Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | Annual Report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended August 31, 2013,

or

| ¨ | Transition report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to .

Commission file number 1-10714

AUTOZONE, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 62-1482048 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 123 South Front Street, Memphis, Tennessee | 38103 | |

| (Address of principal executive offices) | (Zip Code) |

(901) 495-6500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock ($.01 par value) |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was $13,781,127,110.

The number of shares of Common Stock outstanding as of October 21, 2013, was 34,031,760.

Documents Incorporated By Reference

Portions of the definitive Proxy Statement to be filed within 120 days of August 31, 2013, pursuant to Regulation 14A under the Securities Exchange Act of 1934 for the Annual Meeting of Stockholders to be held December 18, 2013, are incorporated by reference into Part III.

Table of Contents

| 4 | ||||||

| Item 1. |

4 | |||||

| 4 | ||||||

| 5 | ||||||

| 6 | ||||||

| 7 | ||||||

| 8 | ||||||

| 8 | ||||||

| 8 | ||||||

| 9 | ||||||

| 9 | ||||||

| 9 | ||||||

| 9 | ||||||

| Item 1A. |

11 | |||||

| Item 1B. |

14 | |||||

| Item 2. |

15 | |||||

| Item 3. |

15 | |||||

| Item 4. |

15 | |||||

| 16 | ||||||

| Item 5. |

16 | |||||

| Item 6. |

18 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

19 | ||||

| Item 7A. |

33 | |||||

| Item 8. |

35 | |||||

| Item 9. |

Changes In and Disagreements with Accountants on Accounting and Financial Disclosure |

69 | ||||

| Item 9A. |

69 | |||||

| Item 9B. |

69 | |||||

| 70 | ||||||

| Item 10. |

70 | |||||

| Item 11. |

70 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

70 | ||||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

70 | ||||

| Item 14. |

70 | |||||

| 71 | ||||||

| Item 15. |

71 | |||||

2

Table of Contents

Forward-Looking Statements

Certain statements contained in this annual report are forward-looking statements. Forward-looking statements typically use words such as “believe,” “anticipate,” “should,” “intend,” “plan,” “will,” “expect,” “estimate,” “project,” “positioned,” “strategy” and similar expressions. These are based on assumptions and assessments made by our management in light of experience and perception of historical trends, current conditions, expected future developments and other factors that we believe to be appropriate. These forward-looking statements are subject to a number of risks and uncertainties, including without limitation: credit market conditions; the impact of recessionary conditions; competition; product demand; the ability to hire and retain qualified employees; consumer debt levels; inflation; weather; raw material costs of our suppliers; energy prices; war and the prospect of war, including terrorist activity; construction delays; access to available and feasible financing; and changes in laws or regulations. Certain of these risks are discussed in more detail in the “Risk Factors” section contained in Item 1A under Part 1 of this Annual Report on Form 10-K for the year ended August 31, 2013, and these Risk Factors should be read carefully. Forward-looking statements are not guarantees of future performance and actual results; developments and business decisions may differ from those contemplated by such forward-looking statements, and events described above and in the “Risk Factors” could materially and adversely affect our business. Forward-looking statements speak only as of the date made. Except as required by applicable law, we undertake no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise. Actual results may materially differ from anticipated results.

3

Table of Contents

AutoZone, Inc. (“AutoZone,” the “Company,” “we,” “our” or “us”) is the nation’s leading retailer and a leading distributor of automotive replacement parts and accessories in the United States. We began operations in 1979 and at August 31, 2013, operated 4,836 stores in the United States, including Puerto Rico; 362 in Mexico; and three in Brazil. Each of our stores carries an extensive product line for cars, sport utility vehicles, vans and light trucks, including new and remanufactured automotive hard parts, maintenance items, accessories and non-automotive products. At August 31, 2013, in 3,421 of our domestic stores we also have a commercial sales program that provides commercial credit and prompt delivery of parts and other products to local, regional and national repair garages, dealers, service stations and public sector accounts. We also have commercial programs in select stores in Mexico, as well as in our stores in Brazil. We also sell the ALLDATA brand automotive diagnostic and repair software through www.alldata.com. Additionally, we sell automotive hard parts, maintenance items, accessories, and non-automotive products through www.autozone.com, and accessories and performance parts through www.autoanything.com, and our commercial customers can make purchases through www.autozonepro.com. We do not derive revenue from automotive repair or installation services.

At August 31, 2013, our stores were in the following locations:

| Store Count | ||||

| Alabama |

103 | |||

| Alaska |

6 | |||

| Arizona |

124 | |||

| Arkansas |

61 | |||

| California |

521 | |||

| Colorado |

72 | |||

| Connecticut |

40 | |||

| Delaware |

13 | |||

| Florida |

255 | |||

| Georgia |

184 | |||

| Idaho |

23 | |||

| Illinois |

228 | |||

| Indiana |

148 | |||

| Iowa |

24 | |||

| Kansas |

41 | |||

| Kentucky |

87 | |||

| Louisiana |

115 | |||

| Maine |

7 | |||

| Maryland |

51 | |||

| Massachusetts |

77 | |||

| Michigan |

166 | |||

| Minnesota |

39 | |||

| Mississippi |

87 | |||

| Missouri |

105 | |||

| Montana |

10 | |||

| Nebraska |

15 | |||

| Nevada |

61 | |||

| New Hampshire |

21 | |||

| New Jersey |

74 | |||

| New Mexico |

62 | |||

| New York |

149 | |||

| North Carolina |

192 | |||

| North Dakota |

1 | |||

| Ohio |

241 | |||

| Oklahoma |

67 | |||

| Oregon |

38 | |||

| Pennsylvania |

142 | |||

| Puerto Rico |

34 | |||

| Rhode Island |

15 | |||

| South Carolina |

84 | |||

| South Dakota |

5 | |||

| Tennessee |

158 | |||

| Texas |

557 | |||

| Utah |

45 | |||

| Vermont |

2 | |||

| Virginia |

107 | |||

| Washington |

75 | |||

| Washington, DC |

5 | |||

| West Virginia |

35 | |||

| Wisconsin |

58 | |||

| Wyoming |

6 | |||

|

|

|

|||

| Total Domestic |

4,836 | |||

| Mexico |

362 | |||

| Brazil |

3 | |||

|

|

|

|||

| Total |

5,201 | |||

|

|

|

|||

4

Table of Contents

Marketing and Merchandising Strategy

We are dedicated to providing customers with superior service and trustworthy advice as well as quality automotive parts and products at a great value in conveniently located, well-designed stores. Key elements of this strategy are:

Customer Service

Customer service is the most important element in our marketing and merchandising strategy, which is based upon consumer marketing research. We emphasize that our AutoZoners (employees) should always put customers first by providing prompt, courteous service and trustworthy advice. Our electronic parts catalog assists in the selection of parts as well as warranties that are offered by us or our vendors on many of the parts that we sell. The wide area network in our stores helps us expedite credit or debit card and check approval processes, locate parts at neighboring AutoZone stores, including our hub stores, and in some cases, place special orders directly with our vendors. We sell automotive hard parts, maintenance items, accessories and non-automotive parts through www.autozone.com for pick-up in store or to be shipped directly to a customer’s home or business. Additionally, we offer smartphone apps that provide customers with store locations, driving directions, operating hours, and product availability.

Our stores generally open at 7:30 or 8 a.m. and close between 8 and 10 p.m. Monday through Saturday and typically open at 9 a.m. and close between 6 and 9 p.m. on Sunday. However, some stores are open 24 hours, and some have extended hours of 6 or 7 a.m. until midnight seven days a week.

We also provide specialty tools through our Loan-A-Tool program. Customers can borrow a specialty tool, such as a steering wheel puller, for which a do-it-yourself (“DIY”) customer or a repair shop would have little or no use other than for a single job. AutoZoners also provide other free services, including check engine light readings where allowed by law, battery charging, the collection of used oil for recycling, and the testing of starters, alternators, batteries, sensors and actuators.

5

Table of Contents

Merchandising

The following tables show some of the types of products that we sell by major category of items:

| Failure |

Maintenance |

Discretionary | ||

| A/C Compressors Batteries & Accessories Belts & Hoses Carburetors Chassis Clutches CV Axles Engines Fuel Pumps Fuses Ignition Lighting Mufflers Radiators Thermostats Starters & Alternators Water Pumps |

Antifreeze & Windshield Washer Fluid Brake Drums, Rotors, Shoes & Pads Chemicals, including Brake & Power Steering Fluid, Oil & Fuel Additives Oil & Transmission Fluid Oil, Air, Fuel & Transmission Filters Oxygen Sensors Paint & Accessories Refrigerant & Accessories Shock Absorbers & Struts Spark Plugs & Wires Windshield Wipers |

Air Fresheners Cell Phone Accessories Drinks & Snacks Floor Mats & Seat Covers Interior and Exterior Accessories Mirrors Performance Products Protectants & Cleaners Sealants & Adhesives Steering Wheel Covers Stereos & Radios Tools Wash & Wax |

We believe that the satisfaction of our customers is often impacted by our ability to provide specific automotive products as requested. Each store carries the same basic products, but we tailor our inventory to the makes and models of the vehicles in each store’s trade area, and our sales floor products are tailored to the local store’s demographics. Our hub stores carry a larger assortment of products that are delivered to local satellite stores. We are constantly updating the products we offer to ensure that our inventory matches the products our customers need or desire.

Pricing

We want to be perceived by our customers as the value leader in our industry, by consistently providing quality merchandise at the right price, backed by a satisfactory warranty and outstanding customer service. For many of our products, we offer multiple value choices in a good/better/best assortment, with appropriate price and quality differences from the “good” products to the “better” and “best” products. A key differentiating component versus our competitors is our exclusive line of in-house brands, which includes the Econocraft, Valucraft, AutoZone, SureBilt, ProElite, Duralast, Duralast Gold, and Duralast Platinum brands. We believe that our overall value compares favorably to that of our competitors.

Brand Marketing: Advertising and Promotions

We believe that targeted advertising and promotions play important roles in succeeding in today’s environment. We are constantly working to understand our customers’ wants and needs so that we can build long-lasting, loyal relationships. We utilize promotions, advertising and loyalty card programs primarily to advise customers about the overall importance of vehicle maintenance, our great value and the availability of high quality parts. Broadcast and internet media are our primary advertising methods of driving traffic to our stores. We utilize in-store signage, in-store circulars, and creative product placement and promotions to help educate customers about products that they need.

Store Design and Visual Merchandising

We design and build stores for high visual impact. The typical AutoZone store utilizes colorful exterior and interior signage, exposed beams and ductwork and brightly lit interiors. Maintenance products, accessories and non-automotive items are attractively displayed for easy browsing by customers. In-store signage and special displays promote products on floor displays, end caps and shelves.

Our commercial sales program operates in a highly fragmented market, and we are one of the leading distributors of automotive parts and other products to local, regional and national repair garages, dealers, service stations and

6

Table of Contents

public sector accounts in the United States, Puerto Rico, Mexico and Brazil. As a part of the program, we offer credit and delivery to our customers, as well as online ordering through www.autozonepro.com. Through our hub stores, we offer a greater range of parts and products desired by professional technicians. We have dedicated sales teams focused on independent repair shops as well as national, regional and public sector commercial accounts.

Store Formats

Substantially all AutoZone stores are based on standard store formats, resulting in generally consistent appearance, merchandising and product mix. Approximately 85% to 90% of each store’s square footage is selling space, of which approximately 40% to 45% is dedicated to hard parts inventory. The hard parts inventory area is generally fronted by counters or pods that run the depth or length of the store, dividing the hard parts area from the remainder of the store. The remaining selling space contains displays of maintenance, accessories and non-automotive items.

We believe that our stores are “destination stores,” generating their own traffic rather than relying on traffic created by adjacent stores. Therefore, we situate most stores on major thoroughfares with easy access and good parking.

Store Personnel and Training

Each store typically employs from 10 to 16 AutoZoners, including a manager and, in some cases, an assistant manager. We provide on-the-job training as well as formal training programs, including an annual national sales meeting, regular store meetings on specific sales and product issues, standardized training manuals and a specialist program that provides training to AutoZoners in several areas of technical expertise from the Company, our vendors and independent certification agencies. All AutoZoners are encouraged to complete tests resulting in certifications by the National Institute for Automotive Service Excellence (“ASE”), which is broadly recognized for training certification in the automotive industry. Training is supplemented with frequent store visits by management.

Store managers, sales representatives, commercial specialists, and managers at various levels across the organization receive financial incentives through performance-based bonuses. In addition, our growth has provided opportunities for the promotion of qualified AutoZoners. We believe these opportunities are important to attract, motivate and retain high quality AutoZoners.

All store support functions are centralized in our store support centers located in Memphis, Tennessee; Monterrey, Mexico; Chihuahua, Mexico and Sao Paulo, Brazil. We believe that this centralization enhances consistent execution of our merchandising and marketing strategies at the store level, while reducing expenses and cost of sales.

Store Automation

All of our stores have Z-net, our proprietary electronic catalog that enables our AutoZoners to efficiently look up the parts that our customers need and to provide complete job solutions, advice and information for customer vehicles. Z-net provides parts information based on the year, make, model and engine type of a vehicle and also tracks inventory availability at the store, at other nearby stores and through special order. The Z-net display screens are placed on the hard parts counter or pods, where both the AutoZoner and customer can view the screen.

Our stores utilize our computerized proprietary Store Management System, which includes bar code scanning and point-of-sale data collection terminals. The Store Management System provides administrative assistance and improved personnel scheduling at the store level, as well as enhanced merchandising information and improved inventory control. We believe the Store Management System also enhances customer service through faster processing of transactions and simplified warranty and product return procedures. In addition, our wide area network enables the stores to expedite credit or debit card and check approval processes, to access national warranty data, to implement real-time inventory controls and to locate and hold parts at neighboring AutoZone stores.

7

Table of Contents

The following table reflects our store development during the past five fiscal years:

| Fiscal Year | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| Beginning stores |

5,006 | 4,813 | 4,627 | 4,417 | 4,240 | |||||||||||||||

| New stores |

197 | 193 | 188 | 213 | 180 | |||||||||||||||

| Closed stores |

2 | — | 2 | 3 | 3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net new stores |

195 | 193 | 186 | 210 | 177 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Relocated stores |

11 | 10 | 10 | 3 | 9 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Ending stores |

5,201 | 5,006 | 4,813 | 4,627 | 4,417 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

We believe that expansion opportunities exist both in markets that we do not currently serve, as well as in markets where we can achieve a larger presence. We attempt to obtain high visibility sites in high traffic locations and undertake substantial research prior to entering new markets. The most important criteria for opening a new store are the projected future profitability and the ability to achieve our required investment hurdle rate. Key factors in selecting new site and market locations include population, demographics, vehicle profile, customer buying trends, commercial businesses, number and strength of competitors’ stores and the cost of real estate. In reviewing the vehicle profile, we also consider the number of vehicles that are seven years old and older, or “our kind of vehicles”; these vehicles are generally no longer under the original manufacturers’ warranties and require more maintenance and repair than newer vehicles. We generally seek to open new stores within or contiguous to existing market areas and attempt to cluster development in markets in a relatively short period of time. In addition to continuing to lease or develop our own stores, we evaluate and may make strategic acquisitions.

Merchandise is selected and purchased for all stores through our store support centers located in Memphis, Tennessee and Monterrey, Mexico. In fiscal 2013, one class of similar products accounted for approximately 10 percent of our total sales. No vendor supplied more than 10 percent of our purchases, and we believe that alternative sources of supply exist, at similar costs, for most types of product sold. Most of our merchandise flows through our distribution centers to our stores by our fleet of tractors and trailers or by third-party trucking firms.

Our hub stores have increased our ability to distribute products on a timely basis to many of our stores and to expand our product assortment. A hub store generally has a larger assortment of products as well as regular replenishment items that can be delivered to a store in its network within 24 hours. Hub stores are generally replenished from distribution centers multiple times per week.

The sale of automotive parts, accessories and maintenance items is highly competitive in many areas, including name recognition, product availability, customer service, store location and price. AutoZone competes in the after-market auto parts industry, which includes both the retail DIY and commercial do-it-for-me (“DIFM”) auto parts and products markets.

Competitors include national, regional and local auto parts chains, independently owned parts stores, online parts stores, jobbers, repair shops, car washes and auto dealers, in addition to discount and mass merchandise stores, department stores, hardware stores, supermarkets, drugstores, convenience stores, home stores, and other online retailers that sell aftermarket vehicle parts and supplies, chemicals, accessories, tools and maintenance parts. AutoZone competes on the basis of customer service, including the trustworthy advice of our AutoZoners; merchandise quality, selection and availability; price; product warranty; store layouts, location and convenience; and the strength of our AutoZone brand name, trademarks and service marks.

8

Table of Contents

We have registered several service marks and trademarks in the United States Patent and Trademark office as well as in certain other countries, including our service marks, “AutoZone” and “Get in the Zone,” and trademarks, “AutoZone,” “Duralast,” “Duralast Gold,” “Duralast Platinum,” “Valucraft,” “Econocraft,” “ALLDATA,” “AutoAnything,” “Loan-A-Tool” and “Z-net.” We believe that these service marks and trademarks are important components of our marketing and merchandising strategies.

As of August 31, 2013, we employed over 71,000 persons, approximately 59 percent of whom were employed full-time. About 92 percent of our AutoZoners were employed in stores or in direct field supervision, approximately 5 percent in distribution centers and approximately 3 percent in store support and other functions. Included in the above numbers are approximately 5,000 persons employed in our Mexico and Brazil operations.

We have never experienced any material labor disruption and believe that relations with our AutoZoners are good.

AutoZone’s primary website is at http://www.autozone.com. We make available, free of charge, at our investor relations website, http://www.autozoneinc.com, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements, registration statements and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act of 1934, as amended, as soon as reasonably feasible after we electronically file such material with, or furnish it to, the Securities and Exchange Commission.

Executive Officers of the Registrant

The following list describes our executive officers. The title of each executive officer includes the words “Customer Satisfaction” which reflects our commitment to customer service. Officers are elected by and serve at the discretion of the Board of Directors.

William C. Rhodes, III, 48—Chairman, President and Chief Executive Officer, Customer Satisfaction

William C. Rhodes, III, was named Chairman of AutoZone during fiscal 2007 and has been President, Chief Executive Officer and a director since March 2005. Prior to his appointment as President and Chief Executive Officer, Mr. Rhodes was Executive Vice President – Store Operations and Commercial. Previously, he held several key management positions with the Company. Prior to 1994, Mr. Rhodes was a manager with Ernst & Young LLP. Mr. Rhodes is a member of the Board of Directors for Dollar General Corporation.

William T. Giles, 54—Chief Financial Officer and Executive Vice President – Finance, Information Technology and ALLDATA, Customer Satisfaction

William T. Giles was named Chief Financial Officer and Executive Vice President – Finance, Information Technology and ALLDATA during October 2012. Prior to that, he was Chief Financial Officer and Executive Vice President – Finance, Information Technology and Store Development from fiscal 2007 to October 2012; Executive Vice President, Chief Financial Officer and Treasurer from June 2006 to December 2006; and Executive Vice President, Chief Financial Officer since May 2006. From 1991 to May 2006, he held several positions with Linens N’ Things, Inc., most recently as the Executive Vice President and Chief Financial Officer. Prior to 1991, he was with Melville, Inc. and PricewaterhouseCoopers. Mr. Giles is a member of the Board of Directors for Brinker International.

Harry L. Goldsmith, 62—Executive Vice President, General Counsel and Secretary, Customer Satisfaction

Harry L. Goldsmith was elected Executive Vice President, General Counsel and Secretary during fiscal 2006. Previously, he was Senior Vice President, General Counsel and Secretary since 1996 and was Vice President, General Counsel and Secretary from 1993 to 1996. In June 2013, Mr. Goldsmith announced his plans to retire, effective January 2014.

9

Table of Contents

Mark A. Finestone, 52—Senior Vice President – Merchandising, Customer Satisfaction

Mark A. Finestone was elected Senior Vice President – Merchandising during fiscal 2008. Previously, he was Vice President – Merchandising since 2002. Prior to joining AutoZone in 2002, Mr. Finestone worked for May Department Stores for 19 years where he held a variety of leadership roles which included Divisional Vice President, Merchandising.

William W. Graves, 53—Senior Vice President – Supply Chain and International, Customer Satisfaction

William W. Graves was named Senior Vice President – Supply Chain and International during October 2012. Prior thereto, he was Senior Vice President – Supply Chain from fiscal 2006 to October 2012 and Vice President – Supply Chain from fiscal 2000 to fiscal 2006. From 1992 to 2000, Mr. Graves served in various capacities with the Company.

Ronald B. Griffin, 59—Senior Vice President and Chief Information Officer, Customer Satisfaction

Ronald B. Griffin was elected Senior Vice President and Chief Information Officer during June 2012. Prior to that, he was Senior Vice President, Global Information Technology at Hewlett-Packard Company. During his tenure at Hewlett-Packard Company, he also served as the Chief Information Officer for the Enterprise Business Division. Prior to that, Mr. Griffin was Executive Vice President and Chief Information Officer for Fleming Companies, Inc. He also spent over 12 years with The Home Depot, Inc., with the last eight years in the role of Chief Information Officer. Mr. Griffin also served at Deloitte & Touche LLP and Delta Air Lines, Inc.

Albert Saltiel, 49—Senior Vice President – Marketing, Customer Satisfaction

Albert “Al” Saltiel was elected Senior Vice President – Marketing during April 2013. Prior to that, he was Chief Marketing Officer and a key member of the leadership team at Navistar International Corporation. Mr. Saltiel has also been with Sony Electronics as General Manager, Marketing, and Ford Motor Company where he held multiple marketing roles.

Thomas B. Newbern, 51—Senior Vice President – Store Operations and Store Development, Customer Satisfaction

Thomas B. Newbern was elected Senior Vice President – Store Operation and Store Development during October 2012. Previously, Mr. Newbern held the titles Senior Vice President – Store Operations from fiscal 2007 to October 2012 and Vice President – Store Operations from fiscal 1998 to fiscal 2007. Previously, he has held several key management positions with the Company.

Charlie Pleas, III, 48—Senior Vice President and Controller, Customer Satisfaction

Charlie Pleas, III, was elected Senior Vice President and Controller during fiscal 2007. Prior to that, he was Vice President and Controller since 2003. Previously, he was Vice President – Accounting since 2000, and Director of General Accounting since 1996. Prior to joining AutoZone, Mr. Pleas was a Division Controller with Fleming Companies, Inc. where he served in various capacities since 1988.

Larry M. Roesel, 56—Senior Vice President – Commercial, Customer Satisfaction

Larry M. Roesel was elected Senior Vice President – Commercial during fiscal 2007. Mr. Roesel came to AutoZone with more than thirty years of experience with OfficeMax, Inc. and its predecessor, where he served in operations, sales and general management.

Michael A. Womack, 46—Senior Vice President – Human Resources, Customer Satisfaction

Michael A. Womack was elected Senior Vice President – Human Resources in June 2012. He was previously Vice President of Human Resources with Cintas Corp. and had been with Cintas since 2003. Before joining Cintas, he was a law partner with the Littler Mendelson law firm.

10

Table of Contents

Our business is subject to a variety of risks. Set forth below are certain of the important risks that we face, the occurrence of which could have a material, adverse effect on our business. These risks are not the only ones we face. Our business could also be affected by additional factors that are presently unknown to us or that we currently believe to be immaterial to our business.

If demand for our products slows, then our business may be materially affected.

Demand for products sold by our stores depends on many factors, including:

| • | the number of vehicles in current service, including those that are seven years old and older. These vehicles are generally no longer under the original vehicle manufacturers’ warranties and tend to need more maintenance and repair than newer vehicles. |

| • | rising energy prices. Increases in energy prices may cause our customers to defer purchases of certain of our products as they use a higher percentage of their income to pay for gasoline and other energy costs. |

| • | the economy. In periods of declining economic conditions, both retail and commercial customers may defer vehicle maintenance or repair. Additionally, such conditions may affect our customers’ ability to obtain credit. During periods of expansionary economic conditions, more of our DIY customers may pay others to repair and maintain their cars instead of working on their own vehicles or they may purchase new vehicles. |

| • | the weather. Mild weather conditions may lower the failure rates of automotive parts, while wet conditions may cause our customers to defer maintenance and repair on their vehicles. Extremely hot or cold conditions may enhance demand for our products due to increased failure rates of our customers’ automotive parts. |

| • | technological advances. Advances in automotive technology and parts design could result in cars needing maintenance less frequently and parts lasting longer. |

For the long term, demand for our products may be affected by:

| • | the number of miles vehicles are driven annually. Higher vehicle mileage increases the need for maintenance and repair. Mileage levels may be affected by gas prices and other factors. |

| • | the quality of the vehicles manufactured by the original vehicle manufacturers and the length of the warranties or maintenance offered on new vehicles. |

| • | restrictions on access to diagnostic tools and repair information imposed by the original vehicle manufacturers or by governmental regulation. |

All of these factors could result in immediate and longer term declines in the demand for our products, which could adversely affect our sales, cash flows and overall financial condition.

If we are unable to compete successfully against other businesses that sell the products that we sell, we could lose customers and our sales and profits may decline.

The sale of automotive parts, accessories and maintenance items is highly competitive and is based on many factors, including name recognition, product availability, customer service, store location and price. Competitors are opening locations near our existing stores. AutoZone competes as a provider in both the DIY and DIFM auto parts and accessories markets.

Competitors include national, regional and local auto parts chains, independently owned parts stores, online parts stores, jobbers, repair shops, car washes and auto dealers, in addition to discount and mass merchandise stores, hardware stores, supermarkets, drugstores, convenience stores, home stores, and other online retailers that sell aftermarket vehicle parts and supplies, chemicals, accessories, tools and maintenance parts. Although we believe we compete effectively on the basis of customer service, including the knowledge and expertise of our AutoZoners; merchandise quality, selection and availability; product warranty; store layout, location and convenience; price; and the strength of our AutoZone brand name, trademarks and service marks; some competitors may gain competitive advantages, such as greater financial and marketing resources allowing them to sell automotive products at lower prices, larger stores with more merchandise, longer operating histories, more

11

Table of Contents

frequent customer visits and more effective advertising. If we are unable to continue to develop successful competitive strategies, or if our competitors develop more effective strategies, we could lose customers and our sales and profits may decline.

We may not be able to sustain our historic rate of sales growth.

We have increased our store count in the past five fiscal years, growing from 4,240 stores at August 30, 2008, to 5,201 stores at August 31, 2013, an average store count increase per year of 5%. Additionally, we have increased annual revenues in the past five fiscal years from $6.523 billion in fiscal 2008 to $9.148 billion in fiscal 2013, an average increase per year of 8%. Annual revenue growth is driven by the opening of new stores and increases in same-store sales. We open new stores only after evaluating customer buying trends and market demand/needs, all of which could be adversely affected by continued job losses, wage cuts, small business failures and microeconomic conditions unique to the automotive industry. Same store sales are impacted both by customer demand levels and by the prices we are able to charge for our products, which can also be negatively impacted by continued recessionary pressures. We cannot provide any assurance that we will continue to open stores at historical rates or continue to achieve increases in same-store sales.

If we cannot profitably increase our market share in the commercial auto parts business, our sales growth may be limited.

Although we are one of the largest sellers of auto parts in the commercial market, to increase commercial sales we must compete against national and regional auto parts chains, independently owned parts stores, wholesalers and jobbers and auto dealers. Although we believe we compete effectively on the basis of customer service, merchandise quality, selection and availability, price, product warranty, distribution locations, and the strength of our AutoZone brand name, trademarks and service marks, some automotive aftermarket jobbers have been in business for substantially longer periods of time than we have, have developed long-term customer relationships and have large available inventories. If we are unable to profitably develop new commercial customers, our sales growth may be limited.

Significant changes in macroeconomic factors could adversely affect our financial condition and results of operations.

Our short-term and long-term debt is rated investment grade by the major rating agencies. These investment-grade credit ratings have historically allowed us to take advantage of lower interest rates and other favorable terms on our short-term credit lines, in our senior debt offerings and in the commercial paper markets. To maintain our investment-grade ratings, we are required to meet certain financial performance ratios. An increase in our debt and/or a decline in our earnings could result in downgrades in our credit ratings. A downgrade in our credit ratings could limit our access to public debt markets, limit the institutions willing to provide credit facilities to us, result in more restrictive financial and other covenants in our public and private debt and would likely significantly increase our overall borrowing costs and adversely affect our earnings.

Moreover, significant deterioration in the financial condition of large financial institutions in calendar years 2008 and 2009 resulted in a severe loss of liquidity and availability of credit in global credit markets and in more stringent borrowing terms. During brief time intervals in the fourth quarter of calendar 2008 and the first quarter of calendar 2009, there was limited liquidity in the commercial paper markets, resulting in an absence of commercial paper buyers and extraordinarily high interest rates on commercial paper. We can provide no assurance that credit market events such as those that occurred in the fourth quarter of 2008 and the first quarter of 2009 will not occur again in the foreseeable future. Conditions and events in the global credit market could have a material adverse effect on our access to short-term debt and the terms and cost of that debt.

Macroeconomic conditions also impact both our customers and our suppliers. Job growth in the United States has stagnated and unemployment has remained at historically high levels during the past five years. If the United States government is unable to reach agreement on legislation addressing the United States’ current debt level and budget deficit, many economists have predicted another economic recession. Continued recessionary conditions could result in additional job losses and business failures, which could result in our loss of certain small business customers and curtailment of spending by our retail customers. In addition, continued distress in global credit markets, business failures and other recessionary conditions could have a material adverse effect on the ability of

12

Table of Contents

our suppliers to obtain necessary short and long-term financing to meet our inventory demands. Moreover, rising energy prices could impact our merchandise distribution, commercial delivery, utility and product costs. All of these macroeconomic conditions could adversely affect our sales growth, margins and overhead, which could adversely affect our financial condition and operations.

Our business depends upon hiring and retaining qualified employees.

We believe that much of our brand value lies in the quality of the more than 71,000 AutoZoners employed in our stores, distribution centers, store support centers, ALLDATA and AutoAnything. We cannot be assured that we can continue to hire and retain qualified employees at current wage rates. If we are unable to hire, properly train and/or retain qualified employees, we could experience higher employment costs, reduced sales, losses of customers and diminution of our brand, which could adversely affect our earnings. If we do not maintain competitive wages, our customer service could suffer due to a declining quality of our workforce or, alternatively, our earnings could decrease if we increase our wage rates.

Inability to acquire and provide quality merchandise could adversely affect our sales and results of operations.

We are dependent upon our vendors continuing to supply us with quality merchandise. If our merchandise offerings do not meet our customers’ expectations regarding quality and safety, we could experience lost sales, increased costs and exposure to legal and reputational risk. All of our vendors must comply with applicable product safety laws, and we are dependent on them to ensure that the products we buy comply with all safety and quality standards. Events that give rise to actual, potential or perceived product safety concerns could expose us to government enforcement action or private litigation and result in costly product recalls and other liabilities. To the extent our suppliers are subject to added government regulation of their product design and/or manufacturing processes, the cost of the merchandise we purchase may rise. In addition, negative customer perceptions regarding the safety or quality of the products we sell could cause our customers to seek alternative sources for their needs, resulting in lost sales. In those circumstances, it may be difficult and costly for us to regain the confidence of our customers. Moreover, if any of our significant vendors experience financial difficulties or otherwise are unable to deliver merchandise to us on a timely basis, or at all, we could have product shortages in our stores that could adversely affect customers’ perceptions of us and cause us to lose customers and sales.

Our ability to grow depends in part on new store openings, existing store remodels and expansions and effective utilization of our existing supply chain and hub network.

Our continued growth and success will depend in part on our ability to open and operate new stores and expand and remodel existing stores to meet customers’ needs on a timely and profitable basis. Accomplishing our new and existing store expansion goals will depend upon a number of factors, including the ability to partner with developers and landlords to obtain suitable sites for new and expanded stores at acceptable costs, the hiring and training of qualified personnel, particularly at the store management level, and the integration of new stores into existing operations. There can be no assurance we will be able to achieve our store expansion goals, manage our growth effectively, successfully integrate the planned new stores into our operations or operate our new, remodeled and expanded stores profitably.

In addition, we extensively utilize hub stores, our supply chain and logistics management techniques to efficiently stock our stores. If we fail to effectively utilize our existing hubs and/or supply chains, we could experience inappropriate inventory levels in our stores, which could adversely affect our sales volume and/or our margins.

Our failure to protect our reputation could have a material adverse effect on our brand name.

We believe our continued strong sales growth is driven in significant part by our brand name. The value in our brand name and its continued effectiveness in driving our sales growth are dependent to a significant degree on our ability to maintain our reputation for safety, high product quality, friendliness, service, trustworthy advice, integrity and business ethics. Any negative publicity about these types of concerns may reduce demand for our merchandise. Failure to comply with ethical, social, product, labor and environmental standards could also jeopardize our reputation and potentially lead to various adverse consumer actions. Failure to comply with applicable laws and regulations, to maintain an effective system of internal controls or to provide accurate and timely financial statement information could also hurt our reputation.

13

Table of Contents

Our business involves the storage of personal information about our customers and AutoZoners. Failure to protect the security of our customers’, employees’ and company information could subject us to costly regulatory enforcement actions, expose us to litigation and our reputation could suffer. While we take significant steps to protect customer, employee and other confidential information, including maintaining compliance with payment card industry standards, our security measures may be breached in the future due to cyber attack, employee error or other acts, and unauthorized parties may obtain access to this data. To date, we have not experienced any significant breaches of information.

Damage to our reputation or loss of consumer confidence for any of these or other reasons could have a material adverse effect on our results of operations and financial condition, as well as require additional resources to rebuild our reputation.

Business interruptions may negatively impact our store hours, operability of our computer and other systems, availability of merchandise and otherwise have a material negative effect on our sales and our business.

War or acts of terrorism, political unrest, hurricanes, windstorms, fires, earthquakes and other natural or other disasters or the threat of any of them, may result in certain of our stores being closed for a period of time or permanently or have a negative impact on our ability to obtain merchandise available for sale in our stores. Some of our merchandise is imported from other countries. If imported goods become difficult or impossible to bring into the United States, and if we cannot obtain such merchandise from other sources at similar costs, our sales and profit margins may be negatively affected.

In the event that commercial transportation is curtailed or substantially delayed, our business may be adversely impacted, as we may have difficulty shipping merchandise to our distribution centers and stores resulting in lost sales and/or a potential loss of customer loyalty. Transportation issues could also cause us to cancel purchase orders if we are unable to receive merchandise in our distribution centers.

We rely extensively on our computer systems to manage inventory, process transactions and summarize results. Our systems are subject to damage or interruption from power outages, telecommunications failures, computer viruses, security breaches and catastrophic events. If our systems are damaged or fail to function properly, we may incur substantial costs to repair or replace them, and may experience loss of critical data and interruptions or delays in our ability to manage inventories or process transactions, which could result in lost sales, inability to process purchase orders and/or a potential loss of customer loyalty, which could adversely affect our results of operations.

Item 1B. Unresolved Staff Comments

None.

14

Table of Contents

The following table reflects the square footage and number of leased and owned properties for our stores as of August 31, 2013:

| No. of Stores | Square Footage | |||||||

| Leased |

2,653 | 16,930,389 | ||||||

| Owned |

2,548 | 17,145,139 | ||||||

|

|

|

|

|

|||||

| Total |

5,201 | 34,075,528 | ||||||

|

|

|

|

|

|||||

We have approximately 4.0 million square feet in distribution centers servicing our stores, of which approximately 1.3 million square feet is leased and the remainder is owned. Our distribution centers are located in Arizona, California, Georgia, Illinois, Ohio, Pennsylvania, Tennessee, Texas, and Mexico. Our primary store support center is located in Memphis, Tennessee, and consists of approximately 260,000 square feet. We also have three additional store support centers located in Monterrey, Mexico; Chihuahua, Mexico and Sao Paulo, Brazil. The ALLDATA headquarters building in Elk Grove, California, and the AutoAnything headquarters space in San Diego, California are leased, and we also own or lease other properties that are not material in the aggregate.

In 2004, we acquired a store site in Mount Ephraim, New Jersey that had previously been the site of a gasoline service station and contained evidence of groundwater contamination. Upon acquisition, we voluntarily reported the groundwater contamination issue to the New Jersey Department of Environmental Protection and entered into a Voluntary Remediation Agreement providing for the remediation of the contamination associated with the property. We have conducted and paid for (at an immaterial cost to us) remediation of contamination on the property. We are also investigating, and will be addressing, potential vapor intrusion impacts in downgradient residences and businesses. The New Jersey Department of Environmental Protection asserted, in a Directive and Notice to Insurers dated February 19, 2013 (“Directive”), that we are liable for the downgradient impacts under a joint and severable liability theory, and we have contested any such assertions due to the existence of other entities/sources of contamination, some of which are also named in the Directive, in the area of the property. Pursuant to the Voluntary Remediation Agreement, upon completion of all remediation required by the agreement, we believe we are eligible to be reimbursed up to 75 percent of qualified remediation costs by the State of New Jersey. We have asked the state for clarification that the agreement applies to off-site work, and the state is considering the request. Although the aggregate amount of additional costs that we may incur pursuant to the remediation cannot currently be ascertained, we do not currently believe that fulfillment of our obligations under the agreement or otherwise will result in costs that are material to our financial condition, results of operations or cash flow.

We are involved in various other legal proceedings incidental to the conduct of our business, including several lawsuits containing class-action allegations in which the plaintiffs are current and former hourly and salaried employees who allege various wage and hour violations and unlawful termination practices. We do not currently believe that, either individually or in the aggregate, these matters will result in liabilities material to our financial condition, results of operations or cash flows.

Item 4. Mine Safety Disclosures

Not applicable.

15

Table of Contents

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is listed on the New York Stock Exchange under the symbol “AZO.” On October 21, 2013, there were 2,778 stockholders of record, which does not include the number of beneficial owners whose shares were represented by security position listings.

We currently do not pay a dividend on our common stock. Our ability to pay dividends is subject to limitations imposed by Nevada law. Any future payment of dividends would be dependent upon our financial condition, capital requirements, earnings and cash flow.

The following table sets forth the high and low sales prices per share of common stock, as reported by the New York Stock Exchange, for the periods indicated:

| Price Range of Common Stock | ||||||||

| High | Low | |||||||

| Fiscal Year Ended August 31, 2013: |

||||||||

| Fourth quarter |

$ | 452.19 | $ | 401.93 | ||||

| Third quarter |

$ | 413.28 | $ | 369.47 | ||||

| Second quarter |

$ | 390.11 | $ | 341.98 | ||||

| First quarter |

$ | 386.80 | $ | 351.27 | ||||

| Fiscal Year Ended August 25, 2012: |

||||||||

| Fourth quarter |

$ | 391.90 | $ | 353.38 | ||||

| Third quarter |

$ | 399.10 | $ | 353.80 | ||||

| Second quarter |

$ | 356.80 | $ | 313.11 | ||||

| First quarter |

$ | 341.89 | $ | 303.00 | ||||

During 1998, the Company announced a program permitting the Company to repurchase a portion of its outstanding shares not to exceed a dollar maximum established by the Company’s Board of Directors. The program was most recently amended on June 11, 2013, to increase the repurchase authorization by $750 million to raise the cumulative share repurchase authorization from $12.65 billion to $13.40 billion.

Shares of common stock repurchased by the Company during the quarter ended August 31, 2013, were as follows:

| Period |

Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Maximum Dollar Value that May Yet Be Purchased Under the Plans or Programs |

||||||||||||

| May 5, 2013, to June 1, 2013 |

23,900 | $ | 417.00 | 23,900 | $ | 268,442,619 | ||||||||||

| June 2, 2013, to June 29, 2013 |

397,712 | 415.79 | 397,712 | 853,076,687 | ||||||||||||

| June 30, 2013, to July 27, 2013 |

400,901 | 431.55 | 400,901 | 680,067,382 | ||||||||||||

| July 28, 2013, to August 31, 2013 |

487,000 | 434.55 | 487,000 | 468,441,939 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

1,309,513 | $ | 427.61 | 1,309,513 | $ | 468,441,939 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The Company also repurchased, at fair value, an additional 22,915 shares in fiscal 2013, 24,113 shares in fiscal 2012, and 30,864 shares in fiscal 2011 from employees electing to sell their stock under the Company’s Sixth Amended and Restated Employee Stock Purchase Plan (the “Employee Plan”), qualified under Section 423 of the Internal Revenue Code, under which all eligible employees may purchase AutoZone’s common stock at 85% of the lower of the market price of the common stock on the first day or last day of each calendar quarter through payroll deductions. Maximum permitted annual purchases are $15,000 per employee or 10 percent of compensation, whichever is less. Under the Employee Plan, 18,228 shares were sold to employees in fiscal 2013, 19,403 shares were sold to employees in fiscal 2012, and 21,608 shares were sold to employees in fiscal 2011. At August 31, 2013, 234,744 shares of common stock were reserved for future issuance under the Employee Plan.

16

Table of Contents

Once executives have reached the maximum purchases under the Employee Plan, the Fifth Amended and Restated Executive Stock Purchase Plan (the “Executive Plan”) permits all eligible executives to purchase AutoZone’s common stock up to 25 percent of his or her annual salary and bonus. Purchases by executives under the Executive Plan were 3,454 shares in fiscal 2013, 3,937 shares in fiscal 2012, and 1,719 shares in fiscal 2011. At August 31, 2013, 248,953 shares of common stock were reserved for future issuance under the Executive Plan.

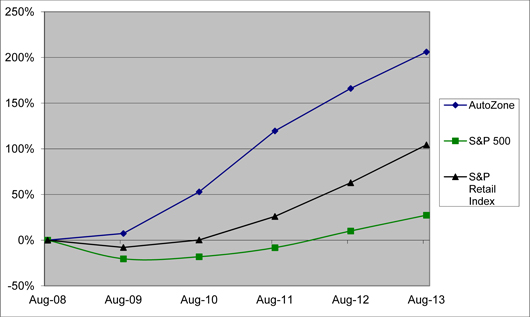

Stock Performance Graph

The graph below presents changes in the value of AutoZone’s stock as compared to Standard & Poor’s 500 Composite Index (“S&P 500”) and to Standard & Poor’s Retail Index (“S&P Retail Index”) for the five-year period beginning August 30, 2008 and ending August 31, 2013.

17

Table of Contents

Item 6. Selected Financial Data

| (in thousands, except per share data, same store sales and selected operating data) |

Fiscal Year Ended August | |||||||||||||||||||

| 2013 (1) | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| Income Statement Data |

||||||||||||||||||||

| Net sales |

$ | 9,147,530 | $ | 8,603,863 | $ | 8,072,973 | $ | 7,362,618 | $ | 6,816,824 | ||||||||||

| Cost of sales, including warehouse and delivery expenses |

4,406,595 | 4,171,827 | 3,953,510 | 3,650,874 | 3,400,375 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

4,740,935 | 4,432,036 | 4,119,463 | 3,711,744 | 3,416,449 | |||||||||||||||

| Operating, selling, general and administrative expenses |

2,967,837 | 2,803,145 | 2,624,660 | 2,392,330 | 2,240,387 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating profit |

1,773,098 | 1,628,891 | 1,494,803 | 1,319,414 | 1,176,062 | |||||||||||||||

| Interest expense, net |

185,415 | 175,905 | 170,557 | 158,909 | 142,316 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes |

1,587,683 | 1,452,986 | 1,324,246 | 1,160,505 | 1,033,746 | |||||||||||||||

| Income tax expense |

571,203 | 522,613 | 475,272 | 422,194 | 376,697 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 1,016,480 | $ | 930,373 | $ | 848,974 | $ | 738,311 | $ | 657,049 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted earnings per share |

$ | 27.79 | $ | 23.48 | $ | 19.47 | $ | 14.97 | $ | 11.73 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted weighted average shares for diluted earnings per share |

36,581 | 39,625 | 43,603 | 49,304 | 55,992 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Same Store Sales |

||||||||||||||||||||

| Increase in domestic comparable store net sales (2) |

0.0 | % | 3.9 | % | 6.4 | % | 5.4 | % | 4.4 | % | ||||||||||

| Balance Sheet Data |

||||||||||||||||||||

| Current assets |

$ | 3,278,013 | $ | 2,978,946 | $ | 2,792,425 | $ | 2,611,821 | $ | 2,561,730 | ||||||||||

| Working (deficit) |

(891,137 | ) | (676,646 | ) | (638,471 | ) | (452,139 | ) | (145,022 | ) | ||||||||||

| Total assets |

6,892,089 | 6,265,639 | 5,869,602 | 5,571,594 | 5,318,405 | |||||||||||||||

| Current liabilities |

4,169,150 | 3,655,592 | 3,430,896 | 3,063,960 | 2,706,752 | |||||||||||||||

| Debt |

4,187,000 | 3,768,183 | 3,351,682 | 2,908,486 | 2,726,900 | |||||||||||||||

| Long-term capital leases |

73,925 | 72,414 | 61,360 | 66,333 | 38,029 | |||||||||||||||

| Stockholders’ (deficit) |

(1,687,319 | ) | (1,548,025 | ) | (1,254,232 | ) | (738,765 | ) | (433,074 | ) | ||||||||||

| Selected Operating Data |

||||||||||||||||||||

| Number of stores at beginning of year |

5,006 | 4,813 | 4,627 | 4,417 | 4,240 | |||||||||||||||

| New stores |

197 | 193 | 188 | 213 | 180 | |||||||||||||||

| Closed stores |

2 | — | 2 | 3 | 3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net new stores |

195 | 193 | 186 | 210 | 177 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Relocated stores |

11 | 10 | 10 | 3 | 9 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Number of stores at end of year |

5,201 | 5,006 | 4,813 | 4,627 | 4,417 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Domestic commercial programs |

3,421 | 3,053 | 2,659 | 2,424 | 2,303 | |||||||||||||||

| Total store square footage (in thousands) |

34,076 | 32,706 | 31,337 | 30,027 | 28,550 | |||||||||||||||

| Average square footage per store |

6,552 | 6,533 | 6,511 | 6,490 | 6,464 | |||||||||||||||

| Increase in store square footage |

4.2 | % | 4.4 | % | 4.4 | % | 5.2 | % | 4.6 | % | ||||||||||

| Inventory per store (in thousands) |

$ | 550 | $ | 525 | $ | 512 | $ | 498 | $ | 500 | ||||||||||

| Average net sales per store (in thousands) |

$ | 1,736 | $ | 1,716 | $ | 1,675 | $ | 1,595 | $ | 1,541 | ||||||||||

| Net sales per store square foot |

$ | 265 | $ | 263 | $ | 258 | $ | 246 | $ | 239 | ||||||||||

| Total employees at end of year (in thousands) |

71 | 70 | 65 | 63 | 60 | |||||||||||||||

| Inventory turnover (3) |

1.6x | 1.6x | 1.6x | 1.6x | 1.5x | |||||||||||||||

| Accounts payable to inventory ratio |

115.6 | % | 111.4 | % | 111.7 | % | 105.6 | % | 96.0 | % | ||||||||||

| After-tax return on invested capital (4) |

32.7 | % | 33.0 | % | 31.3 | % | 27.6 | % | 24.4 | % | ||||||||||

| Adjusted debt to EBITDAR (5) |

2.5 | 2.5 | 2.4 | 2.4 | 2.5 | |||||||||||||||

| Net cash provided by operating activities (in thousands) |

$ | 1,415,011 | $ | 1,223,981 | $ | 1,291,538 | $ | 1,196,252 | $ | 923,808 | ||||||||||

| Cash flow before share repurchases and changes in debt (in thousands) (6) |

$ | 1,007,761 | $ | 949,627 | $ | 1,023,927 | $ | 947,643 | $ | 673,347 | ||||||||||

| Share repurchases (in thousands) |

$ | 1,387,315 | $ | 1,362,869 | $ | 1,466,802 | $ | 1,123,655 | $ | 1,300,002 | ||||||||||

| Number of shares repurchased (in thousands) |

3,511 | 3,795 | 5,598 | 6,376 | 9,313 | |||||||||||||||

| (1) | The fiscal year ended August 31, 2013 consisted of 53 weeks. |

| (2) | The domestic comparable sales increases are based on sales for all domestic stores open at least one year. Relocated stores are included in the same store sales computation based on the year the original store was opened. Closed store sales are included in the same store sales computation up to the week it closes, and excluded from the computation for all periods subsequent to closing. In addition, beginning in fiscal 2013, it also includes all sales through our AutoZone branded websites, including consumer direct ship-to-home sales. All prior period same store sales have been restated to be comparable. The effect of including sales from AutoZone branded websites was not material to any period. |

| (3) | Inventory turnover is calculated as cost of sales divided by the average merchandise inventory balance over the trailing 5 quarters. |

18

Table of Contents

| (4) | After-tax return on invested capital is defined as after-tax operating profit (excluding rent charges) divided by average invested capital (which includes a factor to capitalize operating leases). See Reconciliation of Non-GAAP Financial Measures in Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

| (5) | Adjusted debt to EBITDAR is defined as the sum of total debt, capital lease obligations and annual rents times six; divided by net income plus interest, taxes, depreciation, amortization, rent and share-based compensation expense. See Reconciliation of Non-GAAP Financial Measures in Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

| (6) | Cash flow before share repurchases and changes in debt is defined as the change in cash and cash equivalents less the change in debt plus treasury stock purchases. See Reconciliation of Non-GAAP Financial Measures in Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

We are the nation’s leading retailer, and a leading distributor, of automotive replacement parts and accessories in the United States. We began operations in 1979 and at August 31, 2013, operated 4,836 stores in the United States, including Puerto Rico; 362 in Mexico; and three in Brazil. Each of our stores carries an extensive product line for cars, sport utility vehicles, vans and light trucks, including new and remanufactured automotive hard parts, maintenance items, accessories and non-automotive products. At August 31, 2013, in 3,421 of our domestic stores, we also have a commercial sales program that provides commercial credit and prompt delivery of parts and other products to local, regional and national repair garages, dealers, service stations and public sector accounts. We also have commercial programs in select stores in Mexico, as well as in our stores in Brazil. We also sell the ALLDATA brand automotive diagnostic and repair software through www.alldata.com. Additionally, we sell automotive hard parts, maintenance items, accessories, and non-automotive products through www.autozone.com, and accessories and performance parts through www.autoanything.com, and our commercial customers can make purchases through www.autozonepro.com. We do not derive revenue from automotive repair or installation services.

Executive Summary

We achieved strong performance in fiscal 2013, delivering record net income of $1.016 billion, a 9.3% increase over the prior year, and sales growth of $543.7 million, a 6.3% increase over the prior year. We completed the year with growth in all areas of our business. We are pleased with the results of our retail business and the increase in our commercial business, where we continue to build our internal sales force and continue to refine our parts assortment. Over the past several years, various factors have occurred within the economy that affect both our customers and our industry, including the impact of the recession, continued high unemployment, and other challenging economic conditions. Although we have seen a recent increase in new vehicle sales, we believe our consumers’ cash flows continue to decrease due to the previously listed factors. Given the nature of these macroeconomic factors, we cannot predict whether or for how long these trends will continue, nor can we predict to what degree these trends will impact us in the future.

We believe other macroeconomic factors have adversely affected both our customers and our industry. During fiscal 2013, the average price per gallon of unleaded gasoline in the United States remained at a high level, $3.65 per gallon, compared to $3.57 per gallon during fiscal 2012. We continue to believe gas prices will remain at overall high levels, thereby reducing discretionary spending for all consumers, and, in particular, our customers. With approximately 11 billion gallons of unleaded gas consumed each month across the U.S., each $1 decrease at the pump contributes approximately $11 billion of additional spending capacity to consumers each month. Given the unpredictability of gas prices, we cannot predict whether gas prices will increase or decrease, nor can we predict how any future changes in gas prices will impact our sales in future periods.

An additional macroeconomic factor facing our customer is the reinstitution of payroll taxes back to historic levels. The reduction in our customers’ take home pay as a result of the recent increase in payroll taxes was effective at the beginning of the 2013 calendar year and, at this point, we cannot predict the impact this change has had or will have on our sales in future periods.

During fiscal 2013, failure and maintenance related categories represented the largest portion of our sales mix, at approximately 84% of total sales, with failure related categories continuing to be our strongest performers. While

19

Table of Contents

we have not experienced any fundamental shifts in our category sales mix as compared to previous years, we did experience a slight decline in sales of the maintenance category as a percentage of sales. We believe the slowdown in maintenance related products during fiscal 2013 was largely due to weather related impacts in various regions. Because of the unusually mild winter during fiscal 2012 across parts of the U.S., we saw a reduced benefit from sales of maintenance related products in fiscal 2013 compared to the prior fiscal year. However, sales in the maintenance category did improve in the last quarter of fiscal 2013 due to a more normalized winter in fiscal 2013 as compared to fiscal 2012.

Our primary response to fluctuations in the demand for the products we sell is to adjust our advertising message, store staffing, and product assortment. Specifically, during fiscal 2013, we have closely studied our hub distribution model and store inventory levels and assortment. As a result, we are performing certain strategic tests including adding additional inventory into our hub stores and increasing product availability in our stores. We continue to believe we are well positioned to help our customers save money and meet their needs in a challenging macroeconomic environment.

The two statistics we believe have the closest correlation to our market growth over the long-term are miles driven and the number of seven year old or older vehicles on the road.

Miles Driven

We believe that as the number of miles driven increases, consumers’ vehicles are more likely to need service and maintenance, resulting in an increase in the need for automotive hard parts and maintenance items. While over the long-term, we have seen a close correlation between our net sales and the number of miles driven, we have also seen certain time frames of minimal correlation in sales performance and miles driven. During the periods of minimal correlation between net sales and miles driven, we believe net sales have been positively impacted by other factors, including the number of seven year old or older vehicles on the road. Since the beginning of the fiscal year and through June 2013 (latest publicly available information), miles driven decreased slightly compared to the same period last year.

Seven Year Old or Older Vehicles

Since 2008, new vehicle sales have been significantly lower than historical levels, which we believe contributed to an increasing number of seven year old or older vehicles on the road. We estimate vehicles are driven an average of approximately 12,500 miles each year. In seven years, the average miles driven equates to approximately 87,500 miles. Our experience is that at this point in a vehicle’s life, most vehicles are not covered by warranties and increased maintenance is needed to keep the vehicle operating. According to the latest data provided by the Automotive Aftermarket Industry Association, as of January 1, 2013, the average age of vehicles on the road is 11.3 years as compared to 11.1 years as of January 1, 2012. Although the average age of vehicles continues to increase, it is increasing at a decelerated rate primarily driven by the improvement in new car sales in recent years. However, in the near term, we expect the aging vehicle population to continue to increase, as consumers keep their cars longer in an effort to save money during this uncertain economy. As the number of seven year old or older vehicles on the road increases, we expect an increase in demand for the products we sell.

Results of Operations

Fiscal 2013 Compared with Fiscal 2012

For the fiscal year ended August 31, 2013, we reported net sales of $9.148 billion compared with $8.604 billion for the year ended August 25, 2012, a 6.3% increase from fiscal 2012. This growth was driven primarily by sales from new stores of $222.3 million, the 53rd week sales of $177.7 million, and sales from AutoAnything for a portion of the fiscal year.

At August 31, 2013, we operated 4,836 domestic stores, 362 stores in Mexico and three stores in Brazil, compared with 4,685 domestic stores, 321 stores in Mexico and none in Brazil at August 25, 2012. We reported a total auto parts (domestic, Mexico and Brazil) sales increase of 5.2% for fiscal 2013.

Gross profit for fiscal 2013 was $4.741 billion, or 51.8% of net sales, compared with $4.432 billion, or 51.5% of net sales for fiscal 2012. The improvement in gross margin was primarily driven by lower product acquisition costs, partially offset by the inclusion of AutoAnything (28 basis points).

20

Table of Contents

Operating, selling, general and administrative expenses for fiscal 2013 increased to $2.968 billion, or 32.4% of net sales, from $2.803 billion, or 32.6% of net sales for fiscal 2012. Operating expenses, as a percentage of sales, improved due to lower incentive compensation (19 basis points), partially offset by lower sales growth rates.

Interest expense, net for fiscal 2013 was $185.4 million compared with $175.9 million during fiscal 2012. This increase was primarily due to higher average borrowing levels over the comparable prior year period; partially offset by a decline in borrowing rates. Average borrowings for fiscal 2013 were $3.927 billion, compared with $3.507 billion for fiscal 2012 and weighted average borrowing rates were 4.5% for fiscal 2013, compared to 4.7% for fiscal 2012.

Our effective income tax rate was 36.0% of pre-tax income for fiscal 2013 compared to 36.0% for fiscal 2012.

Net income for fiscal 2013 increased by 9.3% to $1.016 billion, and diluted earnings per share increased 18.3% to $27.79 from $23.48 in fiscal 2012. The impact of the fiscal 2013 stock repurchases on diluted earnings per share in fiscal 2013 was an increase of approximately $1.09.

Effective December 2012, we acquired certain assets and liabilities of AutoAnything, an online retailer of specialized automotive products for up to $150 million, including an initial cash payment of $115 million, up to a $5 million holdback payment for working capital true-ups, and contingent payments not to exceed $30 million. During the third quarter of fiscal 2013, we paid the holdback payment for working capital true-ups of $1.1 million. With this acquisition, we expect to bolster our online presence in the automotive accessory and performance markets. The results of operations from AutoAnything have been included in our Other business activities since the date of acquisition. The purchase price allocation resulted in goodwill of $83.4 million and intangible assets totaling $58.7 million. Goodwill generated from the acquisition is tax deductible and is primarily attributable to expected synergies and the assembled workforce. The contingent consideration is based on the achievement of certain performance metrics through calendar year 2014 with any earned payments due during the first calendar quarter of 2014 and 2015. The fair value of the contingent consideration as of the acquisition date was $22.7 million.

We performed our annual impairment testing in the fourth quarter of fiscal 2013 for the goodwill and indefinite-lived intangible asset related to the acquisition of AutoAnything. Based on an analysis of AutoAnything’s revised planned financial results compared to the initial projections, we determined it was more likely than not the goodwill attributed to AutoAnything was impaired. Accordingly, we performed a goodwill impairment test by comparing the fair value of the reporting unit with its carrying amount, including goodwill. Because the fair value of the reporting unit was lower than its carrying value, we recorded a goodwill impairment charge of $18.3 million during the fourth quarter of fiscal 2013. Based on our evaluation of the future discounted cash flows of AutoAnything’s trade name as compared to its carrying value, it was determined that AutoAnything’s trade name was also impaired. We recorded an impairment charge of $4.1 million during the fourth quarter of fiscal 2013 related to the trade name.