UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| (Mark One) | ||

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(B) OR 12(G) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| OR | ||

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2015 | |

| OR | ||

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| OR | ||

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Date of event requiring this shell company report……………

For the transition period from to

Commission file number 001-37602

| Fuling Global Inc. |

| (Exact name of Registrant as specified in its charter) |

| Cayman Islands |

| (Jurisdiction of incorporation or organization) |

| Southeast Industrial Zone, Songmen Town |

| Wenling, Zhejiang Province |

| People’s Republic of China 317511 |

| (Address of principal executive offices) |

| Gilbert Lee, Chief Financial Officer |

| +1-610-366-8070 – telephone |

|

ir@fulingplasticusa.com Fuling Plastic USA, Inc. |

| 6690 Grant Way, Allentown, PA 18106 |

| (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Ordinary Shares, par value $0.001 per share | Nasdaq |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report: 15,732,795 Ordinary Shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

¨ Yes x No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

¨ Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP x | International Financial Reporting Standards as issued by the International Accounting Standards Board ¨ |

Other ¨ |

If "Other" has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).

¨ Yes x No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

¨ Yes ¨ No

Table of Contents

| 2 |

Conventions Used in this Annual Report

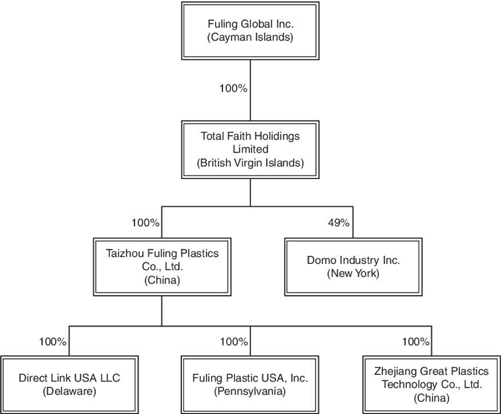

Except where the context otherwise requires and for purposes of this annual report on Form 20-F only, “we,” “us,” “our company,” “Company,” “our” and “Fuling” refer to:

| • | Fuling Global Inc., a Cayman Islands company (“FGI” when individually referenced), which is the parent holding company; | |

| • | Total Faith Holdings Limited, a British Virgin Islands company (“Total Faith” when individually referenced), which is a wholly owned subsidiary of FGI; | |

| • | Taizhou Fuling Plastics Co., Ltd., a PRC company (“Taizhou Fuling”), which is a wholly owned subsidiary of Total Faith; | |

| • | Domo Industry Inc., a New York company (“Domo”), of which Total Faith owns 49% of the equity but maintains effective control; | |

| • | Direct Link USA LLC, a Delaware company (“Direct Link”), which is a wholly owned subsidiary of Taizhou Fuling; | |

| • | Fuling Plastic USA, Inc., a Pennsylvania company (“Fuling USA”), which is a wholly owned subsidiary of Taizhou Fuling; and | |

| • | Zhejiang Great Plastics Technology Co., Ltd., a PRC company (“Great Plastics”), which is a wholly owned subsidiary of Taizhou Fuling. |

This annual report contains translations of certain RMB amounts into U.S. dollar amounts at a specified rate solely for the convenience of the reader. The exchange rates in effect as of December 31, 2015 and 2014 were US $1.00 for RMB 6.4917 and RMB 6.1460, respectively. The average exchange rates for the years ended December 31, 2015 and 2014 were US $1.00 for RMB 6.2288 and RMB 6.1457, respectively. We use period-end exchange rates for assets and liabilities and average exchange rates for revenue and expenses. Capital accounts are translated at their historical exchange rates when the capital transactions occurred. Any discrepancies in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

For the sake of clarity, this annual report follows the English naming convention of first name followed by last name, regardless of whether an individual’s name is Chinese or English. For example, the name of the Chief Operating Officer and Chair of our board of directors will be presented as “Guilan Jiang,” even though, in Chinese, Ms. Jiang’s name is presented as “Jiang Guilan.”

We obtained the industry and market data used in this annual report or any document incorporated by reference from industry publications, research, surveys and studies conducted by third parties and our own internal estimates based on our management’s knowledge and experience in the markets in which we operate. We did not, directly or indirectly, sponsor or participate in the publication of such materials, and these materials are not incorporated in this annual report other than to the extent specifically cited in this annual report. We have sought to provide current information in this annual report and believe that the statistics provided in this p annual report remain up-to-date and reliable, and these materials are not incorporated in this annual report other than to the extent specifically cited in this annual report.

SPECIAL CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

Certain matters discussed in this report may constitute forward-looking statements for purposes of the Securities Act of 1933, as amended (the “Securities Act”), and the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from the future results, performance or achievements expressed or implied by such forward-looking statements. The words “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate,” and similar expressions are intended to identify such forward-looking statements. Our actual results may differ materially from the results anticipated in these forward-looking statements due to a variety of factors, including, without limitation, those discussed under “Item 3—Key Information—Risk Factors,” “Item 4—Information on the Company,” “Item 5—Operating and Financial Review and Prospects,” and elsewhere in this report, as well as factors which may be identified from time to time in our other filings with the Securities and Exchange Commission (the “SEC”) or in the documents where such forward-looking statements appear. All written or oral forward-looking statements attributable to us are expressly qualified in their entirety by these cautionary statements.

| 3 |

The forward-looking statements contained in this report reflect our views and assumptions only as of the date this report is signed. Except as required by law, we assume no responsibility for updating any forward-looking statements.

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable for annual reports on Form 20-F.

Item 2. Offer Statistics and Expected Timetable

Not applicable for annual reports on Form 20-F.

A. Selected Financial Data

The following table presents the selected consolidated financial information for our company. The selected consolidated statements of comprehensive income data for the two years ended December 31, 2014 and 2015 and the selected consolidated balance sheets data as of December 31, 2014 and 2015 have been derived from our audited consolidated financial statements, which are included in this annual report beginning on page F-1. Our historical results do not necessarily indicate results expected for any future periods. The selected consolidated financial data should be read in conjunction with, and are qualified in their entirety by reference to, our audited consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” below. Our audited consolidated financial statements are prepared and presented in accordance with US GAAP.

(All amounts in thousands of U.S. dollars, except Dividend per share in Renminbi and Shares outstanding)

Statement of operations data:

| For the year ended December 31, | ||||||||

| 2015 | 2014 | |||||||

| Revenues | $ | 91,294 | $ | 83,181 | ||||

| Gross profit | $ | 23,648 | $ | 22,077 | ||||

| Operating expenses | $ | 14,678 | $ | 12,429 | ||||

| Income from operations | $ | 8,970 | $ | 9,649 | ||||

| Provision for Income taxes | $ | 1,442 | $ | 1,369 | ||||

| Net income | $ | 7,948 | $ | 7,728 | ||||

| Income from operations per share | $ | 0.73 | $ | 0.83 | ||||

| Net income per share (basic and diluted) | $ | 0.65 | $ | 0.64 | ||||

| Dividend per share in USD | $ | 0 | $ | 0.88 | ||||

| Dividend per share in Renminbi | ¥ | 0 | ¥ | 5.41 | ||||

Balance sheet data:

| As of December 31, | ||||||||

| 2015 | 2014 | |||||||

| Current assets | $ | 49,846 | $ | 34,700 | ||||

| Total assets | $ | 75,729 | $ | 57,224 | ||||

| Current liabilities | $ | 32,411 | $ | 39,769 | ||||

| Total liabilities | $ | 32,411 | $ | 39,769 | ||||

| Total shareholders’ equity (net assets) | $ | 43,319 | $ | 17,455 | ||||

| Capital stock | $ | 16 | $ | 12 | ||||

| Shares outstanding | 15,732,795 | 11,666,667 | ||||||

| 4 |

Exchange Rate Information

Our financial information is presented in U.S. dollars. Our functional currency is Renminbi (“RMB”), the currency of the PRC. Transactions denominated in currencies other than RMB are translated into RMB at the exchange rate quoted by the People’s Bank of China at the dates of the transactions. Exchange gains and losses resulting from transactions denominated in a currency other than the RMB are included in statements of operations as foreign currency transaction gains or losses. Our financial statements have been translated into U.S. dollars in accordance with ASC 830, “Foreign Currency Matters”. The financial information is first prepared in RMB and then is translated into U.S. dollars at period-end exchange rates as to assets and liabilities and average exchange rates as to revenue and expenses. Capital accounts are translated at their historical exchange rates when the capital transactions occurred. The effects of foreign currency translation adjustments are included as a component of accumulated other comprehensive income (loss) in shareholders’ equity. The relevant exchange rates are listed below:

| December 31, 2015 | December 31, 2014 | |||||||||||

| US$1:RMB exchange rate | Period End | 6.4917 | Period End | 6.1460 | ||||||||

| Average | 6.2288 | Average | 6.1457 | |||||||||

We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. We do not currently engage in currency hedging transactions.

The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated (www.oanda.com).

| Midpoint of Buy and Sell Prices for U.S. Dollar per RMB | ||||||||||||||||

| Period | Period-End | Average | High | Low | ||||||||||||

| 2011 | 6.3540 | 6.4633 | 6.6357 | 6.3318 | ||||||||||||

| 2012 | 6.3090 | 6.3115 | 6.3862 | 6.2289 | ||||||||||||

| 2013 | 6.1090 | 6.1938 | 6.3087 | 6.1084 | ||||||||||||

| 2014 | 6.1484 | 6.1458 | 6.2080 | 6.0881 | ||||||||||||

| 2015 | 6.4917 | 6.2288 | 6.4917 | 6.0933 | ||||||||||||

| September | 6.3568 | 6.3685 | 6.3836 | 6.3559 | ||||||||||||

| October | 6.3185 | 6.3503 | 6.3600 | 6.3185 | ||||||||||||

| November | 6.3982 | 6.3703 | 6.3982 | 6.3181 | ||||||||||||

| December | 6.4917 | 6.4509 | 6.4917 | 6.3980 | ||||||||||||

| 2016 | 6.5218 | 6.5444 | 6.6058 | 6.4559 | ||||||||||||

| January | 6.5771 | 6.5643 | 6.5928 | 6.5023 | ||||||||||||

| February | 6.5543 | 6.5497 | 6.5854 | 6.5169 | ||||||||||||

| March (through March 24, 2016) | 6.5218 | 6.5078 | 6.5543 | 6.4559 | ||||||||||||

As of March 24, 2016, the exchange rate is RMB 6.52175 to $1.00.

B. Capitalization and Indebtedness

Not applicable.

| 5 |

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Risks Related to Our Business and Industry

Our U.S. competitors are significantly larger than our company.

The three largest U.S. suppliers of foodservice disposables account for a significant percentage of the industry. As of 2012, Dart Container Corporation, Reynolds Group/Pactiv and Georgia-Pacific collectively held approximately 29% of the U.S. market share in the foodservice disposables industry. The overall industry consists of a small number of competitors, with approximately 50% of our market controlled by the top 10 companies in the industry.

Concentration in the foodservice disposables industry varies widely within specific market segments, with some segments dominated by a small number of producers. For example, Dart Container is the leading supplier of plastic foodservice beverage cups, followed by Pactiv and Berry Plastics. By contrast, the market for cutlery is more fragmented, with a growing portion of the market supplied by contract manufacturers in China.

Nevertheless, we may be unable to compete effectively against such larger, better-capitalized companies, which have well-established, long-term relationships with the large customers we serve and seek to serve.

We are subject to risks related to our dependence on the strength of restaurant, retail and commercial sectors of the economy in various parts of the world.

Our business depends on the strength of the restaurant, retail and commercial sectors of the economy in various parts of the world, primarily in North America, and to a lesser extent Europe, Canada, Central and South America, the Middle East, Africa, and China. These sectors of the economy are affected primarily by factors such as consumer demand and the condition of the retail industry, which, in turn, are affected by general economic conditions. Challenging economic conditions in our target markets may exert considerable pressure on consumer demand, and the resulting impact on consumer spending may have an adverse effect on demand for our products, as well as our financial condition and results of operations.

Our projections and assumptions underlying may be inaccurate, resulting in slower than anticipated growth.

All statements, except historical data, are forward-looking statements. Although we believe the projections in these forward-looking statements are reasonable, we cannot guarantee these projections will happen. Our operational results in the future may be different from our estimates for many reasons, including but not limited to the oil price (our products are by-products of oil, so we are heavily impacted by oil price), shrinking fast food industry production caused by increased production cost and changed consumption habits of food industry, failure to grow capacity and capacity utilization as quickly as anticipated or at all, losing or failing to secure customers and customer orders, shutdown of important clients, and replacement of plastics industry by paper and wood products industry.

Our plans to continue to improve productivity and reduce costs may not be successful, which would adversely affect our ability to compete.

Our success depends on our ability to continually improve our manufacturing operations to gain efficiencies, reduce supply chain costs and streamline selling, general and administrative expenses in order to produce products that are reasonably priced, while still allowing our Company to invest in innovation.

In particular, we are in the midst of installing additional production lines in Allentown, Pennsylvania. Our goal is to manufacture in this facility certain products that are not efficient to manufacture and ship from China. This project may not be completed completely as planned, may be more costly to implement than expected, may have delays in implementation, or may not result in, in full or in part, the savings and other benefits anticipated. In addition, such initiatives require the Company to implement a significant amount of organizational changes, which could have a negative impact on employee engagement, divert management’s attention from other concerns, and if not properly managed, impact the Company’s ability to retain key employees, cause disruptions in the Company’s day-to-day operations and have a negative impact on the Company’s financial results.

Price increases in raw materials and sourced products could harm the Company’s financial results.

Our primary raw materials are (1) plastic resin (primarily polypropylene (“PP”) and polystyrene (“PS”) which includes General Purpose Polystyrene (“GPPS”) and High Impact Polystyrene (“HIPS”)), (2) plastic bags and membranes for packaging cutlery, (3) shipping cartons, (4) plastic colorants, (5) paper napkins, salt, pepper and wet wipes for inclusion in cutlery packages and (6) labeling materials. These raw materials are subject to price volatility and inflationary pressures. Our success is dependent, in part, on our continued ability to reduce our exposure to increases in those costs through a variety of programs, including sales price adjustments based on adjustments in such raw material costs, while maintaining and improving margins and market share. We also rely on third-party manufacturers as a source for our products. These manufacturers are also subject to price volatility and labor cost and other inflationary pressures, which may, in turn, result in an increase in the amount we pay for sourced products. Raw material and sourced product price increases may more than offset our productivity gains and price increases and may adversely impact the Company’s financial results.

| 6 |

Our reliance on third party logistics providers may put us at risk of service failures for our customers.

Although some of our larger competitors have integrated logistics and delivery service companies, we rely on third parties to ship our products from China to our customers. Even after completing installation of the production lines in our Allentown facility, we will continue to rely on third parties for transportation within the United States. One of the bases on which we compete (particularly with regard to our QSR customers) is service. To the extent we are unable to meet their demand for products or do not deliver products on time, we stand a substantial risk of losing key accounts. Because we rely on third parties for logistics services, we may be unable to avoid supply chain failures, even if we are able to meet our manufacturing obligations to customers.

If we fail to protect our intellectual property rights, it could harm our business and competitive position.

We rely on a combination of patent, trademark, domain name and trade secret laws and non-disclosure agreements and other methods to protect our intellectual property rights. We own thirty-three patents in China and one patent in U.S. covering our designs and production technology.

The process of seeking patent protection can be lengthy and expensive, our patent applications may fail to result in patents being issued, and our existing and future patents may be insufficient to provide us with meaningful protection or commercial advantage. Our patents and patent applications may also be challenged, invalidated or circumvented.

We also rely on trade secret rights to protect our business through non-disclosure provisions in employment agreements with employees. If our employees breach their non-disclosure obligations, we may not have adequate remedies in China, and our trade secrets may become known to our competitors.

Implementation of PRC intellectual property-related laws has historically been lacking, primarily because of ambiguities in the PRC laws and enforcement difficulties. Accordingly, intellectual property rights and confidentiality protections in China may not be as effective as in the United States or other western countries. Furthermore, policing unauthorized use of proprietary technology is difficult and expensive, and we may need to resort to litigation to enforce or defend patents issued to us or to determine the enforceability, scope and validity of our proprietary rights or those of others. Such litigation and an adverse determination in any such litigation, if any, could result in substantial costs and diversion of resources and management attention, which could harm our business and competitive position.

Our Chinese patents and registered marks may not be protected outside of China due to territorial limitations on enforceability.

In general, patent and trademark rights have territorial limitations in law and are valid only within the countries in which they are registered.

At present, Chinese enterprises may register their trademarks overseas through two methods. One is to file an application for trademark registration in each single country or region in which protection is desired, while the other is to apply via the Madrid system for international trademark registration. By the second way, under the provisions of the Madrid Agreement concerning the International Registration of Marks (the “Madrid Agreement”) or the Protocol Relating to the Madrid Agreement concerning the International Registration of Marks (the “Madrid Protocol”), applicants may designate their marks in one or more member countries via the Madrid system for international registration.

As of the date of the filing, we have registered one trademark at the International Bureau of the World Intellectual Property Organization (“WIPO”) under the Madrid Agreement and Protocol. We have also applied for territorial extension by designating 15 member countries through WIPO. Currently the registration for this trademark is valid in 13 foreign member countries, including the U.S.

Similar with trademarks, Chinese enterprises may also register their patents overseas through two methods. One is to file an application for patent registration in each single country or region, and the other is to file international application with the China Intellectual Property Office or the International Bureau of World Intellectual Property Organization under the Patent Cooperation Treaty. However, such international application may relate to invention or utility model patents, but does not include industrial design patents.

As of the date of the filing, we have registered one design patent at the United States Patent and Trademark Office. This registration is only valid in the U.S. For more details, please see the disclosure of our patents

Currently, most of our patents and trademarks are registered in China. If we do not register them in other jurisdictions, they may not be protected outside of China. As a result, our business and competitive position could be harmed.

| 7 |

We may be exposed to intellectual property infringement and other claims by third parties which, if successful, could disrupt our business and have a material adverse effect on our financial condition and results of operations.

Our success depends, in large part, on our ability to use and develop our technology and know-how without infringing third party intellectual property rights. If we sell our branded products internationally, and as litigation becomes more common in China, we face a higher risk of being the subject of claims for intellectual property infringement, invalidity or indemnification relating to other parties’ proprietary rights. Our current or potential competitors, many of which have substantial resources and have made substantial investments in competing technologies, may have or may obtain patents that will prevent, limit or interfere with our ability to make, use or sell our branded products in either China or other countries, including the United States and other countries in Asia. The validity and scope of claims relating to patents in our industry involve complex scientific, legal and factual questions and analysis and, as a result, may be highly uncertain. In addition, the defense of intellectual property suits, including patent infringement suits, and related legal and administrative proceedings can be both costly and time consuming and may significantly divert the efforts and resources of our technical and management personnel. Furthermore, an adverse determination in any such litigation or proceedings to which we may become a party could cause us to:

| • | pay damage awards; | |

| • | seek licenses from third parties; | |

| • | pay ongoing royalties; | |

| • | redesign our branded products; or | |

| • | be restricted by injunctions, |

each of which could effectively prevent us from pursuing some or all of our business and result in our customers or potential customers deferring or limiting their purchase or use of our products, which could have a material adverse effect on our financial condition and results of operations.

Outstanding bank loans may reduce our available funds.

We have approximately $15.3 million in outstanding bank loans as of December 31, 2015. The loans are held at multiple banks and are secured by some of our land and property in China as the collateral for the debt. Our assets outside of China, including our Allentown assets, have not been used as collateral for the foregoing loans. While we believe we have adequate capital to repay these bank loans at present, there can be no guarantee that we will be able to pay all amounts when due or to refinance the amounts on terms that are acceptable to us or at all. If we are unable to make our payments when due or to refinance such amounts, our property could be foreclosed and our business could be negatively affected.

While we do not believe they will impact our liquidity, the terms of the debt agreements impose significant operating and financial restrictions on us. These restrictions could also have a negative impact on our business, financial condition and results of operations by significantly limiting or prohibiting us from engaging in certain transactions, including but not limited to: incurring or guaranteeing additional indebtedness; transferring or selling assets currently held by us; and transferring ownership interests in certain of our subsidiaries. The failure to comply with any of these covenants could cause a default under our other debt agreements. Any of these defaults, if not waived, could result in the acceleration of all of our debt, in which case the debt would become immediately due and payable. If this occurs, we may not be able to repay our debt or borrow sufficient funds to refinance it on favorable terms, if any.

We may be unable to refinance our short-term loans.

We expect to be able to refinance its short-term loans based on past experience and our good credit history. We do not believe failure to refinance from certain banks will have significant negative impact on our normal business operations. In both 2015 and 2014, our operating cash flow was positive. In addition, our related parties including our major shareholders and affiliate companies are willing to provide us financial support. However, it is possible for us to have negative cash flow in the future, and for our related parties to be unable or unwilling to provide us financial support as needed. As a result, the failure to refinance our short-term loans could potentially affect our capital expenditure and expansion of business.

If the value of our property decreases, we may not be able to refinance our current debt.

All of our current debt is secured by either mortgages on our real and other business property or guarantees by some of our shareholders. If the value of our real property decreases, we may find that banks are unwilling to loan money to us secured by our business property. A drop in property value could also prevent us from being able to refinance that loan when it becomes due on acceptable terms or at all.

| 8 |

We may require additional financing in the future and our operations could be curtailed if we are unable to obtain required additional financing when needed.

We may need to obtain additional debt or equity financing to fund future capital expenditures. While we do not anticipate seeking additional financing in the immediate future, any additional equity may result in dilution to the holders of our outstanding shares of capital stock. Additional debt financing may include conditions that would restrict our freedom to operate our business, such as conditions that:

| • | limit our ability to pay dividends or require us to seek consent for the payment of dividends; | |

| • | increase our vulnerability to general adverse economic and industry conditions; | |

| • | require us to dedicate a portion of our cash flow from operations to payments on our debt, thereby reducing the availability of our cash flow to fund capital expenditures, working capital and other general corporate purposes; and | |

| • | limit our flexibility in planning for, or reacting to, changes in our business and our industry. |

We cannot guarantee that we will be able to obtain any additional financing on terms that are acceptable to us, or at all.

The loss of any of our key customers could reduce our revenues and our profitability.

Our key customers are principally multinational QSRs, third party distributors, and retail stores, mainly located in the U.S. For the year ended December 31, 2015, sales to our nine largest customers amounted in the aggregate to approximately 50.9% of our total revenue. For the year ended December 31, 2014, sales to our nine largest customers amounted in the aggregate to approximately 50.9% of our total revenue. There can be no assurance that we will maintain or improve the relationships with these customers, or that we will be able to continue to supply these customers at current levels or at all. Any failure to pay by these customers could have a material negative effect on our company’s business. In addition, having a relatively small number of customers may cause our quarterly results to be inconsistent, depending upon when these customers pay for outstanding invoices.

During the years ended December 31, 2015 and 2014, respectively, we had one and zero customers that accounted for 10% or more of our revenues.

| Customer Name | Year Ended December 31, 2015 |

Year Ended December 31, 2014 |

||||||

| Lollicup USA Inc. | 12.9 | % | * | |||||

| * | Less than 10% during the period. |

If we cannot maintain long-term relationships with these major customers, the loss of our sales to them could have an adverse effect on our business, financial condition and results of operations.

We buy our supplies from a relatively limited number of suppliers.

During the year ended December 31, 2015, our four largest suppliers accounted for approximately 50% of our total purchases. During the year ended December 31, 2014, our six largest suppliers accounted for approximately 50.1% of our total purchases. During the years ended December 31, 2015 and 2014, respectively, we had two and two suppliers that accounted for 10% or more of our purchases.

| Supplier Name | Year Ended December 31, 2015 |

Year Ended December 31, 2014 |

||||||

| Brilliance Resources Company Limited | 14.7 | % | 14.7 | % | ||||

| Koco Group Ltd | * | 10.2 | % | |||||

| Grand Chemical Group | 17.3 | % | * | |||||

| * | Less than 10% during the period. |

Because we purchase a material amount of our raw materials from these suppliers, the loss of any such suppliers could result in increased expenses for our company and result in adverse impact on our business, financial condition and results of operations.

| 9 |

Our bank accounts are not fully insured or protected against loss.

We maintain our cash with various banks and trust companies located in mainland China, Hong Kong and the United States. Our cash accounts in the PRC are not insured or otherwise protected. To the extent our U.S. and Hong Kong accounts were to exceed statutory amounts, they would also not be fully protected against loss. Should any bank or trust company holding our cash deposits become insolvent, or if we are otherwise unable to withdraw funds, we would lose the cash on deposit with that particular bank or trust company.

We are substantially dependent upon our senior management and key research and development personnel.

We are highly dependent on our senior management to manage our business and operations and our key research and development personnel for the development of new products and the enhancement of our existing products and technologies. In particular, we rely substantially on our Chief Executive Officer, Mr. Xinfu Hu, and our Chief Operating Officer and Chair, Ms. Guilan Jiang, to manage our operations. Ms. Jiang and Mr. Hu are husband and wife and have been involved in the plastic industry for more than twenty years. Due to their experience in the industry and long relationships with our customer base, they would be difficult to replace.

While we provide the legally required personal insurance for the benefit of our employees, we do not maintain key person life insurance on any of our senior management or key personnel. The loss of any one of them would have a material adverse effect on our business and operations. Competition for senior management and our other key personnel is intense, and the pool of suitable candidates is limited. We may be unable to quickly locate a suitable replacement for any senior management or key personnel that we lose. In addition, if any member of our senior management or key personnel joins a competitor or forms a competing company, they may compete with us for customers, business partners and other key professionals and staff members of our company. Although each of our senior management and key personnel has signed a confidentiality and non-competition agreement in connection with his employment with us, we cannot assure you that we will be able to successfully enforce these provisions in the event of a dispute between us and any member of our senior management or key personnel.

In our efforts to develop new products and methods of manufacturing, we compete for qualified personnel with technology companies and research institutions. Intense competition for these personnel could cause our compensation costs to increase, which could have a material adverse effect on our results of operations. Our future success and ability to grow our business will depend in part on the continued service of these individuals and our ability to identify, hire and retain additional qualified personnel. If we are unable to attract and retain qualified employees, we may be unable to meet our business and financial goals.

Failure to manage our growth could strain our management, operational and other resources, which could materially and adversely affect our business and prospects.

Our growth strategy includes increasing market penetration of our existing products, developing new products and increasing the number and size of customers we serve. Pursuing these strategies has resulted in, and will continue to result in substantial demands on management resources. In particular, the management of our growth will require, among other things:

| • | continued enhancement of our research and development capabilities; | |

| • | stringent cost controls and sufficient liquidity; | |

| • | strengthening of financial and management controls; | |

| • | increased marketing, sales and support activities; and | |

| • | hiring and training of new personnel. |

If we are not able to manage our growth successfully, our business and prospects would be materially and adversely affected.

Risks Related to Doing Business in China

Labor laws in the PRC may adversely affect our results of operations.

On June 29, 2007, the PRC government promulgated the Labor Contract Law of the PRC, which became effective on January 1, 2008. The Labor Contract Law imposes greater liabilities on employers and significantly affects the cost of an employer’s decision to reduce its workforce. Further, it requires certain terminations be based upon seniority and not merit. In the event we decide to significantly change or decrease our workforce, the Labor Contract Law could adversely affect our ability to enact such changes in a manner that is most advantageous to our business or in a timely and cost-effective manner, thus materially and adversely affecting our financial condition and results of operations.

| 10 |

Under the Enterprise Income Tax Law, we may be classified as a “Resident Enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders.

China passed the Enterprise Income Tax Law, or the EIT Law, and it is implementing rules, both of which became effective on January 1, 2008. Under the EIT Law, an enterprise established outside of China with “de facto management bodies” within China is considered a “resident enterprise,” meaning that it can be treated in a manner similar to a Chinese enterprise for enterprise income tax purposes. The implementing rules of the EIT Law define de facto management as “substantial and overall management and control over the production and operations, personnel, accounting, and properties” of the enterprise.

On April 22, 2009, the State Administration of Taxation of China, or the SAT, issued the Circular Concerning Relevant Issues Regarding Cognizance of Chinese Investment Controlled Enterprises Incorporated Offshore as Resident Enterprises pursuant to Criteria of de facto Management Bodies, or the SAT Notice 82, further interpreting the application of the EIT Law and its implementation to offshore entities controlled by a Chinese enterprise or enterprise group. Pursuant to the SAT Notice 82, an enterprise incorporated in an offshore jurisdiction and controlled by a Chinese enterprise or enterprise group will be classified as a “non-domestically incorporated resident enterprise” if (i) its senior management in charge of daily operations reside or perform their duties mainly in China; (ii) its financial or personnel decisions are made or approved by bodies or persons in China; (iii) its substantial assets and properties, accounting books, corporate stamps, board and shareholder minutes are kept in China; and (iv) at least half of its directors with voting rights or senior management often resident in China. After SAT Notice 82, the SAT issued a bulletin, known as SAT Bulletin 45, which took effect on September 1, 2011, to provide more guidance on the implementation of SAT Notice 82 and clarify the reporting and filing obligations of such “non-domestically incorporated resident enterprise.” SAT Bulletin 45 provides procedures and administrative details for the determination of resident status and administration on post-determination matters. On January 29, 2014, the SAT issued Announcement of the State Administration of Taxation on Recognizing Resident Enterprises Based on the Criteria of de facto Management Bodies, to further clarify the reporting and filing procedure for offshore entities controlled by a Chinese enterprise or enterprise group and recognized as a resident enterprise.

The determining criteria set forth in SAT Notice 82 and SAT Bulletin 45 may reflect the SAT’s general position on how the “de facto management body” test should be applied in determining the tax resident status of offshore enterprises, regardless of whether they are controlled by PRC enterprises, PRC enterprise groups or by PRC or foreign individuals. If the PRC tax authorities determine that FGI or its subsidiaries is a PRC resident enterprise for PRC enterprise income tax purposes, a number of unfavorable PRC tax consequences could follow. First, we may be subject to the enterprise income tax at a rate of 25% on our worldwide taxable income as well as PRC enterprise income tax reporting obligations. In our case, this would mean that income such as non-China source income would be subject to PRC enterprise income tax at a rate of 25%. Currently, we do not have any non-China source income, as we complete our sales, including export sales, in China. Second, under the EIT Law and its implementing rules, dividends paid to us from our PRC subsidiaries would be deemed as “qualified investment income between resident enterprises” and therefore qualify as “tax-exempt income” pursuant to the clause 26 of the EIT Law. Finally, it is possible that future guidance issued with respect to the new “resident enterprise” classification could result in a situation in which the dividends we pay with respect to our ordinary shares, or the gain our non-PRC stockholders may realize from the transfer of our ordinary shares, may be treated as PRC-sourced income and may therefore be subject to a 10% PRC withholding tax. If we are required under the EIT Law and its implementing regulations to withhold PRC income tax on dividends payable to our non-PRC stockholders, or if non-PRC stockholders are required to pay PRC income tax on gains on the transfer of their shares of ordinary shares, our business could be negatively impacted and the value of your investment may be materially reduced. Further, if we were treated as a “resident enterprise” by PRC tax authorities, we would be subject to taxation in both China and such countries in which we have taxable income, and our PRC tax may not be creditable against such other taxes.

We may be exposed to liabilities under the Foreign Corrupt Practices Act and Chinese anti-corruption law.

We are subject to the U.S. Foreign Corrupt Practices Act (“FCPA”), and other laws that prohibit improper payments or offers of payments to foreign governments and their officials and political parties by U.S. persons and issuers as defined by the statute for the purpose of obtaining or retaining business. We are also subject to Chinese anti-corruption laws, which strictly prohibit the payment of bribes to government officials. We have operations, agreements with third parties, and make sales in China, which may experience corruption. Our activities in China create the risk of unauthorized payments or offers of payments by one of the employees, consultants or distributors of our company, because these parties are not always subject to our control. We are in process of implementing an anticorruption program, which prohibits the offering or giving of anything of value to foreign officials, directly or indirectly, for the purpose of obtaining or retaining business. The anticorruption program also requires that clauses mandating compliance with our policy be included in all contracts with foreign sales agents, sales consultants and distributors and that they certify their compliance with our policy annually. It further requires that all hospitality involving promotion of sales to foreign governments and government-owned or controlled entities be in accordance with specified guidelines. In the meantime, we believe to date we have complied in all material respects with the provisions of the FCPA and Chinese anti-corruption laws.

However, our existing safeguards and any future improvements may prove to be less than effective, and the employees, consultants or distributors of our Company may engage in conduct for which we might be held responsible. Violations of the FCPA or Chinese anti-corruption laws may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could negatively affect our business, operating results and financial condition. In addition, the government may seek to hold our Company liable for successor liability FCPA violations committed by companies in which we invest or that we acquire.

| 11 |

Uncertainties with respect to the PRC legal system could adversely affect us.

We conduct a substantial amount of our business through our subsidiaries in China. Our operations in China are governed by PRC laws and regulations. Our PRC subsidiaries are generally subject to laws and regulations applicable to foreign investments in China and, in particular, laws and regulations applicable to wholly foreign-owned enterprises. The PRC legal system is based on statutes. Prior court decisions may be cited for reference but have limited precedential value.

Since 1979, PRC legislation and regulations have significantly enhanced the protections afforded to various forms of foreign investments in China. However, China has not developed a fully integrated legal system and recently enacted laws and regulations may not sufficiently cover all aspects of economic activities in China. In particular, because some of these laws and regulations are relatively new, and because of the limited volume of published decisions and their nonbinding nature, the interpretation and enforcement of these laws and regulations involve uncertainties. In addition, the PRC legal system is based in part on government policies and internal rules (some of which are not published on a timely basis or at all) that may have a retroactive effect. As a result, we may not be aware of our violation of these policies and rules until sometime after the violation. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention.

Governmental control of currency conversion may affect the value of your investment.

The PRC government imposes controls on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of China. FGI receives revenues and purchases raw materials primarily in U.S. dollars but incurs other expenses primarily in RMB. Although our main suppliers are based in mainland China or based in Hong Kong with Chinese operating subsidiaries, some of them provide quotations in U.S. dollars. We choose quotations based on price competitiveness. In the past, U.S. dollars quotations were more competitive so we purchase almost all of our raw materials in U.S. dollars. However, recently several RMB quotations were more competitive and we accepted them and paid in RMB.

Under our current corporate structure, FGI’s income is primarily derived from dividend payments from our PRC subsidiaries. Shortages in the availability of foreign currency may restrict the ability of our PRC subsidiaries to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency denominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade-related transactions can be made in foreign currencies without prior approval from SAFE by complying with certain procedural requirements. However, approval from appropriate government authorities is required where RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay dividends in foreign currencies to our security-holders.

We are a holding company and we rely for funding on dividend payments from our subsidiaries, which are subject to restrictions under PRC laws.

We are a holding company incorporated in the Cayman Islands, and we operate our core businesses through our subsidiaries in the PRC and the United States. Therefore, the availability of funds for us to pay dividends to our shareholders and to service our indebtedness depends upon dividends received from these PRC subsidiaries. If our subsidiaries incur debt or losses, their ability to pay dividends or other distributions to us may be impaired. As a result, our ability to pay dividends and to repay our indebtedness will be restricted. PRC laws require that dividends be paid only out of the after-tax profit of our PRC subsidiaries calculated according to PRC accounting principles, which differ in many aspects from generally accepted accounting principles in other jurisdictions. PRC laws also require enterprises established in the PRC to set aside part of their after-tax profits as statutory reserves. These statutory reserves are not available for distribution as cash dividends. In addition, restrictive covenants in bank credit facilities or other agreements that we or our subsidiaries may enter into in the future may also restrict the ability of our subsidiaries to pay dividends to us. These restrictions on the availability of our funding may impact our ability to pay dividends to our shareholders and to service our indebtedness.

Our business may be materially and adversely affected if any of our PRC subsidiaries declare bankruptcy or become subject to a dissolution or liquidation proceeding.

The Enterprise Bankruptcy Law of the PRC, or the Bankruptcy Law, came into effect on June 1, 2007. The Bankruptcy Law provides that an enterprise will be liquidated if the enterprise fails to settle its debts as and when they fall due and if the enterprise’s assets are, or are demonstrably, insufficient to clear such debts.

Our PRC subsidiaries hold certain assets that are important to our business operations. If any of our PRC subsidiaries undergoes a voluntary or involuntary liquidation proceeding, unrelated third-party creditors may claim rights to some or all of these assets, thereby hindering our ability to operate our business, which could materially and adversely affect our business, financial condition and results of operations.

| 12 |

According to the SAFE’s Notice of the State Administration of Foreign Exchange on Further Improving and Adjusting Foreign Exchange Administration Policies for Direct Investment, effective on December 17, 2012, and the Provisions for Administration of Foreign Exchange Relating to Inbound Direct Investment by Foreign Investors, effective May 13, 2013, if any of our PRC subsidiaries undergoes a voluntary or involuntary liquidation proceeding, prior approval from the SAFE for remittance of foreign exchange to our shareholders abroad is no longer required, but we still need to conduct a registration process with the SAFE local branch. It is not clear whether “registration” is a mere formality or involves the kind of substantive review process undertaken by SAFE and its relevant branches in the past.

Fluctuations in exchange rates could adversely affect our business and the value of our securities.

Changes in the value of the RMB against the U.S. dollar, Euro and other foreign currencies are affected by, among other things, changes in China’s political and economic conditions. Any significant revaluation of the RMB may have a material adverse effect on our revenues and financial condition, and the value of, and any dividends payable on our shares in U.S. dollar terms. For example, to the extent that we need to convert U.S. dollars into RMB for our operations, appreciation of the RMB against the U.S. dollar would have an adverse effect on RMB amount we would receive from the conversion. Conversely, if we decide to convert our RMB into U.S. dollars for the purpose of paying dividends on our Ordinary Shares or for other business purposes, appreciation of the U.S. dollar against the RMB would have a negative effect on the U.S. dollar amount available to us. In addition, fluctuations of the RMB against other currencies may increase or decrease the cost of imports and exports, and thus affect the price-competitiveness of our products against products of foreign manufacturers or products relying on foreign inputs.

Since July 2005, the RMB is no longer pegged to the U.S. dollar. Although the People’s Bank of China regularly intervenes in the foreign exchange market to prevent significant short-term fluctuations in the exchange rate, the RMB may appreciate or depreciate significantly in value against the U.S. dollar in the medium to long term. Moreover, it is possible that in the future PRC authorities may lift restrictions on fluctuations in the RMB exchange rate and lessen intervention in the foreign exchange market.

We reflect the impact of currency translation adjustments in our financial statements under the heading “accumulated other comprehensive income (loss).” For years ended December 31, 2015 and 2014, we had a negative adjustment of $702,167 and a negative adjustment of $164,781, respectively, for foreign currency translations. Very limited hedging transactions are available in China to reduce our exposure to exchange rate fluctuations. To date, we have not entered into any hedging transactions. While we may enter into hedging transactions in the future, the availability and effectiveness of these transactions may be limited, and we may not be able to successfully hedge our exposure at all. In addition, our foreign currency exchange losses may be magnified by PRC exchange control regulations that restrict our ability to convert RMB into foreign currencies.

If we become directly subject to the recent scrutiny, criticism and negative publicity involving U.S.-listed Chinese companies, we may have to expend significant resources to investigate and resolve the matter which could harm our business operations and our reputation and could result in a loss of your investment in our shares, especially if such matter cannot be addressed and resolved favorably.

Recently, U.S. public companies that have substantially all of their operations in China, have been the subject of intense scrutiny, criticism and negative publicity by investors, financial commentators and regulatory agencies, such as the SEC. Much of the scrutiny, criticism and negative publicity has centered around financial and accounting irregularities, a lack of effective internal controls over financial accounting, inadequate corporate governance policies or a lack of adherence thereto and, in some cases, allegations of fraud. As a result of the scrutiny, criticism and negative publicity, the publicly traded stock of many U.S. listed Chinese companies has sharply decreased in value and, in some cases, has become virtually worthless. Many of these companies are now subject to shareholder lawsuits and SEC enforcement actions and are conducting internal and external investigations into the allegations. It is not clear what effect this sector-wide scrutiny, criticism and negative publicity will have on our company and our business. If we become the subject of any unfavorable allegations, whether such allegations are proven to be true or untrue, we will have to expend significant resources to investigate such allegations and/or defend the Company. This situation may be a major distraction to our management. If such allegations are not proven to be groundless, our company and business operations will be severely hampered and your investment in our shares could be rendered worthless.

PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident shareholders to penalties and limit our ability to inject capital into our PRC subsidiary, limit our PRC subsidiary’s ability to distribute profits to us, or otherwise adversely affect us.

The SAFE promulgated the Circular on Relevant Issues Relating to Domestic Resident’s Investment and Financing and Roundtrip Investment through Special Purpose Vehicles, or SAFE Circular 37, in July 2014 that requires PRC residents or entities to register with SAFE or its local branch in connection with their establishment or control of an offshore entity established for the purpose of overseas investment or financing. In addition, such PRC residents or entities must update their SAFE registrations when the offshore special purpose vehicle undergoes material events relating to any change of basic information (including change of such PRC citizens or residents, name and operation term), increases or decreases in investment amount, transfers or exchanges of shares, or mergers or divisions.

| 13 |

SAFE Circular 37 was issued to replace the Notice on Relevant Issues Concerning Foreign Exchange Administration for PRC Residents Engaging in Financing and Roundtrip Investments via Overseas Special Purpose Vehicles, or SAFE Circular 75.

If our shareholders who are PRC residents or entities do not complete their registration with the local SAFE branches, our PRC subsidiary may be prohibited from distributing their profits and proceeds from any reduction in capital, share transfer or liquidation to us, and we may be restricted in our ability to contribute additional capital to our PRC subsidiary. Moreover, failure to comply with the SAFE registration described above could result in liability under PRC laws for evasion of applicable foreign exchange restrictions.

Ms. Jiang has completed her SAFE Circular 37 registration. Ms. Sujuan Zhu, Mr. Qian Hu, Mr. Xinzhong Wang, Mr. Jinxue Jiang and Mr. Yongjun Guo have applied to SAFE’s local branch in Taizhou for registration, but we cannot provide any assurances that such registration will be completed in a timely manner. Moreover, we may not be fully informed of the identities of all our beneficial owners who are PRC citizens or residents, and we cannot compel our beneficial owners to comply with SAFE registration requirements.

As a result, we cannot assure you that all of our shareholders or beneficial owners who are PRC citizens or residents have complied with, and will in the future make or obtain any applicable registrations or approvals required by, SAFE regulations. Failure by such shareholders or beneficial owners to comply with SAFE regulations, or failure by us to amend the foreign exchange registrations of our PRC subsidiary, could subject us to fines or legal sanctions, restrict our overseas or cross-border investment activities, limit our subsidiaries’ ability to make distributions or pay dividends or affect our ownership structure, which could adversely affect our business and prospects.

China’s proposed foreign investment law may impose new burdens on our company.

On January 19, 2015, MOFCOM released the draft Foreign Investment Law for public comment (the “Draft FI Law”). The Draft FI Law proposed fundamental changes to the existing foreign investment legal regime in China. If implemented in its current status, the Draft FI Law, once effective, will require Taizhou Fuling to submit an annual report to the foreign investment authority. The information required by the annual report may be extensive and burdensome, such as the foreign invested company’s main products, import and export, employment, financial status, transactions with our affiliates and material disputes. If we fail to make such reporting timely or if there is any concealment in such reporting, we may be subject to fines or other regulatory sanctions.

Risks Related to Our Corporate Structure and Operation

We incur additional costs as a public company, which could negatively impact our net income and liquidity.

We are a public company in the United States. As a public company, we incur significant legal, accounting and other expenses that we did not incur as a private company. In addition, the Sarbanes-Oxley Act and rules and regulations implemented by the SEC and The Nasdaq Capital Market require significantly heightened corporate governance practices for public companies. We expect that these rules and regulations to increase our legal, accounting and financial compliance costs and make many corporate activities more time-consuming and costly.

We do not expect to incur materially greater costs as a public company than those incurred by similarly sized foreign private issuers. If we fail to comply with these rules and regulations, we could become the subject of a governmental enforcement action, investors may lose confidence in us and the market price of our Ordinary Shares could decline.

Entities controlled by our employees, officers and/or directors control a majority of our Ordinary Shares, decreasing your influence on shareholder decisions.

Entities controlled by our employees, officers and/or directors, in the aggregate, continue to own a majority of our outstanding shares. As a result, our employees, officers and directors possess substantial ability to impact our management and affairs and the outcome of matters submitted to shareholders for approval. These shareholders, acting individually or as a group, could exert control and substantial influence over matters such as electing directors and approving mergers or other business combination transactions. This concentration of ownership and voting power may also discourage, delay or prevent a change in control of our company, which could deprive our shareholders of an opportunity to receive a premium for their shares as part of a sale of our company and might reduce the price of our Ordinary Shares. These actions may be taken even if they are opposed by our other shareholders. See “MAJOR SHAREHOLDERS.”

The obligation to disclose information publicly may put us at a disadvantage to competitors that are private companies.

We are publicly listed company in the United States. As a publicly listed company, we are required to file periodic reports with the Securities and Exchange Commission upon the occurrence of matters that are material to our company and shareholders. In some cases, we need to disclose material agreements or results of financial operations that we would not be required to disclose if we were a private company. Our competitors may have access to this information, which would otherwise be confidential. This may give them advantages in competing with our company. Similarly, as a U.S.-listed public company, we are governed by U.S. laws that our non-publicly traded competitors are not required to follow. To the extent compliance with U.S. laws increases our expenses or decreases our competitiveness against such companies, our public listing could affect our results of operations.

| 14 |

We are a “foreign private issuer,” and our disclosure obligations differ from those of U.S. domestic reporting companies. As a result, we may not provide you the same information as U.S. domestic reporting companies or we may provide information at different times, which may make it more difficult for you to evaluate our performance and prospects.

We are a foreign private issuer and, as a result, we are not subject to the same requirements as U.S. domestic issuers. Under the Exchange Act, we are subject to reporting obligations that, to some extent, are more lenient and less frequent than those of U.S. domestic reporting companies. For example, we are required to issue quarterly reports or proxy statements. We are not required to disclose detailed individual executive compensation information. Furthermore, our directors and executive officers are required to report equity holdings under Section 16 of the Exchange Act and are not subject to the insider short-swing profit disclosure and recovery regime.

As a foreign private issuer, we are also exempt from the requirements of Regulation FD (Fair Disclosure) which, generally, are meant to ensure that select groups of investors are not privy to specific information about an issuer before other investors. However, we are still subject to the anti-fraud and anti-manipulation rules of the SEC, such as Rule 10b-5 under the Exchange Act. Since many of the disclosure obligations imposed on us as a foreign private issuer differ from those imposed on U.S. domestic reporting companies, you should not expect to receive the same information about us and at the same time as the information provided by U.S. domestic reporting companies.

As a foreign private issuer, we are permitted to rely on exemptions from certain Nasdaq corporate governance standards applicable to U.S. issuers, including the requirement that a majority of an issuer’s directors consist of independent directors. If we opt to rely on such exemptions in the future, such decision might afford less protection to holders of our ordinary shares.

Section 5605(b)(1) of the Nasdaq Listing Rules requires listed companies to have, among other things, a majority of its board members to be independent, and Section 5605(d) and 5605(e) require listed companies to have independent director oversight of executive compensation and nomination of directors. As a foreign private issuer, however, we are permitted to follow home country practice in lieu of the above requirements. We have agreed with our underwriters that we do not opt to follow home country practice in lieu of such requirements for two years after the completion of our initial public offering. See “Item 16.G. Corporate Governance.” After this period, however, we could decide to follow home country practice. Our board of directors could make such a decision to depart from such requirements by ordinary resolution. The remainder of this risk factor, therefore, discusses risks to shareholders in the event the board of directors were to depart from some of such Nasdaq requirements and instead follow home country practices.

The corporate governance practice in our home country, the Cayman Islands, does not require a majority of our board to consist of independent directors or the implementation of a nominating and corporate governance committee. Since a majority of our board of directors would not consist of independent directors if we relied on the foreign private issuer exemption, fewer board members would be exercising independent judgment and the level of board oversight on the management of our company might decrease as a result. In addition, we could opt to follow Cayman Islands law instead of the Nasdaq requirements that mandate that we obtain shareholder approval for certain dilutive events, such as an issuance that will result in a change of control, certain transactions other than a public offering involving issuances of 20% or greater interests in the company and certain acquisitions of the shares or assets of another company. For a description of the material corporate governance differences between the Nasdaq requirements and Cayman Islands law, see “Description of Share Capital — Differences in Corporate Law” in our registration statement on Form F-1 (File no. 333-205894), filed with the SEC on July 28, 2015, as amended.

Our directors’ and executive officers’ other business activities may pose conflicts of interest.

Our directors and executive officers have other business interests outside the company that could potentially give rise to conflicts of interest. For example, our Chief Operating Officer and Chair, Guilan Jiang, owns 50% of Wenling Fulin Plastic Products Co. Ltd. Ms. Jiang is also its legal representative and general manager. While this company was previously engaged in the plastics industry and, as a result, may have competitive overlap with our company, we do not believe it currently competes with our company. Wenling Fulin Plastic Products Co. Ltd. is a holding company with no investment in any competing business with us, although it has investment in a local commercial bank and leases its land to a restaurant. While the company was previously in our industry, this privately held company’s operations, but not the name, have changed. Notwithstanding the foregoing, if this company were to begin to operate within our industry, we might find a conflict of interest.

Although her business working time at this company is flexible, Ms. Jiang has historically devoted very limited time to matters concerning Wenling Fulin Plastic Products Co. Ltd., and most of her time to matters for FGI. If Ms. Jiang devotes any significant time and effort to this other company in the future, such business activities could both distract her from focusing on FGI and pose a conflict of interest to the extent her activities at Wenling Fulin Plastic Products Co. Ltd. compete with our company.

An insufficient amount of insurance could expose us to significant costs and business disruption.

While we have purchased insurance, including export transportation, product liability and account receivable insurance, to cover certain assets and property of our business, the amounts and scope of coverage could leave our business inadequately protected from loss. For example, not all of our subsidiaries have coverage of business interruption insurance. If we were to incur substantial losses or liabilities due to fire, explosions, floods, other natural disasters or accidents or business interruption, our results of operations could be materially and adversely affected.

| 15 |

Risks Related to Ownership of Our Ordinary Shares

We are an “emerging growth company,” and we cannot be certain if the reduced reporting requirements applicable to emerging growth companies will make our Ordinary Shares less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act, or the JOBS Act. For as long as we continue to be an emerging growth company, we may take advantage of exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We could be an emerging growth company for up to five years, although we could lose that status sooner if our revenues exceed $1 billion, if we issue more than $1 billion in non-convertible debt in a three year period, or if the market value of our Ordinary Shares held by non-affiliates exceeds $700 million as of any June 30 before that time, in which case we would no longer be an emerging growth company as of the following December 31. We cannot predict if investors will find our Ordinary Shares less attractive because we may rely on these exemptions. If some investors find our Ordinary Shares less attractive as a result, there may be a less active trading market for our Ordinary Shares and our share price may be more volatile.

Under the JOBS Act, emerging growth companies can also delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have irrevocably elected not to avail our company of this exemption from new or revised accounting standards and, therefore, are subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

If we are unable to implement and maintain effective internal control over financial reporting in the future, investors may lose confidence in the accuracy and completeness of our financial reports and the market price of our Ordinary Shares may decline.

As a public company, we are required to maintain internal control over financial reporting and to report any material weaknesses in such internal control. In addition, beginning with this annual report on Form 20-F, we are required to furnish a report by management on the effectiveness of our internal control over financial reporting pursuant to Section 404 of the Sarbanes-Oxley Act. We are in the process of designing, implementing, and testing the internal control over financial reporting required to comply with this obligation, which process is time consuming, costly, and complicated. In addition, our independent registered public accounting firm is required to attest to the effectiveness of our internal control over financial reporting beginning with our annual report on Form 20-F following the date on which we are no longer an “emerging growth company,” which may be up to five full years following the date of our initial public offering. If we identify material weaknesses in our internal control over financial reporting, if we are unable to comply with the requirements of Section 404 in a timely manner or assert that our internal control over financial reporting is effective, or if our independent registered public accounting firm is unable to express an opinion as to the effectiveness of our internal control over financial reporting when required, investors may lose confidence in the accuracy and completeness of our financial reports and the market price of our Ordinary Shares could be negatively affected, and we could become subject to investigations by the stock exchange on which our securities are listed, the Securities and Exchange Commission, or the SEC, or other regulatory authorities, which could require additional financial and management resources.

The requirements of being a public company may strain our resources and divert management’s attention.

As a public company, we are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act, the Sarbanes-Oxley Act, the Dodd-Frank Act, the listing requirements of the securities exchange on which we list, and other applicable securities rules and regulations. Despite recent reforms made possible by the JOBS Act, compliance with these rules and regulations will nonetheless increase our legal and financial compliance costs, make some activities more difficult, time-consuming or costly and increase demand on our systems and resources, particularly after we are no longer an “emerging growth company.” The Exchange Act requires, among other things, that we file annual and current reports with respect to our business and operating results. In addition, as long as we are listed on The Nasdaq Capital Market, we are also required to file semi-annual financial statements.

As a result of disclosure of information in this annual report and in filings required of a public company, our business and financial condition will become more visible, which we believe may result in threatened or actual litigation, including by competitors and other third parties. If such claims are successful, our business and operating results could be harmed, and even if the claims do not result in litigation or are resolved in our favor, these claims, and the time and resources necessary to resolve them, could divert the resources of our management and adversely affect our business, brand and reputation and results of operations.

We also expect that being a public company and these rules and regulations make it more expensive for us to obtain director and officer liability insurance, and we may be required to accept reduced coverage or incur substantially higher costs to obtain coverage. These factors could also make it more difficult for us to attract and retain qualified members of our board of directors, particularly to serve on our audit committee and compensation committee, and qualified executive officers.

| 16 |

The market price of our Ordinary Shares may be volatile or may decline regardless of our operating performance, and you may not be able to resell your shares at or above the price you paid.

The trading price for our Ordinary Shares have fluctuated since we first listed our Ordinary Shares. Since our Ordinary Shares became listed on the Nasdaq on November 4, 2015, the trading price of our Ordinary Shares has ranged from US $2.241 to US $5.27 per common share, and the last reported trading price on March 24, 2016 was $2.6499 per Ordinary Share. The market price of our Ordinary Shares may fluctuate significantly in response to numerous factors, many of which are beyond our control, including:

| • | actual or anticipated fluctuations in our revenue and other operating results; | |