UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K/A

(Amendment No. 2)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2012

or

¨ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _____________

Commission file number: 001-34260

CHINA GREEN AGRICULTURE, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 36-3526027 |

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

3rd Floor, Borough A, Block A. No.181, South Taibai Road, Xi’an, Shaanxi Province,

People’s Republic of China 710065

(Address of Principal Executive Offices, Including Zip Code)

Registrant’s telephone number: +86-29-88266368

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.001 Par Value Per Share | NYSE |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such report(s)), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer x |

Non-accelerated filer o Do not check if a smaller reporting company |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $47,940,291 as of December 30, 2011, based on the closing price $3.00 of the Company’s common stock on such date.

The number of outstanding shares of the registrant’s common stock on September 10, 2012 was 27,455,721.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for the 2012 Annual Meeting of Stockholders, which the registrant plans to file with the Securities and Exchange Commission within 120 days after June 30, 2012 are incorporated by reference in Part III of the Form 10-K, as defined below, to the extent described therein.

| 1 |

Explanatory Note

China Green Agriculture, Inc. (the “Company”, “we”, “us”, or “our” is filing this Amendment No. 2 on Form 10-K/A (this “Amendment”) to supplement the disclosure in Item 7 of Part II and Note 2 to its financial statements in its Annual Report on Form 10-K for the year ended June 30, 2012 filed with the U.S. Securities and Exchange Commission (the “Commission”) on September 13, 2012 (the “Form 10-K”) and amended on September 24, 2012 on Form 10-K/A to furnish Exhibit 101 to the Form 10-K (“Form 10-K/A No. 1”).

In this Amendment, the following changes were included:

| · | We included the explanation of our current credit policy and its background under “Net Sales” of “The fiscal year ended June 30, 2012 compared to the fiscal year ended June 30, 2011” and “Critical Accounting Policies and Estimates” under Item 7 of this Amendment. |

| · | We included the description of our practice in evaluating our accounts receivable in Note 2 to financial statements in this Amendment. |

| · | We expanded the analysis under “General and Administrative Expenses” of “The fiscal year ended June 30, 2012 compared to the fiscal year ended June 30, 2011” under Item 7 of this Amendment by including four paragraphs describing the specific amount of write-offs incurred as a result of obsolescence of certain plants in Xi’an Jintai Agriculture Technology Development Company (“Jintai”), one of our operating subsidiaries in China. |

The supplementary disclosure does not affect any numbers in our financial statements contained in Form 10-K and Form 10-K/A No. 1. No other changes have been made to the Form 10-K and Form 10-K/A No. 1. This Amendment does not reflect events occurring after the filing of the Form 10-K and Form 10-K/A No. 1, does not update disclosures contained in the Form 10-K or Form 10-K/A No.1, and does not modify or amend the Form 10-K or Form 10-K/A No.1 except as specifically described in this explanatory note and set forth in detail under Item 7 and Note 2 to financial statements below. Accordingly, this Amendment should be read in conjunction with our Form 10-K, Form 10-K/A No. 1, and our other filings made with the Commission subsequent to the filing of the Form 10-K, including any amendments to those filings.

Pursuant to Rule 12b-15 under the Securities Exchange Act of 1934, as amended, this Amendment contains the complete text of Item 7, the financial statements and currently dated certifications of our Chief Executive Officer and Chief Financial Officer. Capitalized terms not otherwise defined have the meanings ascribed to them in the Form 10-K.

.

PART II

| ITEM 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our consolidated financial statements and the notes to those financial statements appearing elsewhere in this report. This discussion and analysis contains forward-looking statements that involve significant risks and uncertainties. As a result of many factors, such as the slow-down of the global financial markets and its impact on economic growth in general, the competition in the fertilizer industry and the impact of such competition on pricing, revenues and margins, the weather conditions in the areas where our customers are based, the cost of attracting and retaining highly skilled personnel, the prospects for future acquisitions, and the factors set forth elsewhere in this report and our Form 10-K, our actual results may differ materially from those anticipated in these forward-looking statements. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this report will in fact occur. You should not place undue reliance on the forward-looking statements contained in this report.

The forward-looking statements speak only as of the date on which they are made, and, except to the extent required by U.S. federal securities laws, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. Further, the information about our intentions contained in this report is a statement of our intention as of the date of this report and is based upon, among other things, the existing regulatory environment, industry conditions, market conditions and prices and our assumptions as of such date. We may change our intentions, at any time and without notice, based upon any changes in such factors, in our assumptions or otherwise.

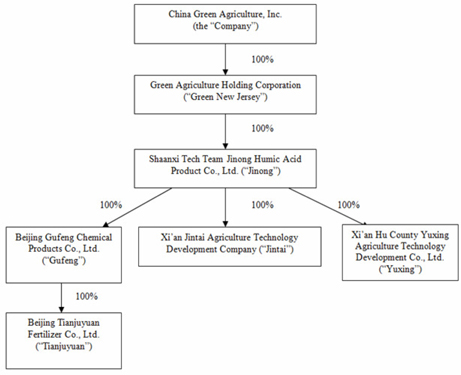

Unless the context indicates otherwise, as used in the following discussion, “Company”, “we,” “us,” and “our,” refer to (i) China Green Agriculture, Inc. (“Green Nevada”), a corporation incorporated in the State of Nevada; (ii) Green Agriculture Holding Corporation (“Green New Jersey”), a wholly-owned subsidiary of Green Nevada incorporated in the State of New Jersey; (iii) Shaanxi TechTeam Jinong Humic Acid Product Co., Ltd. (“Jinong”), a wholly-owned subsidiary of Green New Jersey organized under the laws of the PRC; (iv) Xi’an Jintai Agriculture Technology Development Company (“Jintai”), wholly-owned subsidiary of Jinong in the PRC, (v) Xi’an Hu County Yuxing Agriculture Technology Development Co., Ltd. (“Yuxing”), a wholly-owned subsidiary of Jinong in the PRC; (vi) Beijing Gufeng Chemical Products Co., Ltd., a wholly-owned subsidiary of Jinong in the PRC (“Gufeng”), and (vii) Beijing Tianjuyuan Fertilizer Co., Ltd., Gufeng’s wholly-owned subsidiary in the PRC (“Tianjuyuan”).

Unless the context otherwise requires, all references to (i) “PRC” and “China” are to the People’s Republic of China; (ii) “U.S. dollar,” “$” and “US$” are to United States dollars; and (iii) “RMB”, “Yuan” and Renminbi are to the currency of the PRC or China.

Overview

We are engaged in the research, development, production and sale of various types of fertilizers and agricultural products in the PRC through our wholly-owned Chinese subsidiaries, Jinong, Jintai, Yuxing, Gufeng and Tianjuyuan. Our primary business is fertilizer products, specifically humic-acid based compound fertilizer produced by Jinong and compound fertilizer, blended fertilizer, organic compound fertilizer, slow-release fertilizers, highly-concentrated water-soluble fertilizers and mixed organic-inorganic compound fertilizer produced by Gufeng. In addition, through Jintai and Yuxing, we develop and produce agricultural products, such as top-grade fruits, vegetables, flowers and colored seedlings. For financial reporting purposes, our operations are organized into four business segments: fertilizer products (Jinong), fertilizer products (Gufeng), agricultural products production (Jintai), and agricultural products production (Yuxing).

Jintai and Yuxing also serve as a research and development base for our fertilizer products. The fertilizer business conducted by Jinong and Gufeng generated approximately 96.4%, 96.1% and 88.0% of our total revenues in the fiscal year ended June 30, 2012, 2011 and 2010, respectively. It should be noted that our consolidated results for the 2010 period do not include the results of Gufeng and its subsidiary, Tianjuyuan, which were acquired on July 2, 2010.

| 2 |

Fertilizer Products

As of June 30, 2012, we had developed and produced a total of 443 different fertilizer products in use, of which 126 and 317 were developed and produced by Jinong and Gufeng, respectively.

Below is a table that shows the metric tons of fertilizer sold by Jinong and Gufeng and the revenue per ton for the periods indicated:

| For the years ended June 30, | |||||||||||||||

| 2012 | 2011 | 2010 | YOY Change | YOY Change | YOY Change% | YOY Change% | |||||||||

| (Metric tons) | |||||||||||||||

| JN | 61,590 | 48,038 | 22,834 | 13,552 | 25,204 | 28.2 | % | 110.4 | % | ||||||

| GF | 256,618 | 289,731 | (33,113 | ) | 289,731 | (11.4 | )% | N/A | |||||||

| 318,208 | 337,769 | 22,834 | (19,561 | ) | 314,935 | ||||||||||

| For the years ended June 30, | |||||||||||||||||

| 2012 | 2011 | 2010 | |||||||||||||||

| (Revenue per ton $) | |||||||||||||||||

| JN | $ | 1,432 | $ | 1,366 | $ | 2,006 | |||||||||||

| GF | 473 | 370 | |||||||||||||||

| For the three months ended June 30, | |||||||||||||||

| 2012 | 2011 | 2010 | YOY Change | YOY Change | YOY Change% | YOY Change% | |||||||||

| (Metric tons) | |||||||||||||||

| JN | 15,020 | 14,254 | 9,314 | 766.15 | 4,940 | 5.4% | 53.0 | % | |||||||

| GF | 63,712 | 97,935 | 0 | (34,222 | ) | 97,935 | (34.9 | )% | N/A | ||||||

| 78,733 | 112,189 | 9,314 | (33,456 | ) | 102,875 | ||||||||||

| For the three months ended June 30, | |||||||||||||||||

| 2012 | 2011 | 2010 | |||||||||||||||

| (Revenue per ton $) | |||||||||||||||||

| JN | $ | 1,640 | $ | 1,305 | $ | 1,639 | |||||||||||

| GF | 499 | 411 | |||||||||||||||

For the fiscal year ended June 30, 2012, we sold approximately 318,208 metric tons of fertilizer products, as compared to 337,769 metric tons and 22,834 metric tons for the fiscal year ended June 30, 2011 and 2010, respectively, which did not include sales of products by Gufeng with respect to the number of metric tons we sold in 2010. For the fiscal year ended June 30, 2012, Jinong sold approximately 61,590 metric tons of fertilizer products, as compared to 48,038 metric tons and 22,834 for the fiscal year ended June 30, 2011 and 2010, respectively. For the fiscal year ended June 30, 2012, Gufeng sold approximately 256,618 metric tons of fertilizer products, as compared to 289,731 metric tons for the fiscal year ended June 30, 2011. Our sales of fertilizer products to five provinces accounted for approximately 58.9% of our fertilizer revenue for the fiscal year ended June 30, 2012. Specifically, the provinces and their respective percentage contribution to our fertilizer revenues were Beijing (24.2%), Hebei (16.3%), Jilin (9.0%), Liaoning (6.6%) and Inner Mongolia (2.8%).

As of June 30, 2012, we had a total of 943 distributors covering 22 provinces, four autonomous regions and three central government-controlled municipalities in China. Jinong had 758 distributors in China. Jinong’s sales are not dependent on any single distributor or any group of distributors. Its top five distributors accounted for 2.1% of Jinong’s fertilizer revenues for the fiscal year ended June 30, 2012. Gufeng had 185 distributors, including some large state-owned enterprises. Gufeng’s top five distributors accounted for 47.0% of its revenues for the fiscal year ended June 30, 2012, of which Sinoagri Holding Company Limited accounted for 25.8% of Gufeng’s revenue for the fiscal year ended June 30, 2012.

Agricultural Products

Through Jintai, we develop, produce and sell high-quality flowers, green vegetables and fruits to local marketplaces and various horticulture and planting companies. We also use certain of Jintai’s and Yuxing’s greenhouse facilities to conduct research and development activities for our fertilizer products. The three PRC provinces that accounted for 99.5% of our agricultural products revenue for the fiscal year ended June 30, 2012 were Shaanxi (92.0%), Ningxia (6.5%) and Guangdong (0.9%).

| 3 |

Recent Developments

New Products

During the three months ended June 30, 2012, Jinong launched seven new fertilizer products, which included five broad-spectrum and two powder fertilizer products. Jinong’s new products generated approximately $115,256, or 0.5% of Jinong’s fertilizer revenues for the three months ended June 30, 2012. Jinong also added 46 new distributors for the three months ended June 30, 2012. Jinong’s new distributors accounted for approximately $1,706,005, or 6.9% of Jinong’s fertilizer revenues for the three months ended June 30, 2012. Jinong’s revenue attributable to the new products distributed by its new distributors was approximately $44,110, or 0.2% of Jinong’s fertilizer revenues for the three months ended June 30, 2012. During the three months ended June 30, 2012, Gufeng launched no new fertilizer product. Gufeng added three new distributors during the three months ended June 30, 2012, which accounted for approximately $475,410, or 1.5%, of Gufeng’s fertilizer revenues.

Jintai’s Relocation

We have started to relocate Jintai to the facilities of one of the Company’s other subsidiaries-Yuxing, located in Hu County, Xi’an. Yuxing’s facilities are approximately a one hour drive south of Jintai's current location in the Economic and Technical Development Zone (the "Zone") in the metro area of the city of Xi'an.

As mentioned in the Company's previous quarterly reports, with the rapid growth of urbanization in Xi'an, the Zone has been inhabited by a large and dense population and the periphery of Jintai has bristled with various industrial factories and utility plants. The Zone's concentrated industrial activities and dense population changed the micro bioenvironment for the growth of Jintai's agricultural products and disturbed Jintai's normal fertilizer research and development. Recently such changes caused the death and obsolescence of large amount of Jintai's flowers and seedlings. Additionally, the government recently introduced a new rezoning plan for the Zone, and the land Jintai currently occupies is being converted from agriculture use to residential and commercial use. The rezoning will prohibit the agricultural growth activities that Jintai currently conducts at the property. To continue Jintai's business, the Company will relocate all of Jintai's operations, including greenhouses, inventories, growing seedlings, flowers and parent plants, to Yuxing.

The relocation commenced on March 1, 2012. During the three months ended June 30, 2012, Jintai had no sales revenue due to relocation. We expect Jintai will likely remain unprofitable until the relocation gets completed. The entire relocation process is expected to complete by the end of fiscal year 2013. Further, we may consider merging the subsidiaries of Yuxing and Jintai together to reduce operating cost and streamline management at appropriate time in the future.

| 4 |

Results of Operations

The fiscal year ended June 30, 2012 compared to the fiscal year ended June 30, 2011.

The following table shows the operating results of the Company on a consolidated basis for the fiscal years ended June 30, 2012 and 2011.

| For the Years Ended June 30, | ||||||||||||||||

| 2012 | 2011 | Change | Change% | |||||||||||||

| Sales | ||||||||||||||||

| Jinong | $ | 88,168,740 | $ | 65,629,265 | 22,539,475 | 34.3 | % | |||||||||

| Gufeng | 121,480,943 | 107,081,018 | 14,399,925 | 13.4 | % | |||||||||||

| Jintai | 5,792,002 | 6,826,933 | (1,034,931 | ) | (15.2 | )% | ||||||||||

| Yuxing | 2,082,520 | 180,750 | 1,901,770 | 1052.2 | % | |||||||||||

| Net sales | 217,524,205 | 179,717,966 | 37,806,239 | 21.0 | % | |||||||||||

| Cost of goods sold | ||||||||||||||||

| Jinong | 34,129,304 | 26,449,117 | 7,680,187 | 29.0 | % | |||||||||||

| Gufeng | 96,756,719 | 85,670,990 | 11,085,729 | 12.9 | % | |||||||||||

| Jintai | 5,415,970 | 3,841,391 | 1,574,579 | 41.0 | % | |||||||||||

| Yuxing | 1,946,979 | 136,433 | 1,810,546 | 1327.1 | % | |||||||||||

| Cost of goods sold | 138,248,972 | 116,097,931 | 22,151,041 | 19.1 | % | |||||||||||

| Gross profit | 79,275,233 | 63,620,035 | 15,655,198 | 24.6 | % | |||||||||||

| Operating expenses | ||||||||||||||||

| Selling expenses | 11,548,816 | 7,121,905 | 4,426,911 | 62.2 | % | |||||||||||

| General and administrative expenses | 13,801,407 | 14,386,699 | (585,292 | ) | (4.1 | )% | ||||||||||

| Total operating expenses | 25,350,223 | 21,508,604 | 3,841,619 | 17.9 | % | |||||||||||

| Income from operations | 53,925,010 | 42,111,431 | 11,813,579 | 28.1 | % | |||||||||||

| Other income (expense) | ||||||||||||||||

| Other income (expense) | 60,212 | 23,999 | 36,213 | 150.9 | % | |||||||||||

| Interest income | 364,536 | 282,727 | 81,809 | 28.9 | % | |||||||||||

| Interest expense, net | (1,590,620 | ) | (466,912 | ) | (1,123,708 | ) | 240.7 | % | ||||||||

| Total other income (expense) | (1,165,872 | ) | (160,186 | ) | (1,005,686 | ) | 627.8 | % | ||||||||

| Income before income taxes | 52,759,138 | 41,951,245 | 10,807,893 | 25.8 | % | |||||||||||

| Provision for income taxes | 10,801,313 | 9,037,144 | 1,764,169 | 19.5 | % | |||||||||||

| Net income | 41,957,825 | 32,914,101 | 9,043,724 | 27.5 | % | |||||||||||

| Other comprehensive income | ||||||||||||||||

| Foreign currency translation gain | 4,876,751 | 7,547,145 | (2,670,394 | ) | (35.4 | )% | ||||||||||

| Comprehensive income | $ | 46,834,576 | $ | 40,461,246 | $ | 6,373,330 | 15.8 | % | ||||||||

| Basic weighted average shares outstanding | 26,943,530 | 25,929,517 | 1,014,013 | 3.9 | % | |||||||||||

| Basic net earnings per share | $ | 1.56 | $ | 1.27 | $ | 0.29 | 22.7 | % | ||||||||

| Diluted weighted average shares outstanding | 26,943,530 | 25,929,517 | 1,014,013 | 3.9 | % | |||||||||||

| Diluted net earnings per share | 1.56 | 1.27 | 0.29 | 22.7 | % | |||||||||||

Net Sales

Total net sales for the fiscal year ended June 30, 2012 were $217,524,205, an increase of $37,806,239, or 21.0%, from $179,717,966 for the fiscal year ended June 30, 2011. This increase was largely due to the strong sales of humic acid liquid and compound fertilizer products from Jinong and Gufeng respectively, which had higher selling prices.

For the fiscal year ended June 30, 2012, Jinong’s net sales increased $22,539,475, or 34.3%, to $88,168,740 from $65,629,265 from the fiscal year ended June 30, 2011. This increase was mainly attributable to the greater sales of humic acid fertilizer products including our liquid and powder fertilizers during this period as a result of our increased distributors and the aggressive marketing.

| 5 |

For the fiscal year ended June 30, 2012, net sales at Gufeng were $121,480,943, an increase of $14,399,925, or 13.4%, from $107,081,018 for the fiscal year ended June 30, 2011. The increase was due to the increasing demand for the organic/inorganic humic acid compound fertilizer products of Gufeng, higher average selling price per metric ton for the fiscal year ended June 30, 2012 than the price for the fiscal year ended June 30, 2011, and higher percentage of more expensive humic acid-based fertilizers in Gufeng’s product mix than in the same period in 2011. While with increase of 28% in the average unit price per metric ton at Gufeng from fiscal year 2011 to fiscal year 2012, the total sales volume at Gufeng decreased by 11% in metric tons from the fiscal year ended June 30, 2011 to the fiscal year ended June 30, 2012. Such decrease in sales volume is mainly attributable to the decrease in Gufeng’s export sales volume for the fiscal year ended June 30, 2012.

Jintai’s net sales decreased by $1,034,931, or 15.2%, to $5,792,002 for the fiscal year ended June 30, 2012 from $6,826,933 for the same period in 2011. The decrease was mainly attributable to Jintai’s nearby environmental degradation which resulted in its relocation commenced on March 1, 2012 and is still on going. Therefore, Jintai did not generate any sales revenue since March 1, 2012.

For the fiscal year ended June 30, 2012, Yuxing’s net sales were $2,082,520, an increase of $ 1,901,770, from $180,750 during the fiscal year ended June 30, 2011. The increase was mainly attributable to the strong sales of Yuxing’s top-grade flowers in the fiscal year 2012, while in the fiscal year 2011 Yuxing did not have commercialized top-grade flowers.

The Company’s current credit policy allows clients to pay off their receivable balance by up to 180 days from the point the revenue is recognized. Under this policy, for receivable older than 180 days, the Company will book 100% allowance toward the outstanding balance immediately. Such a policy became effective since the fiscal quarter period ended March 31, 2012. The extended credit period was referred to in the Company’s quarterly report on Form 10-Q for the fiscal quarter ended March 31, 2012. The current policy is a revision of the Company’s previous credit policy, which allowed the clients to pay off receivables up to a shorter period of 90 days, instead of 180 days.

The implementation of the current policy was a result of the change in fertilizer market in the middle of fiscal year 2012. It applies to the Company’s subsidiaries in fertilizer segment, Jinong and Gufeng. Starting from 2011, the economy in China slowed down. The demand in the fertilizer market declined from previous year and remained softened toward year end. In addition, in December 2011, in overseeing the fertilizer market in China, the Ministry of Finance under the supervision of the State Council of the Central Government of the PRC, or the PRC authority, raised the 2012 export tariff for certain fertilizer products that Gufeng exports to in the international market. While we always keep a balanced mix of our domestic clients and oversea clients, Gufeng’s export ability was largely expected to be reduced during 2012 due to the prohibitively high export tariff imposed. We then had to rely on domestic clients to fill in the orders that could be under the export contract instead. To combat the adverse effect of high export tariff, we launched aggressive marketing campaign by forgoing advance payments and offering warehouse credit sales to selected clients. Coupled with the marketing efforts to selected clients, Gufeng and Jinong, adopted the updated 180-day credit policy for all clients, effective beginning 2012. The updated policy eased the payback period and provided much needed liquidity to the constraint clients. These policy adjustments and marketing tools were approved very essential in time for the Company in expanding its sales in the domestic segment and offsetting the negative effect of reduced export capacity up to date.

Cost of Goods Sold

Total cost of goods sold for the fiscal year ended June 30, 2012 was $138,248,972, an increase of $22,151,041, or 19.1%, from $116,097,931 for the fiscal year ended June 30, 2011. This increase was mainly due to the increase in sales and the increase in raw material and manufacturing costs.

Cost of goods sold by Jinong for the fiscal year ended June 30, 2012 was $34,129,304, an increase of $7,680,187, or 29.0%, from $26,449,117 for the same period in 2011. The increase was primarily attributable to the increase in the cost of raw materials and packaging materials.

Cost of goods sold by Gufeng for the fiscal year ended June 30, 2012 was $96,756,719, an increase of $11,085,729, or 12.9%, from $85,670,990 for the same period in 2011. The increase was primarily due to the increase in Gufeng’s fertilizer sales, the increase in Gufeng’s raw material cost and manufacturing costs.

Cost of goods sold by Jintai for the fiscal year ended June 30, 2012 was $5,415,970, an increase of $1,574,579, or 41.0%, from $3,841,391 for fiscal year 2011. The increase was primarily attributable to the obsolescence of Jintai’s butterfly orchids as the result of Jintai’s relocation.

For fiscal year ended June 30, 2012, cost of goods sold by Yuxing was $1,946,979, an increase of $1,810,546, from $136,433 for the fiscal year ended June 30, 2011. The increase was proportional to Yuxing’s sales.

Gross Profit

Total gross profit for the fiscal year ended June 30, 2012 increased by $ 15,655,198, or 24.6%, to $79,275,233, as compared to $63,620,035 for the fiscal year ended June 30, 2011. Gross profit margin was approximately 36.4% and 35.4% for the fiscal year ended June 30, 2012 and 2011, respectively.

Gross profit generated by Jinong increased by $14,859,288, or 37.9%, to $54,039,436 for the fiscal year ended June 30, 2012 from $39,180,148 for the fiscal year ended June 30, 2011. Gross profit margin from Jinong’s sales was approximately 61.3% and 59.7% for the fiscal year ended June 30, 2012 and 2011, respectively.

For the fiscal year ended June 30, 2012, gross profit generated by Gufeng was $ 24,724,224, an increase of $ 3,314,196, or 15.5%, from $21,410,028 for the fiscal year ended June 30, 2011. Gross profit margin from Gufeng’s sales was approximately 20.4% and 20.0% for the fiscal year ended June 30, 2012 and 2011, respectively.

Gross profit from Jintai decreased by $2,609,510, or 87.4%, for the fiscal year ended June 30, 2012, to $376,032, as compared to $2,985,542 for the fiscal year ended June 30, 2011. Gross profit margin from Jintai’s sales was approximately 6.5% and 43.7% for the fiscal years ended June 30, 2012 and 2011, respectively.

| 6 |

For the fiscal year ended June 30, 2012, gross profit from Yuxing was $135,541, an increase of $91,224 or 205.8%, from $44,317 for the fiscal years ended June 30, 2011. Gross profit margin from Yuxing’s sales was approximately 6.5% and 24.5% for the fiscal years ended June 30, 2012 and 2011, respectively.

Selling Expenses

Our selling expenses consist primarily of salaries of sales personnel, advertising and promotion expenses, freight-out costs and related compensation. Selling expenses were $11,548,816, or 5.3%, of net sales for the fiscal year ended June 30, 2012, as compared to $7,121,905, or 4.0% of net sales for the fiscal year ended June 30, 2011, an increase of $4,426,911, or 62.2%. The selling expenses of Gufeng were $3,183,853, or 2.6% of Gufeng’s net sales for the fiscal year ended June 30, 2012, as compared to $ 2,834,005, or 2.6% of Gufeng’s net sales for the fiscal year ended June 30, 2011. The selling expenses of Jinong for the fiscal year ended June 30, 2012 were $8,305,444, or 9.4% of Jinong’s net sales, as compared to selling expenses of $4,254,198, or 6.5% of Jinong’s net sales in fiscal year 2011. Most of this increase was due to Jinong’s expanded marketing efforts and the increase in shipping costs.

General and Administrative Expenses

General and administrative expenses consisted primarily of related salaries, rental expenses, business development, depreciation and travel expenses incurred by our general and administrative departments and legal and professional expenses including expenses incurred and accrued due to pending litigations. General and administrative expenses were $13,801,407, or 6.3% of net sales, for the fiscal year ended June 30, 2012, as compared to $14,386,699, or 8.0%, of net sales for the fiscal year ended June 30 2011, a decrease of $585,292, or 4.1%. This decrease was primarily the result of the decrease of legal and investor relations fees incurred in connection with certain pending litigations in 2011.

In addition, there have been obsolescence incurred write-offs classified as general and administration expenses since June 30, 2011 as described below which resulted in the Jintai's relocation described under the Recent Developments herein above:

As of June 2011, 4,852,236 number of Photinia fraseri were obsolete due to the air and water pollution in the surrounding area of Jintai. The total loss for this obsolescence incurred a write-off of $2,813,993, which equaled to the maintenance cost of Photinia fraseri, and was classified as general and administration expense in Jintai for the fiscal year June 30, 2011.

In addition, 2,028,508 and 1,532,876 number of Photinia fraseri became obsolete as of September 30 and December 31, 2011 respectively due to the exacerbating air and water pollution in the surrounding area of Jintai. The total loss for the obsolescence incurred write-offs of $288,307 and $957,407 respectively. The losses equaled to the maintenance cost of Photinia fraseri, and were classified as general and administration expense in Jintai for the quarter ended September 30 and December 31, 2011.

As of March 31, 2012, 54,682 number of butterfly orchids became obsolete due to disease. The total loss for the obsolescence incurred a write-off of $223,907, which equaled to the maintenance cost of butterfly orchids, and was classified as general and administration expense in Jintai as of March 31, 2012.

Total Other Income (Expenses)

Total other income (expense) consisted of income from subsidies received from the PRC government, interest income, interest expenses and bank charges. Total other expense for the fiscal year ended June 30, 2012 was $1,165,872, as compared to total other income of $160,186 for the fiscal year ended June 30, 2011, an increase in expense of $1,005,686, or 627.8%. The increase was mainly attributable to the $1,590,620 interest expense from Gufeng’s outstanding short-term loans.

Income Taxes

Jinong is subject to a preferred tax rate of 15% as a result of its business being classified as a High-Tech project under the PRC Enterprise Income Tax Law (“EIT”) that became effective on January 1, 2008. Jinong incurred income tax expenses of $6,597,766 for the fiscal year ended June 30, 2012, as compared to $5,157,184 for the fiscal year ended June 30, 2011, an increase of $1,440,582, or 27.9%, which was primarily attributable to Jinong’s increased operating income.

Gufeng, subject to a tax rate of 25%, incurred income tax expenses of $4,203,548 for the fiscal year ended June 30, 2012, as compared to $3,879,959 for the fiscal year ended June 30, 2011, an increase of $323,589, or 8.3%.

Jintai has been exempt from paying income tax as its products fall into the tax exemption list set out in the EIT.

Yuxing has no income tax for the fiscal year ended June 30, 2012 as a result of being exempted from paying income tax due to its products fall into the tax exemption list set out in the EIT, the same treatment as Jintai receives.

Net Income

Net income for the fiscal year ended June 30, 2012 was $41,957,825, an increase of $9,043,724, or 27.5%, compared to $32,914,101 for the fiscal year ended June 30, 2011. The increase was attributable to the increase in gross profit. Net income as a percentage of total net sales was approximately 19.3% and18.3 % for the fiscal year ended June 30, 2012 and 2011, respectively.

| 7 |

The fiscal year ended June 30, 2011 compared to the fiscal year ended June 30, 2010.

The following table shows the operating results of the Company on a consolidated basis for the fiscal years ended June 30, 2011 and 2010.

| For the Years Ended June 30, | ||||||||||||||||

| 2011 | 2010 | Change | Change% | |||||||||||||

| Sales | ||||||||||||||||

| Jinong | $ | 65,629,265 | $ | 45,816,377 | 19,812,888 | 43.2 | % | |||||||||

| Gufeng | 107,081,018 | - | 107,081,018 | n/a | ||||||||||||

| Jintai | 6,826,933 | 6,274,375 | 552,558 | 8.8 | % | |||||||||||

| Yuxing | 180,750 | - | 180,750 | n/a | ||||||||||||

| Net sales | 179,717,966 | 52,090,752 | 127,627,214 | 245.0 | % | |||||||||||

| Cost of goods sold | ||||||||||||||||

| Jinong | 26,449,117 | 17,700,532 | 8,748,585 | 49.4 | % | |||||||||||

| Gufeng | 85,670,990 | - | 85,670,990 | n/a | ||||||||||||

| Jintai | 3,841,391 | 3,438,020 | 403,371 | 11.7 | % | |||||||||||

| Yuxing | 136,433 | - | 136,433 | n/a | ||||||||||||

| Cost of goods sold | 116,097,931 | 21,138,552 | 94,959,379 | 449.2 | % | |||||||||||

| Gross profit | 63,620,035 | 30,952,200 | 32,667,835 | 105.5 | % | |||||||||||

| Operating expenses | ||||||||||||||||

| Selling expenses | 7,121,905 | 2,203,345 | 4,918,560 | 223.2 | % | |||||||||||

| General and administrative expenses | 14,386,699 | 3,822,234 | 10,564,465 | 276.4 | % | |||||||||||

| Total operating expenses | 21,508,604 | 6,025,579 | 15,483,025 | 257.0 | % | |||||||||||

| Income from operations | 42,111,431 | 24,926,621 | 17,184,810 | 68.9 | % | |||||||||||

| Other income (expense) | ||||||||||||||||

| Other income (expense) | 23,999 | (5,321 | ) | 29,320 | -551.0 | % | ||||||||||

| Interest income | 282,727 | 275,449 | 7,278 | 2.6 | % | |||||||||||

| Interest expense, net | (466,912 | ) | (112,475 | ) | (354,437 | ) | 315.1 | % | ||||||||

| Total other income (expense) | (160,186 | ) | 157,653 | (317,839 | ) | -201.6 | % | |||||||||

| Income before income taxes | 41,951,245 | 25,084,274 | 16,866,971 | 67.2 | % | |||||||||||

| Provision for income taxes | 9,037,144 | 3,794,516 | 5,242,628 | 138.2 | % | |||||||||||

| Net income | 32,914,101 | 21,289,758 | 11,624,343 | 54.6 | % | |||||||||||

| Other comprehensive income | ||||||||||||||||

| Foreign currency translation gain | 7,547,145 | 899,481 | 6,647,664 | 739.1 | % | |||||||||||

| Comprehensive income | $ | 40,461,246 | $ | 22,189,239 | 18,272,007 | 82.3 | % | |||||||||

| Basic weighted average shares outstanding | 25,929,517 | 23,468,246 | 2,461,271 | 10.5 | % | |||||||||||

| Basic net earnings per share | $ | 1.27 | $ | 0.91 | 0.36 | 39.9 | % | |||||||||

| Diluted weighted average shares outstanding | 25,929,517 | 23,468,246 | 2,461,271 | 10.5 | % | |||||||||||

| Diluted net earnings per share | 1.27 | 0.91 | 0.36 | 39.9 | % | |||||||||||

Net Sales

Total net sales for the fiscal year ended June 30, 2011 were $179,717,966, an increase of $127,627,214, or 245.0%, from $52,090,752 for the fiscal year ended June 30, 2010. This increase was largely due to the inclusion of Gufeng’s net sales, which contributed $107,081,018, or 59.6%, of our total net sales. Our total net sales without including Gufeng’s net sales for the fiscal year ended June 30, 2011 were $72,636,948, an increase of $20,546,196, or 39.4%, from $52.1 million for the fiscal year ended June 30, 2010.

| 8 |

For the fiscal year ended June 30, 2011, Jinong’s net sales increased $19,812,888, or 43.2%, to $65,629,265 from $45,816,377 from the fiscal year ended June 30, 2010. Sales volume increased 110.4% to 48,038 metric tons for the fiscal year ended June 30, 2011 from 22,835 metric tons for the fiscal year ended June 30, 2010. This increase was mainly attributable to greater sales of products including our liquid fertilizers, powder fertilizers, and particularly, the lower-margin granular fertilizers released since our 40,000 metric-ton production line began production in August 2009. In addition, Jinong launched more promotional activities to increase sales.

Net sales at Gufeng, which included one quarter of production on the new 200,000 metric ton line, for the fiscal year ended June 30, 2011, were $107.1 million.

Jintai’s net sales increased by $552,558, or 8.8%, to $6,826,933 for the fiscal year ended June 30, 2011 from $6,274,375 for the same period in 2010.

Yuxing achieved net sales of $180,750 during the fiscal year ended June 30, 2011. For fiscal year ended June 30, 2010, Yuxing segment had no revenues.

Cost of Goods Sold

Total cost of goods sold for the fiscal year ended June 30, 2011 was $116,097,931, an increase of $94,959,379, or 449.2%, from $21,138,551 for the fiscal year ended June 30, 2010. This significant increase was mainly due to the costs attributable to the production and sale of Gufeng’s products, which accounted for 73.8% of our cost of goods sold. The total cost of goods sold without including Gufeng’s cost of goods sold for the fiscal year ended June 30, 2011 was $30,426,941, an increase of $9,288,389, or 43.9% from $21,138,551 for the fiscal year ended June 30, 2010.

Cost of goods sold by Jinong for the fiscal year ended June 30, 2011 was $26,449,117, an increase of $8,748,585, or 49.4%, from $17,700,532 for the same period in 2010. As a percentage of total net sales, cost of goods sold by Jinong accounted for approximately 14.7% and 34.0% for the fiscal year ended June 30, 2011 and 2010, respectively. The increase in cost of goods sold was attributable to the increase in sales of lower-margin granular fertilizers and the increase in raw materials and packaging materials used as a result of our newly introduced powder and liquid fertilizer products.

Cost of goods sold by Gufeng for the fiscal year ended June 30, 2011 was $85,670,990 which accounted for 73.8% of total cost of goods sold.

Cost of goods sold by Jintai for the fiscal year ended June 30, 2011 was $3,841,391, an increase of $403,371, or 11.7%, from $3,438,020 for fiscal year 2010. The increase in the price of raw materials was the main reason for the increase in Jintai’s cost of goods sold.

Cost of goods sold by Yuxing was $136,433 for the fiscal year ended June 30, 2011. For fiscal year ended June 30, 2010, Yuxing segment had no cost of goods sold.

Gross Profit

Total gross profit for the fiscal year ended June 30, 2011 increased by $32,667,835, or 105.5%, to $63,620,035, as compared to $30,952,200 for the fiscal year ended June 30, 2010. Gross profit margin was approximately 35.4% and 59.4% for the fiscal year ended June 30, 2011 and 2010, respectively. The decrease in gross profit margin was primarily due to the acquisition of Gufeng, which mainly sells low-margin granular fertilizer products. The gross profit without including Gufeng’s gross profit was $42,210,007 with a gross profit margin of 58.1%.

Gross profit generated by Jinong increased by $11,064,303, or 39.4%, to $39,180,148 for the fiscal year ended June 30, 2011 from $28,115,845 for the fiscal year ended June 30 2010. Gross profit margin from Jinong’s sales was approximately 59.7% and 61.4% for the fiscal year ended June 30, 2011 and 2010, respectively. The main reason for the decrease in Jinong’s gross profit margin was primarily attributable to the strong sales of lower-margin granular fertilizers for the fiscal year ended June 30, 2011 compared with a year ago. In addition, the increase in the price of raw materials also contributed to the lower margin than before.

| 9 |

Gross profit generated by Gufeng was $21,410,028 with a gross profit margin of approximately 20.0% for the fiscal year ended June 30, 2011.

Gross profit from Jintai increased by $149,187, or 5.3%, for the fiscal year ended June 30, 2011, to $2,985,542, as compared to $2,836,355 for the fiscal year ended June 30, 2010. Gross profit margin from Jintai’s sales was approximately 43.7% and 45.2% for the fiscal years ended June 30, 2011 and 2010, respectively.

Gross profit from Yuxing was $44,317 with a gross profit margin of approximately 24.5% for the fiscal years ended June 30, 2011.

Selling Expenses

Our selling expenses consist primarily of salaries of sales personnel, advertising and promotion expenses, freight-out costs and related compensation. Selling expenses were $7,121,905, or 4.0%, of net sales for the fiscal year ended June 30, 2011 as compared to $2,203,345 or 4.2% of net sales for the fiscal year ended June 30, 2010, an increase of $4,918,560, or 223.2%. This increase was primarily due to the inclusion of Gufeng’s selling expenses for fiscal year 2011. The selling expenses of Gufeng were $ 2,834,005, or 2.6% of Gufeng’s net sales. The total selling expenses for the fiscal year ended June 30, 2011 without including Gufeng’s selling expenses was $4,287,900, or 5.9% of net sales excluding Gufeng’s net sales. The selling expenses of Jinong for the fiscal year ended June 30, 2011 were $4,254,198, or 6.5% of Jinong’s net sales, compared to selling expenses of $2,176,881, or 4.8% of Jinong’s net sales in fiscal year 2010. Most of this increase was due to Jinong’s expanded marketing efforts such as promotional materials and the increase in shipping costs.

General and Administrative Expenses

General and administrative expenses consisted primarily of related salaries, rental expenses, business development, depreciation and travel expenses incurred by our general and administrative departments and legal and professional expenses including expenses incurred and accrued due to pending litigations. General and administrative expenses were $14,386,699, or 8.0% of net sales, for the fiscal year ended June 30, 2011, as compared to $ 3,822,234, or 7.3%, of net sales for the fiscal year ended June 30 2010, an increase of $10,564,465. This increase was primarily the result of the inclusion of Gufeng’s general and administrative expenses, stock compensation expenses, Jintai’s photinia fraseri seedlings becoming obsolete and additional legal and investor relations fees incurred in connection with certain pending litigations. The general and administrative expenses of Gufeng were $3,287,152 for the fiscal year ended June 30, 2011. In addition, the non-cash stock compensation expense was $3,605,235 for the fiscal year ended June 30, 2011.

Total Other Income (Expenses)

Total other income (expense) consisted of income from subsidies received from the PRC government, interest income, interest expenses and bank charges. Total other expense for the fiscal year ended June 30, 2011 was $160,186, as compared to total other income of $157,653 for the fiscal year ended June 30, 2010, an increase in expense of $317,839, or 201.6%. The increase was mainly attributable to the $466,912 interest expense from Gufeng’s outstanding short-term loans.

Income Taxes

Jinong is subject to a preferred tax rate of 15% as a result of its business being classified as a High-Tech project under the PRC Enterprise Income Tax Law (“EIT”) that became effective on January 1, 2008. Jinong incurred income tax expenses of $5,157,184 for the fiscal year ended June 30, 2011, as compared to $3,794,515 for the fiscal year ended June 30, 2010, an increase of $1,362,669, or 35.9%, which was primarily attributable to Jinong’s increased operating income.

Gufeng, subject to a tax rate of 25%, incurred income tax expenses of $3,879,959 for the fiscal year ended June 30, 2011.

Jintai and Yuxing are currently exempted under PRC regulations from paying income tax.

| 10 |

Net Income

Net income for the fiscal year ended June 30, 2011 was $32,914,101, an increase of $11,624,343, or 54.6%, compared to $21,289,758 for the fiscal year ended June 30, 2010. The increase was attributable to the increase in gross profit. Net income as a percentage of total net sales was approximately 18.2% and 40.9% for the fiscal year ended June 30, 2011 and 2010, respectively.

Discussion of Segment Profitability Measures

As of June 30, 2012, we were engaged in the following businesses: the production and sale of fertilizers through Jinong and Gufeng and the production and sale of high-quality agricultural products by Jintai and Yuxing. For financial reporting purposes, our operations were organized into four main business segments based on location and product: Jinong (fertilizer production), Gufeng (fertilizer production), Jintai (agricultural products production) and Yuxing (agricultural products production). Each of the segments has its own annual budget with regard to development, production and sales.

Each of the four operating segments referenced above has separate and distinct general ledgers. The chief operating decision maker (“CODM”) receives financial information, including revenue, gross margin, operating income and net income produced from the various general ledger systems to make decisions about allocating resources and assessing performance; however, the principal measure of segment profitability or loss used by the CODM is net income by segment.

For Jinong, the net income increased 28.2% by $8,224,216 to $37,363,673 for the fiscal year 2012 from $29,139,457 for the fiscal year 2011, while its net income increased 35.5% by $7,637,205 to $29,139,457 for the fiscal year 2011 from $21,502,252 for the fiscal year 2010.

For Gufeng, the net income increased 12.2% by $1,339,117 to $12,335,102 for the fiscal year 2012 from $10,995,984 for the fiscal year 2011.

For Yuxing, the net loss decreased 41.8% by$122,918.00 to $170,996 for the fiscal year 2012 from $293,914 for the fiscal year 2011, while its net loss increased 62.1% by $112,610 to a net loss of $293,914 for the fiscal year 2011 from a net loss of $181,304 for the fiscal year 2010.

For Jintai, the net loss increased 1,835.9% by $1,766,991 to $1,863,235 for the fiscal year 2012 from the net loss of $96,244 for the fiscal year 2011, while it net income decreased 103.6% by $2,736,477 to a net loss of $96,244 for the fiscal year 2011 from a net profit of $2,640,233 for the fiscal year 2010The loss incurred by Jintai in fiscal year 2012 was primarily due to its relocation.

Liquidity and Capital Resources

Our principal sources of liquidity include cash from operations, borrowings from local commercial banks and net proceeds of offerings of our securities consummated in July 2009 and November/December 2009 (collectively the “Public Offerings”).

As of June 30, 2012, cash and cash equivalents were $71,978,630, an increase of $6,372,217 and $3,270,976, or 9.7% and 5.2%, respectively, from $65,606,413 and $62,335,437 as of June 30, 2011 and 2010, respectively.

We intend to use some of the remaining net proceeds from the Public Offerings (approximately $8.5 million), as well as other working capital if required, to acquire new businesses, upgrade production lines and complete Yuxing’s new greenhouse facilities for agriculture products located on 88 acres of land in Hu County, 18 kilometers southeast of Xi’an city. We believe that we have sufficient cash on hand and positive projected cash flow from operations to support our business growth for the next twelve months to the extent we do not have further significant acquisitions or expansions. However, if events or circumstances occur and we do not meet our operating plan as expected, we may be required to seek additional capital and/or to reduce certain discretionary spending, which could have a material adverse effect on our ability to achieve our business objectives. Notwithstanding the foregoing, we may seek additional financing as necessary for expansion purposes and when we believe market conditions are most advantageous, which may include additional debt and/or equity financings. There can be no assurance that any additional financing will be available on acceptable terms, if at all. Any equity financing may result in dilution to existing stockholders and any debt financing may include restrictive covenants.

| 11 |

The following table sets forth a summary of our cash flows for the periods indicated:

| Fiscal Year Ended June 30, | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| Net cash provided by operating activities | $ | 6,400,398 | $ | 33,647,469 | $ | 12,232,035 | ||||||

| Net cash used in investing activities | (11,883,947 | ) | (32,966,702 | ) | (16,524,693 | ) | ||||||

| Net cash provided by financing activities | 10,278,376 | - | 48,451,548 | |||||||||

| Effect of exchange rate change on cash and cash equivalents | 1,577,390 | 2,590,209 | 381,100 | |||||||||

| Net increase in cash and cash equivalents | 6,372,217 | 3,270,976 | 44,539,990 | |||||||||

| Cash and cash equivalents, beginning balance | 65,606,413 | 62,335,437 | 17,795,447 | |||||||||

| Cash and cash equivalents, ending balance | $ | 71,978,630 | $ | 65,606,413 | $ | 62,335,437 | ||||||

Operating Activities

Net cash provided by operating activities was $6,399,953 for the fiscal year ended June 30, 2012, a decrease of $27,247,516, or 81.0%, and an increase of $21,415,434, or 175.1%%, respectively, from $33,647,469 and $12,232,035 net cash provided by operating activities for fiscal years 2011 and 2010, respectively. The decrease was mainly due to the increased credit sales by Gufeng during the fiscal year ended June 30, 2012, which was part of Gufeng’s warehouse selling. To retain and expand Gufeng’s market share, Gufeng enhanced its warehouse selling and increased the credit sales for Gufeng’s fertilizer products. Credit sales by Jinong have also increased during the fiscal year ended June 30, 2012 contributing to the decrease in cash provided by operations. In addition to an increase in accounts receivables, our inventory has increased to keep up with the increase in our revenues which also results in a decrease in cash provided by operations.

Investing Activities

Net cash used in investing activities for the fiscal year ended June 30, 2012 was $11,883,947, a decrease of $21,082,755, or 64.0% from $32,966,702 for the fiscal year ended June 30, 2011. The $11,883,947 used in investing activities in 2012 was on purchases of property plant and equipment. In 2011 the $32,966,702 used in investing activities consisted of purchases of property, plant and equipment of $22,740,118, the acquisition of Gufeng of $6,720,539 and an increase in construction in progress of $3,506,045.

Financing Activities

Net cash provided by financing activities in the fiscal year ended June 30, 2012 totaled $10,278,376. The net cash provided by financing activities for the same period in 2011 and 2010 was $0 and $48,451,548, mainly due to the Public Offerings. The cash provided by financing activities in 2012 was primarily due to the proceeds of loans of $9,678,375.

At June 30, 2012, 2011 and 2010, our loans payable were as follows:

| June 30, 2012 | June 30, 2011 | June 30, 2010* | ||||||||||

| Short term loans payable: | $ | 13,931,280 | $ | 4,099,550 | $ | - | ||||||

| Total | $ | 13,931,280 | $ | 4,099,550 | $ | - | ||||||

*Excludes Gufeng, which was acquired in July 2010.

| 12 |

Accounts Receivable

We had accounts receivable of $62,001,158 as of June 30, 2012, as compared to $17,517,625 and $15,571,888 as of June 30, 2011 and 2010, respectively, an increase of $44,483,533 and $1,954,737, or 253.9% and 12.5%, respectively. To retain and expand its market share, Gufeng enhanced its warehouse selling and increased the credit sales for Gufeng’s fertilizer products. Jinong has increased its sales of humic acid fertilizer products including liquid and powder fertilizers as a result of increased distributors and the aggressive marketing. The significant increase in account receivable is directly attributed to the significant increase in credit sales over the most recent fiscal year. Management continually monitors and evaluates the structure and collectability of its accounts receivable balances, performs routine assessment of our customers’ creditworthiness and provides an allowance for doubtful accounts when necessary.

Our allowance for doubtful accounts was $679,268 as of June 30, 2012, as compared to $337,801 and $193,403 as of June 30, 2011 and 2010, respectively, an increase of $341,467 and $144,398, or 101.1% and 74.7%, respectively. The increase of allowance for doubtful accounts was mainly due to the increased credit sales in Gufeng.

Inventories

We had an inventory of $28,602,684 as of June 30, 2012, as compared to $23,732,404 and $11,262,647 as of June 30, 2011 and 2010, an increase of $4,870,280 and $12,469,757 or 20.5% and110.7 %. The main reason for this increase was that we increased our packing material reserves and our finished fertilizer products for sale to meet the anticipated large order. Sales for the fiscal year ended June 30, 2012 have increased by approximately 34.3% and 43.2% over the comparable periods in 2011 and 2010, respectively. We have had to increase our inventory to keep up with current demand for our products.

Advances to Suppliers

We had advances to suppliers of $12,207,325 as of June 30, 2012 as compared to $11,487,896 and $221,280 as of June 30, 2011 and 2010, respectively, representing an increase of $719,429 and $11,266,616, or 6.3% and 5,091.6%, respectively. The increase in the amount of advances to suppliers is mainly due to Gufeng’s seasonal compound fertilizer business, which may result in carrying significant amounts of inventory and seasonal variations in working capital. To ensure our ability to deliver compound fertilizer to the distributor timely prior to the planting season, we need to have sufficient raw material in stock to feed the production. To build up the inventory, we typically make advance payment to the supplier to secure the supply of raw material of basic fertilizer. Our inability to predict future seasonal fertilizer demand accurately may result in excess inventory or product shortages.

Accounts Payable

We had accounts payable of $6,881,748 as of June 30, 2012 as compared to $5,981,703 and $328,124 as of June 30, 2011 and 2010, representing an increase of $900,045 and 5,653,579, or 15.0% and 1, 723.0%. The increase was mainly attributable to late payment on packing material due to late receipt of invoices.

Unearned Revenue

We had unearned revenue of $2,625,014 as of June 30, 2012 as compared to $11,059,313 and $41,645 as of June 30, 2011 and 2010, respectively, representing a decrease of $8,434,299, or 76.3% and an increase of $11,017,668, or 26,456.2%, respectively. The decrease in unearned revenue results from the expanded credit sales to selected distributors in Gufeng’s warehouse sales program. Such program is a customized marketing strategy that requires less or few advanced deposit payment from the participating distributors prior to the delivery of fertilizer products. With offering participating distributors certain sales credits in distributing the fertilizer products through the program, the Company manages more account receivables and concurrently has less unearned revenue.

Tax Payable

We had taxes payable of $17,675,389 as of June 30, 2012 as compared to $7,004,865 and $2,304,382 as of June 30, 2011 and 2010, respectively, representing an increase of $10,670,524 and $4,845,891, or 152.3% and 210.3%, respectively. This increase was mainly due to the growth and expansion from Gufeng post to its acquisition, which had taxes payable of $8,267,924 as of June 30, 2012.

| 13 |

Contractual Obligations

At June 30, 2012, our contractual obligations are as follows:

| Payments Due by Period | ||||||||||||||||||||

| Less Than | One to | Three to | More Than | |||||||||||||||||

| One Year | Three Years | Five Years | Five Years | Total | ||||||||||||||||

| Short term loans | $ | 13,931,280 | $ | - | $ | - | $ | - | $ | 13,931,280 | ||||||||||

| Operating lease obligations | 61,686 | 61,686 | 15,419 | 15,419 | 154,210 | |||||||||||||||

| Total | $ | 13,992,966 | $ | 61,686 | $ | 15,419 | $ | 15,419 | $ | 14,085,490 | ||||||||||

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements.

Critical Accounting Policies and Estimates

Management’s discussion and analysis of its financial condition and results of operations are based upon our consolidated financial statements, which have been prepared in accordance with United States generally accepted accounting principles. Our financial statements reflect the selection and application of accounting policies which require management to make significant estimates and judgments. See Note 2 to our consolidated financial statements, “Basis of Presentation and Summary of Significant Accounting Policies.” We believe that the following paragraphs reflect the more critical accounting policies that currently affect our financial condition and results of operations:

Use of estimates

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the amount of revenues and expenses during the reporting periods. Management makes these estimates using the best information available at the time the estimates are made. However, actual results could differ materially from those estimates.

Revenue recognition

Sales revenue is recognized at the date of shipment to customers when a formal arrangement exists, the price is fixed or determinable, the delivery is completed, we have no other significant obligations and collectability is reasonably assured. Payments received before all of the relevant criteria for revenue recognition are satisfied are recorded as unearned revenue.

Our revenue consists of invoiced value of goods, net of a value-added tax (VAT). No product return or sales discount allowance is made as products delivered and accepted by customers are not returnable and sales discounts are not granted after products are delivered.

Accounts receivable

Our policy is to maintain reserves for potential credit losses on accounts receivable. Management reviews the composition of accounts receivable and analyzes historical bad debts, customer concentrations, customer credit worthiness, current economic trends and changes in customer payment patterns to evaluate the adequacy of these reserves. Any accounts receivable that is outstanding for more than 180 days will be accounted as allowance for bad debts.

The adjustment in the credit policy is an ease of payback term for all Jinong and Gufeng’s clients. As such, no specific changes had been involved in the assessments of customer's creditworthiness and account collectability. Subsequent to the policy adjustment, we have been closely monitoring the receivables’ aging and constantly analyzing the collection results.

The current credit policy offers extra 90 days for Jinong and Gufeng’s clients to pay back the sales amount in addition to the initial 90-day period in the predecessor policy. As such, in Jinong and Gufeng, any accounts receivable aging between 90 days to 180 days, will be considered as current, instead of delinquent any more. These accounts, under the 180-day policy, no longer incur any allowance charge against their outstanding balance, but would have incur 100% allowance charge under the previous policy otherwise. In summary, under the 180-day policy, the Company is required to book less allowance charge than under the previous policy. Therefore, the allowance for doubtful accounts fell from approximately two percent of receivables at June 30, 2011 to approximately one percent of receivables at June 30, 2012.

Inventories

Inventory is valued at the lower of cost (determined on a weighted average basis) or market. Inventories consist of raw materials, work in process, finished goods and packaging materials. The Company reviews its inventories regularly for possible obsolete goods and establishes reserves when determined necessary.

| 14 |

Estimate Impairment of Long-Lived Assets

The Company tests long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable through the estimated undiscounted cash flows expected to result from the use and eventual disposition of the assets. Whenever any such impairment exists, an impairment loss will be recognized for the amount by which the carrying value exceeds the fair value.

Estimate Impairment of Intangible Assets

The Company records intangible assets acquired individually or as part of a group at fair value. Intangible assets with definitive lives are amortized over the useful life of the intangible asset, which is the period over which the asset is expected to contribute directly or indirectly to the entity’s future cash flows. The Company evaluates intangible assets for impairment at least annually and more often whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Whenever any such impairment exists, an impairment loss will be recognized for the amount by which the carrying value exceeds the fair value. The Company has not recorded impairment of intangible assets as of June 30, 2012, 2011, and 2010, respectively.

Fair Value Measurement and Disclosures

Our accounting for Fair Value Measurement and Disclosures, defines fair value as the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. This topic also establishes a fair value hierarchy which requires classification based on observable and unobservable inputs when measuring fair value. The fair value hierarchy distinguishes between assumptions based on market data (observable inputs) and an entity’s own assumptions (unobservable inputs). The hierarchy consists of three levels:

Level one — Quoted market prices in active markets for identical assets or liabilities;

Level two — Inputs other than level one inputs that are either directly or indirectly observable; and

Level three — Unobservable inputs developed using estimates and assumptions, which are developed by the reporting entity and reflect those assumptions that a market participant would use.

Determining which category an asset or liability falls within the hierarchy requires significant judgment. The Company evaluates its hierarchy disclosures each quarter. The Company had no assets and liabilities measured at fair value at June 30, 2011.

The carrying values of cash and cash equivalents, trade and other receivables, trade and other payables approximate their fair values due to the short maturities of these instruments.

Stock-Based Compensation

The costs of all employee stock options, as well as other equity-based compensation arrangements, are reflected in the consolidated financial statements based on the estimated fair value of the awards on the grant date. That cost is recognized over the period during which an employee is required to provide service in exchange for the award—the requisite service period (usually the vesting period). Stock compensation for stock granted to non-employees is determined as the fair value of the consideration received or the fair value of equity instruments issued, whichever is more reliably measured.

Income taxes

The Company accounts for income taxes using an asset and liability approach which allows for the recognition and measurement of deferred tax assets based upon the likelihood of realization of tax benefits in future years. Under the asset and liability approach, deferred taxes are provided for the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. A valuation allowance is provided for deferred tax assets if it is more likely than not these items will either expire before the Company is able to realize their benefits, or that future deductibility is uncertain.

| 15 |

Under ASC 740, a tax position is recognized as a benefit only if it is “more likely than not” that the tax position would be sustained in a tax examination, with a tax examination being presumed to occur. The evaluation of a tax position is a two-step process. The first step is to determine whether it is more-likely-than-not that a tax position will be sustained upon examination, including the resolution of any related appeals or litigations based on the technical merits of that position. The second step is to measure a tax position that meets the more-likely-than-not threshold to determine the amount of benefit to be recognized in the financial statements. A tax position is measured at the largest amount of benefit that is greater than 50 percent likely of being realized upon ultimate settlement. Tax positions that previously failed to meet the more-likely-than-not recognition threshold should be recognized in the first subsequent period in which the threshold is met. Previously recognized tax positions that no longer meet the more-likely-than-not criteria should be de-recognized in the first subsequent financial reporting period in which the threshold is no longer met. Penalties and interest incurred related to underpayment of income tax are classified as income tax expense in the year incurred. No significant penalties or interest relating to income taxes have been incurred during the years ended June 30, 2012, 2011 and 2010. GAAP also provides guidance on de-recognition, classification, interest and penalties, accounting in interim periods, disclosures and transition.

Foreign currency translation

The reporting currency of the Company is the US dollar. The functional currency of the Company and Green New Jersey is the US dollar. The functional currency of the Chinese subsidiaries is the Chinese Yuan or Renminbi (“RMB”). For the subsidiaries whose functional currencies are other than the US dollar, all asset and liability accounts were translated at the exchange rate on the balance sheet date; stockholder's equity is translated at the historical rates and items in the cash flow statements are translated at the average rate in each applicable period. Translation adjustments resulting from this process are included in accumulated other comprehensive income in the statement of shareholders’ equity. The resulting translation gains and losses that arise from exchange rate fluctuations on transactions denominated in a currency other than the functional currency are included in the results of operations as incurred.

Segment reporting

FASB ASC 280, (previously SFAS No. 131, Segment Reporting) requires use of the “management approach” model for segment reporting. The management approach model is based on the way a company’s management organizes segments within the company for making operating decisions and assessing performance. Reportable segments are based on products and services, geography, legal structure, management structure, or any other manner in which management disaggregates a company.

During the year ended June 30, 2012, we were organized into four main business segments: Jinong (fertilizer production), Gufeng (fertilizer production), Jintai (agricultural products production) and Yuxing (agricultural products production).

Recent Accounting Pronouncements

For information with respect to recent accounting pronouncements and the impact of these pronouncements on our consolidated financial statements, see Note 2 of Notes to Consolidated Financial Statements included elsewhere in this Report.

| 16 |

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| China Green Agriculture, Inc. | ||

| Date: January18, 2013 | By: | /s/ Tao Li |

| Tao Li | ||

| President and CEO | ||

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of the Registrant and in the capacities and on the dates indicated.

| January 18, 2013 | /s/ Tao Li | |

| Tao Li, Chairman of the Board of Directors, President and CEO | ||

| (principal executive officer) | ||

| January 18, 2013 | /s/ Ken Ren | |

| Ken Ren, Chief Financial Officer | ||

(principal financial officer and principal accounting officer) | ||

| January 18, 2013 | /s/ Yu Hao | |

| Yu Hao, Director | ||

| January 18, 2013 | /s/ Lianfu Liu | |

| Lianfu Liu, Director | ||

| January 18, 2013 | /s/ Yizhao Zhang | |

| Yizhao Zhang, Director | ||

| January 18, 2013 | /s/ Yiru Shi | |

| Yiru Shi, Director | ||

| 17 |

China Green Agriculture, Inc.

Exhibit Index to Amendment No. 2 to Annual Report on Form 10-K/A

For the Year Ended June 30, 2012

| 3.1* | Articles of Incorporation (incorporated herein by reference to the Company’s Quarterly Report on Form 10-QSB, for the quarter ended September 30, 2007, filed with the SEC on November 9, 2007, Exhibit 3.1). |

| 3.2* | Certificate of Change filed with the Secretary of State of the State of Nevada on December 18, 2007 (incorporated herein by reference to the Company’s Current Report on Form 8-K filed with the SEC on January 2, 2008, Exhibit 4.2). |

| 3.3* | Certificate of Correction (incorporated herein by reference to the Company’s Registration Statement on Form S-1 filed with the SEC on February 8, 2008, Exhibit 4.1). |

| 3.4* | Articles of Merger (incorporated herein by reference to the Company’s Current Report on Form 8-K, filed February 5, 2008, Exhibit 3.1). |

| 3.5* | Bylaws (incorporated herein by reference to the Company’s Quarterly Report on Form 10-QSB, for the quarter ended September 30, 2007, filed with the SEC on November 9, 2007, Exhibit 3.2). |

| 4.1* | Specimen Common Stock Certificate (incorporated herein by reference to the Company’s Registration Statement on Form S-3 filed with the SEC on June 8, 2009, Exhibit 4.1). |

| 10.1* | Employment Agreement, dated January 16, 2008, by and between Shaanxi TechTeam Jinong Humic Acid Product Co., Ltd. and Mr. Tao Li (incorporated herein by reference to the Company’s Annual Report on Form 10-K filed with the SEC on September 7, 2010). |

| 10.2* | Employment Agreement, dated June 21, 2010, by and between the Company and Mr. Ken Ren (Incorporated herein by reference to our Current Report on Form 8-K filed with the SEC on June 25, 2010) |

| 10.3* | Share Transfer Agreement, dated July 1, 2010, by and between Shaanxi TechTeam Jinong Humic Acid Product Co., Ltd., Qing Xin Jiang and Qiong Jia (Incorporated herein by reference to the Current Report on Form 8-K filed with the SEC on July 7, 2010). |

| 10.4* | Supplementary Agreement, dated July 1, 2010, by and between Shaanxi TechTeam Jinong Humic Acid Product Co., Ltd., Qing Xin Jiang and Qiong Jia (Incorporated herein by reference to the Current Report on Form 8-K filed with the SEC on July 7, 2010). |

| 18 |

| 10.5* | Employment Agreement by and between Beijing Gufeng Chemical Products Co., Ltd. and Qing Xin Jiang dated July 1, 2010. (Incorporated herein by reference to the Annual Report on Form 10-K filed with the SEC on September 12, 2011) |

| 10.6* | Form of Non-Competition Agreement by and between Beijing Gufeng Chemical Products Co., Ltd. and its two major former shareholders. (Incorporated herein by reference to the Annual Report on Form 10-K filed with the SEC on September 12, 2011) |

| 10.7* | Form of Restricted Stock Grant Agreement (Incorporated herein by reference to the Current Report on Form 8-K filed with the SEC on January 11, 2010). |

| 10.8* | Form of Non-Qualified Stock Option Grant Agreement (Incorporated herein by reference to the Current Report on Form 8-K filed with the SEC on January 11, 2010). |

| 10.9* | Offer Letter dated March 28, 2011 between China Green Agriculture, Inc. and Yizhao Zhang. (Incorporated herein by reference to the Quarterly Report on Form 10-Q filed with the SEC on May 10, 2011) |

| 10.10* | Offer Letter dated March 28, 2011 between China Green Agriculture, Inc. and Lianfu Liu. (Incorporated herein by reference to the Quarterly Report on Form 10-Q filed with the SEC on May 10, 2011) |

| 10.11* | Offer Letter dated October 25, 2011 between China Green Agriculture, Inc. and Yiru Shi |

| 10.12* | Project Construction Contract dated August 10, 2010 between Xi’an Hu County Yuxing Agriculture Science & Technology Co., Ltd. and Xi’an Kingtone Information Technology Co., Ltd. (Incorporated herein by reference to the Quarterly Report on Form 10-Q filed with the SEC on November 12, 2010) |

| 14.1* | Amended and Restated Code of Ethics. (Incorporated herein by reference to the Quarterly Report on Form 10-Q filed with the SEC on November 12, 2010) |

| 21.1* | List of Subsidiaries of the Company. |

| 23.1* | Consent of Kabani & Company, Inc., Independent Registered Public Accounting Firm. |

| 31.1** | Certification of CEO pursuant to Exchange Act Rules 13a-14(a) and 15d-14(a), as adopted pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. |

| 31.2** | Certification of CFO pursuant to Exchange Act Rules 13a-14(a) and 15d-14(a), as adopted pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. |

| 32.1** | Certification pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. |

| 19 |

| 101.INS** | XBRL Instance Document |

| 101.SCH** | XBRL Taxonomy Extension Schema Document |

| 101.CAL** | XBRL Taxonomy Extension Calculation Linkbase Document |

| 101.DEF** | XBRL Taxonomy Extension Definition Linkbase Document |

| 101.LAB** | XBRL Taxonomy Extension Label Linkbase Document |

| 101.PRE** | XBRL Taxonomy Extension Presentation Linkbase Document |

| * | Filed previously. |

| ** | Filed herewith. |

| 20 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of

China Green Agriculture Inc. and its subsidiaries

We have audited the accompanying consolidated balance sheets of China Green Agriculture, Inc. and its subsidiaries (the “Company”) as of June 30, 2012 and 2011, and the related consolidated statements of income and comprehensive income, stockholders' equity, and cash flows for each of the years in the three-year period ended June 30, 2012. Our audits also included the financial statement schedule listed in the Index at Item 15(a) 2. The Company’s management is responsible for these financial statements and schedules. Our responsibility is to express an opinion on these financial statements and schedules based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and schedules are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of China Green Agriculture, Inc. and its subsidiaries as of June 30, 2012 and 2011, and the results of its operations and its cash flows for each of the years in the three-year period ended June 30, 2012 in conformity with accounting principles generally accepted in the United States of America.