Exhbit 99.1

|

CONTENTS

|

|

STRATEGIC REPORT

|

|

|

AT A GLANCE

|

|

|

Financial Highlights

|

4

|

|

CSR Highlights

|

5

|

|

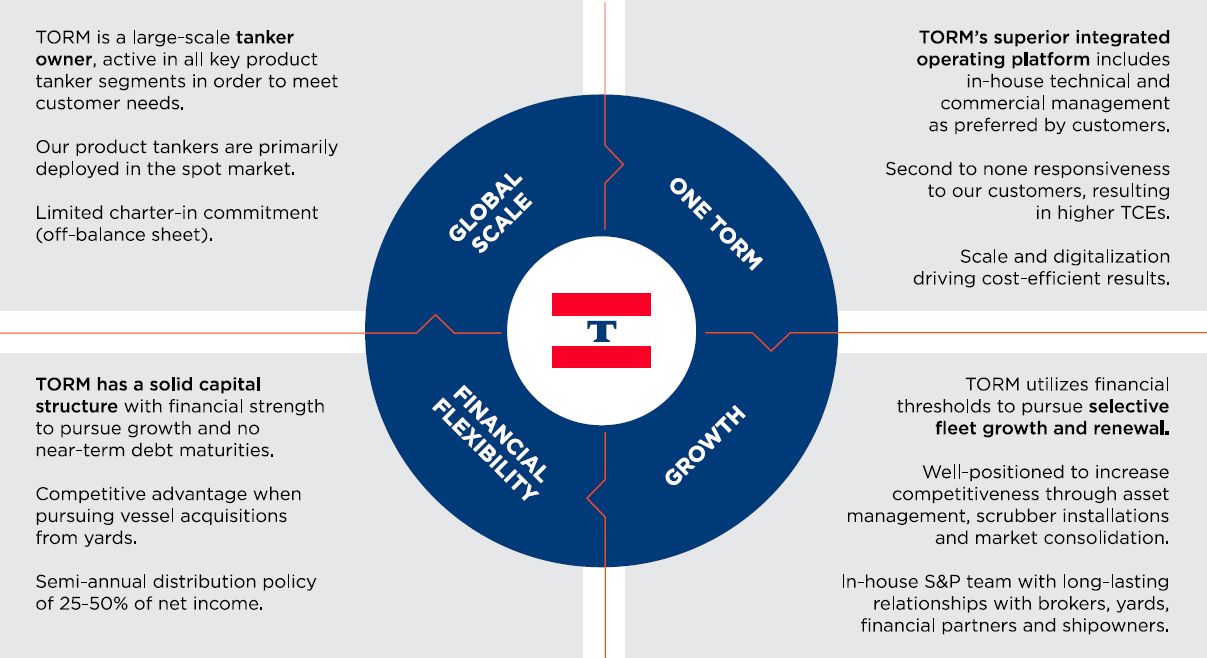

One TORM, A Strong Platform

|

6

|

|

Chairman’s Statement

|

7

|

|

RESULTS

|

|

|

Key Figures

|

9

|

|

The Year in Review

|

11

|

|

Outlook 2020

|

14

|

|

Statement by the Executive Director

|

17

|

|

STRATEGY

|

|

|

Strategic Ambitions and Business Model

|

19

|

|

MARKET

|

|

|

Value Chain in Oil Transportation

|

22

|

|

The Product Tanker Market

|

23

|

|

IMO 2020 Sulfur Regulaltion

|

28

|

|

Key Performance Indicators

|

31

|

|

The TORM Fleet

|

32

|

|

RISK & REVIEW

|

|

|

Risk Management

|

33

|

|

Financial Review 2019

|

39

|

|

OUR RESPONSIBILITY

|

|

|

Our Principles

|

49

|

|

Environmental Efforts

|

50

|

|

Green House Gas Emissions Data

|

53

|

|

Supporting Quality Education

|

54

|

|

Health, Safety and Security

|

56

|

|

Employees

|

58

|

|

Human Rights

|

60

|

|

|

|

|

Corporate Governance Statement

|

61

|

|

GOVERNANCE

|

|

|

GOVERNANCE INTRODUCTION

|

|

|

Chairman’s Introduction

|

63

|

|

Corporate Governance

|

65

|

|

Board of Directors

|

69

|

|

GOVERNANCE INTRODUCTION

|

|

|

Audit Committee Report

|

71

|

|

Risk Committee Report

|

76

|

|

Nomination Committee Report

|

79

|

|

Remuneration Committee Report

|

81

|

|

OTHER

|

|

|

Investor Information

|

91

|

|

Directors’ Report

|

94

|

|

Statement of Directors’ Responsibilities

|

98

|

|

FINANCIAL STATEMENTS

|

|

|

CONSOLIDATED FINANCIAL STATEMENTS

|

|

|

Consolidated Income Statement

|

101

|

|

Consolidated Statement of Comprehensive Income

|

101

|

|

Consolidated Balance Sheet

|

102

|

|

Consolidated Statement of Changes in Equity

|

103

|

|

Consolidated Cash Flow Statement

|

105

|

|

Notes Consolidated

|

106

|

|

PARENT COMPANY FINANCIAL STATEMENTS

|

|

|

Parent Company 2019

|

143

|

|

Balance Sheet

|

144

|

|

Changes in Equity

|

145

|

|

Notes to Parent Financial Statements

|

146

|

|

OTHER

|

|

|

Independent Auditor’s Report

|

151

|

|

TORM Fleet Overview

|

157

|

|

Glossary and APM

|

160

|

|

4

Financial

Highlights |

19

Business

Model |

65

Corporate

Governance |

101

Income

Statement |

2

3

4

5

6

|

CHAIRMAN’S STATEMENT

|

|

The product tanker market improved significantly in 2019 compared to the prior year, resulting in the strongest full-year results in

three years. The strengthening of the market, especially in the fourth quarter of the year, was carried over into 2020, driven by the implementation of new restrictions on sulfur emissions. However, since January 2020, strong freight rates

have been eroded by the global impact of the COVID-19 outbreak. Looking ahead, I believe TORM is well positioned to take advantage of market opportunities wherever they may arise, given the scale of our operations and the integrated One TORM

platform.

Christopher H. Boehringer, Chairman of the Board

The underlying product tanker market experienced volatility throughout the year. In the fourth quarter of 2019, the freight rates reached multi-year highs, and this trend

continued into January 2020 until the COVID-19 outbreak. TORM was well positioned to capture periods of market strength due to our spot-oriented chartering strategy, our continued strong operational performance and our large commercial scale.

CONTINUOUS EFFORTS TO RENEW THE FLEET

In 2019, TORM continued to renew our fleet. We took delivery of five MR newbuildings in 2019 and have taken delivery of one additional MR vessel and two LR1 vessels in

the first quarter of 2020. In addition, we purchased four modern second-hand vessels and sold eight older vessels. The sales were completed at prevailing broker valuations, while the purchases were done below market levels. In January 2020, TORM

made an additional purchase of two fuel-efficient dual-fuel-ready LR2 newbuildings with scrubbers. The vessels will be delivered in the fourth quarter of 2021. The Company’s ongoing effort to maintain scale as well as a competitive fleet age

profile is executed through TORM’s opportunistic approach to making acquisitions that

leverage on strong relationships with shipyards, brokers and financial partners.

MAINTAINING A STRONG CAPITAL STRUCTURE

Maintaining a solid capital structure remains a key priority for TORM, and I am pleased that TORM in January 2020 has obtained commitment from leading ship lending banks

for two separate term facilities and a revolving credit facility of up to a total of USD 496m. These facilities replace four term loans and TORM’s existing revolving credit facility. Following the refinancing, TORM does not have any major debt

maturities until 2026, which supports the Company’s strong liquidity and capital structure. TORM completed sale and leaseback transactions covering eight vessels in 2019, providing total proceeds of USD 151m and further demonstrating our ability

to raise capital.

MARKET CONDITIONS HAVE IMPROVED SIGNIFICANTLY

While product tanker rates trended lower throughout September 2019 following a strong first quarter of the year, average rates were well above the prior year’s levels,

indicating a stronger underlying market. Rates were propelled higher starting in October with a rapid rise in crude

oil tanker rates following sanctions on the COSCO fleet. While this produced a surge that proved to be short-lived, the market did stabilize at a higher level in November

and December. TORM has again in 2019 delivered TCE earnings at the top end of what comparable industry players delivered. This has been achieved in a period where 17 vessels have been taken out of service to have scrubbers installed. TORM’s

medium- to long-term outlook for the product tanker market remains positive. During the last months of 2019 and in 2020 to date, we have already seen that the reduction in the global limit for sulfur emissions from 3.5% to 0.5% and the

accompanying shift in marine fuel consumption have led to increased trade volumes of clean petroleum products to the benefit of the product tanker market.

7

|

CHAIRMAN’S STATEMENT

|

|

|

|

Additionally, the fleet supply outlook is very favorable as the product tanker order book is at low levels not seen in the last two decades.

However, the COVID-19 outbreak impacted the market sentiment negatively from end January 2020.

TORM IS TAKING ADVANTAGE OF IMO 2020

During 2019, TORM prepared for the IMO 2020 sulfur regulation. The Company utilizes a balanced approach and has decided to install scrubbers on a

total of 49 vessels. Already in the first quarter of 2020, we have seen the benefits of our preparations. As with many other shipowning companies, TORM did experience some delays to the scrubber installations at the end of 2019, which

resulted in us postponing some installations into 2020. These installations have only to a limited extent been affected by the COVID-19 outbreak. For the vessels using compliant fuels from January 2020, customized preparation schedules were

executed during the third and fourth quarters.

ONGOING FOCUS ON CLIMATE AND ENVIRONMENT

Since 2009 where TORM signed up for the UN Global Compact, efforts to support both climate and environmental efforts have been an integrated part of

the Company. Today these areas continue to have an important role for TORM and we address these through broad industry partnerships as well as our continuous efforts to reduce climate impact.

130 YEARS AND COUNTING

In 2019, TORM celebrated its 130-year anniversary. TORM has prospered through numerous historical events, and today TORM continues to build on its

legacy. With the One TORM platform and strong company values displayed by our dedicated seafarers and onshore employees every day, TORM stands on a strong, but also flexible, foundation that

|

|

|

|

will allow the Company to keep delivering on its promises for many years ahead.

The Board of Directors has decided to recommend a dividend of USD 7.4m, equivalent to USD 0.10 per share, for approval at the AGM on 15 April 2020.

Should the dividend be approved, payment is expected on 6 May 2020 with ex-dividend date on 17 April 2020. In addition, the Board has decided to conduct share repurchases up to a maximum of USD 1.4m during the first six months of 2020 in

open-market transactions on Nasdaq in Copenhagen. The total distribution of up to USD 8.8m is in line with the Company’s Distribution Policy and corresponds to a maximum of 50% of

|

net income adjusted for the impairment reversal of USD 120m for the six months ended 31 December 2019.

Mr. Christopher H. Boehringer, Chairman of the Board

|

|

8

Key Figures

|

2019

|

2018

|

2017

|

|

|

INCOME STATEMENT (USDM)

|

|||

|

Revenue

|

693

|

635

|

657

|

|

Time charter equivalent earnings (TCE) ¹⁾

|

425

|

352

|

397

|

|

Gross profit ¹⁾

|

252

|

169

|

200

|

|

EBITDA ¹⁾

|

202

|

121

|

158

|

|

Operating profit/(loss) (EBIT)

|

206

|

3

|

40

|

|

Financial items

|

-39

|

-36

|

-36

|

|

Profit/(loss) before tax

|

167

|

-33

|

3

|

|

Net profit/(loss) for the year

|

166

|

-35

|

2

|

|

Net profit/(loss) for the year excluding impairment¹⁾

|

46

|

-35

|

2

|

|

BALANCE SHEET (USDM)

|

|||

|

Non-current assets

|

1,788

|

1,445

|

1,385

|

|

Total assets

|

2,004

|

1,714

|

1,647

|

|

Equity

|

1,008

|

847

|

791

|

|

Total liabilities

|

996

|

867

|

856

|

|

Invested capital ¹⁾

|

1,786

|

1,469

|

1,406

|

|

Net interest-bearing debt ¹⁾

|

786

|

627

|

620

|

|

Cash and cash equivalents, including restricted cash

|

72

|

127

|

134

|

|

2019

|

2018

|

2017

|

|

|

KEY FINANCIAL FIGURES ¹⁾

|

|||

|

Gross margins:

|

|||

|

TCE

|

61.3%

|

55.4%

|

60.4%

|

|

Gross profit

|

36.4%

|

26.6%

|

30.4%

|

|

EBITDA

|

29.2%

|

19.1%

|

24.0%

|

|

Operating profit/(loss)

|

29.7%

|

0.5%

|

6.1%

|

|

Return on Equity (RoE)

|

17.9%

|

-4.3%

|

0.3%

|

|

Return on Invested Capital (RoIC)

|

12.6%

|

0.1%

|

2.8%

|

|

Adjusted Return on Invested Capital (Adjusted RoIC)

|

4.9%

|

0.1%

|

2.4%

|

|

Equity ratio

|

50.3%

|

49.4%

|

48.0%

|

|

SHARE-RELATED KEY FIGURES ¹⁾

|

|||

|

Basic earnings/(loss) per share (USD)

|

2.24

|

-0.48

|

0.04

|

|

Diluted earnings/(loss) per share (USD)

|

2.24

|

-0.48

|

0.04

|

|

Dividend per share (USD)

|

0.10

|

-

|

0.02

|

|

Net Asset Value per share (NAV/share) ²⁾

|

13.6

|

11.6

|

12.8

|

|

Stock price in DKK, end of period (per share of USD 0.01)

|

74.5

|

43.9

|

53.5

|

|

Number of shares (excluding treasury shares), end of period (million)

|

74.4

|

73.9

|

62.0

|

|

Number of shares (excluding treasury shares), weighted average (million)

|

74.0

|

73.1

|

62.0

|

|

¹⁾ For definition of the calculated key figures (the APMs), please

refer to the glossary on pages 160-165.

|

|||

|

²⁾ Based on broker valuations as of 31 December, excluding charter

commitments.

|

|||

9

|

SAFE

HARBOR STATEMENTS AS TO THE FUTURE

|

|

|

| Matters discussed in this release may constitute forward-looking statements. Forward-looking statements reflect our current views

with respect to future events and financial performance and may include statements concerning plans, objectives, goals, strategies, future events or performance, and underlying assumptions and statements other than statements of historical

facts. The words “believe,” “anticipate,” “intend,” “estimate,” “forecast,” “project,” “plan,” “potential,” “may,” “should,” “expect,” “pending” and similar expressions generally identify forward-looking statements.

The forward-looking statements in this release are based upon various assumptions, many of which are based, in turn, upon further

assumptions, including without limitation, management’s examination of historical operating trends, data contained in our records and other data available from third parties. Although the Company believes that these assumptions were

reasonable when made, because these assumptions are inherently subject to significant uncertainties and contingencies that are difficult or impossible to predict and are beyond our control, the Company cannot guarantee that it will achieve

or accomplish these expectations, beliefs or projections.

|

Important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements include the strength

of the world economy and currencies, general market conditions, including fluctuations in charter hire rates and vessel values, changes in demand for “ton-miles” of oil carried by oil tankers and changes in demand for tanker vessel

capacity, the effect of changes in OPEC’s petroleum production levels and worldwide oil consumption and storage, changes in demand that may affect attitudes of time charterers to scheduled and unscheduled dry-docking, changes in TORM’s

operating expenses, including bunker prices, dry-docking and insurance costs, changes in the regulation of shipping operations, including actions taken by regulatory authorities, potential liability from pending or future litigation,

domestic and international political conditions, potential disruption of shipping routes due to accidents, political events including “trade wars,” or acts by terrorists.

|

In light of these risks and uncertainties, you should not place undue reliance on forward-looking statements contained in this

release because they are statements about events that are not certain to occur as described or at all. These forward-looking statements are not guarantees of our future performance, and actual results and future developments may vary

materially from those projected in the forward-looking statements.

Except to the extent required by applicable law or regulation, the Company undertakes no obligation to release publicly any

revisions or updates to these forward-looking statements to reflect events or circumstances after the date of this release or to reflect the occurrence of unanticipated events. Please

see TORM’s filings with the U.S. Securities and Exchange Commission for a more complete discussion of certain of these and other

risks and uncertainties.

|

10

|

The Year in review

|

|||

|

2019 RESULT

|

In 2019, TORM realized an EBITDA of USD 202m (2018: USD 121m). The 2019 profit before tax amounted to USD 167m (2018:

USD -33m) including an impairment reversal of USD 120m.

TORM’s performance has been strong compared to industry peers. Return on Invested Capital (RoIC) was 4.9% (2018: 0.1%),

when adjusted for the impairment reversal.

|

||

| MARKET CONDITIONS |

For the full year 2019, TORM achieved TCE rates of USD/day 16,526 (2018: USD/day 12,982).

After strong rates at the start of the year, the product tanker market softened through the second and

third quarters, before posting a strong recovery in the fourth quarter with freight rates peaking at highs not seen since 2008.

|

||

|

VESSEL

TRANSACTIONS |

During 2019, TORM took delivery of five MR newbuildings and four second-hand MR vessels.

In addition, TORM executed sale and leaseback transactions for eight vessels, covering the acquired four second-hand MR

vessels and four existing MR vessels.

Further, TORM sold eight older vessels (five MR vessels and three Handysize vessels) for a total consideration of USD

65m. Seven of the vessels were delivered to their new owners in 2019, and one Handysize vessel was delivered early January 2020.

As of 31 December 2019, TORM’s fleet consists of 65 owned vessels, 11 vessels under sale and leaseback arrangements and

four vessels on order. During January 2020, TORM made an additional purchase of two fuel-efficient dual-fuel-ready LR2 newbuildings with scrubbers and took delivery of three newbuildings, including two LR1s and one MR.

|

||

|

CORPORATE

EVENTS

|

New Chief Financial Officer and new Board Observer.

Mr. Kim Balle has been appointed Chief Financial Officer (CFO) of TORM A/S with effect from December 2019. Mr. Balle has been Group CFO in DLG and Group

CFO in the private equity-owned CASA A/S. Mr. Balle has a background from the financial sector, where he held a position as Head of Corporate Banking in Danske Bank.

In addition, TORM has appointed Ms. Annette Malm Justad as Board Observer. Ms. Justad has significant managerial experience and has previously served as

CEO of Eitzen Maritime Services. Ms. Justad currently holds several director positions including Chairman of American Shipping Company ASA and Board member of Awilco LNG. As Board Observer, Ms. Justad attended her first Board meeting in

August 2019.

|

||

11

|

The Year in review

|

|||

|

REFINANCING

|

In January 2020, TORM has obtained commitment from leading ship lending banks for two separate term facilities and a

revolving credit facility of up to a total of USD 496m.

These facilities replace four term loans and TORM’s existing revolving credit facility that all together on a fully

drawn basis cover USD 502m in debt. Following the refinancing, TORM does not have any major debt maturities until 2026, which supports the Company’s financial flexibility.

|

||

|

IMO 2020 SULFUR REGULATION

|

TORM has committed to install 49 scrubbers, and most of these will be delivered from our joint venture.

During 2019, TORM successfully conducted 18 scrubber installations on the fleet. On 31 December 2019, 20 vessels

were operating with scrubbers. As of 11 March 2020, 30 vessels are operating with scrubbers and 17 vessels are intended to be fitted with scrubbers during the first, second and third quarters of 2020. The last two scrubbers will be

delivered when the LR2 newbuildings are delivered in the fourth quarter of 2021. For the remaining fleet using compliant fuel, customized schedules preparing the vessels for the new sulfur regulation were executed during the third and

the fourth quarters of 2019.

|

||

|

LIQUIDITY

|

As of 31 December 2019, TORM’s available liquidity was USD 246m and consisted of USD 72m in cash and USD 174m in undrawn credit facilities.

As of 31 December 2019, the net interest-bearing debt1 amounted to USD 786m, and the net loan-to-value

(LTV)2 ratio was estimated at 46%. Cash and cash equivalents, includes restricted cash of USD 16m, primarily related to security placed as collateral for financial instruments. As of 29 February 2020, TORM’s net

interest-bearing debt was estimated at USD 791m and the available liquidity was estimated at USD 297m including USD 76m of sale and leaseback financing that is subject to documentation.

|

||

|

NAV, EQUITY AND VESSEL

VALUES

|

Based on broker valuations, TORM’s fleet including newbuildings had a market value of USD 1,802m as of 31 December

2019. TORM’s NAV3 excluding charter commitments was estimated at USD 1,016m, corresponding to a NAV/share of USD 13.6 or DKK 91.1.

As of 31 December 2019, TORM’s book equity amounted to USD 1,008m. This corresponds to a book equity/share of USD 13.5 or DKK 90.4.

|

||

1 See Glossary on page 162 for a definition of net interest-bearing debt.

2 See Glossary on page 164 for a definition of loan-to-value.

3 See Glossary on page 165 for a definition of NAV.

|

|||

12

|

The Year in review

|

|||

|

ORDER BOOK, CAPEX

AND IMPAIRMENT

|

As of 31 December 2019, TORM’s order book stood at four newbuildings, consisting of two LR1 and two MR vessels, all to be delivered from Guangzhou Shipyard International in China.

Three of these newbuildings have been delivered in the first quarter of 2020. As of 11 March 2020, the order book stands at one MR vessel with

expected delivery in the second quarter of 2020 and two LR2 vessels with expected delivery in the fourth quarter of 2021. Outstanding CAPEX4 relating to the order book, including costs related to the installation of

scrubbers, amounted to USD 51m as of 31 December 2019 and USD 112m as of 29 February 2020 including the two LR2 newbuildings.

As of 31 December 2019, TORM performed an impairment test of the recoverable amount of the most significant assets. Based on this review, Management concluded that the previous impairment

communicated in connection with the 2016 Annual Report should be reversed by USD 120m as the value in use exceeds the carrying amounts.

The book value of the fleet was USD 1,770m as of 31 December 2019 excluding outstanding installments on the newbuildings of USD 51m.

|

||

|

COVERAGE

|

As of 31 December 2019, 9% of the total earning days5 in 2020 were covered at USD/day 23,399.

As of 5 March 2020, the coverage for the first quarter of 2020 was 87% at USD/day 23,818. For the individual

segments, the coverage was 92% at USD/day 28,353 for LR2, 83% at USD/day 25,185 for LR1, 87% at USD/day 22,729 for MR and 92% at USD/day 19,963 for Handysize.

|

||

|

DISTRIBUTION

POLICY

|

TORM intends to distribute 25-50% of net income semi-annually.

The Board of Directors has decided to recommend a dividend of USD 7.4m, equivalent to USD 0.10 per share, for approval at the AGM on 15 April 2020.

Should the dividend be approved, payment is expected on 6 May 2020 with ex-dividend date on 17 April 2020. In addition, the Board has decided to conduct share repurchases up to a maximum of USD 1.4m during the first six months of

2020 in open-market transactions on Nasdaq in Copenhagen. The total distribution of up to USD 8.8m is in line with the Company’s Distribution Policy and corresponds to a maximum of 50% of net income adjusted for the impairment

reversal of USD 120m for the six months ended 31 December 2019.

|

||

4 See Glossary on page 160 for a definition of CAPEX.

5 See Glossary on page 160 for a definition of earning days.

|

|||

13

Outlook 2020

As of 31 December 2019, TORM had covered 2,376 earning days (9% of the total earning days) for 2020 at an average rate of USD/day 23,399.

As of 5 March 2020, the coverage for the first quarter of 2020 was 87% at USD/day 23,818.

OUTLOOK

Taking economic and political uncertainty into account, TORM expects the supply and demand balance within the product tanker market to improve in the period 2020-2022. On

the supply side, limited fleet ordering activity and a historically low order book ensure that fleet growth remains limited, with the net fleet growth currently estimated at approximately 3%. This is low compared to the five-year average fleet

growth.

During 2020-2022, the product tanker ton-mile demand is projected to grow at a compound annual rate of approximately 4%, exceeding growth in tonnage supply. Improvements in

demand are driven by continued oil demand growth and increasing demand for transportation. In particular, the reduction in the global limit for sulfur emissions from 3.5% to 0.5% and the accompanying shift in marine fuel consumption are expected

to lead to continued increased trade in clean petroleum products, but also to add to market inefficiencies especially in the early part of the implementation period. Additionally, changes in the global refinery landscape and increasing

competitive pressure on older refineries are expected to add to demand for transportation. Please see "The Product Tanker Market" section on pages 23-27.

In line with common practice for most UK companies and other major shipping companies, TORM does not provide guidance on earnings. To support the assessment of TORM,

information on covered days, interest-bearing bank debt, the one-year time charter (T/C) market and EBITDA sensitivity to freight rates is included in the Annual Report.

COVERAGE FOR 2020

As of 31 December 2019, TORM had covered 2,376 earning days (9% of the total earning days) for 2020 at an average rate of USD/day 23,399. This means that a change in

freight rates of USD/day 1,000 for the duration of 2020 would impact the full-year EBITDA by USD 25m.

As of 5 March 2020, the coverage for the first quarter of 2020 was 87% at USD/day 23,818. For the individual segments, the coverage was 92% at USD/day 28,353 for LR2, 83%

at USD/day 25,185 for LR1, 87% at USD/day 22,729 for MR and 92% at USD/day 19,963 for Handysize. The covered rates include a premium that TORM has obtained for the scrubber-fitted vessels.

|

2020 EBITDA SENSITIVITY TO CHANGES IN FREIGHT RATES - AS OF 31 DECEMBER 2019

|

|||||||

|

Change in freight rates (USD/day)

|

|||||||

|

USDm

|

-5,000

|

-2,500

|

-1,000

|

1,000

|

2,500

|

5,000

|

|

|

LR2

|

-16

|

-8

|

-3

|

3

|

8

|

16

|

|

|

LR1

|

-14

|

-7

|

-3

|

3

|

7

|

14

|

|

|

MR

|

-93

|

-47

|

-19

|

19

|

47

|

93

|

|

|

Handysize

|

-3

|

-2

|

-1

|

1

|

2

|

3

|

|

|

Total

|

-127

|

-63

|

-25

|

25

|

63

|

127

|

|

14

Outlook 2020

|

As of 31 December 2019, the interest-bearing bank debt totaled USD 786m, and TORM had fixed 73% of the interest exposure for 2020. A change in interest rates of 25

basis points for the duration of 2020 would impact the result before tax by USD 0.8m.

As of 5 March 2020, the one-year T/C market, shown in the table to the right, corresponds to a weighted average one-year T/C rate for TORM’s vessels of USD/day

16,226.

|

ONE-YEAR TIME CHARTER MARKET

|

||

|

Source: Average of selected broker assessments.

|

|||

|

USD/day

|

One-year T/C rate as of 5 March 2020

|

||

|

LR2

|

22,050

|

||

|

LR1

|

14,500

|

||

|

MR

|

15,300

|

||

|

Handysize

|

14,500

|

||

|

Note: The time charter market has limited liquidity.

|

|||

|

The most important factors affecting TORM’s earnings in 2020 are expected to be:

• The effects of the IMO 2020 sulfur regulation

• Global economic growth and consumption of refined oil products

• Refinery economics and maintenance

• Oil trading activity and developments in ton-mile trends

• Fleet growth and newbuilding ordering activity

• Bunker price developments

• One-off market-shaping events such as strikes, embargoes, political instability, weather conditions, COVID-19, etc.

|

|||

15

COVERED AND CHARTERED-IN DAYS IN TORM

– AS OF 31 DECEMBER 2019

– AS OF 31 DECEMBER 2019

|

2020

|

2021

|

2022

|

|

|

Owned days

|

|||

|

LR2

|

3,843

|

3,936

|

3,955

|

|

LR1

|

3,251

|

3,207

|

3,207

|

|

MR

|

16,187

|

16,452

|

16,595

|

|

Handysize

|

708

|

726

|

726

|

|

Total

|

23,988

|

24,322

|

24,483

|

|

2020

|

2021

|

2022

|

|

|

Chartered-in and leaseback days at fixed rate

|

|||

|

LR2

|

364

|

363

|

58

|

|

LR1

|

-

|

-

|

-

|

|

MR

|

3,379

|

3,630

|

3,110

|

|

Handysize

|

-

|

-

|

-

|

|

Total

|

3,743

|

3,993

|

3,168

|

|

2020

|

2021

|

2022

|

|

|

Total physical days

|

|||

|

LR2

|

4,207

|

4,299

|

4,013

|

|

LR1

|

3,251

|

3,207

|

3,207

|

|

MR

|

19,566

|

20,082

|

19,705

|

|

Handysize

|

708

|

726

|

726

|

|

Total

|

27,732

|

28,315

|

27,651

|

|

2020

|

2021

|

2022

|

|

|

Covered, %

|

|||

|

LR2

|

24%

|

2%

|

0%

|

|

LR1

|

12%

|

0%

|

0%

|

|

MR

|

5%

|

0%

|

0%

|

|

Handysize

|

5%

|

0%

|

0%

|

|

Total

|

9%

|

0%

|

0%

|

|

2020

|

2021

|

2022

|

|

|

Covered days

|

|||

|

LR2

|

1,006

|

69

|

-

|

|

LR1

|

397

|

-

|

-

|

|

MR

|

941

|

-

|

-

|

|

Handysize

|

32

|

-

|

-

|

|

Total

|

2,376

|

69

|

-

|

|

2020

|

2021

|

2022

|

|

|

Coverage rates, USD/day

|

|||

|

LR2

|

21,905

|

15,294

|

-

|

|

LR1

|

24,433

|

-

|

-

|

|

MR

|

24,248

|

-

|

-

|

|

Handysize

|

32,531

|

-

|

-

|

|

Total

|

23,399

|

15,294

|

-

|

|

Fair value of freight rate contracts that are mark-to-market in the income statement (USDm):

|

|||

|

Contracts not included above: USD -0.3m

|

|||

|

Contracts included above: USD 0.0m

|

|||

|

Actual no. of days can vary from projected no. of days primarily due to vessel sales and delays of vessel deliveries.

|

|||

16

Statement By The

Executive Director

TORM’s commercial performance has again in 2019 been among the best within our peer group. I believe this ability is due to our in-house operational One TORM platform which among other things

allows us to manage our cost at low break-even levels. Preparing for the IMO 2020 sulfur regulation has been an ongoing effort throughout 2019, and already in the first quarter of 2020 we are seeing the benefits of our preparations through

captured freight rate premiums on our 30 scrubber-fitted vessels.

Mr. Jacob Meldgaard, Executive Director

In 2019, TORM successfully navigated a volatile product tanker market that was impacted by the refining industry’s preparations for the IMO 2020 sulfur regulation. TORM’s results

in 2019 were enhanced by our strong operational focus and our focus on maintaining efficient operations and a low cost base.

The product tanker market strengthened notably following a significant increase in crude tanker rates due to attacks on Saudi Arabian oil facilities. This increase accelerated

dramatically after the US imposed sanctions on two subsidiaries of China’s COSCO Shipping. The last three months of 2019 provided a significant recovery for the broader tanker market supporting TORM’s earnings. For the full year 2019,

TORM’s product tanker fleet realized average Time Charter Equivalent (TCE) earnings of USD/day 16,526. The multi-year highs at the end of 2019 continued into 2020, positively impacted by the IMO 2020 sulfur regulation. But the market was

also negatively impacted by the global COVID-19 outbreak.

The first half of 2019 was impacted by the refining industry’s preparations for the IMO 2020 sulfur regulation. Refinery maintenance was pronounced, and coupled with a series of

unplanned outages, the volume of global refinery capacity

that was offline was 24% higher in the second quarter of 2019 compared to the same period in 2018. In particular, a heavy refinery maintenance season in Asia caused long-haul

diesel flows to drop significantly from the record levels seen in the first quarter of 2019. As the year progressed, geopolitical tensions were brought to the forefront with attacks on vessels near the Strait of Hormuz and the subsequent

attack on Saudi Arabia’s crude oil facilities. Although the effect was temporary, and most of the affected capacity was restored promptly, Saudi Arabia cut runs at several refineries in order to meet its crude export contracts. This

resulted in a decline in product exports, with naphtha flows to the Far East being affected.

STRONG TANKER RATES

Tanker rates surged at the start of the fourth quarter of 2019 when the US imposed sanctions on two subsidiaries of China’s COSCO Shipping. The reaction to the sanctions was first

seen in the crude tanker sector, where rates increased to the highest levels seen since 2008. The positive sentiment carried over into the product tanker segment, where rates for all vessel classes increased sharply before retreating to

levels that still remained elevated. The dramatic rise in crude tanker rates also caused around 15% of the LR2 fleet trading

in clean petroleum products to switch to crude, which will help to sustain product tanker rates over the medium term.

17

Statement

By The Executive Director

WELL PREPARED FOR IMO 2020

In preparation for the IMO 2020 sulfur regulation, TORM has committed to order a total of 49 scrubbers, meaning that slightly more than half of our fleet will be equipped with

scrubbers by the end of the first half of 2020. As the new regulation has been implemented, the business case for installing scrubbers has proven itself as the price spread between 0.5% compliant fuel and high sulfur fuel oil is at levels

strongly supporting the investment case. We believe that our balanced approach provides us with flexibility but also ensures exposure to the economic benefits of scrubbers. Our remaining fleet was prepared and customized to using

compliant fuel prior to 31 December 2019.

OPERATIONAL PERFORMANCE

Throughout 2019, TORM continued to focus on optimizing our fleet and operational performance to further pursue our goal of serving as the Reference Company in the product tanker

industry. To that end, TORM has reduced the expenditure related to the operation of the vessels (OPEX) through continued focus on optimization and planning of the vessels’ repair and maintenance schedules. This has been achieved, while

remaining very competitive on a TCE level through focus on the geographical positioning of the vessels.

The strong relative operational performance is supported by the ongoing development of the One TORM integrated in-house commercial and technical management to ensure a flexible

business approach that optimizes performance while maintaining a proper trade-off between maximizing TCE and minimizing cost. Further, the integrated nature of TORM's

business model provides transparency and additional alignment of management and shareholder interests, thereby mitigating the potential for actual or perceived conflicts of

interest with related parties. To further support the strong operational performance, TORM has continued focus on digitalization and enhancement of business intelligence to monitor the market and company-specific metrics.

ONE TORM SAFETY CULTURE

In line with the Company’s strategic focus on safety performance, TORM continued to promote the safety culture program One TORM Safety Culture –

driving resilience in 2019. The purpose of the program is to continuously strengthen TORM’s safety culture beyond mere compliance.

CLIMATE AND ENVIRONMENTAL EFFORTS

In 2009, TORM signed the UN Global Compact as the first shipping company in Denmark to commit to the internationally recognized set of principles regarding health, safety, labor

rights, environmental protection and anti-corruption. TORM has decided to have specific focus on Sustainable Development Goal (SDG) no. 4 Quality Education and on SDG no. 13 Climate Action, as these directly link to the Company’s current

corporate activities. These two areas are not only material to the Company and its stakeholders, the efforts and initiatives also make good business sense to TORM. As such, TORM sees its commitment to contributing to and reporting on the

SDGs as a natural progression of its commitment to the UN Global Compact.

In September 2019, TORM signed up for the Getting to Zero Coalition. TORM has decided to be an active member supporting the efforts to make commercially viable zero-emission

vessels a scalable reality by 2030. The initiative is supported by leading stakeholders from the maritime industry and the fuel value chain in addition to other large international corporations within sectors spanning wider than shipping.

Our support to the coalition also enables us to be agile if changes are made to the climate and environmental regulation in the future.

The Strategic Report on pages 3-61 has been prepared in accordance with the requirements of the Companies Act 2006 and is approved and signed on behalf of the Board of Directors.

|

Mr. Jacob Meldgaard

Executive Director

18

Strategic

Ambition and Business Model

TORM’s focus on operational improvement and integration is illustrated by TORM’s higher MR TCE earnings when compared to peers.

Long-lasting industry relationships and a strong capital structure drive fleet renewal and upgrades with a fully funded newbuilding program.

TORM’s proactive actions to comply with the IMO 2020 sulfur regulation include scrubber investments and the establishment of a scrubber

joint partnership.

joint partnership.

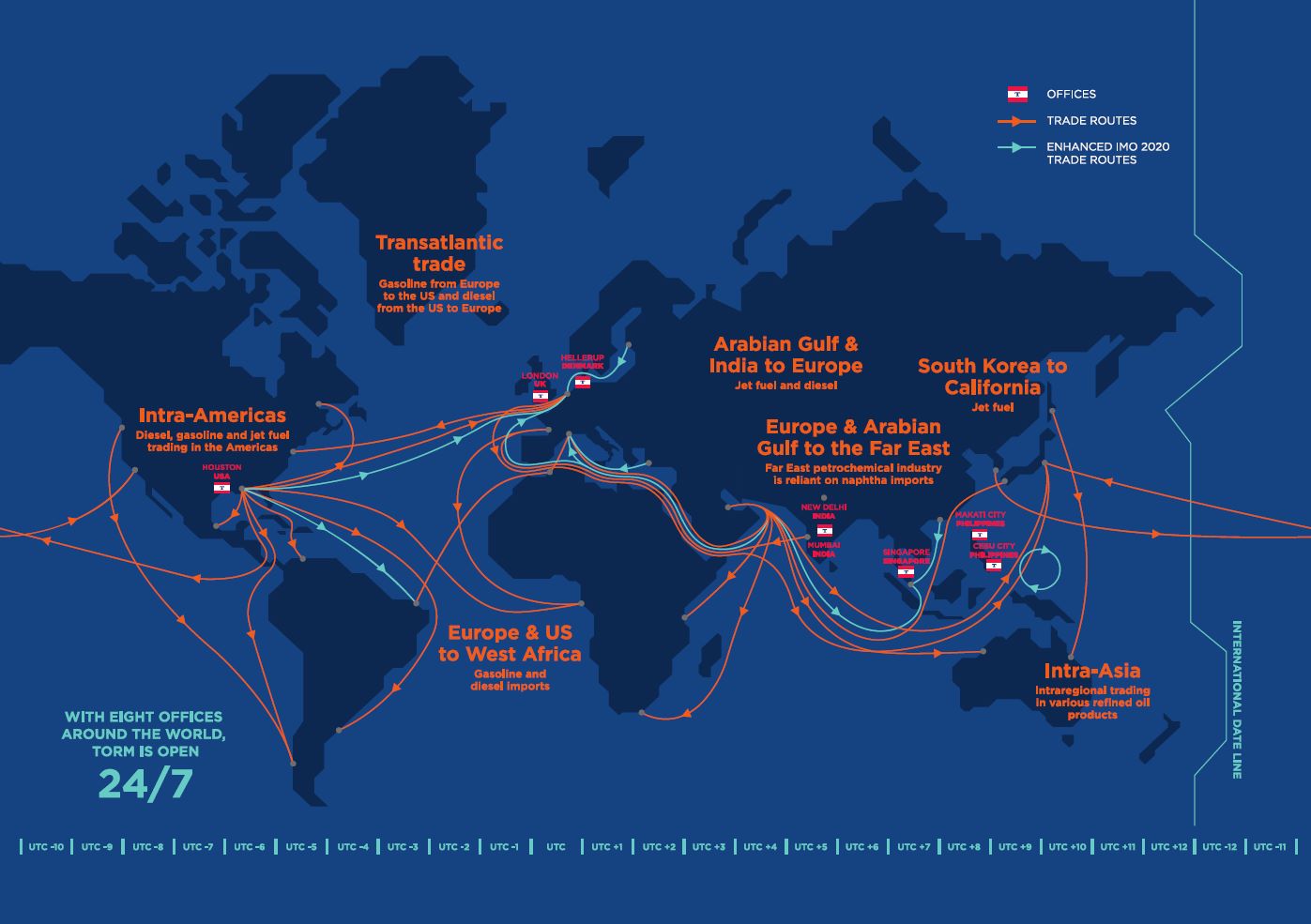

TANKER OWNER AND OPERATOR

TORM is a leading product tanker company with an owned fleet of 67 vessels on the water, 11 vessels under a sale and leaseback arrangement and three newbuildings as

of 11 March 2020. TORM is active within all larger product tanker segments (LR2, LR1, MR and Handysize). This enables TORM to meet customer demand, as global customers have transportation requirements across various vessel classes. TORM is

well positioned to take advantage of the promising long-term market supply and demand fundamentals by utilizing its extensive experience and expertise as a product tanker operator.

TORM’s chartering strategy is to employ the fleet primarily in the spot market, where the Company can optimize earnings from voyage to voyage. TORM may seek to

employ some of its vessels on longer-term time charter-out contracts if customer needs and expected returns are compelling. Due to the large scale of TORM’s fleet, TORM will only enter into long-term charter-in commitments on a case-by-case

assessment and only to the extent they are likely to result in profit.

The Company believes that ownership of vessels combined with TORM’s integrated platform provides a level of control that is essential for ensuring the maximum

amount of flexibility and earning power. At the same time, short-term charter-in agreements (less than 12 months) are consistently evaluated on

an opportunistic basis as part of TORM’s active spot-oriented market approach.

SELECTIVE FLEET RENEWAL AND GROWTH

TORM may selectively grow its tanker fleet and serve as a consolidator in the tanker segment if the right opportunities arise. TORM’s sale and purchase activities

are conducted by our in-house team that leverages relationships with shipbrokers, shipyards, financial institutions and shipowners.

TORM is continuously assessing opportunities to optimize asset management through acquiring attractive high-specification second-hand product tankers that will be

franchise-enhancing and financially accretive. TORM also selectively pursues newbuilding programs with high-quality shipyards when newbuilding contracts provide higher expected return, or if the second-hand market has insufficient supply of

vessels that meet TORM’s customer requirements. In 2019, TORM acquired four additional second-hand vessels at attractive price points below the market benchmarks. In January 2020, TORM made an additional purchase of two fuel-efficient

dual-fuel-ready LR2 newbuildings with scrubbers. The vessels will be delivered in the fourth quarter of 2021.

The specific acquisition criteria for newbuildings and second-hand vessels include:

|

•

|

Price point attractiveness

|

|

•

|

Complementarity to the current fleet

|

|

•

|

Vessel quality level and origin (quality yard)

|

|

•

|

Operational characteristics including main engine design, bunker consumption and cargo intake

|

TORM will from time to time sell vessels that no longer fit the commercial strategy, or if the price point is deemed attractive. During 2019, TORM sold eight older

vessels.

TORM’s in-house technical management has significant experience in newbuilding projects from design to delivery. As of 11 March 2020, TORM’s newbuilding program

consists of one MR vessel with expected delivery in the second quarter of 2020 and two LR2 vessels with expected delivery in the fourth quarter of 2021. In addition, TORM has taken delivery of two LR1 and six MR newbuildings since January

2019.

19

Strategic

Ambition and Business Model

SOLID CAPITAL STRUCTURE

TORM has a solid capital structure combined with a strong liquidity position, a fully funded newbuilding program, no near-term debt maturities and limited off-balance

sheet charter-in commitments. The Company has an attractive debt profile with favorable interest rates, amortization schedules and covenants.

TORM’s capital structure supports a spot employment strategy and also enhances the Company’s financial and strategic flexibility. In addition, balance sheet strength

creates a competitive advantage when pursuing vessel acquisitions, as counterparties prefer well-capitalized companies. TORM plans to finance its business and fleet growth with a combination of operating cash flows, cash-on-hand as well as

financing from lenders and the capital markets. In early 2020, TORM obtained commitment from leading ship lending banks for two separate term facilities and a revolving credit facility of up to a total of USD 496m. These facilities replace

four term loans and TORM’s existing revolving credit facility that all together on a fully drawn basis cover USD 502m in debt. Following the refinancing, TORM does not have any major debt maturities until 2026. Secured bank financing remains

the preferred source of debt funding for TORM, but recent leasing structures reflect TORM’s broad access to various sources of competitive financing. To support the capital structure, TORM works towards improving the liquidity in the

Company’s share to attract a broader investor base. TORM is continuously marketing the share towards investors via investor roadshow activities, conference participation and panel discussions. In addition, TORM listed its share on Nasdaq in

New York in 2017, thereby providing access to a broader base of potential investors. In February 2019, TORM plc’s USD 250m universal shelf registration on Form F-3

became effective with the Securities and Exchange Commission.

ONE TORM – INTEGRATED OPERATING PLATFORM

TORM’s fleet is managed cost-efficiently and effectively by the in-house commercial and technical management teams, which have an industry reputation for strong

commercial performance, safety and operational expertise. Within the One TORM platform, TORM’s employees ensure the high quality of the fleet required by our customers under their strict vetting criteria. TORM believes that the largest

customers prefer an integrated operating model as it provides them with better accountability and insight into safety and vessel performance. Within the One TORM platform, digitalization and enhancement of business intelligence are key focus

areas in order to optimize vessel performance.

The integrated nature of TORM’s operating platform provides transparency and additional alignment of management and shareholder interests, which mitigates the

potential for actual or perceived conflicts of interest with related parties. In addition, it allows for closer control over operating expenses. This is also seen in our competitive OPEX of USD/day 6,371 in 2019.

TORM’s large diverse fleet of well-maintained product tankers gives the Company the advantages of scale both commercially and in terms of cost-efficiency compared to

smaller product tanker owners. The Company’s Management believes that the combination of well-maintained vessels, a presence in all product tanker segments and an integrated operating platform provides the commercial management team with

enhanced flexibility and responsiveness to customer demands. As a result,

TORM has consistently delivered MR TCE earnings and cash flows above industry average.

TORM’s integrated model includes a strategic focus on safety performance. In line with the Company’s strategic focus on safety performance, TORM continued to promote

the safety culture program One TORM Safety Culture – driving resilience in 2019. The purpose of the program is to continuously strengthen TORM’s safety culture beyond mere compliance. This reflects

TORM’s belief that profitability and safety are not mutually exclusive.

It is a key priority for TORM, as a Reference Company in the industry, to minimize pollution of the seas and the atmosphere. Thus, TORM has strong focus on reducing

fuel consumption and CO2 emissions as this is not only good for the environment but also for TORM’s business. This is achieved through committed focus on optimal performance, and industry collaboration.

TORM has identified a number of strategic Key Performance Indicators (KPIs) that the Company believes are vital for the fulfillment of its strategic goals. These

strategic KPIs are described on page 31.

20

Strategic

Ambition and Business Model

21

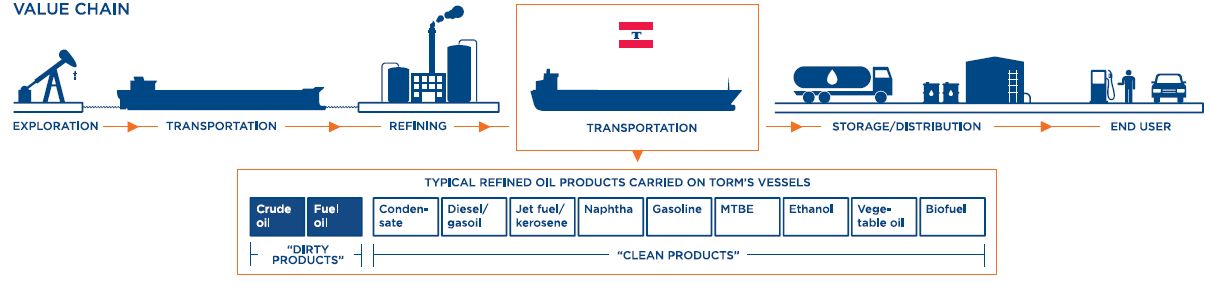

Value Chain in

Oil Transportation

The global oil industry includes a range of activities and processes which contribute to the transformation of primary petroleum resources into usable end products

for industrial and private customers.

The value chain begins with the identification and subsequent exploration of productive petroleum fields. The unrefined crude oil is transported from the production

area to refinery facilities by crude oil tankers, pipelines, road and rail.

TORM is primarily involved in the transportation of refined oil products from the refineries to the end user. In addition to clean products, TORM uses some of its

vessels for transportation of residual fuels from the refineries as well as crude oil directly from the production field to the refinery. These fuel types are commonly referred to as dirty petroleum products, as extensive cleaning of the

vessel’s cargo tanks is required before a vessel can transport clean products again.

In 2019, 95% of TORM's turnover was generated from clean products transportation.

TORM’s integrated operating platform with in-house technical and commercial management enhances responsiveness to customers’ demands and allows TORM to generate value for stakeholders as well as for the Company.

The long-term success of the Company is dependent on TORM’s ability to provide safe and reliable transportation services. In addition to the items explicitly stated in the financial statements, the long-term success of the Company

further builds on the intellectual property of the workforce at TORM and the relationship and cooperation with external stakeholders such as oil traders, state-owned oil companies, oil majors, financial institutions, shipyards, brokers

and governmental agencies.

TORM values the relationship with its key stakeholders and aims at conducting business for the benefit of the Company’s shareholders and other stakeholders. TORM has

supported the UN Global Compact since 2009 and is committed to supporting the UN Sustainable Development Goals. TORM was the first shipping company in Denmark to commit to the internationally recognized set of principles.

Market

The interaction with key stakeholders is described on pages 19-21 under “Strategic Ambition and Business Model”. For more information on broader value generation and

TORM’s Corporate Social Responsibility (CSR) policy, please see pages 49-60.

22

The Product

Tanker Market

Despite volatility, average product tanker earnings in 2019 reached the highest levels since 2015.

Looking ahead, the product tanker market is supported by positive demand developments and limited supply growth.

Looking ahead, the product tanker market is supported by positive demand developments and limited supply growth.

2019 PRODUCT MARKET

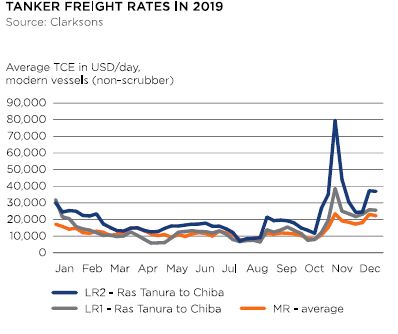

After strong rates at the start of the year, the product tanker market softened through the second and third quarters, before posting a strong recovery in the fourth

quarter with freight rates for larger vessels peaking at levels not seen since 2008.

Demand for oil products was negatively affected by general macroeconomic weakness, resulting in subdued oil demand growth. This together with new refining capacity

entering the market kept refinery margins generally under pressure, notwithstanding temporary margin hikes. Refinery margins deteriorated, especially in Asia, due to slower oil demand growth, new refineries ramping up production and the

region’s typical crude diet becoming more expensive relative to other benchmark regions.

Product tanker freight rates started the year at strong levels supported by open long-haul arbitrage trades and a more supportive supply side after a considerable

number of LR2 vessels had switched to the dirty market at the end of 2018. On the other side, strong diesel arbitrage economics between the East and the West incentivized a high number of newbuilt crude tankers to carry clean petroleum

products on their maiden voyage from the East to the West. This was further intensified by a frontloaded crude tanker newbuilding program

for 2019, with deliveries in the first quarter being particularly high.

Product tanker rates softened nevertheless as spring refinery maintenance gained pace and narrowed the arbitrage opportunities. Refinery maintenance was not only

particularly heavy in 2019, but it also stretched over a longer period than normal, not peaking until May. The particularly heavy spring refinery

maintenance in 2019 was influenced by the refineries’ preparations for the IMO 2020 marine fuel shift. In several regions, planned refinery maintenance was coupled

with series of unplanned outages and economic run cuts amid lower-than-average refinery margins. For example, a crude oil contamination in the Druzhba pipeline in Russia disrupted work at several European refineries. In the US, outages at a

number of gasoline-producing units and the closure of the largest refinery on the US East Coast supported transatlantic and transpacific gasoline flows.

23

The Product

Tanker Market

Towards the end of the third quarter, the tanker market was shaken by attacks on Saudi Arabia’s oil facilities and the imposition of US sanctions on two subsidiaries

of China’s COSCO Shipping, with the latter affecting around 4% of the global VLCC fleet. This initially sent crude tanker rates to highs not seen since 2008, further spreading to the product tanker market with the impact especially pronounced

in the larger segments. The strong reaction of the crude tanker freight rates encouraged several LR2 vessels to switch into dirty trades at the end of the third quarter, during the fourth quarter and into the first months of 2020. This

corresponded to a drop in clean-trading LR2 capacity of around 15% and was further supported by a temporary removal of vessels for scrubber retrofitting, which gained pace in the second half of the year. In addition, crude tanker

cannibalization eased in the second half of the year as the crude market improved and newbuilding deliveries decreased.

After the initial strong surge in product tanker freight rates, the rates underwent a downward correction yet remaining at strong

levels, with rates in the fourth quarter being the highest since the third quarter of 2015. Rates were supported by seasonal demand and multiple open product arbitrage opportunities. Indian diesel exports to the western hemisphere

showed strong momentum. Similarly, gasoline flows from Europe to the Middle East and West Africa picked up. Naphtha arbitrage flows from the West to the East reached a 6-month high in November-December. New refinery capacity ramping up in

China continued to support the country’s product exports.

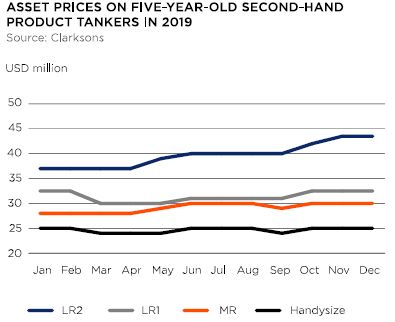

With an improved freight market, vessel values continued to increase. Asset prices on second-hand product tankers

climbed by 9% for modern MR tonnage and 24% for modern LR2 tonnage (source: Clarksons).

Strong freight rates carried over into the start of 2020, as LR2 vessels continued to shift to dirty trades and vessel availability was reduced by scrubber retrofits.

However, the start of a heavy refinery maintenance in the Middle East and a weakening sentiment due to removal of the COSCO sanctions and the outbreak of the COVID-19 in particular weighted on the crude and product tanker markets.

TORM

The value of TORM's fleet measured by broker values increased by 6% during 2019 (when adjusted for vessels acquired and sold during 2019).

In 2019, TORM achieved a gross profit of USD 252m (2018: USD 169m). The increase from 2018 was driven by higher freight rates. TORM’s product tanker fleet realized

TCE

earnings of USD/day 16,526, up 27% year on year, with the LR2 segment at USD/day 19,730, the LR1 segment at USD/day 17,102, the MR segment at USD/day 15,840 and the

Handysize segment at USD/day 14,965.

During 2019, TORM took delivery of five MR vessels from Guangzhou Shipyard International (GSI) all equipped with a scrubber. In January 2020, TORM made an additional

purchase of two fuel- efficient dual-fuel-ready LR2 newbuildings with scrubbers.

ORDER BOOK

As of 31 December 2019

|

Fleet 31.12.2018

|

Delivered in 2019

|

Recycled in 2019

|

Fleet 31.12.2019

|

Order book for 2020-2022

|

Order book as % of end-2019 fleet

|

|

|

LR2

|

358

|

26

|

0

|

384

|

39

|

10%

|

|

LR1

|

364

|

12

|

4

|

372

|

8

|

2%

|

|

MR

|

1,646

|

88

|

14

|

1,720

|

154

|

9%

|

|

Handysize

|

720

|

26

|

8

|

738

|

22

|

3%

|

|

Total

|

3,088

|

152

|

26

|

3,214

|

223

|

7%

|

24

The Product

Tanker Market

As of 11 March 2020, TORM has taken delivery of three additional newbuildings from GSI – one MR vessel and two LR1 vessels. One remaining MR newbuilding is expected

to be delivered in April 2020, and two LR2 vessels are expected to be delivered in the fourth quarter of 2021.

At the end of 2019, TORM operated a fleet of 76 vessels on the water, of which 65 are fully owned and 11 are financial leaseback.

MARKET DRIVERS AND OUTLOOK

Tonnage supply

In 2019, the global product tanker fleet grew by 4.7% in terms of capacity (4.1% in terms of number of vessels). This was up from 2.4% in 2018, which was the lowest

growth in more than 20 years. Vessel deliveries increased in all segments. Fleet growth ranged from 7.3% for the LR2 segment, 2.2% for the LR1 segment,

4.5% for the MR segment and 2.5% for the Handysize segment. However, effective tonnage supply growth was reduced by the LR2 net migration to the dirty market as well

as temporary removal of vessels from the market for scrubber retrofitting, with the latter reportedly experiencing delays compared to initially planned timelines.

4.7%

Product tanker fleet growth

The number of newbuilding orders placed in 2019 remained at similar levels as in 2018, thus remaining below the ten-year

average level. A total of 87 product tankers were ordered in 2019 compared to an annual average of 118 over the past decade. The MR segment accounted for the majority

of orders with 62 units contracted, while the number of LR2 vessels ordered was 23. At the end of 2019, the existing order book for deliveries in 2020-2022 totaled 223 units (corresponding to 6.9% of the current fleet), including 39 LR2

vessels, 8 LR1 vessels, 154 MR vessels and 22 Handysize vessels.

Taking into account lead time in production, TORM anticipates limited ordering of new product tankers with delivery before the end of 2021. Along with improvements on

the freight market, TORM expects ordering activity in 2020 to increase from the relatively low levels seen in the last couple of years. Nevertheless, the ordering activity is expected to remain below the peaks seen in the previous years

underpinned by uncertainty around requirements for vessel propulsion systems in the future.

Around 1.2m dwt of product tanker capacity was recycled in 2019, corresponding to approximately 0.7% of the fleet capacity as of the end of 2018. This was down from

2.2m dwt in the previous year. TORM estimates that approximately 3% of the existing capacity of the global fleet will be phased out or recycled during 2020-2022, as these vessels reach an age where trading possibilities are limited.

With a historically low order book and low probability of over-ordering in the coming years, TORM expects the net product tanker fleet capacity to grow by a compound

annual rate of approximately 3% during 2020-2022.

Tonnage demand

With a slowdown in several major consuming regions and countries, the global demand for oil products grew by 0.9 mb/d in 2019 (source: IEA OMR February 2020). Looking

at individual products, diesel demand was affected by weak global industrial performance, while LPG continued to replace naphtha in the petrochemical industry especially in the OECD countries. In 2020, global oil demand is projected to grow

by around 0.8 mb/d, the lowest since 2011, as the outbreak of the COVID-19 and the widespread shutdown of the Chinese economy are expected to have shaved off around 0.4 mb/d of the global growth (source: IEA OMR February 2020). Nevertheless,

the sharp decline in oil demand in China in the first quarter of the year (and the corresponding cut in refinery runs) is expected to be followed by a rebound that is likely to be supported by additional government stimulus measures.

Clean petroleum product inventories, which were contributing to the market weakness in the previous three years, normalized at historical levels in 2019. This removed

some of the headwinds from the product tanker market recovery.

25

The

Product Tanker Market

In 2020, the market will be affected by the IMO 2020 sulfur regulation. TORM expects that the shift towards low sulfur fuels could lead to an increase of up to 1 mb/d

in demand for diesel/gasoil as a low sulfur bunker fuel or as a feedstock for the latter. This, in turn, is expected to lead to higher interregional trade with clean petroleum products, which will support the product tanker market. The

regions that are diesel net exporters already today have more flexibility to increase diesel production compared to net importing regions, leading to additional demand for large- and medium-sized product tankers. For example, new refining

capacity comes online in Asia and the Middle East, while the complex refining system in the US Gulf allows the region to a higher degree to take advantage of the cheaper excess high sulfur fuel oil (HSFO) in producing cleaner fuels such as

gasoline and diesel/gasoil. The latter development was already clearly visible in the last months of 2019, with increasing flows of HSFO from Russia to the US Gulf refining hub. On top of increased interregional trades, demand for smaller

vessels is expected to increase for intraregional redistribution of new bunker fuels.

The initial evidence from the IMO 2020 effects shows that in the first month of the implementation of the new sulfur rules, uptake of very low sulfur fuel oil (VLSFO) in Singapore, the world’s largest bunkering hub, increased strongly as

owners rushed to shift to new compliant fuels and test the available VLSFO supplies. This development continued into the first month of 2020, leaving gains in marine gas oil (MGO) demand relatively limited. However, the price difference

between MGO and VLSFO has been very low or even

negative so far this year, which has reportedly led to several vessel owners in Europe opting for MGO instead of VLSFO. Also, the VLSFO availability could be lower

during the summer months when a stronger gasoline market increasingly competes for feedstocks.

On the tonnage supply side, the temporary removal of vessels from the market for scrubber retrofitting that already started in 2019 will continue in 2020, thereby

supporting the market.

Over the longer term, global refinery capacity additions will exceed the growth in oil demand, adding to the already existing oversupply of the global refining

capacity. While new

refining capacity is primarily located in Asia and the Middle East, the competitive pressure on older and less efficient refineries in regions such as Europe and

South America will thus increase.

26

The

Product Tanker Market

|

For the European refineries, this effect will be aggravated by increased difficulties in finding export markets for the region’s excess gasoline, as fuel

efficiency gains in regions like North America and new refining capacity coming online in West Africa will reduce demand from the traditional gasoline outlets. Despite refinery capacity addition in Asia and slower demand growth compared

to previous years, the regions’ naphtha deficit is expected to increase, thereby supporting long-haul product tanker trade.

Subsequently, TORM expects the product tanker ton-mile demand on main trade routes to grow by a compound annual rate of around 4 % during 2020-2022, driven by a

shift in demand for marine bunkers towards cleaner fuels and trends in geographical refinery relocation. Generally, positive trends on the product tanker demand side combined with limited tonnage supply growth support a positive freight

market development in the next three-year period, although market volatility is expected.

For further details on factors most likely to change this outlook in either a negative or a positive direction, please see “Outlook” section on pages 14-16.

|

|

27

imo 2020 sulfur

regulation

REGULATION

In October 2016, IMO’s Marine Environment Protection Committee (MEPC) announced that as of 1 January 2020, the global limit for sulfur emissions from fuel oil used on

board vessels operating outside designated emission control areas will be reduced from 3.5% to 0.5%. This will significantly reduce the amount of sulfur oxides emanating from vessels and should have major health and environmental benefits for

the world.

There are two relevant methods for TORM vessels to comply with the new sulfur regulation:

Install an exhaust gas cleaning system, also known as a “scrubber”, which is designed to remove sulfur oxides from a vessel’s engine and boiler exhaust gases, or use

compliant fuel with a sulfur content level below 0.5%

TORM IMO 2020 SULFUR LIMIT PREPARATIONS

TORM has been preparing for the sulfur regulation since 2016, when the first internal sulfur compliance working team was established. The work has included committed

scrubber installations including pilot installations and a joint venture with a scrubber production facility. In addition, TORM ensured that the remaining fleet would be in compliance by 1 January 2020.

Committed scrubber installations

TORM has committed to install 49 scrubbers on both newbuildings and second-hand vessel and has already installed 30 scrubbers as of 11 March 2020. These scrubbers are

installed on two LR2, six LR1 and 22 MR vessels based on a business case and technical and commercial considerations.

Scrubber partnership

In order to secure availability of scrubbers and to forge a closer relationship with the China State Shipbuilding Corporation (CSSC) yard group, TORM established a

joint venture in 2018 with Guangzhou Shipyard International, which is part of the CSSC group, and ME Production, a leading scrubber manufacturer. TORM holds an ownership stake of 27.5% in the joint venture: ME Production China.

The main benefits to TORM have been increased flexibility to secure scrubber production slots. In addition, if the partnership continues to prove successful, TORM

will generate an additional income stream.

ME Production China’s production of scrubbers commenced in November 2018, and the company will deliver a total of 43 scrubbers to TORM.

Scrubber experiences

Throughout 2019, TORM has gained valuable experience from using and installing scrubbers through the pilot scrubber installations on TORM Hilde and TORM Lene. Further

knowledge has been gained from the additional 18 scrubber installations that have taken place in the second half of 2019 on both newbuildings and vessels on the water. These installations have helped TORM to be fully able to use the scrubbers

from 1 January 2020.

28

imo 2020

sulfur regulation

0.5% compliant fuel readiness for remaining fleet

In early 2019, TORM initiated an internal working group to ensure that the remaining TORM fleet without scrubbers would be in full compliance with the IMO 2020 sulfur

regulation by using compliant fuel.

This work included the emptying and cleaning of tanks and investigating potential tank modifications as well as testing, assessing and evaluating the specifications

of the new 0.5% compliant fuels including determining the commingling ability. In the second half of 2019, there was also focus on training the crew to handle the new fuels and ensuring that the vessels switched over to the new 0.5% compliant

fuel as late in December 2019 as possible in order to save fuel costs.

On a global scale, published data on bunker sales shows that the shift from high sulfur fuel oil (HSFO) to low sulfur fuel oil (VLSFO) took off in the last months of

2019, as vessel operators were taking measures to prepare for the IMO 2020 sulfur regulation. In one of the largest bunker hubs, Singapore, the HSFO market share dropped to barely 28% in December from 85% in September. It was primarily VLSFO

that replaced HSFO, reaching a market share of 59% from just 4% three months earlier, when the shipping industry was testing the new compliant fuel. Initial gains in marine gas oil (MGO) demand were less pronounced, reaching an 12% market

share, which was nevertheless up from 7% at the start of 2019 and has a potential to increase further when VLSFO inventories ran down and its supply is limited due to feedstock competition for the gasoline pool.

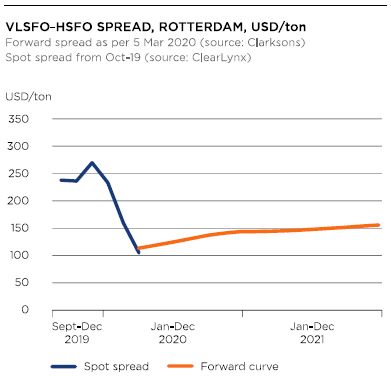

A strong increase in VLSFO demand in the last quarter of 2019 coupled with logistical challenges at a number of bunkering ports supported VLSFO prices, resulting in

VLSFO-HSFO spot spreads in Rotterdam reaching new highs of above USD 300 per ton. In Singapore, VLSFO even reached a premium to the MGO price in December. In the first week of 2020, the VLSFO-HSFO forward spread for the calendar year 2020

peaked at around USD 275 per ton. The recent COVID-19 outbreak and the accompanying fall in the crude oil price have caused the VLSFO-HSFO spot and forward spreads to fall to new lows as the HSFO has recently been linked to the crude oil

price while the new VLSFO product has decreased even further. The spot spread as of 5 March 2020 was USD 109 per ton while the 2021 forward spread was USD 151 per ton. With these spreads, TORM’s scrubber investment has a payback time well

below three years.

29

30

Key Performance

Indicators

For TORM to be considered the Reference Company, TORM assesses the Company’s performance across a wide range of measures and indicators against strategic targets.

|

MR TCE Earnings

USD/day

|

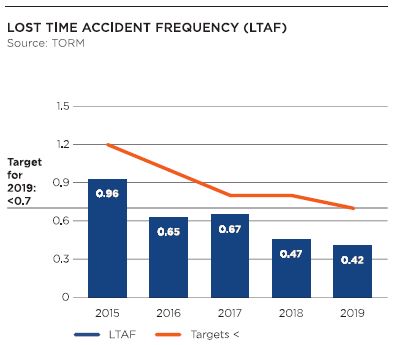

Lost Time Accident Frequency (LTAF)

|

Adjusted Return on Invested Capital (RoIC)

|

Fuel Efficiency Improvement

|

||||||

|

2019: 15,840

2018: 12,847

|

2019: 0.42

2018: 0.47

|

2019: 4.9%

2018: 0.1%

|

2019: 9.3%

2018: 6.9%

|

||||||

|

In 2019, TORM’s commercial performance has consistently been among the best within its peer group. This can be accredited to the Company’s well-maintained fleet

and the integrated operating platform.

This combination provides TORM’s commercial management team with the flexibility and responsiveness to meet customer demands, thereby enabling TORM to outperform

available earning benchmarks.

In 2019, TORM achieved MR TCE earnings of USD/day 15,840 up from USD/day 12,847 in 2018 due to the One TORM platform and the general market development.

|

In line with the Company’s strategic focus on safety performance, TORM continued to promote the safety culture program One

TORM Safety Culture – driving resilience in 2019.

LTAF is an indicator of serious work-related personal injuries that result in more than one day off work per million work hours. The definition of LTAF follows

standard practice among shipping companies.

During 2019, TORM had an improvement of LTAF to 0.42 compared to 0.47 in 2018.

|

Adjusted RoIC illustrates TORM’s ability to generate shareholder value from the capital invested in TORM. It is defined as the net operating profit after tax

(excluding impairment charges or reversals) divided by the invested capital over the same period (excluding impairment charges).

In 2019, TORM achieved an adjusted RoIC of 4.9% compared to 0.1% in 2018. The increase in RoIC from 2018 to 2019 is driven by higher freight rates.

This KPI reflects that although the average age of TORM’s fleet is approximately 11 years, TORM is still able to generate a very attractive RoIC compared to its

peers.

|

Fuel efficiency improvement illustrates TORM's continued strong focus on reducing fuel consumption and the efforts made in this area.

In 2018, TORM improved fuel efficiency by 6.9% compared to a 2015 baseline figure. In 2019, TORM has continued its efforts and achieved further improvements

bringing the fuel efficiency to 9.3% compared to the 2015 baseline. This impressive reduction is a testimony to the strengths of our One TORM platform.

|

31

The Torm fleet

as of 11 March 2020

LR2

Long Range 2 vessels are the largest vessels in TORM’s fleet. They are typically employed on longer trade routes, including naphtha transportation from the Middle

East to the Far East and diesel from the eastern hemisphere into the Atlantic. 12 vessels are currently on the water, and two newbuildings are expected to be delivered in 2021.

MR

The Medium Range vessels are often referred to as the “workhorse” of the product tanker fleet. They cover more trade routes and, compared to the

larger LR vessels, this vessel type has the flexibility to enter into more ports and cover shorter and coastal trades. A typical trade for MR vessels would be gasoline from Europe to the US East Coast.

55 vessels are currently on the water, and one newbuilding is expected to be delivered in the second quarter of 2020.

LR1

Long Range 1 vessels are typically employed on the same routes as LR2 vessels, but they also have the flexibility to cover trades and routes that are traditionally

dominated by the smaller MR vessels. A typical LR1 trade could be diesel or jet fuel from the Middle East to Europe.

Handysize

Handysize vessels are the smallest vessels in TORM’s fleet. They are involved in more varied and typically shorter and coastal trade routes. Typical trades for a

Handysize vessel include transportation of various clean petroleum products within Europe and in the Mediterranean.