UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2020

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____ to ______

Commission File Number: 0-24012

DEEP WELL OIL & GAS, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 98-0501168 | |

| (State

or other jurisdiction of incorporation or organization) |

(I.R.S.

Employer Identification No.) | |

| Suite 700, 10150 – 100 Street, Edmonton, Alberta, Canada | T5J 0P6 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (780) 409-8144

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name

of each exchange on which registered | ||

| None | None | None |

Securities registered pursuant to Section 12(g) of the Act:

| Common Stock, $0.001 par value per share |

| (Title of class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No þ

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☐ No þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ | Smaller reporting company þ |

| Emerging growth company þ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

The aggregate market value of the registrant’s common stock held by non-affiliates computed by reference to the price at which the common equity was sold on or about March 31, 2020 was approximately $1.7 million.

As of September 25, 2021, the Issuer had outstanding approximately 229,374,605 shares of common stock, $0.001 par value per share.

TABLE OF CONTENTS

i

The following are defined terms and abbreviations used herein:

API Gravity – a specific gravity scale developed by the American Petroleum Institute for measuring the density or specific gravity (heaviness) of petroleum liquids, expressed in degrees. The higher the number, the lighter the oil.

Alberta Energy Regulator (“AER” formerly “ERCB”) – The AER is responsible for the development of Alberta’s oil (including oil sands) and gas resources. The AER succeeded the Energy Resources Conservation Board (“ERCB”) and will take on regulatory functions from the Ministry of Environment and Sustainable Resource Development that relate to public lands, water, and the environment. The AER will provide full-lifecycle regulatory oversight of energy resource development in Alberta from application and construction to abandonment and reclamation, and everything in between.

Barrel – the common unit for measuring petroleum, including heavy oil. One barrel contains approximately 159 L.

Battery – equipment to process or store crude oil from one or more wells.

Bbl or Bbls – means barrel or barrels.

Bitumen – a heavy, viscous form of crude oil that generally has an API gravity of less than 10 degrees.

Cdn$ or Cdn dollar – means Canadian dollars.

Celsius – a temperature scale that registers the freezing point of water as 0 degrees and the boiling point as 100 degrees under normal atmospheric pressure. Room temperature is between 20 degrees and 25 degrees Celsius. Temperatures specified herein are quoted in degrees Celsius unless indicated otherwise.

Cold Flow – a production technique where the oil is simply pumped out of the sands not using a Thermal Recovery Technique.

Conventional Crude Oil – crude oil that flows naturally or that can be pumped without being heated or diluted.

Core – a cylindrical rock sample taken from a formation for geological analysis.

Crude Oil – oil that has not undergone any refining. Crude oil is a mixture of hydrocarbons with small quantities of other chemicals such as sulphur, nitrogen and oxygen. Crude oil varies radically in its properties, namely specific gravity and viscosity.

Cyclic Steam Stimulation (“CSS”) or Horizontal Cyclic Steam Stimulation (“HCSS”) – a thermal in situ recovery method, which consists of a three-stage process involving high-pressure steam injected into the formation for several weeks through vertical or horizontal wells. The heat softens the oil while the water vapor helps to dilute and separate the oil from the sand grains. The pressure also creates channels through which the oil can flow more easily to the well. When a portion of the reservoir is thoroughly saturated, the steam is turned off and the reservoir maybe left to “soak” a short period of time. This is followed by the production phase, when the oil flows, or is pumped, up the same wells to the surface. When production rates decline, another cycle of steam injection begins. This process is sometimes called “huff-and-puff” recovery and can be done utilizing vertical or horizontal wells.

Darcy (Darcies) – a measure of rock permeability (the degree to which natural gas or crude oil can move through the rocks).

Density – the heaviness of crude oil, indicating the proportion of large, carbon-rich molecules, generally measured in kilograms per cubic metre (“kg/m3”) or degrees on the American Petroleum Institute (“API”) scale.

Development Well – a well drilled within an area of a natural gas or oil reservoir to the depth of a stratigraphic horizon to which proven reserves have been assigned.

Diluents – light petroleum liquids used to dilute bitumen and heavy oil so they can flow through pipelines.

Drill Stem Test (“DST”) – a method of formation testing. The basic drill stem test tool consists of a packer or packers, valves or ports that may be opened and closed from the surface, and two or more pressure-recording devices. The tool is lowered on the drill string to the zone to be tested. The packer or packers are set to isolate and test the zone from the drilling fluid column.

Drill String – the column, or string, of drill pipe with attached tool joints that transmits fluid and rotational power from the drilling rig on the surface to the drill collars and the bit. Often, the term is loosely applied to include both drill pipe and drill collars.

Enhanced Oil Recovery – any method that increases oil production by using techniques or materials that are not part of normal pressure maintenance or water flooding operations. For example, natural gas can be injected into a reservoir to “enhance” or increase oil production.

ii

Exploratory Well – a well drilled to find and produce natural gas or oil in an unproven area, to find a new reservoir in a field previously found to be productive of natural gas or oil in another reservoir, or to extend a known reservoir.

Farmout – an arrangement whereby the owner of a lease assigns some ownership portion (or all) of the lease(s) to another company (the “Farmee”) in return for the Farmee paying for the drilling on at least some portion of the lease(s) under the Farmout.

Gross Acre/Hectare – a gross acre is an acre in which any portion of a working interest is owned. 1 acre = 0.4046 hectares. 1 hectare = 2.471 acres.

Heavy Oil – oil having an API gravity less than 22.3 degrees.

Horizontal Well – the drilling of a well that deviates from the vertical and travels horizontally through a producing layer of a reservoir.

In-situ – in the oil sands context (in-situ means “in place” in Latin), in-situ methods such as SAGD or CSS through horizontal or vertical wells maybe required to produce the oil if the oil sands deposits are too deep to mine from the surface.

Lease – a legal document giving an operator the right to drill for or produce oil or gas; also, the land on which a lease has been obtained.

License of Occupation (“LOC”) – a surface crown agreement issued by the Alberta Department of Sustainable Resources Development granting the mineral producer the right to occupy public lands for an approved purpose, usually issued primarily for access roads or to construct access roads but may also be issued for other purposes.

Light Crude Oil – liquid petroleum which has a low density and flows freely at room temperature. Also called conventional oil, it has an API gravity of at least 22 degrees and a viscosity less than 100 centipoise.

Mbbl or Mbbls – means one thousand barrels or thousands of barrels.

MMbbl or MMbbls – means one million barrels or millions of barrels.

Mmcf – means million cubic feet.

Mineral Surface Lease (“MSL”) – a surface crown agreement issued by the Alberta Department of Sustainable Resources Development granting the mineral producer the right to construct a well site on publicly owned land.

Net Acre/Hectare – a net acre is the result that is obtained when the fractional ownership working interest of a lease is multiplied by gross acres of that lease.

Oil Sands – naturally occurring mixtures of bitumen, water, sand and clay that are found mainly in three areas of Alberta - Athabasca, Peace River and Cold Lake. A typical sample of oil sand might contain about 12% bitumen by weight.

Pay Zone (Net Oil Pay) – the producing part of a formation.

Permeability – the capacity of a reservoir rock to transmit fluids; or how easily fluids can pass through a rock. The unit of measurement is the darcy or millidarcy.

Porosity – the capacity of a reservoir to store fluids, the volume of the pore space within a reservoir, measured as a percentage.

Possible Reserves * – additional unproved reserves that analysis of geological and engineering data suggests are less likely to be recoverable than probable reserves but have at least a ten percent probability of being recovered.

Primary Recovery – the production of oil and gas from reservoirs using the natural energy available in the reservoirs and pumping techniques.

Proved Developed Reserves * – are those reserves that can be expected to be recovered.

Probable Reserves * – additional reserves that are less certain to be recovered than proved reserves but which, together with proved reserves, are as likely as not to be recovered.

iii

Proved Reserves * – estimated quantities of crude oil, natural gas, and natural gas liquids which geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic, operating methods, and government regulations prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time.

Proved Undeveloped Reserves * – are those reserves that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion.

Saturation – the relative amount of water, oil, and gas in the pores of a rock, usually as a percentage of volume.

SEC – means United States Securities and Exchange Commission.

Section – in reference to a parcel of land, meaning an area of land comprising approximately 640 acres.

Service Well – a well drilled or completed for the purpose of supporting production in an existing field. Specific purposes of service wells include gas injection, water injection, steam injection, air injection, salt-water disposal, water supply for injection, observation, or injection for in-situ combustion.

Solution Gas – natural gas that is found “in solution” within crude oil in underground reservoirs. When the oil comes to the surface, the gas expands and comes out of the solution.

Specific Gravity – the ratio of the heaviness of a substance compared to that of the same volume of water.

Steam-Assisted Gravity Drainage (“SAGD”) – pairs of horizontal wells (an upper well and a lower well) are drilled into an oil sands formation and steam is injected continuously into the upper well. As the steam heats the oil sands formation, the bitumen softens and drains into the lower well, from which it is brought to the surface.

Steam to Oil Ratio (“SOR”) – measures the number of barrels of steam (measured in “Cold Water Equivalent Barrels”) needed for every barrel of oil produced.

Thermal Recovery – a type of improved recovery in which heat is introduced into a reservoir to lower the viscosity of heavy oils and to facilitate their flow into producing wells. The pay zone may be heated by injecting steam (steam drive) or by injecting air and burning a portion of the oil in place (in situ combustion).

Upgrading – the process that converts bitumen and heavy oil into a product with a density and viscosity similar to conventional light crude oil.

US$, USD, or US dollar - means United States dollars.

Viscosity – a measure of a fluid’s resistance to flow. To simplify, the oil’s viscosity represents the measure for which the oil wants to stay put when pushed by moving mechanical components. It varies greatly with temperature. The more viscous the oil the greater the resistance and the less easy it is for it to flow. Centipoise is the common unit for expressing absolute viscosity. Viscosity matters to producers because the oil’s viscosity at reservoir temperature determines how easily oil flows to the well for extraction.

| * | This definition is an abbreviated version of the complete definition as defined by the SEC under Rule 4-10(a) of Regulation S-X. |

Our functional currency is the US dollar. Therefore, our accounts are reported in United States dollars. However, our Canadian subsidiaries maintain their accounts and records in Canadian dollars. As a result, the Canadian dollar amounts are converted according to our stated foreign currency translation accounting policy, except where otherwise indicated, all dollar amounts herein are stated in US dollars.

The following table sets forth the rates of exchange for the Canadian dollar, expressed in US dollars, in effect at the end of the following periods and the average rates of exchange during such periods, as reported by the Bank of Canada.

| Year ending September 30 | 2020 | 2019 | ||||||

| Rate at year end | $ | 0.7497 | $ | 0.7551 | ||||

| Average rate for year | $ | 0.7437 | $ | 0.7537 | ||||

Unless the context indicates another meaning, the terms “Company,” “Deep Well,” “we,” “us” and “our” refer to Deep Well Oil & Gas, Inc. and its subsidiaries through which it conducts business. For definitions of some terms used throughout this report, see “Glossary and Abbreviations”.

iv

Deep Well Oil & Gas, Inc., through its subsidiaries conducts business as an independent junior oil sands exploration and development company. Its subsidiaries are headquartered in Edmonton, Alberta, Canada. Our immediate corporate focus is to develop the existing oil sands land base where our subsidiaries have working interests ranging from 25% to 100% in the Peace River oil sands area of Alberta, Canada. Deep Well Oil & Gas, Inc. is a Nevada corporation and our common stock trades on the OTC Marketplace under the symbol DWOG. We maintain a website at www.deepwelloil.com. The contents of our website are not part of this annual report on Form 10-K for the fiscal year ended September 30, 2020 (this “Annual Report”).

Formation of Organization

Deep Well Oil & Gas, Inc. was originally incorporated on July 18, 1988 under the laws of the state of Nevada as Worldwide Stock Transfer, Inc. and in connection with a plan of reorganization, effective on September 10, 2003, the Company was reorganized and changed its name to Deep Well Oil & Gas, Inc. Deep Well Oil & Gas, Inc. has two wholly owned subsidiaries through which it conducts its operations: (1) Northern Alberta Oil Ltd. (“Northern”) acquired on June 7, 2005, and incorporated under the Business Corporations Act (Alberta), Canada on September 18, 2003; and (2) Deep Well Oil & Gas (Alberta) Ltd., incorporated under the Business Corporations Act (Alberta), Canada on September 15, 2005.

Business Development

Our main objective is to develop our oil sands lease holdings located in the Peace River oil sands area of North Central Alberta, Canada, (also known as our Sawn Lake oil sands properties) using thermal recovery technologies. Currently, we have received approval from the Alberta Energy Regulator (“AER”) for two thermal recovery projects located on our Sawn Lake properties.

Over the last 3 years we have successfully applied to the AER to continue the best sections of our oil sands properties past their initial expiry dates, where resources were identified. Under the oil sands lease continuation regulations an operator or leaseholder must demonstrate certain levels of exploration and development by providing the AER with drilling, coring and seismic data within a certain timeframe in order to maintain the lease past its expiry date. For more information regarding our oil sands properties see “Oil and Gas Properties” under Item 2 “Properties” of this Annual Report on Form 10-K.

In late July of 2013 we entered into a Steam Assisted Gravity Drainage Demonstration Project Joint Operating Agreement (the “SAGD Project”) where we have a 25% working interest with one joint venture partner. In late July of 2013 we entered into a farmout agreement (the “Farmout Agreement”) with an additional joint venture partner (the “Farmee”). The SAGD Project produced bitumen for 18 months, demonstrating the productive capability of our Sawn Lake reservoir. In 2016 a majority of our Company’s Joint Venture partners voted to temporarily suspend operations for the SAGD Project. In early May of 2016, an amended application was submitted to the AER for an expansion of the existing SAGD Project facility site which would potentially increase the operations up to a total of eight SAGD well pairs. The amended application sought approval to expand the current SAGD Project facility site to 3,200 bopd (100% basis). Regulatory approval was received in December 2017 for a commercial expansion of the existing SAGD Project facility site where we have a 25% working interest. It is anticipated that only five SAGD well pairs will be needed to achieve the 3,200 bopd production level. For more information regarding our SAGD Project and our Farmout Agreement, see “Present Activities - Peace River Oil Sands, Alberta Canada (Sawn Lake Properties)” under Item 2 “Properties” of this Annual Report on Form 10-K.

Principal Product

We are engaged in the identification, acquisition, exploration and development of oil sands prospects. Exploration and development for commercially viable production of any oil sands company includes a high degree of risk, which careful evaluation, experience and factual knowledge may not eliminate.

Sawn Lake Oil Sands Properties – Peace River Oil Sands, Alberta, Canada

Currently, we have working interests in six oil sands leases ranging from 25% to 100% in the Peace River oil sands area of Alberta, where we are the operator of four leases. The focus of our Company’s operations is to develop the oil sands reservoir to establish proven reserves and to determine the best technology under which the oil can be produced from our Sawn Lake properties in order to generate positive cash flow. For further information on our oil sands projects see Item 2 “Oil and Gas Properties” in this Annual Report on Form 10-K.

1

Market and Distribution of Product

On lands where we have a 25% working interest, the operator of the SAGD Project markets and distributes all oil produced from the SAGD Project facility. Production from the SAGD Project was trucked and sold to marketing facilities in the Peace River area of Alberta. A majority of the Joint Venture partners voted to temporarily suspend operations for the SAGD Project at the end of February 2016.

On lands where we are the operator, we intend to sell our oil production under both short-term (less than one year) and long-term (one year or more) agreements at prices negotiated with third parties. Under both short-term and long-term contracts, typically either the entire contract (in the case of short-term contracts) or the price provisions of the contract (in the case of long-term contracts) are renegotiated in intervals ranging in frequency from daily to annual. At this time, we have no production on any of the lands where we are the operator and therefore, we have no short-term or long-term contracts. We will adopt specific sales and marketing plans once production is achieved on lands where we are designated as the operator. The operator of our joint SAGD Project marketed and distributed all oil produced from our joint SAGD Project.

Market pricing for bitumen is seasonal, with lower prices in and around the calendar year-end being the norm due to lower demand for asphalt and other bitumen-derived products. By necessity, bitumen is regularly blended with diluent in order to facilitate its transportation through pipelines to North American markets. As such, the effective field price for bitumen is also directly impacted by the input cost of the diluent required, the demand and price of which is also seasonal in nature (higher in winter as colder temperatures necessitate more diluent for transportation). Consequently, bitumen pricing is usually weakest in and around December and not reflective of the annual average realized price or the economics of the “business” overall. We have been advised that, to price bitumen, marketers apply formulas that take as a reference point the prices published for crude oil of particular qualities such as “Western Canadian Select”, “Brent Crude Oil”, “Crude Bitumen 9 API Plant Gate”, “Edmonton Light”, “Lloydminster Blend”, or the more internationally known “West Texas Intermediate” (“WTI”).

Competitive Business Conditions

We operate in a highly competitive environment, competing with major integrated and independent energy companies for desirable oil and natural gas properties as well as for the equipment, labour and materials required to develop and operate those properties. Many of our competitors have longer operating histories and substantially greater financial and other resources. Many of these companies not only explore for and produce crude oil and natural gas, but also carry on refining operations and market petroleum and other products on a worldwide basis. Our larger competitors, by reason of their size and relative financial strength, can more easily access capital markets than we can and may enjoy a competitive advantage, whereas we may incur higher costs or be unable to acquire and develop desirable properties at costs we consider reasonable because of this competition. Larger competitors may be able to absorb the burden of any changes in laws and regulation in the jurisdictions in which we do business and handle longer periods of reduced prices of gas and oil more easily. Our competitors may also be able to pay more for productive oil and natural gas properties and may be able to define, evaluate, bid for and purchase a greater number of properties and prospects than we can. Our ability to acquire additional properties in the future will depend upon our ability to conduct efficient operations, evaluate and select suitable properties, implement advanced technologies and consummate transactions in a highly competitive environment.

Competitive conditions may be substantially affected by various forms of energy legislation and/or regulation considered from time to time by the government of Canada and other countries as well as other factors beyond our control, including international political stability, overall levels of supply and demand for oil and gas, and the markets for synthetic fuels and alternative energy sources.

Customers

The operator of our SAGD Project, distributed and sold all of the oil that was produced from the SAGD Project. Production was sold to 11 different marketing facilities in Alberta.

Royalty Agreements

Through the acquisition of Northern, we potentially became a party to the following:

On December 12, 2003, Nearshore Petroleum Corporation (“Nearshore”) entered into a purported royalty agreement with Mikwec Energy Canada, Ltd. (now known as Northern) that potentially encumbers six of our oil sands leases located within our Sawn Lake properties (the “Purported 6.5% Royalty”). Nearshore claimed to have received the Purported 6.5% Royalty from Northern on the leased substances on the land interests which Northern holds in the above six oil sands leases. Nearshore was a private corporation incorporated in Alberta, Canada, and was owned and controlled by Mr. Steven P. Gawne and his wife, Mrs. Rebekah J. Gawne, who each owned 50% of Nearshore. Mr. Steven P. Gawne was the President, Chief Executive Officer and a director of Deep Well from February 6, 2004 to June 29, 2005. Nearshore has subsequently transferred part or all of the Purported 6.5% Royalty to other parties. Although we continue to deny the validity of the Purported 6.5% Royalty, we determined that it was in the best interests of our shareholders to come to an arrangement to acquire most of the Purported 6.5% Royalty to prevent a potential encumbrance over our land and the possibility of future litigation resulting from these alleged royalty claims. In our fiscal year 2014, we acquired 5.5% of the Purported 6.5 % Royalty for a cost of $3.4 million. See Item 3 Legal Proceedings in this Annual Report on Form 10-K.

2

Government Approval and Crown Royalties

Exploration and Production. Our operations are subject to Canadian federal and provincial governmental regulations. Such regulations include: requiring approval and licenses for the drilling of wells, regulating the location of wells and the method and ability to produce the wells, surface usage and the restoration of land upon which wells have been drilled, the plugging and abandoning of wells and the transportation of production from our wells. Our operations are also subject to various conservation regulations, including the regulation of in-situ recovery processes, the size of spacing units, the number of wells which may be drilled in a unit, the unitization or pooling of oil and gas properties, the rate of production allowable from oil and gas wells and the ability to produce oil and gas.

Investment Canada Act. The Investment Canada Act of 1985, as amended, requires notification and/or review by the government of Canada in certain cases, including but not limited to, the acquisition of control, directly or indirectly, of a Canadian Business by a non-Canadian. In certain circumstances, the acquisition of a working interest in a property that contains recoverable reserves will be treated as the acquisition of an interest in a “business” and may be subject to either notification or review, depending on the size of the interest being acquired and the asset size of the business.

Crown Royalties and Incentives. Crown royalties are determined by provincial and federal government regulation and are generally calculated as a percentage of the value of the gross production with the royalty rate dependent in part upon prescribed reference prices, well productivity, geographical location, field discovery date and the type and quality of the petroleum product produced. From time to time, the governments of Canada and Alberta have established incentive programs such as royalty rate reductions, royalty holidays, tax credits and drilling royalty credits. These incentives are for the purpose of encouraging oil and natural gas exploration or enhanced recovery projects. These incentives generally increase cash flow. Oil sands royalties in Alberta are calculated using a sliding scale for royalty rates ranging from 1% to 9% pre-payout and 25% to 40% post-payout depending on the world oil price. Project “payout” refers to the point in which we earn sufficient revenues to recover all of the allowed costs for the project plus a return allowance. The base royalty starts at 1% and increases for every dollar the world oil price, as reflected by the WTI, is priced above $55 per barrel, to a maximum of 9% when oil is priced at $120 per barrel or greater. The net royalty starts at 25% and increases for every dollar oil is priced above $55 per barrel to 40% when oil is priced at $120 or higher.

Environmental Laws and Regulations

The oil and natural gas industry is subject to environmental laws and regulations pursuant to Canadian local, provincial and federal legislation. Environmental legislation provides for restrictions and prohibitions on releases or emissions of various substances produced or utilized in association with oil and gas industry operations. Legislation requires that well and facility sites be monitored, abandoned and reclaimed to the satisfaction of provincial authorities. A breach of such legislation may result in the imposition of fines and penalties. Under these laws and regulations, we could be liable for personal injury, clean-up costs and other environmental and property damages as well as administrative, civil and criminal penalties. Accordingly, we could be liable or could be required to cease production on properties if environmental damage occurs. Although we maintain insurance coverage, the costs of complying with environmental laws and regulations in the future may harm our business. Furthermore, future changes in environmental laws and regulations could occur that result in stricter standards and enforcement, larger fines and liability, and increased capital expenditures and operating costs, any of which could have a material adverse effect on our financial condition or results of operations. We maintain commercial property and general liability insurance coverage on the properties we operate. We also maintain operators extra expense insurance which provides coverage for well control incidents specifically relating to regaining control of a well, seepage, pollution, clean-up and containment. No coverage is maintained with respect to any fine or penalty required to be paid due to a violation of the regulations set out by the federal and provincial regulatory authorities. We are committed to meeting our responsibilities to protect the environment and anticipate making increased expenditures of both a capital and expense nature as a result of the increasingly stringent laws relating to the protection of the environment.

Employees

Our Company currently has two prime subcontractors and three full-time employees. For further information on our subcontractors see “Compensation Arrangements for Executive Officers” under Item 11 “Executive Compensation” of this Annual Report on Form 10-K. We expect that, from time to time, we will hire more employees, independent consultants and contractors during the stages of implementing our plans.

3

An investment in our common stock is speculative and involves a high degree of risk and uncertainty. You should carefully consider the risks described below, together with the other information contained in our reports filed with the U.S. Securities and Exchange Commission (“SEC”), including the consolidated financial statements and notes thereto of our Company before deciding to invest in our common stock. The risks described below are not the only ones facing our Company. Additional risks not presently known to us, or that we presently consider immaterial may also adversely affect our Company. If any of the following risks occur, our business, financial condition and results of operations and the value of our common stock could be materially and adversely affected.

Any Development Of Our Resources Will Be Subject To Royalties. The royalty regime of Alberta is a significant factor in the profitability of oil and natural gas production in Alberta, Canada. Crown royalties are determined by government regulation and are generally calculated as a percentage of the value of the gross production with the royalty rate dependent in part upon prescribed reference prices, well productivity, geographical location, field discovery date and the type and quality of the petroleum product produced. Penalties and interest may be charged to us if we fail to remit royalties on our production to the Crown as prescribed in the regulation. In addition, there is a risk that the remaining 1% of the Purported 6.5% Royalty could be found to be valid.

We Have A History Of Losses And May Not Achieve Or Sustain Profitability In The Future. Since our inception, we have suffered recurring losses from operations and have been dependent on new investment to sustain our operations. During the years ended September 30, 2020 and 2019 we reported net losses of $103,302 and $197,135 respectively. We may not achieve profitability in the foreseeable future, if at all. In addition, our operating expenses may be more than our future revenue growth. We expect our future cost of revenue and operating expenses to continue to increase in the foreseeable future as we continue to expand on our thermal recovery operations at Sawn Lake, Alberta.

Future Price Declines May Result In A Write-Down Of Asset Carrying Values. Effective July 1, 2015, our Company adopted the full-cost method of accounting for costs related to our oil sands properties. Under the full cost method, oil and gas properties are subject to a ceiling test performed quarterly. A ceiling test write-down is recognized in net earnings if the carrying amount of a cost centre exceeds the “cost centre ceiling”. The cost centre ceiling is the sum of: (i) present value of the estimated future net cash flows from proved oil and natural gas reserves using a 10 percent per year discount factor; (ii) the costs of unproved properties not being amortized; (iii) the lower of cost or fair value of unproved properties included in the costs being amortized; and (iv) related income tax effects. During the 2020 and 2019 fiscal year, no ceiling test write-downs were recorded for our oil and gas properties. Costs associated with unproved properties are excluded from the depletion calculation until it is determined that proved reserves are attributable or impairment has occurred. Unproved properties are assessed annually for impairment. Costs that have been impaired are included in the costs subject to depletion within the full cost pool. A significant decline in oil prices from current levels, or other factors, without other mitigating circumstances, could cause a future write-down of our capitalized costs and a non-cash charge on our income statement.

The Successful Implementation Of Our Business Plan Is Subject To Risks Inherent In The Oil Sands Business. Our oil sands operations are subject to the economic risks typically associated with exploration, development and production activities, including the necessity of significant expenditures to locate and acquire properties, to drill exploratory wells and to produce bitumen using thermal recovery technologies. In addition, the cost and timing of drilling, completing, operating and acquiring regulatory approval for thermal recovery operations on our wells is often uncertain. In conducting exploration and development activities, the presence of unanticipated pressure or irregularities in formations, miscalculations or accidents may cause our exploration, development and production activities to be unsuccessful. This could result in a total loss of our investment in a particular property. If our efforts are unsuccessful in establishing proven reserves, the amounts capitalized as unproven costs may be written down and charged against earnings. Our exploitation and development of oil sands reserves depends upon access to the areas where our operations are to be conducted. We conduct a portion of our operations in regions where we are only able to do so on a seasonal basis. Unless the surface is sufficiently frozen, we are unable to access our properties, drill or otherwise conduct our operations as planned. In addition, if the surface thaws earlier than expected, we must cease our operations for the season earlier than planned. Our operations are affected by road bans imposed from time to time during the break-up and thaw period in the spring. Road bans are also imposed due to heavy rain, mud, rock slides and periods of high water, which can restrict access to our well sites and potential production facility sites. Our inability to access our properties or to conduct our operations as planned would result in a shutdown or slowdown of our operations, which would adversely affect our business.

4

We Rely On Independent Experts And Technical Or Operational Service Providers Over Whom We May Have Limited Control. The success of our business is dependent upon the efforts of various third parties that we do not control. We rely upon various companies to assist us in identifying desirable oil prospects to acquire and to provide us with technical assistance and services. We also rely upon the services of geologists, geophysicists, chemists, engineers and other scientists to explore and analyze oil prospects to determine a method in which the oil prospects may be developed in a cost-effective manner. In addition, we rely upon the owners and operators of oil drilling equipment to drill and develop our prospects to production. Although we have developed relationships with a number of third-party service providers, we cannot assure that we will be able to continue to rely on such persons. If any of these relationships with third-party service providers are terminated or are unavailable on commercially acceptable terms, we may not be able to execute our business plan. Our limited control over the activities and business practices of these third parties, any inability on our part to maintain satisfactory commercial relationships with them or their failure to provide quality services could materially and adversely affect our business, results of operations and financial condition.

Our Interests Are Held In The Form Of Leases That We May Be Unable To Retain. We have working interests in six oil sands leases in North Central Alberta, Canada. Five of these oil sands leases were successfully continued past their initial 15-year fixed term and are now continued into perpetuity. The lease terms include certain commitments related to oil sands properties that require the payments of yearly rents. As required by the Oil Sands Tenure Regulation of the Mines and Minerals Act of Alberta continued oil sands leases past their initial expiry dates are subject to escalating rental payments in respect of each term year of a continued lease that is designated as non-producing. Also, continued oil sands leases must pay annual and escalating rent which is payable at the beginning of each term year. Lessees of continued oil sands leases may eliminate their escalating rent obligations once the lease reaches the minimum level of production guidelines set out by the regulations. If we fail to meet the specific requirements of the lease regarding delay or non-payment of annual rental payments or yearly escalating rents, some or all of our leases may be terminated for failure to pay the required yearly rents. We have one oil sands lease that has not yet been continued past its initial expiry date of April 9, 2024. There can be no assurance that any of the obligations required to maintain each lease will be met. The termination or expiration of our oil sands leases or the working interests relating to our leases may reduce our opportunity to exploit a given prospect for production and thus could have a material adverse effect on our business, results of operations and financial condition.

We Expect Our Operating Expenses To Increase Substantially In The Future And We May Need To Raise Additional Funds. We have a history of net losses and expect that our operating expenses will increase substantially over the next 12 months as we continue to move forward to develop our oil sands leases. In addition, we may experience a material decrease in liquidity due to unforeseen cash calls or other events and uncertainties. As a result, we may need to raise additional funds, and such funds may not be available on favourable terms, if at all. If we cannot raise funds on acceptable terms, we may not be able to execute our business plan, take advantage of future opportunities or respond to competitive pressures or unanticipated requirements. This could have a material adverse effect on our business, results of operations and financial condition.

Our Ability To Produce Sufficient Quantities Of Oil From Our Properties May Be Adversely Affected By A Number Of Factors Outside Of Our Control. The business of exploring for and producing oil and gas involves a substantial risk of investment loss. Drilling oil sands wells involves the risk that the wells may be unproductive or that, although productive, the wells may not produce oil in economic quantities. Other hazards such as unusual or unexpected geological formations, pressures, fires, blowouts, loss of circulation of drilling fluids or other conditions may substantially delay or prevent completion of any well. Adverse weather conditions can also hinder drilling operations. A productive well could become uneconomic due to, for example, pressure depletion, water encroachment or mechanical difficulties, which could impair or prevent the production from the well. There can be no assurance that oil will be produced from all of our properties in which we have interests. Marketability of any oil that we acquire or discover may be influenced by numerous factors beyond our control. The marketability of our production will depend on the proximity of our reserves to and the capacity of, third party facilities and services, including oil and natural gas gathering systems, pipelines, trucking or terminal facilities, and processing facilities. The unavailability or insufficient capacity of these facilities and services could force us to shut-in producing wells, delay the commencement of production, or discontinue development plans for some of our properties, which would adversely affect our financial condition and performance. There may be periods of time when pipeline capacity is inadequate to meet our oil transportation needs. During periods when pipeline capacity is inadequate, we may be forced to reduce production or incur additional expense as existing production is compressed to fit into existing pipelines. Other risk factors include availability of drilling and related equipment, market fluctuations of prices, taxes, royalties, land tenure, allowable production and environmental protection. Our ability to manage these factors could have a material adverse effect on our business, results of operations and financial condition.

We Do Not Control All Of Our Operations. We do not operate all of our oil sands properties and we therefore have limited influence over the testing, drilling and production operations of those properties. Currently, we have a 90% working interest on three oil sands leases, a 100% working interest on one oil sands lease, where we are the operator of the 90% and 100% leases. We also have a 25% working interest on two oil sands leases where one of our joint venture partners is the operator. All six oil sands leases are located in the Peace River oil sands area of Alberta, Canada. Our lack of operational control of the two leases currently not operated by us means we are exposed to the following possibilities:

| ● | the operator might initiate exploration or development on a faster or slower pace than we prefer, or shut-in a currently existing project; |

| ● | the operator might propose to drill more wells or build more facilities on a project than we have funds for or that we deem appropriate, which could mean that we are unable or decline to participate in the project or share in the revenues generated by the project; |

5

| ● | if the operator does not initiate a joint operation proposal to conduct further operations on these two leases, the non-operators are entitled to propose a joint operation that is separate from any already existing project. As a non-operator on those two leases, we might be unable to pursue further operations on the two leases unless we and possibly other joint participating non-operators directly pay the entire cost thereof. |

Any of these events could materially reduce the value of those properties affected.

Aboriginal Peoples May Make Claims Regarding The Lands On Which Our Operations Are Conducted. The AER governs our operations in Alberta, Canada and they have implemented a directive (“Directive 056”) through which the government of Alberta has issued its First Nations Consultation Policy on Land Management and Resource Development on May 16, 2005. The AER expects that all industry applicants adhere to this policy and the consultation guidelines. These requirements and expectations apply to the licensing of all new energy developments and all modifications to existing energy developments, as covered in Directive 056. In the policy, the government of Alberta has developed consultation guidelines to address specific questions about how consultation for land management and resource development should occur in relation to specific activities. Prior to filing an application, we must address all questions, objections, and concerns regarding our proposed development projects and attempt to resolve them. This includes concerns and objections raised by members of the public, industry, government representatives, First Nations, Métis, and other interested parties. This process can cause significant delays in obtaining a drilling permit for exploration and/or a production well license for both oil and gas and could have a material adverse effect on our operations.

Our Operations Are Subject To A Wide Range of Environmental Legislation and Regulation From All Levels Of Government Of Which We Have No Control. Environmental legislation imposes, among other things, restrictions, liabilities and obligations in connection with the generation, handling, storage, transportation, treatment and disposal of hazardous substances and waste and in connection with spills, releases and emissions of various substances into the environment. As well, environmental regulations are imposed on the qualities and compositions of the products sold and imported. Environmental legislation also requires that wells, facility sites and other properties associated with our operations be operated, maintained, abandoned and reclaimed to the satisfaction of applicable regulatory authorities. In addition, certain types of operations, including exploration and development projects and significant changes to certain existing projects, may require the submission and approval of environmental impact assessments. Compliance with environmental legislation can require significant expenditures, and failure to comply with environmental legislation may result in the imposition of fines and penalties and liability for cleanup costs and damages. The costs of complying with environmental legislation in the future could have a material adverse effect on our business, results of operations and financial condition. We anticipate that changes in environmental legislation may require, among other things, reductions in emissions to the air from its operations and result in increased capital expenditures. Future changes in environmental legislation could occur and result in stricter standards and enforcement, larger fines and liability, and increased capital expenditures and operating costs, which could have a material adverse effect on our business, results of operations and financial condition.

Market Fluctuations In The Prices Of Oil Could Adversely Affect Our Business. Prices for oil tend to fluctuate significantly in response to factors beyond our control. These factors include, but are not limited to, the ongoing wars in the Middle East and actions of the Organization of Petroleum Exporting Countries and its maintenance of production constraints, the U.S. political and economic environment, weather conditions, the availability and market acceptance of alternate fuel sources, transportation interruption, the impact of drilling levels on crude oil and natural gas supply, and the environmental and access issues that could limit future drilling activities for the industry. Changes in commodity prices may significantly affect our capital resources, liquidity and expected operating results. Price changes directly affect revenues and can indirectly impact expected production by changing the amount of funds available to reinvest in exploration and development activities. Reductions in oil pricing not only reduce revenues and profits but could also reduce the quantities of reserves that are commercially recoverable. Significant declines in oil prices could result in non-cash charges to earnings due to write-downs. Changes in commodity prices may also significantly affect our ability to estimate the value of producing properties for acquisition and divestiture and often cause disruption in the market for oil producing properties, as buyers and sellers have difficulty agreeing on the value of the properties. Price volatility also makes it difficult to budget for and project the return on acquisitions and development and exploitation of projects. We expect that commodity prices will continue to fluctuate significantly in the future.

Our Stock Price Could Decline. Our common stock is traded on the OTC marketplace. There can be no assurance that an active public market will continue for our common stock or that the market price for our common stock will not decline below its current price. Such price may be influenced by many factors, including but not limited to, investor perception of us and our industry and general economic and market conditions. The trading price of our common stock could be subject to wide fluctuations in response to announcements of our business developments or our competitors, quarterly variations in operating results, and other events or factors. In addition, stock markets have experienced extreme price volatility in recent years. This volatility has had a substantial effect on the market prices of companies, at times for reasons unrelated to their operating performance. Such broad market fluctuations may adversely affect the price of our common stock. Our stock price may decline as a result of future sales of our shares or the perception that such sales may occur.

6

We Could Be Subject To SEC Penalties If We Do Not File All Of Our SEC Reports. We have not timely filed all of our annual and quarterly reports required to be filed by us with the SEC, in a timely manner. It is possible that the SEC could take enforcement action against us, including potentially the de-registration of our securities, if we fail to file our annual and quarterly reports in a timely manner as required by the SEC. If the SEC were to take any such actions, it could adversely affect the liquidity of trading in our common stock and the amount of information about our Company that is publicly available.

Broker-Dealers Are Not Permitted To Solicit Trades In Our Common Stock. Our common stock is considered to be a “penny stock” because it meets one or more of the definitions of “penny stock” in Rule 3a51-1 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The principal result or effect of being designated a “penny stock” is that securities broker-dealers cannot recommend the stock and may only trade in it on an unsolicited basis. The continued inability of brokers to recommend our stock could have a material adverse effect on our business, results of operations and financial condition.

Risks Related To Broker-Dealer Requirements Involving Penny Stocks / Risks Affecting Trading and Liquidity. Section 15(g) of the Exchange Act and Rule 15g-2 promulgated thereunder by the SEC require broker-dealers dealing in penny stocks to provide potential investors with a document disclosing the risks of penny stocks and to obtain a manually signed and dated written receipt of the document before effecting any transaction in a penny stock for the investor’s account. These rules may have the effect of reducing the level of trading activity in the secondary market, if and when one develops. Potential investors in our common stock are urged to obtain and read such disclosure carefully before purchasing any shares that are deemed to be “penny stock.” Moreover, SEC Rule 15g-9 requires broker-dealers in penny stocks to approve the account of any investor for transactions in such stocks before selling any penny stock to that investor. This procedure requires the broker-dealer to (i) obtain from the investor information concerning his or her financial situation, investment experience and investment objectives; (ii) reasonably determine, based on that information, that transactions in penny stocks are suitable for the investor and that the investor has sufficient knowledge and experience as to be reasonably capable of evaluating the risks of penny stock transactions; (iii) provide the investor with a written statement setting forth the basis on which the broker-dealer made the determination in (ii) above; and (iv) receive a signed and dated copy of such statement from the investor, confirming that it accurately reflects the investor’s financial situation, investment experience and investment objectives. Pursuant to the Penny Stock Reform Act of 1990, broker-dealers are further obligated to provide customers with monthly account statements. Compliance with the foregoing requirements may make it more difficult for investors in our stock to resell their shares to third parties or to alternatively dispose of them in the market or otherwise.

The outbreak of health epidemics and pandemics, including COVID-19, could adversely affect our business, financial condition, and results of operations. Health epidemics and pandemics could, and in fact, have spread across the globe and could, and have, impacted worldwide economic activity, including the global demand for oil, natural gas and the price for heavy oil. Health epidemics and pandemics, including the COVID-19 and its variants, can cause certain risks in which we, or our employees, contractors, suppliers, customers and joint venture partners may be prevented from conducting business activities for an indefinite period of time, due to restrictions that may be requested or mandated by governmental authorities, which include quarantines that restrict or prohibit employees from going to work. The ongoing spread of COVID-19 and its variants and mitigation measures to prevent its spread, along with a decline in oil prices, could have a material adverse effect on our business, financial condition, results of operations and our ability to raise funds.

The SEC recently adopted amendments to Rule 15c2-11 under the Securities Exchange Act of 1934, could adversely affect our common stock. Rule 15c2-11 (the “Rule”) becomes effective on September 28, 2021 and will have an impact on the over-the-counter (“OTC”) market regulatory structure. The amended Rule is ostensibly to enhance disclosure and investor protection in the OTC market by ensuring that broker-dealers in the OTC market do not publish quotations for an issuer’s security when current issuer information is not publicly available. Therefore, under the new Amendments to Rule 15c2-11, now, all OTC quoted companies must file at least current annual financial statements or companies will not be publicly quoted on the OTC Markets and risk being downgraded to the Grey Market. Our Company is currently listed on the OTC markets “Pink – No Information” Tier. Currently, we have not filed all of our annual and quarterly reports which are required to be filed by us with the SEC. We are striving to achieve this goal. Even so, it is possible that our common stock may be downgraded to the Grey Market, if it determined that we failed to file our appropriate annual and quarterly reports in a timely manner as required by the SEC. Our Company must file its September 30, 2020 annual financial statements with the SEC in order for our Company to remain publicly quoted on the OTC Markets “Pink - Limited Information” Tier. This document is meant to comply with that requirement. If it is determined that we did not comply with these new requirements, it is highly likely that it may make it more difficult for investors in our stock to resell their shares to third parties or to alternatively dispose of them in the open market or otherwise.

7

Oil and Gas Properties

Acreage

Currently, we have a 90% working interest in three oil sands leases, a 100% working interest in one oil sands lease, and a 25% working interest in an additional two oil sands leases in the Peace River oil sands area of Alberta. These six oil sands leases cover 17,712 gross acres (7,168 gross hectares) with our Company having 11,734 net acres (4,749 net hectares). We are the operator of four of these oil sands leases where we have working interests of either 90% or 100%. For further information, see Oil and Gas Properties on our Balance Sheet and Note 3, 4 and 5 in the notes to our consolidated financial statements contained herein.

The following table summarizes, by geographic area, our gross and net developed and undeveloped acreage as of September 30, 2020:

| sawn lake properties - Peace River Oil Sands as of September 30, 2020 | ||||||||||||||||

| Gross Hectares | Net Hectares | Gross Acres | Net Acres | |||||||||||||

| Developed Acreage | ||||||||||||||||

| Alberta, Canada | 0 | 0 | 0 | 0 | ||||||||||||

| Total | 0 | 0 | 0 | 0 | ||||||||||||

| Undeveloped Acreage | ||||||||||||||||

| Alberta, Canada | 7,168 | 4,749 | 17,712 | 11,734 | ||||||||||||

| Total | 7,168 | 4,749 | 17,712 | 11,734 | ||||||||||||

| TOTAL Developed and Undeveloped | 7,168 | 4,749 | 17,712 | 11,734 | ||||||||||||

Our Sawn Lake oil sands properties under lease as of September 30, 2020, covers 17,712 gross acres (11,734 net acres) of land under six oil sands leases. The lease expiration dates of our Company’s oil sands leases are as follows:

| (i) | The Company has five oil sands leases that cover 14,549 gross acres (8,571 net acres) and have no set expiry date. These continued leases are now held by the Company for perpetuity, subject to yearly escalating rental payments until they are deemed to be producing leases; |

| (ii) | 3,163 gross acres (3,163 net acres) under one oil sands lease are set to expire on April 9, 2024. The Company will be applying to continue this lease into perpetuity. |

Summary of Oil and Gas Reserves

We did not have our properties independently assessed and evaluated for reserves and resources as of September 30, 2020. As of September 30, 2015, DeGolyer and MacNaughton Canada Limited (“DeGolyer”) in compliance with SEC definitions and guidance and in accordance with generally accepted petroleum engineering principles, did assess and evaluate our properties for reserves and resources. Our Company reported no proved reserves as of September 30, 2015.

Drilling and Other Exploratory and Development Activities

The following table summarizes the results of our drilling activities in the Peace River oil sands area of Alberta during the fiscal years ended September 30, 2020, 2019 and 2018.

| Development (Net Wells) | Exploratory (Net Wells) | |||||||||||||||||||||||||||||||

| Oil | Gas | Service Well | Dry | Oil | Gas | Service Well | Dry | |||||||||||||||||||||||||

| September 30, 2020 | ||||||||||||||||||||||||||||||||

| Alberta, Canada | – | – | – | – | – | – | – | – | ||||||||||||||||||||||||

| September 30, 2019 | ||||||||||||||||||||||||||||||||

| Alberta, Canada | – | – | – | – | – | – | – | – | ||||||||||||||||||||||||

| September 30, 2018 | ||||||||||||||||||||||||||||||||

| Alberta, Canada | – | – | – | – | *- | – | – | – | ||||||||||||||||||||||||

| * - | On February 15, 2018, we entered into a contribution agreement with a third-party to drill a well on one of our Sawn Lake oil sands leases in which we acquired cores and logs through the Bluesky formation, but did not acquire a working interest in that well. |

8

Productive Wells

As of the fiscal year ended September 30, 2020; we had no producing wells. All of our producing wells were shut-in in February 2016 in accordance with a majority of our Company’s Joint Venture partners voting to temporarily suspend operations for the SAGD Project at the end of February 2016.

Present Activities – Peace River Oil Sands, Alberta Canada (Sawn Lake Properties)

Currently we have no wells in the process of being drilled. Our Company to date has, but not limited to, drilled or participated in 13 wells over our Sawn Lake leases to expand the boundaries of the Bluesky oil sands reservoir; commissioned various independent reservoir simulation studies of our properties; successfully produced bitumen from the SAGD Project, which outperformed independent reservoir production type curves; acquired AER approval for two thermal recovery projects, which includes our joint SAGD Project facility expansion to produce up to 3,200 bopd; successfully entered into Farmout Agreements; and we have successfully applied to the AER to continue the best sections of our oil sands properties past their initial expiry dates, where resources were identified. Previously, under the prior oil sands lease continuation regulations an operator or leaseholder must demonstrate certain levels of exploration and development by providing the AER with drilling, coring and seismic data within a certain timeframe in order to maintain the lease past its expiry date.

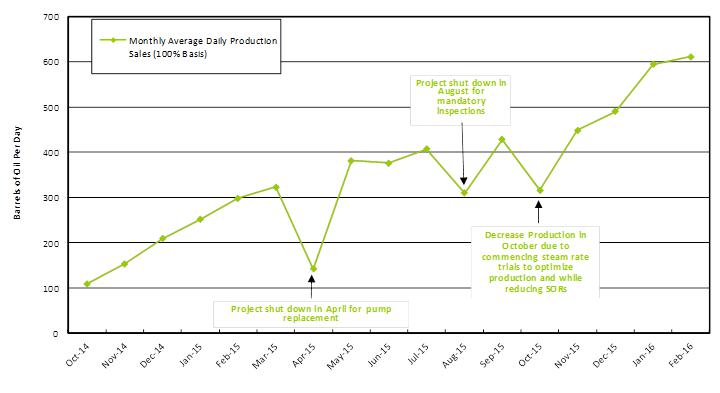

We are focused on developing the bitumen resources located on our Sawn Lake properties using thermal recovery technology development. A SAGD Project on our Sawn Lake properties commenced in 2013 where we have a 25% working interest. The SAGD Project consists of one SAGD well pair drilled to a depth of 650 meters and a horizontal length of 780 meters and the SAGD facility for steam generation, water handling, and bitumen treating. Steam injection commenced in May 2014 and production commenced on September 16, 2014. The SAGD Project reached a steady state production level in February of 2016 of 620 bopd, on a 100% basis (155 bopd net to us) from one SAGD well pair and achieved an instantaneous Steam oil Ratio (“ISOR”) efficiency of 2.1, demonstrating the productive capability of our Sawn Lake reservoir with significant future potential value. The lower the ISOR the lower the production costs and emissions per barrel of oil produced. The production results of the current SAGD Project successfully confirmed the capability of the Bluesky reservoir to produce using thermal recovery technology. A majority of our Company’s Joint Venture partners voted to temporarily suspend operations for the SAGD Project at the end of February 2016.

The successful results of our joint SAGD Project were used to update our reservoir models and will be used in the preparation of an updated independent evaluation of our Sawn Lake properties.

Regulatory approval was received in December 2017 for a commercial expansion of the existing SAGD Project facility site where we have a 25% working interest. This expansion application sought approval to expand the current SAGD Project facility site to 3,200 bopd (100% basis). It is anticipated that only five SAGD well pairs will need to be operating to achieve this production level. The SAGD Project development plan will be done in stages to reduce initial financial costs. The first stage anticipates the reactivation of the existing SAGD facility and existing SAGD well pair, along with the drilling of one additional SAGD well pair, initially producing from two SAGD well pairs. The second stage anticipates drilling an additional three SAGD well pairs to produce up to 3,200 bopd and the expansion of the existing SAGD facility to generate the additional steam required. The lead time to acquiring the necessary equipment and commencing operations is estimated to be about 18 months and another 6 months is required for the start of bitumen production (after development of the steam chamber). A Sawn Lake full field development plan using SAGD batteries has been defined by the operator of the SAGD Project. As 2021 and 2022 proceed, the operator of the SAGD Project should be consulting with its joint venture partners regarding development potential and alternatives for the SAGD Project.

In accordance with the Farmout Agreement, the Farmee has agreed to provide up to $40,000,000 in funding for our portion of the costs for the SAGD Project, in return for a net 25% working interest in 11 sections where we had a working interest of 50% before the execution of the Farmout Agreement. Under the terms of the Farmout Agreement the Farmee also is required to provide funding to cover the monthly administrative expenses of our Company, provided that such funding shall not to exceed $30,000 per month. The total share of the material costs and operating expenses of our Company’s joint SAGD Project is funded in accordance with the Farmout Agreement. The Farmee shall also continue to cover our Company’s administrative costs up to $30,000 per month until completion in all substantial respects of the SAGD Project agreement entered into on July 30, 2013 between the Company and the operator of the SAGD Project.

The development progress of our Sawn Lake oil sands properties is governed by several factors such as federal and provincial governmental regulations. Long lead times in getting regulatory approval for thermal recovery projects are commonplace in our industry. Road bans, winter access only roads and environmental regulations can, and often, do delay development of similar projects and our projects. Because of these and other factors, our oil sands projects can take significantly longer to complete than regular conventional drilling programs for lighter oil. To date, our geological, engineering, economic studies, and our SAGD Project production results lead us to believe that our working interest may be able to support future full profitable commercial production.

We previously received approval from the AER for a horizontal cyclic steam stimulation project (“HCSS Project”) application. It is anticipated that we will develop a thermal demonstration project on our properties followed by a commercial expansion project on one half section of land located on section 10-92-13W5 of our Sawn Lake oil sands properties where we currently have a 90% working interest. The final performance results and revised reservoir modeling studies from our current SAGD Project will be used to fine-tune our HCSS Project facility design before we initiate start-up operations on the half section of land where we plan to drill two horizontal wells to test the use of HCSS technology. We performed an environmental field study and surveyed the proposed location of our planned HCSS Project site and received AER approval for the surface wellsite and access road for this project.

9

Provident Premier Master Fund Ltd. vs Northern Alberta Oil Ltd., Deep Well Oil & Gas (Alberta) Ltd., Andora Energy Corporation and MP Energy West Canada Corp.

On October 28, 2019, Provident Premier Master Fund Ltd. (the “Plaintiff”), filed and served an Amended Statement of Claim against Northern Alberta Oil Ltd., Deep Well Oil & Gas (Alberta) Ltd., Andora Energy Corporation and MP Energy West Canada Corp. (the “Defendants”) in the Court of Queen’s Bench of Alberta Judicial District of Calgary. The Original Statement of Claim had been filed on November 1, 2018 but the Company states that it was never served, so the Company was not aware of the claim until served with the Amended Statement of Claim. The Plaintiff claims that on December 12, 2003, Nearshore Petroleum Corporation (“Nearshore”) entered into a royalty agreement with Northern Alberta Oil Ltd. (“Northern”) in which Northern supposedly granted a 6.5% gross overriding royalty (the “Purported GORR”) in all petroleum substances produced, saved and marketed from certain oil sands leases located within the Company’s Sawn Lake properties. The Plaintiff further claims that on September 22, 2006, Nearshore and Gemini Strategies LLC (“Gemini”) entered into a royalty conveyance agreement whereby Nearshore sold 1% of the Purported GORR to Gemini. The Plaintiff further states that Gemini acquired the 1% of the Purported GORR as agent for Provident, Grey K Fund LP (“Grey K”) and Grey K Offshore Fund Ltd. (“Grey K Offshore”). The Plaintiff further claims that on September 22, 2006, Gemini delivered a notice of assignment, in accordance with the 1993 Canadian Association of Petroleum Landmen Assignment Procedure (the “1993 CAPL”), to the grantors of the 1% of the Purported GORR, novating Provident (66.67%, net 0.6667%), Grey K (19.33%, net 0.1933%) and Grey K Offshore (14%, net 0.14%) into the Purported GORR agreement. The Plaintiff further claims that on September 2, 2009, any legal title in the Purported GORR beneficially owned by Grey K and Grey K Offshore vested in the Crown in right of Alberta pursuant to Section 229(1) of the Business Corporations Act and pursuant to section 15 of the Unclaimed Personal Property and Vested Property Act. The Plaintiff further claims that the Purported GORR was payable by one or more of the Defendants to Provident and that the Defendants are in breach of the Purported GORR agreement by failing to pay the Purported GORR. Despite the allegation within the claim that the Purported GORR was payable to each of Provident, Grey K and Grey K Offshore, the only Plaintiff named in the Amended Statement of Claim is Provident and relief is only being sought by Provident in relation to its purported 0.67% interest.

On October 22, 2020, Provident Premier Master Fund Ltd. (the “Plaintiff”), filed and served a Second Amended Statement of Claim against Northern Alberta Oil Ltd., Deep Well Oil & Gas (Alberta) Ltd., Andora Energy Corporation and MP Energy West Canada Corp. (the “Defendants”) in the Court of Queen’s Bench of Alberta Judicial District of Calgary. The Original Statement of Claim had been filed on November 1, 2018, but the Company states that it was never served so the Company was not aware of the claim until served with the first Amended Statement of Claim filed with the Court of Queen’s Bench of Alberta Judicial District of Calgary on October 24, 2019. The Plaintiff claims that on December 12, 2003, Nearshore Petroleum Corporation (“Nearshore”) entered into a royalty agreement with Northern Alberta Oil Ltd. (“Northern”) in which Northern supposedly granted a 6.5% gross overriding royalty the (“Purported GORR”) in all petroleum substances produced, saved and marketed from certain oil sands leases held by the Company located within the Company’s Sawn Lake properties. The Plaintiff seeks: 1) A declaration that the Plaintiff is the legal owner of 0.67% of the Purported GORR payable on all oil sands produced from the lands which is payable by one or more of the Defendants; 2) as stated in Clause 18(b) of the Second Amended Statement of Claim, an accounting to determine the amount of the outstanding royalty; 3.) Judgment or restitution in the amount determined pursuant to section 18(b) in the approximate amount of $74,970 ($100,000 Cdn) plus such further amounts as come due following the filing of the action; and 4) Interest and costs.

On November 30, 2020, the Defendants filed a Statement of Defence against the Plaintiff in the Court of Queen’s Bench of Alberta Judicial District of Calgary. The Defendants continue to deny the validity of the Purported GORR in the first instance. As well, if the Purported GORR was valid, which is denied, it was not a gross overriding interest, but rather an overriding interest, which allowed for the deduction of operating and marketing costs. The Defendants plan to vigorously defend itself against the Plaintiff’s claims.

December 21,2020, Northern Alberta Oil Ltd., Deep Well Oil & Gas (Alberta) Ltd. (the “Third-Party Defendants”) filed a Statement of Defence to Third Party Claim against the Plaintiff in the Court of Queen’s Bench of Alberta Judicial District of Calgary. The remedy sought by the Third-Party Defendants is: 1.) the Third-Party Defendants ask that the Plaintiff’s claim against MP Energy West Canada Corp. and Andora Energy Corporation be dismissed, with costs payable by the Plaintiff; and 2.) The Third-Party Defendants ask that no costs be payable in relation to the Third-Party Claim.

10

Andora Energy Corporation vs Northern Alberta Oil Ltd. and Deep Well Oil & Gas (Alberta), Ltd.

On December 3, 2020, Andora Energy Corporation (the “Plaintiff”), filed a Statement of Claim against Northern Alberta Oil Ltd. and Deep Well Oil & Gas (Alberta) Ltd. (the “Defendants”) in the Court of Queen’s Bench of Alberta Judicial District of Calgary. The Company states that it was first served with this Statement of Claim on January 26, 2021. The Plaintiff claims that the Defendants owe the Plaintiff $100,316 ($133,808 Cdn) for unpaid joint interest billings. The Plaintiff seeks: 1.) Judgment, or alternatively damages, in the amount of the indebtedness, or such further amounts as may be due and owing as at the date of trail; 2.) Interest on the amount found to be owing; 3.) Costs of this action; and 4.) Such further and other relief as counsel may advise and the court deems just.

On February 17, 2021, the Defendants filed a Statement of Defence against the Plaintiff in the Court of Queen’s Bench of Alberta Judicial District of Calgary. The Defendants claim that the Plaintiff owes monies to the Defendants for, but are not limited to, leases operated by the Defendants, and that the Defendants have a right to off-set costs against any monies that may be owed to the Plaintiff’s.

On March 18, 2021, Andora Energy Corporation (the “Plaintiff”), filed an Application for Summary of Judgment and Affidavit to support the Application for Summary of Judgment against Northern Alberta Oil Ltd. and Deep Well Oil & Gas (Alberta) Ltd. (the “Defendants”) in the Court of Queen’s Bench of Alberta Judicial District of Calgary. The Plaintiff seeks the repayment of outstanding joint interest billings pursuant to a joint operating agreement between the parties (the “JOA”). The Plaintiff seeks an Order granting the following relief: 1.) summary judgment in favour of Plaintiff as against the Defendant Northern Alberta Oil Ltd. in the amount of $98,367 ($131,209 Cdn); 2.) summary judgment in favour of Plaintiff as the Defendant Deep Well Oil & Gas (Alberta) Ltd. in the amount of $14,777 ($19,710 Cdn); 3.) interest on the amounts pursuant to the contractual interest rate prescribed by the JOA, or alternatively, pursuant to the Judgement Interest Act RSA 2000, c J-1; 4.) costs of this Action, including costs of this Application, on such basis as the Court deems appropriate; and 5.) such further and other relief as counsel may advices and the Court may deem just.

On June 21, 2021, the Defendants filed an Affidavit against the Plaintiff’s application for an order for summary judgment against the Defendants in the Court of Queen’s Bench of Alberta Judicial District of Calgary. The Defendants claim that the Plaintiff owes $128,597 ($171,531 Cdn) to the Defendants for, but are not limited to, leases operated by the Defendants, and that the Defendants have a right to off-set costs against any monies that may be owed to the Plaintiff’s.

On June 22, 2021, upon an application by the Plaintiff for an order for summary judgment against the Defendants and upon the Court reviewing the Affidavits filed by the Plaintiff and Defendants and upon hearing counsel for the Plaintiff and counsel for the Defendants, the Justice in Chambers denied the Plaintiff’s order for a summary judgment against the Defendants.

The Defendants deny the Plaintiff’s claim regarding all of the monies which are claimed to be owed to the Defendants by the Plaintiff. The Defendants plan to vigorously defend itself against the Plaintiff’s claims, but has provided for some of the claimed amounts in the Company’s books as of September 30, 2020.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

11

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Deep Well’s stock is currently quoted on the OTC Marketplace under the trading symbol DWOG. The following table sets forth the high and low sales prices for Deep Well common stock as reported on the OTC Marketplace for the fiscal years indicated below. These over-the-counter market quotations reflect inter-dealer prices, without retail mark-up, markdown or commission and may not necessarily represent actual transactions:

| High* | Low* | |||||||

| Fiscal September 30, 2019 | ||||||||

| First Quarter | $ | 0.05 | $ | 0.02 | ||||

| Second Quarter | $ | 0.06 | $ | 0.01 | ||||

| Third Quarter | $ | 0.04 | $ | 0.01 | ||||

| Fourth Quarter | $ | 0.05 | $ | 0.01 | ||||