Exhibit 99.1

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

The Clorox Company

(Dollars in millions, except per share

amounts)

Management’s Discussion and Analysis of

Financial Condition and Results of Operations (MD&A) is designed to provide

a reader of The Clorox Company’s (the Company or Clorox) financial statements

with a narrative from the perspective of management on the Company’s financial

condition, results of operations, liquidity and certain other factors that may

affect future results. In certain instances, parenthetical references are made

to relevant sections of the Notes to Consolidated Financial Statements to direct

the reader to a further detailed discussion. This section should be read in

conjunction with the Consolidated Financial Statements and Supplementary Data

included in this Annual Report on Form 10-K. The following sections are included

herein:

- Executive Overview

- Results of Operations

- Financial Position and Liquidity

- Contingencies

- Quantitative and Qualitative Disclosures about Market Risk

- Recently Issued Accounting Pronouncements

- Critical Accounting Policies and Estimates

- Summary of Non-GAAP Financial Measures

EXECUTIVE OVERVIEW

Clorox is a leading multinational

manufacturer and marketer of consumer and professional products with

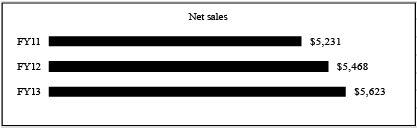

approximately 8,400 employees worldwide as of June 30, 2013, and fiscal year

2013 net sales of $5,623. Clorox sells its products primarily through mass

merchandisers, retail outlets, e-commerce channels, distributors and medical

supply providers. Clorox markets some of the most trusted and recognized brand

names, including its namesake bleach and cleaning products, Clorox Healthcare™,

HealthLink®, Aplicare® and Dispatch® products,

Green Works® naturally derived products, Pine-Sol®

cleaners, Poett® home care products, Fresh Step® cat

litter, Glad® bags, wraps and containers, Kingsford®

charcoal, Hidden Valley® and KC Masterpiece® dressings and

sauces, Brita® water-filtration products, and Burt’s Bees®

and güd® natural personal care products. The Company manufactures

products in more than two dozen countries and markets them in more than 100

countries.

The Company primarily markets its leading

brands in midsized categories considered to have attractive economic profit

potential. Most of the Company’s products compete with other nationally

advertised brands within each category and with “private label” brands.

The Company operates through strategic

business units that are aggregated into four reportable segments: Cleaning,

Household, Lifestyle and International.

- Cleaning consists of laundry, home care and professional products

marketed and sold in the United States. Products within this segment include

laundry additives, including bleach products under the Clorox®

brand and Clorox 2® stain fighter and color booster; home

care products, primarily under the Clorox®, Formula

409®, Liquid-Plumr®, Pine-Sol®, S.O.S®

and Tilex® brands; naturally derived products under the Green

Works® brand; and professional cleaning and disinfecting products

under the Clorox®, Dispatch®, Aplicare®,

HealthLink® and Clorox HealthcareTM brands.

- Household

consists of charcoal, cat litter and plastic bags, wraps and container

products marketed and sold in the United States. Products within this segment

include plastic bags, wraps and containers under the Glad® brand;

cat litter products under the Fresh Step®, Scoop Away®

and Ever Clean® brands; and charcoal products under the

Kingsford® and Match Light® brands.

1

- Lifestyle

consists of food products, water-filtration systems and filters, and natural

personal care products marketed and sold in the United States. Products within

this segment include dressings and sauces, primarily under the Hidden

Valley®, KC Masterpiece® and Soy Vay® brands;

water-filtration systems and filters under the Brita® brand; and

natural personal care products under the Burt’s Bees® and

güd® brands.

- International consists of products sold outside the United States. Products within

this segment include laundry, home care, water-filtration, charcoal and cat

litter products, dressings and sauces, plastic bags, wraps and containers and

natural personal care products, primarily under the Clorox®,

Javex®, Glad®, PinoLuz®, Ayudin®,

Limpido®, Clorinda®, Poett®,

Mistolin®, Lestoil®, Bon Bril®,

Nevex®, Brita®, Green Works®,

Pine-Sol®, Agua Jane®, Chux®,

Kingsford®, Fresh Step®, Scoop Away®, Ever

Clean®, KC Masterpiece®, Hidden Valley® and

Burt’s Bees® brands.

Non-GAAP Financial Measures

This Executive Overview, the succeeding

sections of MD&A and Exhibit 99.3 include certain financial measures that

are not defined by accounting principles generally accepted in the United States

of America (U.S. GAAP). These measures, which are referred to as non-GAAP

measures, are listed below.

- Economic profit (EP)

- Free cash flow and free cash flow as a percentage of net sales

- Earnings from continuing operations before interest and taxes (EBIT)

margin (the ratio of EBIT to net sales)

- Debt to earnings from continuing operations before interest, taxes,

depreciation and amortization ratio (EBITDA ratio)

Where indicated, each of the following non-GAAP

financial measures excludes the fiscal year

2011 noncash goodwill impairment charge:

- Adjusted diluted net earnings per share from continuing

operations

- Earnings from continuing operations before income taxes and noncash

goodwill impairment charge

For a discussion of these measures and the

reasons management believes they are useful to investors, refer to “Summary of

Non-GAAP Financial Measures” below. For a discussion of the EBITDA ratio, please

refer to “Credit Arrangements” below. This MD&A and Exhibit 99.3 include

reconciliations to the most directly comparable financial measures calculated

and presented in accordance with U.S. GAAP.

Fiscal Year 2013 Financial

Highlights

In fiscal year 2013, Clorox reported

earnings from continuing operations of $574. The Company delivered solid

results, including 3% net sales growth, $4.31 diluted net earnings per share

from continuing operations and free cash flow of $583 million, which was

approximately 10% of net sales. This compares to earnings from continuing

operations of $543 and diluted net earnings per share from continuing operations

of $4.10 in fiscal year 2012.

Key fiscal year 2013 financial results are

summarized as follows:

- The Company’s fiscal year 2013 net sales grew 3%,

with gains in all four segments, reflecting strong product innovation and the

benefit of price increases, partially offset by unfavorable foreign currency

exchange rates.

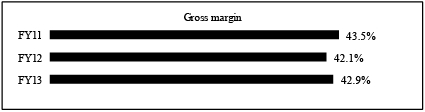

- Gross margin increased 80 basis points to 42.9% in

fiscal year 2013 from 42.1% in fiscal year 2012, reflecting the benefit of

cost savings and price increases, partially offset by higher manufacturing and

logistics costs.

- EP increased to $426 in fiscal year 2013 compared

to $402 in fiscal year 2012 (refer to the reconciliation of EP to earnings

from continuing operations before income taxes in Exhibit 99.3).

2

- The Company delivered diluted net earnings per

share from continuing operations in fiscal year 2013 of $4.31, an increase of

approximately 5% from fiscal year 2012 diluted net earnings per share of

$4.10.

- Free cash flow was $583 or 10% of net sales in

fiscal year 2013, an increase from $428 or 8% of net sales in fiscal year 2012

(refer to “Free cash flow” below).

- The Company returned $335 in dividends to stockholders and in May 2013

announced an increase of nearly 11% in the annual cash dividend to $2.84 per

share from $2.56 per share. In fiscal year 2013, the Company repurchased a

total of 1.5 million shares of its common stock at a cost of approximately

$128.

Strategic Goals and Initiatives

Since 2007, Clorox has been operating

under its Centennial Strategy, which has guided its strategic choices and

financial goals to drive growth through fiscal year 2013. The Company delivered

solid results, including 3% compounded annual growth rate for net sales and 6%

compounded annual growth rate for EP in the past five-year period. In October of

this year, the Company will unveil its 2020 strategy, which builds on the

success of the Centennial Strategy and directs the Company to the highest value

opportunities for long-term, profitable growth and strong stockholder returns.

The Company’s long-term financial goals

include sales growth of 3-5%, EBIT margin growth between 25-50 basis points and

free cash flow as a percentage of net sales of about 10-12%, which Clorox

anticipates using to invest in the business, maintain debt leverage within its

target range and return excess cash to stockholders. With a commitment to

maintaining a healthy dividend, the Company’s goal is to continue delivering

total stockholder returns in the top third of its peer group.

Clorox is also focused on addressing the

competitive intensity it continues to anticipate in disinfecting wipes and

laundry additives in fiscal year 2014, with demand-building plans that include

an increase in merchandising activity as well as product innovation. In

addition, the Company is focused on managing the challenges that continue to

pressure its margins, particularly in Venezuela and Argentina, as well as the

recent changes in the economy impacting foreign currencies and commodity costs.

Clorox will continue to reshape its

portfolio toward businesses aligned with the four consumer megatrends of health

& wellness, sustainability, the multicultural marketplace and

affordability/value. The Company is also focused on the growth pillars of U.S.

retail, professional products and international businesses: growing U.S. retail

through execution of its “3D” demand creation model; growing professional

products by expanding its healthcare business organically and through bolt-on

acquisitions; and growing international businesses by focusing on existing

markets where the Company has significant scale and competitive

advantage.

Clorox also will continue enhancing its

capabilities in the “3Ds”: Desire, Decide and Delight, as a means of increasing

consumer loyalty. 3D capabilities include targeted marketing communications to

drive consumer desire, stand-out product packaging and in-store promotions to

compel purchase decisions at the point of decide and superior-quality products

to delight consumers. Moreover, Clorox continues to drive its product innovation

efforts, with an annual target of 3 percentage points of incremental sales

growth from new products.

Looking forward, the Company will continue

to execute against its strategy to deliver profitable growth and long-term

stockholder value.

3

RESULTS OF OPERATIONS

Management’s discussion and analysis of

the Company’s results of operations, unless otherwise noted, compares fiscal

year 2013 to fiscal year 2012, and fiscal year 2012 to fiscal year 2011, using

percentage and basis point changes calculated on a rounded basis, except as

noted.

CONSOLIDATED

RESULTS

Continuing operations

Net sales in fiscal year 2013 increased 3%. Volume was flat, driven by

higher shipments in the professional products business, primarily due to base

healthcare and cleaning business strength and the benefit of acquisitions in

fiscal year 2012; higher shipments of Glad® premium trash bags,

primarily due to new product innovation and increased merchandising events;

higher shipments of Clorox® disinfecting wipes behind strong

merchandising activities and a heightened flu season; higher shipments of Hidden

Valley® products behind strong merchandising activity and innovation;

higher shipments of Burt’s Bees® natural personal care products,

primarily driven by new product innovation and promotional events; and higher

shipments of the new concentrated Clorox® liquid bleach. These

increases were offset by lower shipments of charcoal products, primarily due to

poor weather conditions and price increases; the exit from international

nonstrategic export businesses; lower shipments of Brita®

water-filtration products, primarily due to decreased merchandising activities,

price increases and a comparison to strong volume in the prior year behind the

launch of the Brita® Bottle; lower shipments of Glad® base

trash bags, primarily due to decreased merchandising and a shift to premium

trash products, and Glad® food storage products, primarily due to

distribution losses; lower shipments of Clorox 2® stain fighter and

color booster, primarily due to category softness and distribution losses; and

lower shipments in Canada. Net sales growth outpaced volume primarily due to the

benefit of price increases (approximately 270 basis points), partially offset by

unfavorable foreign currency exchange rates (approximately 60 basis points).

Net sales in fiscal year 2012 increased

5%. Volume increased 2%, driven by higher shipments in the professional products

business, primarily due to the acquisitions of HealthLink and Aplicare, Inc.;

higher shipments of Clorox® disinfecting wipes behind strong

merchandising activities; higher shipments in Argentina; higher shipments of

Fresh Step® cat litter behind new product innovation; higher

shipments of Burt’s Bees® natural personal care products, primarily

driven by increased merchandising and new products, including the launch of the

güd® natural personal care line; and higher shipments of the

Brita® Bottle. These increases were partially offset by lower

shipments of Clorox® laundry additives, primarily due to price

increases; the fiscal year 2012 exit from international nonstrategic export

business; lower shipments of Glad® base trash bags due to price

increases; lower shipments in Venezuela, primarily driven by the Venezuelan

government’s price control law; and lower shipments of Pine-Sol®

cleaners, primarily due to price increases. Net sales growth outpaced volume

growth primarily due to the benefit of price increases (approximately 480 basis

points), partially offset by unfavorable product mix (approximately 110 basis

points) and higher trade-promotion spending (approximately 60 basis points).

4

Gross profit increased 5% in fiscal year 2013, from $2,304 to $2,412, and

gross margin, defined as gross profit as a percentage of net sales, increased 80

basis points to 42.9%. Gross margin expansion in fiscal year 2013 reflects 160

basis points from cost savings and 120 basis points from the benefit of price

increases. These factors were partially offset by 170 basis points from higher

manufacturing and logistics costs, including the impact of inflationary

pressures in Argentina and Venezuela.

Gross profit increased 1% in fiscal

year 2012, from $2,273 to $2,304, and gross margin decreased 140 basis points to

42.1%. Gross margin contraction in fiscal year 2012 reflects 220 basis points

from higher commodity costs, 180 basis points from higher manufacturing and

logistics costs and 90 basis points from unfavorable product mix. These factors

were partially offset by 220 and 160 basis points from the benefits of price

increases and cost savings, respectively.

Expenses

|

|

|

|

|

|

|

|

|

|

|

% Change |

|

% of Net

sales |

|

|

2013 |

|

2012 |

|

2011 |

|

2013

to

2012 |

|

2012

to

2011 |

|

2013 |

|

2012 |

|

2011 |

| Selling and administrative expenses |

|

$ |

807 |

|

$ |

798 |

|

$ |

735 |

|

1 |

% |

|

9 |

% |

|

14.4 |

% |

|

14.6 |

% |

|

14.1 |

% |

| Advertising

costs |

|

|

500 |

|

|

482 |

|

|

502 |

|

4 |

|

|

(4 |

) |

|

8.9 |

|

|

8.8 |

|

|

9.6 |

|

| Research and development costs |

|

|

130 |

|

|

121 |

|

|

115 |

|

7 |

|

|

5 |

|

|

2.3 |

|

|

2.2 |

|

|

2.2 |

|

Selling and administrative

expenses increased slightly in fiscal

year 2013, primarily driven by higher wages and employee benefits, largely due

to international inflation, as well as investments made in systems and processes

to support the long-term growth of the Burt’s Bees business. These increases

were largely offset by prior year non-repeating advisory fees related to a

withdrawn proxy contest, as well as fiscal year 2013 lower employee incentive

compensation costs and cost savings.

Selling and administrative expenses

increased in fiscal year 2012, driven by higher employee incentive compensation

costs, non-repeating advisory fees related to a withdrawn proxy contest in

fiscal year 2012, and fiscal year 2012 investments in IT systems and the new

Pleasanton facility, partially offset by cost savings.

Advertising

costs as a percentage of sales increased

slightly during fiscal year 2013. Activity was primarily in support of new

products, including the launch of new concentrated Clorox® liquid

bleach and Burt’s Bees® natural personal care products.

Advertising costs as a percentage of

sales decreased during fiscal year 2012, primarily driven by reduced media

spending.

Research and development

costs increased slightly as a percentage

of net sales in fiscal year 2013, primarily driven by costs related to the

investment in and transition to the Company’s new Pleasanton research and

development facility.

Research and development costs as a

percentage of net sales remained flat in fiscal year 2012 as the Company

continued to support its new products and established brands with an emphasis on

innovation.

Goodwill impairment, interest

expense, other (income) expense, net, and the effective tax rate on income from

continuing operations

|

|

2013 |

|

2012 |

|

2011 |

| Goodwill

impairment |

|

$ |

- |

|

$ |

- |

|

|

$ |

258 |

|

| Interest expense |

|

|

122 |

|

|

125 |

|

|

|

123 |

|

| Other (income) expense,

net |

|

|

- |

|

|

(13 |

) |

|

|

(23 |

) |

| Income taxes on continuing

operations |

|

|

279 |

|

|

248 |

|

|

|

276 |

|

Goodwill

impairment

During fiscal year 2011, the Company

recorded a noncash goodwill impairment charge related to the Burt’s Bees

business of $258, of which $164 and $94 was reflected in the Lifestyle and

International reportable segments, respectively. There was no substantial tax

benefit associated with this noncash charge (see Note 7 of the Notes to

Consolidated Financial Statements).

5

Interest expense

decreased $3 in fiscal year 2013,

primarily due to a lower weighted-average interest rate on long-term debt

resulting from the issuance of senior notes in September 2012 and the maturities

of senior notes in October 2012 and March 2013. Interest expense in fiscal year

2012 increased by $2, primarily due to higher average commercial paper

balances.

Other (income) expense,

net, of $0 in fiscal year 2013 included

$(12) of income from equity investees, $(4) from gains on fixed asset sales,

net, and $(4) of low-income housing partnership gains; partially offset by $11

of foreign currency exchange losses and $9 of amortization of trademarks and

other intangible assets.

Other (income) expense, net, of $(13) in

fiscal year 2012 included $(11) of income from equity investees and $(6) of

income from transition services related to the Company’s sale of its global auto

care businesses (Auto Businesses); partially offset by $9 of amortization of

trademarks and other intangible assets.

Other (income) expense, net, of $(23) in

fiscal year 2011 included $(13) of low-income housing partnership gains, $(9) of

income from transition services related to the Company’s sale of its Auto

Businesses and $(8) of income from equity investees; partially offset by $9 of

amortization of trademarks and other intangible assets.

The effective tax rate on earnings

from continuing operations was 32.7%,

31.4% and 49.0% in fiscal years 2013, 2012 and 2011, respectively. The increase

in the fiscal year 2013 effective tax rate was primarily due to lower tax on

foreign earnings and higher uncertain tax position releases in fiscal year 2012.

The current and prior year periods also reflect benefits from tax settlements.

The substantially lower tax rate in fiscal year 2012 as compared to fiscal year

2011 was primarily due to the non-deductible noncash goodwill impairment charge

of $258 in fiscal year 2011 related to the Burt’s Bees reporting unit, as there

was no substantial tax benefit associated with this noncash charge. Also

contributing to the decrease in fiscal year 2012 was lower tax on foreign

earnings, favorable tax settlements and a decrease in the blended state tax

rate, partially offset by higher uncertain tax position releases in fiscal year

2011.

Diluted net earnings per share from

continuing operations

The following table presents a

reconciliation of diluted net earnings per share from

continuing operations to adjusted diluted net earnings per share from continuing

operations for fiscal year 2011, which excludes the then-recorded noncash goodwill impairment charge:

|

|

|

|

|

|

|

|

|

|

|

% Change |

|

|

2013 |

|

2012 |

|

2011 |

|

2013

to

2012 |

|

2012

to

2011 |

| Diluted net earnings per

share from continuing operations |

|

$ |

4.31 |

|

$ |

4.10 |

|

$ |

2.07 |

|

5.1 |

% |

|

98.1 |

% |

| Add back: Noncash goodwill impairment per

share |

|

|

- |

|

|

- |

|

|

1.86 |

|

- |

|

|

(100 |

) |

Adjusted diluted net earnings per share from

continuing

operations |

|

$ |

4.31 |

|

$ |

4.10 |

|

$ |

3.93 |

|

5.1 |

|

|

4.3 |

|

Diluted net earnings per share from

continuing operations increased $0.21 in fiscal year 2013, driven by the benefit

of price increases and strong cost savings. These factors were partially offset

by higher manufacturing and logistics costs and other supply chain costs,

including the impact of inflationary pressures in Argentina and Venezuela,

unfavorable foreign currency exchange rates and a higher effective tax rate.

Government imposed price controls in Argentina and Venezuela also had a negative

impact on net sales, gross margin and diluted net earnings per share from

continuing operations.

Diluted net earnings per share from

continuing operations increased $2.03 in fiscal year 2012, driven primarily by

the noncash goodwill impairment charge of $258 recognized in fiscal year 2011.

Excluding the fiscal year 2011 noncash goodwill impairment charge, the Company’s

adjusted diluted net earnings per share from continuing operations increased

$0.17 in fiscal year 2012, driven by price increases implemented across the

portfolio, higher volume, strong cost savings, share repurchases and a lower

effective tax rate. These factors were partially offset by higher commodity

costs; inflationary pressures impacting manufacturing and logistics costs; and

higher selling and administrative costs, primarily due to higher employee

incentive compensation costs and investments in the Company’s information

technology (IT) systems and a new facility located in Pleasanton,

Calif.

6

Free cash flow

|

|

2013 |

|

2012 |

|

2011 |

| Net cash provided by

continuing operations |

|

$ |

777 |

|

|

$ |

620 |

|

|

$ |

690 |

|

| Less: capital expenditures |

|

|

(194 |

) |

|

|

(192 |

) |

|

|

(228 |

) |

| Free cash flow |

|

$ |

583 |

|

|

$ |

428 |

|

|

$ |

462 |

|

| Free cash flow as a percentage of net

sales |

|

|

10.4 |

% |

|

|

7.8 |

% |

|

|

8.8 |

% |

Free cash flow as a percentage of

net sales increased in fiscal year 2013,

primarily due to favorable changes in working capital, the prior year settlement

of interest rate forward contracts and higher earnings.

Free cash flow as a percentage of net

sales decreased in fiscal year 2012, primarily due to lower tax payments in

fiscal year 2011, resulting from favorable tax depreciation rules, and the

timing of tax payments in fiscal year 2012.

Discontinued operations

In September 2010, the Company entered

into a definitive agreement to sell its Auto Businesses to an affiliate of

Avista Capital Partners in an all-cash transaction. In November 2010, the

Company completed the sale pursuant to the terms of a Purchase and Sale

Agreement (Purchase Agreement) and received cash consideration of $755. The

Company also received cash flows of approximately $30 related to net working

capital that was retained by the Company as part of the sale. Included in

earnings from discontinued operations for the fiscal year ended June 30, 2011,

was an after-tax gain on the transaction of $247.

The following table includes financial

results attributable to the Auto Businesses as of June 30, 2011:

| Net sales |

$ |

95 |

|

| Earnings before income taxes |

$ |

34 |

|

| Income tax expense on

earnings |

|

(11 |

) |

| Gain on sale, net of tax |

|

247 |

|

| Earnings from discontinued

operations, net of tax |

$ |

270 |

|

SEGMENT RESULTS FROM CONTINUING

OPERATIONS

The following presents the results from

continuing operations of the Company’s reportable segments and certain

unallocated costs reflected in Corporate (see Note 20 of the Notes to

Consolidated Financial Statements for a reconciliation of segment results to

consolidated results):

Cleaning

|

|

|

|

|

|

|

|

|

|

|

% Change |

|

|

2013 |

|

2012 |

|

2011 |

|

2013

to

2012 |

|

2012

to

2011 |

| Net sales |

|

$ |

1,783 |

|

$ |

1,692 |

|

$ |

1,619 |

|

5 |

% |

|

5 |

% |

| Earnings from continuing operations before

income taxes |

|

|

420 |

|

|

381 |

|

|

356 |

|

10 |

|

|

7 |

|

7

Fiscal year 2013 versus fiscal year

2012: Net sales, volume and earnings from

continuing operations before income taxes increased during fiscal year 2013.

Cleaning segment volume growth was 3%, driven by higher shipments in the

professional products business, primarily due to base healthcare and cleaning

business strength and the benefit of acquisitions in fiscal year 2012; higher

shipments of Clorox® disinfecting wipes behind strong merchandising

activities and a heightened flu season; and higher shipments of the new

concentrated Clorox® liquid bleach. These increases were partially

offset by lower shipments of Clorox® 2 stain fighter and color

booster due to category softness and distribution losses and lower shipments of

Pine-Sol® cleaners, primarily due to price increases. Net sales

growth outpaced volume growth primarily due to the benefit of price increases

(approximately 170 basis points). The increase in earnings from continuing

operations before income taxes was primarily due to higher net sales and $35 of

cost savings, primarily related to the new concentrated Clorox®

liquid bleach and package redesign. These increases were partially offset

by $24 of higher manufacturing and logistics and other supply chain costs; $13

of higher selling and administrative costs, primarily related to the

acquisitions in fiscal year 2012 and costs associated with the transition to new

concentrated Clorox® liquid bleach; and $10 of higher advertising and

sales promotion expenses, primarily in support of new concentrated Clorox®

liquid bleach.

Fiscal year 2012 versus fiscal year

2011: Net sales, volume and earnings from

continuing operations before income taxes increased during fiscal year 2012.

Cleaning segment volume growth was 2%, driven by higher shipments in the

professional products business, primarily due to the acquisitions of HealthLink

and Aplicare, Inc. and distribution gains in health care channels; higher

shipments of Clorox® disinfecting wipes behind strong merchandising

activities; and higher shipments of Clorox® disinfecting bathroom

cleaner due to product innovation. These increases were partially offset by

lower shipments of Clorox® laundry additives, primarily due to price

increases. Net sales growth outpaced volume growth primarily due to the benefit

of price increases (approximately 450 basis points), partially offset by

unfavorable product mix (approximately 190 basis points). The increase in

earnings from continuing operations before income taxes was primarily due to

higher net sales, $22 of cost savings due to various manufacturing efficiencies

and $10 of lower advertising and sales promotion expenses. These increases were

partially offset by $30 of higher commodity costs, primarily resin, $14 of

unfavorable product mix and $14 of higher manufacturing and logistics

costs.

Household

|

|

|

|

|

|

|

|

|

|

|

% Change |

|

|

2013 |

|

2012 |

|

2011 |

|

2013

to

2012 |

|

2012

to

2011 |

| Net sales |

|

$ |

1,693 |

|

$ |

1,676 |

|

$ |

1,611 |

|

1 |

% |

|

4 |

% |

| Earnings from continuing operations before

income taxes |

|

|

336 |

|

|

298 |

|

|

278 |

|

13 |

|

|

7 |

|

Fiscal year 2013 versus fiscal year

2012: Net sales and earnings from continuing

operations before income taxes increased while volume decreased during fiscal

year 2013. Household segment volume decline was 3%, driven by lower shipments of

charcoal products due to poor weather conditions and price increases, and lower

shipments of Glad® base trash bags, primarily due to decreased

merchandising and a shift to premium trash products, and Glad® food

storage products, primarily due to distribution losses. These decreases were

partially offset by higher shipments of Glad® premium trash bags

primarily due to new product innovation and increased merchandising events. The

variance between net sales and volume was primarily due to the benefit of price

increases (approximately 340 basis points). The increase in earnings from

continuing operations before income taxes was driven by $31 of cost savings,

primarily related to various manufacturing efficiencies, and $26 from the

benefit of price increases; partially offset by $15 of higher manufacturing and

logistics and other supply chain costs.

Fiscal year 2012 versus fiscal year

2011: Net sales, volume and earnings from

continuing operations before income taxes increased during fiscal year 2012.

Household segment volume growth was 1%, driven by higher shipments of Fresh

Step® cat litter behind new product innovation and higher shipments

of Glad® OdorShield® trash bags with Febreze®;

partially offset by lower shipments of Glad® base trash bags due to

price increases. Net sales growth outpaced volume growth primarily due to the

benefit of price increases (approximately 530 basis points). The increase in

earnings from continuing operations before income taxes was primarily due to

higher net sales and $35 of cost savings related to various manufacturing

efficiencies. These increases were partially offset by $44 of higher commodity

costs, primarily resin, and $30 of higher manufacturing and logistics costs.

8

Lifestyle

|

|

|

|

|

|

|

|

|

|

|

% Change |

|

|

2013 |

|

2012 |

|

2011 |

|

2013

to

2012 |

|

2012

to

2011 |

| Net sales |

|

$ |

929 |

|

$ |

901 |

|

$ |

849 |

|

3 |

% |

|

6 |

% |

Earnings from continuing operations

before

income

taxes |

|

|

259 |

|

|

265 |

|

|

91 |

|

(2 |

) |

|

191 |

|

| Noncash goodwill impairment |

|

|

- |

|

|

- |

|

|

164 |

|

- |

|

|

(100 |

) |

Earnings from continuing operations before

income

taxes and

noncash goodwill impairment charge |

|

$ |

259 |

|

$ |

265 |

|

$ |

255 |

|

(2 |

) |

|

4 |

|

Fiscal year 2013 versus fiscal year

2012: Net sales and volume increased while

earnings from continuing operations before income taxes decreased during fiscal

year 2013. Lifestyle segment volume growth was 2%, driven by higher shipments of

Hidden Valley® products behind strong merchandising activity and

innovation, and higher shipments of Burt’s Bees® natural personal

care products, primarily driven by new product innovation and promotional

events. These increases were partially offset by lower shipments of Brita®

water-filtration products, primarily due to decreased merchandising

activities, price increases and a comparison to strong volume in the prior year

behind the launch of the Brita® Bottle; and lower shipments of KC

Masterpiece® sauces, primarily due to competitive activity. Net sales

growth outpaced volume growth primarily due to the benefit of price increases

(approximately 120 basis points). The decline in earnings from continuing

operations before income taxes was primarily due to approximately $12 of higher

other supply chain costs and $8 of higher selling and administrative expenses,

both driven, in part, by investments in systems and processes to support the

long-term growth of the Burt’s Bees business, and $7 of higher advertising and

sales promotion expenses in support of new products. These increases were

partially offset by higher net sales and $10 of cost savings, primarily related

to various manufacturing efficiencies.

Fiscal year 2012 versus fiscal year

2011: Net sales, volume, earnings from

continuing operations before income taxes and earnings from continuing

operations before income taxes and noncash goodwill impairment charge increased

during fiscal year 2012. Lifestyle segment volume growth was 3%, driven by

higher shipments of Burt’s Bees® natural personal care products, due

to increased merchandising and new products, including the launch of the

güd® natural personal care line, higher shipments of the

Brita® Bottle and the acquisition of Soy Vay Enterprises, Inc. These

increases were partially offset by lower shipments of bottled Hidden

Valley® salad dressings due to price increases and lower shipments of

Brita® pour through water-filtration products. Net sales growth

outpaced volume growth primarily due to the benefit of price increases

(approximately 360 basis points). The increase in earnings from continuing

operations before income taxes was primarily driven by the noncash goodwill

impairment charge of $164 in fiscal year 2011. The increase in earnings from

continuing operations before income taxes and noncash goodwill impairment charge

was primarily due to higher net sales and $10 of cost savings related to various

manufacturing efficiencies, partially offset by $20 of higher commodity costs,

primarily soybean oil.

International

|

|

|

|

|

|

|

|

|

|

|

% Change |

|

|

2013 |

|

2012 |

|

2011 |

|

2013

to

2012 |

|

2012

to

2011 |

| Net sales |

|

$ |

1,218 |

|

$ |

1,199 |

|

$ |

1,152 |

|

2 |

% |

|

4 |

% |

Earnings from continuing

operations before

income

taxes |

|

|

96 |

|

|

119 |

|

|

55 |

|

(19 |

) |

|

116 |

|

| Noncash goodwill

impairment |

|

|

- |

|

|

- |

|

|

94 |

|

- |

|

|

(100 |

) |

Earnings from continuing

operations before income

taxes and noncash

goodwill impairment charge |

|

$ |

96 |

|

$ |

119 |

|

$ |

149 |

|

(19 |

) |

|

(20 |

) |

9

Fiscal year 2013 versus fiscal year

2012: Net sales increased while volume and

earnings from continuing operations before income taxes decreased during fiscal

year 2013. International segment volume decline was 2%, driven by the exit from

nonstrategic export businesses and lower shipments in Canada, partially offset

by higher shipments in Asia and certain regions in Latin America. The variance

between net sales and volume was primarily due to the benefit of price increases

(approximately 450 basis points) and favorable product mix (approximately 160

basis points), partially offset by unfavorable foreign currency exchange rates

(approximately 290 basis points). The decrease in earnings from continuing

operations before income taxes was primarily due to $55 of higher manufacturing

and logistics and other supply chain costs and $12 of higher selling and

administrative costs, both factors reflecting the impact of inflationary

pressures in Argentina and Venezuela; $24 of unfavorable foreign currency

exchange rates; and other smaller items. These decreases were partially offset

by $53 from the benefit of price increases; $15 of cost savings, primarily

related to various manufacturing efficiencies; and $11 of favorable product mix.

Government imposed price controls in Argentina and Venezuela also had a negative

impact on International segment net sales, gross margin and earnings from

continuing operations before income taxes.

Fiscal year 2012 versus fiscal year

2011: Net sales, volume and earnings from

continuing operations before income taxes increased while earnings from

continuing operations before income taxes and the noncash goodwill impairment

charge decreased during fiscal year 2012. International segment volume growth

was 2%, driven by higher shipments in Argentina, partially offset by the exit

from nonstrategic export businesses, and lower shipments in Venezuela, primarily

as a result of the Venezuelan government’s price control law. Net sales growth

outpaced volume growth, primarily due to the benefit of price increases

(approximately 530 basis points), partially offset by unfavorable foreign

currency exchange rates (approximately 110 basis points). The increase in

earnings from continuing operations before income taxes was primarily driven by

the noncash goodwill impairment charge of $94 in fiscal year 2011. The decrease

in earnings from continuing operations before income taxes and noncash goodwill

impairment charge was primarily due to $37 of higher manufacturing and logistics

costs due to the impact of inflationary pressures in Argentina and Venezuela;

$25 of higher selling and administrative costs associated with investments in IT

systems; and $19 of higher commodity costs, primarily resin. These decreases

were partially offset by higher net sales and $14 of cost savings, primarily

related to various manufacturing efficiencies.

Venezuela

The financial statements of the Company’s

subsidiary in Venezuela are consolidated under the rules governing the

preparation of financial statements in a highly inflationary economy. As such,

the subsidiary’s non-U.S. dollar (non-USD) monetary assets and liabilities are

remeasured into USD each reporting period with the resulting gains and losses

reflected in other (income) expense, net.

On February 8, 2013, the Venezuelan

government announced a devaluation of the official currency exchange rate

(CADIVI) from 4.3 to 6.3 bolívares fuertes (VEF) per USD and the elimination of

the alternative currency exchange system, SITME. Prior to February 8, 2013, the

Company had been utilizing the rate at which it had been obtaining USD through

SITME to remeasure its Venezuelan financial statements, which was 5.7 VEF per

USD at the announcement date. In response to these developments, the Company

began utilizing the CADIVI rate of 6.3 VEF per USD. The Company recorded a

remeasurement loss of $4 related to the devaluation in fiscal year 2013, which

was reflected in other (income) expense, net.

In March 2013, the Venezuelan government

announced the creation of a new alternative currency exchange system (SICAD),

which is intended to complement CADIVI. Based on a number of factors, including

the limited number of SICAD auctions held to date, restrictions placed on

eligible participants, the amount of USD available to purchase through the

auction process, and the lack of official information about the resulting

exchange rate, the Company does not believe it is appropriate to use the SICAD

rate as the official remeasurement rate at this time.

As a measure of sensitivity given the

uncertainty of exchange rates in Venezuela, based on the VEF-denominated net

monetary position as of June 30, 2013, a hypothetical additional 10% VEF

devaluation would result in an additional remeasurement loss of $3.

Price Control Laws

In fiscal years 2013 and 2012, government

imposed price control laws in Argentina and Venezuela negatively impacted the

net selling prices of certain products sold in those countries. The Company’s

ability to grow net sales and net earnings in Argentina and Venezuela will be

affected by a number of factors, including the government imposed price

controls, possible future currency devaluations, local economic conditions,

inflation rates and the availability of raw materials and utilities.

10

Corporate

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% Change |

|

|

2013 |

|

2012 |

|

2011 |

|

2013

to

2012 |

|

2012

to

2011 |

| Losses from continuing

operations before income taxes |

|

$ |

(258 |

) |

|

$ |

(272 |

) |

|

$ |

(217 |

) |

|

(5 |

)% |

|

25 |

% |

Corporate includes certain non-allocated

administrative costs, interest income, interest expense and certain other

non-operating income and expenses. Corporate assets include cash and cash

equivalents, property and equipment, other investments and deferred

taxes.

Fiscal year 2013 versus fiscal year

2012: The decrease in losses from continuing

operations before income taxes was primarily due to prior year non-repeating

advisory fees related to a withdrawn proxy contest, as well as lower employee

incentive compensation costs in fiscal year 2013. These factors were partially

offset by higher wages and employee benefit costs in fiscal year 2013.

Fiscal year 2012 versus fiscal year

2011: The increase in losses from continuing

operations before income taxes was primarily due to higher employee incentive

compensation and benefit costs, higher low-income housing partnership gains in

fiscal year 2011 and non-repeating advisory fees related to a withdrawn proxy

contest in fiscal year 2012; partially offset by lower IT expenses reflected in

Corporate.

FINANCIAL POSITION AND

LIQUIDITY

Management’s discussion and analysis of

the Company’s financial position and liquidity describes its consolidated

operating, investing and financing activities, contractual obligations and

off-balance sheet arrangements.

The following table summarizes cash

activities as of June 30:

|

|

2013 |

|

2012 |

|

2011 |

| Net cash provided by

continuing operations |

|

$ |

777 |

|

|

$ |

620 |

|

|

$ |

690 |

|

| Net cash (used for) provided by investing

activities |

|

|

(55 |

) |

|

|

(277 |

) |

|

|

544 |

|

| Net cash used for

financing activities |

|

|

(685 |

) |

|

|

(321 |

) |

|

|

(1,078 |

) |

The Company’s cash position includes

amounts held by foreign subsidiaries, and as a result the repatriation of

certain cash balances from some of the Company’s foreign subsidiaries could

result in additional tax costs. However, these cash balances are generally

available without legal restriction to fund local business operations. In

addition, a portion of the Company’s cash balance is held in U.S. dollars by

foreign subsidiaries, whose functional currency is their local currency. Such

U.S. dollar balances are reported on the foreign subsidiaries’ books, in their

functional currency, with the impact from foreign currency exchange rate

differences recorded in other (income) expense, net. The Company’s cash holdings

were as follows as of June 30:

|

|

2013 |

|

2012 |

|

2011 |

| Non-U.S. dollar balances held by non-U.S.

dollar functional currency subsidiaries |

|

$ |

115 |

|

$ |

81 |

|

$ |

98 |

| U.S. dollar balances held by non-U.S. dollar functional

currency subsidiaries |

|

|

36 |

|

|

35 |

|

|

15 |

| Non-U.S. dollar balances held by U.S. dollar

functional currency subsidiaries |

|

|

18 |

|

|

20 |

|

|

26 |

| U.S. dollar balances held by U.S. dollar functional

currency subsidiaries |

|

|

130 |

|

|

131 |

|

|

120 |

| Total |

|

$ |

299 |

|

$ |

267 |

|

$ |

259 |

The Company’s total cash balance was $299

as of June 30, 2013, as compared to $267 as of June 30, 2012. The increase of

$32 was primarily attributable to $777 of net cash provided by continuing

operations, $593 of net proceeds from the September 2012 long-term debt

issuance, $135 of proceeds from the sale-leaseback of the Company’s general

office building in Oakland, Calif. and former Technical and Data Center in

Pleasanton, Calif., and $133 of proceeds from the issuance of common stock for

employee stock plans and other. These increases were partially offset by $850 of

repayments of long-term debt, $335 of dividend payments, $194 of capital

expenditures, $128 of share repurchases and $98 of repayments of commercial

paper borrowings.

11

The Company’s total cash balance remained

essentially flat as of June 30, 2012, as compared to June 30, 2011.

As of June 30, 2013, total current assets

exceeded total current liabilities by $286, and, as of June 30, 2012, total

current liabilities exceeded total current assets by $685. The year-over-year

change was primarily attributable to $850 of current maturities of long-term

debt as of June 30, 2012.

Operating Activities

Net cash provided by continuing operations

increased to $777 in fiscal year 2013 from $620 in fiscal year 2012. The

increase was primarily due to favorable changes in working capital, driven by

lower tax payments in fiscal year 2013 as a result of favorable tax settlements;

the prior year settlement of interest rate forward contracts; and higher

earnings.

Net cash provided by continuing operations

decreased to $620 in fiscal year 2012 from $690 in fiscal year 2011. The

decrease was primarily due to lower tax payments in fiscal year 2011, resulting

from favorable tax depreciation rules and the timing of tax payments in the

current year; and the settlement of interest rate forward contracts.

Investing Activities

Capital expenditures were $194, $192 and

$228, respectively, in fiscal years 2013, 2012 and 2011. Capital spending as a

percentage of net sales was 3.5%, 3.5% and 4.4% for fiscal years 2013, 2012 and

2011, respectively. The increase in fiscal year 2013 capital spending was driven

by investments in the Company’s new Pleasanton, Calif. facility. The decrease in

fiscal year 2012 capital spending was primarily associated with higher spending

for manufacturing efficiencies in the prior fiscal year.

In fiscal year 2013, the Company completed

sale-leaseback transactions under which it sold its general office building in

Oakland, Calif. and former Technical and Data Center in Pleasanton, Calif. to

unrelated parties for combined net proceeds of $135. The Company entered into

operating lease agreements with the respective buyers for portions of the

buildings for up to 15 years, all of which contain renewal options.

In December 2011, the Company acquired

HealthLink, Aplicare, Inc. and Soy Vay Enterprises, Inc., including each

business’ workforce, for purchase prices aggregating $97, funded through

commercial paper borrowings. The cash amount paid of $93 represents the

aggregate purchase prices less cash acquired. Results for HealthLink and

Aplicare, Inc., providers of infection control products for the health care

industry, are reflected in the Cleaning reportable segment. Results for Soy Vay

Enterprises, Inc., a California-based operation that provides the Company a

presence in the market for Asian sauces, are reflected in the Lifestyle

reportable segment. These acquisitions added a modest benefit of approximately

1% to the Company’s net sales and volume, respectively, for the fiscal years

ended June 30, 2013 and 2012.

In fiscal year 2011, investing activities

included $747 of proceeds from the sale of the Auto Businesses, net of

transaction costs.

Financing Activities

Capital Resources and

Liquidity

Net cash used for financing activities was

$685 in fiscal year 2013, as compared to $321 in fiscal year 2012. The change

was primarily due to a reduction in total debt and higher dividends paid during

fiscal year 2013, partially offset by fewer share repurchases and an increase in

employee stock option exercises.

Net cash used for financing activities was

$321 in fiscal year 2012, as compared to $1,078 in fiscal year 2011. The

decrease in net cash used for financing activities was primarily due to the use

of proceeds from the sale of the Auto Businesses to repay commercial paper in

fiscal year 2011.

In March 2013, $500 in senior notes with

an annual fixed interest rate of 5.00% became due and were repaid. The repayment

was funded in part with commercial paper borrowings and in part with a portion

of the proceeds from the sale-leaseback transaction of the Company’s Oakland,

Calif. general office building.

12

In October 2012, $350 in senior notes with

an annual fixed interest rate of 5.45% became due and were repaid. The repayment

was funded with a portion of the proceeds from the September 2012 issuance of

$600 in senior notes with an annual fixed interest rate of 3.05%, payable

semi-annually in March and September, and a maturity date of September 15, 2022.

The remaining proceeds from notes were used to repay commercial

paper.

In November 2011, the Company issued $300

in senior notes with an annual fixed interest rate of 3.80%, payable

semi-annually in May and November, and a maturity date of November 15, 2021.

Proceeds from the notes were used to repay commercial paper.

The senior notes issued in September 2012

and November 2011 rank equally and ratably in right of payment with all of the

Company’s existing and future senior unsecured indebtedness and senior to any

future subordinated unsecured indebtedness. These notes were issued under the

Company’s shelf registration statement filed in November 2011, which allows the

Company to offer and sell an unlimited amount of its senior unsecured

indebtedness from time to time and expires in November 2014.

In fiscal year 2011, $300 in senior notes

became due and were repaid. The Company funded the debt repayments with

commercial paper borrowings and operating cash flows.

Credit Arrangements

As of June 30, 2013, the Company had a

$1.1 billion revolving credit agreement with an expiration date of May 2017.

There were no borrowings under the agreement, and the Company believes that

borrowings under the revolving credit agreement are and will continue to be

available for general corporate purposes. The agreement includes certain

restrictive covenants and limitations. The primary restrictive covenant is a

maximum ratio of total debt to earnings before interest, taxes, depreciation and

amortization (EBITDA) for the trailing four quarters (EBITDA ratio), as defined

in the Company’s revolving credit agreement, of 3.50. The following table sets

forth the calculation of the EBITDA ratio as of June 30, using EBITDA for the

trailing four quarters, as contractually defined:

|

|

2013 |

|

2012 |

| Earnings from continuing

operations |

|

$ |

574 |

|

$ |

543 |

| Add back: |

|

|

|

|

|

|

| Interest

expense |

|

|

122 |

|

|

125 |

| Income tax

expense |

|

|

279 |

|

|

248 |

| Depreciation and

amortization |

|

|

182 |

|

|

178 |

| Deduct: |

|

|

|

|

|

|

| Interest

income |

|

|

3 |

|

|

3 |

| EBITDA |

|

$ |

1,154 |

|

$ |

1,091 |

| Total debt |

|

$ |

2,372 |

|

$ |

2,721 |

| EBITDA ratio |

|

|

2.06 |

|

|

2.49 |

The Company is in compliance with all

restrictive covenants and limitations in the credit agreement as of June 30,

2013, and anticipates being in compliance with all restrictive covenants for the

foreseeable future. The Company continues to monitor the financial markets and

assess its ability to fully draw on its revolving credit agreement, and

currently expects that any drawing on the agreement will be fully

funded.

The Company had $45 of foreign and other

credit lines as of June 30, 2013, of which $3 was outstanding and $42 was

available for borrowing.

13

Based on the Company’s working capital

requirements, anticipated ability to generate positive cash flows from

operations in the future, investment-grade credit ratings, demonstrated access

to long- and short-term credit markets and current borrowing availability under

credit agreements, the Company believes it will have the funds necessary to meet

its financing requirements and other fixed obligations as they become due.

Should the Company undertake other transactions requiring funds in excess of its

current cash levels and available credit lines, it would consider the issuance

of additional debt or other securities to finance acquisitions, repurchase

shares, refinance debt or fund other activities for general business purposes.

The Company’s access to or cost of such additional funds could be adversely

affected by any decrease in credit ratings, which were the following as of June

30:

|

|

2013 |

|

2012 |

|

|

Short-term |

|

Long-term |

|

Short-term |

|

Long-term |

| Standard and

Poor’s |

|

A-2 |

|

BBB+ |

|

A-2 |

|

BBB+ |

| Moody’s |

|

P-2 |

|

Baa1 |

|

P-2 |

|

Baa1 |

Share Repurchases and Dividend

Payments

On May 13, 2013, the Company’s board of

directors terminated the share repurchase programs previously authorized on May

13, 2008 and May 18, 2011, and authorized a share repurchase program for an

aggregate purchase amount of up to $750. This reduces the total dollar value of

shares that the Company can repurchase under its open market share repurchase

program from $821 to $750. This open market share repurchase program is in

addition to the Company’s evergreen repurchase program (Evergreen Program), the

purpose of which is to offset the impact of share dilution related to

share-based awards. The Evergreen Program has no authorization limit as to

amount or timing of repurchases.

Share repurchases under authorized

programs were as follows during the fiscal years ended June 30:

|

|

2013 |

|

2012 |

|

2011 |

|

|

Amount |

|

Shares

(000) |

|

Amount |

|

Shares

(000) |

|

Amount |

|

Shares

(000) |

| Open-market purchase

programs |

|

$ |

- |

|

- |

|

$ |

158 |

|

2,429 |

|

$ |

521 |

|

7,654 |

| Evergreen Program |

|

|

128 |

|

1,500 |

|

|

67 |

|

990 |

|

|

134 |

|

2,122 |

| Total |

|

$ |

128 |

|

1,500 |

|

$ |

225 |

|

3,419 |

|

$ |

655 |

|

9,776 |

During fiscal years 2013, 2012 and 2011,

the Company declared dividends per share of $2.63, $2.44 and $2.25,

respectively. During fiscal years 2013, 2012 and 2011, the Company paid

dividends per share of $2.56, $2.40 and $2.20, respectively, equivalent to $335,

$315 and $303, respectively.

Contractual

Obligations

The Company had contractual obligations as

of June 30, 2013, payable or maturing in the following fiscal years:

|

|

2014 |

|

2015 |

|

2016 |

|

2017 |

|

2018 |

|

Thereafter |

|

Total |

Long-term debt maturities including

interest

payments (See

Note 9) |

|

$ |

93 |

|

$ |

668 |

|

$ |

359 |

|

$ |

53 |

|

$ |

442 |

|

$ |

1,022 |

|

$ |

2,637 |

| Notes and loans payable (See Note

9) |

|

|

202 |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

202 |

| Purchase obligations

(1) |

|

|

357 |

|

|

141 |

|

|

62 |

|

|

46 |

|

|

41 |

|

|

24 |

|

|

671 |

| Operating leases (See Note 16) |

|

|

45 |

|

|

38 |

|

|

36 |

|

|

33 |

|

|

29 |

|

|

117 |

|

|

298 |

Contributions to non-qualified

supplemental

postretirement

plans (2) |

|

|

17 |

|

|

15 |

|

|

15 |

|

|

17 |

|

|

17 |

|

|

76 |

|

|

157 |

| Venture Agreement terminal obligation (See

Note 11) |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

- |

|

|

284 |

|

|

284 |

| Total |

|

$ |

714 |

|

$ |

862 |

|

$ |

472 |

|

$ |

149 |

|

$ |

529 |

|

$ |

1,523 |

|

$ |

4,249 |

14

| (1) |

|

Purchase obligations are defined

as purchase agreements that are enforceable and legally binding and that

contain specified or determinable significant terms, including quantity,

price and the approximate timing of the transaction. For purchase

obligations subject to variable price and/or quantity provisions, an

estimate of the price and/or quantity has been made. Examples of the

Company’s purchase obligations include contracts to purchase raw

materials, commitments to contract manufacturers, commitments for

information technology and related services, advertising contracts,

utility agreements, capital expenditure agreements, software acquisition

and license commitments, and service contracts. Approximately 19% of the

Company’s purchase obligations relate to service contracts for information

technology that have been outsourced. The raw material contracts included

above are entered into during the regular course of business based on

expectations of future purchases. Many of these raw material contracts are

flexible to allow for changes in the Company’s business and related

requirements. If such changes were to occur, the Company believes its

exposure could differ from the amounts listed above. Any amounts reflected

in the consolidated balance sheets as accounts payable and accrued

liabilities are excluded from the table above. |

| (2) |

|

Represents expected payments

through 2023. Based on the accounting rules for retirement and

postretirement benefit plans, the liabilities reflected in the Company’s

consolidated balance sheets differ from these expected future payments

(see Note 19 of the Notes to Consolidated Financial

Statements). |

As of June 30, 2013, the liability

recorded for uncertain tax positions, excluding associated interest and

penalties, was approximately $69. In the twelve months succeeding June 30, 2013,

audit resolutions could potentially reduce total unrecognized tax benefits by up

to $2, primarily as a result of cash settlement payments. Since the ultimate

amount and timing of further cash settlements cannot be predicted due to the

high degree of uncertainty, liabilities for uncertain tax positions are excluded

from the contractual obligations table (see Note 18 of the Notes to Consolidated

Financial Statements).

Off-Balance Sheet

Arrangements

In conjunction with divestitures and other

transactions, the Company may provide typical indemnifications (e.g.,

indemnifications for representations and warranties and retention of previously

existing environmental, tax and employee liabilities) that have terms that vary

in duration and in the potential amount of the total obligation and, in many

circumstances, are not explicitly defined. The Company has not made, nor does it

believe that it is probable that it will make, any payments relating to its

indemnifications, and believes that any reasonably possible payments would not

have a material adverse effect, individually or in the aggregate, on the

Company’s consolidated financial statements taken as a whole.

As of June 30, 2013, the Company was a

party to a letter of credit of $14, related to one of its insurance carriers, of

which $0 had been drawn upon.

The Company had not recorded any

liabilities on any of the aforementioned guarantees as of June 30,

2013.

CONTINGENCIES

The Company is involved in certain

environmental matters, including response actions at various locations. The

Company had a recorded liability of $13 and $14 as of June 30, 2013 and 2012,

respectively, for its share of aggregate future remediation costs related to

these matters. One matter in Dickinson County, Michigan, for which the Company

is jointly and severally liable, accounted for a substantial majority of the

recorded liability as of both June 30, 2013 and 2012. The Company has agreed to

be liable for 24.3% of the aggregate remediation and associated costs for this

matter pursuant to a cost-sharing arrangement with a third party. With the

assistance of environmental consultants, the Company maintains an undiscounted

liability representing its current best estimate of its share of the capital

expenditures, maintenance and other costs that may be incurred over an estimated

30-year remediation period. Currently, the Company cannot accurately predict the

timing of future payments that may be made under this obligation. In addition,

the Company’s estimated loss exposure is sensitive to a variety of uncertain

factors, including the efficacy of remediation efforts, changes in remediation

requirements and the future availability of alternative clean-up technologies.

Although it is reasonably possible that the Company’s exposure may exceed the

amount recorded, any amount of such additional exposures, or range of exposures,

is not estimable at this time.

15

In October 2012, a Brazilian appellate

court issued an adverse decision in a lawsuit pending in Brazil against the

Company and one of its wholly-owned subsidiaries, The Glad Products Company

(Glad). The lawsuit was initially filed in a Brazilian lower court in 2002 by

two Brazilian companies and one Uruguayan company (collectively Petroplus)

related to joint venture agreements for the distribution of STP auto-care

products in Brazil with three companies that became subsidiaries of the Company

as a result of the Company’s merger with First Brands Corporation in January

1999 (collectively, Clorox Subsidiaries). The pending lawsuit seeks

indemnification for damages and losses for alleged breaches of the joint venture

agreements and abuse of economic power by the Company and Glad. Petroplus had

previously unsuccessfully raised the same claims and sought damages from the

Company and the Clorox Subsidiaries in an International Chamber of Commerce

(ICC) arbitration proceeding in Miami filed in 2001. The ICC arbitration panel

unanimously ruled against Petroplus in a final decision in November 2003 (Final

ICC Arbitration Award). The Final ICC Arbitration Award was ratified by the

Superior Court of Justice of Brazil in May 2007 (Foreign Judgment), and the

United States District Court for the Southern District of Florida subsequently

confirmed the Final ICC Arbitration Award and recognized and adopted the Foreign

Judgment as a judgment of the United States District Court for the Southern

District of Florida (U.S. Judgment). Despite this, in March 2008 a Brazilian

lower court ruled against the Company and Glad in the pending lawsuit and

awarded Petroplus R$23 ($13) plus interest. The value of that judgment,

including interest and foreign exchange fluctuations as of June 30, 2013, was

approximately $35.

Among other defenses, because the Final

ICC Arbitration Award, the Foreign Judgment and the U.S. Judgment relate to the

same claims as those in the pending lawsuit, the Company believes that Petroplus

is precluded from re-litigating these claims. Based on the unfavorable appellate

court decision, the Company believes that it is reasonably possible that a loss

could be incurred in this matter in excess of amounts accrued, and that the

estimated range of such loss in this matter is from $0 to $29. The Company

continues to believe that its defenses are meritorious, and has appealed the

decision to the highest courts of Brazil, which could take years to resolve.

Expenses related to this litigation and any potential additional loss would be

reflected in discontinued operations, consistent with the Company’s

classification of expenses related to its discontinued Brazil operations.

In a separate action filed in 2004 by

Petroplus, a lower Brazilian court in January 2013 nullified the Final ICC

Arbitration Award. The Company believes this judgment is inconsistent with the

Foreign Judgment and the U.S. Judgment and that it is without merit. The Company

has appealed this decision.

Glad and the Clorox Subsidiaries have also

filed separate lawsuits against Petroplus alleging misuse of the STP trademark

and related matters, which are currently pending before Brazilian courts, and

have taken other legal actions against Petroplus, which are pending.

The Company is subject to various other

lawsuits and claims relating to issues such as contract disputes, product

liability, patents and trademarks, advertising, and employee and other matters.

Based on management’s analysis of these claims and litigation, it is the opinion

of management that the ultimate disposition of these matters, to the extent not

previously provided for, will not have a material adverse effect, individually

or in the aggregate, on the Company’s consolidated financial statements taken as

a whole.

QUANTITATIVE AND QUALITATIVE

DISCLOSURES ABOUT MARKET RISK

As a multinational company, the Company is

exposed to the impact of foreign currency fluctuations, changes in commodity

prices, interest-rate risk and other types of market risk.

In the normal course of business, where

available at a reasonable cost, the Company manages its exposure to market risk

using contractual agreements and a variety of derivative instruments. The

Company’s objective in managing its exposure to market risk is to limit the

impact of fluctuations on earnings and cash flow through the use of swaps,

forward purchases and futures contracts. Derivative contracts are entered into

for non-trading purposes with major credit-worthy institutions, thereby

decreasing the risk of credit loss.

The Company uses different methodologies,

when necessary, to estimate the fair value of its derivative contracts. The

estimated fair values of the majority of the Company’s contracts are based on

quoted market prices, traded exchange market prices, or broker price quotations,

and represent the estimated amounts that the Company would pay or receive to

terminate the contracts.

16

Sensitivity Analysis for Derivative

Contracts

For fiscal years 2013 and 2012, the

Company’s exposure to market risk was estimated using sensitivity analyses,

which illustrate the change in the fair value of a derivative financial

instrument assuming hypothetical changes in foreign exchange rates, commodity

prices or interest rates. The results of the sensitivity analyses for foreign

currency derivative contracts, commodity derivative contracts and interest rate

contracts are summarized below. Actual changes in foreign exchange rates,

commodity prices or interest rates may differ from the hypothetical changes, and

any changes in the fair value of the contracts, real or hypothetical, would be

partly to fully offset by an inverse change in the value of the underlying

hedged items.

The changes in the fair value of

derivatives are recorded as either assets or liabilities in the consolidated

balance sheets with an offset to net earnings or other comprehensive income,

depending on whether or not, for accounting purposes, the derivative is

designated and qualified as a cash flow hedge. During the fiscal years ended

June 30, 2013, 2012 and 2011, the Company had no hedging instruments designated

as fair value hedges. In the event the Company has contracts not designated as

hedges for accounting purposes, the Company recognizes the changes in the fair

value of these contracts in other (income) expense, net.

Foreign Currency

Risk

The Company seeks to minimize the impact

of certain foreign currency fluctuations by hedging transactional exposures with

foreign currency forward contracts. As of June 30, 2013, the Company’s foreign

currency transactional exposures pertaining to derivative contracts existed with

the Canadian, Australian and New Zealand dollars. As of June 30, 2012, the

Company’s foreign-currency transactional exposure pertaining to derivative

contracts existed with the Canadian dollar. Based on a hypothetical decrease or

increase of 10% in the value of the U.S. dollar against the Canadian,

Australian, and New Zealand dollars as of June 30, 2013, the estimated fair

value of the Company’s then-existing foreign currency derivative contracts would

decrease or increase by $4, with the corresponding impact included in

accumulated other comprehensive net losses. Based on a hypothetical decrease or

increase of 10% in the value of the U.S. dollar against the Canadian dollar as