UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2013

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________ to ________

Commission File Number: 1-11373

Cardinal Health, Inc.

(Exact name of registrant as specified in its charter)

Ohio | 31-0958666 |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

7000 Cardinal Place, Dublin, Ohio | 43017 |

(Address of principal executive offices) | (Zip Code) |

(614) 757-5000 | |

(Registrant’s telephone number, including area code) | |

Securities registered pursuant to Section 12(b) of the Act: | |

Title of class | Name of each exchange on which registered |

Common shares (without par value) | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o |

Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of voting stock held by non-affiliates of the registrant on December 31, 2012, based on the closing price on December 31, 2012, was $13,998,206,699.

The number of the registrant’s common shares, without par value, outstanding as of August 9, 2013, was the following: 339,461,413.

Documents Incorporated by Reference:

Portions of the registrant’s Definitive Proxy Statement to be filed for its 2013 Annual Meeting of Shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K.

Cardinal Health, Inc. and Subsidiaries | ||

Table of Contents | ||

Item | Page | |

1 | ||

1A | ||

1B | ||

2 | ||

3 | ||

4 | ||

5 | ||

6 | ||

7 | ||

7A | ||

8 | ||

9 | ||

9A | ||

9B | ||

10 | ||

11 | ||

12 | ||

13 | ||

14 | ||

15 | ||

Cardinal Health, Inc. and Subsidiaries | ||

Important Information Regarding Forward-Looking Statements

This Form 10-K (including information incorporated by reference) includes forward-looking statements, addressing expectations, prospects, estimates and other matters that are dependent upon future events or developments. Many forward-looking statements appear in “Item 7: Management’s Discussion and Analysis of Financial Condition and Results of Operations,” but there are others throughout this document, which may be identified by words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “will,” “should,” “could,” “would,” “project,” “continue,” “likely,” and similar expressions, and include statements reflecting future

results or guidance, statements of outlook and expense accruals. These matters are subject to risks and uncertainties that could cause actual results to differ materially from those projected, anticipated or implied. The most significant of these risks and uncertainties are described below in “Item 1A: Risk Factors” and in Exhibit 99.1 to this Form 10-K. Forward-looking statements in this document speak only as of the date of this document. Except to the extent required by applicable law, we undertake no obligation to update or revise any forward-looking statement.

1

Cardinal Health, Inc. and Subsidiaries | ||

Part I | ||

Item 1: Business

General

Cardinal Health, Inc. is an Ohio corporation formed in 1979. As used in this report, “we,” “our,” “us” and similar pronouns refer to Cardinal Health, Inc. and its subsidiaries, unless the context requires otherwise. We are a healthcare services company providing pharmaceutical and medical products and services that help pharmacies, hospitals, ambulatory surgery centers, clinical laboratories, physician offices and other healthcare providers focus on patient care while reducing costs, enhancing efficiency and improving quality. We also provide medical products to patients in the home.

Our fiscal year ends on June 30. References to fiscal 2013, 2012 and 2011 are to the fiscal years ended June 30, 2013, 2012 and 2011, respectively. Except as otherwise specified, information in this Form 10-K is provided as of June 30, 2013.

Pharmaceutical Segment

In the United States, including Puerto Rico, the Pharmaceutical segment:

• | distributes branded and generic pharmaceutical, over-the-counter healthcare and consumer products through its Pharmaceutical Distribution division to retailers (including chain and independent drug stores and pharmacy departments of supermarkets and mass merchandisers), hospitals and other healthcare providers. This division: |

• | maintains prime vendor relationships that streamline the purchasing process resulting in greater efficiency and lower costs for our customers; |

• | renders services to pharmaceutical manufacturers including distribution, inventory management, data reporting, new product launch support, and contract pricing and chargeback administration; |

• | franchises retail pharmacies under the Medicine Shoppe® and Medicap® brands; and |

• | provides pharmacy services to hospitals and other healthcare facilities; |

• | operates nuclear pharmacies and cyclotron facilities through its Nuclear Pharmacy Services division that manufacture, prepare and deliver radiopharmaceuticals for use in nuclear imaging and other procedures in hospitals and physician offices; and |

• | distributes specialty pharmaceutical products, provides services to pharmaceutical manufacturers, third-party payors and healthcare providers supporting the marketing, distribution and payment for specialty pharmaceutical products, and operates a specialty pharmacy through its Specialty Solutions division. |

In China, the Pharmaceutical segment distributes branded, generic and specialty pharmaceuticals, over-the-counter and consumer products as well as provides logistics, marketing and other services and operates specialty pharmacies through Cardinal Health China.

Pharmaceutical Distribution

Our Pharmaceutical Distribution division generates gross margin when the aggregate selling price to our customers exceeds the aggregate cost

of products sold, net of cash discounts. Gross margin includes margin from our generic pharmaceutical programs and margin from branded pharmaceutical agreements. Margin from our generic pharmaceutical programs includes price discounts and rebates and may include price appreciation on some products. Our earnings on generic pharmaceuticals are generally highest during the period immediately following the initial launch of a generic product because generic pharmaceutical selling prices are generally highest during that period and tend to decline over time, although this may vary. Margin from branded pharmaceutical agreements refers primarily to fees we receive for rendering a range of distribution and related services to manufacturers and also includes benefits from pharmaceutical price appreciation.

Bulk and Non-Bulk Sales

The Pharmaceutical segment historically has differentiated between bulk and non-bulk sales based on the nature of our customers’ operations when presenting information on the segment's operations. The table below shows the Pharmaceutical segment's revenue, segment expenses, segment profit and segment profit as a percentage of revenue for bulk and non-bulk sales:

(in millions) | 2013 | 2012 | 2011 | ||||||||

Non-bulk sales: | |||||||||||

Revenue from non-bulk sales | $ | 61,309 | $ | 57,738 | $ | 51,816 | |||||

Segment expenses allocated to non-bulk sales (1) | 59,693 | 56,334 | 50,622 | ||||||||

Segment profit from non-bulk sales (1) | $ | 1,616 | $ | 1,404 | $ | 1,194 | |||||

Segment profit from non-bulk sales as a percentage of revenue from non-bulk sales (1) | 2.64 | % | 2.43 | % | 2.31 | % | |||||

Bulk sales: | |||||||||||

Revenue from bulk sales | $ | 29,788 | $ | 40,187 | $ | 41,928 | |||||

Segment expenses allocated to bulk sales (1) | 29,670 | 40,033 | 41,793 | ||||||||

Segment profit from bulk sales (1) | $ | 118 | $ | 154 | $ | 135 | |||||

Segment profit from bulk sales as a percentage of revenue from bulk sales (1) | 0.40 | % | 0.38 | % | 0.32 | % | |||||

(1) | Segment expenses and profit required complex and subjective estimates and allocations based upon assumptions, past experience and judgment that we believe were reasonable. |

Bulk sales consisted of sales to retail chain customers’ centralized warehouse operations and customers’ mail order businesses in the United States. All other sales were classified as non-bulk. Sales to a retail chain pharmacy customer were classified as bulk sales with respect to its warehouse operations and non-bulk sales with respect to its retail stores.

Substantially all bulk sales consisted of products shipped in the same form that we received them from the manufacturer; a small portion of bulk sales were broken down into smaller units prior to shipping. In contrast, non-bulk sales required more complex servicing. For non-bulk sales, we may have received inventory in large or full case quantities and broken it down into smaller quantities, warehoused the product for a longer period of time, picked individual products specific to a customer’s order and delivered that smaller order to a customer location.

Bulk sales generated significantly lower segment profit as a percentage of revenue than non-bulk sales. Customers received lower pricing on bulk sales of the same products than non-bulk sales, as bulk sales required fewer services to be provided to these customers, and hence, less costs were incurred by us in providing these products. In addition, bulk sales in the aggregate generated higher segment cost of products sold as a percentage of revenue than non-bulk sales due to the mix of products sold

2

Cardinal Health, Inc. and Subsidiaries | ||

within the bulk category. Segment distribution, selling, general and administrative expenses as a percentage of revenue from bulk sales were substantially lower than from non-bulk sales because bulk sales required substantially fewer services to be rendered by us than non-bulk sales.

In light of the reduction in bulk sales after the expiration of our pharmaceutical distribution contract with Walgreen Co. ("Walgreens"), we do not expect the distinction between revenue and profit from bulk sales to be meaningful in the future. As such, in the future, we do not expect to present separate information on bulk and non-bulk sales to investors.

Specialty Pharmaceutical Products and Services

We refer to products and services offered by our Specialty Solutions division as “specialty pharmaceutical products and services.” The Specialty Solutions division currently (1) distributes oncology, rheumatology, urology and other pharmaceutical products ("specialty pharmaceutical products") to physician offices; (2) distributes human plasma products and some specialty pharmaceutical products to hospitals and other healthcare providers; (3) provides various consulting and other services to pharmaceutical manufacturers, third-party payors and healthcare providers primarily supporting the marketing, distribution and payment for specialty pharmaceutical products; and (4) operates a specialty pharmacy. Our use of the terminology "specialty pharmaceutical products and services" may not be comparable to the use of that terminology by other industry participants.

Pharmaceutical Segment Financial Statements

See Note 14 of the “Notes to Consolidated Financial Statements” for Pharmaceutical segment revenue, profit and assets for fiscal 2013, 2012 and 2011.

Medical Segment

The Medical segment distributes a broad range of medical, surgical and laboratory products to hospitals, ambulatory surgery centers, clinical laboratories, physician offices and other healthcare providers in the United States, Canada and China and to patients in the home in the United States. This segment also manufactures, sources and develops its own line of private brand medical and surgical products. Manufactured products include: single-use surgical drapes, gowns and apparel; exam and surgical gloves; and fluid suction and collection systems. The segment also assembles and offers sterile and non-sterile procedure kits. Our manufactured products are sold directly or through third-party distributors in the United States, Canada, Europe, South America and the Asia/Pacific region. In addition, the segment provides supply chain services, including spend management, distribution management and inventory management services, to healthcare providers.

Medical Segment Financial Statements

See Note 14 of the “Notes to Consolidated Financial Statements” for Medical segment revenue, profit and assets for fiscal 2013, 2012 and 2011.

Acquisitions and Divestitures

In the past five fiscal years, we completed the following four acquisitions:

Date | Company | Location | Line of Business | Acquisition Price (in millions) | |||||||

Mar 18, 2013 | AssuraMed, Inc. ("AssuraMed") | Twinsburg, Ohio | Medical products distribution | $ | 2,070 | ||||||

Dec 21, 2010 | Kinray, Inc. | Whitestone, New York | Pharmaceutical, generic, health and beauty, and home health care products distribution | $ | 1,336 | ||||||

Nov 29, 2010 | Cardinal Health China | Shanghai, China | Pharmaceutical and medical products distribution | $ | 458 | (1) | |||||

Jul 15, 2010 | Healthcare Solutions Holding, LLC ("P4 Healthcare") | Ellicott City, Maryland | Specialty pharmaceutical services | $ | 520 | (2) | |||||

(1) | Includes the assumption of approximately $57 million in debt. |

(2) | Includes $506 million in cash paid on the acquisition date and $14 million paid in fiscal 2012 and 2013 in connection with the contingent consideration obligation. The contingent consideration obligation had an acquisition date fair value of $92 million. |

In addition, we completed several smaller acquisitions during the last five fiscal years, including purchasing Borschow Hospital & Medical Supplies, Inc. in fiscal 2009 and Futuremed Healthcare Products Corporation in fiscal 2012.

During the past five fiscal years, we also completed several divestitures, including selling our United Kingdom-based Martindale injectable manufacturing business in fiscal 2010. In addition, effective August 31, 2009, we separated our clinical and medical products businesses through a distribution to our shareholders of 81 percent of the then outstanding common stock of CareFusion Corporation ("CareFusion") and retained the remaining shares of CareFusion common stock (the "CareFusion Spin-Off"). During fiscal 2010 and 2011, we disposed of the remaining shares of CareFusion common stock.

Customers

Our largest customers, CVS Caremark Corporation (“CVS”) and Walgreens accounted for approximately 23 percent and 20 percent, respectively, of our fiscal 2013 revenue. In the aggregate, our five largest customers, including CVS and Walgreens, accounted for approximately 52 percent of our fiscal 2013 revenue. In March 2013, we announced that our pharmaceutical distribution contract with Walgreens, which expires at the end of August 2013, would not be renewed. Our pharmaceutical distribution contract with Express Scripts, Inc. ("Express Scripts"), which was our third largest customer in fiscal 2012, expired in September 2012.

In addition, we have agreements with group purchasing organizations (“GPOs”) that act as agents to negotiate vendor contracts on behalf of their members. Our two largest GPO relationships in terms of member revenue are with Novation, LLC and Premier Purchasing Partners, L.P. Sales to members of these two GPOs collectively accounted for 13 percent of our revenue in fiscal 2013.

3

Cardinal Health, Inc. and Subsidiaries | ||

Suppliers

We rely on many different suppliers. Products obtained from our five largest suppliers accounted for an aggregate of approximately 25 percent of our revenue during fiscal 2013, but no single supplier’s products accounted for more than 6 percent of that revenue. Overall, we believe our relationships with our suppliers are good.

The Pharmaceutical Distribution division is a party to distribution service agreements with pharmaceutical manufacturers. These agreements generally have terms ranging from one year, with an automatic renewal feature, to five years. Generally, these agreements are terminable before they expire only if the parties mutually agree, if there is an uncured breach of the agreement, or if one party is the subject of a bankruptcy filing or similar insolvency event. Some agreements allow the manufacturer to terminate the agreement without cause within a defined notice period.

Competition

We operate in a highly competitive environment in the distribution of pharmaceuticals and related healthcare services. We also operate in a highly competitive environment in the development, manufacturing and distribution of medical and surgical products. We compete on many levels, including service offerings, support services, breadth of product lines and price.

In the Pharmaceutical segment, we compete with wholesale distributors with national reach (including McKesson Corporation, AmerisourceBergen Corporation and H.D. Smith), regional wholesale distributors (including Morris & Dickson Co., L.L.C.), self-warehousing chains, specialty distributors, third-party logistics companies (including United Parcel Service, Inc.) and nuclear pharmacies, among others. In addition, the Pharmaceutical segment has experienced competition from a number of organizations offering generic pharmaceuticals, including telemarketers. We also compete with manufacturers that sell all or part of their product offerings direct.

In the Medical segment, we compete with many different distributors, including Owens & Minor, Inc., Thermo Fisher Scientific Inc., McKesson Corporation, Henry Schein, Inc., Medline Industries, Inc., Mediq NV (through Byram Healthcare) and CCS Medical Holdings, Inc. We also compete with regional medical products distributors and third-party logistics companies. In addition,we compete with manufacturers that sell all or part of their product offerings direct. Competitors of the Medical segment’s manufacturing and procedural kit businesses include Kimberly-Clark Corporation, Ansell Limited, DeRoyal Industries Inc., Medline Industries, Inc., Professional Hospital Supply and Medical Action Industries.

Employees

At June 30, 2013, we had approximately 24,200 employees in the United States and approximately 9,400 employees outside of the United States. Overall, we consider our employee relations to be good.

Intellectual Property

We rely on a combination of trade secret, patent, copyright and trademark laws, nondisclosure and other contractual provisions, and technical measures to protect our products, services and intangible assets. We hold patents relating to: (1) medical and surgical products, such as fluid suction and irrigation devices; surgical waste management systems; surgical and medical examination gloves; surgical drapes, gowns and facial protection

products; and patient temperature management products; and (2) the distribution of our nuclear pharmacy products and service offerings. We also operate under licenses for certain proprietary technologies, and in certain instances we license our technologies to third parties.

We believe that we have taken all necessary steps to protect our proprietary rights, but no assurance can be given that we will be able to successfully enforce or protect our rights in the event that they are infringed upon by a third party. While all of these proprietary rights are important to our operations, we do not consider any particular patent, trademark, license, franchise or concession to be material to our overall business.

Regulatory Matters

Our business is highly regulated in the United States at both the federal and state level and in foreign countries. Depending upon their specific business, our subsidiaries may be subject to regulation by government entities including:

• | the U.S. Food and Drug Administration (the “FDA”); |

• | the U.S. Drug Enforcement Administration (the “DEA”); |

• | the U.S. Nuclear Regulatory Commission (the “NRC”); |

• | the U.S. Department of Health and Human Services; |

• | the U.S. Federal Trade Commission; |

• | U.S. Customs and Border Protection; |

• | state boards of pharmacy; |

• | state controlled substance agencies; |

• | state health departments, insurance departments or other comparable state agencies; and |

• | foreign agencies that are comparable to those listed above. |

These regulatory agencies have a variety of civil, administrative and criminal sanctions at their disposal. They can suspend our ability to distribute products or can initiate product recalls; they can seize products or impose criminal, civil and administrative sanctions; and they can seek injunctions to halt the manufacture and distribution of products.

Distribution

The FDA, DEA and various state authorities regulate the marketing, purchase, storage and distribution of pharmaceutical and medical products under various state and federal statutes including the Prescription Drug Marketing Act of 1987 and the Federal Controlled Substances Act (the "CSA"), which governs the sale, packaging, storage and distribution of controlled substances. Wholesale distributors of controlled substances must hold valid DEA registrations and state-level licenses, meet various security and operating standards, and comply with the CSA. As further discussed in Note 8 of the "Notes to Consolidated Financial Statements," in May 2012, we entered into a settlement agreement with the DEA pursuant to which our Lakeland, Florida pharmaceutical distribution center's registration to distribute controlled substances will be reinstated by the DEA in May 2014, subject to our compliance with the settlement agreement. Prior to reinstatement, our Lakeland facility will continue to distribute pharmaceutical products (other than controlled substances) while controlled substances will be shipped to customers from our other distribution centers.

Manufacturing and Marketing

Our subsidiaries that manufacture and source medical devices or pharmaceuticals may be subject to regulation by the FDA and comparable

4

Cardinal Health, Inc. and Subsidiaries | ||

foreign agencies including regulations regarding compliance with good manufacturing practices and quality systems.

The FDA and other domestic and foreign governmental agencies administer requirements that cover the design, testing, safety, effectiveness, manufacturing, labeling, promotion and advertising, distribution, importation and post-market surveillance of some of our manufactured products. We need specific approval or clearance from regulatory authorities before we can market and sell many of our products in particular countries. Even after we obtain approval or clearance to market a product, the product and our manufacturing processes are subject to continued regulatory review.

From time to time, we may determine that products we manufacture or market do not meet our specifications, regulatory requirements, or published standards. When we or a regulatory agency identify a quality or regulatory issue, we investigate and take appropriate corrective action, which may include withdrawing the product from the market, correcting the product at the customer location, revising product labeling, and notifying customers.

Nuclear Pharmacies and Related Businesses

Our nuclear pharmacies and cyclotron facilities require licenses or permits and must abide by regulations from the NRC, applicable state boards of pharmacy and the radiologic health agency or department of health of each state in which we operate. In addition, our cyclotron facilities must comply with the FDA's good manufacturing practices regulations for positron emission tomography, or PET, drugs.

Prescription Drug Pedigree Tracking and Supply Chain Integrity

There have been increasing efforts by Congress and state and federal agencies to regulate the pharmaceutical distribution system in order to prevent the introduction of counterfeit, adulterated or mislabeled drugs into the pharmaceutical distribution system (also known as "pedigree tracking”). The U.S. House of Representatives passed a pedigree tracking bill in June 2013 that would initially establish a lot-based pedigree tracking system. Some states also have adopted or are considering adopting pedigree tracking laws. For example, effective July 2016, California will require that pharmaceutical wholesalers implement electronic track-and-trace capabilities for pharmaceutical products.

Government Healthcare Programs

We are subject to healthcare fraud and abuse laws. These laws generally prohibit companies from soliciting, offering, receiving or paying any compensation in order to induce someone to order or purchase items or services that are in any way paid for by Medicare, Medicaid or other U.S. government-sponsored healthcare programs. They also prohibit submitting or causing to be submitted any fraudulent claim for payment by the federal government. Violations of these laws may result in criminal or civil penalties, as well as breach of contract claims and qui tam actions (false claims cases initiated by private parties purporting to act on behalf of federal or state governments).

AssuraMed is a Medicare-certified supplier with respect to a small portion of its business. It must meet defined Medicare quality standards and maintain accreditation to receive reimbursement from Medicare, and must comply with applicable billing, payment and record-keeping requirements. Failure to comply with Medicare supplier standards and billing requirements could result in civil and criminal sanctions, including the loss

of our ability to participate in Medicare and other federal and state healthcare programs.

In addition, our U.S. federal and state government contracts are subject to specific procurement regulations. Failure to comply with applicable rules or regulations or with a contractual or other requirements may result in qui tam actions, monetary damages and criminal and civil penalties. In addition, our government contracts could be terminated and we could be suspended or debarred from government contract work.

Health and Personal Information Practices

Services and products provided by some of our businesses involve access to patient-identifiable healthcare information. The Health Insurance Portability and Accountability Act of 1996, as augmented by the Health Information Technology for Economic and Clinical Health Act, as well as some state laws, regulate the use and disclosure of patient-identifiable health information, including requiring specified privacy and security measures. Federal and state officials have increasingly focused on how patient-identifiable healthcare information should be handled, secured and disclosed.

Some of our businesses collect and maintain other sensitive personal information that is subject to federal and state laws protecting such information. Security and disclosure of personal information is also highly regulated in many other countries in which we operate.

Environmental, Health and Safety Laws

In the United States and other countries, we are subject to various federal, state and local environmental laws, as well as laws relating to safe working conditions, laboratory and manufacturing practices.

Laws Relating to Foreign Trade and Operations

U.S. and international laws require us to abide by standards relating to the import and export of finished goods, raw materials and supplies and the handling of information. We also must comply with various export control and trade embargo laws, which may require licenses or other authorizations for transactions within some countries or with some counterparties.

Similarly, we are subject to laws concerning the conduct of our foreign operations, including the U.S. Foreign Corrupt Practices Act, Chinese anti-corruption laws and other foreign anti-bribery laws. Among other things, these laws generally prohibit companies and their intermediaries from offering, promising or making payments to officials of foreign governments for the purpose of obtaining or retaining business.

Regulation in China

Our China operations are subject to national, regional and local regulations, including licensing and regulatory requirements of the China National Health and Family Planning Commission, Ministry of Commerce, Ministry of Finance, the China Food and Drug Administration, the National Reform and Development Commission and the General Administration of Customs.

Other Information

Although our agreements with manufacturers sometimes require us to maintain inventory levels within specified ranges, our distribution businesses are generally not required by our customers to maintain particular inventory levels other than as needed to meet service level requirements. Certain supply contracts with U.S. government entities require us to maintain sufficient inventory to meet emergency demands,

5

Cardinal Health, Inc. and Subsidiaries | ||

but we do not believe those requirements materially affect inventory levels.

Our customer return policies generally require that the product be physically returned, subject to restocking fees. We only allow customers to return products that can be added back to inventory and resold at full value, or that can be returned to vendors for credit.

We offer market payment terms to our customers.

Revenue and Long-Lived Assets by Geographic Area

See Note 14 of the “Notes to Consolidated Financial Statements” for revenue and long-lived assets by geographic area.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports are available free of charge on our website (www.cardinalhealth.com), under the “Investors—Financial information—SEC filings” caption, as soon as reasonably practicable after we electronically file them with, or furnish them to, the Securities and Exchange Commission (the “SEC”).

You may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website (www.sec.gov) where you can search for annual, quarterly and current reports, proxy and information statements, and other information regarding us and other public companies.

Item 1A: Risk Factors

The risks described below could materially and adversely affect our results of operations, financial condition, liquidity and cash flows. These are not the only risks we face. Our businesses also could be affected by risks that we are not presently aware of or that we currently consider immaterial to our operations.

We could suffer the adverse effects of competitive pressures.

As described in greater detail in "Item 1: Business" above, we operate in markets that are highly competitive. Because of competition, our businesses face continued pricing pressure from our customers and suppliers. If we are unable to offset margin reductions caused by these pricing pressures through steps such as effective sourcing and enhanced cost control measures, our results of operations and financial condition could be adversely affected.

In addition, in recent years, the healthcare industry has continued to consolidate. Further consolidation among our customers and suppliers (including branded pharmaceutical manufacturers) could give the resulting enterprises greater bargaining power, which may adversely impact our results of operations.

CVS Caremark Corporation is a large customer that generates a significant amount of our revenue.

Our sales and credit concentration is significant. CVS accounted for approximately 23 percent of our fiscal 2013 revenue and 19 percent of our gross trade receivable balance at June 30, 2013. While we recently renewed our pharmaceutical distribution contracts with CVS, if CVS does not renew its contracts with us in the future, or terminates its contracts early, defaults in payment or significantly reduces its purchases of our products, our results of operations and financial condition could be adversely affected. Our contract with Walgreens will expire in August 2013

and sales to Walgreens accounted for approximately 20 percent of our fiscal 2013 revenue. We expect the expiration of the Walgreens contract to have an adverse impact on our results of operations, as discussed below in "Item 7: Management's Discussion and Analysis of Financial Condition and Results of Operations."

Our Pharmaceutical segment's margin may be affected by fewer or less profitable generic pharmaceutical launches, prices established by manufacturers and other factors that are beyond our control.

As described in greater detail in "Item 1: Business" above, margin in our Pharmaceutical segment consists, in part, of margin from our generic pharmaceutical programs and branded pharmaceutical price appreciation.

The number of new generic pharmaceutical launches varies from year to year, and the margin impact of new launches varies from product to product. Fewer generic pharmaceutical launches or launches that are less profitable than those previously experienced will have an adverse effect on our year-over-year margins. Additionally, prices for existing generic pharmaceuticals generally decline over time, although this may vary. Price deflation on existing generic pharmaceuticals will have an adverse effect on our margins.

With respect to branded pharmaceutical price appreciation, if branded manufacturers increase prices less frequently or by amounts that are smaller than have been experienced historically, we will earn less margin from branded pharmaceutical agreements.

The U.S. healthcare environment is changing in many ways, some of which may not be favorable to us.

The healthcare industry continues to undergo significant changes designed to increase access to medical care, improve safety, contain costs and increase efficiencies. Medicare and Medicaid reimbursement levels have declined; the use of managed care has increased; distributors, manufacturers, healthcare providers and pharmacy chains have consolidated and have formed strategic alliances; and large purchasing groups are prevalent. The industry also has experienced a shift away from traditional healthcare venues like hospitals and into clinics and office settings, and, in some cases, patients’ homes.

With respect to cost containment, the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act enacted in March 2010 have provisions designed to reduce costs of Medicare and Medicaid, including changing the federal upper payment limit for Medicaid reimbursement to no less than 175 percent of the average weighted manufacturer's price for generic pharmaceuticals. The Centers for Medicare and Medicaid Services is also considering providing states with alternatives to traditional reimbursement measures.

We could be adversely affected directly or indirectly (if our customers are adversely affected) by these and other changes in the delivery or pricing of, or reimbursement for, pharmaceuticals, medical devices or healthcare services.

Our business is subject to rigorous regulatory and licensing requirements.

The healthcare industry is highly regulated. As described in greater detail in "Item 1: Business" above, we are subject to regulation in the United States at both the federal and state level and in China and other foreign countries. If we fail to comply with these regulatory requirements, or if allegations are made that we fail to comply, our results of operations and

6

Cardinal Health, Inc. and Subsidiaries | ||

financial condition could be adversely affected.

To lawfully operate our businesses, we are required to hold permits, licenses and other regulatory approvals from, and to comply with operating and security standards of, governmental bodies. Failure to maintain or renew necessary permits, licenses or approvals, or to comply with required standards, could have an adverse effect on our results of operations and financial condition.

Products that we manufacture, source, distribute or market are required to comply with regulatory requirements. Noncompliance or concerns over noncompliance may result in suspension of our ability to distribute, import or manufacture products, product recalls or seizures, or criminal and civil sanctions.

We are required to comply with laws relating to healthcare fraud and abuse. If we fail to comply with these laws, we could be subject to federal or state government investigations or qui tam actions (false claims cases initiated by private parties purporting to act on behalf of federal or state governments), which could result in civil and criminal sanctions, including the loss of licenses or the ability to participate in Medicare, Medicaid and other federal and state healthcare programs. The requirements of these laws are extremely complex and subject to varying interpretations. It is possible that regulatory authorities could challenge our policies and practices, which may adversely affect our operations, results of operations and financial condition.

AssuraMed is a Medicare-certified supplier with respect to a small portion of its business. Its failure to comply with Medicare supplier standards and billing requirements could result in civil and criminal sanctions, including the loss of our ability to participate in Medicare and other federal and state healthcare programs.

Our government contracts are subject to specific procurement regulations. Failure to comply with applicable rules or regulations or with a contractual or other requirement may result in qui tam actions, monetary damages and criminal and civil penalties. In addition, our government contracts could be terminated and we could be suspended or debarred from government contract work.

Our global operations are required to comply with the U.S. Foreign Corrupt Practices Act, Chinese anti-corruption and similar anti-bribery laws in other jurisdictions and with U.S. and foreign export control, trade embargo and customs laws. If we fail to comply with any of these laws, we could suffer civil and criminal sanctions.

Our China operations are subject to national, regional and local regulations. The regulatory environment in China is evolving, and officials in the Chinese government exercise broad discretion in deciding how to interpret and apply regulations. It is possible that the Chinese government's current or future interpretation and application of existing or new regulations will negatively impact our China operations, result in regulatory investigations or lead to fines or penalties.

We could be subject to adverse changes in the tax laws or challenges to our tax positions.

We are a large multinational corporation with operations in the United States and many foreign countries. As a result, we are subject to the tax laws of many jurisdictions. From time to time, legislative initiatives are proposed in the United States, such as the repeal of last-in, first-out ("LIFO") treatment of inventory or a change in the current U.S. taxation of

income earned by foreign subsidiaries, that could adversely affect our tax positions, effective tax rate, tax payments or financial condition. Tax laws are extremely complex and subject to varying interpretations. Tax authorities have challenged some of our tax positions and it is possible that they will challenge others. These challenges may adversely affect our effective tax rate, tax payments or financial condition.

The CareFusion Spin-Off may have unexpected tax consequences.

In connection with the August 2009 CareFusion Spin-Off, we received a private letter ruling from the Internal Revenue Service (“IRS”) to the effect that the contribution by us of the assets of the clinical and medical products businesses to CareFusion and the distribution of CareFusion shares to our shareholders would qualify as a tax-free transaction under Sections 355 and 368(a)(1)(D) of the Internal Revenue Code (the “Code”). In addition, we received opinions of tax counsel to the effect that the CareFusion Spin-Off would qualify as a transaction that is described in Sections 355(a) and 368(a)(1)(D) of the Code. The IRS private letter ruling and the opinions of counsel rely on certain facts, assumptions, representations and undertakings from us and CareFusion regarding the past and future conduct of the companies' respective businesses and other matters. If any of these facts, assumptions, representations or undertakings is incorrect or not otherwise satisfied, we and our shareholders may not be able to rely on the IRS ruling or the opinions of tax counsel. Similarly, the IRS could determine on audit that the CareFusion Spin-Off is taxable if it determines that any of the facts, assumptions, representations or undertakings are not correct or have been violated or if the IRS disagrees with the conclusions in the opinions of counsel that are not covered by the private letter ruling or for other reasons. If the CareFusion Spin-Off is determined to be taxable for U.S. federal income tax purposes, we and our shareholders that are subject to U.S. federal income tax could incur significant tax liabilities.

Our business and operations depend on the proper functioning of information systems and critical facilities.

We rely on information systems to obtain, rapidly process, analyze and manage data to:

• | facilitate the purchase and distribution of inventory items from numerous distribution centers; |

• | receive, process and ship orders on a timely basis; |

• | manage the accurate billing and collections for thousands of customers; |

• | process payments to suppliers; |

• | facilitate the manufacturing and assembly of medical products; and |

• | generate financial information. |

Our business also depends on the proper functioning of our critical facilities, including our national logistics center. Our results of operations could be adversely affected if these systems or facilities, or our customers' access to them, are interrupted, damaged by unforeseen events, cyber security incidents or other actions of third parties, or fail for any extended period of time.

In addition, data security breaches could adversely impact our operations, results of operations or our ability to satisfy legal requirements, including those related to patient-identifiable health information.

7

Cardinal Health, Inc. and Subsidiaries | ||

Because of the nature of our business, we may become involved in legal proceedings that could adversely impact our cash flows or results of operations.

Due to the nature of our businesses, which includes the manufacture and distribution of healthcare products, we may from time to time become involved in disputes or legal proceedings. For instance, some of the products we manufacture or distribute may be alleged to cause personal injury or violate the intellectual property rights of another party, subjecting us to product liability or infringement claims. While we generally obtain indemnity rights from the manufacturers of products we distribute and we carry product liability insurance, it is possible that liability from such claims could exceed those protections. We also may be named in breach of contract claims or qui tam actions (false claims cases initiated by private parties purporting to act on behalf of federal or state governments). Litigation is inherently unpredictable, and the unfavorable resolution of one or more of these legal proceedings could adversely affect our cash flows or results of operations.

Acquisitions can have unanticipated results.

An important element of our growth strategy has been to acquire other businesses that expand or complement our existing businesses. Acquisitions involve risks: we may overpay for a business or fail to realize the synergies and other benefits we expect from the acquisition; future developments may impair the value of our purchased goodwill or intangible assets; or we may encounter unforeseen accounting, internal control, regulatory or compliance issues.

We depend on certain suppliers to make their raw materials and products available to us and are subject to fluctuations in costs of raw materials and products.

We depend on the availability of various components, compounds, raw materials (including radioisotopes) and energy supplied by others for our operations. Any of our supplier relationships could be interrupted due to events beyond our control, including natural disasters, or could be terminated. A sustained supply interruption could have an adverse effect on our business.

Our manufacturing businesses use oil-based resins, cotton, latex and other commodities as raw materials in many products. Prices of oil and gas also affect our distribution and transportation costs. Prices of these commodities are volatile and have fluctuated significantly in recent years, so costs to produce and distribute our products also have fluctuated. Due to competitive dynamics and contractual limitations, we may be unable to pass along cost increases through higher prices. If we cannot fully offset cost increases through other cost reductions, or recover these costs through price increases or surcharges, our results of operations could be adversely affected.

Our global operations are subject to economic, political and currency risks.

Our global operations are affected by local economic environments, including inflation, recession, currency volatility and competition. Political changes also can disrupt our global operations, as well as our customers and suppliers, in a particular location. We may not be able to hedge or obtain insurance to protect us against these risks, and any hedges or insurance may be expensive and may not successfully mitigate these risks.

Economic conditions may adversely affect demand for our products and services.

Deterioration in general economic conditions in the United States and other countries in which we do business could adversely affect the amount of prescriptions filled and the number of medical procedures undertaken and, therefore, reduce purchases of our products and services by our customers, which could adversely affect our results of operations.

Item 1B: Unresolved Staff Comments

Not applicable.

Item 2: Properties

In the United States, at June 30, 2013, the Pharmaceutical segment operated 21 primary pharmaceutical distribution facilities and one national logistics center; two specialty distribution facilities and two other distribution facilities; one specialty pharmacy and over 150 nuclear pharmacy laboratories, manufacturing and distribution facilities. The Medical segment operated over 60 medical-surgical distribution, assembly, manufacturing, and research operation facilities. Our U.S. operating facilities are located in 45 states and in Puerto Rico.

Outside the United States, at June 30, 2013, our Medical segment operated over 20 facilities in Canada, the Dominican Republic, Malaysia, Malta, Mexico, and Thailand that engage in manufacturing, distribution or research. In addition, our Pharmaceutical and Medical segments utilized various distribution facilities in China.

At June 30, 2013, we owned over 70 operating facilities and leased more than 200 operating facilities. Our principal executive offices are headquartered in an owned building located at 7000 Cardinal Place in Dublin, Ohio.

We consider our operating properties to be in satisfactory condition and adequate to meet our present needs. However, we regularly evaluate operating properties and may make further additions and improvements or consolidate locations as we seek opportunities to expand our business.

Item 3: Legal Proceedings

In addition to the proceedings described below, the legal proceedings described in Note 8 of the "Notes to Consolidated Financial Statements" are incorporated in this "Item 3: Legal Proceedings" by reference.

In June 2012, Henry Stanley, Jr., a purported shareholder, filed a derivative action on behalf of Cardinal Health, Inc. in the U.S. District Court for the Southern District of Ohio (the "federal case") against the current and certain former members of our Board of Directors. A similar action was filed by Daniel Himmel, a purported shareholder, in the Common Pleas Court of Delaware County, Ohio (the "state case") against the current and certain former members of our Board of Directors and certain of our officers. The complaints allege that the defendants breached their fiduciary duties in connection with the DEA's suspension of our Lakeland, Florida distribution center's registration to distribute controlled substances in February 2012, and the suspension and reinstatement of such registrations at three of our facilities in 2007 and 2008. The state action also makes claims based on corporate waste and unjust enrichment. The complaints seek, among other things, unspecified money damages from the defendants and an award of attorney's fees. In October 2012, the court granted the defendants' motion to dismiss the federal action with prejudice, and in August 2013, the court of appeals affirmed the decision. In July

8

Cardinal Health, Inc. and Subsidiaries | ||

2013, the court granted the defendants' motion to dismiss the state action, and in August 2013, the plaintiff appealed the court's decision.

Separately, in September 2012, a purported shareholder made demand on our Board of Directors to take action against the current and certain former members of our Board of Directors to recover damages based on allegations similar to those set forth in the derivative actions above. Our Board of Directors formed a special committee of independent directors to investigate the allegations made in the shareholder demand. After receiving and evaluating the special committee's findings and recommendations, our Board of Directors determined in May 2013 that pursuing the shareholder claims was not in the best interest of the company.

Item 4: Mine Safety Disclosures

Not applicable.

Executive Officers of the Registrant

The following is a list of our executive officers as of August 9, 2013:

Name | Age | Position |

George S. Barrett | 58 | Chairman and Chief Executive Officer |

Jeffrey W. Henderson | 48 | Chief Financial Officer |

Michael C. Kaufmann | 50 | Chief Executive Officer, Pharmaceutical segment |

Donald M. Casey, Jr. | 53 | Chief Executive Officer, Medical segment |

Craig S. Morford | 54 | Chief Legal and Compliance Officer |

Carole S. Watkins | 53 | Chief Human Resources Officer |

Mark R. Blake | 42 | Executive Vice President, Strategy and Corporate Development |

Stephen T. Falk | 48 | Executive Vice President, General Counsel and Corporate Secretary |

The business experience summaries provided below for our executive officers describe positions held during the last five years (unless otherwise indicated).

Mr. Barrett has served as Chairman and Chief Executive Officer since August 2009. From January 2008 to August 2009, he served as Vice Chairman of Cardinal Health and Chief Executive Officer, Healthcare Supply Chain Services.

Mr. Henderson has served as Chief Financial Officer since May 2005.

Mr. Kaufmann has served as Chief Executive Officer, Pharmaceutical segment, since August 2009. From April 2008 until August 2009, he served as our Group President, Pharmaceutical Supply Chain.

Mr. Casey has served as Chief Executive Officer, Medical segment, since April 2012. Before joining us, he served as Chief Executive Officer of the Gary and Mary West Wireless Health Institute, a non-profit research organization focused on lowering the cost of healthcare through novel technology solutions, from March 2010 to March 2012. Prior to that, he served as World Wide Franchise Chairman, Comprehensive Care at Johnson & Johnson, a developer and manufacturer of health care products, from 2007 to 2009.

Mr. Morford has served as Chief Legal and Compliance Officer since May 2009. From May 2008 to May 2009, he served as our Chief Compliance Officer.

Ms. Watkins has served as Chief Human Resources Officer since 2000.

Mr. Blake has served as Executive Vice President, Strategy and Corporate Development since October 2009. From August 2006 until October 2009, he held various business development positions with Medco Health Solutions, Inc., a pharmacy benefits management services company, including Vice President, Business Development and Senior Director, Business Development.

Mr. Falk has served as Executive Vice President, General Counsel and Corporate Secretary since May 2009. From April 2007 to May 2009, he served as our Executive Vice President and General Counsel of Healthcare Supply Chain Services.

9

Cardinal Health, Inc. and Subsidiaries | ||

Part II | ||

a

Item 5: Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common shares are listed on the New York Stock Exchange under the symbol “CAH.” The following table reflects the range of the reported high and low closing prices of our common shares as reported on the New York Stock Exchange Composite Tape and the per share dividends declared for the fiscal years ended June 30, 2013 and 2012, and from July 1, 2013 through the period ended on August 9, 2013:

High | Low | Dividends | |||||||||

Fiscal 2012 | |||||||||||

Quarter Ended: | |||||||||||

September 30, 2011 | $ | 46.83 | $ | 37.99 | $ | 0.215 | |||||

December 31, 2011 | 45.49 | 39.88 | 0.215 | ||||||||

March 31, 2012 | 43.31 | 40.82 | 0.215 | ||||||||

June 30, 2012 | 43.33 | 40.33 | 0.2375 | ||||||||

Fiscal 2013 | |||||||||||

Quarter Ended: | |||||||||||

September 30, 2012 | $ | 43.50 | $ | 37.75 | $ | 0.2375 | |||||

December 31, 2012 | 42.65 | 39.29 | 0.275 | ||||||||

March 31, 2013 | 47.09 | 41.62 | 0.275 | ||||||||

June 30, 2013 | 48.76 | 41.85 | 0.3025 | ||||||||

Fiscal 2014 | |||||||||||

Through August 9, 2013 | $ | 51.57 | $ | 47.02 | $ | 0.3025 | |||||

At August 9, 2013 there were approximately 10,827 shareholders of record of our common shares.

We anticipate that we will continue to pay quarterly cash dividends in the future. The payment and amount of future dividends remain, however, within the discretion of our Board of Directors and will depend upon our future earnings, financial condition, capital requirements and other factors.

Issuer Purchases of Equity Securities | |||||||||||||

Period | Total Number of Shares Purchased (1) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Program (2) | Approximate Dollar Value of Shares That May Yet be Purchased Under the Program (2) (in millions) | |||||||||

April 1 – 30, 2013 | 394 | $ | 42.93 | — | $ | 650 | |||||||

May 1 – 31, 2013 | 2,194,527 | 47.46 | 2,194,160 | 546 | |||||||||

June 1 – 30, 2013 | 3,563,986 | 47.42 | 3,084,186 | 400 | |||||||||

Total | 5,758,907 | $ | 47.43 | 5,278,346 | $ | 400 | |||||||

(1) | Includes 394, 207 and 265 common shares purchased in April, May and June 2013, respectively, through a rabbi trust as investments of participants in our Deferred Compensation Plan; 160 and 1,072 restricted shares surrendered in May and June 2013, respectively, by equity compensation plan participants upon vesting to meet tax withholding; and 478,463 common shares owned and tendered in June 2013 by an equity compensation plan participant to meet the exercise price and tax withholding for stock option exercises. |

(2) | On August 8, 2012, our Board of Directors approved a $750 million share repurchase program (the "August 2012 program"), which expires on August 31, 2015. During fiscal 2013, we repurchased 10.2 million common shares having an aggregate cost of $450 million, including $350 million under the August 2012 program. |

10

Cardinal Health, Inc. and Subsidiaries | ||

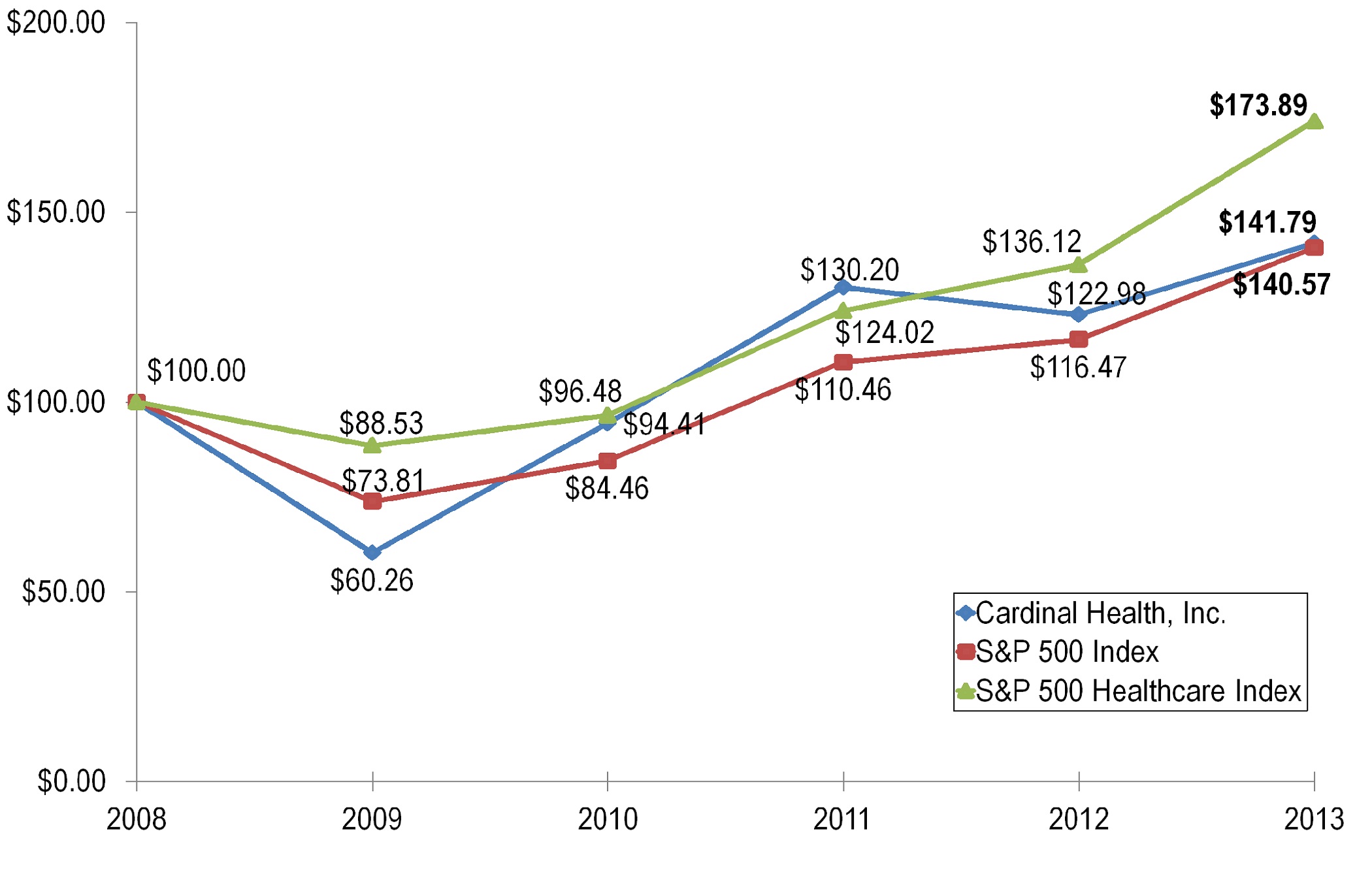

Performance Graphs

Five Year Performance Graph

The following line graph compares the cumulative total return of our common shares with the cumulative total return of the Standard & Poor’s Composite—500 Stock Index (the "S&P 500 Index") and the Standard & Poor's Composite—500 Healthcare Index (the "S&P 500 Healthcare Index"). The line graph assumes, in each case, an initial investment of $100 on June 30, 2008, based on the market prices at the end of each fiscal year through and including June 30, 2013, and reinvestment of dividends. The S&P 500 Index and S&P 500 Healthcare Index investments are weighted on the basis of market capitalization at the beginning of each period. We have adjusted the market price of our common shares prior to August 31, 2009 to reflect the CareFusion Spin-Off on August 31, 2009.

June 30 | |||||||||||||||||||||||

2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||||||||||||||||||

Cardinal Health, Inc. | $ | 100.00 | $ | 60.26 | $ | 94.41 | $ | 130.20 | $ | 122.98 | $ | 141.79 | |||||||||||

S&P 500 Index | 100.00 | 73.81 | 84.46 | 110.46 | 116.47 | 140.57 | |||||||||||||||||

S&P 500 Healthcare Index | 100.00 | 88.53 | 96.48 | 124.02 | 136.12 | 173.89 | |||||||||||||||||

Post CareFusion Spin-Off Graph

We have included a second line graph below to show our cumulative total return compared with the cumulative total return of the S&P 500 Index and the S&P 500 Healthcare Index since the CareFusion Spin-Off on August 31, 2009. The line graph assumes, in each case, an initial investment of $100 on August 31, 2009 through and including June 30, 2013, and reinvestment of dividends. We have adjusted the market price of our common shares on August 31, 2009 to reflect the CareFusion Spin-Off.

August 31 2009 | June 30 2010 | June 30 2011 | June 30 2012 | June 30 2013 | |||||||||||||||

Cardinal Health, Inc. | $ | 100.00 | $ | 138.45 | $ | 190.95 | $ | 180.33 | $ | 207.88 | |||||||||

S&P 500 Index | 100.00 | 102.68 | 134.20 | 141.48 | 170.92 | ||||||||||||||

S&P 500 Healthcare Index | 100.00 | 100.55 | 129.25 | 141.86 | 181.22 | ||||||||||||||

11

Cardinal Health, Inc. and Subsidiaries | ||

Item 6: Selected Financial Data

The consolidated financial data below includes all business combinations as of the date of acquisition that occurred during these periods. The following selected consolidated financial data should be read in conjunction with the consolidated financial statements and related notes and “Item 7: Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

(in millions, except per common share amounts) | 2013 (1) | 2012 | 2011 | 2010 | 2009 | ||||||||||||||

Earnings Data: | |||||||||||||||||||

Revenue | $ | 101,093 | $ | 107,552 | $ | 102,644 | $ | 98,503 | $ | 95,992 | |||||||||

Earnings from continuing operations | $ | 335 | $ | 1,070 | $ | 966 | $ | 587 | $ | 758 | |||||||||

Earnings/(loss) from discontinued operations (2) | (1 | ) | (1 | ) | (7 | ) | 55 | 394 | |||||||||||

Net earnings | $ | 334 | $ | 1,069 | $ | 959 | $ | 642 | $ | 1,152 | |||||||||

Basic earnings/(loss) per common share: | |||||||||||||||||||

Continuing operations | $ | 0.98 | $ | 3.10 | $ | 2.77 | $ | 1.64 | $ | 2.12 | |||||||||

Discontinued operations (2) | — | — | (0.02 | ) | 0.15 | 1.10 | |||||||||||||

Net basic earnings per common share | $ | 0.98 | $ | 3.10 | $ | 2.75 | $ | 1.79 | $ | 3.22 | |||||||||

Diluted earnings/(loss) per common share: | |||||||||||||||||||

Continuing operations | $ | 0.97 | $ | 3.06 | $ | 2.74 | $ | 1.62 | $ | 2.10 | |||||||||

Discontinued operations (2) | — | — | (0.02 | ) | 0.15 | 1.08 | |||||||||||||

Net diluted earnings per common share | $ | 0.97 | $ | 3.06 | $ | 2.72 | $ | 1.77 | $ | 3.18 | |||||||||

Cash dividends declared per common share | $ | 1.0900 | $ | 0.8825 | $ | 0.8000 | $ | 0.7200 | $ | 0.5950 | |||||||||

Balance Sheet Data: | |||||||||||||||||||

Total assets | $ | 25,819 | $ | 24,260 | $ | 22,846 | $ | 19,990 | $ | 25,119 | |||||||||

Long-term obligations, less current portion | 3,686 | 2,418 | 2,175 | 1,896 | 3,272 | ||||||||||||||

Shareholders’ equity (3) | 5,975 | 6,244 | 5,849 | 5,276 | 8,725 | ||||||||||||||

(1) | During the fourth quarter of fiscal 2013, we recognized a non-cash goodwill impairment charge of $829 million ($799 million, net of tax) related to our Nuclear Pharmacy Services division. |

(2) | On August 31, 2009, we separated the clinical and medical products businesses from our other businesses through a pro rata distribution to shareholders of 81 percent of the then outstanding common stock of CareFusion and met the criteria for classification of these businesses as discontinued operations. During the fourth quarter of fiscal 2009, we committed to plans to sell our United Kingdom-based Martindale injectable manufacturing business within our Pharmaceutical segment, and met the criteria for classification of this business as discontinued operations. |

(3) | As noted above, on August 31, 2009, we completed the distribution to our shareholders of 81 percent of the then outstanding common stock of CareFusion. The distribution of CareFusion common stock to our shareholders resulted in the recognition of a $3.7 billion non-cash dividend. |

12

Cardinal Health, Inc. and Subsidiaries | ||

Financial Review | ||

Item 7: Management’s Discussion and Analysis of Financial Condition and Results of Operations

The discussion and analysis presented below refers to, and should be read in conjunction with, the consolidated financial statements and related notes included in this Form 10-K. Unless otherwise indicated, throughout this Management's Discussion and Analysis of Financial Condition and Results of Operations, we are referring to our continuing operations.

Overview

We are a healthcare services company providing pharmaceutical and medical products and services that help pharmacies, hospitals, ambulatory surgery centers, clinical laboratories, physician offices and other healthcare providers focus on patient care while reducing costs, enhancing efficiency and improving quality. We also provide medical products to patients in the home.

We report our financial results in two segments: Pharmaceutical and Medical.

During fiscal 2013, revenue decreased 6 percent to $101.1 billion, largely due to the previously disclosed expiration of our pharmaceutical distribution contract with Express Scripts and the impact of brand-to-generic pharmaceutical conversions.

Gross margin increased 8 percent to $4.9 billion, reflecting strong performance in our Pharmaceutical segment generic programs. Operating earnings decreased 44 percent to $1.0 billion and earnings from continuing operations decreased 69 percent to $335 million due to an $829 million ($799 million, net of tax) non-cash goodwill impairment charge related to our Nuclear Pharmacy Services division.

Our cash and equivalents balance was $1.9 billion at June 30, 2013, compared to $2.3 billion at June 30, 2012. The decrease in cash and equivalents during fiscal 2013 was driven by acquisitions of $2.2 billion, share repurchases of $450 million and dividends of $353 million, offset by strong net cash provided by operating activities of $1.7 billion and net proceeds from long-term obligations of $981 million. We plan to execute a balanced deployment of available capital to position ourselves for sustainable competitive advantage and to enhance shareholder value.

Large Customers

On April 25, 2013, we announced the renewal of our pharmaceutical distribution contracts with CVS. CVS accounted for approximately 23 percent of our fiscal 2013 revenue.

Our pharmaceutical distribution contract with Walgreens will expire at the end of August 2013. Because sales to Walgreens generated approximately 20 percent of our consolidated revenue for fiscal 2013, we expect the expiration of this contract to have an adverse impact on our results of operations. We are taking steps to reduce our costs and otherwise mitigate the impact of the expiration of the Walgreens contract in fiscal 2014 and afterward. Largely as a result of the contract expiration, we do not currently expect diluted earnings per share from continuing operations to grow in fiscal 2014 compared to fiscal 2013, excluding the effects in both periods of restructuring and employee severance costs; acquisition-related costs and credits; impairments and gains and losses on disposal of assets (including the $829 million Nuclear Pharmacy Services division goodwill impairment charge in fiscal 2013); net litigation recoveries and charges; and charges and tax benefits associated with each of these items. After the expiration of this contract, we also anticipate

a significant net working capital decrease based on reduced inventory and accounts receivable, partially offset by reduced accounts payable. Based on the expected working capital decrease and other factors, we anticipate that the expiration of the Walgreens contract will result in a net after-tax benefit to cash flow from operating activities in fiscal 2014 in excess of $500 million.

Goodwill

In conjunction with the preparation of our consolidated financial statements for the fiscal year ended June 30, 2013, we recently completed our annual goodwill impairment test, which we perform annually in the fourth quarter. As part of this annual test, we concluded that the entire goodwill amount of our Nuclear Pharmacy Services division was impaired, resulting in a non-cash impairment charge of $829 million ($799 million, net of tax). This impairment charge does not impact our liquidity, cash flows from operations, or compliance with debt covenants.

The majority of the goodwill of our Nuclear Pharmacy Services division was acquired through our acquisition of Syncor International Corporation in fiscal 2003 ($681 million of goodwill). Excluding the impact of the impairment charge, we have a total of approximately $1.0 billion of invested capital in our Nuclear Pharmacy Services division (inclusive of the Syncor acquisition), accumulated over the past 12 years.

As previously disclosed in our Quarterly Reports on Form 10-Q for the quarters ended December 31, 2012, and March 31, 2013, our Nuclear Pharmacy Services division has experienced significant softness in the low-energy diagnostics market. During the second half of fiscal 2013, we experienced sustained volume declines and price erosion for the core, low-energy products provided by this division. In addition, we experienced reduced sales for some existing high-energy diagnostic products, slower-than-expected adoption of new high-energy diagnostic products, and recent reimbursement developments that may adversely impact the future growth of these products. Using this information, we adjusted our outlook and long-term business plans for this division during our annual budgeting process, which we recently concluded. This update resulted in significant reductions in the anticipated future cash flows and estimated fair value for this reporting unit. See Note 5 of the “Notes to Consolidated Financial Statements” for additional information.

Restructuring

On January 30, 2013, we announced a restructuring plan within our Medical segment. Under this restructuring plan, we are moving production of procedure kits from our facility in Waukegan, Illinois to other facilities and selling property and consolidating office space in Waukegan, Illinois. In addition, we reorganized our Medical segment and plan to sell our sterilization processes in El Paso, Texas. We estimate the total costs associated with this restructuring plan to be approximately $79 million on a pre-tax basis, of which $51 million was recognized during fiscal 2013. Of the estimated $28 million remaining costs to be recognized through the end of fiscal 2014, we estimate that approximately $3 million will be employee-related costs; $11 million will be facility exit and other costs; and $14 million will be an expected loss on disposal of the property in Waukegan, Illinois described above. We have evaluated this property and have determined that at June 30, 2013 it does not meet the criteria for classification as held for sale. The costs recognized during 2013 are classified as restructuring and employee severance and impairments and loss on disposal of assets in the consolidated statements of earnings. We

13

Cardinal Health, Inc. and Subsidiaries | ||

Financial Review (continued) | ||

expect to start realizing cost savings and other benefits from the plan in fiscal 2014.

Acquisitions

On March 18, 2013, we completed the acquisition of AssuraMed for $2.07 billion, net of cash acquired, in an all-cash transaction. We funded the acquisition through the issuance of $1.3 billion in fixed rate notes and cash on hand. The acquisition of AssuraMed, a provider of medical supplies to homecare providers and patients in the home, expands our ability to serve this patient base. We expect the amortization of acquisition-related intangible assets to be a significant expense in future periods. Excluding the impact of amortization of acquisition-related intangible assets, this acquisition had a positive impact on operating earnings in fiscal 2013 and we expect it to have a positive impact on operating earnings in future periods. See Note 2 of the “Notes to Consolidated Financial Statements” for additional information on the AssuraMed acquisition.

Other Trends

Within our Pharmaceutical segment, we expect continued strength in our generic pharmaceutical programs as well as continued price appreciation from branded pharmaceutical products in fiscal 2014.

Within our Medical segment, variability in the cost of commodities such as oil-based resins, cotton, latex, diesel fuel and other commodities can have a significant impact on cost of products sold. Although commodity prices fluctuate, we do not expect changes in commodity prices to have a significant impact on our year-over-year results of operations in fiscal 2014. We also expect a continuation of relatively flat procedural-based utilization in fiscal 2014.

Results of Operations

Revenue

Revenue | Change | ||||||||||||||||

(in millions) | 2013 | 2012 | 2011 | 2013 | 2012 | ||||||||||||

Pharmaceutical | $ | 91,097 | $ | 97,925 | $ | 93,744 | (7 | )% | 4 | % | |||||||

Medical | 10,060 | 9,642 | 8,922 | 4 | % | 8 | % | ||||||||||

Total segment revenue | 101,157 | 107,567 | 102,666 | (6 | )% | 5 | % | ||||||||||

Corporate | (64 | ) | (15 | ) | (22 | ) | N.M. | N.M. | |||||||||

Total revenue | $ | 101,093 | $ | 107,552 | $ | 102,644 | (6 | )% | 5 | % | |||||||

Fiscal 2013 Compared to Fiscal 2012

Pharmaceutical Segment

Revenue for fiscal 2013 compared to the prior year was negatively impacted by the expiration on September 30, 2012 of our pharmaceutical distribution contract with Express Scripts (approximately $6.7 billion), the revenue from which was classified as bulk sales. Revenue from existing pharmaceutical distribution customers decreased by approximately $3.6 billion, primarily as a result of brand-to-generic pharmaceutical conversions. Brand-to-generic pharmaceutical conversions impact our revenue because generic pharmaceuticals generally sell at a lower price than the corresponding brand product and because some of our customers primarily source generic products directly from manufacturers rather than from us. The decrease was partially offset by increased pharmaceutical distribution revenue from new customers (approximately $3.8 billion) and revenue growth within our Specialty Solutions division ($961 million).

Revenue from bulk sales was $29.8 billion and $40.2 billion for fiscal 2013 and 2012, respectively. Bulk sales for fiscal 2013 decreased by 26 percent driven primarily by the expiration of our contract with Express Scripts and brand-to-generic conversions. Revenue from non-bulk sales was $61.3 billion and $57.7 billion for fiscal 2013 and 2012, respectively. Non-bulk sales for fiscal 2013 increased by 6 percent driven by growth from new customers. See “Item 1: Business” for more information about bulk and non-bulk sales. In light of the reduction in bulk sales after the expiration of our pharmaceutical distribution contract with Walgreens, we do not expect the distinction between revenue and profit from bulk sales to be meaningful in the future. As such, in the future, we do not expect to present separate information on bulk and non-bulk sales to investors.

Medical Segment

Revenue for fiscal 2013 compared to the prior year reflects the benefit of acquisitions ($459 million).

Fiscal 2012 Compared to Fiscal 2011

Pharmaceutical Segment

Revenue was positively impacted during fiscal 2012 compared to the prior year by acquisitions ($2.3 billion) and increased sales to existing customers ($2.0 billion).

Medical Segment

Revenue was positively impacted during fiscal 2012 compared to the prior year by increased volume from existing customers ($335 million), including the positive impact from sales of self-manufactured and private brand products and the transition during the fourth quarter of fiscal 2011 of our relationship with CareFusion from a fee-for-service arrangement to a traditional distribution model ($131 million).

Cost of Products Sold

Consistent with the change in revenue, cost of products sold decreased $6.8 billion (7 percent) during fiscal 2013, and increased by $4.5 billion (5 percent) during fiscal 2012. See the gross margin discussion below for additional drivers impacting cost of products sold.

Gross Margin

Gross Margin | Change | ||||||||||||||||

(in millions) | 2013 | 2012 | 2011 | 2013 | 2012 | ||||||||||||

Gross margin | $ | 4,921 | $ | 4,541 | $ | 4,162 | 8 | % | 9 | % | |||||||

Fiscal 2013 Compared to Fiscal 2012

Gross margin increased in fiscal 2013 compared to the prior year driven by strong performance in our generic pharmaceutical programs ($350 million) and acquisitions ($131 million). Increased margin from branded pharmaceutical distribution agreements (exclusive of the related volume impact) also had a positive impact on gross margin ($81 million). Pricing changes, including rebates (exclusive of the related volume impact), adversely impacted gross margin ($211 million), driven in part by customer and product mix. The adverse impact of these pricing changes is offset by sourcing programs and other sources of margin. As a result of significant market softness, gross margin from our Nuclear Pharmacy Services division decreased by $71 million in fiscal 2013.

The cost of oil-based resins, cotton, latex and other commodities used in our Medical segment self-manufactured products had a slightly favorable impact on gross margin. As described above, while the expiration of the

14

Cardinal Health, Inc. and Subsidiaries | ||

Financial Review (continued) | ||

Express Scripts contract resulted in lower revenue, it had a slightly unfavorable impact on gross margin.

Fiscal 2012 Compared to Fiscal 2011

Gross margin increased in fiscal 2012 compared to the prior year primarily due to strong performance in our generic pharmaceutical programs ($344 million), including the impact of new product launches and price appreciation on a few specific products, and acquisitions ($137 million). Favorable Medical segment product sales mix and increased sales volume resulted in a $100 million favorable impact to gross margin. Pricing changes, including rebates (exclusive of the related volume impact), adversely impacted gross margin ($205 million). The adverse impact of these pricing changes was offset by sourcing programs and other sources of margin. Increased cost of oil-based resins, cotton, latex and other commodities used in our Medical segment self-manufactured products decreased gross margin by $66 million.

Distribution, Selling, General and Administrative ("SG&A") Expenses