Table of Contents

As filed with the Securities and Exchange Commission on February 13, 2012

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

EMPIRE STATE REALTY TRUST, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 6798 | 37-1645259 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

One Grand Central Place

60 East 42nd Street

New York, New York 10165

(212) 953-0888

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Anthony E. Malkin

Chairman, Chief Executive Officer and President

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

With copies to:

| Arnold S. Jacobs, Esq. Steven A. Fishman, Esq. Proskauer Rose LLP Eleven Times Square New York, New York 10036 (212) 969-3000 |

Larry P. Medvinsky, Esq. Jason D. Myers, Esq. Clifford Chance US LLP 31 West 52nd Street New York, New York 10019 (212) 878-8000 |

Approximate date of commencement of the proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2)(3) |

Amount of Registration Fee | ||

| Class A Common Stock, par value $.01 per share |

$1,362,135,000 | $156,101 | ||

| Total |

$156,101 | |||

|

| ||||

|

|

|

| ||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o), promulgated under the Securities Act of 1933, as amended. |

| (2) | Represents the maximum aggregate offering price of shares of Class A common stock issuable upon consummation of the transactions described herein assuming the aggregate purchase price equals the aggregate exchange value of such shares. |

| (3) | Represents the shares of Class A common stock that will be issued to participants in the three subject LLCs pursuant to this Registration Statement. Participants also may elect at their option to receive cash, to the extent available, subject to a cap. To the extent cash is paid to certain participants in lieu of Class A common stock, the proposed maximum aggregate offering price of the Class A common stock will be proportionately reduced. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

| Empire State Building Associates L.L.C. |

60 East 42nd St. Associates L.L.C. | 250 West 57th St. Associates L.L.C. |

One Grand Central Place

60 East 42nd Street

New York, New York 10165

NOTICE OF CONSENT SOLICITATION TO PARTICIPANTS

, 2012

Malkin Holdings LLC, the supervisor of each limited liability company listed above, requests that you consent to the following:

Proposed consolidation of your subject LLC into Empire State Realty Trust, Inc. As described in the attached Prospectus/Consent Solicitation Statement, Malkin Holdings LLC, as supervisor, proposes a consolidation of certain office and retail properties in Manhattan and the greater New York metropolitan area owned by Empire State Building Associates L.L.C., 60 East 42nd St. Associates L.L.C. and 250 West 57th St. Associates L.L.C., or the subject LLCs, and certain private entities supervised by the supervisor, and certain related management businesses into Empire State Realty Trust, Inc., or the company. The consolidation is conditioned, among other things, upon the closing of the initial public offering of the company’s Class A common stock. The company will issue to each of the participants in the subject LLCs a specified number of shares of Class A common stock that the company expects to be listed on the New York Stock Exchange or, at each participant’s option, cash for up to [12-15]% of the shares of Class A common stock issuable to a participant, as described herein. After the series of transactions in which the subject LLCs will be consolidated into the company, the company will own, through direct and indirect subsidiaries, the assets of the subject LLCs and the assets of the private entities, along with certain related management businesses. There are 22 private entities involved in the consolidation, including the operating lessees of each of the subject LLCs, from which all required consents to the consolidation have previously been obtained. Attached to the supplement for each subject LLC as Appendix B is the contribution agreement for each subject LLC, which describes the terms of the consolidation in detail. Only the participants holding participation interests in a subject LLC during the consent solicitation period are entitled to notice of, and to vote “FOR” or “AGAINST,” the proposed consolidation. For the reasons the supervisor believes this proposal is fair and reasonable, see “Background of and Reasons for the Consolidation.”

Proposal to authorize the supervisor to sell or contribute the property interests in a third-party portfolio transaction. As a potential alternative to the consolidation, the supervisor requests that the participants consent to the sale or contribution of the subject LLCs’ property interests as part of a sale or contribution of the properties owned by the subject LLCs and the private entities as a portfolio to a third party. The third-party portfolio transaction would be undertaken only if the supervisor determines that the offer price includes what the supervisor believes is an adequate premium above the value that is expected to be realized over time from the consolidation and certain other conditions are met. For the reasons the supervisor believes this proposal is fair and reasonable, see “Third-Party Portfolio Proposal.”

Voluntary pro rata reimbursement program for expenses of legal proceedings with former property manager and leasing agent. In addition, the participants are being asked to consent to a voluntary pro rata reimbursement to the supervisor and Peter L. Malkin for the prior advances of all costs, plus interest, incurred in connection with litigations and arbitrations with the former property manager and leasing agent of the properties owned by the subject LLCs. For the reasons the supervisor believes this proposal is reasonable, see “Voluntary Pro Rata Reimbursement Program for Expenses of Legal Proceedings with Former Property Manager and Leasing Agent.”

The supervisor invites you to vote using the enclosed consent form because it is important that your participation interest in your subject LLC be represented. Please sign, date and return the enclosed consent form in the accompanying postage-paid envelope. You also may revoke your consent to the consolidation, the third-party portfolio proposal, or both, at any time in writing before the later of the date that consents from participants equal

Table of Contents

to the percentage required to approve the consolidation and the third-party portfolio proposal, as applicable, as set forth later in the attached Prospectus/Consent Solicitation Statement are received by your subject LLC and the 60th day after the date of the attached Prospectus/Consent Solicitation Statement.

Malkin Holdings LLC

| By: Peter L. Malkin Chairman |

Anthony E. Malkin President |

The attached Prospectus/Consent Solicitation Statement is dated , 2012 and is being mailed to participants on or about , 2012.

Table of Contents

The information in this Prospectus/Consent Solicitation Statement is not complete and may be changed. A registration statement relating to the securities has been filed with the Securities and Exchange Commission. Empire State Realty Trust, Inc. may not sell the securities offered by this Prospectus/Consent Solicitation Statement until the registration statement filed with the Securities and Exchange Commission becomes effective. This Prospectus/Consent Solicitation Statement is not an offer to sell these securities and Empire State Realty Trust, Inc. is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED FEBRUARY 13, 2012

PROSPECTUS/CONSENT SOLICITATION STATEMENT

shares of Class A common stock, par value $.01 per share

If you are a participant in any of the following subject LLCs, your vote is very important:

| Empire State Building Associates L.L.C. |

60 East 42nd St. Associates L.L.C. |

250 West 57th St. Associates L.L.C. |

Malkin Holdings LLC, the supervisor of three publicly-registered entities, Empire State Building Associates L.L.C., 60 East 42nd St. Associates L.L.C. and 250 West 57th St. Associates L.L.C., or the subject LLCs, requests that you, as a holder of a participation interest in one or more of the subject LLCs, vote on whether to approve the proposed consolidation of the subject LLC in which you are a participant into Empire State Realty Trust, Inc., or the company, as part of a consolidation of office and retail properties in Manhattan and the greater New York metropolitan area owned by the subject LLCs and the private entities supervised by the supervisor, along with certain related management businesses, into the company, as described in more detail herein. Such transaction is referred to herein as the consolidation. The principals of the supervisor include Peter L. Malkin and Anthony E. Malkin.

The supervisor believes you will benefit from this consolidation through newly created opportunities for liquidity, enhanced operating and financing abilities and efficiencies, combined balance sheets, increased growth opportunities, enhanced property diversification, and continued leadership by the principals of the supervisor under the accountability of the governance structure of a reporting company with the U.S. Securities and Exchange Commission, or the SEC, with a board of directors consisting predominantly of independent directors. Anthony E. Malkin will be the only management member of the board of directors.

The supervisor believes that the consolidation is the best way for participants to achieve liquidity and maximize the value of their investment in their subject LLC. Following the consolidation, participants may liquidate their investments and realize current values in cash as and when they desire (subject to the restrictions of the applicable U.S. federal and state securities laws and after expiration of the lock-up period as described in this prospectus/consent solicitation) or may hold shares of Class A common stock they receive in the company in which certain executives of the supervisor will be members of the senior management team and Anthony E. Malkin, an executive and principal of the supervisor, will be Chairman, Chief Executive Officer, President and a director of the company.

The supervisor recommends that you vote “FOR” the consolidation. The Malkin Holdings group, (as defined herein) will receive substantial benefits from the consolidation and have conflicts of interest making this recommendation. See “Conflicts of Interest.”

As a potential alternative to the consolidation, the supervisor also requests that the participants consent to the sale or contribution of the subject LLCs’ property interests as part of a sale or contribution of the properties owned by the subject LLCs and the private entities as a portfolio to an unaffiliated third party. While the supervisor believes the consolidation represents the best opportunity for participants to achieve liquidity and to maximize the value of their investment, the supervisor believes it also is in the best interest of all participants for the supervisor to have the flexibility and discretion, subject to certain conditions, to accept an offer for the portfolio of properties from an unaffiliated third party if the supervisor determines that the offer price includes what the supervisor believes is an adequate premium above the value that is expected to be realized over time from the consolidation.

Table of Contents

The supervisor recommends that you vote “FOR” the third-party portfolio transaction proposal. The Malkin Holdings group will receive substantial benefits from the consolidation and have conflicts of interest making this recommendation. See “Conflicts of Interest.”

Participants also are being asked to consent to a voluntary pro rata reimbursement program pursuant to which the supervisor and Peter L. Malkin, a principal of the supervisor, will be reimbursed for the prior advances of all costs, plus interest, incurred in connection with the legal proceedings required to remove and replace the former property manager and leasing agent. The supervisor believes that the voluntary pro rata reimbursement program is fair and reasonable because the successful resolution of the legal proceedings allowed the properties owned by the subject LLCs and certain of the private entities to participate in a renovation and repositioning turnaround program conceived and implemented by the supervisor. The estate of Leona M. Helmsley, or the Helmsley estate, as part of an agreement with the supervisor covering this and other matters, has paid the voluntary pro rata reimbursement to the supervisor for its pro rata share of costs advanced, plus interest, which totaled $5,021,048.

This solicitation of consents expires at 5:00 p.m., Eastern time on , 2012, unless the supervisor extends the solicitation period for one or more proposals.

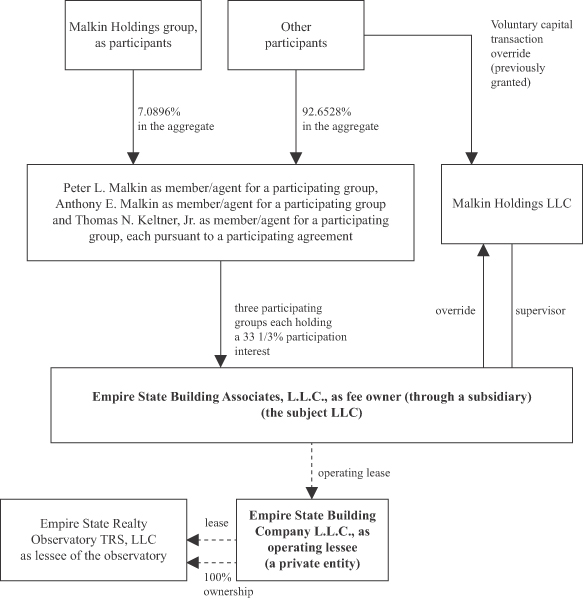

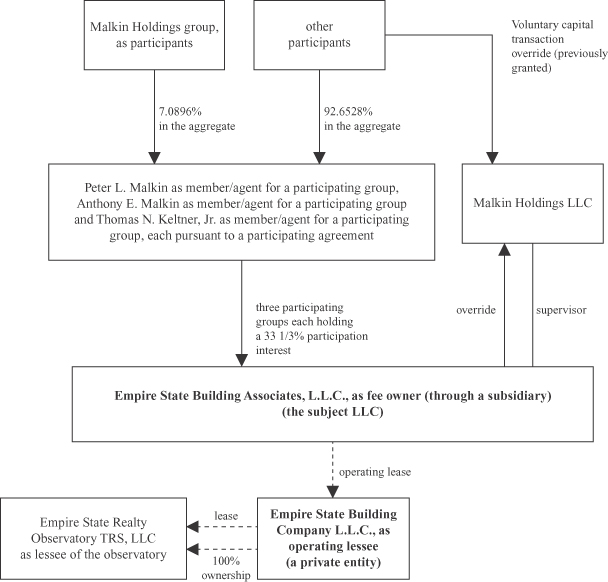

The Wien group, which consists of each of the lineal descendants of Lawrence A. Wien, including Peter L. Malkin and Anthony E. Malkin (including spouses of such descendants), any estates of any of the foregoing, any trusts now or hereafter established for the benefit of any of the foregoing, or any corporation, partnership, limited liability company or other legal entity controlled by Anthony E. Malkin for the benefit of any of the foregoing, collectively owns participation interests in the subject LLCs and has advised that it will vote in favor of the consolidation and the third-party portfolio proposal. These participation interests represent the following percentage ownership for each subject LLC: 8.5921% for Empire State Building Associates L.L.C., 8.7684% for 60 East 42nd St. Associates L.L.C. and 7.3148% for 250 West 57th St. Associates L.L.C.

The supervisor and the Malkin Holdings group receive substantial benefits and from inception have had conflicts of interest in connection with the subject LLCs, including in connection with the consolidation or a third-party portfolio transaction. There are material risks and potential disadvantages associated with the consolidation or a third-party portfolio transaction. The supervisor and the Malkin Holdings group will receive substantial benefits in connection with the consolidation or a third-party portfolio transaction. See “Risk Factors” beginning on page 60 and “Conflicts of Interest” beginning on page 184.

THE SUPERVISOR BELIEVES THAT THE CONSOLIDATION PROVIDES SUBSTANTIAL BENEFITS AND IS FAIR TO THE PARTICIPANTS IN EACH SUBJECT LLC AND RECOMMENDS THAT ALL PARTICIPANTS VOTE “FOR” THE CONSOLIDATION. SEE “BACKGROUND OF AND REASONS FOR THE CONSOLIDATION—THE SUPERVISOR’S REASONS FOR PROPOSING THE CONSOLIDATION.”

THE SUPERVISOR BELIEVES IT IS IN THE BEST INTERESTS OF THE PARTICIPANTS TO PROVIDE THE SUPERVISOR WITH THE AUTHORITY TO APPROVE A THIRD-PARTY PORTFOLIO TRANSACTION AS AN ALTERNATIVE TO THE CONSOLIDATION AND RECOMMENDS THAT ALL PARTICIPANTS VOTE “FOR” THE THIRD-PARTY PORTFOLIO PROPOSAL. SEE “THIRD PARTY PORTFOLIO PROPOSAL” FOR THE SUPERVISOR’S REASONS FOR RECOMMENDING APPROVAL OF THE PROPOSAL.

THE SUPERVISOR BELIEVES THAT THE VOLUNTARY PRO RATA REIMBURSEMENT PROGRAM IS FAIR AND REASONABLE AND RECOMMENDS THAT ALL PARTICIPANTS WHO HAVE NOT PREVIOUSLY CONSENTED TO THE VOLUNTARY PRO RATA REIMBURSEMENT PROGRAM “CONSENT TO” THE PROPOSAL. SEE “VOLUNTARY PRO RATA REIMBURSEMENT PROGRAM FOR EXPENSES OF LEGAL PROCEEDINGS WITH FORMER PROPERTY MANAGER AND LEASING AGENT” FOR A DISCUSSION OF THE SUPERVISOR’S REASONS FOR RECOMMENDING APPROVAL OF THE PROPOSAL AND THE BENEFITS TO THE SUPERVISOR.

Table of Contents

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Class A common stock or passed upon the accuracy or adequacy of this Prospectus/Consent Solicitation Statement. Any representation to the contrary is a criminal offense.

After you read this Prospectus/Consent Solicitation Statement, the company and the supervisor urge you to read the accompanying supplement for your subject LLC. The supplement contains information particular to your subject LLC. This information is material in your decision whether to vote “FOR” or “AGAINST” the consolidation.

THIS PROSPECTUS/CONSENT SOLICITATION IS AUTHORIZED FOR DELIVERY TO PARTICIPANTS ONLY WHEN ACCOMPANIED BY ONE OR MORE SUPPLEMENTS RELATING TO THE SUBJECT LLCS IN WHICH SUCH PARTICIPANTS HOLD PARTICIPATION INTERESTS. SEE “WHERE YOU CAN FIND MORE INFORMATION.”

WHO CAN HELP ANSWER YOUR QUESTIONS?

If you have more questions about the proposed consolidation or would like additional copies of this Prospectus/Consent Solicitation Statement or the supplement relating to your subject LLC(s) (which will be provided at no cost), you should contact the person designated on the consent form sent to you.

To obtain timely delivery, you should request this information no later than , 2012.

The date of this Prospectus/Consent Solicitation Statement is , 2012.

Table of Contents

i

Table of Contents

ii

Table of Contents

iii

Table of Contents

iv

Table of Contents

EXPLANATORY NOTE: The information concerning the appraisal by Duff & Phelps LLC, the independent valuer, contained in this Registration Statement on Form S-4 is based on the preliminary appraisal by the independent valuer as of July 1, 2011 and the information concerning the fairness opinion of Duff & Phelps LLC is based on the draft form of fairness opinion provided by the independent valuer. The valuation will be updated as of a date in closer proximity to the effective date of this Registration Statement on Form S-4, and the fairness opinion is expected to be delivered as of a date in closer proximity to such effective date.

v

Table of Contents

IMPORTANT NOTICE: The contents of this Prospectus/Consent Solicitation Statement were not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding U.S. federal income tax penalties that may be imposed on the taxpayer. The following was written to support the promotion or marketing of the transactions addressed by this prospectus/consent solicitation. Each taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

The company uses market data and industry forecasts and projections throughout this Prospectus/Consent Solicitation Statement, and in particular in the section entitled “Business of the Subject LLCs.” The company has obtained substantially all of this information from a market study prepared for the company by Rosen Consulting Group, or RCG, a nationally recognized real estate consulting firm in January 2012. The company has paid RCG a fee for such services. Such information is included herein in reliance on RCG’s authority as an expert on such matters. See “Experts.” In addition, the company has obtained certain market data from publicly available information and industry publications. These sources generally state that the information they provide has been obtained from sources believed to be reliable. Forecasts are based on industry surveys and the preparer’s expertise in the industry and there is no assurance that any of the projected amounts will be achieved. The company believes this data others have compiled are reliable, but it has not independently verified this information. Any forecasts prepared by RCG are based on data (including third party data), models and experience of various professionals, and are based on various assumptions, all of which are subject to change without notice.

The term “greater New York metropolitan area” is used herein to refer only to Fairfield County, Connecticut and Westchester County, New York. The manner in which the company defines its property markets and submarkets differs from how RCG has done so in its market study included herein. Further, RCG’s definition of the New York metropolitan area differs from the company’s definition of the greater New York metropolitan area. RCG’s definition includes Putnam County and Rockland County in New York and Bergen County, Hudson County, and Passaic County in Northern New Jersey and excludes Fairfield County in Connecticut.

Unless the context otherwise requires or indicates, references in this Prospectus/Consent Solicitation Statement, which is referred to herein as the prospectus/consent solicitation, to:

| (i) | the subject LLCs refers to Empire State Building Associates L.L.C., 60 East 42nd St. Associates L.L.C. and 250 West 57th St. Associates L.L.C., |

| (ii) | the private entities refer to the privately-held entities supervised by the supervisor, which are all of the entities, other than the subject LLCs, listed in the chart under the section “Summary—The Subject LLCs, the Private Entities and the Management Companies,” which will be included in the consolidation, |

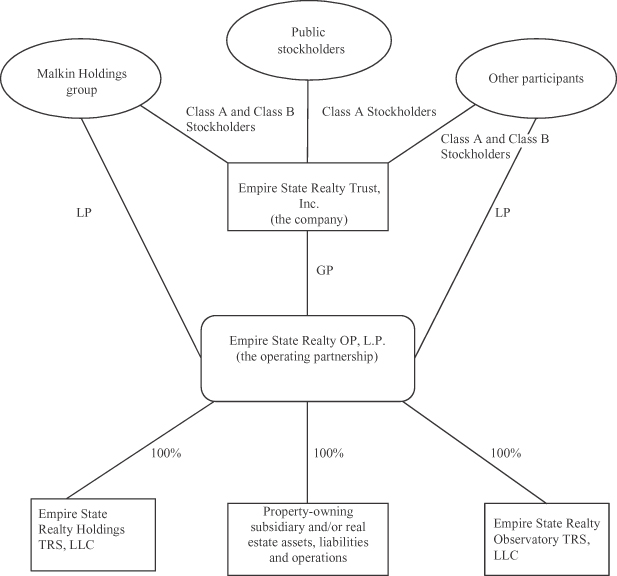

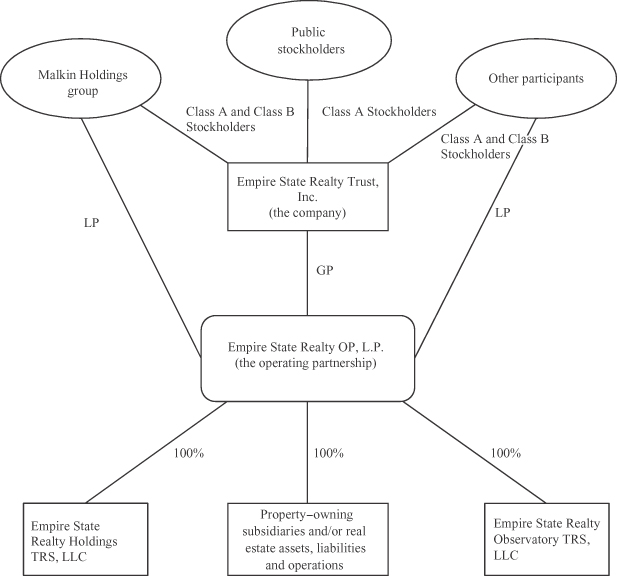

| (iii) | the company refers to Empire State Realty Trust, Inc. (formerly known as Empire Realty Trust, Inc.), a Maryland corporation, together with its consolidated subsidiaries, including Empire State Realty OP, L.P. (formerly known as Empire Realty Trust, L.P.), a Delaware limited partnership, which is referred to herein as the operating partnership, after giving effect to the series of transactions involving the consolidation of the subject LLCs and the private entities described in this prospectus/consent solicitation that have consented to the consolidation and a combination of (a) Malkin Holdings LLC, a New York limited liability company that acts as the supervisor of, and performs various asset management services and routine administration with respect to, the subject LLCs and certain of the private entities (as discussed in this prospectus/consent solicitation), which is referred to herein as the supervisor; (b) Malkin Properties, L.L.C., a New York limited liability company that serves as the manager and leasing agent to certain of the private entities in Manhattan, (c) Malkin Properties of New York, L.L.C., a New York limited liability company that serves as the manager and leasing agent to certain of the private entities located in Westchester County, New York, (d) Malkin Properties of |

vi

Table of Contents

| Connecticut, Inc. a Connecticut corporation that serves as the manager and leasing agent to certain of the private entities in the State of Connecticut and (e) Malkin Construction Corp., a Connecticut corporation that is a general contractor and provides services to the private entities and third parties (including certain tenants at the properties owned by the private entities), which collectively are referred to herein as the management companies, |

| (iv) | the properties refers to the subject LLCs’ direct or indirect fee ownership interests in the Empire State Building, One Grand Central Place and 250 West 57th Street, respectively, |

| (v) | the properties of the company and the portfolio refer to the properties, the other assets of the subject LLCs, the ownership interests of the private entities in their properties and the other assets of the private entities, |

| (vi) | the agents refer to holders of the membership interests in the subject LLCs for the benefit of participants in the agent’s participating group; each of the agents is an affiliate of the supervisor, |

| (vii) | the participants refer to the holders of participation interests in the membership interests held by the agents and, as applicable, investors in the private entities, |

| (viii) | the participation interests refer to the beneficial ownership interests of participants in the membership interest of the subject LLCs held by an agent for the benefit of participants and, as applicable, membership or partnership interests or the beneficial interests therein held by investors in the private entities, |

| (ix) | common stock and shares of common stock refer to both shares of the company’s Class A common stock, par value $0.01, and Class B common stock, par value $0.01 per share, unless otherwise indicated, |

| (x) | the IPO refers to the initial public offering of the Class A common stock of the company, and IPO price refers to the price per share of Class A common stock in the IPO, |

| (xi) | operating partnership units refer to the operating partnership’s limited partnership interests, and |

| (xii) | organizational documents refer to the limited liability company agreement, the participation agreements and the terms of any voluntary capital transaction override program and voluntary pro rata reimbursement programs for each subject LLC, to the extent applicable. |

All references to the enterprise value refer to the value of the company after completion of the consolidation determined in connection with the IPO by the company in consultation with the investment banking firms managing the IPO and prior to the issuance of Class A common stock in the IPO and any issuance of Class A common stock pursuant to equity incentive plans.

All references to the aggregate exchange value refer to the aggregate exchange value of the subject LLCs, the private entities and the management companies based on the appraisal by Duff & Phelps, LLC, the independent valuer.

All references (other than information labeled as pro forma information, including the pro forma financial statements) to the number of shares of common stock, on a fully-diluted basis, issued in the consolidation refer to the number of shares of Class A common stock and Class B common stock issued or received in the consolidation, prior to the issuance of Class A common stock in the IPO and pursuant to any incentive plans, assuming that (i) the enterprise value in connection with the IPO equals the aggregate exchange value, (ii) the offering price per share in the IPO used herein which is used solely for illustrative purposes equals a hypothetical $10 per share, (iii) all of the subject LLCs, the private entities and the management companies participate in the consolidation, (iv) no cash is paid to the participants in the subject LLCs, the private entities or the management companies in the consolidation, (v) no shares of Class A common stock are issued to the supervisor pursuant to the voluntary pro rata reimbursement program, (vi) no fractional shares are issued and (vii) all operating partnership units issued in the consolidation are redeemed on a one-for-one basis and all shares of Class B common stock issued in the consolidation are converted on a one-for one basis for shares of Class A common stock.

vii

Table of Contents

The enterprise value will be determined by the market conditions and the performance of the portfolio at the time of the IPO. The enterprise value may be higher or lower than the aggregate exchange value. The aggregate exchange value used herein is based on the appraisal prepared by the independent valuer. Historically, in a typical initial public offering of a REIT, the enterprise value and initial public offering price are at a discount to the net asset value of the REIT’s portfolio of properties, which in turn may be above or below the aggregate exchange value.

All references to distributions to participants assume that all amounts payable under the voluntary pro rata reimbursement program are paid out of cash distributions from the subject LLCs and the private entities, as applicable and that no shares of Class A common stock are issued to the supervisor for amounts due under the voluntary pro rata reimbursement program.

The supervisor has made certain of these assumptions to permit the presentation of information in tables in this prospectus/consent solicitation on a consistent basis. For example, while throughout this prospectus/consent solicitation the supervisor has assumed for purposes of this presentation of information that no cash is paid, cash will be paid to non-accredited investors in the private entities and to participants in the subject LLCs and to certain investors in the private entities that are charitable organizations and exempt from New York City real property transfer tax and elect to receive cash pursuant to the cash option described herein.

All references to the stockholders refer to the holders of Class A common stock and Class B common stock of the company.

All references to the Malkin Family refer to Anthony E. Malkin, Peter L. Malkin, each of their lineal descendants (including spouses of any of the foregoing), any estates of any of the foregoing, any trusts now or hereafter established for the benefit of any of the foregoing, or any corporation, partnership, limited liability company or other legal entity controlled by Anthony E. Malkin for the benefit of any of the foregoing.

All references to the Malkin Holdings group refer to the Malkin Family and Thomas N. Keltner, Jr., and his spouse.

All references to the Wien group refer to each of the lineal descendants of Lawrence A. Wien, including Peter L. Malkin and Anthony E. Malkin (including spouses of such descendants), any estates of any of the foregoing, any trusts now or hereafter established for the benefit of any of the foregoing, or any corporation, partnership, limited liability company or other legal entity controlled by Anthony E. Malkin for the benefit of any of the foregoing.

For demonstrative purposes, the supervisor has assigned a hypothetical IPO offering price of $10 per share. That value is strictly hypothetical and is for illustrative purposes only.

All references to the property and assets owned by the company upon completion of the consolidation refer to the company upon completion of the consolidation, without giving effect to the IPO, and assuming that all required consents of the participants in the subject LLCs have been obtained and all of the properties and assets to be acquired from the subject LLCs, the private entities and the management companies pursuant to the consolidation have been acquired.

All references to a third-party portfolio transaction refer to the sale or contribution of the subject LLCs’ property interests and other assets as part of a sale or contribution of the properties owned by the subject LLCs and the private entities as a portfolio to a third party. The description of the company in this prospectus/consent solicitation assumes that all of the properties and assets to be acquired from the subject LLCs, the private entities and the management companies pursuant to the consolidation have been acquired by the company rather than a third party pursuant to a third-party portfolio transaction.

Certain terms and provisions of various agreements are summarized in this prospectus/consent solicitation. These summaries are qualified in their entirety by reference to the complete text of any such agreements, which

viii

Table of Contents

are either attached as exhibits or appendices to this prospectus/consent solicitation or the supplement for your subject LLC in the form in which they are expected to be signed (but subject to change, including potentially significant changes, as described below) or filed as an exhibit to the Registration Statement on Form S-4 of which this prospectus/consent solicitation is a part. The parties to such agreements may make changes (including changes that may be deemed material) to the forms of the agreements attached as appendices or exhibits hereto, contained in the applicable supplement or filed as exhibits to the Registration Statement on Form S-4.

ix

Table of Contents

THE CONSOLIDATION

| Q: | What am I being asked to approve? |

A: The supervisor, which is an affiliate of Peter L. Malkin and Anthony E. Malkin, is submitting the following proposals for your approval:

| • | A consolidation of your subject LLC and certain office and retail properties in Manhattan and the greater New York metropolitan area owned by the subject LLCs and the private entities, all of which are supervised by the supervisor, and certain related management businesses, into the company, which is intended to qualify for taxation as a real estate investment trust for U.S. federal income tax purposes, which is referred to herein as a REIT. |

| • | As a potential alternative to the consolidation, the sale or contribution of the subject LLCs’ property interests as part of a sale or contribution of the properties owned by the subject LLCs and the private entities as a portfolio to a third party if the supervisor determines that the offer price includes what the supervisor believes is an adequate premium above the value that is expected to be realized over time from the consolidation and certain other conditions are met. |

| • | Voluntary pro rata reimbursement to the supervisor and Peter L. Malkin for the prior advances of all costs, plus interest, incurred in connection with litigations and arbitrations with the former property manager and leasing agent of the property. |

Each of these proposals is subject to a separate consent, and approval of each proposal is not dependent on approval of any other proposal.

| Q: | Who is the supervisor? |

A: The supervisor of the subject LLCs, Malkin Holdings LLC, provides asset management services for, and supervises the operations of, the subject LLCs. Anthony E. Malkin and Peter L. Malkin are principals of the supervisor. The supervisor also provides similar services to the private entities, including the private entities that hold operating lease interests in the properties owned by the subject LLCs.

| Q: | Why is the supervisor proposing the consolidation? |

A: The supervisor believes this transaction represents the logical next step of value creation after years of action under the supervisor’s leadership to preserve, restore, and enhance your investment in the subject LLC. Included in that history is a challenging time, which began with litigation commenced in 1997 by Peter L. Malkin and the supervisor to remove Helmsley-Spear, Inc., which is referred to herein as the former property manager and leasing agent (after it was sold by entities controlled by Leona M. Helmsley) as property manager and leasing agent of the properties owned by the subject LLCs and other properties which are now included in the plans for this consolidation.

Since the successful resolution of that litigation, the supervisor has overseen the engagement by the subject LLCs of independent property management and leasing agents and the transformation of the Empire State Building to a self management structure, retaining a third party agent for leasing only; developed and is in the process of effecting a comprehensive renovation and repositioning program for improving the physical condition of and upgrading the credit quality of tenants at the property, and raised the properties’ profile as part of a well regarded portfolio brand. The supervisor believes that it is an opportune time for the subject LLCs to take advantage of the opportunity to participate in the consolidation which will afford participants administrative and operating efficiencies, as well as better value protection through diversification.

Additionally, the supervisor believes the consolidation provides value enhancement through better access to capital and options for liquidity for investors who so desire.

1

Table of Contents

The supervisor has reviewed this transaction carefully and believes that current and anticipated property results provide favorable prospects for the consolidation. The supervisor will consider the capital market conditions at the time the IPO is ready to commence, but the supervisor is confident that a well located, well run, well capitalized portfolio of office and retail properties in Manhattan and in the greater New York metropolitan area is a desirable portfolio for an IPO. The consolidation and IPO will launch the company as a public company with its Class A common stock expected to be listed on the New York Stock Exchange, which is referred to herein as the NYSE, upon completion of the IPO.

The supervisor believes that the consolidation is the best way for participants to achieve liquidity and to maximize the value of their investment in the subject LLCs. The supervisor believes that benefits to participants from the consolidation include:

| • | Liquidity for participants that elect to receive shares of Class A common stock expected to be listed on the NYSE, which investors may sell from time to time as and when they so desire (subject to the restrictions of applicable U.S. federal and state securities laws and after expiration of the lock-up period as described in this prospectus/consent solicitation). Presently there is no active trading market for the participation interest you hold in your subject LLC, which is only an indirect interest in real property subject to an operating lease, which is not under the operational control of your subject LLC; |

| • | Anticipated regular quarterly cash distributions on their shares of Class A common stock, which will include distributions of at least 90% of the company’s annual net taxable income, determined without regard to the deduction for dividends paid and excluding any net capital gains, which is required for REIT qualification as described below; |

| • | Conversion of the current governance structure which is inefficient and costly in general and in which participants do not share in the same economic benefit that they would receive through ownership and operation of the properties by a single entity into a modern, centralized and efficient governance structure; |

| • | The opportunity to continue to hold interests in an entity operating under the brand developed by the supervisor and to participate in any future growth of the company, while removing obstacles to obtaining true synergies and realization of value, such as combining financings, movements of tenants from one building to another, sharing of employees and management and oversight; |

| • | Anticipated value enhancement through operating and capital structure efficiencies and the benefit of property diversification; |

| • | The opportunity to continue to hold interests in an entity in which certain executives of the supervisor will be members of the senior management team and Anthony E. Malkin will be Chairman, Chief Executive Officer, President and a director of the company; |

| • | The governance structure of an SEC reporting company with its Class A common stock expected to be listed on the NYSE, which provides accountability through the oversight of the company by a board of directors consisting predominantly of independent directors and |

| • | Immediate liquidity for those participants that receive cash upon exercise of the cash option. |

| Q: | What is the proposed consolidation upon which I am being asked to vote? |

A: You are being requested to approve the consolidation in which your subject LLC will contribute its assets to the operating partnership in exchange for Class A common stock of the company and/or cash. All of the subject LLCs together represent 41.5% of the aggregate exchange value. As part of the consolidation, the company also will enter into similar transactions with the other subject LLCs, private entities and the management companies described elsewhere in this prospectus/consent solicitation.

Through the consolidation, the company intends to combine the properties of the subject LLCs and the private entities and the assets and operations of the supervisor and the other management companies into the

2

Table of Contents

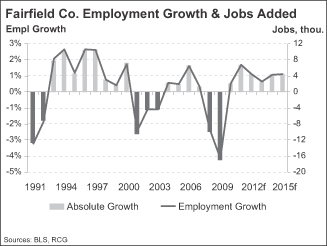

company, and intends to elect and to qualify as a REIT for U.S. federal income tax purposes. The closing of the consolidation will occur simultaneously with the closing of an IPO of the company’s Class A common stock. If the consolidation is approved by the three subject LLCs, the company acquires the properties from each of private entities and the company acquires the management companies, the company will own 12 office properties which, as of September 30, 2011, encompass approximately 7.7 million rentable square feet of office space, and which were approximately 79.9% leased as of September 30, 2011 (or 83.0% giving effect to leases signed but not yet commenced as of that date). Seven of these properties are located in the midtown Manhattan market and encompass in the aggregate approximately 5.8 million rentable square feet of office space, including the Empire State Building, the world’s most famous office building. The Manhattan office properties also contain an aggregate of 432,176 rentable square feet of premier retail space on the ground floor and/or lower levels. The remaining five office properties are located in Fairfield County, Connecticut and Westchester County, New York, encompassing approximately 1.8 million rentable square feet in the aggregate. The majority of the square footage for these five properties is located in densely populated metropolitan communities with immediate access to mass transportation. Additionally, the company has entitled land at the Stamford Transportation Center in Stamford, Connecticut, adjacent to one of its office properties, that will support the development of an approximately 340,000 rentable square foot office building and garage. As of September 30, 2011, the portfolio also included four standalone retail properties located in Manhattan and two standalone retail properties located in the city center of Westport, Connecticut, encompassing 204,452 rentable square feet in the aggregate. As of September 30, 2011, the standalone retail properties were approximately 96.8% leased in the aggregate (or 96.8% giving effect to leases signed but not yet commenced as of that date).

The consolidation offers participants the opportunity to become stockholders of the company, which will have as senior management certain executives of the supervisor, a recognized operator of office and retail properties in Manhattan and the greater New York metropolitan area. The supervisor has a comprehensive knowledge of its markets that has been developed through the supervisor’s principals’ substantial experience. The consolidation also will result in the creation of a company with a board of directors consisting predominantly of independent directors, which will be responsible for overseeing the operations of the company. Anthony E. Malkin will be the only management member of the board of directors.

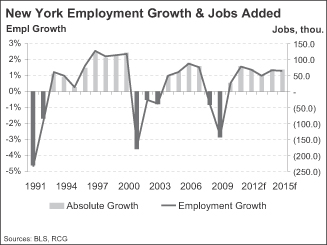

All of the properties are located in Manhattan and the greater New York metropolitan area, which, according to RCG, is one of the most-prized office markets in the world and a world-renowned retail market due to a combination of supply constraints, high barriers to entry, near-term and long-term prospects for job creation, vacancy absorption and rental rate growth. The supervisor believes that the company will represent a unique opportunity to invest in a well-capitalized company with real estate in these most-prized markets and recognized and respected leadership. The company’s primary focus will be to continue to own, operate and manage its current portfolio and to acquire and reposition office and retail properties in Manhattan and the greater New York metropolitan area.

| Q: | Has the company received consents from the private entities and the management companies for the consolidation? |

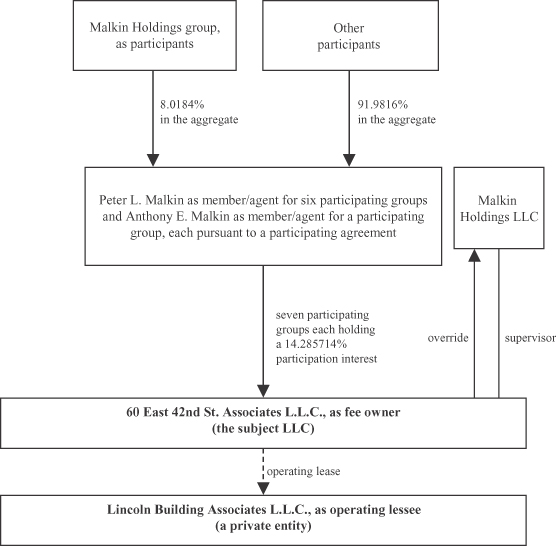

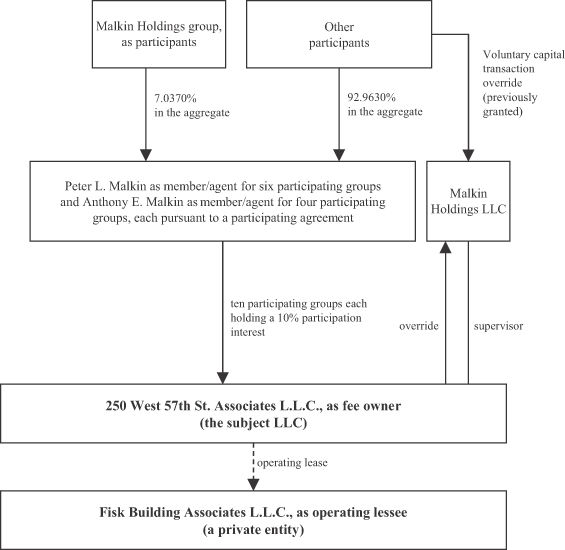

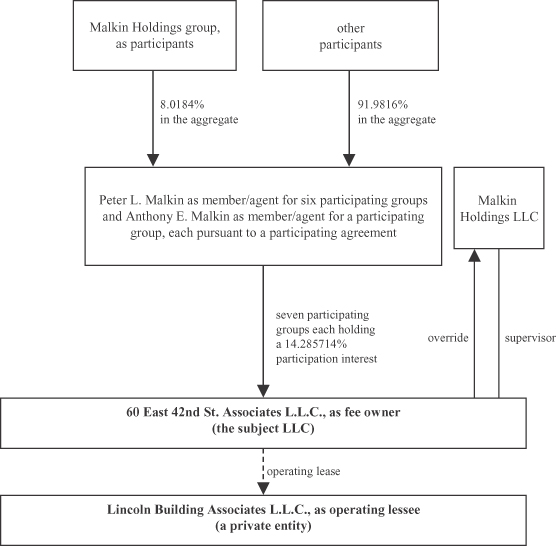

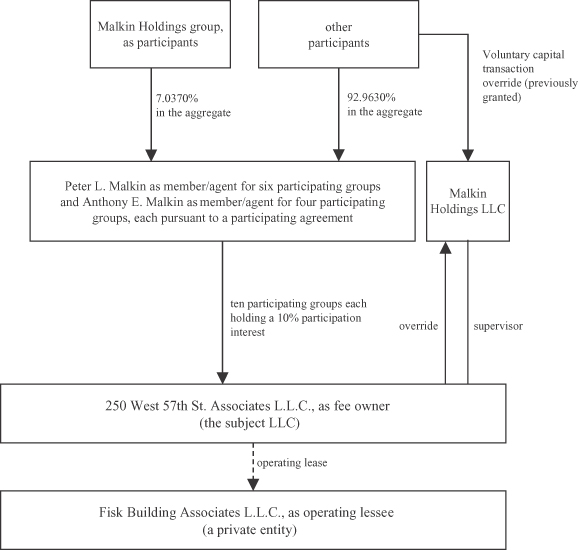

A: All required consents of the private entities and the management companies, including the consents of the Wien group and the interests of the estate of Leona M. Helmsley (which is referred to herein as the Helmsley estate), to the acquisition by the company of the assets of the private entities and the management companies have been obtained prior to the date of this prospectus/consent solicitation. In addition, the Wien group collectively owns participation interests in the subject LLCs and has advised that it will vote in favor of the consolidation and the third-party portfolio proposal. These participation interests represent the following percentage ownership for each subject LLC: 8.5921% for Empire State Building Associates L.L.C., 8.7684% for 60 East 42nd St. Associates L.L.C. and 7.3148% for 250 West 57th St. Associates L.L.C.

3

Table of Contents

| Q: | What are the conditions for the consolidation to close? |

A: The following conditions must be satisfied to consummate the consolidation of the subject LLC: (i) requisite consent of the participants in the subject LLC must have been received; (ii) the closing of the IPO and the listing of the Class A common stock on the NYSE or another national securities exchange; (iii) the closing of the consolidation no later than December 31, 2014; (iv) the participation of Empire State Building Associates L.L.C. and the private entity which owns an interest in the Empire State Building participating in the consolidation and (v) other customary conditions. The consolidation is not conditioned on any of the other subject LLCs or private entities participating in the consolidation.

| Q: | What will I be entitled to receive if I vote “FOR” the consolidation and either proposal is approved by my subject LLC? |

A: If you vote “FOR” the consolidation and your subject LLC participates in the consolidation, you will receive shares of Class A common stock in exchange for the participation interest that you own in your subject LLC.

| Q: | What will I be entitled to receive if I don’t vote “FOR” the consolidation and either proposal is approved by my subject LLC? |

A: If you vote “AGAINST” the consolidation, you do not vote or you “ABSTAIN,” and your subject LLC participates in the consolidation, if you are a participant in 250 West 57th St. Associates L.L.C., you will receive shares of Class A common stock, and, as set forth under the section entitled “Summary—Voting Procedures for the Consolidation Proposal and the Third-Party Portfolio Proposal”, if you are a participant in Empire State Building Associates L.L.C. and 60 East 42nd St. Associates L.L.C., your participation interests will be subject to a buyout pursuant to the subject LLC’s organizational documents. The buyout amount would be substantially lower than the exchange value. These buyout amounts are $100 for the interest held by a participant in Empire State Building Associates L.L.C. and $100 for the interest held by a participant in 60 East 42nd St. Associates L.L.C., as compared to the exchange value of $33,085 per $1,000 original investment for Empire State Building Associates L.L.C. and $38,972 per $1,000 original investment for 60 East 42nd St. Associates L.L.C., respectively. Prior to an agent purchasing the participation interests of non-consenting participants for the benefit of the applicable subject LLC, the agent will give such participants not less than ten days’ notice after the required consent is received by a subject LLC to permit them to consent to the consolidation or the third-party portfolio proposal, as applicable, in which case their participation interests will not be purchased.

| Q: | If my subject LLC consolidates with the company, may I choose to receive something other than shares of Class A common stock? |

A: Yes, you will have the option to receive cash (at a price per share equal to the IPO price reduced by the underwriting discount per share paid by the company in the IPO) for up to [12-15] % of the shares of Class A common stock issuable to you in the consolidation, by electing a cash option in the consent form accompanying this prospectus/consent solicitation. This election is referred to herein as the cash option. The cash option provides those participants that wish to receive cash the ability to have immediate liquidity. Participants in the subject LLCs are being provided with the option to enable them to receive cash to cover a portion of U.S. federal income taxes payable in connection with the shares of Class A common stock issued to them in the consolidation. The cash option is limited to [12-15] % to assist the company in meeting the conditions for obtaining the reduced New York City and New York State transfer tax rate applicable to REITs, which the supervisor believes may be available with respect to a portion of the consolidation transfers, depending on the circumstances of the consolidation and certain events following the consolidation.

4

Table of Contents

| Q: | How was the value of my participation interest determined? |

A: The value of your participation interest, as described in this prospectus/consent solicitation, was determined based on the exchange value for your subject LLC. The exchange value of your subject LLC and the other subject LLCs, the private entities and the management companies is the value of each of and all these entities based on the appraisal by Duff & Phelps, LLC, which is referred to herein as Duff & Phelps or the independent valuer, which serves as the independent valuer for all the subject LLCs, the private entities and the management companies. Shares of common stock, operating partnership units and/or cash, as applicable, will be allocated among the subject LLCs, the private entities and the management companies based upon the exchange values of each subject LLC, each private entity and the management companies. The exchange value was then allocated among the participants and the holders of the override interests by the independent valuer in accordance with each subject LLC’s organizational documents. However, as described elsewhere in this prospectus/consent solicitation, while the exchange value was used to establish the relative value of the properties and participation interests, this value does not necessarily represent the fair market value of your participation interest.

The fair market value of the consideration that you receive will not be known until the pricing of the IPO. The value of the consideration will be based on the enterprise value determined in connection with pricing of the IPO. The enterprise value will be determined by the market conditions and the performance of the portfolio at the time of the IPO. The enterprise value may be higher or lower than the aggregate exchange value. The exchange value used herein is based on the appraisal prepared by the independent valuer. Historically, in a typical initial public offering of a REIT, the enterprise value and initial public offering price are at a discount to the net asset value of the REIT’s portfolio of properties, which in turn may be above or below the aggregate exchange value.

| Q: | How many shares of Class A common stock will I be entitled to receive if my subject LLC is consolidated with the company? |

A: The number of shares of Class A common stock that will be allocated to each subject LLC in the consolidation based on the exchange value is set forth in the chart under the caption “Summary—The Consolidation—Allocation of Common Stock.” You will receive a portion of the Class A common stock allocated to your subject LLC in accordance with your percentage interest in the subject LLC and the subject LLC’s organizational documents. The number of shares of Class A common stock presented in this prospectus/consent solicitation is based on the hypothetical $10 per share exchange value arbitrarily assigned by the supervisor to illustrate the number of shares of Class A common stock that a participant would receive if the enterprise value of the company determined in connection with the IPO were the same as the aggregate exchange value and the IPO price were $10 per share. The actual number of shares of common stock, on a fully-diluted basis, issued in the consolidation will equal the enterprise value divided by the actual IPO price upon pricing of the IPO. The enterprise value will be determined by the market conditions and the performance of the portfolio at the time of the IPO. The enterprise value may be higher or lower than the aggregate exchange value. The exchange value used herein is based on the appraisal prepared by the independent valuer. Historically, in a typical initial public offering of a REIT, the enterprise value and initial public offering price are at a discount to the net asset value of the REIT’s portfolio of properties, which in turn may be above or below the aggregate exchange value.

| Q: | What are the rights of holders of Class A common stock and Class B common stock? |

A: Each share of Class A common stock will entitle the holder to one vote, and each outstanding share of Class B common stock will entitle the holder to 50 votes on each matter on which holders of Class A common stock are entitled to vote, including the election of directors, and the holders of shares of Class A common stock and Class B common stock will vote together as a single class. Subject to the provisions of the company’s charter regarding the restrictions on ownership and transfer of the company’s stock, shares of Class A common stock and Class B common stock will have equal dividend, liquidation and other rights.

5

Table of Contents

Accredited investors in the private entities and the management companies which had an option to elect operating partnership units at the time that they made their election of consideration in the private solicitation had an option to elect to receive one share of Class B common stock in lieu of one operating partnership unit for every 50 non-voting operating partnership units such participant would otherwise receive in the consolidation.

| Q: | Why am I being asked to consent to a third-party portfolio proposal? |

A: As a potential alternative to the consolidation, you also are being asked to consent to the sale or contribution of the subject LLC’s property interest as part of a sale or contribution of the properties owned by the subject LLCs and the private entities as a portfolio to a third party. Through solicitation of consents, for the first time the properties owned by the subject LLCs and the private entities can be joined as a single portfolio. While the supervisor believes the consolidation and IPO represent the best opportunity for participants in the subject LLCs and the private entities to achieve liquidity and to maximize the value of their respective investments, the supervisor also believes it is in the best interest of all participants for the supervisor to be able to approve offers from unaffiliated third parties for the portfolio as a whole.

Market forces are dynamic, unpredictable, and subject to volatility. Should the public awareness of the proposed consolidation and IPO produce potential compelling offers from unaffiliated third parties to purchase the consolidated portfolio, it will be costly and time consuming to solicit consents to allow a sale or contribution of the portfolio to a third party, and there is considerable risk that any opportunity which might appear would be lost without the requested consent in place. Therefore, the supervisor believes that it is advisable to have the flexibility and discretion, subject to certain conditions, to accept an offer for the entire portfolio of properties from an unaffiliated third party, rather than pursue the consolidation and IPO, if the supervisor determines the offer price includes what the supervisor believes is an adequate premium above the value that is expected to be realized over time from the consolidation. The supervisor has agreed that it will not accept a third-party offer unless it is unanimously approved by a committee which will include representatives of the supervisor and a representative of the Helmsley estate. Any third-party interested in making a portfolio proposal will be instructed to make its offer for all cash. It is possible that participants or the supervisor and its affiliates may be offered an option to receive securities in lieu of all or a portion of the cash. The supervisor will be authorized to approve offers only if definitive agreements are entered into prior to December 31, 2015 or such earlier date as the supervisor may set with or without notice or public announcement.

| Q: | What will I be entitled to receive if I don’t vote “FOR” the third-party portfolio proposal and it is approved by my subject LLC? |

A: If you vote “AGAINST” the third-party portfolio proposal, you do not vote or you “ABSTAIN,” and your subject LLC participates in the third-party portfolio proposal, if you are a participant in 250 West 57th St. Associates L.L.C. you will receive the same consideration as other participants and, as set forth under the section entitled “Summary—Voting Procedures for the Consolidation Proposal and the Third-Party Portfolio Proposal”, if you are a participant in Empire State Building Associates L.L.C. and 60 East 42nd St. Associates L.L.C., your participation interests will be subject to a buyout pursuant to the subject LLC’s organizational documents. The buyout amount would be substantially lower than the exchange value in connection with the allocation of consideration in the consolidation. These buyout amounts are $100 for the interest held by a participant in Empire State Building Associates L.L.C. and $100 for the interest held by a participant in 60 East 42nd St. Associates L.L.C., as compared to the exchange value of $33,085 per $1,000 original investment for Empire State Building Associates L.L.C. and $38,972 per $1,000 original investment for 60 East 42nd St. Associates L.L.C., respectively. Prior to an agent purchasing the participation interests of non-consenting participants for the benefit of the applicable subject LLC, the agent will give such participants not less than ten days’ notice after the required consent is received by a subject LLC to permit them to consent to the consolidation or the third-party portfolio proposal, as applicable, in which case their participation interests will not be purchased.

6

Table of Contents

| Q: | Why am I being asked to consent to a voluntary pro rata reimbursement program? |

A: You are being asked to consent to a voluntary pro rata reimbursement program pursuant to which the supervisor and Peter L. Malkin, a principal of the supervisor, will be reimbursed for the prior advances of all costs, plus interest, incurred in connection with the legal proceedings with Helmsley-Spear, Inc., the former property manager and leasing agent, which resulted in the removal of the former property manager and leasing agent as property manager and leasing agent of the properties owned by the subject LLCs and certain of the private entities and has enabled a renovation and repositioning turnaround program to be implemented by the supervisor. If you consent to the voluntary pro rata reimbursement program, the supervisor and Peter L. Malkin will be reimbursed for your pro rata share of costs, plus interest, previously incurred out of your share of the excess cash of your subject LLC that is being distributed to participants, and, to the extent that is insufficient, the shares of Class A common stock that you would receive in the consolidation or the consideration that you would receive in a third-party portfolio transaction, as applicable, will be reduced by the balance (valued, if the consolidation is consummated, at the IPO price) and such balance would be paid to the supervisor and Peter L. Malkin in shares of Class A common stock, if the consolidation is consummated, or out of distributions that you would receive from the proceeds of a third-party portfolio transaction, if consummated, or out of distributions from operations of the subject LLC.

The table below shows the amount to be received by the supervisor out of the distributions of each consenting participant for each $1,000 of original investment by a participant pursuant to the voluntary pro rata reimbursement program:

| Exchange Value of Shares of Common Stock to be Received by Participants per $1,000 Original Investment |

Voluntary Reimbursement | |||||||||||

| Per $1,000 Original Investment |

Total | |||||||||||

| Empire State Building Associates L.L.C. |

$ | 33,085 | $ | 101 | $ | 3,329,234 | ||||||

| 60 East 42nd St. Associates L.L.C. |

$ | 38,972 | $ | 236 | $ | 1,653,504 | ||||||

| 250 West 57th St. Associates L.L.C. |

$ | 35,722 | $ | 204 | $ | 733,795 | ||||||

The Helmsley estate, as part of an agreement with the supervisor covering this and other matters, has paid the voluntary pro rata reimbursement to the supervisor for its pro rata share of costs advanced, plus interest, which totaled $5,021,048.

To consent to this proposal, simply indicate on the enclosed consent form that you want to consent to this proposal, then sign and mail it in the enclosed return envelope as soon as possible. If you “CONSENT” to the voluntary pro rata reimbursement program, your consent is made only with respect to your participation interest, and your participation in the program is not dependent on the consent of any other participant. If you sign and send in your consent form and do not indicate that you want to consent, you will be counted as “NOT” consenting to this proposal. If you indicate on your consent form that you “ABSTAIN,” you will be counted as “NOT” consenting to this proposal.

| Q: | What is a REIT, and why will the company elect to be a REIT? |

A: A REIT is an entity that has elected and qualifies to be taxed as a “real estate investment trust” under the Internal Revenue Code of 1986, as amended, referred to herein as the Code. A REIT is subject to requirements under the Code related to, among other things, the nature of its income and the composition of its assets, the amount of its annual distributions, and the diversity of its stock ownership. The primary benefit of REIT qualification is that a REIT is generally entitled to a deduction for dividends that it pays and, therefore, is not subject to U.S. federal corporate income tax on its net income distributed to its stockholders if it distributes its net taxable income to its stockholders on an annual basis. Therefore, upon a distribution of dividends by the company to its stockholders, income generated by the company will be taxed only at the stockholder-level. By contrast, a non-REIT “C” corporation is subject to U.S. federal corporate income tax on its taxable income without regard to dividends paid, and its stockholders are subject to U.S. federal income tax on dividends received.

7

Table of Contents

| Q: | What is the operating partnership? |

A: The structure of the company generally is referred to as an “UPREIT” structure. Substantially all of the company’s assets will be held directly or indirectly by the operating partnership. Holders of operating partnership units will have the same rights to distributions as stockholders. This structure generally will enable the company to acquire assets in transactions that will not trigger the recognition of gain to the owners of the acquired assets, assuming certain conditions are met.

The company will be the sole general partner of the operating partnership. As the sole general partner of the operating partnership, the company generally has the exclusive power under the operating partnership agreement to manage and conduct the business of the operating partnership, without the consent of the holders of operating partnership units or the stockholders.

The operating partnership units will be owned by the company and by any person who transfers interests or assets to the operating partnership or one of its subsidiaries in exchange for operating partnership units, including participants in the private entities and the Malkin Holdings group that will be issued operating partnership units as part of the consolidation in exchange for their participation interests and override interests in the private entities and the subject LLCs and their interests in certain of the management companies, as applicable. The company will own one operating partnership unit for each outstanding share of common stock.

| Q: | What is the scope of the public U.S. REIT market? |

A: According to the National Association of Real Estate Investment Trusts, as of September 30, 2011, there were approximately 140 REITs in the U.S. that trade on one of the major stock exchanges, with 130 trading on the NYSE. Total equity market capitalization was approximately $413 billion and the total assets of these listed REITs amounted to approximately $827 billion.

| Q: | Who can vote on the consolidation and third-party portfolio proposal? |

A: Participants in each subject LLC who hold participation interests in such subject LLC during the consent solicitation period are entitled to vote “FOR” or “AGAINST” each of the proposed consolidation and the third-party portfolio proposal with respect to such subject LLC. In the event of a transfer of a participation interest that previously has been voted, that vote will remain in effect unless revoked by the transferee.

The Wien group collectively owns participation interests in the subject LLCs and has advised that it will vote in favor of the consolidation and the third-party portfolio proposal. These participation interests represent the following percentage ownership for each subject LLC: 8.5921% for Empire State Building Associates L.L.C., 8.7684% for 60 East 42nd St. Associates L.L.C. and 7.3148% for 250 West 57th St. Associates L.L.C.

| Q: | How do I vote “FOR” the consolidation and the third-party portfolio proposal? |

A: Simply indicate on the enclosed consent form how you want to vote for each proposal, then sign and mail it in the enclosed return envelope as soon as possible so that your participation interest may be voted “FOR” or “AGAINST” each proposal. If you sign and send in your consent form and do not indicate how you want to vote on either one of these proposals, your consent will be counted as a vote “FOR” such proposal. If you do not submit your consent form or you indicate on your consent form that you “ABSTAIN” from either proposal, it will have the effect of voting “AGAINST” such proposal. If you vote “FOR” the consolidation and your subject LLC participates in the consolidation, you effectively will preclude other alternatives, other than a third-party portfolio transaction, unless you vote “AGAINST” the third-party portfolio proposal. These alternatives include continuation of your subject LLC and a sale of your subject LLC’s interest in the property and the resulting distribution of the net proceeds to its participants. Each of these proposals is subject to a separate consent and approval of each proposal is not dependent on approval of any other proposal.

8

Table of Contents

| Q: | Can I change my vote on the consolidation proposal or the third-party portfolio proposal after I mail my consent form? |

A: Yes. You can change your vote on the consolidation proposal, the third-party portfolio proposal, or both, at any time before the later of the date that consents from participants holding the required percentage interests are received by your subject LLC and the 60th day after the date of this prospectus/consent solicitation. The required percentage interests for Empire State Building Associates L.L.C. is 80% of the outstanding participation interests in each of the three participating groups, for 60 East 42nd St. Associates L.L.C. is 90% of the outstanding participation interests in each of the seven participating groups and for 250 West 57th St. Associates L.L.C. is 75% of the outstanding participation interests in eight out of the ten participating groups. You can change your vote in one of two ways: you can send us a written statement that you would like to change your vote, or you can send us a new consent form. Any change in your vote or new consent form should be sent to MacKenzie Partners, Inc. our vote tabulator.

| Q: | Are there any tax consequences as a result of the consolidation? |

A: You will generally recognize gain or loss for U.S. federal income tax purposes with respect to your participation interest equal to the amount by which the sum of any cash and the value of any shares of Class A common stock you receive in connection with the consolidation, plus the amount of liabilities allocable to your participation interest, exceeds your tax basis in your participation interest. You will recognize “phantom income” (i.e., income in excess of any cash and the value of any shares of common stock you receive) if you have a “negative capital account” with respect to your participation interest. The supervisor urges you to consult with your tax advisor to evaluate the tax consequences to you in your particular circumstances as a result of the consolidation.

| Q: | Will I be able to transfer the shares of Class A common stock I receive in the consolidation? |

A: As stockholders, participants will own Class A common stock which is expected to be listed on the NYSE, and therefore will be publicly valued and freely tradable. Participants will be able to achieve liquidity by selling all or part of the shares of Class A common stock (subject to the restrictions of applicable U.S. federal and state securities laws and after expiration of the lock-up period as described herein).

| Q: | In addition to this prospectus/consent solicitation, I received a supplement. What is the difference between this prospectus/consent solicitation and the supplement? |

A: The purpose of this prospectus/consent solicitation is to describe the consolidation generally and to provide you with a summary of the investment considerations generally applicable to all of the subject LLCs. The purpose of the supplement is to describe the investment considerations particular to your subject LLC.

After you read this prospectus/consent solicitation, the supervisor urges you to read the supplement. The supplement contains information particular to your subject LLC. This information is material in your decision whether to vote “FOR” or “AGAINST” the consolidation.

| Q: | When do you expect the consolidation to be completed? |

A: The company plans to complete the consolidation as soon as possible after the receipt of the approval by the required vote of your subject LLC’s participants and the approval by the required vote of the other subject LLCs’ participants, conditioned on the closing of the IPO. The company is unable to estimate the closing date of the consolidation and has required that it be completed no later than December 31, 2014. Your consent form must be received by , 2012, unless the supervisor extends the solicitation period. The supervisor reserves the right to extend on one or more occasions the solicitation period for one

9

Table of Contents

or more proposals for one or more subject LLCs without extending for other proposals or subject LLCs whether or not it has received approval for the consolidation or the third-party portfolio proposal.

| Q: | If I own participation interests in more than one subject LLC, what should I do? |

A: For each subject LLC in which you own a participation interest, in the same mailing in which you received this prospectus/consent solicitation you have received a transmittal letter, supplement and consent form which provides for vote with respect to the consolidation proposal and the third-party portfolio proposal. Regardless of how many subject LLCs in which you own a participation interest, you have received a single copy of the prospectus/consent solicitation. Participants in each subject LLC will vote separately on whether or not to approve the consolidation. Accordingly, if you hold participation interests in more than one subject LLC, you must complete one consent form for each subject LLC in which you are a participant.

| Q: | Information in this prospectus/consent solicitation is based on a $1,000 original investment. Where can I find information about my actual original investment? |

A: Information is presented in this prospectus/consent solicitation based on a $1,000 original investment to allow participants to determine the effect on them individually. Information regarding the amount of your actual original investment will be provided on the consent form sent to you.

10

Table of Contents

WHO CAN HELP ANSWER YOUR QUESTIONS?

If you have more questions about the consolidation or would like additional copies of the prospectus/consent solicitation or the supplement relating to your subject LLC(s) (which will be provided at no cost), you should contact the person designated on the consent form sent to you.

11

Table of Contents

This summary highlights information contained elsewhere in this prospectus/consent solicitation and may not contain all of the information regarding the consolidation that is important to you. To understand the consolidation and the third-party portfolio proposal fully and for a more complete description of the terms of and risks related to the consolidation and the third-party portfolio proposal, you should read carefully this entire prospectus/consent solicitation, the accompanying supplement relating to your subject LLC, the accompanying transmittal letter and the other documents to which the supervisor or the company, as applicable, has referred you, including the appendices and documents incorporated into this prospectus/consent solicitation by reference. See “Where You Can Find More Information.”

Purpose of this Prospectus/Consent Solicitation

You are being requested to approve the consolidation in which your subject LLC will contribute its assets to the company as part of the consolidation in exchange for Class A common stock of the company and/or cash. As part of the consolidation, the company also will enter into similar transactions with the other subject LLCs, the private entities and with the supervisor and other management companies that provide services to the subject LLCs and these entities. The company will be led by its Chairman, Chief Executive Officer and President, Anthony E. Malkin, who has provided portfolio leadership as president of the supervisor, while Peter L. Malkin will continue to provide guidance as Chairman Emeritus, all supported by the supervisor’s team of executives and staff, who are expected to join the company as part of the consolidation. The consolidation also will result in the creation of a company with a board of directors consisting predominantly of independent directors, which will be responsible for overseeing the operations of the company. Anthony E. Malkin will be the only management member of the board of directors.

The supervisor believes you will benefit from this consolidation through newly created opportunities for liquidity, enhanced operating and financing abilities and efficiencies, combined balance sheets, increased growth opportunities, enhanced property diversification, and continued leadership by the principals of the supervisor under the accountability of the governance structure of a company with its Class A common stock expected to be listed on the New York Stock Exchange, which is referred to herein as the NYSE, and a board of directors consisting predominantly of independent directors.

The supervisor believes this transaction represents the logical next step of value creation after years of action under the supervisor’s leadership to preserve, restore, and enhance your investment in the subject LLC. Included in that history is a challenging time, which began with litigation commenced in 1997 by Peter L. Malkin and the supervisor to remove Helmsley-Spear, Inc., the former property manager and leasing agent (after it was sold by entities controlled by Leona M. Helmsley), as property manager and leasing agent of the properties owned by the subject LLCs and other properties, which are now included in the plans for this consolidation.

Since the successful resolution of that litigation, the supervisor has overseen the engagement by the subject LLCs of independent property management and leasing agents, developed and substantially effected a comprehensive renovation and repositioning program for improving the physical condition of and upgrading the credit quality of tenants at the property, and raised the property’s profile as part of a well regarded portfolio brand. The supervisor believes that it is an opportune time for the subject LLCs to take advantage of the opportunity to participate in the consolidation which will afford participants the administrative and operating efficiencies, as well as better value protection through diversification. Additionally, the supervisor believes the consolidation provides value enhancement through better access to capital and liquidity for investors who so desire.