UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

OR

For fiscal year ended

OR

OR

Date of event requiring this shell company report______________

For the transition period from __________ to ___________

Commission file number

(Exact name of the Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

Guangdong Province,

Tel: +86-020-28381666

(Address of principal executive offices)

Guangdong Province,

Tel: +86-

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of each exchange on which registered | |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

N/A

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each

of the Issuer’s classes of capital or ordinary shares as of the close of the period covered by the annual report:

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒

If this report is an annual or transition report,

indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act

of 1934. ☐ Yes ☒

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. ☒

Indicate by check mark whether the registrant

has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted

pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit and post such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer.

| ☐ | Large Accelerated filer | ☐ | Accelerated filer |

| ☒ | | Emerging growth company |

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | ☐ International Financial | ☐ Other |

| Reporting Standards as issued by | ||

| the International Accounting | ||

| Standards Board |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

Table of Contents

i

INTRODUCTION

Unless otherwise indicated and except where the context otherwise requires, references in this annual report on Form 20-F to:

| ● | “ADS(s)” refers to our American depositary share(s), each ADS representing 1.5 ordinary shares; |

| ● | “assets under management” or “AUM” refers to the net asset value of funds we manage under our asset management services, for which we are entitled to management fees and performance-based carried interest; |

| ● | “China” or the “PRC” refers to the People’s Republic of China, excluding, for the purpose of this annual report only, the Hong Kong Special Administrative Region, Macau Special Administrative Region and Taiwan; |

| ● | “EIT” refers to PRC enterprise income tax; |

| ● | “emerging middle class population” refers to individuals in China with investable assets of between RMB30,000 and RMB600,000; |

| ● | “FoF(s)” refers to fund(s) of funds; |

| ● | “MOFCOM” refers to the Ministry of Commerce of the PRC; |

| ● | “affluent population” refers to individuals in China with investable assets of between RMB600,000 and RMB6 million; |

| ● | “NASDAQ” refers to the NASDAQ Global Market; |

| ● | “NPL(s)” refers to non-performing loan(s); |

| ● | “ordinary shares” refers to our ordinary shares, par value US$0.001 per share; |

| ● | “PIPE” refers to private investment in public equity; |

| ● |

“Puyi,” “we,” “us,” “our company,” “our group” and “our” refer to Puyi Inc. and its subsidiaries and consolidated entities; |

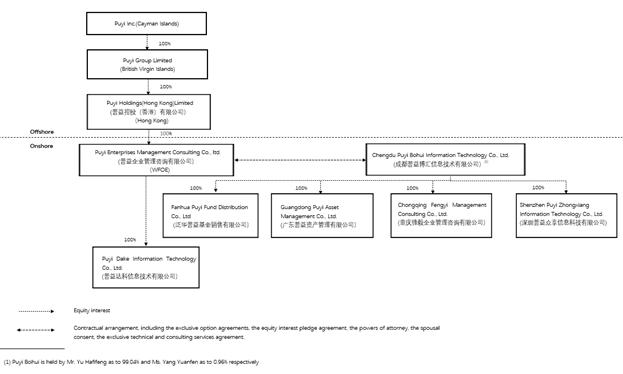

| ● | “Puyi Consulting” or “WFOE” refers to Puyi Enterprises Management Consulting Co., Ltd. (普益企业管理咨询有限公司), which was incorporated as our wholly foreign-owned subsidiary in Chengdu, Sichuan, PRC in August 2018; |

| ● | “QDII” refers to Qualified Domestic Institutional Investor; |

| ● | “RMB” and “Renminbi” refer to the legal currency of China; |

| ● | “SAFE” refers to the State Administration of Foreign Exchange of China; |

| ● | “transaction value” refers to the aggregate value of the wealth management products we distribute through our wealth management business during a given period; |

| ● | “TMT” refers to the telecommunications, media and technology; |

| ● | “US$,” “U.S. dollars,” “$” and “dollars” refer to the legal currency of the United States; and |

| ● | “VIE(s)” refers to variable interest entity(ies). |

Our reporting currency is the Renminbi because our business is mainly conducted in China and a substantial majority of our revenues is denominated in Renminbi. This annual report contains translations of Renminbi amounts into U.S. dollars at specific rates solely for the convenience of the reader. The conversion of Renminbi into U.S. dollars in this annual report is based on the exchange rate set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. Unless otherwise noted, all translations from Renminbi to U.S. dollars and from U.S. dollars to Renminbi in this annual report were made at a rate of RMB6.4566 to US$1.00, the exchange rate on June 30, 2021 set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange and through restrictions on foreign trade.

ii

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements that involve risks and uncertainties. All statements other than statements of historical facts are forward-looking statements. Known and unknown risks, uncertainties and other factors, including those listed under “Risk Factors,” may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements.

You can identify some of these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “likely to” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements relate to, among others:

| ● | our goals and strategies; |

| ● | our future business development, financial condition and results of operations; |

| ● | the expected growth of the industries in which we operate; |

| ● | our expectations regarding demand for and market acceptance of the products and services we distribute, manage or offer; |

| ● | our expectations regarding keeping and strengthening our relationships with product providers; |

| ● | relevant government policies and regulations relating to the industries in which we operate; |

| ● | our ability to attract and retain qualified employees; |

| ● | our ability to stay abreast of market trends and technological advances; |

| ● | our plans to invest in research and development to enhance our product choices and service offerings; |

| ● | competition in the industries in which we operate; |

| ● | general economic and business conditions in China and internationally; |

| ● | other conditions affecting our business, including the international trade tension and the COVID-19 pandemic; |

| ● | our ability to obtain certain licenses and permits necessary to operate and expand our businesses; and |

| ● | our ability to effectively protect our intellectual property rights and not infringe on the intellectual property rights of others. |

iii

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable

ITEM 3. KEY INFORMATION

A. Selected Financial Data

The following selected consolidated financial data as of June 30, 2020 and 2021 and for the years ended June 30, 2019, 2020 and 2021 have been derived from our audited consolidated financial statements included in this annual report beginning on page F-1. The financial data as of June 30, 2019 is included in the 2020 annual report of the group.

The selected financial data should be read in conjunction with our consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” included elsewhere in this annual report. The consolidated financial statements have been prepared and presented in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). Our historical results are not necessarily indicative of our results for any future periods. See “Item 3. Key Information — D. Risk Factors” in this annual report.

Selected Consolidated Statements of Operations and Comprehensive Income (Loss)

| For the year ended June 30, | ||||||||||||||||

| 2019 | 2020 | 2021 | ||||||||||||||

| RMB | RMB | RMB | US$ | |||||||||||||

| (in thousands) | ||||||||||||||||

| Net revenues: | ||||||||||||||||

| Wealth management services | 193,082 | 106,444 | 176,589 | 27,350 | ||||||||||||

| Corporate financing services | 6,271 | 6 | - | - | ||||||||||||

| Asset management services | 2,767 | 23,033 | 13,464 | 2,085 | ||||||||||||

| Information technology services and others | 1,111 | - | 1,147 | 178 | ||||||||||||

| Total net revenues | 203,231 | 129,483 | 191,200 | 29,613 | ||||||||||||

| Operating costs and expenses: | ||||||||||||||||

| Cost of sales | (31,092 | ) | (31,759 | ) | (44,043 | ) | (6,821 | ) | ||||||||

| Selling expenses | (67,487 | ) | (84,074 | ) | (130,145 | ) | (20,157 | ) | ||||||||

| General and administrative expenses | (48,572 | ) | (67,174 | ) | (90,194 | ) | (13,969 | ) | ||||||||

| Total operating costs and expenses | (147,151 | ) | (183,007 | ) | (264,382 | ) | (40,947 | ) | ||||||||

| Income (loss) from operations | 56,080 | (53,524 | ) | (73,182 | ) | (11,334 | ) | |||||||||

| Other income, net: | ||||||||||||||||

| Investment income | 172 | 1,499 | 1,899 | 294 | ||||||||||||

| Interest income | 5,956 | 11,003 | 10,919 | 1,691 | ||||||||||||

| Interest expenses | (1,048 | ) | - | - | - | |||||||||||

| Sundry income, net | 259 | 5,077 | 4,690 | 726 | ||||||||||||

| Income (loss) before income taxes | 61,419 | (35,945 | ) | (55,674 | ) | (8,623 | ) | |||||||||

| Income tax (expense) benefit | (9,396 | ) | 2,394 | 9,608 | 1,488 | |||||||||||

| Net income (loss) | 52,023 | (33,551 | ) | (46,066 | ) | (7,135 | ) | |||||||||

| less: net income (loss) attributable to non-controlling interests | (1,508 | ) | (648 | ) | 304 | 47 | ||||||||||

| Net income (loss) attributable to Puyi Inc.’s shareholders | 53,531 | (32,903 | ) | (46,370 | ) | (7,182 | ) | |||||||||

| Net income (loss) per share: | ||||||||||||||||

| Basic and diluted | 0.630 | (0.364 | ) | (0.513 | ) | (0.079 | ) | |||||||||

| Net income (loss) per ADS: | ||||||||||||||||

| Basic and diluted | 0.945 | (0.546 | ) | (0.770 | ) | (0.119 | ) | |||||||||

| Weighted average number of shares used in computation: | ||||||||||||||||

| Basic and diluted | 84,997,628 | 90,472,014 | 90,472,014 | 90,472,014 | ||||||||||||

| Net income (loss) | 52,023 | (33,551 | ) | (46,066 | ) | (7,135 | ) | |||||||||

| Other comprehensive income (loss), net of tax: Foreign currency translation adjustments | 11 | 456 | (1,277 | ) | (198 | ) | ||||||||||

| Total comprehensive income (loss) | 52,034 | (33,095 | ) | (47,343 | ) | (7,333 | ) | |||||||||

| Less: Comprehensive income (loss) attributable to the non-controlling interests | (1,508 | ) | (648 | ) | 304 | 47 | ||||||||||

| Comprehensive income (loss) attributable to Puyi Inc.’s shareholders | 53,542 | (32,447 | ) | (47,647 | ) | (7,380 | ) | |||||||||

1

Selected Consolidated Statements of Financial Position

| As of June 30, | ||||||||||||||||

| 2019 | 2020 | 2021 | ||||||||||||||

| RMB | RMB | RMB | US$ | |||||||||||||

| (in thousands) | ||||||||||||||||

| Total current assets | 467,124 | 393,222 | 403,326 | 62,467 | ||||||||||||

| Total assets | 479,409 | 432,711 | 467,903 | 72,469 | ||||||||||||

| Total current liabilities | 75,833 | 47,521 | 130,292 | 20,180 | ||||||||||||

| Total liabilities | 75,833 | 62,230 | 147,602 | 22,861 | ||||||||||||

| Total equity interest attributable to the company | 400,403 | 367,956 | 320,301 | 49,608 | ||||||||||||

| Non-controlling interests | 3,173 | 2,525 | - | - | ||||||||||||

Selected Consolidated Statements of Cash Flows:

| For the year ended June 30, | ||||||||||||||||

| 2019 | 2020 | 2021 | ||||||||||||||

| RMB | RMB | RMB | US$ | |||||||||||||

| (in thousands) | ||||||||||||||||

| Net cash provided by (used in) operating activities | 98,040 | (88,749 | ) | (2,825 | ) | (438 | ) | |||||||||

| Net cash provided by (used in) investing activities | 62,539 | (53,081 | ) | 47,990 | 7,433 | |||||||||||

| Net cash provided by financing activities | 155,262 | - | - | - | ||||||||||||

| Net increase (decrease) in cash and cash equivalents, and restricted cash | 315,841 | (141,830 | ) | 45,165 | 6,995 | |||||||||||

| Cash and cash equivalents, and restricted cash at beginning of year | 112,000 | 430,268 | 288,894 | 44,744 | ||||||||||||

| Cash and cash equivalents, and restricted cash at end of year | 430,268 | 288,894 | 332,782 | 51,541 | ||||||||||||

B. Capitalization and Indebtedness

Not applicable

C. Reasons for the Offer and Use of Proceeds

Not applicable

D. Risk Factors

Risks Related to Our Business and Industry

The wealth management products that we distribute involve various risks and our failure to identify or fully appreciate such risks will negatively affect our reputation, client relationships, operations and prospects.

Under our wealth management services, we distribute a broad variety of wealth management products. The products we distribute can be divided into publicly raised fund products and privately raised fund products. These products often have different structures and involve various risks, including default risks, interest risks, liquidity risks and other risks. Our success in distributing these products depends, in part, on our successful identification and full appreciation of risks associated with such products. Not only must we keep pace with third-party wealth management product providers and prudently select products, but we must also accurately describe the products to, and evaluate them for, our clients. Although we seek to implement strict risk management policies and procedures, they may not be fully effective in mitigating the risk exposure of our clients in all market environments or against all types of risks. Moreover, our clients could experience losses on raised capital as a result of poor investment performance by our distributed funds. In addition, in the event that any of the distributed funds under our management were to perform poorly, it would be more difficult for us to raise new capital. If we fail to identify and fully appreciate any of the aforementioned risks associated with products we distribute to our clients, or fail to disclose such risks to our clients, and as a result our clients suffer financial loss or other damages resulting from their purchase of the wealth management products following our wealth management and product recommendations and services, our reputation, client relationships, business and prospects will be materially and adversely affected.

2

If we fail to maintain or renew existing licenses or to obtain additional licenses and permits necessary to conduct our operations in China pursuant to applicable laws and regulations from time to time governing our operations, we may be subject to limitations or uncertainties with respect to our business activities and render our operations non-compliant, and our business would be materially and adversely affected.

China’s wealth management marketplace is a relatively new and evolving industry, and the laws and regulations governing our services are still developing. There are substantial uncertainties as to the legal system and the interpretation and implementation of the PRC laws and regulations applicable to the wealth management industry. The PRC government has adopted a unified regulatory framework governing the distribution and management of fund products. Under the Measures for the Supervision and Administration of Distributors of Publicly Offered Securities Investment Funds which was promulgated by the China Securities Regulatory Commission (the “CSRC”) on August 28, 2020 and effective on October 1, 2020 (the “Distributor Measures”), a license is required for the distribution of standardized products, including publicly raised fund products and privately raised securities investment fund products. See “Item 4. K Information on the Company — B. Business Overview — Regulations”. Fanhua Puyi has obtained a fund distribution license from the CSRC and we entered into a majority of fund distribution agreements with fund managers through this subsidiary.

In addition, fund managers managing privately raised funds are required to register with the Asset Management Association of China (“AMAC”); unregistered individuals or institutions are not permitted to conduct securities investment activities under the names of “funds” or “fund management.” To comply with PRC laws, we currently collaborate with licensed fund managers and structure our fund management services as providing services to them. Neither the fund management services under service agreements with fund managers, nor our service fees generated from such agreements are prohibited by the applicable laws and regulations. However, we cannot assure you that the relevant PRC government will agree with our interpretation of the relevant laws and regulations. If the PRC government interprets the relevant rules differently and deems our role in such arrangements as requiring the fund management license, it may order us to cease our provision of fund management services until we acquire the fund management license. We cannot assure you that we will be able to obtain the fund management license promptly, if at all, and any failure to do so would require us to permanently cease such services, which may materially and adversely affect our business.

As the wealth management services industry in China is at an early stage of development, new laws and regulations applicable to our business may be adopted to address new issues that arise from time to time or to require additional licenses and permits for distribution of products other than funds, such as asset management plans issued by security companies or insurance companies. As a result, substantial uncertainties exist regarding the evolution of the regulatory system and the interpretation and implementation of current and any future Chinese laws and regulations applicable to the wealth management services industry.

We cannot assure you that we will be able to maintain our existing licenses and permits, renew any of them when their current term expires or obtain additional licenses required for our future business expansion. If we are unable to maintain and renew one or more of our current licenses and permits, or obtain such renewals or additional licenses required for our future business expansion on commercially reasonable terms, our operations and prospects could be materially disrupted. Moreover, new PRC regulations promulgated in the future may require that we obtain additional licenses or permits in order to continue to conduct our business operations and we cannot assure you that we would be able to obtain such licenses or permits in a timely fashion, or at all. If any of the foregoing were to occur, our business, financial condition and prospects would be materially and adversely affected.

3

We may not be able to continue to retain or expand our primary target client base of the affluent and emerging middle class population or maintain or increase the amount of investments made by our primary clients in the products we distribute.

Our target client base is China’s large population of affluent and emerging middle class individuals. In light of China’s rapidly-evolving wealth management industry, we cannot assure you that we will be able to maintain or increase the number of our clients or that our existing clients will maintain the same level of investment in the wealth management products that we distribute. As China’s wealth management industry is at an early stage of development and is currently highly fragmented, we face competition from numerous types of market players including commercial banks and their wealth management subsidiaries, non-bank traditional financial institutions and online-based service providers. Moreover, many of our existing and future competitors may be better equipped or adopt better sales and marketing tactics directed toward our target clients, and may capture market opportunities to grow their client bases more effectively compared to us. In addition, the evolving regulatory landscape of China’s financial service industry may not affect us and our competitors proportionately with respect to the ability to maintain or grow our client base, and may lose our leading position if we fail to maintain or further grow our client base at the same pace as our competitors. A decrease in the number of our clients or a decrease in their spending on the products that we distribute may reduce revenues derived from our wealth management services and our asset management services. If we fail to continue to meet our clients’ expectations on the returns from the products we distribute or manage or if they are no longer satisfied with our services, they may leave us for our competitors and our reputation may be damaged by these clients, which may, in turn, adversely affect our business, financial condition, results of operations and ability to attract new clients.

If we are required to obtain ICP licenses for the operation of our apps, we may not be able to offer relevant information and transaction processing services and our business and operations may be negatively affected.

We have launched two mobile apps; one is “Puyi Fund” (普益基金), which enables our clients to complete transactions online in relation to our fund products, and the other is “i Financial Planner” (i理财师), which provides seed clients (our repeat clients who also market our products or services to potential clients) with a one-stop online management tool and empowers our in-house financial advisors to provide better services. According to the Provisions on the Administration of Mobile Internet Application Information Services, or the App Provisions, issued by Cyberspace Administration of China on June 28, 2016, any owner or operator providing information services through a mobile internet application, or an “app,” must obtain the relevant qualification(s) as required by laws and regulations. The App Provisions, however, do not further clarify the scope of “information services,” nor do they specify what “relevant qualification(s)” that an app owner or operator must obtain. In practice, operational activities of a company conducted through an app is subject to the supervision of the local departments of the Information Communications Administration, and often, the local departments differentiate the operational activities conducted through websites and through apps. In many cases, standalone apps through which a company provides information services without any web-based online services are not required to obtain ICP licenses. However, the interpretation and enforcement of such laws and regulations are subject to the substantial discretion of the local authorities. Although we currently do not hold any ICP license, we cannot rule out the possibility that the local departments of the Information Communications Administration would take the view that the current primary information services and transaction processing services provided by us through the apps would require an ICP license or that, without such license, we would be prohibited from rendering such services. If we were required an ICP license for our apps, our inability to obtain the license in a timely manner or at all may have a material adverse effect on our business and operations.

If we fail to recruit and retain qualified seed clients and in-house financial advisors, our business could suffer.

We rely on our seed clients and in-house financial advisors to market our products or services to potential clients as well as to provide services to and to develop and maintain relationships with our existing clients. As we further grow our business and expand into new cities and regions, our need for high quality seed clients and financial advisors will increase. We have been actively recruiting and will continue to recruit qualified seed clients and financial advisors to join our coverage network. However, there is no assurance that we can recruit and retain a sufficient number of seed clients and financial advisors who meet our high quality requirements to support our further growth. In some of the branch offices that we have recently established or plan to establish, the pool from which we can recruit seed clients or financial advisors is smaller than in major economic centers such as Shanghai and Beijing. Even if we are able to recruit sufficient seed clients and financial advisors, we may need to incur significant training and administrative related expenses in order to prepare them to market our products or services, which would increase our operating costs and reduce our profitability. In addition, we pay service fees to our seed clients as returns. Although such fees are not prohibited by applicable laws and regulations, we cannot assure you that relevant authorities would not deem that our seed clients are distributing products on our behalf and prohibit such fee payment in the future. If so, we may be subject to fines and/or may be ordered to cease paying such fees to our seed clients, we may be unable to attract and retain highly productive seed clients, and our business could be materially and adversely affected.

4

We rely on highly qualified product providers that we collaborate with.

We view our collaborative relationships as a core asset for developing our wealth management business, product portfolios and professional networks. As of June 30, 2021, we sourced products from high quality third-party global product providers in China, including 61 public fund companies and three leading securities firms. These parties have contributed to a majority of our fund products, including approximately 3,264 publicly raised fund products. In addition, we actively seek collaborative opportunities with well-recognized fund managers to manage our FoFs, which allows us to deliver returns to our clients in a cost-effective manner. As such, our business is heavily dependent on our relationships with these third-party providers and, although we have maintained stable relationships with them, any material deterioration or termination of our relationships with any major product providers or fund managers, or the failure to further expand our network with such third-party products, could inhibit our ability to secure products or manage funds, which in turn would have a material adverse effect on our business, financial condition and growth prospects. In addition, a decline in the financial condition of one or more of our third-party product providers may expose us to credit losses or defaults, limit our access to liquidity or otherwise disrupt the operations of our businesses. Downgrades in the credit or financial strength ratings assigned to the counterparties with whom we collaborate or other adverse reputational impacts to such counterparties could create the perception that our financial condition will be adversely impacted as a result of potential future defaults by such counterparties, which could have a negative impact on our business and operating performance as well as on our clients’ confidence in us and our products.

A decline in the investment performance of products distributed or managed by us could negatively impact our revenues and profitability.

Investment performance is a key competitive factor for the products that we distribute and manage. Strong investment performance helps us to retain and expand our client base and to generate new sales of products and services, and is therefore an important element to our goals of maximizing the value of products and services provided to our clients and our AUM. There can be no assurance as to how our future investment performance will compare to our competitors or that our historical performance will be indicative of future returns. Any drop or perceived drop in investment performance as compared to our competitors could cause a decline in sales of our investment products and services, which may also reduce our aggregate AUM and management fees. Poor investment performance could also adversely affect our ability to expand the distribution of third-party wealth management products and our self-developed products.

In addition, the profitability of our growing asset management services depends on, among others, fees charged based on the AUM. Any impairment on the assets that we manage, whether caused by fluctuations or downturns in the underlying markets or otherwise, will reduce our revenues generated from asset management business, which in turn may materially and adversely affect our overall financial performance and results of operations.

Any material decrease in the fee rates for our services may have an adverse effect on our revenues, cash flow and results of operations.

We derive a majority of our revenues from distribution commissions and performance-based fees from wealth management services, and the management fees and carried interest from the funds that we manage. The relative fee rates are negotiated between us and third-party product providers or the investors and vary from product to product. Future fee rates may be subject to change based on the prevailing political, economic, regulatory, taxation and competitive factors that affect product providers or investors. These factors, which are not within our control, include the capacity of product providers to place new business and realize profits, client demand and preference for wealth management products, the availability of comparable products from other product providers at a lower cost and the availability of alternative wealth management products for clients. In addition, the historical volume of wealth management products that we have distributed or managed may have a significant impact on our bargaining power with third-party wealth management product providers in relation to the fee rates for future products. As we do not determine, and cannot predict, the timing or extent of fee rate changes with respect to our wealth management products and our fund management services, it is difficult for us to assess the potential effect of any of these changes on our operations. In order to maintain our relationships with our product providers and to enter into contracts for new products, we may have to accept lower distribution commission rates or other less favorable terms, which could reduce our revenues. Furthermore, as we continue to grow our asset management business, we may face similar risks in connection with the fee rates for the provision of related services.

5

We depend on a small number of third-party fund product providers to derive a substantial portion of our net revenues and this dependence is likely to continue.

We derive a substantial portion of our net revenues from a limited number of third-party fund product providers. For accounting purposes, we treat these third-party product providers as our customers under our wealth management services. For the years ended June 30, 2020 and 2021, we had three and two major third-party fund product providers, respectively, the net revenues generated from which individually accounted for more than 10% of our total net revenues, and collectively accounted for 59.8% and 79.5% of our total net revenues, respectively. If we lose any of our major third-party fund product providers or any of these major third-party fund product providers significantly reduces its volume of business with us, and we are unable to seek alternative third-party fund product providers on a timely basis, or at all, our net revenues and profitability would be substantially reduced. In addition, the volume of products we source and distribute from specific third-party fund product providers may vary from period to period, particularly because we are not the exclusive distributor for any such particular product provider. Our high customer concentration may also adversely affect our ability to negotiate fee rates with these third-party fund product providers, which may in turn materially and adversely affect our results of operations.

Our risk management policies and procedures may not be fully effective in identifying or mitigating risk exposure in all market environments or against all types of risk, including employee and seed client misconduct.

We have devoted significant resources to developing our risk management policies and procedures and will continue to do so. Nonetheless, our ability to identify, monitor and manage risks may not be fully effective in mitigating our risk exposure in all market environments or against all types of risk. Many of our risk management policies and procedures are based upon observed historical market behavior or statistics based on historical models.

During periods of market volatility or due to unforeseen events, the historically derived correlations upon which these methods are based may not be valid. As a result, these methods may not predict future exposures accurately, which could be significantly greater than what our models indicate. This could cause us to incur investment losses or cause our hedging and other risk management strategies to be ineffective. Other risk management methods depend upon the evaluation of information regarding markets, clients, catastrophe occurrence, public health problems and pandemic, regulations, policies or other matters that are publicly available or otherwise accessible to us, which may not always be accurate, complete, up-to-date or properly evaluated.

Moreover, we are subject to the risks of error and misconduct by our employees and seed clients, including:

| ● | engaging in misrepresentation or fraudulent activities when marketing or distributing wealth management products to clients; |

| ● | improperly using or disclosing confidential information of our clients, third-party wealth management product providers or other parties; |

| ● | concealing unauthorized or unsuccessful activities; or |

| ● | otherwise not complying with laws and regulations or our internal policies or procedures. |

Although we have established an internal compliance system to supervise service quality and regulation compliance, these risks may be difficult to detect in advance and deter, and could harm our business, results of operations and financial performance.

In addition, although we perform due diligence on potential clients, we cannot assure you that we will be able to identify all the possible issues based on the information available to us. If certain investors do not meet the relevant qualification requirements for products we distribute or under applicable laws, we may also be deemed in default of the obligations required by law and in our contracts with our product providers. Management of operational, legal and regulatory risks requires, among other things, policies and procedures to properly record and verify a large number of transactions and events. In the event that our policies and procedures are not fully effective in mitigating our risk exposure in all market environments or against all types of risk, our business, financial condition and results of operations may be materially and adversely affected.

6

Our business is subject to risks related to lawsuits and other claims brought by our clients.

We are subject to lawsuits and other claims in the ordinary course of our business. Pursuant to the Minutes of the National Courts’ Civil and Commercial Trial Work Conference (the “Conference”) issued by the Supreme People’s Court on November 8, 2019, where the issuer or distributor of a financial product fails to fulfill its suitability obligation, leading to any loss to the financial consumer in the process of purchasing the financial product, the financial consumer may not only request the issuer of the financial product to bear the liability for compensation, but also request the distributor of the financial product to bear the liability for compensation jointly and severally. In particular, we may face arbitration claims and lawsuits brought by our clients who have bought wealth management products based on our recommendations which turned out to be unsuitable. We may also encounter complaints alleging misrepresentation on the part of our employees and seed clients or that we have failed to carry out a duty owed to them. This risk may be heightened during periods when credit, equity or other financial markets are deteriorating in value or are volatile, or when clients or investors are experiencing losses. Actions brought against us may result in settlements, awards, injunctions, fines, penalties or other results adverse to us, including harm to our reputation. Our contract with our third-party wealth management product providers do not provide for indemnification of our costs, damages or expenses resulting from such lawsuits. As such, even if we are successful in defending against these actions, the defense of such matters may result in our incurring significant expenses. Predicting the outcome of such matters is inherently difficult, particularly where claimants seek substantial or unspecified damages, or when arbitration or legal proceedings are at an early stage. A substantial judgment, award, settlement, fine or penalty could materially and adversely affect our operating results or cash flows for a particular future period, depending on our results for that period.

Our reputation and brand recognition are crucial to our business. Any harm to our reputation or failure to enhance our brand recognition may materially and adversely affect our business, financial condition and results of operations.

Our reputation and brand recognition, which primarily depend on earning and maintaining the trust and confidence of current or potential clients, are critical to our business. Our reputation and brand are vulnerable to many threats that can be difficult or impossible to control, as well as costly or impossible to remediate. Regulatory inquiries or investigations, lawsuits initiated by clients or other third parties, employee or seed client misconduct, perceptions of conflicts of interest and rumors, among other things, could substantially damage our reputation, even if they are baseless or satisfactorily addressed. In addition, any perception that the quality of our wealth management and product recommendations and services may not be the same as or better than that of other wealth management advisory firms or wealth management product distributors can also damage our reputation. Moreover, any negative media publicity about the financial service industry in general or product or service quality problems of other firms in the industry, including our competitors, may also negatively impact our reputation and brand. If we are unable to maintain a good reputation or further enhance our brand recognition, our ability to attract and retain clients, wealth management product providers and key employees could be harmed and, as a result, our business and revenues would be materially and adversely affected.

We face significant competition in the wealth management services industry, and if we are unable to compete effectively with our existing and potential competitors, we could lose our market share and our results of operations and financial condition may be materially and adversely affected.

The wealth management market in China is at an early stage of development and is currently highly fragmented and competitive, and we expect competition to persist and intensify. In distributing wealth management products, we face direct competition primarily from (i) commercial banks and their wealth management subsidiaries, (ii) non-bank traditional financial institutions, such as securities firms, fund managers and insurance companies with internal sales capabilities, (iii) online-based service providers, and (iv) third-party professional wealth management services providers that are not associated with financial institutions. In addition, there is a risk that we may not successfully identify new product and service opportunities or develop and introduce these opportunities in a timely and cost-effective manner. New competitors that are better adapted to the wealth management services industry may emerge, we lose market share in key market segments and our business, financial condition and results of operations may be materially and adversely affected.

Further, our competitors may have greater financial and marketing resources than we do. For example, the commercial banks we compete with tend to enjoy significant competitive advantages due to their nationwide distribution network, established brand and credit, and much larger client base and settlement capabilities. Moreover, many of the wealth management product providers we work with, such as fund managers or securities firms, are also engaged in, or may in the future engage in, the distribution of wealth management products and they may benefit from their vertical integration of manufacturing and distribution.

7

In addition, in the asset management services sector, we may also face competition from fund management companies that have emerged or will emerge in the asset management business in China in the foreseeable future.

Our failure to respond in a timely and cost-effective manner to rapid product innovation in the financial industry may have an adverse effect on our business and operating results.

The financial industry is increasingly influenced by frequent new product and service introductions and evolving industry standards. We believe that our future success will depend on our ability to continue to anticipate product innovations and to offer additional product and service opportunities that meet evolving standards on a timely and cost-effective basis. We cannot assure you that we will successfully identify new product and service opportunities or develop and introduce these opportunities in a timely and cost-effective manner. In addition, product and service opportunities that our competitors develop or introduce may render our products and services noncompetitive. Any of foregoing could have a material adverse effect on our business and results of operations.

We may not be able to effectively implement our future business strategies, in which case our business and results of operations may be materially and adversely affected.

Driven by market research and our deep understanding of client needs, since 2019 we have been strategically devoting more resources to standardized fund products, including publicly raised fund products and privately raised securities investment fund products, we have further increased our capital investments in training for seed clients and financial advisors as well as in investor education to raise investor awareness on the benefits of these products. As a result of the foregoing, our operating costs and expenses significantly increased by 44.5% for the year ended June 30, 2021 from the year ended June 30, 2020, due to our increased selling and marketing efforts, recruitment of additional investment advisors for sales and premium training expenses to seed clients and financial advisors, and our increased general and administrative expenses, which were in line with our business expansion. Such increase led to a decrease in our income from operations for the year ended June 30, 2021. We anticipate that we will need to continue to implement a variety of initiatives and allocate more resources to drive the continuing growth of our business. All of these endeavors involve risks and will require substantial management efforts, attention and skills, and additional expenditure. We cannot assure you that our current and planned personnel, systems, procedures and controls will be adequate to support our future operations, or that we will be able to implement our future business strategies effectively, and failure to do so may materially and adversely affect our business and results of operations.

Any significant failure in our information technology systems could have a material adverse effect on our business and profitability.

Our business is highly dependent on the ability of our information technology systems to process a large amount of information of wealth management products, clients and transactions in a timely manner. The proper functioning of our OA system, finance system, investment advisor platform, operation database, client service and other data processing systems, together with the communication systems between our various branch offices and our headquarters in Guangzhou, is critical to our business and our ability to compete effectively. In particular, we rely on the online service platforms provided through our app, Puyi Fund (普益基金) to provide our clients with up-to-date product-related information online and a full-scope of online transaction processing services through which clients can execute transactions and monitor their investments portfolio. We cannot assure you that our business activities would not be materially disrupted in the event of a partial or complete failure of any of these information technology or communication systems, which could be caused by, among other things, software malfunction, computer virus attacks or conversion errors due to system upgrading. In addition, a prolonged failure of our information technology system could damage our reputation and materially and adversely affect our future prospects and profitability.

8

Any failure to protect our clients’ privacy and confidential information could lead to legal liability, adversely affect our reputation and have a material adverse effect on our business, financial condition or results of operations.

Our services involve the exchange, storage and analysis of highly confidential information, including detailed personal and financial information regarding our affluent and emerging middle class clients, through a variety of electronic and non-electronic means, and our reputation and business operations are highly dependent on our ability to safeguard the confidential personal data and information of our clients. We rely on a network of process and software controls to protect the confidentiality of data provided to us or stored on our systems. We face various security threats on a regular basis, including cyber-security threats to and attacks on our technology systems that are intended to gain access to our confidential information, destroy data or disable our systems.

If we do not take adequate measures to prevent security breaches, maintain adequate internal controls or fail to implement new or improved controls, this data, including personal information, could be misappropriated or confidentiality could otherwise be breached. We could be subject to liability if we fail to prevent security breaches, improper access to, or inappropriate disclosure of, any client’s personal information, or if third parties are able to illegally gain access to any client’s name, address, portfolio holdings, or other personal and confidential information. In addition, the rapid upgrade and development of information system technologies and the evolving business models may cause new and unexpected information system risks. Although we have developed systems and internal control processes that are designed to prevent or detect security breaches and protect our clients’ data, we cannot assure you that such measures will provide absolute security. In addition, when we source and distribute fund products from third party fund product providers or fund managers, we may need to share with them certain personal information of our clients, such as names, addresses, phone numbers and transaction accounts. As required by the relevant PRC laws and regulations, we may also need to share such personal information of our clients with the custodians of the fund products we sell. We have limited control or influence over the security policies or measures adopted by our business partners. The seed clients we recruit may also violate their confidentiality obligations and disclose or use information about our clients illegally. Any such failure could subject us to claims for identity theft or other similar fraud claims or claims for other misuses of personal information, such as unauthorized marketing or unauthorized access to personal information. Such events would also cause our clients to lose their trust and confidence in us, which may result in a material adverse effect on our business, results of operations and financial condition.

As the PRC government continues to focus on the supervision of data security and protection of personal information, we could be subject to new laws and regulations relating to the collection, storage, processing or use of personal information that could affect how we collect, store, process and use data. For example, the Cyber Security Law of the People’s Republic of China (the “Cyber Security Law”) requires that personal information and important data collected and generated by operators of critical information infrastructure in the course of their operations in China shall be stored in the territory of China, and the law imposes enhanced regulation and additional security obligations on operators of critical information infrastructure. In addition, the National Standards under the Information Security Technology-Personal Information Security Specification sets forth requirements of collection, storage, use, exchange and disclosure of data. Furthermore, the Personal Information Protection Law of the People’s Republic of China promulgated recently has imposed restrictions on entities and individuals that collect and process personal data and sensitive information. We expect that data security and personal information protection will receive increasing and constant attention and scrutiny from regulators and the public, which may increase our compliance costs and confront us with evolving challenges associated with data security and personal information protection. Any improper use of such personal data and information could harm our reputation and our business as well as result in claims and penalties, including fines, suspension of business and revocation of required licenses.

We may not be able to prevent unauthorized use of our intellectual property, which could reduce demand for the products that we distribute and the services we provide, adversely affect our revenues and harm our competitive position.

We rely primarily on a combination of copyright, trade secret, trademark and anti-unfair competition laws and contractual rights to establish and protect our intellectual property rights. We cannot assure you that the steps we have taken or will take in the future to protect our intellectual property or piracy will prove to be sufficient. For example, although we require our employees, wealth management product providers and seed clients to enter into confidentiality agreements in order to protect our trade secrets, other proprietary information and, most importantly, our client information, these agreements might not effectively prevent disclosure of our trade secrets, know-how or other proprietary information and might not provide an adequate remedy in the event of unauthorized disclosure of such confidential information. In addition, other parties may independently discover trade secrets and proprietary information, and in such cases we could not assert any trade secret rights against such parties. Implementation of intellectual property-related laws in China has historically been lacking, primarily due to ambiguity in the PRC laws and enforcement difficulties. Accordingly, intellectual property rights and confidentiality protection in China may not be as effective as in the United States or other countries. Current or potential competitors may use our intellectual property without our authorization in the development of products and services that are substantially equivalent or superior to ours, which could reduce demand for our products and services, adversely affect our revenues and harm our competitive position. Even if we were to discover evidence of infringement or misappropriation, our recourse against such competitors may be limited or could require us to pursue litigation, which could involve substantial costs and diversion of management’s attention from the operation of our business.

9

We may face intellectual property infringement claims that could be time consuming and costly to defend and may result in the loss of significant rights by us.

Although we have not been subject to any litigation, pending or threatened, alleging infringement of third parties’ intellectual property rights, we cannot assure you that such infringement claims will not be asserted against us in the future. Intellectual property litigation is expensive and time-consuming and could divert resources and management attention from the operation of our business. If there is a successful claim of infringement, we may be required to alter our services, cease certain activities, pay substantial royalties and damages to, and obtain one or more licenses from, third parties. We may not be able to obtain those licenses on commercially acceptable terms, or at all. Any of those consequences could cause us to lose revenues, impair our client relationships and harm our reputation.

Our future success depends on our continuing efforts to retain our existing management team and other key employees as well as to attract, integrate and retain highly skilled and qualified personnel, and our business may be disrupted if we are unable to do so.

Our future success depends heavily on the continued services of our current executive officers. We also rely on the skills, experience and efforts of other key employees, including management, marketing, support, research and development, technical and services personnel. Qualified employees are in high demand throughout wealth management services industries in China, and our future success depends on our ability to attract, train, motivate and retain highly skilled employees and the ability of our executive officers and other members of senior management to work effectively as a team.

If one or more of our executive officers or other key employees are unable or unwilling to continue in their present positions, we may not be able to find replacements easily or at all, which may disrupt our business operations. We do not have key personnel insurance in place. If any of our executive officers or other key employees joins a competitor or forms a competing company, we may lose clients, know-how, key professionals and staff members. Each of our executive officers has entered into a non-competition agreement with us as well as an employment agreement with us which contains confidentiality provisions. However, if any dispute arises between our executive officers and us, we cannot assure you of the extent to which any of these agreements could be enforced in China, where these executive officers reside, because of the uncertainties of China’s legal system. See “— Risks Related to Doing Business in China — Uncertainties with respect to the PRC legal system could adversely affect us.” In the event that such agreements are deemed unenforceable in the context of a dispute with one of our employees, our business, financial condition and results of operations may be materially and adversely affected.

Our principal shareholders have substantial influence over our group and their interests may not be aligned with the interests of our other shareholders.

Mr. Yu Haifeng, our founder and chairman, beneficially owns 87.6% of our share capital and as a result, has substantial influence over our business operations, including decisions regarding mergers, consolidations and the sale of all or substantially all of our assets, election of directors and other significant corporate actions. Mr. Yu may take actions that are not in our best interests or the best interests of our other shareholders. This concentration of ownership may discourage, delay or prevent a change in control of our group, which could deprive our shareholders of an opportunity to receive a premium for their shares as part of a sale of our group and might reduce the price of our ADSs. These actions may be taken even if they are opposed by our other shareholders. In such events, our business, financial condition and results of operations may be materially and adversely affected.

10

As a “controlled company” under the NASDAQ listing rules, we may follow certain exemptions from certain corporate governance requirements that could adversely affect our public shareholders.

Our principal shareholder owns more than a majority of the voting power of our outstanding ordinary shares. Under the NASDAQ listing rules, a company of which more than 50.0% of the voting power is held by an individual, group or another company is a “controlled company” and is permitted to phase in its compliance with the independent committee requirements. Although we do not intend to rely on the “controlled company” exemption under the NASDAQ listing rules, we could elect to rely on this exemption in the future. If we were to elect to rely on the “controlled company” exemption, a majority of the members of our board of directors might not be independent directors and our nominating and corporate governance and compensation committees might not consist entirely of independent directors. Accordingly, during the period we remain a controlled company relying on the exemption and during any transition period following a time when we are no longer a controlled company, our shareholders would not have the same protections afforded to shareholders of companies that are subject to all of the corporate governance requirements.

Our revenues and operating results can fluctuate from period to period, which could cause the price of our ADSs to fluctuate.

Our revenues and operating results have fluctuated in the past and may fluctuate from period to period in the future due to a variety of factors, many of which are beyond our control. Factors relating to our business that may contribute to these fluctuations include the following factors, as well as other factors described elsewhere in this annual report:

| ● | a decline or slowdown of the growth in the value of wealth management products, which may reduce the value of products we distribute for wealth management product providers and the products provided by us and, in turn, our revenues and cash flows; |

| ● | negative public perception and reputation of the wealth management services industry; |

| ● | unanticipated delays of anticipated rollouts of our products or services; |

| ● | unanticipated changes to economic terms in contracts with our wealth management product providers, including renegotiations; |

| ● | changes in laws or regulatory policy that could impact our ability to provide wealth management services and/or asset management services; |

| ● | failure to enter into contracts with new wealth management product providers; |

| ● | increasing costs and expenses incurred by the establishment of new branches in economically developed cities and the recruitment of exclusive in-house financial advisors; |

| ● | cancellations or non-renewal of existing contracts with wealth management product providers; and |

| ● | changes in the number of clients who decide to terminate their relationship with us or who ask us to redeem their investment in our products. |

As a result of these and other factors, the results of any prior interim or annual periods should not be relied upon as indications of our future revenues or operating performance.

11

We are an emerging growth company within the meaning of the Securities Act and may take advantage of certain reduced reporting requirements, and this could make it more difficult to compare our performance with other public companies.

We are an “emerging growth company,” as defined in the JOBS Act, and we may take advantage of certain exemptions from various requirements applicable to other public companies that are not emerging growth companies including, most significantly, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 so long as we are an emerging growth company. As a result, if we elect not to comply with such auditor attestation requirements, our investors may not have access to certain information they may deem important. In addition, Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a registration statement under the U.S. Securities Act of 1933, as amended (the “Securities Act”) declared effective or do not have a class of securities registered under the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”)) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such an election to opt out is irrevocable. We have elected to opt in to such extended transition period, which means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can delay the adoption of the new or revised standard until private companies adopt the new or revised standard. Accordingly, our financial statements may not be comparable to other public companies that are not emerging growth companies or that are emerging growth companies which have opted out of using the extended transition because of the potential differences in accounting standards used.

We are a foreign private issuer within the meaning of the rules under the Exchange Act and are therefore exempt from certain provisions applicable to U.S. domestic issuers.

Because we qualify as a foreign private issuer under the Exchange Act, we are exempt from certain provisions of the securities rules and regulations in the United States that are applicable to U.S. domestic issuers, including:

| ● | the rules under the Exchange Act requiring the filing with the U.S. Securities and Exchange Commission (“SEC”) of quarterly reports on Form 10-Q or current reports on Form 8-K; |

| ● | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; |

| ● | the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and |

| ● | the selective disclosure rules by issuers of material nonpublic information under Regulation FD. |

We are required to file an annual report on Form 20-F within four months of the end of each fiscal year. In addition, we intend to publish our results on an annual basis as press releases, distributed pursuant to the rules and regulations of the NASDAQ Global Market. Press releases relating to financial results and material events will also be furnished to the SEC on Form 6-K. However, the information we are required to file with or furnish to the SEC will be less extensive and less timely compared to that required to be filed with the SEC by U.S. domestic issuers. As a result, our shareholders may not be afforded the same protections or information that would be made available to you were you investing in a U.S. domestic issuer.

As a company incorporated in the Cayman Islands, we are permitted to adopt certain home country practices in relation to corporate governance matters in lieu of the corporate governance listing standards applicable to U.S. domestic issuers, which home country practices may afford comparatively less protection to shareholders.

As a company incorporated in the Cayman Islands, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from the NASDAQ Global Market corporate governance requirements; these practices may afford less protection to shareholders than they would enjoy if we complied fully with the NASDAQ Global Market corporate governance requirements. For example, as a foreign private issuer, we are not required to: (i) have a majority of the board be independent; (ii) have a compensation committee or a nominating/corporate governance committee consisting entirely of independent directors; or (iii) have regularly scheduled executive sessions with only independent directors each year.

12

We intend to follow home country practice in lieu of the requirements under the NASDAQ Global Market rules with respect to certain corporate governance standards. Accordingly, our shareholders not be provided with the benefits of certain corporate governance requirements of the NASDAQ Global Market rules.

If we fail to implement and maintain an effective system of internal control, we may be unable to accurately or timely report our results of operations or prevent fraud, and investor confidence and the market price of the ADSs may be materially and adversely affected.

We are subject to the reporting requirements of the Exchange Act, the Sarbanes-Oxley Act and the rules and regulations of the NASDAQ Global Select Market. The Sarbanes-Oxley Act requires, among other things, that we maintain effective disclosure controls and procedures and internal control over financial reporting. Commencing with our fiscal year ended June 30, 2020, we must perform system and process evaluation and testing of our internal control over financial reporting to allow management to report on the effectiveness of our internal control over financial reporting in our Form 20-F filing, as required by Section 404 of the Sarbanes-Oxley Act.

In the course of preparing our consolidated financial statements and in connection with the audit, our management identified one material weakness, which was first identified in 2018 and had been in place for the following two years ended June 30, 2020, related to the lack of sufficient financial reporting and accounting personnel with appropriate knowledge of U.S. GAAP and SEC reporting requirements to formalize key controls over financial reporting and to prepare consolidated financial statements and related disclosures. To remedy this material weakness and improve our internal control over financial reporting, we implemented a number of measures including but not limited to (i) setting up a separate and independent department - the Financial Reporting Department which is led by a new hired experienced general manager who is familiar with U.S. GAAP, this manager and the Financial Reporting Department are responsible to deal with complex U.S. GAAP technical accounting issues, and make relevant disclosures in accordance with U.S. GAAP and the financial reporting requirements set forth by the SEC; (ii) establishing relevant processes that are necessary for preparing consolidated financial reports and relevant disclosure; (iii) conducting trainings for the management and relevant personnel to enable them to have a full understanding of financial reporting requirements set forth by the SEC as well as the responsibilities of listed companies; and (iv) working closely with our auditors and lawyers to seek professional advice and guidance to address the material weakness. As of June 30, 2021, our management determined that the aforementioned measures have remediated the material weakness. However, since the Company is still in the process of replenishing and building up a qualified finance and accounting team with sufficient dedicated resources, our management assessed that the deficiency related to the lack of dedicated resources to take responsibility for the finance and accounting functions and the preparation of financial statements in compliance with U.S. GAAP and SEC reporting requirements still existed as of June 30, 2021. Therefore, based on the definition of “material weakness” and “significant deficiency” in the standards established by the Public Company Accounting Oversight Board of the United States, our management concluded that the deficiency now only rises to the level of a significant deficiency. For details, see “Item 15. Controls and Procedures—B. Management’s Annual Report on Internal Control Over Financial Reporting.”

Once we cease to be an “emerging growth company” as the term is defined in the JOBS Act, our independent registered public accounting firm must attest to and report on the effectiveness of our internal control over financial reporting. Even though our management, by then, may conclude that our internal controls over financial reporting are effective, our independent registered public accounting firm, after conducting its own independent testing, may not reach the same conclusion. In addition, our reporting obligations may place a significant strain on our management, operational and financial resources and systems for the foreseeable future. We may be unable to timely complete our evaluation testing and any required remediation.

Our internal control over financial reporting will not prevent or detect all errors and all fraud. A control system, regardless of how well designed and operated, can provide only reasonable, not absolute, assurance that the control system’s objectives will be met. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that misstatements due to error or fraud will not occur or that all control issues and instances of fraud will be detected.

As of June 30, 2021, our management concluded that our internal controls over financial reporting were effective. However, if we fail to maintain effective internal controls over financial reporting in the future, our management may conclude that our internal controls over financial reporting are not effective and we may not be able to produce timely and accurate financial statements. If that were to happen, the market price of the ADSs could decline and we could be subject to sanctions or investigations by the NASDAQ Global Select Market, SEC or other regulatory authorities.

13

We have limited insurance coverage.

Insurance companies in China do not offer as extensive an array of insurance products as insurance companies in more developed economies do. Other than casualty insurance on some of our assets, we do not have commercial insurance coverage for our other assets and personnel nor do we have insurance coverage for our general business operations, business interruption, litigation or product liability. We have determined that the costs of insurance coverage for these risks and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. Any uninsured occurrence of loss or damage to property, litigation or business disruption may result in our incurring substantial costs and the diversion of resources, which could have a material and adverse effect on our results of operations and financial condition.

The current tension in international trade, particularly with regard to U.S. and China trade policies, may adversely impact our business, financial condition, and results of operations.

Although our business is not focused on cross-border transactions, if we plan to expand our business internationally in the future, any unfavorable government policies on international trade, such as capital controls or tariffs, may affect the demand for our products and services, impact our competitive position, or prevent us from being able to conduct business in certain countries. If any new tariffs, legislation, or regulations are implemented, or if existing trade agreements are renegotiated, such changes could adversely affect our business, financial condition, and results of operations. Recently, there have been heightened tensions in international economic relations, such as between the United States and China. The U.S. government has recently imposed, and has recently proposed to impose additional, new, or higher tariffs on certain products imported from China to penalize China for what it characterizes as unfair trade practices. China has responded by imposing, and proposing to impose additional, new, or higher tariffs on certain products imported from the United States. Following mutual retaliatory actions for months, on January 15, 2020, the United States and China entered into the Economic and Trade Agreement between the United States of America and the People’s Republic of China as a phase one trade deal, effective on February 14, 2020. While the “Phase One” agreement was signed between the United States and China on trade matters, it remains unclear what additional actions, if any, will be taken by the U.S., China or other governments with respect to international trade, tax policy related to international commerce, or other trade matters.

Although the direct impact of the current international trade tension, and any escalation of such tension, on the wealth management industry in China is uncertain, the negative impact on general, economic, political and social conditions in China may adversely impact our business, financial condition and results of operations.

The global spread of COVID-19 pandemic could materially and adversely affect our business, financial condition and operating results.

The COVID-19 continues to have a severe and negative impact on the Chinese and the global economy. Whether this will lead to a prolonged downturn in the economy is still unknown. The global spread of COVID-19 pandemic in major countries of the world have and may continue result in global economic distress, and the nature of and extent to which it may affect our results of operations will depend on future developments of the COVID-19 pandemic, which are highly uncertain and difficult to predict. For the year ended June 30, 2021, our offline sales have been adversely affected, and there may be potential continuing impacts on subsequent periods if the pandemic and the resulting disruption were to extend over a prolonged period. We have taken and will continue to take a series of measures to compensate for the adverse impact of the COVID-19, including but not limited to the expansion of our online sales and the development and optimization of our online trading system to facilitate the smooth operation of our online sales; however, if the global spread of the COVID-19 and the corresponding deterioration cannot be contained, risks set forth in this annual report may be exacerbated or accelerated at a heightened level.

14

Risks Related to Our Corporate Structure

If the PRC government finds that the agreements that establish the structure for operating our businesses in China do not comply with PRC regulations relating to fund management businesses, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations.