UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

10-K

| x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31,

2013

or

| o |

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934 |

For the transition period from to

Commission file number: 333-188611

ComHear,

Inc.

(Exact name of registrant as specified in

its charter)

| Delaware |

|

|

|

46-1186821 |

(State or Other Jurisdiction of

Incorporation or Organization) |

|

|

|

(I.R.S. Employer Identification

Number) |

37 W. 28th St., 3rd Floor

New York, New York 10001

(Address of principal

executive offices)

(212) 574-4401

(Registrant’s telephone number,

including area code)

Securities registered pursuant to Section 12(b) of

the Act:

None

Securities registered pursuant to Section 12(g) of

the Act:

None

Indicate by check mark if the

registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o

No x

Indicate by check mark if the registrant

is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o

No x

Indicate by check mark whether the

registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of

1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant

has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted

and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or

for such shorter period that the registrant was required to submit and post such files). Yes x

No o

Indicate by check mark if disclosure of

delinquent filers in response to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of

the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this

Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as defined in Rule 12b-2

of the Act):

| Large accelerated filer o |

|

Accelerated filer o |

| Non-accelerated filer o |

|

Smaller reporting company x |

| (Do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes o

No x

The aggregate market value of voting and

non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold by

the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter: $3,162,418.

The number of shares of the registrant’s

common stock outstanding as of March 28, 2014 was 17,115,061.

TABLE OF CONTENTS

| |

|

|

|

Page |

| PART I |

| Item 1. |

|

Business |

|

3 |

| Item 1A. |

|

Risk Factors |

|

11 |

| Item 1B. |

|

Unresolved Staff Comments |

|

14 |

| Item 2. |

|

Properties |

|

14 |

| Item 3. |

|

Legal Proceedings |

|

14 |

| Item 4. |

|

Mine Safety Disclosures |

|

14 |

| |

|

|

|

|

PART II

|

| |

| Item 5. |

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Repurchases of Equity Securities |

|

15 |

| Item 6. |

|

Selected Financial Data |

|

15 |

| Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

16 |

| Item 7A. |

|

Quantitative and Qualitative Disclosures About Market Risk |

|

19 |

| Item 8. |

|

Financial Statements and Supplementary Data |

|

19 |

| Item 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

20 |

| Item 9A. |

|

Controls and Procedures |

|

20 |

| Item 9B. |

|

Other Information |

|

20 |

| |

|

|

|

|

PART III

|

| |

| Item 10. |

|

Directors, Executive Officers and Corporate Governance |

|

21 |

| Item 11. |

|

Executive Compensation |

|

23 |

| Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

26 |

| Item 13. |

|

Certain Relationships and Related Transactions and Director Independence |

|

27 |

| Item 14. |

|

Principal Accountant Fees and Services |

|

27 |

| |

|

|

|

|

PART IV

|

| |

| Item 15. |

|

Exhibits and Financial Statement Schedules |

|

28 |

| |

|

|

|

|

| Signatures |

|

|

|

31 |

CAUTIONARY NOTICE

This annual report

on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Those forward-looking statements include our

expectations, beliefs, intentions and strategies regarding the future. Such forward-looking statements relate to, among other things,

our market, strategy, competition, development plans, financing, revenues, operations and compliance with applicable laws. These

and other factors that may affect our financial results are discussed more fully in “Risk Factors” and “Management’s

Discussion and Analysis of Financial Condition and Results of Operations” included in this report. Market data used throughout

this report is based on published third party reports or the good faith estimates of management, which estimates are presumably

based upon their review of internal surveys, independent industry publications and other publicly available information. Although

we believe that such sources are reliable, we do not guarantee the accuracy or completeness of this information, and we have not

independently verified such information. We caution readers not to place undue reliance on any forward-looking statements. We do

not undertake, and specifically disclaim any obligation, to update or revise such statements to reflect new circumstances or unanticipated

events as they occur, and we urge readers to review and consider disclosures we make in this and other reports that discuss factors

germane to our business. See in particular our reports on Forms 10-K, 10-Q, and 8-K subsequently filed from time to time with the

Securities and Exchange Commission.

PART I

Overview

ComHear,

Inc. (the “company” or “we” or “us”) was incorporated under the laws of the State of Delaware

on October 12, 2012, however, our current business operations commenced in January 2010. Please see “Our Company” further

below for a summary of our corporate formation and development and a discussion of our predecessor operations.

We

are an audio and wearables technology products, software and services company. Our wearables technology category is defined

as “In the Service of Sound” and we produce “Audio that feels good, sounds great, and is good for

you.” We have four primary areas of focus, as follows:

Ÿ We

have developed comfortable, extended wear earbud, eartips and ear headset products, which we market under the trademarks EarPuff

and EarTOPs, respectively. Our EarPuff and EarTOPs are based on a proprietary and eco-friendly product known as BioFoam, a biodegradable

and disposable material and process for comfortable, extended wear earbud, eartips and on/over the ear headset products. We intend

to market and sell our BioFoam based EarPuff and EarTOPs to the in the ear and the on/over the ear headset OEMs and industrial

verticals segments. We believe these products provide a consistent and superior comfortable fit for active, extended personal daily

use.

Ÿ We

have developed Kinetic Audio Processing (KAP) software which we intend to market as a stand-alone software application to

headset OEMs and bundle with our EarPuff and EarTOPs products. Our KAP software produces

a psychoacoustic effect that provides a richer and louder sound without increasing the overall sound pressure level, or volume.

We believe this technology opens a new world of immersive and high quality audio for both in ear and over the ear headsets without

needing to use high volume settings to obtain the same result. We intend to bundle with our EarPuff and EarTOPs products and license

to chipset manufacturers.

Ÿ We

have an audio wearable line called Playbutton that is a patent protected MP3 digital music player in the form of a fully customizable,

brandable button. We intend to further develop the Playbutton to include advanced audio, communication and sensing technologies

to create a wearable technology platform for delivering audio content and services.

Ÿ We

have acquired an exclusive license to audio beamforming technology that is intended to deliver personal audio communications without

a headset for personal audio, conferencing, automotive, home theater, and other applications. We intend to develop commercial applications

of the audio beamforming technology under the trademark, “MyBeam.”

We

commenced the sales of our Playbutton product in 2012 and to date all of our revenue from operations has been derived from our

sale of the Playbuttons. We have completed the development of our EarPuff and EarTOPs products and KAP software are currently pursuing

licensing and distribution agreements with OEM and other industry participants. As of the date of this report, we have entered

into a sales representation agreement with Wolfson Microelectronics PLC, however we have not entered into any agreements with OEMs

or others for the distribution and sale of our EarPuff, EarTOPs or KAP software.

Our

management team created the category of mobile headset and wearable technology back in the early 1990s while with Jabra Corp.,

which became the leading mobile headset company in North America and was acquired by GNNetcom in 2000. While at Jabra, our management

team conducted several innovations, including being the first to miniaturize and fit a speaker and microphone in the ear, developing

the first over-the-air programming for headset settings, and inventing and patenting the EarGel, the most comfortable headset eartip

to date - until EarPuff.

Our

goal is to become a globally recognized audio and wearable technology market leader. We intend to pursue our goal by leading with

a thesis of making audio sound and feel great for extended wear, expanding on our Playbutton audio platform to include enhanced

audio and then sensing capabilities, and focusing on the development of innovative software and service for the audio OEM and retail

markets. We intend to start with OEM and retail distribution partners and brands to drive scale, market awareness, and branding,

and then build the brand into a globally recognized leader in our target segments.

Our Market

The

global headset market is estimated to reach 1.5 billion – 2 billion units in 2013 through inclusion with mobile devices,

personal audio players and through retail. The global retail headset market is expected to grow from $5 billion in 2012 to over

$6 billion by 2013 and continue at a 20% annual growth rate through 2018. We intend to sell our EarPuff and EarTOPs products first

to the OEM segment to drive consumer awareness and manufacturing scale and then enter retail in late 2014 with one of our OEM partners

that has strong retail presence. The wearable technology market, which includes smart watches, reality augmentation devices such

as Google Glass, as well as motion, sensing, bio-assistive and other technologies, is expected to grow from $2.7 billion in 2012

to over $15 billion in 2018. We intend to focus our marketing in wearables technology on our Playbutton product and grow it as

a platform for other audio and sensing technologies. Global advertising expenditures in North America are expected to grow 3.5%

in 2013 to a projected $505 billion global Ad-spend for the year. We have structured our brand partnership approach by targeting

trendsetting, influential brands to position the Playbutton as the future product by combining music and brand. In 2012, Total

music purchases (Physical Albums, Digital Albums and Digital Songs) were at an all-time high, surpassing 1.65 billion units that

year, up 3.1% vs. 2011. For the fifth consecutive year, more vinyl albums were purchased than any other year in the history of

Nielsen SoundScan. In 2012, vinyl album sales reached 4.6 million in sales, breaking the previous record of 3.9 million LP

album sales in 2011. Since premium purchasers are less price sensitive and are actively seeking for a higher valued product, we

believe that value is not about price but about the balance between price and benefits. Our internal research suggests that with

digital having no physical tangibility, the ‘super fan’ is still seeking to buy a physical or premium format of music.

We believe the Playbutton provides recording artists and their labels with a unique opportunity to reach these premium purchasers

who are looking for a special fan experience.

Products and Services

EarPuff

Our EarPuff is a BioFoam-based

eartip that fits on the earpiece part of a headset that fits into the ear canal. We believe that the EarPuff has many superior

qualities to the silicon or pvc eartips currently in use. Our internal testing demonstrates that the EarPuff provides greater passive

noise cancellation than other retail in-the-ear headsets. In addition, we believe the EarPuff provides a better and more consistent

coupling to the ear canal, which reduces the loss of low frequencies typical in many earbud products. We intend to market the EarPuff

primarily as an OEM part to the manufacturers of headset devices. We customize the EarPuff for headset OEMs by way of our EarSeq

connector, an insert that allows the EarPuff to meet or exceed manufacturer’s pull-test requirements while conforming to

the various eartip attachment nozzle specifications of the various headset OEMs.

The primary component

of our Ear Puff and EarTOP products is BioFoam, a proprietary soy-based product for which we have an exclusive license. Pursuant

to our collaboration agreement with the licensor, we hold the exclusive right, for a seven year period ending October 2020 to manufacture

and sell wearable electronics, sensors and audio products utilizing BioFoam. We believe our BioFoam based EarPuff provides a tighter

and more consistent fit than non-foam tips and accommodates more ear-type variations. The BioFoam allows perspiration to evaporate

rather than accumulate and the expansive properties of BioFoam provides a more comfortable and sustained fit, resulting in a headset

that is less prone to fall out of the ear. Finally, BioFoam distributes the weight of the headset evenly across the entire ear

canal and devices utilizing our BioFoam-based EarPuff feel perceptively lighter. BioFoam is sustainable and biodegradable and yet

durable.

We have completed the

development of our EarPuff and are currently pursuing licensing and distribution

agreements with OEM and other industry participants. We expect to sell EarPuffs in pairs, bundled as a “Pair and Spares”

or in sets, as specified by our OEM customers. We also plan to create multiple pair sets for aftermarket channels, as well as industrial

quantity (500 to 2,500 units) packaging for healthcare, call center, and other enterprise verticals. We have received initial testing

quantity orders for EarPuff from certain OEMs and channel partners and are actively working with large headset OEMs towards integration

into their supply chain. We anticipate the commencement of sales of our EarPuff products to headset OEMs in or about the second

half of 2014.

EarTOPs

The EarTOPs is an earpad,

or cushion, for on-the-ear and over-the-ear headset products. The EarTOPs also utilizes BioFoam as its primary component and is

customized for headset OEMs by way of our EarSeq connector. The EarTOPs offers many of the same characteristics of the EarPuff,

including:

| · | Soft, comfortable, BioFoam earpad; |

| · | A slow resiliency for a consistent fit, better sounding audio and sound isolation; |

| · | Passive noise cancellation; |

| · | Cooler than the leather or leather alternatives (by 10-15% according to 3rd party testing); |

| · | Customized to connect to on/over-the-ear headsets with our EarSeq; and |

| | · | Made

from sustainable soy-based BioFoam. |

Similar to the EarPuff,

we intend to market the EarTOPs primarily as an OEM part to the manufacturers of headset devices and also to certain aftermarket

channels. We have completed the development of our EarTOPs and are currently pursuing

licensing and distribution agreements with OEM and other industry participants. We anticipate the commencement of sales

of our EarTOPs products to headset OEMs in or about the second half of 2014.

KAP Software

We

have developed kinetic audio processing (KAP) software which we intend to market as a stand-alone software application to

headset OEMs and bundle with our EarPuff and EarTOPs products. Our KAP software produces

a psychoacoustic effect that provides a richer and louder sound without increasing the overall sound pressure level, or volume.

We believe this technology opens a new world of immersive and high quality audio for both in ear and over the ear headsets without

needing to use high volume settings to obtain the same result. We intend to bundle the KAP software with our EarPuff and EarTOPs

products and license to chipset manufacturers.

Our KAP software was

created by our chief technology officer, Alan Kraemer, who holds over 25 patents in digital audio signal processing and is the

former chief technology officer of SRS Labs, Inc., a Santa Ana, California-based

audio technology engineering company that specializes in audio enhancement solutions for a wide variety of consumer electronic

devices. The KAP software is optimized on a headset-by-headset basis to increase performance in low-cost headset speaker drivers

or elevate the richness of higher-end drivers. We intend to license our KAP software to headset OEMS and audio chipset companies.

We also intend to offer the KAP software as a bundled product with our EarPuff and EarTOPs. We have completed development of KAP

for porting to audio chipsets and we have developed customized applications in order for the software to be integrated into iOS,

Android and Windows mobile phone applications.

Playbutton

The Playbutton is a

patent-protected fully customizable music player housed in a branded, wearable button. In its physical form, the Playbutton is

a low cost MP3 digital music player with the characteristics and quality of an iPod Shuffle. The Playbutton is unique in that it

comes in the form of a wearable button that can be pinned to your shirt or jacket. The button is customizable to offer the customer

the opportunity to either promote its brand name or logo in the case of major retailers and other commercial enterprises, as in

the case of Giorgio Armani, Gap and Coca Cola, or promote the artist whose music is featured on the device, as in the case of Justin

Bieber, Lady Gaga, Florence + the Machine and other major recording artists. We manufacture our Playbutton device according to

the specifications and customized details of our customers. The Playbutton device can be produced with up to 16 GB of memory, thereby

allowing artist, brands and others to also offer video content by way of the device in addition to music.

We initially intend

to distribute the Playbutton through three vertical markets, consisting of our OEM and retail partners,

brands and venues or artist merchandise facilities. For OEM and retail partners, our Playbutton represents a new medium

to enhance their products, increase revenue, and sub-brand by aligning with target segment-specific artists and genres. For brands,

our Playbutton and the music and other digital content loaded onto the Playbutton is a unique and stylish way for major brands

to promote brand identity and loyalty, by making each user a walking billboard and advocate. This peer-to-peer marketing allows

for increased brand recognition through its targeted spread. For venues or artist merchandise facilities, our Playbutton allows

artists to sell their albums plus exclusive content and insights at concerts, or to allow users to return from a concert with a

date specific tour button of their favorite artist and download the recorded audio from that nights’ performance.

MyBeam

We have acquired an

exclusive license to audio beamforming technology that we believe is capable of delivering personal audio communication without

a headset. The technology has the potential to create personal listening areas in a public space. For example, a device incorporating

the technology might target discrete audio beams to a primary user or group of users. Those users might be targeted by location,

sensors, or an application and the beams could contain different content for different users. In another case two beams will be

directed towards the left and right ears of a single listener to enable 3D binaural reproduction without the use of headphones.

We intend to develop commercial applications of the audio beamforming technology under the trademark, “MyBeam,” for

audio, conferencing, automotive, home theater and other applications.

The MyBeam device currently

under development is approximately the length of a tablet and links to a user’s laptop, tablet or smartphone and relies on

the two beam binaural modality described above. The device is intended to allow the user to reshape the incoming audio. Using the

MyBeam technology, participants in a teleconference are expected to be able to control the acoustic position of other participants

relative to where the user is located on screen. Instead of all voices on a conference call seeming to come from a single point

in space, the MyBeam device will allow the user to make each voice appear to come from a different location, which should improve

intelligibility and be capable of cognitively grouping a team or provide for sidebars within a conference. The system is also intended

to allow the user to move participants acoustically closer or farther away, thereby providing control over the audio mix of the

conference call. The MyBeam technology will employ software and hardware, including speaker arrays, to target a specific audio

feed to a specific listening zone.

Other uses of the MyBeam

technology potentially include in car, where navigation instructions would be placed in space where the next command may be, to

the left for a left turn, thereby lowering the cognitive load of the driver and preventing left/right confusion for increased safety.

At the same time as the navigation beam is being sent to the driver, the passenger next to the driver might be listening to a beam

of music.

In the binaural modality,

MyBeam is intended to be able to produce a high definition three dimensional listening experience that is referred to as holographic

audio. Piggybacking on the trend towards personal media consumption on tablets and smartphones, we intend to provide an experience

that immerses the user and not the entire room in a multidimensional personal theater experience.

The MyBeam technology

and commercial applications are currently under development and we expect to complete the first prototype of the device before

December 2014 and introduce the first device for commercial sale by June 2015. The MyBeam technology was invented by the Sonic

Arts R&D group of the Qualcomm Institute, a division of the University of California at San Diego. We acquired a license to

the patented technology pursuant to a license agreement effective February 1, 2014 with the Regents of the University of California.

The license grants us the US rights to utilize the patented technology in all consumer and enterprise electronics and software

services, excluding only microphone arrays. The term of the license is for the life of the underlying patents. For the first five

years of the license agreement, or until February 1, 2019, our license rights are exclusive and thereafter they are renewable or

may be non-exclusive.

Marketing

We intend to market

our EarPuff and EarTOPs products and KAP software to OEM headset and chipset manufacturers. We intend to support our OEM and retail

partners with online and printed marketing materials detailing the features and benefits of our products, white papers showing

the technical benefits and advantages of our products, and supporting the tech press and blogging community around quality audio

and wearable technology to drive market awareness of our products and mission. We also intend to distribute our Playbutton

through OEM and retail partners and directly to brands and venues or artist merchandise facilities. We have established an online

store at which end users can build and purchase their own customized Playbutton.

Manufacturing

We do not own any

manufacturing facilities and intend to utilize third party manufacturing for all of our products. We currently produce our Playbutton

products through contract manufacturers located in China, and we expect that all or substantially all of our EarPuff and EarTOPs

products will also be manufactured in China. We do not have any long-term contracts with our existing manufacturers. We procure

finished and packaged products from our manufacturers so that we require no subassembly.

Competition

Competition for the

eartip or earpad segment falls into three main categories, internally manufactured eartips, third party eartip or earpad sourced

from China, and Comply foam, a product line from Hearing Components, Inc. Most of our competitors have significant competitive

advantages, including greater financial, distribution, marketing and other resources, longer operating histories, better brand

recognition among certain groups of consumers, and greater economies of scale. In addition, many of these competitors have long-term

relationships with many of the larger retailers.

We intend to compete

against the established eartip and earpad products on the basis of comfort, audio sound quality and cost. We believe that our BioFoam

based EarPuff and EarTOPs products are softer and more comfortable than the existing silicon and foam products currently in use.

We also believe that our products provide a better and more consistent fit for the user. We believe we are the only company that

bundles audio enhancing software with an eartip or ear pad specifically tuned to each headset for no additional cost to the OEM.

As a result of the superior fit and the noise cancelling KAP software, we believe that our EarPuff and EarTOPs products will provide

a superior audio experience.

The Playbutton is a

multi-faceted device that competes on several levels. Even though the Playbutton is unique in that it is positioned to spans over

three different verticals, each of our target markets are highly competitive and we will be confronted by competition in all areas

of our business. In addition, the great majority of our competitors have far greater experience and resources than we do. Further,

the marketing of any product or service that, like the Playbutton, relies on the element of fashion and style, is subject to intense

competition from other products and services that seek to influence and respond to evolving styles, trends and personal tastes.

As a music player, the Playbutton must compete with well-established music player devices, most importantly the iPod and iPod Shuffle

devices manufactured by Apple, Inc., as well as smartphones, virtually all of which can operate as a music player device. As a

music distribution device, the Playbutton will have to compete directly with a well-established music distribution industry, including

traditional CDs and downloadable music content such as Apple’s iTunes Store.

Intellectual Property and Proprietary Rights

We have filed patent

applications for our Ear Puff (in-the-ear headset eartip), EarSeq (headset-to-eartip-sequence connector), EarTOP (on/over-the-ear

headset pad), and our KAP (kinetic audio processing) software. The pending Ear Puff patent applications were filed in the United

States, Canada, Japan, China and the European Union. The pending EarSEQ, EarTOPs and KAP patent applications were filed in the

United States. Our trademark for “EarPuff” has been registered as U.S. Registration No. 4418796 and has pending applications

in Canada, Japan, China, the EU, and other foreign jurisdictions. The trademark application for “EarSeq” has been filed

with the U.S. Trademark Office and is currently pending.

With regard to our

Playbutton product, we own three U.S. design patents covering ornamental designs for a portable media player in the form of a button,

including the U.S. Patent No. D645,473 issued on September 9, 2011, U.S. Patent No. D657,775 issued on April 17, 2012 and

U.S. Patent No.D669,500 to be issued on October 23, 2012. We have filed an international patent application under the Patent Cooperation

Treaty and applied for a utility patent in Canada. We also own the U.S. and European registered trademarks for the mark “Playbutton.”

We acquired the Playbutton patent and trademark rights in October 2012 from Parte, LLC, which is controlled by Nick Dangerfield,

a former member of our board of directors and the inventor of the Playbutton. In connection with that acquisition, we issued to

Parte an irrevocable, royalty-free license to manufacture and sell Playbuttons in Japan, South Korea and Taiwan.

The primary component

of our Ear Puff and EarTOPs products is BioFoam, a proprietary soy-based product which we license from the owner. Pursuant

to a collaboration agreement between us and the owner of the BioFoam product, we hold the exclusive right, for a seven year period

ending October 2020, to manufacture and sell wearable electronics, sensors and audio products utilizing BioFoam.

We acquired a license

to the patented MyBeam technology pursuant to a license agreement effective as of February 1, 2014 with the Regents of the University

of California. The license grants us the US rights to utilize the patented technology in all consumer and enterprise electronics

and software services. The term of the license is for the life of the underlying patents. For the first five years of the license

agreement, or until February 1, 2019, our license rights are exclusive and, thereafter, our license rights will become non-exclusive

unless we are able to negotiate an extension of our exclusive license rights. The license agreement imposes certain conditions

on our continued license rights, including our commitment to (i) pay royalties on the net sales of products and software

incorporating the licensed patents; (ii) spend the funds necessary to successfully commercialize the licensed products, currently

estimated to be $3 million, including a minimum of $1.5 million during the first year of the agreement; and (iii) successfully

develop the first prototype by December 1, 2014 and introduce the first licensed product for sale in the US by June 30, 2015.

We have also entered

into a Multiple Project Research Agreement dated February 4, 2014 with the Regents of the University of California. Pursuant to

this agreement, we have agreed to collaborate with the University of California on certain research projects from time to time

over the three year term of the agreement. We have agreed to support the research under the agreement with up to $800,000 of funding

per year, for a total of $2.4 million. Any inventions or discoveries made under the agreement by the University of California alone

or jointly with us will be owned solely by the University or owned jointly with us, respectively. The agreement provides us with

the first right to negotiate a commercial, royalty bearing license to any inventions or discoveries under the agreement that are

owned by the University solely or jointly with us.

Government Regulation

Our business is subject

to federal, state and international laws relating to the manufacture and sale of electronic devices and the distribution of proprietary

content.

Our Company

ComHear, Inc. (“we”

or “us” or “the company” or “ComHear”) was formed on October 12, 2012 under the laws of the

State of Delaware under the name Playbutton Acquisition Corp. We were formed for the purpose of acquiring Playbutton, LLC, a Delaware

limited liability company engaged in the business of marketing its core product, the Playbutton, a customizable music player housed

in a branded, wearable button. On October 15, 2012, we entered into a Unit Exchange Agreement with Playbutton, LLC and the members

of Playbutton, LLC pursuant to which the members of Playbutton, LLC agreed to transfer to us all of the issued and outstanding

membership interests of Playbutton, LLC in exchange for our issuance of 3,384,079 shares of our common stock to the members of

Playbutton, LLC. We closed on our acquisition of Playbutton, LLC on December 18, 2013, at which time Playbutton, LLC became our

wholly-owned operating subsidiary and the former members of Playbutton, LLC, as a group, became our controlling shareholders.

In connection with

our acquisition of Playbutton, LLC, on October 15, 2012, Playbutton, LLC entered into an Intellectual Property Purchase Agreement

with Parte, LLC, the owner of the patents, trademark and other proprietary rights relating to the Playbutton product. Parte is

owned by Nick Dangerfield, the inventor of the Playbutton. In September 2011, Playbutton, LLC had entered into a license agreement

with Parte pursuant to which Parte granted Playbutton, LLC the exclusive rights to use the patents, trademark and other proprietary

rights relating to the Playbutton product in all areas of the world other than Japan, Taiwan and South Korea. Pursuant to the Intellectual

Property Purchase Agreement, Parte sold to Playbutton, LLC all right, title and interest in and to all patents, trademark and other

proprietary rights relating to the Playbutton product in consideration of our issuance of 892,375 shares of our common stock to

Parte. In addition, Playbutton, LLC entered into a License Agreement with Parte pursuant to which Playbutton, LLC granted to Parte,

effective as of the close of the transactions under the Intellectual Property Purchase Agreement, an exclusive, perpetual and royalty-free

license to use the Playbutton intellectual property in Japan and a non-exclusive, perpetual and royalty-free license to use the

Playbutton intellectual property in Taiwan and South Korea.

Following the execution

of the Unit Exchange Agreement, Intellectual Property Purchase Agreement and Parte License Agreement, we commenced the private

placement of 2,000,000 units of our securities at $2.00 per unit, each unit consisting of two shares of our common stock and one

warrant to purchase one share of our common stock at an exercise price of $1.50 per share. The private placement was conducted

by WFG Investments, Inc., as placement agent. In the private placement, we sold a total of 1,264,275 units to 43 investors for

the net proceeds of $2,257,050, after payment of WFG Investments’ commissions.

On February 21, 2013,

we changed our corporate name to Playbutton Corporation.

On December 5, 2013,

we entered into a Unit Exchange Agreement with Taida Company, LLC and the members of Taida, pursuant to which the members of Taida

agreed to transfer to us all of the issued and outstanding membership interests of Taida in exchange for our issuance of 7,578,651

shares of our common stock to the members of Taida. Taida, LLC was founded by Randy Granovetter, our current president and chief

executive officer, and is the owner of the audio technology relating to the EarPuffs, EarTOPs, KAP software and MyBeam products.

We closed on our acquisition of Taida on January 17, 2014, at which time Taida, LLC became our wholly-owned operating subsidiary

and the former members of Taida, LLC, as a group, become our controlling shareholders. At that time, the senior management of Taida,

including Randy Granovetter, Mike Silva, Gordon Schenk, and Alan Kraemer, were appointed to serve as our senior executive officers.

In connection with

our acquisition of Taida Company, LLC, we made arrangements for the cancellation of 2,809,891 shares of our issued and outstanding

common stock. In October 2013, Silent Ventures, LLC, formerly the principal stockholder of our company, conducted the private sale

of all 2,230,584 shares of our common stock held by Silent Ventures. The purchaser of those shares has agreed to cancel, for no

consideration, 1,730,584 of the common shares formerly held by Silent Ventures subject and immediately prior to our acquisition

of Taida. In addition, Parte LLC, our second largest stockholder, agreed to sell back to us 1,079,307 shares of our common stock

held by Parte for the total consideration of $175,000. Our repurchase of the 1,079,307 shares from Parte and the cancellation of

the 1,730,584 shares formerly held by Silent Ventures took place on January 31, 2014.

Following the execution

of the Unit Exchange Agreement with Taida, LLC, we commenced the private placement of shares of our common stock at $1.23 per share.

The private placement was conducted by WFG Investments, Inc., as placement agent. In the private placement, we sold a total of

4,067,051 shares to 47 investors for the gross proceeds of $5,002,473, including $4,772,475 of cash proceeds and the conversion

to our common shares of $229,998 of investment notes previously issued by Taida. We paid fees and sales commissions of $319,896.80

in connection with the private placement.

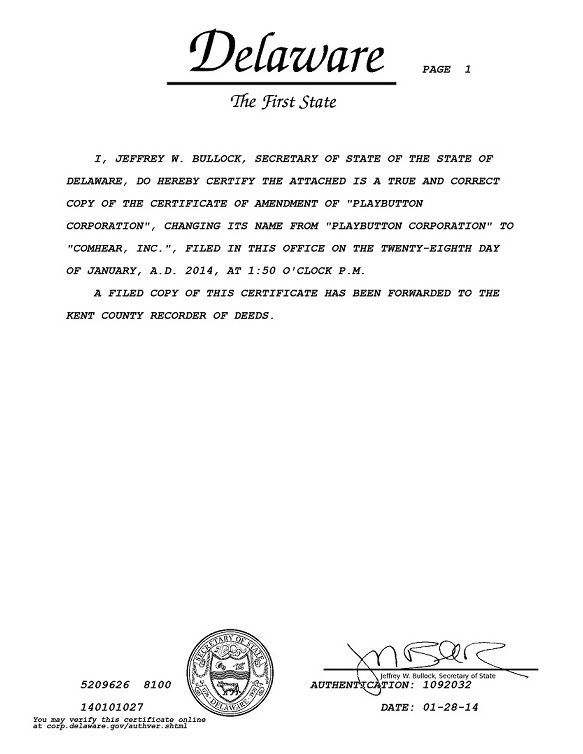

On January 28, 2014,

we changed our corporate name to “ComHear, Inc.”

Employees

As of the date of this

report, we have 16 employees.

Available Information

Our website is located

at www.comhear.com. The information on or accessible through our website is not part of this annual report on Form 10-K. A

copy of this annual report on Form 10-K is located at the SEC’s Public Reference Room at 100 F Street, NE, Washington,

D.C. 20549. Information on the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330. The

SEC also maintains an internet site that contains reports and other information regarding our filings at www.sec.gov.

There are numerous

and varied risks, known and unknown, that may prevent us from achieving our goals. If any of these risks actually occur,

our business, financial condition or results of operation may be materially adversely affected. In such case, the trading

price of our common stock could decline and investors could lose all or part of their investment.

Since we have

a limited operating history, it is difficult for potential investors to evaluate our business. We commenced revenue-producing

operations in late September 2011 and from inception through December 31, 2013, we have generated $1,224,338 of revenue, all of

which relates to our sale of our Playbutton product. In January 2014, we acquired Taida Company, LLC, the owner of the assets and

operations relating to our EarPuff, EarTOPS, BioFoam technology, KAP and software and MyBeam technology. Taida was formed in January

2010 and as of the date of this report has not commenced revenue producing operations. Our limited operating history makes it difficult

for potential investors to evaluate our historical or prospective operations. As an early stage company, we are subject to all

the risks inherent in the initial organization, financing, expenditures, complications and delays in a new business. Investors

should evaluate an investment in us in light of the uncertainties encountered by developing companies in a competitive environment.

Our business is dependent upon the implementation of our business plan. There can be no assurance that our efforts will be successful

or that we will ultimately be able to attain profitability.

We may need additional

financing to execute our business plan and fund operations, which additional financing may not be available on reasonable terms

or at all. As of December 31, 2013, we had approximately $$943,492 of working capital. Since December 31, 2013, we acquired

an additional $5,002,473 of working capital through the sale of our common shares, including $4,772,475 of cash proceeds and the

conversion to our common shares of $229,998 of investment notes previously issued by Taida. While we believe that our working capital

on hand as of the date of this report will be sufficient to fund our operations for, at least, the next 12 months, there can be

no assurance that we will not require significant additional capital within the next 12 months. For example, in our Ear Puff line

of business, we will endeavor to receive upfront payments from OEMs to cover custom tooling and early production. However, we may

be unable to obtain upfront payments from the OEMs or we may want to forego upfront payment in order to obtain better commercial

terms or we may encounter a situation where we need to ramp up our production faster than we are able to finance through payments

from our OEM customers. In either situation, we may require additional capital for investment, operations and working capital.

As another example, to date, we have been able to finance the production of our Playbutton products by way of upfront payments

received from our customers at the time of their placement of a purchase order. While we believe that we will continue to be able

to obtain advance deposits sufficient to fund production of non-retail purchase orders, there can be no assurance that this practice

will not change as result of adverse economic conditions impacting our customers or otherwise. Also, in the event that we are able

to secure a large retail order, for example an order for Playbutton music albums for distribution through Walmart, Target or the

like, the retailer is unlikely to provide an adequate advance to build the required inventory. In the event we are no longer able

to obtain advance deposits from non-retail customers or we acquire a large retail order, we may require additional capital in order

to finance the production of product inventory.

In the event we require

additional working capital, we will consider raising additional funds through various financing sources, including the sale of

our equity and debt securities and the procurement of commercial debt financing, with a bias toward debt financing over equity

raisings. However, there can be no guarantees that such funds will be available on commercially reasonable terms, if at all. If

such financing is not available on satisfactory terms, we may be unable to expand or continue our business as desired and operating

results may be adversely affected. Any debt financing will increase expenses and must be repaid regardless of operating results

and may involve restrictions limiting our operating flexibility. If we issue equity securities to raise additional funds, the percentage

ownership of our existing stockholders will be reduced and our stockholders may experience additional dilution in net book value

per share.

Our ability to obtain

needed financing may be impaired by such factors as the capital markets, both generally and specifically in our industry, and the

fact that we are not yet profitable, which could impact the availability or cost of future financings. If the amount of capital

we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital

needs, we may be required to reduce or even cease operations.

We

are continuing to develop customer acceptance of our Playbutton products and we have not yet launched our EarPuff, EarTOPS or KAP

products and software. Until such time as our products and software are widely accepted in the marketplace we do not expect to

achieve a profitable level of operations. We commenced the marketing and sale of our Playbutton products in September

2011 and through December 31, 2013 we have generated only $1,224,338 of revenue from our Playbutton’s operations. While we

have completed the development of our Ear Puff and EarTOPS products and our KAP software, we have not generated any revenue from

their sale or licensing nor have we entered into any agreements with OEMs or others with respect to the licensing of our Ear Puff

or EarTOPS or our KAP software. We may be unable to generate sufficient

demand for our products and software. If we fail to generate sufficient demand for our products and software, we may be unable

to sustain operations or generate a return to investors. No independent organization has conducted market research providing management

with independent assurance from which to estimate potential demand for our products and software. The overall market may not be

receptive to our products, and we may not successfully compete in the target market for our products.

Our

products are subject to certain licensing requirements and we may not be able to maintain those licensed rights. The

primary component of our Ear Puff and EarTOPS products is BioFoam, a proprietary soy-based product which we license from its owner.

Pursuant to a collaboration agreement between us and the owner of the BioFoam product, we hold the exclusive right, for a seven

period ending October 2020, to manufacture and sell wearable electronics, sensors and audio products utilizing BioFoam. Our continuing

rights to the BioFoam product are subject to customary terms and conditions and our failure to comply with those terms and conditions

could result in the loss of our rights to use the BioFoam product. We also acquired a license to the patented MyBeam technology

and device pursuant to a license granted by the University of California. Our MyBeam license agreement imposes certain conditions

on our continued license rights, including our commitment to spend the funds necessary to successfully commercialize the licensed

products, currently estimated to be $3 million, and successfully develop the first prototype by December 1, 2014 and introduce

the first licensed product for sale in the US by June 30, 2015. The loss of our rights to use the BioFoam

product or MyBeam technology for any reason would have a material adverse effect on our operations and prospects and could result

in the termination of the line of products impacted by the loss of license rights.

We depend upon

a limited number of third-party suppliers to provide our component parts and manufacture our finished products, and any disruptions

in the operations, or the loss, of any of these third parties, could harm our ability to meet our delivery obligations to our

customers, reduce our revenues, increase our cost of sales and harm our business. We have exclusive materials sourcing

and manufacturing contracts for our Ear Puff and EarTOPS products and any future products incorporating BioFoam. While these contracts

provide us with certain strategic and competitive advantages, they also provide a reliance on our supply and manufacturing partners.

We have attempted to mitigate our dependence on our supplier and manufacturer of BioFoam-based products by including provisions

in our agreements that provide for additional manufacturing partners in certain circumstances. Were we to need to move to other

suppliers of our BioFoam based products, there would most likely be time delays and additional capital investment required which

would impact our operations and may put delivery commitments to our customers at risk. With respect to our Playbutton product,

we source all of our component parts from suppliers in Asia, primarily China, and our Playbutton products are manufactured by

third-party contract manufacturers located in China.

A supplier’s

ability to meet our product manufacturing demand is limited mainly by its overall capacity and current capacity availability. Our

ability to meet customer demand depends, in part, on our ability to obtain timely and adequate delivery of parts and components

from our suppliers. A reduction or interruption in our product supply source, an inability of our suppliers to react to shifts

in product demand or an increase in component prices could have a material adverse effect on our business or profitability. Component

shortages could adversely affect our ability and that of our customers to ship products on a timely basis and, as a result, our

customers’ demand for our products. Any such shipment delays or declines in demand could reduce our revenues and harm our

ability to achieve or sustain desired levels of profitability. Additionally, failure to meet customer demand in a timely manner

could damage our reputation and harm our customer relationships. Our operations may also be harmed by lengthy or recurring disruptions

at any of our suppliers’ manufacturing facilities and by disruptions in the distribution channels from our suppliers and

to our customers. Any such disruptions could cause significant delays in shipments until we are able to shift the products from

an affected manufacturer to another manufacturer. If the affected supplier was a sole-source supplier, we may not be able to obtain

the product without significant cost and delay. The loss of a significant third-party supplier or the inability of a third-party

supplier to meet performance and quality specifications or delivery schedules could harm our ability to meet our delivery obligations

to our customers and negatively impact our revenues and business operations.

A significant

portion of our component parts are subject to significant price fluctuations, which can adversely impact our cost of sales and

profit margin. Approximately 72% of our cost of goods of a Playbutton is represented by the battery, PCBA (circuit board)

and flash memory components. While these components are readily available from a number of suppliers, the cost of each component

has historically been subject to significant price fluctuations based on supply and demand. To date, we have been able to produce

our Playbutton products on a just-in-time basis which allows us to minimize the risk that the component costs may significantly

increase from the time we contract with our customer to the time we order the component parts. We believe that as our production

runs and associated component purchases increase, we will be able to minimize the risks associated with component pricing by inventorying

component parts and entering into hedge transactions that secure the delivery of component parts at reasonable prices. Until such

time, if ever, as we are able to minimize the risk associated with the cost of our product components, any significant increase

in the costs of the Playbutton battery, PCBA (circuit board) or flash memory components may negatively impact our profit margin

for our Playbutton products sold.

We may be unable

to adequately protect our intellectual property rights and our existing intellectual property rights may not effectively protect

us from competition. Our success depends upon maintaining the confidentiality and proprietary nature of our intellectual

property rights, including our patents and our trademarks. As of the date of this report, we have received U.S. trademarks for

“EarPuff” and “Playbutton”. We have filed for trademark registration of the “EarPuff” “EarTOPS”

and “EarSeq” trademarks in the U.S., Japan, China, the European Union, and other foreign jurisdictions, however, we

have not registered our Playbutton trademark outside of the United States nor our other marks in all foreign jurisdictions. While

we intend to conduct additional foreign registrations of our trademarks, there can be no assurance that we will be successful in

doing so. We have applied for and have pending patent applications for our Ear Puff (in-the-ear headset eartip), EarSeq (Headset-to-Eartip-Sequence

connector), EarTOPS (on/over the ear headset pad), and our KAP (kinetic audio processing) software in the United States, Canada,

the EU, China, Japan, and other foreign jurisdictions stemming from PCT patent applications. There can be no assurance that we

will be successful in acquiring issued patents in any jurisdiction for our EarPuff, EarSeq or EarTOPs products or the KAP software.

Our

ability to compete may be damaged, and our revenues may be reduced, if we are unable to protect our intellectual property rights

adequately. Patent, trademark, trade secret and copyright laws provide limited protection. The protections provided by laws governing

intellectual property rights do not prevent our competitors from developing, independently, products similar or superior to our

products. In addition, effective protection of copyrights, trade secrets, trademarks, and other proprietary rights may be unavailable

or limited in certain foreign countries. We may be unaware of certain non-publicly available patent applications, which, if issued

as patents, could relate to our products and software as currently designed or as we may modify them in the future. Legal or regulatory

proceedings to enforce our patents, trademarks or copyrights could be costly, time consuming, and could divert the attention of

management and technical personnel.

We may engage

in acquisitions or strategic transactions that could result in significant changes or management disruption and fail to enhance

stockholder value. From time to time, we may engage in acquisitions or strategic transactions with the goal of maximizing

stockholder value. However, achieving the anticipated benefits of acquisitions or strategic transactions will depend in part upon

our ability to integrate the acquired businesses, products or technologies in an efficient and effective manner. The integration

of businesses, products or technologies that have previously operated independently may result in significant challenges, and we

may be unable to accomplish the integration smoothly or successfully. We cannot assure you that the integration of acquired businesses,

products or technologies with our business will result in the realization of the full benefits anticipated by us to result from

the acquisition.

There is no public

trading market for our stock. As of the date of this report, there is no public trading market for our common stock. In

August 2013, we commenced the process of seeking approval from FINRA for the quotation of our common shares on the OTC Bulletin

Board, however we suspended the approval process pending the completion of our acquisition of Taida and our concurrent private

placement sale of our common shares. We intend to resume the process of seeking approval from FINRA for the quotation of our common

shares on the OTC Bulletin Board at the appropriate time. However, there can be no assurance that we will obtain FINRA approval

or that a market for our shares will develop. Furthermore, for companies whose securities are traded in the OTC Bulletin Board,

it is more difficult:

| · | to obtain accurate quotations, |

| · | to obtain coverage for significant news events because major wire services generally do not publish

press releases about such companies, and |

| · | to obtain needed capital. |

No Dividends.

We do not expect to pay cash dividends on our common stock in the foreseeable future.

Control By Management

May Limit Your Ability to Influence the Outcome of Director Elections and Other Transactions Requiring Stockholder Approval.

As of the date of this report, our directors and executive officers beneficially own approximately 42.3% of our outstanding common

stock. As a result, in addition to their board seats and offices, such persons will have significant influence over and control

all corporate actions requiring stockholder approval, irrespective of how our other stockholders, including investors in the offering,

may vote, including the following actions:

| · | to elect or defeat the election of our directors; |

| · | to amend or prevent amendment of our certificate of incorporation or bylaws; |

| · | to effect or prevent a merger, sale of assets or other corporate transaction; and |

| · | to control the outcome of any other matter submitted to our stockholders for vote. |

Such persons’

stock ownership may discourage a potential acquirer from making a tender offer or otherwise attempting to obtain control of our

company, which in turn could reduce our stock price or prevent our stockholders from realizing a premium over our stock price.

| Item 1B. |

Unresolved Staff Comments |

Not applicable.

Company Executive Offices

We lease 1,800 square

feet in New York, New York on a month-to-month basis at the lease rate of $4,500 per month. We believe that our current facilities

are adequate for our foreseeable needs.

| Item 3. |

Legal Proceedings |

As of the date of this

report, there are no pending legal proceedings to which we or our properties are subject, except for routine litigation incurred

in the normal course of business.

| Item 4. |

Mine Safety Disclosures |

Inapplicable.

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters

and Issuer Repurchases of Equity Securities Market Information |

As of the date of this

report, there is no public trading market for our common stock. While we intend to pursue the process of seeking approval from

FINRA for the quotation of our common shares on the OTC Bulletin Board, there can be no assurance that we will be able to obtain

FINRA approval or that a market for our shares will develop.

Holders of Record

As of March 28, 2014,

there were approximately 65 holders of record of our common stock.

Dividend Policy

We have never declared

or paid cash dividends on our common stock. We presently intend to retain earnings to finance the operation and expansion of our

business.

Equity Compensation Plan Information

We have adopted the

a 2012 Equity Incentive Plan providing for the grant of non-qualified stock options and incentive stock options to purchase shares

of our common stock and for the grant of restricted and unrestricted share grants. We have reserved 2,500,000 shares

of our common stock under the plan. All officers, directors, employees and consultants to our company are eligible to

participate under the plan. The purpose of the plan is to provide eligible participants with an opportunity to acquire

an ownership interest in our company.

The following table

sets forth certain information as of December 31, 2013 about our stock plans under which our equity securities are authorized

for issuance.

| Plan Category | |

| (a)

Number of Securities to be Issued Upon Exercise of Outstanding Options | | |

| (b)

Weighted-Average Exercise

Price of Outstanding Options | | |

| (c)

Number

of Securities Remaining Available for Future Issuance Under Equity Compensation

Plans (Excluding Securities Reflected In Column (a)) | |

| Equity compensation plans approved by security holders | |

| 150,000 | | |

$ | 1.00 | | |

| 2,350,000 | |

| Equity compensation plans not approved by security holders | |

| – | | |

| – | | |

| – | |

| Total | |

| 150,000 | | |

$ | 1.00 | | |

| 2,350,000 | |

| Item 6. |

Selected Financial Data |

Not applicable.

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Introduction

ComHear, Inc. (“we”

or “us” or “the company” or “ComHear” ) was formed on October 12, 2012 under the laws of the

State of Delaware under the name Playbutton Acquisition Corp. We were formed for the purpose of acquiring Playbutton, LLC, a Delaware

limited liability company engaged in the business of marketing its core product, the Playbutton, a customizable music player housed

in a branded, wearable button. We acquired Playbutton, LLC on December 18, 2013, at which time Playbutton, LLC became our wholly-owned

operating subsidiary. On February 21, 2013, we changed our corporate name to Playbutton Corporation.

On January 17, 2014,

we acquired Taida Company, LLC, a Delaware limited liability company founded by Randy Granovetter, our current president and chief

executive officer. Taida is the owner of the audio technology relating to the EarPuffs, EarTOPs, KAP software and MyBeam technology.

On January 28, 2014, we changed our corporate name to ComHear, Inc. For a more complete summary of these transactions and other

material transactions concerning our corporate formation and development, please see Part I, Item 1 “Business - Our Company”.

Our audited consolidated

financial statements included in this report reflect our financial condition and results of operations as consolidated with Playbutton,

LLC. Because we completed our acquisition of Taida after our fiscal year end, our audited consolidated financial statements included

in this report do not reflect the financial condition and results of operations of Taida. As of the date of this report, Taida

had not commended revenue producing operations.

General

We

are an audio and wearables technology products, software and services company. Our wearables technology category is defined as

“In the Service of Sound” and we produce “Audio that feels good, sounds great, and is good for you.” We

have four primary areas of focus, as follows:

· We

have developed comfortable, extended wear earbud, eartips and ear headset products, which we market under the trademarks EarPuff

and EarTOPs, respectively. Our EarPuff and EarTOPs are based on a proprietary and eco-friendly product known as BioFoam, a biodegradable

and disposable material and process for comfortable, extended wear earbud, eartips and on/over the ear headset products. We intend

to market and sell our BioFoam based EarPuff and EarTOPs to the in the ear and the on/over the ear headset OEMs and industrial

verticals segments. We believe these products provide a consistent and superior comfortable fit for active, extended personal daily

use.

· We

have developed kinetic audio processing (KAP) software which we intend to market as a stand-alone software application to

headset OEMs and bundle with our EarPuff and EarTOPs products. Our KAP software produces

a psychoacoustic effect that provides a richer and louder sound without increasing the overall sound pressure level, or volume.

We believe this technology opens a new world of immersive and high quality audio for both in ear and over the ear headsets without

needing to use high volume settings to obtain the same result. We intend to bundle with our EarPuff and EarTOPs products and license

to chipset manufacturers.

· We

have an audio wearable line called Playbutton that is a patent protected MP3 digital music player in the form of a fully customizable,

brandable button. We intend to further develop the Playbutton to include advanced audio, communication and sensing technologies

to create a wearable technology platform for delivering audio content and services.

· We

have acquired an exclusive license to audio beamforming technology that is intended to deliver personal audio communications without

a headset for personal audio, conferencing, automotive, home theater, and other applications. We intend to develop commercial applications

of the audio beamforming technology under the trademark, “MyBeam.”

We

commenced the sales of our Playbutton product in 2012 and to date all of our revenue from operations has been derived from our

sale of the Playbuttons. We have completed the development of our EarPuff and EarTOPs products and KAP software are currently pursuing

licensing and distribution agreements with OEM and other industry participants. As of the date of this report, we have entered

into a sales representation agreement with Wolfson Microelectronics PLC, however we have not entered into any agreements with OEMs

or others for the distribution and sale of our EarPuff, EarTOPs or KAP software.

Results of Operations For the Years

Ended December 31, 2013 and 2012

| | |

Year Ended

December 31, | | |

Year Ended

December 31, | |

| | |

2013 | | |

2012 | |

| Net sales | |

$ | 174,750 | | |

$ | 683,463 | |

| Gross profit | |

$ | 40,502 | | |

$ | 157,347 | |

| Operating expenses | |

$ | 1,217,269 | | |

$ | 1,202,959 | |

| Loss from operations | |

$ | (1,176,767 | ) | |

$ | (1,045,612 | ) |

| Other income (expense) | |

$ | (43,668 | ) | |

$ | 533 | |

| Net loss | |

$ | (1,220,435 | ) | |

$ | (1,045,079 | ) |

| Loss per common share – basic and diluted | |

$ | (0.16 | ) | |

$ | (0.29 | ) |

Revenue

We had net sales for

the year ended December 31, 2013 and 2012 of $174,750 and $683,463, respectively. Net sales were driven by the sale of 13,514 Playbutton

units during the year ending December 31, 2013, and the sale of 61,185 Playbutton units during the year ending December 31, 2012.

Net sales decreased during the year ending December 31, 2013 compared to the prior year as a result of a decision by management

and the board in late 2012 to broaden our business plan from a focus solely on music publishers and brands looking to create customized

Playbuttons for specific marketing projects, which tend to be more sporadic and one-off transactions, to a retail centered focus

for mass quantity sales spanning multiple locations with recurring revenue streams. As we made the transition to retail and refocused

our resources, revenue dropped by approximately 75% in 2013. We began retail commercial trials in 2013, but to date have not executed

an agreement for national distribution with a retailer.

Gross Profit

Gross profit for the

years ended December 31, 2013 and 2012 was 23%, or $40,502 and $157,347, respectively. The decrease in gross profit was largely

the result of decreased revenue during the period.

Operating Expenses

Operating expenses

for the year ended December 31, 2013 were $1,217,269, as compared to $1,202,959 for the year ended December 31, 2012, an increase

of $14,310. The increase in operating expenses is primarily the result of:

| |

· |

An increase in payroll and payroll related expenses of $268,000 due to employee raises and the hiring of new employees during 2013; |

| |

· |

An increase in legal and professional fees in the amount of $309,000 as a result of our financing activities, public reporting requirements and business development consulting; |

| |

· |

An increase in charitable contributions of $9,000; |

| |

· |

An increase in rent and insurance expense of $36,000; |

| |

· |

An increase in conferences and travel related expense of $43,000; |

| |

· |

An increase in research and development expense of $19,000. Research and development expenses consist primarily of payments to third parties for the development of Our product. We expense research and development costs as incurred.; and |

| |

· |

An increase in bad debt expense of $12,000 due to the Company exhausting collection efforts and writing off an account during the year. |

These increases in operating expenses were

offset by a decrease in the following:

| |

· |

A decrease in stock based compensation of $680,000. The decrease was primarily due to stock awards issued during the prior year for intellectual property; |

| |

· |

A decrease in advertising expense in the amount of $18,500 as a result of significant non-recurring expenses incurred during the year ended December 31, 2012 associated with the development of our website; and |

| |

· |

A decrease in royalty expense of $8,900 due to an amendment to our former license agreement pursuant to which our royalty obligations were terminated starting in April 2012. |

Loss from Operations

Loss from operations

for the year ended December 31, 2013 was $(1,176,767), as compared to $(1,045,612) for the year ended December 31, 2012. The increase

in loss from operations was primarily attributable to the decrease in sales and the increase in operating expenses as detailed

above.

Other Income (Expenses)

Other income (expenses)

for the year ended December 31, 2013 was $(43,668), as compared to $533 for the year ended December 31, 2012. Other expense

during the year ended December 31, 2013 consisted of liquidated damages of $(52,248) due to our failure to meet the effectiveness

deadline of our registration statement. Other expense during the year ended December 31, 2012 consisted of interest expense of

$438. Other income during the comparable years consisted of interest income and miscellaneous income.

Net Loss

Net Loss for the year

ended December 31, 2013 was $(1,220,435) or loss per share of $(0.16), as compared to a net loss of $(1,045,079) or loss per share

of $(0.29), for the year ended December 31, 2012. The increase in net loss was primarily attributable to the decrease in sales

and increase in operating expenses and other income (expenses) as detailed above.

Inflation did not have

a material impact on the Company’s operations for the year.

Liquidity and Capital Resources

As of December 31,

2013, we had $943,492 of working capital. aOur working capital position has significantly improved following

our December 31, 2013 fiscal year end as a result of our private placement sale of 4,067,051 shares

of common stock at an offering price of $1.23 per share, of which 3,880,060 shares were sold for gross cash proceeds of $4,772,473

and 186,991 shares were sold for the conversion of $229,998 of indebtedness under the investment notes issued by Taida at the rate

of $1.23 per share. After the payment of $319,897 of selling commissions and fees, we realized cash net proceeds of $4,682,576,

of which $550,000 was applied towards the repayment of the remaining indebtedness under the Taida investment notes.

We believe that our

working capital on hand as of the date of this report will be sufficient to fund our plan of operations over the next 12 months.

However, there can be no assurance that we will not require additional capital within the next 12 months. For example, in our Ear

Puff line of business, we will endeavor to receive upfront payments from OEMs to cover custom tooling and early production. However,

we may be unable to obtain upfront payments from the OEMs or we may want to forego upfront payment in order to obtain better commercial

terms or we may encounter a situation where we need to ramp up our production faster than we are able to finance through payments

from our OEM customers. In either situation, we may require additional capital for investment, operations and working capital.

As another example, to date, we have been able to finance the production of our Playbutton products by way of upfront payments

received from our customers at the time of their placement of a purchase order. While we believe that we will continue to be able

to obtain advance deposits sufficient to fund production of non-retail purchase orders, there can be no assurance that this practice

will not change as result of adverse economic conditions impacting our customers or otherwise. Also, in the event that we are able

to secure a large retail order, for example an order for Playbutton music albums for distribution through Walmart, Target or the

like, the retailer is unlikely to provide an adequate advance to build the required inventory. In the event we are no longer able

to obtain advance deposits from non-retail customers or we acquire a large retail order, we may require additional capital in order

to finance the production of product inventory. . In the event we are no longer able to obtain advance deposits from non-retail

customers or we acquire a large retail order, we will require additional capital in order to finance the production of product

inventory. We would endeavor to acquire the required capital through commercial credit facilities, however there can be no assurance

we would qualify for commercial debt financing on terms acceptable to us or at all. If commercial debt financing is unavailable,

we would endeavor to acquire the additional capital through the sale of our debt or equity securities, the success of which there

can be no assurance.

Our plan of operations

over the next 12 months is to lower the cost of goods sold on our Playbutton product and focus on high unit revenue opportunities.

We are actively pursuing OEM sales with our EarPuff, EarTOP and KAP software and have a licensing agreement with Wolfson Microelectronics

plc for KAP software. We are investing in research and development to commercialize our MyBeam technology and will be pursuing

professional services contracts as we move towards commercial trials of our beamforming technology. We also intend to pursue strategic

opportunities to grow our business both organically and through acquisition. We intend to explore alliances and possible acquisitions

of complementary businesses.

The following table summarizes total current

assets, liabilities and working capital at December 31, 2013 and December 31, 2012.

| | |

December 31,

2013 | | |

December 31,

2012 | |

| Current Assets | |

$ | 1,136,960 | | |

$ | 2,177,837 | |

| Current Liabilities | |

| (193,468 | ) | |

| (70,543 | ) |

| Working Capital (Deficit) | |

$ | 943,492 | | |

$ | 2,107,294 | |

Net Cash Provided by (Used in) Operating

Activities

Net cash used in operating

activities for the years ended December 31, 2013 and 2012 was $(1,181,389) and $(350,014), respectively. The net loss for the years

ended December 31, 2013 and 2012 was $1,220,435 and $1,045,079, respectively. The increase in cash used in operating activities

for the year ended December 31, 2013 as compared December 31, 2012, was primarily for payroll and payroll related expenses, legal

and professional fees, and prepayments on inventory orders.

Net Cash Provided by (Used in) Investing

Activities

Net cash used in investing

activities for the years ended December 31, 2013 and 2012 was $(551,749) and $0, respectively. The increase in cash used in investing

activities for the year ended December 31, 2013 as compared December 31, 2012, was primarily for computer purchases of $1,749 and

the Company entered into two convertible note purchase agreements with Taida pursuant to which the Company loaned Taida a total

of $550,000.