UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(MARK ONE)

x QUARTERLY REPORT PURSUANT TO SECTION 13 or 15 (d) OF THE SECURITIES

EXCHANGE ACT OF 1934

FOR THE FISCAL QUARTERLY PERIOD ENDED DECEMBER 31, 2012

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 or 15 (d) OF THE SECURITIES

EXCHANGE ACT OF 1934

COMMISSION FILE NUMBER: 1-11906

MEASUREMENT SPECIALTIES, INC.

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

| New Jersey | 22-2378738 | |

|

(STATE OR OTHER JURISDICTION OF INCORPORATION OR ORGANIZATION) |

(I.R.S. EMPLOYER IDENTIFICATION NO. ) |

1000 LUCAS WAY, HAMPTON, VA 23666

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES)

(757) 766-1500

(REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No £.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Securities Exchange Act of 1934. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ | Smaller reporting company ¨ |

| (Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes ¨ No x.

Indicate the number of shares outstanding of each of the issuer’s classes of stock, as of the latest practicable date: On January 28, 2013, the number of shares outstanding of the Registrant’s common stock was 15,437,824.

MEASUREMENT SPECIALTIES, INC.

FORM 10-Q

TABLE OF CONTENTS

DECEMBER 31, 2012

| PART I. | FINANCIAL INFORMATION | 3 | |

| ITEM 1. | FINANCIAL STATEMENTS | 3 | |

| CONSOLIDATED CONDENSED STATEMENTS OF OPERATIONS (UNAUDITED) | 3 | ||

| CONSOLIDATED CONDENSED STATEMENTS COMPREHENSIVE INCOME (UNAUDITED) | 4 | ||

| CONSOLIDATED CONDENSED BALANCE SHEETS (UNAUDITED) | 5 | ||

| CONSOLIDATED CONDENSED STATEMENTS OF SHAREHOLDERS’ EQUITY(UNAUDITED) | 7 | ||

| CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS (UNAUDITED) | 8 | ||

| NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (UNAUDITED) | 9 | ||

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 23 | |

| ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 40 | |

| ITEM 4. | CONTROLS AND PROCEDURES | 41 | |

| PART II. | OTHER INFORMATION | 41 | |

| ITEM 1. | LEGAL PROCEEDINGS | 41 | |

| ITEM 1A. | RISK FACTORS | 41 | |

| ITEM 6. | EXHIBITS | 42 | |

| SIGNATURES | 43 | ||

| 2 |

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

MEASUREMENT SPECIALTIES, INC. AND SUBSIDIARIES

CONSOLIDATED CONDENSED STATEMENTS OF OPERATIONS

(UNAUDITED)

| Three months ended | Nine months ended | |||||||||||||||

| December 31, | December 31, | |||||||||||||||

| (Amounts in thousands, except share and per share amounts) | 2012 | 2011 | 2012 | 2011 | ||||||||||||

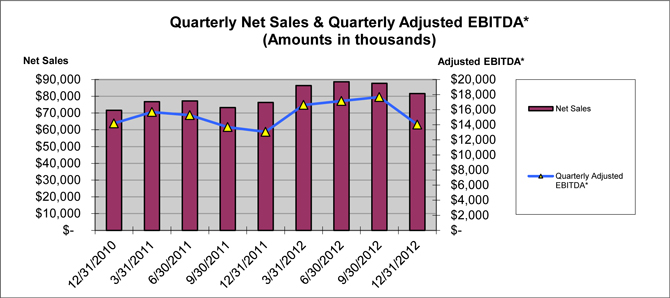

| Net sales | $ | 81,628 | $ | 76,341 | $ | 258,006 | $ | 226,768 | ||||||||

| Cost of goods sold | 49,074 | 47,470 | 151,790 | 135,449 | ||||||||||||

| Gross profit | 32,554 | 28,871 | 106,216 | 91,319 | ||||||||||||

| Selling, general, and administrative expenses | 24,873 | 22,406 | 75,527 | 66,282 | ||||||||||||

| Operating income | 7,681 | 6,465 | 30,689 | 25,037 | ||||||||||||

| Interest expense, net | 688 | 806 | 2,072 | 1,932 | ||||||||||||

| Foreign currency exchange loss (gain) | (7 | ) | 27 | 235 | 47 | |||||||||||

| Equity income in unconsolidated joint venture | (143 | ) | (240 | ) | (534 | ) | (612 | ) | ||||||||

| Impairment of asset held for sale | - | - | 489 | - | ||||||||||||

| Acquisition earn-out adjustment | - | - | (3,775 | ) | - | |||||||||||

| Other expense (income) | (28 | ) | (10 | ) | (15 | ) | 41 | |||||||||

| Income before income taxes | 7,171 | 5,882 | 32,217 | 23,629 | ||||||||||||

| Income tax expense | 1,075 | 1,187 | 7,144 | 4,269 | ||||||||||||

| Net income | $ | 6,096 | $ | 4,695 | $ | 25,073 | $ | 19,360 | ||||||||

| Earnings per common share - Basic: | ||||||||||||||||

| Net income - Basic | $ | 0.40 | $ | 0.31 | $ | 1.63 | $ | 1.29 | ||||||||

| Net income - Diluted | $ | 0.38 | $ | 0.30 | $ | 1.55 | $ | 1.22 | ||||||||

| Weighted average shares outstanding - Basic | 15,352 | 15,040 | 15,348 | 15,059 | ||||||||||||

| Weighted average shares outstanding - Diluted | 16,087 | 15,818 | 16,126 | 15,918 | ||||||||||||

See accompanying notes to consolidated condensed financial statements.

| 3 |

MEASUREMENT SPECIALTIES, INC. AND SUBSIDIARIES

CONSOLIDATED CONDENSED STATEMENTS OF

COMPREHENSIVE INCOME

FOR THE THREE AND NINE MONTHS ENDED DECEMBER 31, 2012 AND 2011

(UNAUDITED)

| Three months ended | Nine months ended | |||||||||||||||

| December 31, | December 31, | |||||||||||||||

| (Amounts in thousands) | 2012 | 2011 | 2012 | 2011 | ||||||||||||

| Net income | $ | 6,096 | $ | 4,695 | $ | 25,073 | $ | 19,360 | ||||||||

| Other comprehensive income, net of income taxes: | ||||||||||||||||

| Currency translation adjustments | 2,273 | (2,595 | ) | (581 | ) | (2,883 | ) | |||||||||

| Comprehensive income | $ | 8,369 | $ | 2,100 | $ | 24,492 | $ | 16,477 | ||||||||

See accompanying notes to consolidated condensed financial statements.

| 4 |

MEASUREMENT SPECIALTIES, INC. AND SUBSIDIARIES

CONSOLIDATED CONDENSED BALANCE SHEETS

(UNAUDITED)

| (Amounts in thousands) | December 31, 2012 | March 31, 2012 | ||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 32,161 | $ | 32,725 | ||||

| Accounts receivable trade, net of allowance for doubtful accounts of $957 and $766, respectively | 50,360 | 49,315 | ||||||

| Inventories, net | 60,662 | 57,704 | ||||||

| Deferred income taxes, net | 1,768 | 1,626 | ||||||

| Prepaid expenses and other current assets | 4,193 | 5,229 | ||||||

| Other receivables | 1,623 | 2,967 | ||||||

| Asset held for sale | 940 | 1,429 | ||||||

| Total current assets | 151,707 | 150,995 | ||||||

| Property, plant and equipment, net | 65,282 | 60,484 | ||||||

| Goodwill | 154,612 | 144,455 | ||||||

| Acquired intangible assets, net | 58,722 | 49,378 | ||||||

| Deferred income taxes, net | 4,011 | 3,613 | ||||||

| Investment in unconsolidated joint venture | 2,734 | 3,038 | ||||||

| Other assets | 7,427 | 6,244 | ||||||

| Total assets | $ | 444,495 | $ | 418,207 | ||||

See accompanying notes to consolidated condensed financial statements.

| 5 |

MEASUREMENT SPECIALTIES, INC. AND SUBSIDIARIES

CONSOLIDATED CONDENSED BALANCE SHEETS

(UNAUDITED)

| (Amounts in thousands, except share amounts) | December 31, 2012 | March 31, 2012 | ||||||

| LIABILITIES AND SHAREHOLDERS' EQUITY | ||||||||

| Current liabilities: | ||||||||

| Short-term debt | $ | - | $ | 1,867 | ||||

| Current portion of long-term debt | 198 | 123 | ||||||

| Current portion of capital lease obligations | 26 | 30 | ||||||

| Deferred acquisition payment | 1,480 | - | ||||||

| Accounts payable | 25,597 | 31,879 | ||||||

| Accrued expenses | 5,297 | 5,116 | ||||||

| Accrued compensation | 10,002 | 8,755 | ||||||

| Income taxes payable | 1,962 | 3,124 | ||||||

| Deferred income taxes, net | 521 | 375 | ||||||

| Other current liabilities | 2,856 | 3,201 | ||||||

| Total current liabilities | 47,939 | 54,470 | ||||||

| Revolver | 86,000 | 80,251 | ||||||

| Long-term debt, net of current portion | 20,538 | 20,711 | ||||||

| Capital lease obligations, net of current portion | 11 | 30 | ||||||

| Acquisition earn-out contingencies | 1,826 | 4,317 | ||||||

| Deferred income taxes, net | 11,336 | 10,184 | ||||||

| Other liabilities | 6,497 | 5,227 | ||||||

| Total liabilities | 174,147 | 175,190 | ||||||

| Equity: | ||||||||

| Serial preferred stock; 221,756 shares authorized; none outstanding | - | - | ||||||

| Common stock, no par; 25,000,000 shares authorized; 15,403,666 shares and 15,297,151 shares issued and outstanding | - | - | ||||||

| Additional paid-in capital | 104,274 | 101,435 | ||||||

| Retained earnings | 154,086 | 129,013 | ||||||

| Accumulated other comprehensive income | 11,988 | 12,569 | ||||||

| Total equity | 270,348 | 243,017 | ||||||

| Total liabilities and shareholders' equity | $ | 444,495 | $ | 418,207 | ||||

See accompanying notes to consolidated condensed financial statements.

| 6 |

MEASUREMENT SPECIALTIES, INC. AND SUBSIDIARIES

CONSOLIDATED CONDENSED STATEMENTS OF SHAREHOLDERS’ EQUITY

FOR THE NINE MONTHS ENDED DECEMBER 31, 2012 AND 2011

(UNAUDITED)

| Accumulated | ||||||||||||||||||||

| Shares of | Additional | Other | ||||||||||||||||||

| Common | Paid-in | Retained | Comprehensive | |||||||||||||||||

| (Amounts in thousands, except share amounts) | Stock | Capital | Earnings | Income | Total | |||||||||||||||

| Balance, March 31, 2011 | 14,989,675 | $ | 93,608 | $ | 101,309 | $ | 14,152 | $ | 209,069 | |||||||||||

| Net income | 19,360 | - | 19,360 | |||||||||||||||||

| Currency translation adjustment | - | (2,883 | ) | (2,883 | ) | |||||||||||||||

| Unregcognized pension plan costs | - | - | ||||||||||||||||||

| Comprehensive income | - | |||||||||||||||||||

| Non-cash equity based compensation | 3,662 | - | - | 3,662 | ||||||||||||||||

| Amounts from exercise of stock options | 327,335 | 5,123 | - | - | 5,123 | |||||||||||||||

| Tax benefit from exercise of stock options | 819 | - | - | 819 | ||||||||||||||||

| Purchases of company stock | (229,911 | ) | (6,505 | ) | - | - | (6,505 | ) | ||||||||||||

| Balance, December 31, 2011 | 15,087,099 | $ | 96,707 | $ | 120,669 | $ | 11,269 | $ | 228,645 | |||||||||||

| Balance, March 31, 2012 | 15,297,151 | $ | 101,435 | $ | 129,013 | $ | 12,569 | $ | 243,017 | |||||||||||

| Net income | 25,073 | - | 25,073 | |||||||||||||||||

| Currency translation adjustment | - | (581 | ) | (581 | ) | |||||||||||||||

| Non-cash equity based compensation | 3,744 | - | - | 3,744 | ||||||||||||||||

| Amounts from exercise of stock options | 321,676 | 4,950 | - | - | 4,950 | |||||||||||||||

| Tax benefit from exercise of stock options | 1,145 | - | - | 1,145 | ||||||||||||||||

| Purchases of company stock | (215,161 | ) | (7,000 | ) | - | - | (7,000 | ) | ||||||||||||

| Balance, December 31, 2012 | 15,403,666 | $ | 104,274 | $ | 154,086 | $ | 11,988 | $ | 270,348 | |||||||||||

See accompanying notes to consolidated condensed financial statements.

| 7 |

MEASUREMENT SPECIALTIES, INC. AND SUBSIDIARIES

CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Nine months ended December 31, | ||||||||

| (Amounts in thousands) | 2012 | 2011 | ||||||

| Cash flows from operating activities: | ||||||||

| Net income | $ | 25,073 | $ | 19,360 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Depreciation and amortization | 13,211 | 11,948 | ||||||

| Non-cash equity based compensation | 3,744 | 3,662 | ||||||

| Acquisition earn-out adjustment | (3,775 | ) | - | |||||

| Impairment of asset held for sale | 489 | - | ||||||

| Deferred income taxes | (1,660 | ) | (479 | ) | ||||

| Equity income in unconsolidated joint venture | (534 | ) | (612 | ) | ||||

| Unconsolidated joint venture distributions | 825 | 582 | ||||||

| Net change in operating assets and liabilities: | ||||||||

| Accounts receivable, trade | 968 | 2,142 | ||||||

| Inventories | (686 | ) | (2,932 | ) | ||||

| Prepaid expenses, other current assets and other receivables | 2,224 | 596 | ||||||

| Other assets | (1,366 | ) | (1,910 | ) | ||||

| Accounts payable | (6,867 | ) | 1,622 | |||||

| Accrued expenses, accrued compensation, other current and other liabilities | 2,582 | (3,576 | ) | |||||

| Income taxes payable | 557 | (3,209 | ) | |||||

| Net cash provided by operating activities | 34,785 | 27,194 | ||||||

| Cash flows from investing activities: | ||||||||

| Purchases of property and equipment | (11,244 | ) | (9,759 | ) | ||||

| Acquisition of business, net of cash acquired, and acquired intangible assets | (27,466 | ) | (46,317 | ) | ||||

| Net cash used in investing activities | (38,710 | ) | (56,076 | ) | ||||

| Cash flows from financing activities: | ||||||||

| Borrowings from revolver and short-term debt | 25,797 | 48,900 | ||||||

| Repayments of revolver and capital leases | (21,859 | ) | (14,559 | ) | ||||

| Repayments of long-term debt | (88 | ) | (141 | ) | ||||

| Payment of deferred financing costs | - | (353 | ) | |||||

| Purchase of treasury stock | (7,000 | ) | (6,500 | ) | ||||

| Proceeds from exercise of options and employee stock purchase plan | 4,950 | 5,123 | ||||||

| Excess tax benefit from exercise of stock options | 1,145 | 819 | ||||||

| Net cash provided by (used in) financing activities | 2,945 | 33,289 | ||||||

| Net change in cash and cash equivalents | (980 | ) | 4,407 | |||||

| Effect of exchange rate changes on cash | 416 | (715 | ) | |||||

| Cash, beginning of year | 32,725 | 20,860 | ||||||

| Cash, end of period | $ | 32,161 | $ | 24,552 | ||||

| Supplemental Cash Flow Information: | ||||||||

| Cash paid or received during the period for: | ||||||||

| Interest paid | $ | (1,966 | ) | $ | (1,627 | ) | ||

| Income taxes paid | (5,928 | ) | (5,928 | ) | ||||

| Income taxes refunded | - | 72 | ||||||

See accompanying notes to condensed consolidated financial statements.

| 8 |

MEASUREMENT SPECIALTIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

FOR THE THREE AND NINE MONTHS ENDED DECEMBER 31, 2012 AND 2011

(UNAUDITED)

(Currency amounts in thousands, except share and per share amounts)

1. DESCRIPTION OF BUSINESS

Interim financial statements: The information presented as of December 31, 2012 and for the three and nine months ended December 31, 2012 and 2011 is unaudited, and reflects all adjustments (consisting only of normal recurring adjustments) which Measurement Specialties, Inc. (the “Company,” “MEAS,” or “we”) considers necessary for the fair presentation of the Company’s financial position as of December 31, 2012, the results of its operations for the three and nine months ended December 31, 2012 and 2011, and cash flows for the nine months ended December 31, 2012 and 2011. The Company’s March 31, 2012 consolidated condensed balance sheet information was derived from the audited consolidated financial statements for the year ended March 31, 2012, which is included as part of the Company’s Annual Report on Form 10-K.

The consolidated condensed financial statements included herein have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) and the instructions to Form 10-Q and Regulation S-X. Accordingly, certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. generally accepted accounting principles have been condensed or omitted. These consolidated condensed financial statements should be read in conjunction with the Company’s audited consolidated financial statements for the year ended March 31, 2012, which are included as part of the Company’s Annual Report on Form 10-K.

Description of business: Measurement Specialties, Inc. is a global leader in the design, development and manufacture of sensors and sensor-based systems for original equipment manufacturers (“OEM”) and end users, based on a broad portfolio of proprietary technology and typically characterized by the MEAS brand name. We are a global business and we believe we have a high degree of diversity when considering our geographic reach, broad range of products, number of end-use markets and breadth of customer base. The Company is a multi-national corporation with fifteen primary manufacturing facilities strategically located in the United States, China, France, Ireland, Germany, Switzerland and Scotland, enabling the Company to produce and market globally a wide range of sensors that use advanced technologies to measure precise ranges of physical characteristics. These sensors are used for engine and vehicle, medical, general industrial, consumer and home appliance, military/aerospace, environmental water monitoring, and test and measurement applications. The Company’s products include sensors for measuring pressure, linear/rotary position, force, torque, piezoelectric polymer film sensors, custom microstructures, load cells, vibrations and acceleration, optical absorption, humidity, gas concentration, gas flow rate, temperature, fluid properties and fluid level. The Company’s advanced technologies include piezo-resistive silicon, polymer and ceramic piezoelectric materials, application specific integrated circuits, micro-electromechanical systems (“MEMS”), foil strain gauges, electromagnetic force balance systems, fluid capacitive devices, linear and rotational variable differential transformers, anisotropic magneto-resistive devices, electromagnetic displacement sensors, hygroscopic capacitive structures, ultrasonic measurement systems, optical measurement systems, negative thermal coefficient (“NTC”) ceramic sensors, 3-6 DOF (degree of freedom) force/torque structures, complex mechanical resonators, magnetic reed switches, high frequency multipoint scanning algorithms, and high precision submersible hydrostatic level detection.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES:

Principles of consolidation: The consolidated condensed financial statements include the accounts of the Company and its wholly-owned subsidiaries (the “Subsidiaries”). All significant intercompany balances and transactions have been eliminated in consolidation.

| 9 |

The Company accounts for its 50 percent ownership interest in Nikkiso-THERM (“NT”), a joint venture in Japan and the Company’s one variable interest entity (“VIE”), under the equity method of accounting. Under the equity method of accounting, the Company does not consolidate the VIE but recognizes its proportionate share of the profits and losses of the unconsolidated VIE.

Use of estimates: The preparation of the consolidated condensed financial statements, in accordance with U.S. generally accepted accounting principles, requires management to make estimates and assumptions which affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and revenues and expenses during the reporting period. Significant items subject to such estimates and assumptions include the useful lives of fixed assets, carrying amount and analysis of recoverability of property, plant and equipment, asset held for sale, acquired intangibles, goodwill, deferred tax assets, valuation allowances for receivables, inventories, income tax uncertainties and other contingencies, including acquisition earn-outs, and stock based compensation. Actual results could differ from those estimates.

Recently adopted accounting pronouncements: In June 2011, the FASB issued new accounting standards for reporting comprehensive income. The new accounting standards revise only the presentation of comprehensive income in financial statements and require that net income and other comprehensive income be reported either in a single, continuous statement of comprehensive income or in two separate, but consecutive, statements. Presentation of components of comprehensive income in the statements as changes in stockholders’ equity will no longer be allowed. In December 2011, the FASB issued an amendment to the new accounting standards for reporting comprehensive income with the Deferral of the Effective Date for Amendments to the Presentation of Reclassifications of Items Out of Accumulated Other Comprehensive, which defers the changes that relate to the presentation of reclassification adjustments. These new reporting requirements were effective for fiscal years, and interim periods within those years, beginning after December 15, 2011, which is the Company’s 2013 fiscal year. Early adoption of the standard was permitted. The Company applied the new reporting requirements effective April 1, 2012.

3. STOCK BASED COMPENSATION AND PER SHARE INFORMATION

Non-cash equity-based compensation expense for the three months ended December 31, 2012 and 2011 was $1,500 and $1,162, respectively, and for the nine months ended December 31, 2012 and 2011 was $3,744 and $3,662, respectively. During the nine months ended December 31, 2012, the Company granted 409,050 stock awards from the 2010 Equity Incentive Plan (the “2010 Plan”). The estimated fair value of stock options and restricted stock units granted during the nine months ended December 31, 2012 approximated $6,123, net of expected forfeitures and is being recognized over the respective vesting periods. During the three and nine months ended December 31, 2012, the Company recognized $834 and $1,789, respectively, of expense related to these stock awards.

The Company has five share-based compensation plans for which equity awards are currently outstanding. These plans are administered by the compensation committee of the Board of Directors, which approves grants to individuals eligible to receive awards and determines the number of shares and/or options subject to each award, the terms, conditions, performance measures, and other provisions of the award. The Chief Executive Officer can also grant individual awards up to certain limits as approved by the compensation committee. Awards are generally granted based on the individual’s performance. Terms for stock option awards include pricing based on the closing price of the Company’s common stock on the award date, and generally vest over three to five year requisite service periods using a graded vesting schedule or subject to performance targets established by the compensation committee. Shares issued under stock option plans are newly issued common stock. Readers should refer to Note 13 of the consolidated financial statements in the Company’s Annual Report on Form 10-K for the fiscal year ended March 31, 2012 for additional information related to the five share-based compensation plans under which awards are currently outstanding.

The Company uses the Black-Scholes-Merton option pricing model to estimate the fair value of equity-based awards with the following assumptions for the indicated periods.

| 10 |

| Three months ended December 31, | Nine months ended December 31, | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Dividend yield | - | - | - | - | ||||||||||||

| Expected volatility | 61.1 | % | 68.6 | % | 60.8 | % | 68.6 | % | ||||||||

| Risk free interest rate | 0.7 | % | 1.8 | % | 0.7 | % | 1.8 | % | ||||||||

| Expected term after vesting (in years) | 2.0 | 2.0 | 2.0 | 2.0 | ||||||||||||

| Weighted-average grant-date fair value | $ | 16.61 | $ | 17.79 | $ | 15.49 | $ | 17.79 | ||||||||

The assumptions above are based on multiple factors, including historical exercise patterns of employees with respect to exercise and post-vesting employment termination behaviors, expected future exercise patterns for these employees and the historical volatility of our stock price. The expected term of options granted is derived using company-specific, historical exercise information and represents the period of time that options granted are expected to be outstanding. The risk-free interest rate for periods within the contractual life of the option is based on the U.S. Treasury yield curve in effect at the time of grant.

During the nine months ended December 31, 2012, a total of 321,676 stock awards were exercised yielding $4,950 in cash proceeds and excess tax benefit of $1,145 recognized as additional paid-in capital. At December 31, 2012, there was $4,997 of unrecognized compensation cost adjusted for estimated forfeitures related to share-based payments, which is expected to be recognized over a weighted-average period of approximately 1.51 years.

Per share information: Basic and diluted per share calculations are based on net income. Basic per share information is computed based on the weighted average common shares outstanding during each period. Diluted per share information additionally considers the shares that may be issued upon exercise or conversion of stock options, less the shares that may be repurchased with the funds received from their exercise. Outstanding awards relating to approximately 347,860 and 139,902 weighted shares were excluded from the calculation for the three months ended December 31, 2012 and 2011, respectively, and outstanding awards relating to approximately 259,063 and 417,635 weighted shares were excluded from the calculation for the nine months ended December 31, 2012 and 2011, as the impact of including such awards in the calculation of diluted earnings per share would have had an anti-dilutive effect.

The computation of the basic and diluted net income per common share is as follows:

Net income (Numerator) | Weighted Average Shares in thousands (Denominator) | Per-Share Amount | ||||||||||

| Three months ended December 31, 2012: | ||||||||||||

| Basic per share information | $ | 6,096 | 15,352 | $ | 0.40 | |||||||

| Effect of dilutive securities | - | 735 | (0.02 | ) | ||||||||

| Diluted per-share information | $ | 6,096 | 16,087 | $ | 0.38 | |||||||

| Three months ended December 31, 2011: | ||||||||||||

| Basic per share information | $ | 4,695 | 15,040 | $ | 0.31 | |||||||

| Effect of dilutive securities | - | 778 | (0.01 | ) | ||||||||

| Diluted per-share information | $ | 4,695 | 15,818 | $ | 0.30 | |||||||

| Nine months ended December 31, 2012: | ||||||||||||

| Basic per share information | $ | 25,073 | 15,348 | $ | 1.63 | |||||||

| Effect of dilutive securities | - | 778 | (0.08 | ) | ||||||||

| Diluted per-share information | $ | 25,073 | 16,126 | $ | 1.55 | |||||||

| Nine months ended December 31, 2011: | ||||||||||||

| Basic per share information | $ | 19,360 | 15,059 | $ | 1.29 | |||||||

| Effect of dilutive securities | - | 859 | (0.07 | ) | ||||||||

| Diluted per-share information | $ | 19,360 | 15,918 | $ | 1.22 | |||||||

| 11 |

4. INVENTORIES

Inventories are valued at the lower of cost or market (“LCM”) using the first-in first-out method. Inventories and inventory reserves for slow-moving, obsolete and lower of cost or market exposures at December 31, 2012 and March 31, 2012 are summarized as follows:

| December 31, 2012 | March 31, 2012 | |||||||

| Raw Materials | $ | 32,349 | $ | 30,419 | ||||

| Work-in-Process | 10,259 | 11,929 | ||||||

| Finished Goods | 22,383 | 19,613 | ||||||

| 64,991 | 61,961 | |||||||

| Inventory Reserves | (4,329 | ) | (4,257 | ) | ||||

| $ | 60,662 | $ | 57,704 | |||||

5. PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment are stated at cost. Equipment under capital leases is stated at the present value of minimum lease payments. Property, plant and equipment are summarized as follows:

| December 31, 2012 | March 31, 2012 | Useful Life | ||||||||

| Production equipment and tooling | $ | 67,433 | $ | 60,144 | 3-10 years | |||||

| Building and leasehold improvements | 35,601 | 26,390 | 39 to 45 years or lesser of useful life or remaining term of lease | |||||||

| Furniture and equipment | 17,237 | 15,890 | 3-10 years | |||||||

| Construction-in-progress | 5,224 | 12,943 | ||||||||

| Total | 125,495 | 115,367 | ||||||||

| Less: accumulated depreciation and amortization | (60,213 | ) | (54,883 | ) | ||||||

| $ | 65,282 | $ | 60,484 | |||||||

Included in construction in progress at December 31, 2012 and March 31, 2012 was approximately $288 and $8,375, respectively, related to the construction of new facilities in France and China. Total depreciation expense was $2,334 and $2,267 for the three months ended December 31, 2012 and 2011, respectively. Total depreciation expense was $6,885 and $6,503 for the nine months ended December 31, 2012 and 2011, respectively. Property and equipment included $37 and $60 in capital leases at December 31, 2012 and March 31, 2012, respectively.

6. ACQUISITIONS, ACQUIRED INTANGIBLES AND ASSET HELD FOR SALE

Acquisitions: The Company continually evaluates potential acquisitions that either strategically fit with the Company’s existing portfolio or expand the Company’s portfolio into new and attractive business areas. The Company has completed a number of acquisitions that have been accounted for as purchases and have resulted in the recognition of goodwill in the Company’s financial statements. This goodwill arises because the purchase prices for these businesses reflect a number of factors, including the future earnings and cash flow potential of these businesses, and other factors at which similar businesses have been purchased by other acquirers, the competitive nature of the process by which the Company acquired the business, and the complementary strategic fit and resulting synergies these businesses bring to existing operations.

Goodwill balances presented in the consolidated condensed balance sheets of foreign acquisitions are translated at the exchange rate in effect at each balance sheet date; however, opening balance sheets used to calculate goodwill and acquired intangible assets are based on purchase date exchange rates, except for earn-out payments, which are recorded at the exchange rates in effect on the date the earn-out is accrued or adjusted. The following table shows the roll forward of goodwill reflected in the financial statements for the nine months ended December 31, 2012:

| 12 |

| Accumulated goodwill | $ | 147,808 | ||

| Accumulated impairment losses | (3,353 | ) | ||

| Balance March 31, 2012 | 144,455 | |||

| Attributable to 2012 acquisitions | 1,189 | |||

| Attributable to 2013 acquisitions | 8,843 | |||

| Effect of foreign currency translation | 125 | |||

| Balance December 31, 2012 | $ | 154,612 |

The following briefly describes the Company’s acquisitions since March 31, 2011.

Eureka: On July 8, 2011, the Company acquired certain assets of Eureka Environmental, Inc. (“Eureka”), a sensor company based in Austin, Texas, for $2,250. The transaction was funded from available cash on hand. Eureka manufactures a range of multi-probe pressure sensors mainly used for monitoring water quality. The water monitoring industry is large and a significant growth opportunity for the Company. The sellers have the potential to receive additional amounts in the form of a contingent payment based on certain earnings thresholds through calendar 2013, for which the Company initially recorded as part of purchase price the fair value estimate of $2,100. During the three months ended September 30, 2012, the Company determined that Eureka’s earnings were expected to be below initially estimated earn-out levels, as a result of changes in certain assumptions based on current economic and market conditions in the water monitoring industry. Accordingly, the Company recorded a fair value adjustment of $1,883, decreasing the acquisition earn-out liability to $309, and recognized the adjustment in the Consolidated Condensed Statements of Operations.

Celesco: On September 30, 2011, the Company completed the acquisition of all of the capital stock of Transducer Controls Corporation, a sensor company doing business as Celesco (“Celesco”) based in Chatsworth, California, for $37,375, including an estimated $2,375 in acquired cash. The purchase price was subsequently increased by $220 based on final calculations of established working capital levels. The transaction was funded from borrowings under the Company’s Senior Secured Credit Facility, as defined in Note 8 below. Celesco is a leading supplier to OEMs of a range of position sensors, including short and long stroke string pot, linear potentiometer and rotary sensors. In fiscal year 2013, the Company recorded certain adjustments to goodwill mainly related to income taxes to finalize purchase price allocation for the Celesco acquisition.

Gentech: On October 31, 2011, the Company completed the acquisition of all of the capital stock of Timesquest Limited, a holding company and the sole shareholder of Gentech International Limited (“Gentech”), for £6,500 or approximately $10,500, net of cash acquired, based on foreign currency exchange rates at the date of the acquisition. The transaction was funded from borrowings under the Company’s Senior Secured Credit Facility. Gentech is a level sensor and non-contact level switch company based in Ayrshire, Scotland. The seller can earn up to an additional £1,500 or approximately $2,400 if certain sales performance goals are achieved for the two year period ending December 31, 2013, for which the Company initially recorded as part of purchase price a fair value estimate of £1,387 or approximately $2,200 based on exchange rates at the date of acquisition. During the three months ended September 30, 2012, the Company determined that Gentech’s sales were expected to be below initially estimated earn-out levels as a result of changes in certain assumptions based on current sales trends. Accordingly, the Company recorded a fair value adjustment of £1,171 or approximately $1,892 (based on the weighted average exchange rate for the nine months ending December 31, 2012) decreasing the acquisition earn-out liability to £216 or approximately $317 at December 31, 2012, and recognized the adjustment in the Consolidated Condensed Statements of Operations. The acquisition of Gentech is expected to allow the Company to compete in the urea tank market with combined level and quality sensors. In fiscal year 2013, the Company recorded certain adjustments to goodwill mainly related to income taxes to finalize purchase price allocation for the Gentech acquisition.

| 13 |

Cosense: On April 2, 2012, the Company acquired the assets of Cosense, Inc. (“Cosense”), a Long Island, New York based manufacturer of ultrasonic sensors and switches used in semiconductor, medical, aerospace and industrial applications for $11,500. The Company paid $10,013 at close in cash from a combination of available cash on hand and from borrowings under the Company’s Senior Secured Credit Facility, and the Company will pay an additional $1,500 on April 2, 2013, subject to offset for certain indemnification rights. The acquisition of Cosense provides the Company with an ultrasonic sensor used for single-point, multi-point and continuous liquid level measurement, along with entrained bubble detection, which is considered an innovative solution complementary to the Company’s existing product offering, particularly within the high purity semiconductor, medical infusion pump and commercial aerospace markets. For the nine months ended December 31, 2012, approximately $5,533 in net sales, approximately $588 in net income and transaction related costs of approximately $24 related to Cosense were recorded as a component of selling, general and administrative expenses in the Company’s consolidated condensed financial statements. The purchase price allocation for the Cosense acquisition is subject to certain adjustments and will be finalized within the permitted measurement period. The Company’s preliminary purchase price allocation related to the Cosense acquisition is as follows:

| Assets: | ||||

| Inventory | $ | 470 | ||

| Plant and equipment | 30 | |||

| Acquired intangible assets | 7,155 | |||

| Goodwill | 3,831 | |||

| Total purchase price | 11,486 | |||

| Deferred acquisition payment | (1,473 | ) | ||

| Cash paid | $ | 10,013 |

RTD: On October 1, 2012, the Company acquired the assets of Resistance Temperature Detector Company, Inc. and its parent company, Cambridge Technologies, Inc. (collectively “RTD”), a designer and manufacturer of temperature sensors and probes based in Ham Lake, Minnesota. The Company paid $17,225 in cash at close from a combination of available cash on hand and from borrowings under the Company’s Senior Secured Credit Facility. The purchase price was subsequently increased by $58 based on final calculations of established working capital levels. The seller has the potential to receive up to $1,500 in additional consideration if certain sales targets are achieved during calendar 2013, for which the Company initially recorded as part of purchase price a fair value estimate of $1,200. The RTD acquisition is expected to provide both operational and strategic synergies in that RTD adds to the Company’s temperature portfolio with a presence in the motor/generator market, and services all of the major OEMs in that space, as well as custom temperature sensors for factory automation, medical and general industrial markets. For the nine months ended December 31, 2012, approximately $3,747 in net sales, approximately $470 in net income and transaction related costs of approximately $148 were recorded as a component of selling, general and administrative expenses related to RTD and were included in the Company’s consolidated condensed financial statements for the nine months ended December 31, 2012. The purchase price allocation for the RTD acquisition is subject to certain adjustments and will be finalized within the permitted measurement period. The Company’s preliminary purchase price allocation related to the RTD acquisition is as follows:

| Assets: | ||||

| Cash | $ | 50 | ||

| Accounts receivable | 2,456 | |||

| Inventory | 2,076 | |||

| Prepaid and other | 15 | |||

| Plant and equipment | 1,018 | |||

| Acquired intangible assets | 8,465 | |||

| Goodwill | 5,012 | |||

| Total purchase price | 19,092 | |||

| Accounts payable | (609 | ) | ||

| 18,483 | ||||

| Accrued earn-out contingency | (1,200 | ) | ||

| Cash paid | $ | 17,283 |

Asset held for sale: The Company completed the consolidation of the former PSI facility into the existing MEAS Hampton facility during the quarter ended June 30, 2011. The PSI facility is no longer utilized for manufacturing and is held for sale. Accordingly, the former PSI facility is classified as an asset held for sale in the consolidated condensed balance sheet, since it meets the held for sale criteria under the applicable accounting guidelines. Based on continued softening of the real-estate market in Hampton, Virginia, the Company re-assessed the market value of the asset held for sale and as a result, the Company recorded an impairment charge of $489 during the three months ended September 30, 2012 to write-down the asset to its estimated fair value. The carrying value of the former PSI facility is $940 as of December 31, 2012, and approximates fair value less cost to sell.

| 14 |

Acquired intangible assets: In connection with all acquisitions, the Company acquired certain identifiable intangible assets, including customer relationships, proprietary technology, patents, trade-names, order backlogs and covenants-not-to-compete. Additionally, the Company has purchased certain identifiable intangible assets as asset acquisitions.

Sentelligence: On August 31, 2011, the Company acquired a license to certain intellectual property rights related to fluid property sensors utilizing optical spectral technology for $1,717 through a 10 year license agreement with Sentelligence, Inc. The Company recorded the $1,717 payment as an acquired intangible asset subject to amortization over the life of the license agreement. Additionally, the license agreement includes annual royalty payments based on a percentage of net sales with certain annual minimum royalty requirements to maintain exclusive rights under the license agreement. As part of the cost of the intellectual property, the Company initially recorded $617 for the present value of the minimum royalty liability.

The gross amounts and accumulated amortization, along with the range of amortizable lives, are as follows:

| December 31, 2012 | March 31, 2012 | |||||||||||||||||||||||||

| Weighted- Average Life in years | Gross Amount | Accumulated Amortization | Net | Gross Amount | Accumulated Amortization | Net | ||||||||||||||||||||

| Amortizable intangible assets: | ||||||||||||||||||||||||||

| Customer relationships | 10 | $ | 69,782 | $ | (25,467 | ) | $ | 44,315 | $ | 58,735 | $ | (21,547 | ) | $ | 37,188 | |||||||||||

| Patents | 15 | 4,029 | (2,000 | ) | 2,029 | 4,058 | (1,781 | ) | 2,277 | |||||||||||||||||

| Tradenames | 2 | 2,640 | (2,576 | ) | 64 | 2,562 | (2,428 | ) | 134 | |||||||||||||||||

| In-process research & development | Indefinite | - | - | - | 230 | - | 230 | |||||||||||||||||||

| Backlog | 1 | 5,488 | (5,350 | ) | 138 | 4,910 | (4,910 | ) | - | |||||||||||||||||

| Covenants-not-to-compete | 3 | 1,326 | (1,123 | ) | 203 | 1,202 | (1,071 | ) | 131 | |||||||||||||||||

| Proprietary technology | 11 | 15,977 | (4,004 | ) | 11,973 | 12,469 | (3,051 | ) | 9,418 | |||||||||||||||||

| $ | 99,242 | $ | (40,520 | ) | $ | 58,722 | $ | 84,166 | $ | (34,788 | ) | $ | 49,378 | |||||||||||||

Amortization expense for acquired intangible assets for the three months ended December 31, 2012 and 2011 was $2,119 and $2,501, respectively, and amortization expense for the nine months ended December 31, 2012 and 2011 was $6,116 and $5,167, respectively. Annual amortization expense for the years ending December 31 is estimated as follows:

| Amortization | ||||

| Year | Expense | |||

| 2013 | $ | 7,313 | ||

| 2014 | 6,930 | |||

| 2015 | 6,850 | |||

| 2016 | 6,521 | |||

| 2017 | 6,385 | |||

| Thereafter | 24,723 | |||

| $ | 58,722 | |||

Pro forma Financial Data (Unaudited): The following represents the Company’s pro forma consolidated condensed income from continuing operations, net of income taxes, for the three and nine months ended December 31, 2012 and 2011, based on purchase accounting information assuming the Eureka, Celesco, Gentech, Cosense and RTD acquisitions occurred as of April 1, 2011, giving effect to purchase accounting adjustments. The pro forma data is for informational purposes only and may not necessarily reflect results of operations had the acquired companies been operated as part of the Company since April 1, 2011.

| 15 |

Three months ended December 31, | Nine months ended December 31, | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Net sales | $ | 81,628 | $ | 85,630 | $ | 264,908 | $ | 253,178 | ||||||||

| Net income | $ | 6,096 | $ | 7,064 | $ | 26,491 | $ | 24,876 | ||||||||

| Net income per share: | ||||||||||||||||

| Basic | $ | 0.40 | $ | 0.47 | $ | 1.73 | $ | 1.65 | ||||||||

| Diluted | $ | 0.38 | $ | 0.45 | $ | 1.64 | $ | 1.56 | ||||||||

7. FAIR VALUE MEASUREMENTS:

Accounting standards define fair value based on an exit price model, establish a framework for measuring fair value where the Company’s assets and liabilities are required to be carried at fair value and provide for certain disclosures related to the valuation methods used within a valuation hierarchy as established within the accounting standards. This hierarchy prioritizes the inputs into three broad levels as follows. Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities. Level 2 inputs are quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets in markets that are not active, or other observable characteristics for the asset or liability, including interest rates, yield curves and credit risks, or inputs that are derived principally from or corroborated by observable market data through correlation. Level 3 inputs are unobservable inputs based on the Company’s assumptions. A financial asset or liability’s classification within the hierarchy is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The Company's assessment of the significance of a particular input to the fair value measurement requires judgment, and may affect the valuation of fair value of assets and liabilities and their placement within the fair value hierarchy levels.

A summary of financial assets and liabilities that are measured at fair value on a recurring basis as of December 31, 2012 and March 31, 2012 are as follows:

Quoted prices in active | Significant other observable inputs (Level 2) | Significant unobservable inputs (Level 3) | Total | |||||||||||||

| December 31, 2012 | ||||||||||||||||

| Liabilities: | ||||||||||||||||

| Foreign currency exchange contracts | $ | - | $ | - | $ | - | $ | - | ||||||||

| Acquisition earn-out contingencies | - | - | 1,826 | 1,826 | ||||||||||||

| March 31, 2012 | ||||||||||||||||

| Assets: | ||||||||||||||||

| Foreign currency exchange contracts | $ | - | $ | 11 | $ | - | $ | 11 | ||||||||

| Liabilities: | ||||||||||||||||

| Acquisition earn-out contingencies | - | - | 4,317 | 4,317 | ||||||||||||

The table below provides a reconciliation of the fair value of the acquisition earn-out contingencies measured on a recurring basis for which the Company has designated as Level 3:

| Beginning April 1, 2012 | $ | 4,317 | ||

| Attributable to 2013 acquisitions | 1,200 | |||

| Changes in fair value | (3,775 | ) | ||

| Effect of foreign currency translation | 84 | |||

| Balance at December 31, 2012 | $ | 1,826 |

| 16 |

The foreign currency exchange contracts do not qualify for hedge accounting, and as a result, changes in the fair value of the currency swap are reflected in the accompanying consolidated condensed statements of operations. The fair value of the Company’s foreign currency contracts was based on Level 2 measurements in the fair value hierarchy. The fair value of the foreign currency contracts is based on forward exchange rates relative to current exchange rates which were obtained from independent financial institutions reflecting market quotes. The fair value of the acquisition earn-out contingencies is determined using a modeling technique based on significant unobservable inputs calculated using a probability-weighted income approach. Key assumptions include discount rates for present value factor of 16% for Eureka, 3.36% for Gentech and for 4.0% for RTD, which are based on industry specific weighted average cost of capital, adjusted for, among other things, time and risk, as well as forecasted annual earnings before interest, taxes, depreciation and amortization of $1,039 for Eureka and forecasted annual revenues of £10,800 for Gentech over the life of the earn-outs. The estimated fair value of acquisition earn-out contingencies could differ significantly from actual amounts. Adjustments to the fair value of earn-outs are recorded to earnings with that portion of the adjustment relating to the time value of money as interest expense and the non-interest portion of the change in earn-outs as a separate non-operating item in the statement of operations. During the three months ended September 30, 2012, as a result of the assessment of actual and projected earnings and sales scenarios, the Company determined that Eureka’s earnings and Gentech’s sales were expected to be below originally estimated earn-out levels. Accordingly, the Company recorded fair value adjustments of $1,883 and $1,892 decreasing the acquisition earn-out liabilities for Eureka and Gentech, respectively, and recognized the adjustments in the Consolidated Condensed Statements of Operations.

There were no transfers between Level 1, Level 2 and Level 3 of the fair value hierarchy during the nine months ended December 31, 2012.

Fair Value of Financial Instruments: In addition to the fair value disclosure requirements related to financial instruments carried at fair value, accounting standards require interim disclosures regarding the fair value of all of the Company’s financial instruments. The methods and significant assumptions used to estimate the fair value of financial instruments and any changes in methods or significant assumptions from prior periods are also required to be disclosed.

The fair values and carrying amounts of other financial instruments as of December 31, 2012 and March 31, 2012 are as follows:

| December 31, 2012 | March 31, 2012 | |||||||||||||||

| Carrying Amount | Fair Value | Carrying Amount | Fair Value | |||||||||||||

| Liabilities: | ||||||||||||||||

| Short-term borrowings and notes payable | $ | - | $ | - | $ | 1,867 | $ | 1,867 | ||||||||

| Captial leases | 37 | 37 | 60 | 60 | ||||||||||||

| Revolver | 86,000 | 86,000 | 80,251 | 80,251 | ||||||||||||

| Term debt | 20,736 | 20,736 | 20,834 | 20,834 | ||||||||||||

For promissory notes payable, capital lease obligations, and long-term debt, the fair value is determined as the present value of expected future cash flows discounted at the current interest rate, which approximates rates currently offered by lending institutions for loans of similar terms and comparable maturities to companies with comparable credit risk. These are considered Level 2 inputs. The fair value of the revolver approximates carrying value due to the variable interest nature of the debt. There were no changes in the methods or significant assumptions to estimate fair value of the Company’s financial instruments from prior periods.

Certain assets and liabilities are measured at fair value on a nonrecurring basis after initial recognition. That is, the assets and liabilities are not measured at fair value on an ongoing basis but are subject to fair value adjustments in certain circumstances, for example, when there is evidence of impairment. No circumstances were identified, including evidence of impairment, during the nine months ending December 31, 2012, except for the triggering event requiring an impairment analysis for asset held for sale for which the Company recorded an impairment charge of $489 during the three months ended September 30, 2012 to write-down an asset held for sale to its estimated fair value, less cost to sell. The fair value measurement of this asset was determined using relevant market data, which are classified as Level 2 inputs.

| 17 |

Derivative instruments and risk management: The Company is exposed to market risks from changes in interest rates, commodities, credit and foreign currency exchange rates, which could impact its results of operations and financial condition. The Company attempts to address its exposure to these risks through its normal operating and financing activities. In addition, the Company’s relatively broad-based business activities help to reduce the impact that volatility in any particular area or related areas may have on its operating results as a whole. Readers should refer to Note 7 in the Annual Report for the fiscal year ended March 31, 2012 for additional information related to the Company’s exposures to market risks for interest rates, commodities and credit.

Foreign currency exchange rate risk: Foreign currency exchange rate risk arises from the Company’s investments in subsidiaries owned and operated in foreign countries, as well as from transactions with customers in countries outside the U.S. and transactions denominated in currencies other than the applicable functional currency.

The effect of a change in currency exchange rates on the Company’s net investment in international subsidiaries is reflected in the “accumulated other comprehensive income” component of shareholders’ equity. The Company does not hedge the Company’s net investment in subsidiaries owned and operated in countries outside the U.S.

Although the Company has a U.S. dollar functional currency for reporting purposes, it has manufacturing and operating sites throughout the world and a large portion of its sales are generated in foreign currencies. A substantial portion of the Company’s revenue is priced in U.S. dollars, and most of its costs and expenses are priced in U.S. dollars, with the remaining priced in Chinese RMB, Euros, Swiss francs and British pounds. Sales by subsidiaries operating outside of the United States are translated into U.S. dollars using exchange rates effective during the respective period. As a result, the Company is exposed to movements in the exchange rates of various currencies against the U.S. dollar. Accordingly, the competitiveness of its products relative to products produced locally (in foreign markets) may be affected by the performance of the U.S. dollar compared with that of our foreign customers’ currencies. Refer to Note 10, Segment Information, for details concerning net sales invoiced from our facilities within the U.S. and outside of the U.S., as well as long-lived assets. Therefore, both positive and negative movements in currency exchange rates against the U.S. dollar will continue to affect the reported amount of sales, profit, and assets and liabilities in the Company’s consolidated condensed financial statements.

During the nine months ended December 31, 2012, the RMB did not fluctuate significantly relative to the U.S. dollar. The RMB appreciated approximately 3.6% and 4.0%, respectively, relative to the U.S. dollar during fiscal 2012 and 2011. The Chinese government no longer pegs the RMB to the U.S. dollar, but established a currency policy letting the RMB trade in a narrow band against a basket of currencies. The Company has more expenses in RMB than sales (i.e., short RMB position), and as such, if the U.S. dollar weakens relative to the RMB, our operating profits will decrease. We continue to consider various alternatives to hedge this exposure, and we are attempting to manage this exposure through, among other things, forward purchase contracts, pricing and monitoring balance sheet exposures for payables and receivables.

Fluctuations in the value of the Hong Kong dollar have not been significant since October 17, 1983, when the Hong Kong government tied the value of the Hong Kong dollar to that of the U.S. dollar. However, there can be no assurance that the value of the Hong Kong dollar will continue to be tied to that of the U.S. dollar.

The Company’s French, Irish and German subsidiaries have more sales in Euros than expenses in Euros and the Company’s Swiss subsidiary has more expenses in Swiss francs than sales in Swiss francs, and as such, if the U.S. dollar weakens relative to the Euro and Swiss franc, our operating profits increase in France, Ireland and Germany, but decrease in Switzerland. The Company’s British subsidiary has more expenses in British pounds than sales in British pounds, and as such, if the U.S. dollar weakens relative to the British pound, our operating profits decrease in the United Kingdom.

| 18 |

The Company has a number of foreign currency exchange contracts in Asia for the purposes of hedging the Company’s short-position exposure to the RMB. At December 31, 2012, the Company has a number of RMB/U.S. dollar currency contracts with notional amounts totaling $13,600 and exercise dates through December 31, 2013 at average exchange rates of 0.1577 (RMB to U.S. dollar conversion rate). With the RMB/U.S. dollar contracts, for every 10 percent depreciation of the RMB, the Company would be exposed to approximately $1,360 in additional foreign currency exchange losses. Since these derivatives are not designated as hedges for accounting purposes, changes in their fair value are recorded in results of operations, not in other comprehensive income. To manage our exposure to potential foreign currency transaction and translation risks, we may purchase additional foreign currency exchange forward contracts, currency options, or other derivative instruments, provided such instruments may be obtained at suitable prices.

Fair values of derivative instruments not designated as hedging instruments are as follows:

| December 31, | March 31, | |||||||||

| Financial position: | 2012 | 2012 | Location | |||||||

| Foreign currency contracts - RMB | $ | - | $ | 11 | Other assets (liabilities) | |||||

The effect of derivative instruments not designated as hedging instruments on the statements of operations and cash flows for the three and nine months ended December 31, 2012 and 2011 is as follows:

| Three months ended December 31, | Nine months ended December 31, | |||||||||||||||||

| Results of operations: | 2012 | 2011 | 2012 | 2011 | Location | |||||||||||||

| Foreign currency contracts - RMB | $ | (217 | ) | $ | 8 | $ | (4 | ) | $ | (149 | ) | Foreign currency exchange (gain) loss | ||||||

| Foreign currency exchange contracts - Japanese yen | - | 1 | - | - | ||||||||||||||

| Total | $ | (217 | ) | $ | 9 | $ | (4 | ) | $ | (149 | ) | |||||||

| Nine months ended December 31, | ||||||||||

| Cash flows from operating activities: Source (Use) | 2012 | 2011 | Location | |||||||

| Foreign currency exchange contracts - RMB | $ | 15 | $ | 277 | Prepaid expenses (Accrued expenses) | |||||

| Total | $ | 15 | $ | 277 | ||||||

8. LONG-TERM DEBT:

Long-term debt and revolver: The Company entered into a Credit Agreement (the "Senior Secured Credit Facility") dated June 1, 2010, among JPMorgan Chase Bank, N.A., as administrative agent and collateral agent (in such capacity, the "Senior Secured Facility Agents"), Bank America, N.A., as syndication agent, HSBC Bank USA, N.A., as document agent, and certain other parties thereto (the "Credit Agreement") to refinance the Amended and Restated Credit Agreement effective as of April 1, 2006 among the Company, General Electric Capital Corporation (“GE”), as agent and a lender, and certain other parties thereto and to provide for the working capital needs of the Company including to effect permitted acquisitions.

The Senior Secured Credit Facility, as amended, consists of a $110,000 revolving credit facility (the "Revolving Credit Facility") with a $75,000 accordion feature enabling expansion of the Revolving Credit Facility to $185,000. The Revolving Credit Facility has a variable interest rate based on the LIBOR, EURIBOR or the ABR Rate (prime based rate) with applicable margins ranging from 1.25% to 2.00% for LIBOR and EURIBOR based loans or 0.25% to 1.00% for ABR Rate loans. The applicable margins may be adjusted quarterly based on a change in the leverage ratio of the Company. The Senior Secured Credit Facility also includes the ability to borrow in currencies other than U.S. dollars, such as the Euro and Swiss Franc, up to $66,000. Commitment fees on the unused balance of the Revolving Credit Facility range from 0.25% to 0.375% per annum of the average amount of unused balances. The Revolving Credit Facility will expire on November 8, 2016 and all balances outstanding under the Revolving Credit Facility will be due on such date. The Company has provided a security interest in substantially all of the Company's U.S. based assets as collateral for the Senior Secured Credit Facility and private placement of credit facilities entered into by the Company from time to time not to exceed $50,000, including the Prudential Shelf Facility (as defined below). The Senior Secured Credit Facility includes an inter-creditor arrangement with Prudential and is on a pari passu (equal force) basis with the Prudential Shelf Facility.

| 19 |

The Senior Secured Credit Facility, as amended, includes specific financial covenants for maximum leverage ratio and minimum fixed charge coverage ratio, as well as customary representations, warranties, covenants and events of default for a transaction of this type. Consolidated earnings before interest, taxes, depreciation and amortization (“EBITDA”) for debt covenant purposes is the Company's consolidated net income determined in accordance with GAAP minus the sum of income tax credits, interest income, gain from extraordinary items for such period, any non-cash gains, and gains due to fluctuations in currency exchange rates, plus the sum of any provision for income taxes, interest expense, loss from extraordinary items, any aggregate net loss during such period arising from the disposition of capital assets, the amount of non-cash charges for such period, amortized debt discount for such period, losses due to fluctuations in currency exchange rates and the amount of any deduction to consolidated net income as the result of any grant to any members of the management of the Company of any equity interests. The Company's leverage ratio consists of total debt less unrestricted cash maintained in U.S. bank accounts which are subject to control agreements in favor of JPMorgan Chase Bank, N.A., as Collateral Agent, to Consolidated EBITDA. Adjusted fixed charge coverage ratio is Covenant EBITDA less capital expenditures for the last twelve months, excluding capital expenditures for the last twelve months in connection with the facilities being constructed in France in an aggregate amount up to $11,000 through March 31, 2013 and China in an aggregate amount up to $6,000 through March 31, 2016, divided by fixed charges. Fixed charges are the last twelve months of scheduled principal payments, taxes paid in cash and consolidated interest expense. All of the aforementioned financial covenants are subject to various adjustments, many of which are detailed in the Credit Agreement.

As of December 31, 2012, the Company utilized the LIBOR based rate for $86,000 of the Revolving Credit Facility. The weighted average interest rate applicable to borrowings under the Revolving Credit Facility was approximately 1.8% at December 31, 2012. As of December 31, 2012, the outstanding borrowings on the Revolving Credit Facility, which is classified as non-current, were $86,000. The Company’s borrowing capacity is limited by financial covenant ratios, including earnings ratios, and as such, our borrowing capacity is subject to change. At December 31, 2012, the Company could have borrowed an additional $24,000 under the Revolving Credit Facility.

On June 1, 2010, the Company entered into a Master Shelf Agreement (the "Prudential Shelf Facility") with Prudential Investment Management, Inc. ("Prudential") whereby Prudential agreed to purchase up to $50,000 of senior secured notes (the "Senior Secured Notes") issued by the Company. Prudential purchased two Senior Secured Notes each for $10,000 and the remaining $30,000 of such Senior Secured Notes may be purchased at the discretion of Prudential or one or more of its affiliates upon the request of the Company. The Prudential Shelf Facility has a fixed interest rate of 5.70% and 6.15% for each of the two $10,000 Senior Secured Notes issued by the Company and the Senior Secured Notes issued thereunder are due on June 1, 2015 and 2017, respectively. The Prudential Shelf Facility includes specific financial covenants for maximum total leverage ratio and minimum fixed charge coverage ratio consistent with the Senior Secured Credit Facility, as well as customary representations, warranties, covenants and events of default. The Prudential Shelf Facility includes an inter-creditor arrangement with the Senior Secured Facility Agents and is on a pari passu (equal force) basis with the Senior Secured Facility.

The Company was in compliance with its debt covenants at December 31, 2012.

Deferred financing costs: Amortization of deferred financing costs totaled $70 and $79 for the three months ended December 31, 2012 and 2011, respectively, and for the nine months ended December 31, 2012 and 2011, amortization of deferred financing costs totaled $210 and $269, respectively. Annual amortization expense of deferred financing costs associated with the refinancing is estimated to be approximately $280.

China credit facility: On November 3, 2009, the Company’s subsidiary in China (“MEAS China”) entered into a two year credit facility agreement (the “China Credit Facility”) with China Merchants Bank Co., Ltd (“CMB”). On December 23, 2011, MEAS China renewed the China Credit Facility and extended the expiration to November 25, 2013. The China Credit Facility permits MEAS China to borrow up to RMB 68,000 (approximately $10,700). Specific covenants include customary limitations, compliance with laws and regulations, use of proceeds for operational purposes, and timely payment of interest and principal. MEAS China has pledged its Shenzhen facility to CMB as collateral. The interest rate will be based on the London Inter-bank Offered Rate (“LIBOR”) plus a LIBOR spread, depending on the term of the loan when drawn. The purpose of the China Credit Facility is primarily to provide additional flexibility in funding operations of MEAS China. At December 31, 2012, MEAS China had not borrowed any amounts under the China Credit Facility.

| 20 |

European credit facility: On July 21, 2010, the Company’s subsidiary in France (“MEAS Europe”) entered into a five year credit facility agreement (the “European Credit Facility”) with La Societe Bordelaise de Credit Industriel et Commercial (“CIC”). The European Credit Facility permits MEAS Europe to borrow up to €2,000 (approximately $2,600). Specific covenants include certain financial covenants for maximum leverage ratio and net debt to equity ratio, as well as customary limitations, compliance with laws and regulations, use of proceeds, and timely payment of interest and principal. MEAS Europe has pledged its Les Clayes-sous-Bois, France facility to CIC as collateral. The interest rate is based on the EURIBOR interest rate plus a spread of 1.8%. The EURIBOR interest rate will vary depending on the term of the loan when drawn. The purpose of the European Credit Facility is primarily to provide additional flexibility in funding operations of MEAS Europe. At December 31, 2012, MEAS Europe had not borrowed any amounts under the European Credit Facility.

Long-term debt and promissory notes: Below is a summary of the long-term debt and promissory notes outstanding at December 31, 2012 and March 31, 2012:

| December 31, | March 31, | |||||||

| 2012 | 2012 | |||||||

| Term notes at 5.70% due in full on June 1, 2015 | $ | 10,000 | $ | 10,000 | ||||

| Term notes at 6.15% due in full on June 1, 2017 | 10,000 | 10,000 | ||||||

| Governmental loans from French agencies at no interest and payable based on R&D expenditures | 736 | 834 | ||||||

| 20,736 | 20,834 | |||||||

| Less current portion of long-term debt | 198 | 123 | ||||||

| $ | 20,538 | $ | 20,711 | |||||

The annual principal payments of long-term debt, promissory notes and revolver as of December 31, 2012 are as follows:

| Years ending December 31, | Term | Other | Subtotal | Revolver | Total | |||||||||||||||

| 2013 | $ | - | $ | 198 | $ | 198 | $ | - | $ | 198 | ||||||||||

| 2014 | - | 132 | 132 | - | 132 | |||||||||||||||

| 2015 | 10,000 | - | 10,000 | - | 10,000 | |||||||||||||||

| 2016 | - | - | - | 86,000 | 86,000 | |||||||||||||||

| 2017 | 10,000 | 406 | 10,406 | - | 10,406 | |||||||||||||||

| Total | $ | 20,000 | $ | 736 | $ | 20,736 | $ | 86,000 | $ | 106,736 | ||||||||||

9. COMMITMENTS AND CONTINGENCIES:

Litigation:

Pending Legal Matters

There are currently no material pending legal proceedings. From time to time, the Company is subject to legal proceedings and claims in the ordinary course of business. The Company currently is not aware of any such legal proceedings or claims that the Company believes will have, individually or in the aggregate, a material adverse effect on the Company’s business, financial condition, or operating results.

| 21 |

Contingency: Exports of technology necessary to develop and manufacture certain of the Company’s products are subject to U.S. export control laws and similar laws of other jurisdictions, and the Company may be subject to adverse regulatory consequences, including government oversight of facilities and export transactions, monetary penalties and other sanctions for violations of these laws. In certain instances, these export control regulations may prohibit the Company from developing or manufacturing certain of its products for specific end applications outside the United States. In late May 2009, the Company became aware that certain of its piezo products when designed or modified for use with or incorporation into a defense article are subject the International Traffic in Arms Regulations ("ITAR") administered by the United States Department of State. Certain technical data relating to the design of the products may have been exported to China without authorization from the U.S. Department of State. As required by the ITAR, the Company conducted a thorough investigation into the matter. Based on the investigation, the Company filed in December 2009 a final voluntary disclosure with the U.S. Department of State relating to that matter, as well as to exports and re-exports of other ITAR-controlled technical data and/or products to Canada, India, Ireland, France, Germany, Italy, Israel, Japan, the Netherlands, South Korea, Spain and the United Kingdom, which disclosure has since been supplemented. In the course of the investigation, the Company also became aware that certain of its products may have been exported from France without authorization from the relevant French authorities. The Company investigated this matter thoroughly. In December 2009, it also voluntarily submitted to French customs authorities a list of products that may have required prior export authorization, which has since been supplemented to exclude certain products. The French authorities have confirmed no fine or penalty associated with the French export issues will be imposed because the French authorities consider the matter closed and the period of time for enforcement under French stature of limitations expired in December 2012. In addition, the Company has taken steps to mitigate the impact of potential violations, and we are in the process of strengthening our export-related controls and procedures. The U.S. Department of State and other regulatory authorities encourage voluntary disclosures and generally afford parties mitigating credit for submitting such voluntary disclosures. The Company nevertheless could be subject to potential regulatory consequences related to these possible violations ranging from a no-action letter, government oversight of facilities and export transactions, monetary penalties, and in extreme cases, debarment from government contracting, denial of export privileges and/or criminal penalties. It is not possible at this time to predict the precise timing or probable outcome of any potential regulatory consequences related to these possible violations. Moreover, due to the unpredictable nature of the probable outcome of these voluntary proceedings, the Company cannot make a reasonable estimate of the possible loss or range of losses at this time. The Company has incurred cumulatively through December 31, 2012 approximately $575 in legal fees associated with the French customs and ITAR matters.

Acquisition Earn-Outs: The Company has an earnings based earn-out in connection with the Eureka acquisition, for which the Company initially recorded an estimated fair value of $2,100 on July 8, 2011. The Company has a sales based earn-out in connection with the Gentech acquisition, for which the Company initially recorded a fair value estimate of £1,387 or approximately $2,200, based on exchange rates at the date of acquisition. The Company has a sales based earn-out in connection with the RTD acquisition, for which the Company initially recorded a fair value estimate of $1,200. During the three months ended September 30, 2012, the Company determined that Eureka’s earnings and Gentech’s sales were expected to be below initially estimated earn-out levels. Accordingly, the Company recorded fair value adjustments of $1,883 and £1,171 or approximately $1,892 (based on the weighted average exchange rate for the nine months ending December 31, 2012) decreasing the acquisition earn-out liabilities for Eureka and Gentech, respectively. At December 31, 2012, the acquisition earn-out liabilities for Eureka, Gentech and RTD totaled $309, £216 or approximately $317, and $1,200, respectively.

10. SEGMENT INFORMATION:

The Company continues to have one reporting segment, a sensor business, under applicable accounting guidelines for segment reporting. For a description of the products and services of the Sensor business, see Note 1. Management continually assesses the Company’s operating structure, and this structure could be modified further based on future circumstances and business conditions.

| 22 |

Geographic information for revenues based on country from which invoiced and long-lived assets based on country of location, which includes property, plant and equipment, but excludes intangible assets and goodwill, net of related depreciation and amortization follows:

| Three months ended December 31, | Nine months ended December 31, | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Net Sales: | ||||||||||||||||

| United States | $ | 32,339 | $ | 26,734 | $ | 98,300 | $ | 79,699 | ||||||||

| France | 14,357 | 13,023 | 45,663 | 39,606 | ||||||||||||

| Germany | 3,338 | 4,246 | 10,870 | 15,242 | ||||||||||||

| Ireland | 6,375 | 6,219 | 20,964 | 21,581 | ||||||||||||

| Switzerland | 3,982 | 4,971 | 12,128 | 13,420 | ||||||||||||

| Scotland | 2,751 | 2,459 | 9,556 | 2,459 | ||||||||||||

| China | 18,486 | 18,689 | 60,525 | 54,761 | ||||||||||||

| Total: | $ | 81,628 | $ | 76,341 | $ | 258,006 | $ | 226,768 | ||||||||

| December 31, 2012 | March 31, 2012 | |||||||

| Long Lived Assets: | ||||||||

| United States | $ | 9,179 | $ | 7,375 | ||||

| France | 18,688 | 16,962 | ||||||

| Germany | 3,114 | 3,294 | ||||||

| Ireland | 3,055 | 3,216 | ||||||

| Switzerland | 3,082 | 2,928 | ||||||

| Scotland | 379 | 323 | ||||||

| China | 27,785 | 26,386 | ||||||

| Total: | $ | 65,282 | $ | 60,484 | ||||

11. SUBSEQUENT EVENT:

On February 1, 2013, the Company entered into Amendment No. 4 to the Credit Agreement (the “Credit Agreement Amendment”) among the Company, the financial institutions party thereto and JPMorgan Chase Bank, N.A., as administrative agent to amend the Company’s senior secured facility (the “Senior Secured Facility”) under that certain Credit Agreement dated as of June 1, 2010, among the Company, the lenders party thereto from time to time, and JPMorgan Chase Bank, N.A., as administrative agent. The Credit Agreement Amendment increased the aggregate commitment to $185,000 from $110,000, reset the accordion feature to $75,000 for future expansion and added PNC Bank to the group of lenders.

On February 1, 2013, the Company entered into a Fourth Amendment to Note Purchase Agreement (the “Prudential Amendment”) among Prudential Insurance Company of America (“Prudential”) other note-holders party thereto, the Company, and certain subsidiaries of the Company party thereto to amend that certain Note Purchase and Private Shelf Agreement dated June 1, 2010, among the Company, Prudential and other note-holders party thereto (the “Note Purchase Agreement”). The Prudential Amendment amended the Note Purchase Agreement to provided conformity with the Credit Agreement Amendment since the Prudential Shelf Agreement is on a pari passu (equal force) basis with the Senior Secured Facility.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

(Amounts in thousands, except per share data)

| 23 |

Information Relating To Forward-Looking Statements