Exhibit 99.1

News Release

NORBORD REPORTS SECOND QUARTER 2017 RESULTS; INCREASES QUARTERLY DIVIDEND

Note: Financial references in US dollars unless otherwise indicated.

Q2 2017 HIGHLIGHTS

| • | Adjusted earnings of $1.10 per diluted share, more than double Q2 2016 |

| • | Adjusted EBITDA of $165 million, $71 million higher than Q2 2016 |

| • | North Central benchmark OSB price averaged $330 per Msf, up 25% from Q2 2016 |

| • | Capacity utilization at Norbord’s North American mills up 3% year-over-year |

| • | Repaid $61 million in temporary drawings on accounts receivable securitization program |

| • | Declared quarterly dividend of C $0.50 per share for shareholders of record on September 1, 2017 – an increase of C $0.20 |

TORONTO, ON (July 28, 2017) – Norbord Inc. (TSX and NYSE: OSB) today reported Adjusted EBITDA of $165 million for the second quarter of 2017 versus $94 million in the second quarter of 2016 and $103 million in the first quarter of 2017. The improvement is primarily due to higher North American oriented strand board (OSB) prices and shipment volumes. North American operations generated Adjusted EBITDA of $157 million compared to $85 million in the same quarter last year and $102 million in the prior quarter. European operations delivered Adjusted EBITDA of $9 million versus $11 million in the same quarter last year and $6 million in the prior quarter.

“Our second quarter Adjusted EBITDA result is our best since 2004,” said Peter Wijnbergen, Norbord’s President and CEO. “The improved operational performance of our North American mills resulted in lower manufacturing costs and higher shipments this quarter. OSB demand remains strong as US housing starts continue to recover and benchmark OSB prices are currently at multi-year highs.”

“In Europe, our financial performance is nearly back in line with its long-term quarterly trend despite the currency translation headwind from the weaker Pound Sterling and the negative impact of higher resin prices. Demand from our key UK and German markets remains strong and we expect the improvement in our European business to continue. Our project to modernize and expand the Inverness, Scotland OSB mill to serve this rapidly growing customer demand is well advanced and remains on track to begin production later this year.”

Norbord recorded Adjusted earnings of $95 million or $1.10 per share (basic and diluted) in the second quarter of 2017 versus $42 million or $0.49 per share (basic and diluted) in the second quarter of 2016 and $50 million or $0.58 per share (basic and diluted) in the first quarter of 2017. Adjusted earnings exclude non-recurring or other items and use a normalized income tax rate:

| $ millions |

Q2 2017 |

Q1 2017 |

Q2 2016 |

6 mos 2017 |

6 mos 2016 |

|||||||||||||||

| Earnings |

97 | 49 | 44 | 146 | 67 | |||||||||||||||

| Adjusted for: |

||||||||||||||||||||

| Loss on disposal of assets |

2 | 5 | — | 7 | — | |||||||||||||||

| Stock-based compensation and related costs |

1 | 1 | — | 2 | — | |||||||||||||||

| Costs to achieve merger synergies |

— | — | 2 | — | 3 | |||||||||||||||

| Costs related to High Level fire |

— | — | 1 | — | 1 | |||||||||||||||

| Reported income tax expense |

30 | 13 | 10 | 43 | 13 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted pre-tax earnings |

130 | 68 | 57 | 198 | 84 | |||||||||||||||

| Income tax expense at statutory rate |

(35 | ) | (18 | ) | (15 | ) | (53 | ) | (22 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted earnings |

95 | 50 | 42 | 145 | 62 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Market Conditions

In North America, year-to-date US housing starts were up 4% versus the same period in 2016. The seasonally adjusted annualized rate was 1.22 million in June, 2% higher than the pace this time last year, while the pace of permits (the more forward-looking indicator) was 1.25 million. Single-family starts, which use approximately three times more OSB than multi-family, increased by 8%. The consensus forecast from US housing economists stands at approximately 1.23 million starts in 2017, which suggests a 5% year-over-year improvement.

North American benchmark OSB prices improved significantly in the second quarter of 2017 as new home construction activity and OSB demand continue to improve. Benchmark OSB prices declined briefly in mid-May before recovering by the end of June, and the North Central benchmark OSB price averaged $330 per Msf (7/16-inch basis) for the quarter. The table below summarizes average benchmark OSB prices ($ per Msf, 7/16-inch basis) by region for the relevant quarters:

| North American region |

% of Norbord’s operating capacity |

Q2-2017 | Q1-2017 | Q2-2016 | ||||||||||||

| North Central |

16 | % | 330 | 293 | 264 | |||||||||||

| South East |

33 | % | 320 | 292 | 245 | |||||||||||

| Western Canada |

32 | % | 324 | 265 | 242 | |||||||||||

In Europe, Norbord’s core panel markets remained strong, with double-digit year-over-year OSB demand growth in both the UK and Germany. European panel prices in US dollar terms were impacted by the significant devaluation of the Pound Sterling following the Brexit referendum in June 2016. In local currency terms, OSB prices in the UK were up 11% from the same quarter last year and 4% versus the prior quarter. On the continent, OSB prices were 3% lower than the same quarter last year but improved 2% versus the prior quarter. UK medium density fibreboard (MDF) and particleboard prices were up 10% and 6% year-over-year and 1% and 4% quarter-over-quarter, respectively.

Performance

North American OSB shipments increased 3% year-over-year and 7% quarter-over-quarter due to increased mill productivity and fewer maintenance shuts than the first quarter. Approximately 25% of Norbord’s OSB sales volume went to specialty end-uses (industrial applications and export markets), which is solid progress toward the Company’s long-term goal of 50%. The improved mill productivity also increased capacity utilization versus both comparative periods. Norbord’s operating North American OSB mills produced at 99% of stated capacity (excluding the two curtailed mills in Huguley, Alabama and Chambord, Quebec), up from 96% in the same quarter last year and 94% in the prior quarter.

Norbord’s North American OSB cash production costs per unit (before mill profit share) decreased 7% compared to the prior quarter and increased 3% versus the same quarter last year. Quarter-over-quarter, costs decreased due to the timing of annual maintenance shuts and related costs as well as improved usages. The year-over-year increase was primarily due to higher resin prices.

In Europe, Norbord’s shipments were 3% higher than the same quarter last year and 1% lower than the prior quarter. The European mills produced at 105% of stated capacity in the quarter compared to 104% in the same quarter last year and 98% in the prior quarter. Capacity utilization increased primarily due to improved productivity, with fewer maintenance shuts also having some impact quarter-over-quarter.

Norbord’s mills did not generate any net Margin Improvement Program (MIP) gains in the first half of 2017 due to the timing and scope of annual maintenance shuts and related costs taken earlier in the year.

The Company’s $135 million modernization and expansion of its Inverness, Scotland OSB mill remains on budget and on track to start up in the second half of 2017, with no disruption to existing production volumes in the interim. Capital spending of $24 million was incurred during the quarter ($55 million year-to-date), bringing the total project spending to-date to $88 million.

All other capital and intangible investments (excluding the Inverness project) were $34 million in the second quarter and $63 million year-to-date. Norbord’s 2017 regular capital expenditure budget is $120 million (excluding the Inverness project) which includes manufacturing cost reduction and productivity improvement projects across the mills as well as the remaining $30 million to prepare the Huguley mill for restart. Year-to-date, $23 million has been spent on the Huguley restart project. Norbord currently expects to restart the Huguley mill no earlier than the fourth quarter of 2017 and achieve a normal run rate in the first quarter of 2018 in order to meet anticipated customer demand next year. In addition, the Company expects to invest most of the remaining $47 million budgeted to complete the Inverness project in 2017.

Operating working capital was $181 million at quarter-end compared to $163 million at the end of the same quarter last year and $171 million at the end of the prior quarter. Working capital increased versus both comparative periods due to higher North American OSB shipments and prices. Quarter-over-quarter, this was partially offset by lower inventory due to the seasonal log inventory drawdown at the northern mills. The year-over-year increase was also driven by better weather conditions for building seasonal log inventories at the northern mills this year, higher incentive program accruals and higher accrued capital expenditures related to the Inverness project. Working capital continues to be managed at minimal levels across the Company.

At year-end, Norbord had unutilized liquidity of $358 million, consisting of $7 million in cash and $351 million in unused credit lines. During the quarter, the Company repaid the $61 million in temporary drawings on its accounts receivable securitization program. The Company’s tangible net worth was $1,028 million and net debt to total capitalization on a book basis was 36%, with both ratios well within bank covenants.

Developments

As previously announced in June, the Quebec Minister of Forests, Wildlife and Parks has granted Norbord a wood allocation for its curtailed Chambord, Quebec mill that will take effect on April 1, 2018. Norbord does not currently have plans to restart Chambord, but will continue to monitor market conditions.

On July 10th, Norbord announced that its OSB mill in 100 Mile House, British Columbia had temporarily suspended production due to wild fires burning nearby in the region and in order to comply with evacuation orders. The mill resumed operation approximately two weeks later. The curtailment is not expected to materially impact Norbord’s third quarter results.

Dividend

The Board of Directors declared a quarterly dividend of C $0.50 per common share, payable on September 21, 2017 to shareholders of record on September 1, 2017. This is a C $0.20 per common share or 67% increase over last quarter’s level. The increase reflects the strength in North American benchmark OSB prices this year and resulting robust operating cash flow for the Company, the positive market outlook for the Company’s products and the continuing expectation that free cash flow will be sufficient to fund current growth and other attractive capital investment commitments for the foreseeable future. Any dividends reinvested under the Company’s Dividend Reinvestment Plan will be used by the transfer agent to purchase common shares from Norbord’s treasury (see Amended and Restated Dividend Reinvestment Plan below).

Norbord’s dividends are declared in Canadian dollars. Registered and beneficial shareholders may opt to receive their dividends in either Canadian dollars or the US dollar equivalent. Unless they request the US dollar equivalent, shareholders will continue to receive dividends in Canadian dollars. The US dollar equivalent of the dividend will be based on the Bloomberg FX Fixings Service (BFIX) noon exchange rate on the record date or, if the record date falls on a weekend or holiday, on the BFIX noon exchange rate of the preceding business day.

Registered shareholders wishing to receive the US dollar dividend equivalent should contact Norbord’s transfer agent, AST Trust Company (Canada), by phone at 1-800-387-0825 or by email at inquiries@canstockta.com. Beneficial shareholders (i.e., those holding their Norbord shares with their brokerage) should contact the broker with whom their shares are held.

Norbord’s variable dividend policy targets the payment to shareholders of a portion of free cash flow based upon the Company’s financial position, results of operations, cash flow, capital requirements and restrictions under the Company’s revolving bank lines, as well as the market outlook for the Company’s principal products and broader market and economic conditions, among other factors. The Board retains the discretion to amend the Company’s dividend policy in any manner and at any time as it may deem necessary or appropriate in the future. For these reasons, as well as others, the Board in its sole discretion can decide to increase, maintain, decrease, suspend or discontinue the payment of cash dividends in the future.

Amended and Restated Dividend Reinvestment Plan

Norbord also announced today that the Board of Directors has approved amendments to its dividend reinvestment plan (the Plan), previously only available to residents of Canada, to enable shareholders who are residents of the United States to participate in the Plan. The Plan allows participants in Canada and the United States to reinvest cash dividends paid on their common shares (Shares) to purchase additional Shares. The Plan was also amended to allow Norbord the flexibility to purchase such additional Shares on the open market or issue them from treasury. These amendments will be effective upon Norbord filing a registration statement on Form F-3 relating to the Plan (the Registration Statement) with the US Securities and Exchange Commission, which it currently expects to do prior to September 1, 2017, and will be applicable to Norbord’s dividend payable on September 21, 2017.

On each dividend payment date, cash dividends payable on a participant’s Shares are paid by Norbord to AST Trust Company (Canada), Norbord’s registrar and transfer agent which serves as agent under the Plan (the Plan Agent). The Plan Agent uses those funds (less any applicable withholding taxes) to

purchase Shares. The Shares acquired by the Plan Agent under the Plan will be, at Norbord’s election, either (i) newly issued Shares from Norbord’s treasury at a price equal to the volume-weighted average price of the Shares on the TSX or the NYSE, as directed by Norbord from time to time, for the five (5) trading days preceding the relevant dividend payment date, or (ii) Shares purchased on either the TSX or the NYSE, at the direction of Norbord from time to time, at a price equal to the average price paid per Share on the open market by the Plan Agent.

Enrollment in the Plan is optional. Eligible shareholders may elect to reinvest 25%, 50%, 75% or 100% of the cash dividend paid on their Shares. No action is required of participants currently enrolled in the Plan who do not wish to change their current election. Registered holders of Shares may enroll in the Plan following filing of the Registration Statement by enrolling online through the Plan Agent’s self-service web portal as identified from time to time by the Plan Agent or by downloading the Enrollment Form from https://www.canstockta.com/en/InvestorServices/Investor_Information/Issuer_List/IssuerDetail.jsp?companyCode=5098 and duly completing and delivering it to the Plan Agent. Beneficial shareholders should make appropriate arrangements with their broker, investment dealer, financial institution or other nominee.

Shareholders whose Shares are registered in the name of The Depository Trust Company (DTC), may participate in the Plan only by (i) directing his or her broker to transfer all or any number of whole Shares into his or her name and then enrolling such Shares in the Plan or (ii) making appropriate arrangements with the broker, investment dealer, financial institution or other nominee who holds such Shares to transfer all or any number of whole Shares into CDS Clearing and Depository Services Inc. (CDS) and enroll in the Plan on the shareholder’s behalf, either as a nominee that delivers a completed and executed enrollment form to the Plan Agent in the manner provided in the Plan, or, if applicable, as a CDS participant through enrollment by CDS.

Information on the Plan will be accessible on the Plan Agent’s website at www.canstockta.com or on Norbord’s website at http://www.norbord.com/investors/shareholder-information/dividends following the filing of the Registration Statement.

This press release does not constitute an offer to sell or the solicitation of an offer to buy any of the Shares, nor will there be any distribution of the Shares in any jurisdiction in which such distribution would be unlawful. Any distribution of the Shares to US participants will be made only by means of the prospectus and the related registration statement. Norbord anticipates filing the Registration Statement with the US Securities and Exchange Commission prior to September 1, 2017. These Shares may not be sold nor may offers to buy be accepted in the United States prior to the time the registration statement becomes effective. After filing, copies of the registration statement may be obtained under Norbord’s profile on EDGAR at www.sec.gov. You may also obtain copies of such documents from Norbord by writing to the Corporate Secretary, at 1 Toronto Street, Suite 600, Toronto, Ontario, M5C 2W4.

Additional Information

Norbord’s Q2 2017 letter to shareholders, news release, management’s discussion and analysis, consolidated unaudited interim financial statements and notes to the financial statements have been filed on SEDAR (www.sedar.com), EDGAR (www.sec.gov) and are available in the investor section of the Company’s website at www.norbord.com. Shareholders may receive a hard copy of Norbord’s audited annual financial statements free of charge upon request. The Company has also made available on its website presentation materials containing certain historical and forward-looking information relating to Norbord, including materials that contain additional information about the Company’s financial results. Shareholders are encouraged to read this material.

Conference Call

Norbord will hold a conference call for analysts and institutional investors on Friday, July 28, 2017 at 11:00 a.m. ET. The call will be broadcast live over the internet via www.norbord.com and www.newswire.ca. An accompanying presentation will be available in the “Investors/Conference Call” section of the Norbord website prior to the start of the call. A replay number will be available approximately one hour after completion of the call and will be accessible until August 27, 2017 by dialing 1-888-203-1112 or 647-436-0148 (passcode 1063562 and pin 9184). Audio playback and a written transcript will be available on the Norbord website.

Norbord Profile

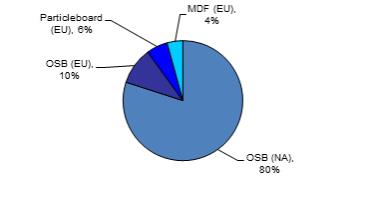

Norbord Inc. is a leading global manufacturer of wood-based panels and the world’s largest producer of oriented strand board (OSB). In addition to OSB, Norbord manufactures particleboard, medium density fibreboard and related value-added products. Norbord has assets of approximately $1.8 billion and employs approximately 2,600 people at 17 plant locations in the United States, Canada and Europe. Norbord is a publicly traded company listed on the Toronto Stock Exchange and New York Stock Exchange under the symbol “OSB”.

-end-

Contact:

Heather Colpitts

Senior Manager, Corporate Affairs

Tel. (416) 365-0705

info@norbord.com

This news release contains forward-looking statements, as defined by applicable securities legislation, including statements related to our strategy, projects, plans, future financial or operating performance and other statements that express management’s expectations or estimates of future performance. Often, but not always, forward-looking statements can be identified by the use of words such as “set up,” “on track,” “expect,” “estimate,” “forecast,” “target,” “outlook,” “schedule,” “represent,” “continue,” “intend,” “should,” “would,” “could,” “will,” “can,” “might,” “may,” and other expressions which are predictions of or indicate future events, trends or prospects and which do not relate to historical matters identify forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Norbord to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

Although Norbord believes it has a reasonable basis for making these forward-looking statements, readers are cautioned not to place undue reliance on such forward-looking information. By its nature, forward-looking information involves numerous assumptions, inherent risks and uncertainties, both general and specific, which contribute to the possibility that the predictions, forecasts and other forward-looking statements will not occur. Factors that could cause actual results to differ materially from those contemplated or implied by forward-looking statements include: assumptions in connection with the economic and financial conditions in the US, Europe, Canada and globally; risks inherent to product concentration and cyclicality; effects of competition and product pricing pressures; risks inherent to customer dependence; effects of variations in the price and availability of manufacturing inputs, including continued access to fibre resources at competitive prices; availability of rail services and port facilities; various events that could disrupt operations, including natural or catastrophic events and ongoing relations with employees; impact of changes to, or non-compliance with, environmental regulations; impact of any product liability claims in excess of insurance coverage; risks inherent to a capital intensive industry; impact of future outcomes of tax exposures; potential future changes in tax laws; effects of currency exposures and exchange rate fluctuations; future operating costs, availability of financing, impact of future cross-border trade rulings or agreements; ability to implement new or upgraded information technology infrastructure; impact of information technology service disruptions or failures; and other risks and factors described from time to time in filings with Canadian securities regulatory authorities.

Except as required by applicable law, Norbord does not undertake to update any forward-looking statements, whether written or oral, that may be made from time to time by, or on behalf of, the Company, whether as a result of new information, future events or otherwise, or to publicly update or revise the above list of factors affecting this information. See the “Caution Regarding Forward-Looking Information” statement in the February 2, 2017 Annual Information Form and the cautionary statement contained in the “Forward-Looking Statements” section of the 2016 Management’s Discussion and Analysis dated February 2, 2017 and Q2 2017 Management’s Discussion and Analysis dated July 27, 2017.

Norbord defines Adjusted EBITDA as earnings determined in accordance with International Financial Reporting Standards (IFRS) before finance costs, income taxes, depreciation and amortization, non-recurring or other items, and Adjusted earnings as earnings determined in accordance with IFRS before non-recurring or other items and using a normalized income tax rate, and Adjusted earnings per share is Adjusted earnings divided by the weighted average number of common shares outstanding. Adjusted EBITDA, Adjusted earnings, and Adjusted earnings per share are non-IFRS financial measures, do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other companies. See “Non-IFRS Financial Measures” in Norbord’s 2016 Management’s Discussion and Analysis dated February 2, 2017 and Q2 2017 Management’s Discussion and Analysis dated July 27, 2017 for a quantitative reconciliation of Adjusted EBITDA, Adjusted earnings, and Adjusted earnings per share to earnings (the most directly comparable IFRS measure).

Peter Wijnbergen

President & CEO

July 28, 2017

To Our Shareholders:

I am delighted to report our best quarterly earnings since 2004 that reflect robust markets for our OSB products in North America and Europe, combined with growing demand from our customers in Asia. Adjusted EBITDA came in at $165 million and our Adjusted earnings were $1.10 per diluted share.

In North America, with the winter season maintenance efforts behind us, our operational performance moved back in line with our strong track record. Our improved productivity and shipments coincided with North Central benchmark prices that were 27% higher year-to-date. So far this year, 95% of our volume growth has been directed to our specialty and housing value-added products sales. Our specialty sales currently represent approximately 25% of our total volume and we are pleased to see solid progress toward our long-term goal of 50%. Demand from all our end-use customer segments remains strong, reflecting the continued favourable market conditions for home builders and the broader economy.

In Europe, sales volume increased over the prior quarter, and Adjusted EBITDA moved back to within $1 million of its long-term quarterly trend despite significantly higher resin prices and the ongoing currency translation headwind. OSB demand continues to see double-digit year-over-year growth in both the UK and Germany. With healthy order files and an encouraging sales outlook, we expect our European financial performance will continue to improve.

Our strong operating performance also translated into strong cash flow. As anticipated, we completely paid down the $61 million A/R securitization drawing during the quarter, which served as a temporary bridge when we paid off $200 million in bond debt earlier this year. We finished the quarter with cash on our balance sheet and over $350 million in liquidity.

During the quarter, we also made good progress on a number of our strategic projects.

The expansion of our mill in Inverness, Scotland is well advanced and the major equipment is now being commissioned. This project is on budget and remains on target to begin production later this year. Once operational, the incremental volume from the Inverness mill will help us serve rapidly growing European customer demand.

Last quarter, we announced the decision to invest the remaining capital required to prepare our Huguley, Alabama mill for restart, and the majority of that investment has now been completed. With customers continuing to indicate strong and growing demand for Norbord OSB, we believe that additional production will be required and will be of immediate strategic value to our Company. We continue to be guided by our strategy to produce only what we can sell. Our current thinking would have us restart Huguley no earlier than Q4 and achieve a normal run rate in Q1 in order to meet anticipated customer demand next year.

In June, we secured a wood allocation for our curtailed mill in Chambord, Quebec. As we consider the potential for restarting production at the mill, the government wood allocation is a critical first step, and we are pleased to have secured this within just eight months of acquiring the mill. The agreement represents an optimal allotment for our purposes, and reflects the productive relations we have maintained with the provincial government through our work in both La Sarre and Chambord. We believe improving market conditions will support an eventual restart of the Chambord mill, and we are engaging with the local union leadership and undertaking detailed engineering work as part of our planning.

Looking ahead, I am very optimistic about the remainder of 2017. In Europe, the negative impact of resin cost escalation appears to have peaked and should retreat somewhat in the second half of the year. In North America, benchmark OSB prices are at multi-year highs and we expect robust OSB market conditions to persist as the US housing market strengthens and demand continues to expand beyond traditional end-uses. Our balance sheet continues to improve as we generate cash and due to the permanent deleveraging we undertook earlier this year. Reflecting our strong balance sheet and cash flow and this very positive outlook, our Board has increased our quarterly dividend to C $0.50 per share, representing the second increase since we implemented our variable dividend policy in 2013.

Finally, as already reported, we were forced to temporarily suspend production at our mill in 100 Mile House, British Columbia in early July as a result of wildfires in the region and resulting evacuation orders. The mill is now operating again and the curtailment is not expected to materially impact our Q3 results. Our thoughts are with those in the BC interior who have been and continue to be affected by the fires. I would like to thank our employees in 100 Mile House for their tireless efforts to safeguard the mill and contribute to the community response.

This letter includes forward-looking statements, as defined by applicable securities legislation including statements related to our strategy, projects, plans, future financial or operating performance, market outlook, and other statements that express management’s expectations or estimates of future performance. Often, but not always, forward-looking statements can be identified by the use of words such as “expect,” “suggest,” “support,” “believe,” “should,” “potential,” “likely,” “continue,” “forecast,” “plan,” “indicate,” “consider,” “future,” or variations of such words and phrases or statements that certain actions “may,” “could,” “must,” “would,” “might,” or “will” be undertaken, occur or be achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of Norbord to be materially different from any future results, performance or achievement expressed or implied by the forward-looking statements. See the cautionary language in the Forward-Looking Statements section of the 2016 Management’s Discussion and Analysis dated February 2, 2017 and Q2 2017 Management’s Discussion and Analysis dated July 27, 2017.

Norbord defines Adjusted EBITDA as earnings determined in accordance with International Financial Reporting Standards (IFRS) before finance costs, income taxes, depreciation and amortization, and non-recurring or other items, Adjusted earnings as earnings determined in accordance with IFRS before non-recurring or other items and using a normalized income tax rate, and Adjusted earnings per share as Adjusted earnings divided by the weighted average number of common shares outstanding. Adjusted EBITDA, Adjusted earnings, and Adjusted earnings per share are non-IFRS financial measures, do not have any standardized meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other companies. See the Non-IFRS Financial Measures section in Norbord’s Q2 2017 Management’s Discussion and Analysis dated July 27, 2017 for a quantitative reconciliation of Adjusted EBITDA, Adjusted earnings, and Adjusted earnings per share to earnings (the most directly comparable IFRS measure).

Interim Consolidated Balance Sheets

| (Unaudited) (US $ millions) |

Jul 1, 2017 | Dec 31, 2016 | ||||||

| Assets |

||||||||

| Current assets |

||||||||

| Cash and cash equivalents |

$ | 7 | $ | 161 | ||||

| Accounts receivable |

184 | 141 | ||||||

| Taxes receivable |

1 | — | ||||||

| Investment tax credit receivable |

5 | — | ||||||

| Inventory |

206 | 185 | ||||||

| Prepaids |

7 | 10 | ||||||

|

|

|

|

|

|||||

| 410 | 497 | |||||||

| Non-current assets |

||||||||

| Property, plant and equipment |

1,330 | 1,262 | ||||||

| Intangible assets |

24 | 22 | ||||||

| Deferred income tax assets |

5 | 4 | ||||||

| Other assets |

3 | 14 | ||||||

|

|

|

|

|

|||||

| 1,362 | 1,302 | |||||||

|

|

|

|

|

|||||

| $ | 1,772 | $ | 1,799 | |||||

|

|

|

|

|

|||||

| Liabilities and shareholders’ equity |

||||||||

| Current liabilities |

||||||||

| Accounts payable and accrued liabilities |

$ | 216 | $ | 218 | ||||

| Taxes payable |

7 | 1 | ||||||

| Current portion of long-term debt |

— | 200 | ||||||

|

|

|

|

|

|||||

| 223 | 419 | |||||||

| Non-current liabilities |

||||||||

| Long-term debt |

547 | 546 | ||||||

| Other liabilities |

33 | 27 | ||||||

| Deferred income tax liabilities |

185 | 157 | ||||||

|

|

|

|

|

|||||

| 765 | 730 | |||||||

|

|

|

|

|

|||||

| Shareholders’ equity |

784 | 650 | ||||||

|

|

|

|

|

|||||

| $ | 1,772 | $ | 1,799 | |||||

|

|

|

|

|

|||||

Interim Consolidated Statements of Earnings

| (Unaudited) Periods ended Jul 1 and Jun 25 (US $ millions, except per share information) |

Q2 2017 | Q2 2016 | 6 mos 2017 | 6 mos 2016 | ||||||||||||

| Sales |

$ | 536 | $ | 447 | $ | 1,003 | $ | 831 | ||||||||

| Cost of sales |

(370 | ) | (353 | ) | (729 | ) | (675 | ) | ||||||||

| General and administrative expenses |

(2 | ) | (3 | ) | (8 | ) | (5 | ) | ||||||||

| Depreciation and amortization |

(27 | ) | (24 | ) | (51 | ) | (45 | ) | ||||||||

| Loss on disposal of assets |

(2 | ) | — | (7 | ) | — | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

135 | 67 | 208 | 106 | ||||||||||||

| Non-operating expense: |

||||||||||||||||

| Finance costs |

(8 | ) | (13 | ) | (19 | ) | (26 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings before income tax |

127 | 54 | 189 | 80 | ||||||||||||

| Income tax expense |

(30 | ) | (10 | ) | (43 | ) | (13 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings |

$ | 97 | $ | 44 | $ | 146 | $ | 67 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings per common share |

||||||||||||||||

| Basic |

$ | 1.13 | $ | 0.51 | $ | 1.70 | $ | 0.78 | ||||||||

| Diluted |

1.12 | 0.51 | 1.69 | 0.78 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Interim Consolidated Statements of Comprehensive Income

| (Unaudited) Periods ended Jul 1 and Jun 25 (US $ millions) |

Q2 2017 | Q2 2016 | 6 mos 2017 | 6 mos 2016 | ||||||||||||

| Earnings |

$ | 97 | $ | 44 | $ | 146 | $ | 67 | ||||||||

| Other comprehensive (loss) income, net of tax |

||||||||||||||||

| Items that will not be reclassified to earnings: |

||||||||||||||||

| Actuarial loss on post-employment obligation |

(3 | ) | (8 | ) | (6 | ) | (12 | ) | ||||||||

| Items that may be reclassified subsequently to earnings: |

||||||||||||||||

| Foreign currency translation gain (loss) on foreign operations |

12 | (6 | ) | 17 | (11 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other comprehensive income (loss), net of tax |

9 | (14 | ) | 11 | (23 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income |

$ | 106 | $ | 30 | $ | 157 | $ | 44 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Interim Consolidated Statements of Changes in Shareholders’ Equity

| (Unaudited) Periods ended Jul 1 and Jun 25 (US $ millions) |

Q2 2017 | Q2 2016 | 6 mos 2017 | 6 mos 2016 | ||||||||||||

| Share capital |

||||||||||||||||

| Balance, beginning of period |

$ | 1,345 | $ | 1,335 | $ | 1,341 | $ | 1,334 | ||||||||

| Issue of common shares upon exercise of options and Dividend Reinvestment Plan |

— | 2 | 4 | 3 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance, end of period |

$ | 1,345 | $ | 1,337 | $ | 1,345 | $ | 1,337 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Merger reserve |

$ | (96 | ) | $ | (96 | ) | $ | (96 | ) | $ | (96 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Contributed surplus |

||||||||||||||||

| Balance, beginning of period |

$ | 8 | $ | 10 | $ | 9 | $ | 10 | ||||||||

| Stock options exercised |

— | — | (1 | ) | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance, end of period |

$ | 8 | $ | 10 | $ | 8 | $ | 10 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Retained deficit |

||||||||||||||||

| Balance, beginning of period |

$ | (359 | ) | $ | (543 | ) | $ | (402 | ) | $ | (559 | ) | ||||

| Earnings |

97 | 44 | 146 | 67 | ||||||||||||

| Common share dividends |

(20 | ) | (6 | ) | (26 | ) | (13 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance, end of period(i) |

$ | (282 | ) | $ | (505 | ) | $ | (282 | ) | $ | (505 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Accumulated other comprehensive loss |

||||||||||||||||

| Balance, beginning of period |

$ | (200 | ) | $ | (179 | ) | $ | (202 | ) | $ | (170 | ) | ||||

| Other comprehensive income (loss) |

9 | (14 | ) | 11 | (23 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance, end of period |

$ | (191 | ) | $ | (193 | ) | $ | (191 | ) | $ | (193 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Shareholders’ equity |

$ | 784 | $ | 553 | $ | 784 | $ | 553 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

(i) Retained deficit comprises: |

||||||||||||||||

| Deficit arising on cashless exercise of warrants in 2013 |

$ | (263 | ) | $ | (263 | ) | ||||||||||

| All other retained deficit |

(19 | ) | (242 | ) | ||||||||||||

|

|

|

|

|

|||||||||||||

| $ | (282 | ) | $ | (505 | ) | |||||||||||

Interim Consolidated Statements of Cash Flows

| (Unaudited) Periods ended Jul 1 and Jun 25 (US $ millions) |

Q2 2017 | Q2 2016 | 6 mos 2017 | 6 mos 2016 | ||||||||||||

| CASH PROVIDED BY (USED FOR): |

||||||||||||||||

| Operating activities |

||||||||||||||||

| Earnings |

$ | 97 | $ | 44 | $ | 146 | $ | 67 | ||||||||

| Items not affecting cash: |

||||||||||||||||

| Depreciation and amortization |

27 | 24 | 51 | 45 | ||||||||||||

| Deferred income tax |

12 | 8 | 25 | 10 | ||||||||||||

| Loss on disposal of assets |

2 | — | 7 | — | ||||||||||||

| Other items |

(10 | ) | (3 | ) | (4 | ) | 3 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 128 | 73 | 225 | 125 | |||||||||||||

| Net change in non-cash operating working capital balances |

2 | 10 | (55 | ) | (40 | ) | ||||||||||

| Net change in taxes receivable and investment tax credit receivable |

14 | — | 13 | 1 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 144 | 83 | 183 | 86 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Investing activities |

||||||||||||||||

| Investment in property, plant and equipment |

(62 | ) | (21 | ) | (118 | ) | (34 | ) | ||||||||

| Investment in intangible assets |

(1 | ) | (2 | ) | (3 | ) | (3 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (63 | ) | (23 | ) | (121 | ) | (37 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Financing activities |

||||||||||||||||

| Common share dividends paid |

(19 | ) | (7 | ) | (25 | ) | (13 | ) | ||||||||

| Accounts receivable securitization repayments, net |

(61 | ) | (55 | ) | — | (30 | ) | |||||||||

| Issue of common shares |

— | 2 | 3 | 2 | ||||||||||||

| Bank advances |

(2 | ) | — | — | — | |||||||||||

| Repayment of debt |

— | — | (200 | ) | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (82 | ) | (60 | ) | (222 | ) | (41 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Foreign exchange revaluation on cash and cash equivalents held |

8 | (2 | ) | 6 | (5 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cash and cash equivalents |

||||||||||||||||

| Increase (decrease) during period |

7 | (2 | ) | (154 | ) | 3 | ||||||||||

| Balance, beginning of period |

— | 14 | 161 | 9 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance, end of period |

$ | 7 | $ | 12 | $ | 7 | $ | 12 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||