receipt and intra-basin delivery services to commence in November 2021 and April 2022. This $1.5 billion expansion of the NGTL System consists of approximately 197 km (122 miles) of new pipeline, three compressor units, meter stations and associated facilities. Applications for approvals to construct and operate the facilities are expected to be filed with the NEB in second quarter 2019 and, pending receipt of regulatory approvals, construction would start as early as third quarter 2020. In 2018, we placed approximately $0.6 billion of projects in service. |

NGTL System - North Montney Mainline (NMML) | |

2016 | In September 2016, the Government of Canada approved a sunset clause extension request that we filed in March 2016, for the NMML Certificate of Public Convenience and Necessity (CPCN), for one year to June 10, 2017. |

2017 | In March 2017, we filed an application with the NEB for a variance to the existing approvals for the NMML project to remove the condition that the project could only proceed once a positive FID was made for the Pacific Northwest LNG project. The NMML project consists of approximately 206 km (128 miles) of new pipeline, three compressor units and 14 meter stations. The NMML project is underpinned by restructured 20-year commercial contracts with shippers and is not dependent on the Pacific Northwest LNG project proceeding. |

TransCanada Annual information form 2018 | 5 | |

Date | Description of development |

2018 | In July 2018, the NEB issued an amending order and amended CPCN following the Government of Canada approval of our application, to the existing NMML project approvals to remove the condition requiring a positive FID for the Pacific Northwest LNG project prior to commencement of construction. The NEB directed NGTL to seek approval for a revised tolling methodology for the project following a provisional period defined as one year after the receipt of the Government of Canada decision, otherwise stand-alone tolling will be imposed as a default. NGTL is working with its shippers to address this requirement and is confident an acceptable tolling mechanism, other than stand-alone tolling, will be established. Construction on the NMML project was initiated in August 2018. The first phase of the project is anticipated to be in service by fourth quarter 2019, and the second phase by second quarter 2020. The current estimated project cost increased from original estimates by $0.2 billion to $1.6 billion mainly due to construction schedule delays and an increase in market-dependent construction costs. |

NGTL System - Revenue Requirement Settlements | |

2017 | The two-year revenue requirement agreement for 2016-2017 Settlement expired on December 31, 2017. The 2016-2017 Settlement fixed ROE at 10.1 per cent on 40 per cent deemed common equity, established depreciation at a forecast composite rate of 3.16 per cent and fixed OM&A costs at $222.5 million annually. An incentive mechanism for variances enabled NGTL to capture savings from improved performance and provided for the flow-through of all other costs, including pipeline integrity expenses and emissions costs. On November 24, 2017, the NEB approved interim tolls for 2018. |

2018 | In June 2018, the NEB approved the 2018-2019 Revenue Requirement Settlement (2018-2019 Settlement), as filed, and the resulting final 2018 tolls. The 2018-2019 Settlement, which is effective from January 1, 2018 to December 31, 2019, fixes ROE at 10.1 per cent on 40 per cent deemed common equity and increases the composite depreciation rate from 3.18 per cent to 3.45 per cent. OM&A costs are fixed at $225 million for 2018 and $230 million for 2019 with a 50/50 sharing mechanism for any variances between the fixed amounts and actual OM&A costs. All other costs, including pipeline integrity expenses and emissions costs, are treated as flow-through expenses. |

Canadian Mainline – Eastern Mainline Project | |

2016 | The Eastern Mainline project was conditioned on the approval and construction of the Energy East pipeline. Refer to the General development of the business – Liquids Pipelines section for information on Energy East. |

2017 | In October 2017, after a careful review of the changed circumstances, we informed the NEB that we would not be proceeding with the Energy East and Eastern Mainline project applications, that in effect provided public notice that the projects were canceled. Refer to the General development of the business – Liquids Pipelines section for information on Energy East. |

Canadian Mainline - Long-Term Fixed-Price (LTFP) Services | |

2017 | In November 2017, we began offering a new NEB-approved service on the Canadian Mainline referred to as the Dawn LTFP service. This service enables WCSB producers to transport up to 1.5 PJ/d (1.4 Bcf/d) of natural gas at a simplified toll of $0.77/GJ from the Empress receipt point in Alberta to the Dawn hub in Southern Ontario. The LTFP service is underpinned by ten-year contracts that have early termination rights after five years. Any early termination will result in an increased toll for the last two years of the contract. |

2018 | In December 2018, we announced 670 TJ/d (625 MMcf/d) of new natural gas transportation contracts from the WCSB on the Canadian Mainline. Upon NEB approval of this LTFP service, referred to as the North Bay Junction (NBJ) LTFP service, incremental volumes under these LTFP contracts will reach markets in Ontario, Québec, New Brunswick, Nova Scotia and the Northeastern U.S. using existing capacity on the Canadian Mainline as well as new compression facilities. Customers have executed 15-year precedent agreements to proceed with the project with an estimated capital cost of $96 million. |

2019 | In January 2019, we filed an application for approval of the NBJ LTFP with the NEB, and expect a decision in third quarter 2019. |

Canadian Mainline Settlement | |

2017 | While the NEB-approved Canadian Mainline's 2015-2030 tolls and tariff settlement (LDC Settlement) specified tolls for 2015-2020, the NEB ordered a toll review halfway through this six-year period. A supplemental agreement for the 2018-2020 period was executed between TransCanada and eastern LDCs and filed with the NEB in December 2017 (Supplemental Agreement). The Supplemental Agreement, supported by a majority of Canadian Mainline stakeholders, proposed lower tolls, preserved an incentive arrangement that provides an opportunity for 10.1 per cent, or greater return, on a 40 per cent deemed common equity and described the revenue requirements and billing determinants for the 2018-2020 period. Interim tolls for 2018, as established by the Supplemental Agreement, were filed and subsequently approved by the NEB in December 2017. |

2018 | In October 2018, we concluded the written hearing process for the Canadian Mainline 2018-2020 toll review with the filing of our reply evidence to the NEB. In December 2018, the NEB 2018 decision was issued (NEB 2018 Decision), approving all elements of the application, including our cost and volume forecasts, higher depreciation rates and continuation of pricing discretion, with the exception of the amortization period for the Long Term Adjustment Account (LTAA), which is now to be amortized over 2018 to 2020. The impact of the NEB 2018 Decision was reflected in lower tolls effective February 1, 2019. |

2019 | As directed by the NEB, we filed a compliance filing in January 2019, the outcome of which is expected in first quarter 2019. |

6 | TransCanada Annual information form 2018 | |

Date | Description of development |

LNG PIPELINE PROJECTS | |

Prince Rupert Gas Transmission (PRGT) | |

2016 | In September 2016, PNW LNG received an environmental certificate from the Government of Canada for a proposed LNG plant at Prince Rupert, B.C. In December 2016, PNW LNG received an LNG export license from the NEB which extended the export term from 25 years to 40 years. We continued our engagement with Indigenous groups and signed project agreements with 14 First Nation groups along the pipeline route, which outlined financial and other benefits and commitments that would be provided to each First Nation for as long as the project was in service. |

2017 | In July 2017, we were notified that PNW LNG would not be proceeding with their proposed LNG project and that Progress Energy would be terminating their agreement with us for development of the PRGT project. In accordance with the terms of the agreement, we received a payment of $0.6 billion from Progress Energy in October 2017 for full recovery of our costs plus carrying charges. |

Coastal GasLink | |

2016 | In first quarter 2016, we continued to engage with Indigenous groups and announced project agreements with 11 First Nation groups along the pipeline route, which outlined financial and other benefits and commitments that would be provided to each First Nation group for as long as the project was in service. We also continued to engage with stakeholders along the pipeline route and progressed detailed engineering and construction planning work to refine the capital cost estimate. In response to feedback received, we applied for a minor route amendment to the BCEAO in order to provide an option in the area of concern. In July 2016, the LNG Canada joint venture participants announced a delay to their FID for the proposed facility in Kitimat, B.C. We worked with LNG Canada to maintain the appropriate pace of the Coastal GasLink development schedule and work activities. We continued our engagement with Indigenous groups along our pipeline route and concluded long-term project agreements with 17 First Nation communities. |

2017 | The continuing delay in the FID for the LNG Canada project triggered a restructuring of the provisions in the Coastal GasLink project agreement with LNG Canada that resulted in the payment of certain amounts to TransCanada with respect to carrying charges on costs incurred. In 2017, we received payments of $88 million related to carrying charges on costs incurred since inception of the project. Coastal GasLink filed an amendment to the Environmental Assessment Certificate in November 2017 for an alternate route on a portion of the pipeline. |

2018 | In October 2018, we announced that we are proceeding with construction of the Coastal GasLink pipeline project following the LNG Canada joint venture participants' announcement that they had reached a positive FID to build the LNG Canada natural gas liquefaction facility in Kitimat, B.C. Coastal GasLink will provide the natural gas supply to the LNG Canada facility and is underpinned by 25-year TSAs (with additional renewal provisions) with each of the five LNG Canada participants. Coastal GasLink will be a 670 km (416 miles) pipeline with an initial capacity of approximately 2.2 PJ/d (2.1 Bcf/d) with potential expansion capacity up to 5.4 PJ/d (5.0 Bcf/d). All necessary regulatory permits have been received to allow us to proceed with construction activities which began in December 2018, with a planned in-service date in 2023. Coastal GasLink has signed project and community agreements with all 20 elected Indigenous bands along the pipeline route, confirming strong support from Indigenous communities across the province of B.C. In July 2018, an individual asked the NEB to consider whether the Coastal GasLink pipeline should be federally regulated by the NEB. In October 2018, the NEB advised that it would consider the question of jurisdiction, granted Coastal GasLink standing in the matter, and reserved the right to decide on the participation of all other potentially interested parties, including the individual who raised the question. In December 2018, the NEB issued a process letter addressing participation and set the schedule which is expected to conclude in the second half of 2019, with a decision to follow. In December 2018, the B.C. Supreme Court issued an interim injunction, ordering opponents of the Coastal GasLink project to allow pipeline construction workers access to a blockaded area of the Coastal GasLink right of way, south of Houston, B.C. The Coastal GasLink capital cost estimate is $6.2 billion with the majority of the construction spend occurring in 2020 and 2021. Subject to terms and conditions, differences between the estimated capital cost and final cost of the project will be recovered in future pipeline tolls. As part of the Coastal GasLink funding plan, we are exploring joint venture partners and project financing. The total capital cost includes pre-FID costs incurred of $470 million. In accordance with provisions in the agreements with the LNG Canada joint venture participants, all five parties elected to reimburse us for their share of pre-FID costs, totaling $470 million, in November 2018. In addition, all five LNG Canada joint venture participants elected to make cash payments throughout the construction period with respect to carrying charges on costs incurred. |

2019 | In January 2019, the RCMP moved to enforce the injunction issued by the B.C. Supreme Court. Following negotiations, the blockaders agreed to abide by the terms of the injunction and allow access to the area. |

TransCanada Annual information form 2018 | 7 | |

Developments in the U.S. Natural Gas Pipelines Segment

Date | Description of development |

U.S. NATURAL GAS PIPELINES - COLUMBIA | |

Columbia Acquisition | |

2016 | On July 1, 2016, we acquired 100 per cent ownership of Columbia for a purchase price of US$10.3 billion in cash. The acquisition was initially financed through proceeds of $4.4 billion from the sale of subscription receipts, draws on acquisition bridge facilities in the aggregate amount of US$6.9 billion and existing cash on hand. The sale of the subscription receipts was completed on April 1, 2016, through a public offering, and following the closing of the acquisition, the subscription receipts were exchanged into 96.6 million TransCanada common shares. |

Columbia Pipeline Partners LP (CPPL) | |

2016 | In November 2016, we announced that we entered into an agreement and plan of merger through which Columbia agreed to acquire, for cash, all of the outstanding publicly held common units of CPPL. |

2017 | In February 2017, we completed the acquisition, for cash, of all outstanding publicly held common units of CPPL at a price of US$17.00 and a stub period distribution of US$0.10 per common unit for an aggregate transaction value of US$921 million. |

Columbia Gas - Leach XPress | |

2016 | The FEIS for the Leach XPress project was received in September 2016. The project transports approximately 1.6 PJ/d (1.5 Bcf/d) of Marcellus and Utica gas supply to delivery points along the pipeline and to the Leach interconnect with Columbia Gulf, and consists of 260 km (160 miles) of 36-inch greenfield pipe, 39 km (24 miles) of 36-inch loop, three km (two miles) of 30-inch greenfield pipe, 82.8 MW (111,000 hp) of greenfield compression and 24.6 MW (33,000 hp) of brownfield compression. |

2018 | The US$1.6 billion project was placed in service in January 2018. |

Columbia Gas - Mountaineer XPress | |

2016 | The FERC 7(C) application for the Mountaineer XPress project was filed in April 2016. The project is designed to transport supply from the Marcellus and Utica shale plays to points along the system and to the Leach interconnect with Columbia Gulf. The project consists of 275 km (171 miles) of 36-inch greenfield pipeline, ten km (six miles) of 24-inch lateral pipeline, 0.6 km (0.4 miles) of 30-inch replacement pipeline, 114.1 MW (153,000 hp) of greenfield compression and 55.9 MW (75,000 hp) of brownfield compression. |

2017 | The FERC certificate for the Mountaineer XPress project was received in December 2017. |

2019 | Approximately 45 per cent of the Mountaineer XPress project was placed in service in January 2019, with the remainder to be placed in service in February and March 2019, along with Gulf Xpress (see Columbia Gulf - Gulf XPress below). Total estimated project costs have been revised upwards to US$3.2 billion reflecting the impact of delays of various regulatory approvals from the FERC and other agencies, increased contractor construction costs due to unusually high demand for construction resources in the region, unusually high instances of inclement weather throughout construction, and modifications to contractor work plans to mitigate construction delays associated with these impacts. |

Columbia Gas - WB XPress | |

2017 | The FERC certificate for the WB XPress project was received in November 2017. |

2018 | The WB XPress project, designed to transport approximately 1.4 PJ/d (1.3 Bcf/d) of Marcellus gas supply westbound to the Gulf Coast and eastbound to Mid-Atlantic markets, was placed in service in October 2018 and November 2018 for the Western Build and Eastern Build, respectively. |

Columbia Gas - Buckeye XPress | |

2017 | The Buckeye XPress project represents an upsizing of an existing pipeline replacement project in conjunction with our Columbia Gas modernization program. The US$0.2 billion cost to upsize the replacement pipe and install compressor upgrades will enable us to offer approximately 290 TJ/d (275 MMcf/d) of incremental pipeline capacity to accommodate growing Appalachian production. We expect the project to be placed in service in late-2020. |

Columbia Gulf - Rayne XPress | |

2016 | The FEIS for the Rayne XPress project was received in September 2016. The project transports approximately 1.1 PJ/d (1 Bcf/d) of supply from an interconnect with the Leach XPress pipeline project and another interconnect, to markets along the system and to the Gulf Coast. The project consists of bi-directional compressor station modifications along Columbia Gulf, 38.8 MW (52,000 hp) of greenfield compression, 20.1 MW (27,000 hp) of replacement compression and six km (four miles) of 30-inch pipe replacement. |

2017 | The US$0.4 billion project was placed in service in November 2017. |

8 | TransCanada Annual information form 2018 | |

Date | Description of development |

Columbia Gulf - Gulf XPress | |

2016 | The FERC 7(C) application for the Gulf XPress project was filed in April 2016. The project is associated with the Mountaineer XPress expansion to move Appalachian supply to the Gulf Coast by the addition of seven greenfield mid-point compressor stations along the Columbia Gulf route. |

2017 | The FERC certificate for the Gulf XPress project was received on December 29, 2017. |

2019 | The US$0.6 billion project is expected to be placed in service in February and March 2019. |

Columbia Gulf - Cameron Access | |

2018 | The Cameron Access project, designed to transport approximately 0.9 PJ/d (0.8 Bcf/d) of gas supply to the Cameron LNG export terminal in Louisiana, was placed in service in March 2018. |

Columbia Gulf - Louisiana XPress | |

2018 | In November 2018, we sanctioned the Louisiana XPress project which will connect supply directly to Gulf Coast LNG export markets with the addition of three greenfield mid-point compressor stations along Columbia Gulf. The estimated US$0.4 billion project is expected to be placed in service in 2022. |

Modernization I & II | |

2017 | Columbia Gas and its customers entered into a settlement arrangement, approved by the FERC, which provides recovery and return on investment to modernize its system, improve system integrity, and enhance service reliability and flexibility. The modernization program includes, among other things, replacement of aging pipeline and compressor facilities, enhancements to system inspection capabilities, and improvements in control systems. The US$1.5 billion Modernization I arrangement was completed under the terms of a 2012 settlement agreement, with the final US$0.2 billion spent in 2017. Modernization II has been approved for up to US$1.1 billion of work starting in 2018 and to be completed through 2020. As per terms of the arrangements, facilities in service by October 31 collect revenues effective February 1 of the following year. |

OTHER U.S. NATURAL GAS PIPELINES | |

ANR Pipeline | |

2016 | ANR Pipeline filed a Section 4 Rate Case that requested an increase to ANR's maximum transportation rates in January 2016. Shifts in ANR’s traditional supply sources and markets, necessary operational changes, needed infrastructure updates, and evolving regulatory requirements were driving required investment in facility maintenance, reliability and system integrity as well as an increase in operating costs that resulted in the current tariff rates not providing a reasonable return on our investment. We also pursued a collaborative process to find a mutually beneficial outcome with our customers through settlement negotiations. ANR's last rate case filing was more than 20 years ago. ANR reached a settlement with its shippers effective August 1, 2016 and received FERC approval on December 16, 2016. Per the settlement, transmission reservation rates would increase by 34.8 per cent and storage rates would remain the same for contracts one to three years in length, while increasing slightly for contracts of less than one year and decreasing slightly for contracts more than three years in duration. There is a moratorium on any further rate changes until August 1, 2019. ANR may file for new rates after that date if it has spent more than US$0.8 billion in capital additions, but must file for new rates no later than an effective date of August 1, 2022. |

Great Lakes | |

2017 | In October 2017, Great Lakes filed a rate settlement with the FERC to satisfy its obligations from its previous 2013 rate settlement for new rates to be in effect by January 1, 2018 (2017 Great Lakes Rate Settlement). In conjunction with the Canadian Mainline's LTFP service (see Canadian Regulated Pipelines – Long-Term Fixed-Price Service above), Great Lakes entered into a new ten-year gas transportation contract with the Canadian Mainline. This NEB-approved contract, effective November 1, 2017, contains volume reduction options up to full contract quantity beginning in year three. |

Portland Natural Gas Transmission System (Portland) | |

2016 | In January 2016, we closed the sale of our 49.9 per cent of our total 61.7 per cent interest in Portland to TC PipeLines, LP (TCLP) for US$223 million. Proceeds were comprised of US$188 million in cash and the assumption of US$35 million of a proportionate share of Portland debt. |

2017 | In June 2017, we closed the sale of a 49.34 per cent of our 50 per cent interest in Iroquois, along with an option to sell the remaining 0.66 per cent at a later date, to TCLP. At the same time, we closed the sale of our remaining 11.81 per cent interest in Portland to TCLP. Proceeds from these transactions were US$765 million, before post-closing adjustments, and were comprised of US$597 million in cash and US$168 million representing a proportionate share of Iroquois and Portland debt. In December 2017, Portland executed precedent agreements with several LDCs in New England and Atlantic Canada to re-contract certain system capacity set to expire in 2019, as well as expand the Portland system to bring its certificated capacity from 222 TJ/d (210 MMcf/d) up to 290 TJ/d (275 MMcf/d). The approximate US$80 million Portland XPress Project will proceed concurrently with upstream capacity expansions. The in-service dates of the Portland XPress project are being phased-in over a three-year period, beginning November 1, 2018. |

2018 | Phase I of Portland XPress was placed in service on November 1, 2018. |

TransCanada Annual information form 2018 | 9 | |

Date | Description of development |

Iroquois Gas Transmission System, L.P. (Iroquois) | |

2016 | FERC approvals were obtained for settlements with shippers for our Iroquois, Tuscarora and Columbia Gulf pipelines in third quarter 2016. In March 2016, we acquired an additional 4.87 per cent interest in Iroquois for an aggregate purchase price of US$54 million and in May 2016, a further 0.65 per cent was acquired for US$7 million. As a result, our interest in Iroquois increased to 50 per cent. |

2017 | In June 2017, we closed the sale of a 49.34 per cent of our 50 per cent interest in Iroquois, along with an option to sell the remaining 0.66 per cent at a later date, to TCLP. At the same time, we closed the sale of our remaining 11.81 per cent interest in Portland to TCLP. Refer to the Portland Natural Gas Transmission System section above. |

Developments in the Mexico Natural Gas Pipelines segment

Date | Description of development |

MEXICO NATURAL GAS PIPELINES | |

Topolobampo | |

2016 | In November 2012, we were awarded the contract to build, own and operate the Topolobampo project. Construction on the project is supported by a 25-year TSA for 720 TJ/d (670 MMcf/d) with the CFE. The Topolobampo project is a 560 km (348 miles), 30-inch pipeline that will receive gas from the upstream pipelines near El Encino, Chihuahua, and will deliver natural gas from these interconnecting pipelines to delivery points along the pipeline route including our Mazatlán pipeline at El Oro, Sinaloa. |

2017 | The Topolobampo project was substantially complete, excluding a 20 km (12 miles) section due to delays experienced by the Secretary of Energy, the government department which conducts indigenous consultations in Mexico. Under the terms of the TSA, the delays were recognized as a force majeure event with provisions allowing for the collection of revenue as per the original TSA service commencement date of July 2016. The pipeline cost is approximately US$1.2 billion, an increase of US$0.2 billion from the original estimate, due to the delays. |

2018 | The Topolobampo project was placed in service in June 2018. |

Mazatlán | |

2016 | In November 2012 we were awarded the contract to build, own and operate the Mazatlán project. This project is a 430 km (267 miles), 24-inch pipeline running from El Oro to Mazatlán, Sinaloa, with an estimated cost of US$0.4 billion. This pipeline is supported by a 25-year natural gas TSA for 214 TJ/d (200 MMcf/d) with the CFE. Physical construction was completed in 2016 and was awaiting natural gas supply from upstream interconnecting pipelines. We met our obligations and collected revenue as per provisions in the contract and per the original TSA service commencement date of December 2016. |

2017 | The Mazatlán project was placed into full service in July 2017. |

Tula | |

2016 | In November 2015, we were awarded the contract to build, own and operate the 36-inch, 324 km (201 miles) pipeline with a 16-inch, 24 km (15 miles) lateral, supported by a 25-year natural gas TSA for 949 TJ/d (886 MMcf/d) with the CFE. The pipeline will transport natural gas from Tuxpan, Veracruz to markets near Tula, extending through the states of Puebla and Hidalgo. |

2017 | Construction of the Tula pipeline was substantially completed in 2017, with the exception of approximately 90 km (56 miles) of the pipeline. |

2018 | The CFE has approved the recognition of force majeure events for the Tula pipeline, including the continuation of the payment of fixed capacity charges to us that began in first quarter 2018. Commencement of constructing the central segment of the project has been delayed due to a lack of progress by the Secretary of Energy, the governmental department responsible for indigenous consultation. Project completion has been revised to the end of 2020. We have negotiated separate CFE contracts that would allow certain segments of the pipeline to be placed in service when gas is available. |

Villa de Reyes | |

2016 | In April 2016, we were awarded the contract to build, own and operate the 36- and 24-inch Villa de Reyes pipelines, totaling 420 km (261 miles). Construction of the pipeline is supported by a 25-year natural gas TSA for 949 TJ/d (886 MMcf/d) with the CFE. The bi-directional pipeline will transport natural gas from Tula, Hidalgo to Villa de Reyes, San Luis Potosí, connecting to the Tamazunchale and Tula pipelines including a lateral to the Salamanca industrial complex in Guanajuato. |

2017 | Construction of the project commenced, however, delays due to archeological investigations by state authorities caused the in-service date to be revised to the second half of 2019. |

2018 | The CFE has approved the recognition of force majeure events for the Villa de Reyes pipeline, including the continuation of the payment of fixed capacity charges to us that began in first quarter 2018. Construction for the project is ongoing and is anticipated to be in service in the second half of 2019. We have negotiated separate CFE contracts that would allow certain segments of the pipeline to be placed in service when gas is available. |

10 | TransCanada Annual information form 2018 | |

Date | Description of development |

Sur de Texas | |

2016 | The Sur de Texas project is a joint venture with IEnova in which we hold a 60 per cent interest representing an investment of approximately US$1.3 billion. Construction of the pipeline is supported by a 25-year natural gas TSA for 2.8 PJ/d (2.6 Bcf/d) with the CFE. The 42-inch, 775 km (482 miles) pipeline will begin offshore in the Gulf of Mexico, at the border near Brownsville, Texas, and end in Tuxpan, Veracruz. The project will deliver natural gas to our Tamazunchale and Tula pipelines and to other third-party facilities. |

2017 | Approximately 60 per cent of the off-shore construction completed at December 31, 2017. |

2018 | Offshore construction was completed in May 2018 and the project continues to progress toward an anticipated in-service date in early second quarter 2019. An amending agreement was signed with the CFE that recognizes force majeure events and the commencement of payments of fixed capacity charges began on October 31, 2018. |

Further information about developments in the Natural Gas Pipelines business, including changes that we expect will occur in the current financial year, can be found in the MD&A in the Natural Gas Pipelines business section; Canadian Natural Gas Pipelines – Understanding our Canadian Natural Gas Pipelines segment, Significant events, Financial results and Outlook sections; U.S. Natural Gas Pipelines – Understanding our U.S. Natural Gas Pipelines segment, Significant events, Financial results and Outlook sections; and Mexico Natural Gas Pipelines – Understanding our Mexico Natural Gas Pipelines segment, Significant events, Financial results and Outlook sections, which sections of the MD&A are incorporated by reference herein.

TransCanada Annual information form 2018 | 11 | |

LIQUIDS PIPELINES

Development in the Liquids Pipelines Segment

Date | Description of development |

Keystone Pipeline System | |

2016 | The Houston Lateral pipeline and terminal, an extension from the Keystone Pipeline to Houston, Texas, went into service in August 2016. The terminal has an initial storage capacity for 700,000 barrels of crude oil. The HoustonLink pipeline which connects the Houston Terminal to Magellan's Houston and Texas City, Texas delivery system was completed in December 2016. The CITGO Petroleum (CITGO) Sour Lake pipeline connection between the Keystone Pipeline and CITGO's Sour Lake, Texas terminal was placed in service in December 2016. |

2017 | In fourth quarter 2017, we concluded open seasons for the Keystone pipeline and Marketlink and secured incremental long-term contractual support. In November 2017, the Keystone pipeline was temporarily shut down after a leak was detected in Marshall County, South Dakota. The estimated volume of the release was 5,000 barrels as reported to the NRC and the PHMSA. On November 29, 2017, the pipeline was repaired and returned to service at a reduced pressure in the affected section of the pipeline. This shutdown did not have a significant impact on our 2017 earnings. |

2018 | In 2018, we concluded successful open seasons for Marketlink securing incremental contractual support. We continue to expand our terminal facilities which are integral to our operations, with the completion of an additional one million barrels of storage at Cushing, Oklahoma. |

Keystone XL | |

2016 | In January 2016, the South Dakota PUC accepted Keystone XL's certification that it continued to comply with the conditions in its existing 2010 permit authority in the state. In January 2016, we filed a Notice of Intent to initiate a claim under Chapter 11 of NAFTA in response to the U.S. Administration’s decision to deny a Presidential permit for the Keystone XL Pipeline on the basis that the denial was arbitrary and unjustified. Through the NAFTA claim, we were seeking to recover more than US$15 billion in costs and damages that we estimated to have suffered as a result of the U.S. Administration’s breach of its NAFTA obligations. In June 2016, we filed a Request for Arbitration in a dispute against the U.S. Government pursuant to the Convention on Settlement of Investment Disputes between States and Nationals of Other States, the Rules of Procedure for the Institution of Conciliation and Arbitration Proceedings and Chapter 11 of NAFTA. In January 2016, we also filed a lawsuit in the U.S. Federal Court in Houston, Texas, asserting that the U.S. President’s decision to deny construction of Keystone XL exceeded his power under the U.S. Constitution. The federal court lawsuit did not seek damages, but rather a declaration that the permit denial was without legal merit and that no further Presidential action was required before construction of the pipeline could proceed. |

2017 | In January 2017, the U.S. President signed a Presidential Memorandum inviting TransCanada to refile an application for the U.S. Presidential Permit (Presidential Permit), which we later filed with the DOS. In February 2017, we filed an application with the Nebraska PSC to seek approval for the Keystone XL pipeline route through the state. In March 2017, the DOS issued a Presidential Permit authorizing construction of the U.S./ Canada border crossing facilities of Keystone XL. We discontinued our claim under Chapter 11 of NAFTA and withdrew the U.S. Constitutional challenge. In March 2017, two lawsuits were filed in Montana District Court challenging the validity of the Presidential Permit. Along with the U.S. Government, we filed motions for dismissal of these lawsuits which were subsequently denied in November 2017. The cases will now proceed to the consideration of summary judgment motions. In July 2017, we launched an open season to solicit additional binding commitments from interested parties for transportation of crude oil on the Keystone pipeline and for Keystone XL from Hardisty, Alberta to Cushing, Oklahoma and the U.S. Gulf Coast, which concluded in October 2017. In November 2017, we received PSC approval for the alternative mainline route and we filed a motion with the PSC to reconsider its ruling and permit us to file an amended application that would support their decision and would address certain issues related to their selection of the alternative route, which was denied in December 2017. In December 2017, opponents of Keystone XL and intervenors in the Nebraska regulatory proceeding filed an appeal of the PSC decision seeking to have that decision overturned. TransCanada supports the decision of the PSC and will actively participate in the appeal process to defend that decision. |

2018 | We have secured commercial support for all available Keystone XL project capacity and commenced certain pre-construction activities. The Nebraska Supreme Court agreed to hear an appeal of the Nebraska PSC route approval, in which oral arguments were heard in November 2018. We expect the Nebraska Supreme Court, as the final arbiter, could reach a decision by first quarter 2019. The Presidential Permit was challenged in two separate lawsuits commenced in Montana. Together with the DOJ, we are actively participating in these lawsuits to defend both the issuance of the Presidential Permit and the exhaustive environmental assessments that support the U.S. President's actions. Legal arguments addressing the merits of these lawsuits were heard in second quarter 2018. In third quarter 2018, the U.S. District Court in Montana issued a Partial Order requiring the DOJ and the DOS (collectively, the Federal Defendants) to prepare a supplemental environmental impact statement (SEIS) to the 2014 Final SEIS. In fourth quarter 2018, the U.S. District Court Judge in Montana invalidated the Presidential Permit and granted a partial injunction on the Keystone XL project. We applied to the U.S. District Court for a stay of its various decisions affecting the issuance of the Presidential Permit and the extensive environmental assessments that have been done in support of its issuance.That stay application was heard on January 14, 2019 and we are awaiting a decision. We intend to further pursue a stay of these decisions with the Ninth Circuit Court of Appeals. Our plans to commence construction of the Keystone XL project in 2019 will be impacted by the timing and |

12 | TransCanada Annual information form 2018 | |

Date | Description of development |

2018 (continued) | outcome of our appeal and stay proceedings. In September 2018, two U.S. Native American communities filed a lawsuit in Montana challenging the Presidential Permit. We have been granted intervenor status in the lawsuits. Initial briefing dates have been established, but no further action has occurred. The South Dakota PUC permit for the Keystone XL project was issued in June 2010 and certified in January 2016. An appeal of that certification was denied in June 2017 and that decision was further appealed to the South Dakota Supreme Court. In June 2018, the Supreme Court dismissed the appeal against the certification of the Keystone XL project finding that the lower court lacked jurisdiction to hear the case. This decision is final as there can be no further appeals from this decision by the Supreme Court. |

Energy East | |

2016 | In May 2016, we filed a consolidated application with the NEB for the Energy East pipeline. In June 2016, Energy East achieved a major milestone with the NEB’s announcement determining the Energy East pipeline application was sufficiently complete to initiate the formal regulatory review process. However, in August 2016, panel sessions were canceled as three NEB panelists recused themselves from continuing to sit on the panel to review the project due to allegations of reasonable apprehension of bias. As a result, all hearings for the project were adjourned until further notice. |

2017 | In January 2017, the NEB appointed three new permanent panel members to undertake the review of the Energy East and Eastern Mainline projects, and subsequently voided all decisions made by the previous hearing panel members and removing such decisions from the official hearing record. We were not required to refile the application and parties were not required to reapply for intervener status. In September 2017, we requested the NEB suspend the review of the Energy East and Eastern Mainline project applications for 30 days to provide time for us to conduct a careful review of the NEB's changes, which were announced in August 2017. In October 2017, after careful review of the changed circumstances, we informed the NEB that we would not be proceeding with the Energy East and Eastern Mainline project applications. We also notified the MDDELCC that we were withdrawing the Energy East project from the environmental review process. As the Energy East pipeline was also to provide transportation services for the Upland pipeline, the DOS was notified in October 2017, that we would no longer be pursuing the U.S. Presidential Permit application for that project. We reviewed the $1.3 billion carrying value of the projects, including AFUDC capitalized since inception, and recorded a $954 million after-tax impairment charge in our fourth quarter 2017 results. We ceased capitalizing AFUDC on the projects effective August 23, 2017, the date of the NEB's announced scope changes. With Energy East's inability to reach a regulatory decision, no recoveries of costs from third parties are forthcoming. |

Grand Rapids | |

2016 | Construction continued on the Grand Rapids pipeline. We entered into a partnership with Brion Energy Corporation (Brion) to develop Grand Rapids with each party owning 50 per cent of the pipeline project. Our partner has also entered into a long-term transportation service contract in support of the project. Construction progressed on the 20-inch diluent joint venture pipeline between Edmonton and Fort Saskatchewan, Alberta. The joint venture between Grand Rapids and Keyera was incorporated into Grand Rapids to provide enhanced diluent supply alternatives to our shippers. |

2017 | In August 2017, the Grand Rapids pipeline, jointly owned by TransCanada and PetroChina Canada Ltd. (formerly Brion), was placed in service. The 460 km (287 miles) crude oil transportation system connects producing area northwest of Fort McMurray, Alberta to terminals in the Heartland, Alberta market region. |

Northern Courier | |

2016 | Construction continued on the Northern Courier pipeline, a 90 km (56 miles) pipeline system that transports bitumen and diluent between the Fort Hills mine site and Suncor Energy's terminal located north of Fort McMurray, Alberta. The project is fully underpinned by long-term contracts with the Fort Hills partnership. |

2017 | The Northern Courier pipeline achieved commercial in-service in November 2017. |

White Spruce | |

2016 | In December 2016, we finalized a long-term transportation agreement to develop and construct the 20-inch, 72 km (45 miles) White Spruce pipeline, which would transport crude oil from Canadian Natural Resources Limited's Horizon facility in northeast Alberta to the Grand Rapids pipeline. |

2018 | In February 2018, the AER issued a permit for the construction of the $200 million White Spruce pipeline. Construction has commenced with an anticipated in-service date in second quarter 2019. |

Further information about developments in the Liquids Pipelines business, including changes that we can expect will occur in the current financial year, can be found in the MD&A in the Liquids Pipelines – Understanding our Liquids Pipelines business, Significant events, Financial results and Outlook sections, which sections of the MD&A are incorporated by reference herein.

TransCanada Annual information form 2018 | 13 | |

ENERGY

Development in the Energy Segment

Date | Description of development |

CANADIAN POWER | |

Alberta PPAs | |

2016 | In March 2016, we issued notice to the Balancing Pool to terminate our Alberta PPAs. In July 2016, we, along with the ASTC Power Partnership (ASTC), issued a notice referring the matter to be resolved by binding arbitration pursuant to the dispute resolution provisions of the PPAs. On July 25, 2016, the Government of Alberta brought an application in the Court of Queen’s Bench to prevent the Balancing Pool from allowing termination of a PPA held by another party which contains identically worded termination provisions to our PPAs. In December 2016, management engaged in settlement negotiations with the Government of Alberta and finalized terms of the settlement of all legal disputes related to the PPA terminations. The Government of Alberta and the Balancing Pool agreed to our termination of the PPAs resulting in the transfer of all our obligations under such PPAs to the Balancing Pool. Upon final settlement of the PPA terminations, we transferred to the Balancing Pool a package of environmental credits held to offset the PPA emissions costs and recorded a non-cash charge of $92 million before-tax ($68 million after-tax) related to the carrying value of our environmental credits. In first quarter 2016, as a result of our decision to terminate the PPAs, we recorded a non-cash impairment charge of $240 million before-tax ($176 million after-tax) comprised of $211 million before-tax ($155 million after-tax) related to the carrying value of our Sundance A and Sheerness PPAs and $29 million before-tax ($21 million after-tax) on our equity investment in the ASTC which previously held the Sundance B PPA. |

Napanee | |

2018 | Construction is substantially complete and commissioning activities are continuing at our 900 MW natural gas-fired power plant at Ontario Power Generation's Lennox site in eastern Ontario, in the town of Greater Napanee. We expect our total investment in the Napanee facility will be approximately $1.7 billion, with commercial operations expected to begin in second quarter 2019. |

Cartier Wind | |

2018 | In October 2018, we completed the sale of our interests in the Cartier Wind power facilities in Québec to Innergex Renewable Energy Inc. for net proceeds of approximately $630 million, before post-closing adjustments, resulting in a gain of $170 million ($143 million after-tax). |

Bécancour | |

2016 | In 2015, we executed an agreement with Hydro-Québec Distribution (HQ) allowing HQ to dispatch up to 570 MW of peak winter capacity from our Bécancour facility for a term of 20 years commencing in December 2016. The regulator in Québec, Régie de l'énergie, reversed its initial decision to approve this agreement. In November 2016, HQ released a new ten-year supply plan indicating additional peak winter capacity from Bécancour was not required. Management does not expect further developments at Bécancour until November 2019 when the next ten-year supply plan is filed. |

Bruce Power | |

2016 | Bruce Power entered into an agreement with the IESO in 2015 to extend the operating life of the facility to the end of 2064. This new agreement represents an extension and material amendment to the earlier agreement that led to the refurbishment of Units 1 and 2 at the site. The amended agreement, which took effect on January 1, 2016, allows Bruce Power to immediately invest in life extension activities for Units 3 through 8. Beginning in January 2016, Bruce Power received a uniform price of $65.73 per MWh for all units, which included certain flow-through items such as fuel and lease expense recovery. Over time, the uniform price is subject to adjustments for the return of and on capital invested at Bruce Power under the asset management (AM) and major component replacement (MCR) programs, along with various other pricing adjustments that would allow for a better matching of revenues and costs over the long-term. In connection with this opportunity, we exercised our option to acquire an additional 14.89 per cent ownership interest in Bruce B for $236 million from the Ontario Municipal Employees Retirement System. Subsequent to this acquisition, Bruce A and Bruce B were merged to form a single partnership structure, of which we hold a 48.4 per cent interest. |

2018 | In September 2018, Bruce Power submitted its final cost and schedule duration estimate (basis of estimate) for the Unit 6 MCR program to the IESO. The IESO has verified the basis of estimate and the Unit 6 MCR program is scheduled to begin in early-2020 with an expected completion in late-2023. Our project cost estimates reflect our expected investment of approximately $2.2 billion (in nominal dollars) in Bruce Power's Unit 6 MCR program and its ongoing AM program through 2023 as well as approximately $6.0 billion (in 2018 dollars) for the remaining five-unit MCR program and the remainder of the AM program beyond 2023. Future MCR investments will be subject to discrete decisions for each unit with specified off-ramps available for Bruce Power and the IESO. Bruce Power's current contract price of approximately $68 per MWh is expected to increase to approximately $75 per MWh on April 1, 2019 to reflect capital to be invested under the Unit 6 MCR program and the AM program as well as normal annual inflation adjustments. |

14 | TransCanada Annual information form 2018 | |

Date | Description of development |

Ontario Solar | |

2017 | In October 2017, we entered into an agreement to sell our Ontario solar assets comprised of eight facilities with a total generating capacity of 76 MW, to Axium Infinity Solar LP. On December 19, 2017, we closed the sale for $541 million, before post-closing adjustments, resulting in a gain of $127 million ($136 million after-tax). |

Coolidge Generating Station | |

2018 | On December 14, 2018, we entered into an agreement to sell our Coolidge generating station in Arizona to SWG Coolidge Holdings, LLC for approximately US$465 million, subject to timing of closing and related adjustments. Salt River Project Agriculture Improvement and Power District, the PPA counterparty, exercised its contractual right of first refusal on a sale to a third party in January 2019. The sale will result in an estimated gain of approximately $65 million ($50 million after tax), to be recognized upon closing of the sale transaction which is expected to occur in mid-2019. |

U.S. POWER | |

Ironwood | |

2016 | In February 2016, we acquired the 778 MW Ironwood natural gas fired, combined cycle power plant located in Lebanon, Pennsylvania for US$653 million in cash after post-acquisition adjustments. The Ironwood power plant delivers energy into the PJM Interconnection area power market. |

Monetization of U.S. Northeast Power Business | |

2016 | In November 2016, we announced the sale of Ravenswood, Ironwood, Ocean State Power and Kibby Wind to Helix Generation, LLC, an affiliate of LS Power Equity Advisors and the sale of TC Hydro to Great River Hydro, LLC, an affiliate of ArcLight Capital Partners, LLC. |

2017 | In April 2017, we closed the sale of TC Hydro to Great River Hydro, LLC for US$1.07 billion, before post-closing adjustments and recorded a gain of $715 million ($440 million after-tax). In June 2017, we closed the sale of Ravenswood, Ironwood, Ocean State Power and Kibby Wind to Helix Generation, LLC for US$2.029 billion, before post-closing adjustments. In addition to the pre-tax losses of approximately $829 million ($863 million after-tax) and a $1,085 million ($656 million after-tax) impairment charge that we recorded in 2016 upon entering into agreements to sell these assets, an additional pre-tax loss on sale of approximately $211 million ($167 million after-tax) was recorded in 2017, primarily related to an adjustment to the purchase price and repair costs for an unplanned outage at Ravenswood prior to close, partially offset by insurance recoveries for a portion of the repair costs. Proceeds from the sale transactions were used to fully retire the remaining bridge facilities that partially funded the acquisition of Columbia. On December 22, 2017, we entered into an agreement to sell our U.S. power retail contracts as part of the continued wind down of our U.S. power marketing operations. |

2018 | In March 2018, we closed the sale of our U.S. power retail contracts for proceeds of approximately US$23 million and recognized income of US$10 million (US$7 million after-tax). |

Further information about developments in the Energy business, including changes that we expect will occur in the current financial year, can be found in the MD&A in the Energy – Understanding our Energy business, Significant events, Financial results and Outlook sections, which sections of the MD&A are incorporated by reference herein.

TransCanada Annual information form 2018 | 15 | |

Business of TransCanada

Our energy infrastructure business is made up of pipeline, storage and power generation assets that gather, transport, produce, store or deliver natural gas, crude oil and other petroleum products and electricity to support businesses and communities in North America.

Our vision is to be the leading energy infrastructure company in North America, focusing on pipeline and power generation opportunities in regions where we have or can develop a significant competitive advantage. Refer to the About our business – 2018 Financial highlights, Consolidated results section of the MD&A for our revenues from operations by segment, for the years ended December 31, 2018 and 2017, which section of the MD&A is incorporated by reference herein.

The following is a description of each of TransCanada's three core businesses.

NATURAL GAS PIPELINES

Our natural gas pipeline network transports natural gas from supply basins to local distribution companies, power generation plants, industrial facilities, interconnecting pipelines and other businesses across Canada, the U.S. and Mexico.

In addition to our natural gas pipelines, we have regulated natural gas storage facilities in the U.S. with a total working gas capacity of 535 Bcf, making us one of the largest providers of natural gas storage and related services to key markets in North America. We also own and manage midstream assets that provide specific natural gas producer services including gathering, treatment, conditioning, processing and liquids handling with a focus on the Appalachian Basin.

Our Natural Gas Pipelines business is split into three operating segments representing its geographic diversity: Canadian Natural Gas Pipelines, U.S. Natural Gas Pipelines and Mexico Natural Gas Pipelines.

A description of the natural gas pipelines and regulated natural gas storage assets we operate in addition to further information about our pipeline holdings, developments and opportunities, significant regulatory developments and competitive position which relate to our Natural Gas Pipelines business can be found in the Natural Gas Pipelines Business, Canadian Natural Gas Pipelines, U.S. Natural Gas Pipelines and Mexico Natural Gas Pipelines sections of the MD&A, which sections of the MD&A are incorporated by reference herein.

LIQUIDS PIPELINES

Our existing liquids pipelines infrastructure connects Alberta crude oil supplies to U.S. refining markets in Illinois, Oklahoma and the U.S. Gulf Coast, as well as U.S. crude oil supplies from the key market hub at Cushing, Oklahoma to the U.S. Gulf Coast. We also provide intra-Alberta liquids transportation.

A description of pipelines and properties we operate, in addition to further information about our pipeline holdings, developments and opportunities, significant regulatory developments and competitive position which relate to our Liquids Pipelines business can be found in the MD&A in the Liquids Pipelines section, which section of the MD&A is incorporated by reference herein.

REGULATION OF NATURAL GAS PIPELINES AND LIQUIDS PIPELINES

Canada

Natural Gas Pipelines

The NGTL System, Canadian Mainline, and Foothills System (collectively, the Systems) are regulated by the NEB under the National Energy Board Act (Canada). The NEB regulates the construction and operation of facilities, and the terms and conditions of services, including rates, for these Canadian regulated natural gas transmission systems.

The NEB approves tolls and services that provide TransCanada the opportunity to recover costs of transporting natural gas, including the return of capital (depreciation) and return on the average investment base for each of the Systems. Generally, Canadian natural gas pipelines request the NEB to approve the pipeline’s cost of service and tolls once a year, and recover or refund the variance between actual and expected revenues and costs in future years.

The NGTL System is operating under a two-year settlement arrangement for 2018-2019 with an incentive agreement with shippers providing a 50/50 sharing mechanism for any variance between fixed and actual OM&A costs. Further information relating to the 2018-2019 Settlement can be found in the Natural Gas Pipelines – Developments in the Canadian Natural Gas Pipelines Segment section above and in the Canadian Natural Gas Pipelines – Significant Events, NGTL System section of the MD&A, which section of the MD&A is incorporated by reference herein.

16 | TransCanada Annual information form 2018 | |

The Canadian Mainline is entering the fifth year of a six-year fixed toll settlement that includes an incentive arrangement where it has discretion to price certain of its short-term services, such as interruptible transportation, at market prices. Settlements of this nature provide the pipeline an incentive to either decrease costs and/or increase revenues on the pipeline with a beneficial sharing mechanism to both the shippers and TransCanada. In December 2018, the NEB approved the 2018-2020 tolls application as filed, except for the amortization of the LTAA. Further information relating to the NEB 2018 Decision can be found in the Natural Gas Pipelines – Developments in the Canadian Natural Gas Pipelines Segment section above and in the Natural Gas Pipelines – Canadian Natural Gas Pipelines – Significant Events, Canadian Mainline section of the MD&A, which section of the MD&A is incorporated by reference herein.

New facilities on or associated with the Systems are approved by the NEB before construction begins and the NEB regulates the operations of each of the Systems. Net earnings of the Systems may be affected by changes in investment base, the allowed ROE, the level of deemed common equity and any incentive earnings.

West Coast LNG – Natural Gas Pipeline Project

The Coastal GasLink natural gas pipeline project is being proposed and developed primarily under the regulatory regime administered by the OGC and the BCEAO. The OGC is responsible for overseeing oil and gas operations in B.C., including exploration, development, pipeline transportation and reclamation. The BCEAO is an agency that manages the review of proposed major projects in B.C., as required by the B.C. Environmental Assessment Act.

Liquids Pipelines

The NEB regulates the terms and conditions of service, including rates, construction and operation of the Canadian portion of the Keystone Pipeline System. The rates for transportation service on the Keystone Pipeline System are calculated in accordance with a methodology agreed to in transportation service agreements between Keystone and its shippers, and approved by the NEB. The Northern Courier and Grand Rapids pipelines are regulated by the AER. The AER regulates the construction and operation of pipelines and associated facilities in Alberta.

Liquids Pipelines Projects

The White Spruce pipeline is under development and is primarily under the regulatory regime administered by the AER. The AER administers approvals required to construct and operate the pipelines and associated facilities in accordance with Directive 56, approvals to obtain land access under the Public Land Act and environmental approvals under the Environmental and Protection Enhancement Act.

United States

Natural Gas Pipelines

TransCanada is subject to regulation by various federal, state and local governmental agencies, including those specifically described below.

The Company's wholly owned and partially owned U.S. pipelines and natural gas storage facilities are natural gas companies subject to the jurisdiction of the FERC. The Natural Gas Act of 1938 grants the FERC authority over the construction, acquisition and operation of pipelines and related facilities utilized in the transportation and sale of natural gas in interstate commerce, including the extension, enlargement or abandonment of service using such facilities. The FERC also has authority to regulate rates and charges for transportation and storage of natural gas in interstate commerce. Pipeline safety is regulated by PHMSA. Natural gas pipelines that cross the international border between Canada and the U.S., such as the Great Lakes, GTN and Portland pipelines, require a Presidential Permit from the DOS.

Liquids Pipelines

The FERC regulates the terms and conditions of service, including transportation rates, of interstate liquids pipelines, including the U.S. portion of the Keystone Pipeline System and Marketlink. The siting and construction of pipeline facilities are regulated by the specific state regulator in which the pipeline facilities are located. Pipeline safety is regulated by PHMSA. Liquids pipelines that cross the international border between Canada and the U.S., such as the Keystone and Keystone XL pipelines, require a Presidential Permit from the DOS.

Mexico

Natural Gas Pipelines

TransCanada’s pipelines in Mexico are regulated by the Comisión Reguladora de Energía who approve construction of new pipeline facilities and ongoing operations of the infrastructure. Our Mexican pipelines have approved tariffs, services and related rates; however, the contracts underpinning the construction and operation of the facilities are long-term negotiated fixed rate contracts.

TransCanada Annual information form 2018 | 17 | |

These rates are only subject to change under specific circumstances such as certain types of force majeure events or changes in law.

ENERGY

Our Energy business consists of power generation and unregulated natural gas storage assets.

The power business includes approximately 6,600 MW of generation capacity that we currently either own or are developing. Our power generation assets are located in Alberta, Ontario, Québec, New Brunswick and Arizona, and are powered by natural gas and nuclear fuel sources. The majority of these assets are supported by long-term contracts.

We own and operate approximately 118 Bcf of unregulated natural gas storage capacity in Alberta and hold a contract with a third party for additional storage, in total accounting for approximately one-third of all storage capacity in the province.

On December 14, 2018, we entered into an agreement to sell our Coolidge Generating Station for approximately US$465 million.

Our U.S. power retail contracts were sold on March 1, 2018 as part of the continued wind-down of our U.S. Northeast power marketing business.

Further information about Energy assets we operate and Energy assets currently under construction, along with our Energy holdings and significant developments, and opportunities in relation to our Energy business, can be found in the MD&A in the Energy section, which section of the MD&A is incorporated by reference herein.

General

EMPLOYEES

At Year End, TransCanada's principal operating subsidiary, TCPL, had 7,081 employees, substantially all of whom were employed in Canada and the U.S., as set forth in the following table.

Calgary (includes U.S. employees working in Canada) | 2,646 | |

Western Canada (excluding Calgary) | 560 | |

Eastern Canada | 322 | |

Houston (includes Canadian employees working in the U.S.) | 801 | |

U.S. Midwest | 877 | |

U.S. Northeast | 257 | |

U.S. Southeast/ Gulf Coast (excluding Houston) | 1,240 | |

U.S. West Coast | 87 | |

Mexico | 291 | |

Total | 7,081 | |

CORPORATE RESTRUCTURING AND BUSINESS TRANSFORMATION

In mid-2015, we commenced a business restructuring and transformation initiative to reduce overall costs and maximize the effectiveness and efficiency of our existing operations. For more information about our corporate restructuring and business transformation, refer to the Corporate – Corporate restructuring and business transformation section of the MD&A, which section of the MD&A is incorporated by reference herein.

18 | TransCanada Annual information form 2018 | |

HEALTH, SAFETY, SUSTAINABILITY AND ENVIRONMENTAL PROTECTION AND SOCIAL POLICIES

The Board's Health, safety, sustainability and environment (HSSE) Committee oversees operational risk, people and process safety, security of personnel, environmental and climate-change related risks, and monitors development and the implementation of systems, programs and policies relating to HSSE matters through regular reporting from management. We use an integrated management system that establishes a framework for managing these risks and which is used to capture, organize, document, monitor and improve our related policies, programs and procedures.

Our management system is modeled after international standards, conforms to external industry consensus standards and voluntary programs, and complies with applicable legislative requirements. It follows a continuous improvement cycle organized into four key areas:

• | planning – risk and regulatory assessment, objective and target setting, defining roles and responsibilities |

• | implementing – development and implementation of programs, procedures and standards to manage operational risk |

• | reporting – incident reporting and investigation, and performance monitoring |

• | action – assurance activities and review of performance by management. |

The HSSE Committee reviews HSSE performance and operational risk management. It receives detailed reports on: