Great Basin Gold Ltd.: Exhibit 99.2 - Filed by newsfilecorp.com

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

| Cautionary Note regarding Forward Looking Statements

|

|

|

|

This discussion includes certain statements that may be

deemed "forward-looking statements" and information. These

forward-looking statements constitute "forward-looking statements" within

the meaning of Section 27A of the Securities Act of 1933

and Section 21E of the Securities Exchange Act of

1934. All statements in this discussion, other than statements of

historical facts, that address future production, reserve potential,

exploration drilling, exploitation activities and events or developments

that the Company expects to take place in the future are forward- looking

statements and information. Although the Company believes the expectations

expressed in such forward- looking statements and information are based on

reasonable assumptions, such statements are not guarantees of future

performance and actual results or developments may differ materially from

those in the forward-looking statements and information. Factors that

could cause actual results to differ materially from those in

forward-looking statements include market prices, exploitation and

exploration successes, drilling and development results, continued

availability of capital and financing and general economic, market or

business conditions. Investors are cautioned that any such statements are

not guarantees of future performance and actual results or developments

may differ materially from those stated herein. |

|

|

| Cautionary Note regarding Non-GAAP Measurements |

|

|

|

Cash cost per ounce/tonne is a not a generally accepted

accounting principle ("GAAP") based figure but rather is intended to serve

as a performance measure providing some indication of the mining and

processing efficiency and effectiveness of operations. It is determined by

dividing the relevant mining and processing costs including royalties by

the ounces produced/tonnes milled in the period. There may be some

variation in the method of computation of "cash cost per ounce/tonne" as

determined by the Company compared with other mining companies. Cash costs

per ounce/tonne may vary from one period to another due to operating

efficiencies, waste to ore ratios, grade of ore processed and gold

recovery rates in the period. We provide this measure to our investors to

allow them to also monitor operational efficiencies. As a Non-GAAP

Financial Measure cash costs should not be considered in isolation or as a

substitute for measures of performance prepared in accordance with GAAP.

Adjusted loss per share is also a Non-GAAP measure and is calculated by

excluding the impact of certain fair-value accounting charges and once-off

transactions. We also make reference in our disclosures to “working

capital” which is also a Non-GAAP measure and includes cash and cash

equivalents, trade and other receivables, current inventories, trade

payables and accrued liabilities. There are material limitations

associated with the use of such Non-GAAP measures.

|

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Great Basin is a mineral exploration and development company

that is currently focused on delivering two advanced stage projects: trial

mining at the Hollister Gold Project (“Hollister”) on the Carlin Trend in

Nevada, USA and production ramp-up of the Burnstone Mine (“Burnstone”) in

the Witwatersrand Goldfields in South Africa. Due to delays experienced in the Burnstone production ramp-up which have caused near term liquidity challenges for the Company, a special committee of directors was formed to pursue a strategic review process with the objective to alleviate these strains by exploring alternatives which include possible asset divestitures, refinancing and/or other financial restructuring. The strategic process is further discussed below.

This Management’s Discussion and Analysis ("MD&A") should

be read in conjunction with the annual financial statements of Great Basin Gold

Ltd. ("Great Basin", the "Company", or the “Group”) for the years ended December

31, 2011 and 2010 which are prepared in accordance with International Financial

Reporting Standards (“IFRS” or “GAAP”) and are available through the internet on

SEDAR at www.sedar.com. All dollar amounts herein are expressed in Canadian

Dollars (“$”) unless stated otherwise. This MD&A is prepared as of August

14, 2012.

Combined Operations

|

3 months

ended |

6 months

ended |

| June 30 2012 |

March 31 2012 |

June 30 2011 |

June 30 2012 |

June 30 2011 |

| Recovered Au eqv oz |

21,080 |

22,911 |

31,651 |

43,990 |

61,244 |

| Au eqv oz sold |

20,473 |

21,555 |

40,141 |

42,028 |

60,259 |

| Realized Au eqv price |

$1,581 |

$1,548 |

$1,413 |

$1,564 |

$1,379 |

| Revenue ($’000) |

$32,371 |

$33,373 |

$56,738 |

$65,744 |

$83,081 |

| (Loss) profit from operating activities

($’000) |

($19,641) |

($7,650) |

$6,808 |

($27,291) |

$6,431 |

| Net (loss) profit ($’000) |

($21,990) |

($17,770) |

($1,051) |

($39,760) |

($21,392) |

| Adjusted loss per share |

($0.05) |

($0.03) |

($0.00) |

($0.08) |

($0.02)

|

Hollister

23,720 tonnes (Q1, 2012:21,142 tonnes) were trial mined at the Company's

Hollister operation in Q2, 2012 yielding 14,857 gold equivalent contained ounces

(Q1, 2012:20,459 Au eqv oz). Although tonnage mined was slightly below planned

levels, a lower-than-plan mining grade of 0.63 Au eqv oz/t (Q1, 2012:0.97 Au eqv

oz/t) resulted in a lower than planned recovery of 14,688 Au eqv oz for the

quarter (Q1, 2012:16,240 Au eqv oz). The high grade nature of the Hollister ore

body can lead to quarterly grade fluctuations which is evident when comparing

the grade of 1.35 Au eqv oz in Q2 2011 to the grade of 0.63 Au eqv oz/t achieved

in Q2 2012. In order to counter decreasing grade trends, efforts in the current

(third) quarter are focused on decreasing stope width and controlling dilution

with early indications of up to 20% reduction in stope widths being achievable. Long hole stoping accounted for approximately 11% of production during the period and was also the main contributor to the excessive dilution. Current mine planning suggests an increase in grade for the remainder of the year as a result of higher-grade stopes being available for mining. The Company is currently updating its mine plan in conjunction with updating reserve estimates which may impact production estimates going forward.

During the first half of 2012, Hollister experienced challenges

in mining flexibility due to the lack of available working stopes as well as a

high rate in personnel turnover. Development for the quarter was focused on

providing access to the Upper Zone for additional delineation, infrastructure

construction, and accelerated production from higher grade mining areas.

The Esmeralda Mill at 93% availability processed 25,811 dry

tonnes during the quarter (Q1, 2012:20,042 tonnes) and during Q2 2012 achieved

recoveries of 90% and 59% for gold and silver respectively (Q1, 2012:87% Au and

62% Ag). Work on the acid wash and carbon regeneration circuit was completed

during June, 2012 and all dore is now being poured on site.

2

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

14,863 Au eqv oz were sold during the quarter (Q1, 2012:15,357

Au eqv oz) with Au eqv oz recovered not sold decreasing by 2,239 to 12,208 Au

eqv oz on June 30, 2012. Cash costs per Au eqv oz for the quarter of $983 were

recorded (Q1, 2012:$850) and were negatively impacted by the lower mining grade

achieved as well as the additional transport costs incurred to process the

carbon at Rand Refinery in South Africa.

Burnstone

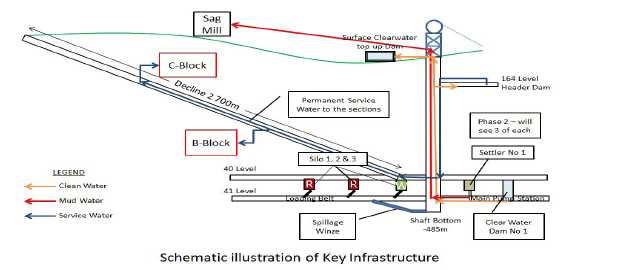

Technical challenges at the Burnstone mine continued in the second quarter with the temporary service water handling system failing to serve the increasing mining areas during May and June which severely adversely affected production levels. Development and stoping activities were constrained due to the limited supply of service water. Although a temporary solution was implemented by early June, and production and development levels in July were back to levels achieved at the end of 2011, quarterly targeted levels for development and stoping were not met and this will have a related negative impact on production targets for the remainder of the year.

As a result of the infrastructural challenges, the Burnstone

operations produced 6,392 Au oz for the quarter (Q1, 2012: 6,671 Au oz),

compared to the forecast of 17,790 Au oz. Good progress is being made with the

completion of the permanent water handling system expected to be commissioned

during the September quarter which will reduce the risk of production

interruptions as a result of service water supply.

Good progress was also made during the quarter with vertical

shaft and other infrastructure construction that will enable the mine to regain

its momentum in meeting the increasing development and production targets. Cash

costs for the quarter of $2,325 were recorded (Q1, 2012 : $2,182) and were

impacted by the low head grade of material delivered to the mill but due to the

low volumes from the delay in ramp-up these costs are not yet considered

meaningful relative to post-ramp-up (steady state) production cost estimates.

Steady state production is not expected to be achieved until 2014.

The Company plans to implement a number of steps in the near term as part of its Burnstone turnaround plan. The Company believes it will be able to reduce costs through reduction of off-site supervisory and premises costs and improved use of labour and water-handling. These cost saving actions could result in aggregate reductions in the range of ZAR20 million ($2.5 million) per month after a few months. Based in part on discussions with the Snowden Group, the independent technical advisors retained by the Company’s lenders, the Company's management currently estimates production in 2012 of 30,000 Au eqv ounces and 90,000-100,000 Au eqv ounces in 2013.

Financial Results and Corporate Matters

Revenue of $32 million was recorded for the quarter, a decrease of 44% over the comparative period in 2011. The decrease in revenue can largely be attributed to the decrease in ounces sold from the Company’s Nevada operations which had sold a record amount of metal in Q2 2011 as a result of exceptionally high grade material and settlement of some ounces recovered in Q1 2011. The increase in cash and non-cash costs had a negative impact on the loss from operations which came to $20 million (Q2, 2011:$7 million profit). A further $1.4 million impairment charge arising from the loan advanced to our South African BEE partner (Tranter) was recorded. The guarantee has now been fully called upon and the monies loaned by Great Basin to Tranter and in turn paid by Tranter to its banker, Investec, have been written down to a nominal value in the Great Basin accounts. The operational performance from the Nevada and South African operations resulted in a working capital deficit of approximately $23 million on June 30, 2012.

Strategic Review Process

The Company also announced that its Board of Directors has recently initiated a review process to consider a range of strategic alternatives with a view to preserving and enhancing shareholder value in light of the continuing financial challenges resulting from the operational challenges experienced particularly with the production ramp up at the Burnstone mine. Strategic alternatives are likely to include, but are not limited to, the sale of all or a portion of the Company's assets, a merger or other business combination transaction involving a third party acquiring all of the Company, a capital raising, sale of royalties or metal streams, recapitalization, reorganization, or restructuring of the Company, as well as continued execution of the Company's existing business plan, or some combination of these alternatives.

A special committee ("Special Committee"), consisting of

independent directors, Ron Thiessen, Patrick Cooke, Anu Dhir, Barry Coughlan and

Philip Kotze has been appointed to oversee the strategic review process. CIBC World Markets Inc. (“CIBC”) has been retained as financial advisor to the Board.

As part of this strategic review process the Company’s President, Chief Executive Officer (“CEO”) and director, Mr Dippenaar has resigned with immediate effect and Mr Lou van Vuuren, the Company’s Chief Financial Officer (“CFO”) has been appointed as Interim CEO with immediate effect. In addition, Patrick Cooke, a director of the Company and the audit committee chair, will temporarily serve as unremunerated Interim CFO.

The Company has implemented an aggressive cost reduction program and is also working with its lenders to potentially restructure the current term loan facilities to improve the Company’s cash flow in the short to medium term. The Special Committee currently intends to seek to raise through a combination of asset sales or new equity a minimum amount of $60 million to relieve the near and intermediate liquidity concerns.

3

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

It is the Company's current intention not to disclose developments with respect to the strategic review process unless and until the Board of Directors has approved a specific transaction or otherwise determines that disclosure is necessary or appropriate. Investors should be aware that financing will be solicited on terms the Company can not currently predict and that a transaction could be announced at any time. The Company cautions that there are no assurances or guarantees that the process will result in a transaction or, if a transaction is undertaken, as to the terms or timing of such transaction.

Ron Thiessen, Great Basin Chairman, commented: “The water infrastructure setbacks at our Burnstone mine and the slower access to higher grade stopes at Hollister converged at a difficult time and have created a near term liquidity challenge for the Company which the Special Committee will need to address as a priority. While the Board believes in the underlying value of the Company’s two principal gold projects, our current financial situation requires that we investigate all potential liquidity sources. As our financial situation and the results of our Strategic Review process may require us to institute material changes in the Company, the Board felt changes in the executive suite were prudent. Mr Dippenaar oversaw the development of the Company’s two gold mining projects during a period which witnessed the worldwide financial crisis, skyrocketing capital cost and other challenges which the Company ultimately overcame. We thank him for his dedication and wish him well in his future endeavours. Mr van Vuuren has been Great Basin’s CFO since 2008, has longterm relationships with the Company’s lenders and understands every facet of the Company’s operations. He will be of key assistance to the Special Committee and we welcome his assumption of duties as Interim CEO.”

Revenue

The table below provides a summary of Au eqv oz sold.

|

3 months

ended |

6 months

ended |

| June 30 2012 |

March 31 2012 |

June 30 2011 |

June 30 2012 |

June 30 2011 |

| Au eqv oz sold – Nevada operations |

14,863 |

15,357 |

34,522 |

30,220 |

51,846 |

| Au eqv oz sold – South African operations

|

5,610 |

6,198 |

5,619 |

11,808 |

8,413 |

| Total Au eqv oz sold |

20,473 |

21,555 |

40,141 |

42,028 |

60,259

|

Au eqv oz sold for the quarter by our Nevada operation were

impacted by the time delay in completing final settlements for the carbon

processed through third party refiners as well as the lower average contained Au

eqv grade and tonnes trial mined. Recovered metal not sold decreased by 2,239 Au

eqv oz to 12,208 Au eqv oz during the quarter following a settlement adjustment

of 2,360 Au eqv oz from in-carbon inventory. The completion of the upgrade to

the acid wash and carbon regeneration circuit in June 2012 allowed for dore to

again be poured at our Esmeralda mill which reduced our dependency on third

party refiners.

Revenue from our South African operation was below plan for Q2

2012 due to challenges experienced in increasing the levels of production while

completing the permanent water reticulation and materials hoisting

infrastructure. Ore tonnages for the quarter were constrained by the available

water reticulation and hoisting capacity which resulted in limited stoping in

the mining areas. The completion of the permanent water reticulation and

hoisting infrastructure during Q3 2012 will allow for an increase in ore tonnes

mined and Au oz recovered. Refer to section 4.2 below for additional information

on the impact of the infrastructural constraints on production for the second

quarter.

Included in revenue for the quarter is $1.8 million (Q1

2012:$1.9 million) derived from the sale of 63,013 Ag oz (Q1 2012:71,524 Ag oz)

trial mined at our Hollister property.

4

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Production costs

The following table provides a breakdown of the production

costs incurred.

|

3 months

ended |

6 months

ended |

| June 30 2012 |

March 31 2012 |

June 30 2011 |

June 30 2012 |

June 30 2011 |

| Production costs – Nevada operations

($’000) |

16,540 |

13,043 |

20,840 |

29,583 |

32,080 |

| Production costs – South African operations

($’000) |

13,625 |

14,028 |

8,432 |

27,653 |

10,888 |

| Total production costs ($’000) |

30,165 |

27,071 |

29,272 |

57,236 |

42,968 |

| Cash production cost per Au eqv oz – Nevada

operations |

$983 |

$850 |

$611 |

$915 |

$631 |

| Cash production cost per Au oz – South

African operations |

$2,325 |

$2,182 |

$1,883 |

$2,250 |

$2,300 |

| Cash production cost per tonne – Nevada

operations |

$566 |

$651 |

$703 |

$603 |

$680 |

| Cash production cost per tonne – South

African operations |

$58 |

$89 |

$57 |

$69 |

$63 |

The increase in cash production costs for the Nevada operations

as compared to Q1, 2012 as well as the comparative 2011 quarter is mainly due to

the in-carbon gold transport costs incurred in sending the carbon to Rand

Refinery in South Africa as well as the lower grade material extracted from

trial mining activities. Although the additional carbon transport costs also

negatively impacted on the costs per tonne, the comparison of the costs per

tonne is a more accurate indication of the cost control efforts at our Nevada

operations and also highlights the impact on cash costs as a result of grade

variances.

The average head-grade of material delivered to the mill at our

South African operations negatively impacted on the cost on a per ounce basis.

Cost per tonne remains within the target range with the impact of an increase in

volume evident when the cost per tonne of Q1 2012 is compared to the cost per

tonne for Q2 2012.

Depletion charge

|

3 months

ended |

6 months

ended |

| June 30 2012 |

March 31 2012 |

June 30 2011 |

June 30 2012 |

June 30 2011 |

| Nevada operations ($’000) |

1,086 |

1,004 |

1,625 |

2,090 |

2,720 |

| South African operations ($’000) |

51 |

56 |

231 |

107 |

270 |

| Total ($’000) |

1,137 |

1,060 |

1,856 |

2,197 |

2,990

|

This is a non-cash amortization charge on the Hollister and

Burnstone mineral properties.

Depreciation charge

|

3 months

ended |

6 months

ended |

| June 30 2012 |

March 31 2012 |

June 30 2011 |

June 30 2012 |

June 30 2011 |

| Nevada operations ($’000) |

993 |

970 |

1,265 |

1,963 |

1,986 |

| South African operations ($’000) |

3,050 |

2,417 |

4,719 |

5,467 |

5,212 |

| Total ($’000) |

4,043 |

3,387 |

5,984 |

7,430 |

7,198

|

This is a non-cash depreciation charge for the Nevada and South

African operations.

Exploration expenses

The exploration expenses predominantly relate to exploration at

our Hollister property which amounted to $2.4 million for the quarter (Q1

2012:$1.7 million) and $4.1 million year to date (2011:$5.5 million). The

balance relates to our Tanzanian properties, with minimal costs incurred on

exploration activities at Burnstone.

5

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Pre-development expenses

Pre-development expenditures relate to underground development

at our Hollister Project which amounted to $5.1 million (Q1 2012:$4.7 million)

for the quarter and $9.8 million year to date (2011:$7.4 million). Additional

development was incurred during H1 2012 to improve flexibility for trial mining

for the remainder of 2012. Underground development costs at our Hollister

project will be expensed until such time as the Environmental Impact Statement

(“EIS”) has been completed (expected Q3 2012). Refer to section 4.1 for more

details on the Hollister Project permitting.

Foreign exchange gain

This movement predominantly relates to the fluctuation between the Canadian dollar (“$”) and United States dollar (“US$”) on the US$150 million term facility agreement as well as the associated Zero Cost Collar (“ZCC”) hedge structure as these are denominated in US$.

Stock based compensation

The income statement charge relating to this non-cash expense

is a function of the quantum and timing of stock options issued with the

valuation and charge related thereto a Black Scholes function of the option

price and volatility of the Company’s share price. As a result of the decline in

the Company’s share price and to retain key decision makers and employees,

Directors, employees and certain consultants were allowed to cancel unexercised

employee and non-employee stock options and receive new options equal to 50% of

the cancelled options at an exercise price of $0.75 and vesting period of 24

months. The cancellation of these options was concluded on June 7, 2012. The

impact of the cancellation and replacement of these options will have a $1.7

million impact on earnings over the 24 month vesting period.

Impairment of loan due from related party

An impairment provision for a further $1.4 million (Q1

2012:$2.6 million) was recorded during the quarter against the loan advanced to

our BEE partner under the 2010 guarantee agreement as a result of the prolonged

decrease in the value of the Company shares owned by our BEE partner that serves

as collateral for the advance. Refer to section 7 for further details.

Loss on derivative instruments

| |

a. |

Unrealized profit (loss) and mark-to-market

adjustments on financial instruments |

| |

|

|

| |

|

A net profit of $8.1 million (Q1 2012: loss of $0.5 million) was recognized during the quarter on the fair value movement of the ZCC hedge programs totaling to a year to date profit of $7.6 million (2011:loss of $7.4 million) . A fair value loss of $7.3 million was recorded in March 2011 on initial recognition of the ZCC hedge program for the US$70 million term loan. The fair value adjustment recorded in the financial statements is calculated with reference to the price of the call options and is impacted by gold price volatility, US interest rates and the quantity and remaining term of the put and call options in the structure. Refer to section 11 for further detail on the ZCC hedge structures. |

| |

|

|

| |

b. |

Loss on settlement of Senior Secured

Notes |

| |

|

|

| |

|

During Q1 2011 this non-cash accounting charge of $8.8

million was recorded as a result of the accounting policy followed for the

Senior Secured Notes that were issued in 2008. A monthly accretion charge

to increase the recorded liability was processed to increase the liability

to the settlement value over the maturity period of the notes. Due to the

notes being settled on March 15, 2011 as opposed to their original due

date of December 12, 2011 the remaining accretion charge was recorded on

the day of settlement, resulting in an accounting loss on settlement. From

a cash flow perspective the notes were settled in terms of the note

agreement and no additional costs were incurred on

settlement. |

Other comprehensive loss

A $25 million cumulative translation adjustment debit was

recorded for the quarter (Q1 2012:$19 million credit) relating to the South African Rand (“ZAR”) weakening

and the US$ strengthening against the $. The translation adjustment is recorded

on conversion of the respective subsidiaries’ trial balances from their

functional currency to the reporting currency of the Company.

6

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

| 3. |

Financial condition review |

Total assets

Total assets increased by $38 million and current assets

decreased by $6 million since December 31, 2011, predominantly due to the

decrease in cash and cash equivalents and trade and other receivables while the

recorded value of inventories increased. The net movement in total assets

includes a $13 million depreciation and depletion charge as well as $7 million

credit in foreign exchange movement on property, plant and equipment following

the devaluation of the ZAR against the $.

Total liabilities

Total liabilities increased by $25 million since December 31,

2011 mainly due to the following reasons:

-

Trade payables and accrued liabilities

Increased by $22 million

following the execution of a $25 million short term gold advance in June 2012.

-

Long term debt

The Convertible Debentures increased by $4 million due to

the accretion charge being recorded over the term of this facility.

-

Other liabilities

The fair value adjustment on the ZCC programs resulted

in a $7 million decrease in the liability.

Shareholder’s equity

During the six months ended June 30, 2012, the Company’s issued

share capital increased by 76.7 million common shares due to the completion of a

$57 million public offering in April 2012.

At June 30, 2012 and the date of this MD&A, the Company had

552 million common shares and 38 million share purchase warrants issued and

outstanding. A further 16 million share options were also issued and

outstanding.

Liquidity

The Company generated net cash of $3.6 million from operating

activities during the quarter, compared to $23.8 million for the comparative

period. The pre-development costs incurred at the Company’s Hollister project

are being expensed and are also included under cash utilised in operating

activities as opposed to investment activities where capital development is

included.

Cash utilized in investment activities decreased to $34.3

million during the quarter compared to $58.1 million in Q2 2011.

Net proceeds of $3.5 million were received from financing

activities during Q2 2012 (Q2 2011:$4.4 million). The net proceeds relate

predominantly to the closing of the over-alotment of the March 2012 public

offering (refer below) and a further $10 million drawn on the $150 million

credit facility.

The Company monitors its spending plans, repayment obligations

and cash resources and acts with the objective of ensuring that there is

sufficient capital in order to meet short term business requirements, after

taking into account cash flows from operations and the Company’s holdings of

cash and cash equivalents.

The slower than planned production build-up during the later

part of Q2 2011 at Burnstone had a consequential impact on the cash resources of

the Company. On March 15, 2012 the Company announced that it has entered into an

agreement pursuant to which a syndicate of Underwriters have agreed to, on a

bought deal basis, to buy 66,700,000 units of the Company (the “Units”), at a

price of $0.75 per unit, for aggregate gross proceeds of approximately

$50 million (the "Offering"), by way of a short form prospectus. Each unit

consisted of one common share of Great Basin Gold (a “Common Share”) and one

half of a purchase warrant (each whole warrant, a “Warrant”). Each warrant will

be exercisable for a period of 2 years following the closing of the Offering at

an exercise price of $0.90 per warrant. The Offering successfully closed on

March 30, 2012 with the 15% over-allotment option granted to the Underwriters

closing on April 5, 2012. Net proceeds from the Offering, totaling $54 million,

were primarily used for the production ramp up of the Burnstone Mine.

7

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Strategic Review Process

On August 14, 2012 the Company announced that its Board of

Directors has recently initiated a review process to consider a range of

strategic alternatives with a view to preserving and enhancing shareholder value

in light of the continuing financial challenges resulting from the operational

deficiencies experienced particularly with the production ramp up at the

Burnstone mine. Strategic alternatives are likely to include, but are not

limited to, the sale of all or a portion of the Company's assets, a merger or

other business combination transaction involving a third party acquiring all of

the Company, a capital raising, recapitalization, reorganization, or

restructuring of the Company, as well as continued execution of the Company's

existing business plan, or some combination of these alternatives.

A Special Committee ("Special Committee"), consisting of

independent directors, Ron Thiessen, Patrick Cooke, Anu Dhir, Barry Coughlan and

Philip Kotze has been appointed to oversee the strategic review process. CIBC

has been retained as financial advisor to the Board.

The Company has also implemented an aggressive cost reduction

program and is also working with its lenders to potentially restructure the

current term loan facilities to improve the Company’s cash flow in the short to

medium term.

It is the Company's current intention not to disclose

developments with respect to the strategic review process unless and until the

Board of Directors has approved a specific transaction or otherwise determines

that disclosure is necessary or appropriate. The Company cautions that there are

no assurances or guarantees that the process will result in a transaction or, if

a transaction is undertaken, as to the terms or timing of such transaction.

At June 30, 2012, the Company had a net working capital1

deficit of $23 million that included $17 million in cash reserves.

The Company has no "Purchase Obligations", defined as “any

agreement to purchase goods or services that is enforceable and legally binding

on the Company that specifies all significant terms, including: fixed or minimum

quantities to be purchased; fixed, minimum or variable price provisions; and the

approximate timing of the transaction”.

| 4. |

Operations review |

| |

|

| 4.1 |

Nevada Operations |

The Company’s Nevada operations consist of trial mining at the

Hollister Gold Project (“Hollister”) located in the northern part of the Carlin

Trend and the Esmeralda Property and Mill (“Esmeralda”) located in south west

Nevada close to the border between Nevada and California. Great Basin’s surface

exploration efforts at Hollister during 1997-2001 resulted in the discovery and

delineation of several high-grade epithermal gold-silver vein systems on the

property. The main vein systems, called Clementine and Gwenivere, have been

accessed by decline and underground development for geological and resource confirmation and trial extraction of mineral resources; the

development also provides staging for the ongoing exploration and development

drilling that is in progress.

______________________________

1 Working capital

includes cash and cash equivalents, trade and other receivables, inventories,

trade payables and accrued liabilities and is considered a non-GAAP measure.

8

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

The Environmental Impact Statement (EIS) process for the

Hollister Project is currently underway by the Bureau of Land Management

(“BLM”). Pending the completion of the EIS process and receipt of BLM approval

for the amended Plan of Operations, the underground exploration and development

activities at Hollister must be conducted within the 275,000 ore tons per year

limit set out in the Water Pollution Control Permit issued by the Nevada

Department of Environmental Protection, and in a manner that aims to fully

protect the environment and archaeological resources near the development and

will not create any additional surface disturbance or significant new

environmental impacts.

Esmeralda consists of patented and unpatented mining claims,

fee lands, water rights and a mill. Ore extracted through the trial mining

activities conducted at Hollister is trucked to Esmeralda for metallurgical

processing.

Other features of Esmeralda include crushing facilities,

stockpile areas, waste rock facilities, roads and other miscellaneous areas.

There are currently no mining activities or further exploration work being

conducted at Esmeralda.

Esmeralda is approximately 220 miles (354 kilometers) from

Winnemucca and approximately 290 miles (467 kilometers) from Hollister with 80%

of the latter distance over paved roads.

Trial stoping and milling

|

3 months

ended |

6 months

ended |

| June 30 2012 |

March 31 2012

|

June 30 2011 |

June 30 2012 |

June 30 2011

|

| Ore tonnes to surface |

23,719 |

21,142 |

25,297 |

44,861 |

47,125 |

| Contained Au oz extracted |

13,311 |

18,087 |

28,075 |

31,398 |

48,252 |

| Contained Ag oz extracted |

72,144 |

110,712 |

233,880 |

182,856 |

393,328 |

| Contained Au eqv oz extracted |

14,857 |

20,459 |

34,246 |

35,316 |

56,680 |

| Contained average grade Au oz/tonne

(gram/tonne) |

0.56 (17.45 g/t) |

0.86 (26.6 g/t) |

1.11 (34.52 g/t) |

0.70 (21.77 g/t) |

1.02 (31.85 g/t) |

| Contained average grade Ag oz/tonne

(gram/tonne) |

3.04 (94.55 g/t) |

5.24 (162.9 g/t) |

9.25 (287.56 g/t) |

4.08 (126.78 g/t) |

8.35 (259.71 g/t)

|

| Tonnes milled |

25,811 |

20,042 |

22,237 |

45,853 |

43,871 |

| Recovered Au oz |

13,625 |

14,758 |

23,179 |

28,383 |

45,191 |

| Recovered Ag oz |

49,589 |

69,147 |

151,825 |

118,736 |

263,582 |

| Recovered Au eqv oz |

14,688 |

16,240 |

26,757 |

30,927 |

50,839 |

| Recovery % Au |

90% |

87% |

95% |

89% |

92% |

| Recovery % Ag |

59% |

62% |

75% |

61% |

75% |

| Au eqv oz sold |

14,863 |

15,357 |

34,522 |

30,220 |

51,846

|

The Nevada operations extracted 14,857 Au eqv ounces from trial mining activities during the quarter, (Q1 2012: 20,459). As previously indicated, the high grade nature of the Hollister ore body can lead to quarterly grade fluctuations which is evident when comparing the grade of 1.35 Au eqv oz in Q2 2011 to the grade of 0.63 Au eqv oz/t achieved in Q2 2012. Current mine planning suggests an increase in grade for the remainder of the year as a result of higher grade stopes being available for mining. The Company is currently updating its mine plan in conjunction with updating reserve estimates which may impact production estimates going forward.

__________________________________

2 Gold

equivalent (“Au eqv”) calculations use US$1,400/oz for Au and US$30/oz for

Ag.

9

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

The decision taken in the beginning of 2012 to focus on

additional ore development with the aim to improve mining flexibility by

increasing the availability of additional stopes to allow for improved grade

blending of extracted ore, is expected to have a positive impact on the mining

grade for the remainder of the year.

Recoveries from our Esmeralda mill improved during Q2 2012 due

to more effective carbon stripping following the completion of the installation

of the remaining components of the acid wash and carbon regeneration circuit

during the quarter. Further improvements to recoveries are expected in Q3 2012

as the newly commissioned stripping circuit is optimized. The final shipments of

carbon to Rand Refinery in South Africa were completed during the quarter with

the final settlement of recoveries from the carbon to be finalized during Q3

2012. Metal in-process and at the refiners decreased by 2,239 Au eqv oz to

12,208 Au eqv oz at the end of the quarter as a result of the discontinuing of

the carbon shipments as well as a carbon inventory adjustment on final assays

received. Inventory balances are expected to decrease further during Q3 2012 now

that dore is being poured at the Esmeralda mill again and as a result of the

settlement of the final assays on the carbon campaign.

Recovered ounces are expected to return to the quarterly

average of 20,000 – 24,000 Au eqv oz as a result of the improvement in mining

grade well as the further improvement in recoveries.

Progress on the Environmental Impact Statement

The Draft EIS was published in the federal register on June 1,

2012, which commenced a 45 day public comment process which ended June 15.

Twenty eight comment letters and/or emails were received. Management is of the

opinion that the comments received have already been substantively addressed in

the Draft EIS, but any decision lies with BLM. The Company will meet with BLM

and the third party contractor to review the comments and decide on the approach

to responding to those comments. Should BLM agree with management that no

additional analyses will be necessary the targeted timing for the record of

decision would remain late November 2012.

Underground Exploration

In total 65 boreholes (15,656 feet or 4,744 meters) were

completed during the quarter. These comprised 2 exploration and cover boreholes

testing Pit Feeder targets (totaling 1,507 feet or 457 meters), and 63 stope

delineation holes (totaling 14,173 feet or 4,295 meters). As of the end of June

2012, three (3) drills were running underground; the Bazooka drill at 5460 MB

Main Clementine, the SJ 252 in the 5050 WLAT MB1 East Clementine; the U6 drill

in the 5190WLAT effecting Gloria in fill.

Surface Exploration

The target rationalization and prioritization at Hollister

continued during the reporting period with a number of new targets to be

investigated in future. These targets include:

-

a number of structures that are similar to those that control the geometry

of the Gwenivere and Clementine vein systems;

-

To the southeast, altered intrusive rocks have been interpreted from the

geophysical data, interfacing with the Hatter vein system. The planned Hatter

drilling program will provide orientated core for the analysis of structural

controls to the vein system. Surface mapping has indicated a ENE-WSW trend (as

opposed to E-W). An initial borehole completed in May confirmed two

orientations of mineralized veining, supporting a N-S and E-W structural

control;

The existence of Carlin age (38-43 Million year old)

mineralization in the southeastern portion of the claim block cannot be ruled

out. In this area, a conspicuous structural interface with the Carlin Trend has

been identified which warrants further investigation. CSMAT high resolution

resistivity data, when integrated with empirical borehole data, has defined the

potential for a number of new vein system targets. Final approvals to continue

with the surface drilling program were obtained from the BLM in May following a

site visit. Initial drilling on the surface diamond drilling

program planned for the Hatter and Velvet South / Butte East targets was

initiated in May 2012. Two boreholes were completed on the Hatter and Velvet

targets while the planned surface program includes a further eight orientated

core boreholes on the Hatter target and in the order of twenty-two boreholes

testing the Butte East and Velvet South targets. The surface drilling program

will be continued once adequate cash flow from operations are generated to fund

the program.

10

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Preliminary assay results for the 2 Hatter / Velvet surface

boreholes are indicated below:

Vein

System |

Drill Hole ID |

Vein Intersect

(ft) |

Drilled

Thickness (ft) |

Est.

True

Thickness

(ft) |

Analytical

Results |

From |

To |

Au

(opt) |

Au

(g/t) |

Ag

(opt) |

Ag

(g/t) |

| Hatter |

HAT 002 |

1397.5 |

1398.4 |

0.9 |

0.3 |

0.069 |

2.37 |

3.2 |

109 |

| Hatter |

HAT 002 |

1473.2 |

1474.7 |

1.5 |

0.5 |

0.170 |

5.83 |

0.1 |

3 |

| Velvet |

VEL 003 |

290.0 |

293.0 |

3.0 |

1.7 |

0.061 |

2.10 |

<0.1 |

0.6 |

| Velvet |

VEL 003 |

370.4 |

374.2 |

4.2 |

2.4 |

0.071 |

2.44 |

0.1 |

4 |

| Velvet |

VEL 003 |

795.9 |

801.5 |

4.6 |

2.6 |

0.106 |

3.64 |

<0.1 |

0 |

Plans for remainder of 2012

The Company plans to continue its trial mining (ore removal and

test-processing) activities at Hollister within the allowable ore tonnage

authorizations of its existing permits, with all extracted material to be

processed at the Esmeralda mill. The Nevada operations plan to produce an

estimated 70,000 to 80,000 Au eqv oz in 2012 at a cash production cost estimated

to range between US$850 to US$950 for the full year.

The Company is continuing with underground infill drilling with

a view to bringing the current inferred mineral resources into the indicated or

measured categories, as well as step-out drilling to further explore the

potential for western, eastern and Upper Zone extensions to the mineralized vein

systems. The results of underground mapping and exploration drilling continue to

refine the Company’s understanding of the Hollister Property deposit, to the

extent that additional vein style mineralization targets have been identified

outside of the Clementine – Gwenivere system. Surface drilling to further test

the Hatter and Butte East / South Velvet targets has been put on hold and will

be dependent on sufficient cash resources.

The Company will also continue working on finalization of the

EIS for Hollister by Q4 2012.

| 4.2 |

South African operations |

The Burnstone Mine is located in the South Rand area of the

Witwatersrand Goldfields, approximately 50 miles (80 kilometers) southeast of

the city of Johannesburg and near the town of Balfour. The Burnstone Mine has

received all of the required permits to complete the development and to commence

full-scale underground mining. Blocks B and C are the areas of the ore body to

be mined in the next 36 months, while underground access to the remaining areas

of the ore body under the mine plan is being developed.

11

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Production results

|

3 months

ended |

6 months

ended |

| June 30 2012 |

March 31 2012 |

June 30 2011 |

June 30 2012 |

June 30 2011 |

| Ore development (meters) |

1,766 |

2,542 |

1,550 |

4,308 |

2,717 |

| Waste development (meters) |

1,476 |

1,170 |

1,872 |

2,646 |

3,955 |

| Total development (meters) |

3,242 |

3,712 |

3,422 |

6,954 |

6,672 |

| Stoping (square meters) |

4,916 |

7,029 |

5,122 |

11,945 |

8,882 |

| Ore tonnes to surface – development |

103,671 |

126,872 |

154,849 |

230,543 |

230,457 |

| Ore tonnes to surface – stoping |

12,987 |

24,712 |

22,990 |

37,699 |

39,498 |

| Ore tonnes to surface – total |

116,658 |

151,584 |

177,839 |

268,242 |

269,955 |

| Contained Au oz extracted - development |

2,023 |

3,895 |

3,168 |

5,918 |

5,688 |

| Contained Au oz extracted - stoping |

1,795 |

3,411 |

1,830 |

5,206 |

2,719 |

| Contained Au oz extracted - total |

3,818 |

7,306 |

4,998 |

11,124 |

8,407 |

| Contained average grade Au eqv oz/tonne

(g/t)– development |

0.02 (0.61 g/t) |

0.03 (0.95 g/t) |

0.02 (0.64 g/t) |

0.03 (0.87 g/t) |

0.02 (0.64 g/t) |

| Contained average grade Au eqv oz/tonne

(g/t) – stoping |

0.14 (4.30 g/t) |

0.14 (4.29 g/t) |

0.08 (2.57 g/t) |

0.14 (4.30 g/t) |

0.07 (2.25 g/t) |

| Contained average grade Au eqv oz/tonne

(g/t) – total |

0.03 (1.01 g/t) |

0.05 (1.44 g/t) |

0.03 (0.96 g/t) |

0.04 (1.20 g/t) |

0.03 (0.96 g/t) |

| Tonnes milled |

231,513 |

151,873 |

202,660 |

383,386 |

402,538 |

| Recovered Au oz |

6,392 |

6,671 |

4,894 |

13,063 |

10,405 |

| Recovery % Au |

87% |

90% |

85% |

89% |

84% |

| Au oz sold |

5,610 |

6,198 |

5,619 |

11,808 |

8,413

|

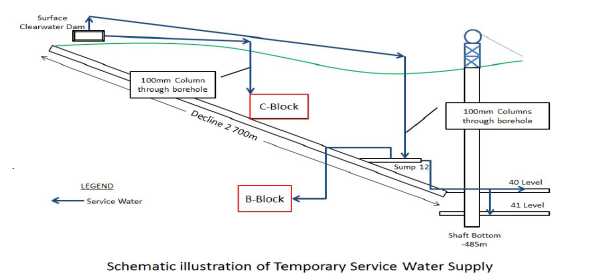

Burnstone experienced setbacks in its planned production

build-up during Q2 2012. The main contributor to the production delays was the

delay in the completion of the vertical shaft and the associated permanent

infrastructure (see below). The delays in completion of the associated shaft

infrastructure impacted on service water supply, handling of excess water and

the cleaning of spillage in the vertical shaft bottom which negatively impacted

shaft availability. Water is required to clean, support and drill and the time

lost in replacing burst plastic pipes from the temporary infrastructure and

de-water the affected area severely impacted production goals.

12

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

An interim upgrade of the temporary infrastructure commenced in

March 2012 and the first of the required permanent infrastructure planned for

completion by late August 2012:

| |

a. |

Water reticulation |

| |

|

|

| |

|

Service water is required to operate the drill rigs as

well as to clean the broken ore from the long hole stopes. The temporary

plastic columns in the decline could not supply the increase in demand on

service water due to the size of the pipe column and the rapidly

increasing development into new mining areas. Pressure Release Valves

(“PRV”) were initially installed to reduce the pressure build-up in the

pipe column and thereby preventing pipe column failure. Due to the

permanent water settlers not being available the excessive dirt in the

water causes these PRV’s to fail, which then cause the pipes to

burst. |

A further improvement to the temporary

water supply system was required and in May 2012 we commenced drilling dedicated

boreholes from surface into the various mining regions thereby separating the

supply of service water for the various mining areas which reduced the

requirement to deliver high volumes through one pipe column.

In addition, additional storage

capacity, pumps and pipe columns were also added to the vertical shaft and

decline to ensure adequate capacity to remove the dirty water from the mine into

the temporary settling dams. The volume of dirty water that can now be handled

has been increased substantially which will reduce the time required to

de-water ends following a pipe column failure. These upgrades have led to

a substantial improvement in service water delivery as of the end of June

2012.

13

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

| |

b. |

Shaft availability |

| |

|

|

| |

|

Shaft availability impacts on the ability to remove

broken mineralized material from the mine. Production had to be reduced to

fit within the available rock hoisting capacity because otherwise the

mining area became congested. Flooding caused by the failure of the water

reticulation system also created spillage at shaft bottom. Exacerbating

the spillage, under-designed shaft loading arrangements caused shaft

unavailability during the time it took to remove the spillage. Development

of a dedicated decline down to shaft bottom commenced in Q1 2012, and

holed with the shaft barrel in early August. This decline will allow

access to effectively clean the spillage at shaft bottom and is expected

to significantly improve shaft availability. The improvement in the water

reticulation system since mid-June 2012 has already positively impacted on

shaft availability due to less spillage from

flooding. |

The infrastructure problems have adversely impacted on the

Burnstone Mine’s ability to achieve its production targets during the second

quarter. When comparing the trend achieved during the four quarters of 2011 with

the first two quarters of 2012, the impact of the infrastructure challenges in

H1 2012 are evident. As originally planned, a continuation of the increase in

the monthly development (refer graph below) as evident from the trend in 2011

would have allowed Burnstone to achieve its planned production build-up.

The benefit from improvements in the temporary infrastructure

has already had a positive impact on the development rates for July 2012 as is

evident from the graph above. Production interruptions were significantly less

than in May and June 2012. The completion of the permanent infrastructure

expected to significantly reduce the risk of future production interruptions.

The combination of the above factors may have resulted in

erroneous investor concerns that long hole stoping (“LHS”) as a mining method

has been the cause of the underperformance at Burnstone. However this is not

management’s view. The photos below are from recent results using LHS and

illustrate that LHS results in good stoping width and fragmentation control.

14

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

1320 Diag 6 Panel 1 – Good stoping width control &

fragmentation

1320 Diag 6 Panel 2 – Good stoping width control (82cm) in

Chlorotoid Shale area

As a result of the infrastructure challenges ore development

for the quarter did not achieve the planned 5,863 meters which impacted on

opening up stopes and delivery of development ore tonnes to the plant. The

interrupted delivery of clean service water to the mining areas had an even more

severe impact on stoping as not only is water required for the drill rigs but

also to clean the stopes once blasted. Stoping for the quarter was therefore

significant below the planned square meters. The lower than planned development

and stoping impacted on the Au ounces delivered to the plant as well as Au oz

recovered and sold.

15

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Underground Evaluation and Surface Drilling

Infill drilling from surface has continued during Q2 2012 with

the objective of improving on the evaluation and structural geometry of certain

mining blocks. Underground evaluation is principally effected by channel

sampling of exposed sidewalls of development drives and stope panels. Horizontal

or shallow dipping cover drilling is undertaken for development control.

The surface drilling continued, but with a reduction to a total

of three drill rigs. Two drill rigs have completed delineating reef on

Vlakfontein Portion 20, and will move to C Upper extensions, and one drill rig

is being used to drill service boreholes. A total of 4,484 meters of drill core

were produced during the Q2 2012.

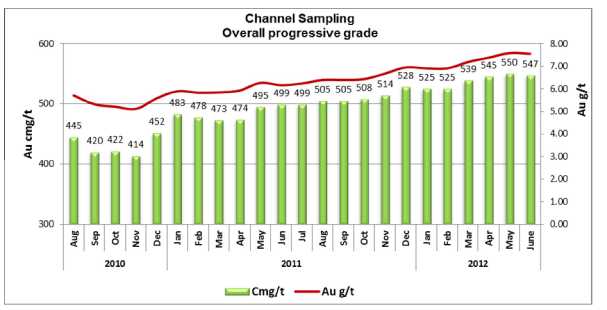

During Q2 2012, 2,620 channel samples were taken from 2,536

metres of development. Channel sampling statistics to end June 2012 indicate

22,372 samples, and an average overall channel width of 73 cm grading 7.55 g/t

Au for a Au content of 547 cmg/t. These results are in-line with or better than

mine development expectations. The current Life-of-Mine plan indicates an

average channel width of 68 cm.

Plans for remainder of 2012 and 2013

Reef development remains the key to delivering the planned ore production build-up. Our infrastructure and production teams need to achieve increasing development targets. Our production build-up plan incorporates the required improvements to infrastructure and training for our people that are required to enable Burnstone to catch-up to its production build-up plan. The Company plans to implement a number of steps in the near term as part of its Burnstone turnaround plan. The Company believes it will be able to reduce costs through reduction of off-site supervisory and premises costs and improved use of labour and water-handling. These cost saving actions could result in aggregate reductions in the range of ZAR20 million ($2.5 million) per month after a few months. Based in part on discussions with the Snowden Group, the independent technical advisors retained by the Company’s lenders, the Company's management currently estimates production in 2012 of 30,000 Au eqv ounces and 90,000-100,000 Au eqv ounces in 2013.

Gold opened at US$1,663 on April 2, 2012 and traded within this

range up to early May 2012 when uncertainty in resolving the Euro debt crisis

resulted in a downward trend in gold prices. Volatile trading continued for the

remainder of the quarter with the price ranging from US$1,540 to US$1,635 per oz

and a closing price of US$1,598 was recorded on June 30, 2012. Gold prices

remained under pressure subsequent to quarter end and traded between US$1,556

and US$1,625 up to the date of this MD&A.

The price of silver also impacts

on the revenue and earnings of the Company, although to a lesser extent than the

price of gold. Silver opened on April 2, 2012 at US$32,43 and traded similar to

gold with the highest closing for the quarter of US$32.97 recorded on April 3,

2012 before losing ground to close at US$27.08 on June 30, 2012. Silver traded between US$26.67 and

US$28.33 subsequent to quarter end up to the date of this MD&A.

16

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

The volatility in the gold price and unstable global economic

conditions impacted the share price performance of most junior developing

precious metal resource Companies. We believe that the delays in the production

build-up at our Burnstone Mine and the liquidity concerns created by these

delays have impacted severely on our share price.

The exchange rate between the US$, $ and ZAR impacts on the

Company’s earnings and cash flow. The ZAR opened at R7.76 against the US$ on

April 2, 2012 and after trading at an average exchange rate of US$1 = ZAR8.12

during the quarter, it closed at US$1 = ZAR8.17 on June 30, 2012. The US$ and $

traded at an average of US$1 = $1.0101 during the quarter.

|

Jun 30

2012

|

Mar 31

2012

|

Dec 31

2011

|

Sept 30

2011

|

Jun 30

2011

|

Mar 31

2011

|

Dec 31

2010

|

Sept 30

2010

|

Current assets

Other assets |

55,743

832,293 |

75,725

829,924 |

61,907

788,403 |

46,263

729,034 |

76,575

750,077 |

105,633

718,825 |

35,038

720,345 |

60,102

618,993 |

| Total assets |

888,036 |

905,649 |

850,310 |

775,297 |

826,652 |

824,458 |

755,383 |

679,095 |

Current liabilities

Non-current liabilities

Shareholders’ equity |

105,009

298,403

484,624 |

83,705

300,293

521,651

|

79,459

299,283

471,568

|

100,263

229,220

445,814 |

87,952

216,748

521,952

|

89,265

226,479

508,714

|

115,525

174,141

465,717 |

87,352

217,146

374,597

|

Total liabilities and

shareholders’ equity |

888,036 |

905,649 |

850,310 |

775,297 |

826,652 |

824,458 |

755,383 |

679,095 |

Working (deficit)

capital1 |

(22,786) |

15,242 |

3,465 |

(5,438) |

30,314 |

49,419 |

(27,976) |

(19,821) |

Revenue

Expenses

(Loss) profit for the

period |

32,371

(54,361)

(21,990) |

33,373

(51,143)

(17,770) |

40,570

(2,928)

37,642 |

46,673

(80,660)

(33,987) |

56,738

(57,789)

(1,051) |

26,343

(46,684)

(20,341) |

42,714

(35,528)

7,186 |

12,230

(35,567)

(23,337) |

Basic (loss) earnings

per

share |

$ (0.04) |

$ (0.04) |

$ 0.08 |

$ (0.07) |

$ 0.00 |

$ (0.05) |

$ 0.02 |

$ (0.07) |

Adjusted (loss)

earnings

per share |

$ (0.05) |

$ (0.03) |

$ (0.01) |

$ (0.03) |

$ 0.00 |

$ (0.01) |

$ 0.02 |

$ (0.05) |

Weighted average

number

of common

shares outstanding

(thousands) |

551,997 |

476,464 |

475,709 |

473,856 |

454,559 |

431,624 |

405,857 |

351,739

|

1 Working capital includes cash and cash

equivalents, trade and other receivables, inventories, trade payables and

accrued liabilities and is considered a non-GAAP measure.

Management believes the disappointing second quarter results

are anomalous and notes that the Company’s adjusted loss per share had generally

been decreasing on a quarterly basis. Decreasing losses were attributable to the

increased revenue from trial mining at Hollister as well as the increasing

production from Burnstone following commencement of production in Q1 2011.

Proceeds from metal sales also benefited from higher average gold and silver

prices over the past 24 months. Since early 2011 metal sales from our Hollister

property was however impacted by the timing of in-carbon gold delivery to third

party refiners due to the challenges in pouring dore on site at our Esmeralda

mill. Until steady state production is reached from both operations quarterly

fluctuations in metal recovered and sold is expected to impact on the reported

earnings. The Company further continues with an aggressive cost management

project aimed at reducing the costs at operations as well as exploration and

general corporate expenses. Fair value and market to market adjustments on

financial instruments also leads to variability in the quarterly profit/loss as

is evident in the table above.

| 7. |

Off-Balance Sheet

Arrangements |

(a) Financial guarantee

In 2007 Great Basin completed a series of transactions in order

to achieve compliance with South Africa’s post-apartheid legislation designed to

facilitate participation by historical disadvantaged South Africans (“HDSAs”) in

the mining industry. This legislation is reflected in the South African Mining

Charter and required Great Basin to achieve a target of 26% ownership by

HDSA in the Company’s South African projects by 2014. In order to comply with

these requirements, Tranter Burnstone (Pty) Ltd (“Tranter”), an HDSA company,

acquired 19,938,650 Great Basin treasury common shares for $38 million (ZAR260

million) which, because it involved indirect economic participation in both the

Hollister and Burnstone projects, was deemed equivalent to a 26% interest in

Burnstone. Tranter borrowed ZAR200 million ($27 million) from Investec Bank Ltd

(“Investec”), a South African bank, to partly fund the purchase of the shares

and Great Basin gave a loan guarantee in favour of Tranter limited of ZAR140

($19 million) million. A loan of $15 million (ZAR 116 million) was advanced to

Tranter up to May 2012 under the guarantee agreement to enable Tranter to meet

its interest payment obligation to Investec.

17

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Tranter was notified by Investec in January 2012 that it is in

breach of the requirements of its loan agreement due to an unfunded cash margin

call as a consequence of the decline in the value of the Great Basin common

shares which serve as collateral for the loan. The Company has advanced

approximately $2.7 million (ZAR20 million) since October 2011 under the

Guarantee agreement to assist Tranter to meet the margin call requirements plus

a further approximately $11 million (ZAR86 million) which was required to meet

the unfunded margin call requirements. Following negotiations between the

Company, Tranter and Investec, a Term sheet was entered into during late April

setting out the mutually beneficial proposal whereby the Company provides

Tranter with further financial assistance over a period of 18 months to enable

them to meet their proposed restructured loan repayment obligations. In terms of

the proposal Investec will remove all cash margin requirements and also

restructure the repayment in such a matter that the required assistance from the

Company does not impact on its short term cash requirements. Finalization of

this restructured financial support is being delayed as a result of the

strategic review process the Company has initiated.

The Company has recognized an impairment provision of $18

million against the loan to Tranter as a consequence of an assessment that the

likelihood that the monies advanced will be recovered is remote.

(b) Gold Fields royalty arbitration

The Company received notification from Gold Fields Limited

("Gold Fields") that it intends to seek rescission of a 2007 agreement under

which Gold Fields cancelled a 2% net smelter royalty over a majority of Area 1

of the Burnstone Mine. Under that transaction, which was part of the Tranter

transaction described above, Gold Fields cancelled the royalty for consideration

of $11 million (ZAR 80 million), that was paid by Great Basin in 2007, and on

the condition that Gold Fields should receive certain Mining Charter score card

credits from the South African government, Gold Fields donated the proceeds to

Tranter which Tranter used to part fund the acquisition of the Great Basin

shares. As Gold Fields has not received these credits, the Company and Gold

Fields have been discussing a mutually acceptable settlement that will not

impact on the transformation agenda of the South African Government. On March

12, 2012, Gold Fields gave notice of arbitration to the Company in respect of

this matter. Other than legal fees, management does not expect this issue to

have an impact on the Company's near term cash-flow, development or production

targets.

| 8. |

Contractual

obligations |

| Payments due by

period |

|

Total

($’million) |

Less than one

year

($’million) |

1 to 3 years

($’million) |

3 to 5 years

($’million) |

More than 5

years

($’million) |

Convertible debentures (a)(b)

Term loan facilities (a)(c)

Finance lease liabilities

(a)(d)

Operating lease obligations

Asset retirement

obligations

Other (e) |

146.7

219.8

0.6

0.1

7.2

0.8 |

10.1

33.1

0.5

0.1

Nil

0.1 |

136.6

119.1

0.1

Nil

Nil

0.2 |

Nil

67.6

Nil

Nil

Nil

0.2 |

Nil

Nil

Nil

Nil

7.2

0.3 |

| Total |

$ 375.2 |

$ 43.9 |

$ 256 |

$ 67.8 |

$ 7.5

|

Notes

| |

(a) |

Amounts include scheduled interest

payments. |

18

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

| |

(b) |

The convertible debentures mature on November 30, 2014

and bear interest at the rate of 8% per annum. Interest is payable

semi-annually in arrears on May 30 and November 30 of each year. The

debentures are direct senior unsecured obligations of the Company and are

guaranteed by certain of the Company’s subsidiaries. |

| |

|

|

| |

(c) |

Term loan I |

| |

|

|

| |

|

In December 2011 the Company restructured Term loan I by

increasing the facility to $152.6 million (US$150 million) and extending

repayment to 2016. $132 million (US$130 million) of the restructured

facility was drawn down on December 15, 2011 with the remaining $20

million (US$20 million) drawn down during the 6 months ended June 30,

2012. Term loan I has a maximum term of 5 years from December 15, 2011 and

capital will be repaid in 16 quarterly consecutive installments,

commencing on March 15, 2013. Term loan I bears interest at a premium of

4% over the 3 month US LIBOR rate and is secured by the Company’s

Burnstone property, its assets and certain subsidiary

guarantees. |

| |

|

|

| |

|

Term loan II |

| |

|

|

| |

|

The Company closed the $69 million (US$70 million) Term

loan II on March 15, 2011. Term loan II has been fully drawn down and is

being repaid in 14 remaining quarterly consecutive installments, and bears

interest at a premium of 3.75% over the 3 month US LIBOR rate. The Nevada

assets and certain guarantees by the Company serve as security for the

loan. |

| |

|

|

| |

(d) |

The principal debt amounts will be repaid in equal

monthly installments over a period of 12 to 13 months and bear interest at

rates between 6.5% and 22.4% on outstanding capital. The finance leases

are collateralized by the leased assets which had a carrying value of $1

million at June 30, 2012. |

| |

|

|

| |

(e) |

Other obligations include nominal environmental

obligations. |

| 9. |

Transactions with Related

Parties |

Related party transactions are recorded at the exchange amount

which is the amount of consideration paid or received as agreed to by the

parties. Refer section 7(a) for details on the only related party transaction in

the second quarter which was the one involving guarantees in favour of our BEE

partner. Information relating to the Company’s related party transactions is

available in the Company’s annual financial statements which are available on

SEDAR at www.sedar.com.

| 10. |

Critical Accounting Estimates-Going Concern

and Asset Impairment Analysis |

The Company's accounting policies are presented in note 3 of

the most recent annual consolidated financial statements. The preparation of

financial statements requires management to use judgment in applying its

accounting policies and estimates and assumptions about the future. Estimates

and other judgments are continuously evaluated and are based on management’s

experience and other factors, including expectations about future events that

are believed to be reasonable under the circumstances. These estimates may have

a significant impact on the financial statements.

The accompanying financial statements and this management’s discussion and analysis disclosure have been prepared on the basis that the Company is a going concern and that the realizable value of its material assets is at least equal to their carrying values. In order to rely on this assumption management prepared sensitivity value analyses of the Company’s principal projects. Burnstone was designed to be able to produce some 200,000+ ounces Au per year in steady-state operations. The sensitivity analysis demonstrates that if Burnstone achieves only approximately two thirds of this goal (140,000 ounces per year from 2014 onwards) there is no impairment currently called for (using current consensus gold price forecasts and a 10% discount rate). Great Basin’s engineering team has confirmed that it believes the minimum 140,000 ounces is very achievable. In addition to the in-house valuation performed on the Nevada project, the Company recently received non-binding third party proposals to purchase the Hollister assets for amounts supporting the carrying value of these assets.

19

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

The Board of Directors has recently initiated a review process to consider a range of strategic alternatives with a view to preserving and enhancing shareholder value in light of the Company’s continuing financial challenges. Strategic alternatives are likely to include, but are not limited to, the sale of all or a portion of the Company's assets, a merger or other business combination transaction involving a third party acquiring all of the Company, a capital raising, recapitalization, reorganization, or restructuring of the Company, as well as continued execution of the Company's existing business plan, or some combination of these alternatives. The Company is also working with its lenders to potentially restructure the current term loan facilities to improve the Company’s cash flow in the short to medium term. In assessing whether the Company was a going concern management was cognizant of the near term liquidity challenges. However after assessing the carrying value of the principal assets management and the Board of Directors concluded that the realizable value of the Company’s aggregate assets continues to exceed aggregate liabilities by a significant margin. Given the residual shareholders’ equity in the business, management and the Board believes that a solution to the liquidity issue is more likely than not and hence has concluded in favour of going concern treatment. The short term liquidity problem is currently the principal risk facing the Company and its shareholders.

| 11. |

Financial Instruments |

(i) Zero cost collar program I

In connection with Term loan I (refer note 8(a) of the interim consolidated financial statements for the three and six months ended June 30, 2012), the Company executed a zero cost collar hedge program for a total 165,474 gold ounces over a period of five years that commenced in January 2012.

The pricing and delivery dates of the put and call options are presented in note (iii) below.

The marked-to-market movements until June 30, 2012 were

calculated using an option pricing model with inputs based on the following

assumptions:

| |

June 30 2012 |

December 31 2011 |

Gold price (per ounce)

Risk free interest rate

Expected life

Gold price volatility |

US$1,599

0.31% - 0.96%

1 – 54 months

18.08% - 27.50% |

US$1,564

0.33% - 1.285%

1 – 60 months

20.35% - 32% |

Gold delivery positions as at June 30, 2012:

| |

June 302012 |

December 31 2011 |

Expired unexercised at no cost

Delivered

Remaining

positions |

7,776 ounces

Nil ounces

157,698 ounces

|

Nil ounces

Nil ounces

165,474 ounces

|

(ii) Zero cost collar program II

In connection with Term loan II (refer note 8(b) of the interim

consolidated financial statements for the three and six months ended June 30,

2012), the Company executed a ZCC hedge program for a total 117,500 gold ounces

over a period of four years that commenced in January 2012.

The pricing and delivery dates of the put and call options are

presented in note (iii) below.

The marked-to-market movements until June 30, 2012 were

calculated using an option pricing model with inputs based on the following

assumptions:

| |

June 30 2012 |

December 31 2011 |

Gold price (per ounce)

Risk free interest rate

Expected life

Gold price volatility |

US$1,599

0.31% - 0.79%

1 – 42 months

18.08% - 26.51% |

US$1,564

0.33% - 1.06%

1 – 48 months

20.35% - 30.76% |

20

|

MANAGEMENT'S DISCUSSION AND

ANALYSIS |

|

| QUARTER ENDED JUNE 30, 2012 |

|

Gold delivery positions as at June 30, 2012:

| |

June 30 2012 |

December 31 2011 |

Expired unexercised at no cost

Delivered

Remaining

positions |

5,250 ounces

Nil ounces

112,250 ounces

|

Nil ounces

Nil ounces

117,500 ounces

|

(iii) Gold delivery positions

The Company’s gold delivery positions as at June 30, 2012 are

as follows:

Put options

|

Strike price |

2012

AU oz

|

2013

AU oz

|

2014

AU oz

|

2015

AU oz

|

2016