UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT

OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of August, 2015

Commission File Number: 001-35129

Arcos Dorados Holdings Inc.

(Exact name of registrant as specified in its charter)

Roque Saenz Peña 432

B1636FFB Olivos, Buenos Aires, Argentina

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

| Form 20-F | X |

Form 40-F |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

| Yes | No | X |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

| Yes | No | X |

ARCOS DORADOS HOLDINGS INC.

TABLE OF CONTENTS

| ITEM | |

| 1. | Press Release dated August 11, 2015 entitled “Arcos Dorados Reports Second Quarter 2015 Financial Results” |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Arcos Dorados Holdings Inc. | ||||||

| By: | /s/ Juan David Bastidas | |||||

| Name: | Juan David Bastidas | |||||

| Title: | Chief Legal Counsel | |||||

Date: August 11, 2015

Item 1

FOR IMMEDIATE RELEASE

ARCOS DORADOS REPORTS SECOND QUARTER 2015 FINANCIAL RESULTS

Achieved

high single-digit comparable sales growth and delivered consolidated

Adjusted EBITDA margin expansion.

Buenos Aires, Argentina, August 11, 2015 – Arcos Dorados Holdings, Inc. (NYSE: ARCO) (“Arcos Dorados” or the “Company”), Latin America’s largest restaurant chain and the world’s largest McDonald’s franchisee, today reported unaudited results for the quarter ended June 30, 2015.

Second Quarter 2015 Key Results

| • | As reported consolidated revenues were $759.0 million, a 17.3% decline versus the second quarter of 2014. On an organic basis1 and excluding Venezuela consolidated revenues grew 7.7%. |

| • | Systemwide comparable sales increased by 8.5% year-over-year. |

| • | As reported Adjusted EBITDA was $41.1 million, or 2.2% lower year-over-year. Organic Adjusted EBITDA excluding Venezuela, increased by 9.8% versus the prior year quarter. |

| • | As reported General and Administrative expenses (G&A) declined by $9.7 million, or 12.6%, year-over-year. |

| • | As reported net income was $7.0 million, compared to a $99.0 million loss in the year-ago period, which included charges related to the transition to a weaker exchange rate in Venezuela. |

“We are making clear headway on our long-term strategy to improve profitability and shareholder value, having delivered solid margin expansion and a reduction in G&A expenses in the second quarter. Against a backdrop of slowing economic growth, softer consumer spending and elevated currency depreciation in our key countries, second quarter results reflected promotions with a strong track record and efforts to provide our customers with more affordable dining options. We were particularly pleased to see traction in our family business.”

_______________________

1 For a definition of organic results please refer to page 13 of this document.

Second Quarter 2015 Results

Consolidated

| Figure

1. AD Holdings Inc Consolidated: Key Financial Results (In millions of U.S. dollars, except as noted) |

| 2Q14 (a) |

Special

Items (b) |

Currency Translation (c) | Organic

Growth (d) |

2Q15 (a+b+c+d) |

% As Reported | % Organic | |

| Total Restaurants (Units) | 2,075 | 2,120 | 2.2% | ||||

| Sales by Company-operated Restaurants | 881.4 | (236.0) | 83.3 | 728.7 | -17.3% | 9.5% | |

| Revenues from franchised restaurants | 36.5 | (14.9) | 8.7 | 30.3 | -17.1% | 23.7% | |

| Total Revenues | 917.9 | (250.9) | 92.0 | 759.0 | -17.3% | 10.0% | |

| Systemwide Comparable Sales | 8.5% | ||||||

| Adjusted EBITDA | 42.0 | (4.1) | (33.1) | 36.2 | 41.1 | -2.2% | 95.4% |

| Adjusted EBITDA Margin | 4.6% | 5.4% | |||||

| Net income (loss) attributable to AD | (99.0) | 81.6 | (23.0) | 47.3 | 7.0 | NM | NM |

| No. of shares outstanding (thousands) | 210,117 | 210,447 | |||||

| EPS (US$/Share) | (0.47) | 0.03 |

(2Q15 = 2Q14 + Special items + Currency translation + Organic growth). Please refer to “Definitions” section for further detail.

The 17.3% decline in Arcos Dorados’ second quarter as reported revenues resulted mainly from the 37.7% year-over-year average depreciation of the Brazilian real and the use of a weaker official exchange rate to remeasure the results of the Company’s Venezuelan operations. On an organic basis, revenue growth of 10.0% was driven by an 8.5% expansion in systemwide comparable sales, reflecting average check growth, partially offset by a modest decline in traffic. The net addition of 45 restaurants during the last 12-month period contributed $23.0 million to organic revenue growth.

Special items impacting Adjusted EBITDA consisted of:

| Special

Items (In thousands of U.S. dollars) |

|||

| 2Q | 2Q | Variation | |

| 2015 | 2014 | ||

| Royalty waiver from Venezuela | - | 3,124 | -3,124 |

| CADs net (loss) gain (i) | -109 | 839 | -948 |

| TOTAL | -109 | 3,963 | -4,072 |

| (i) Compensation expense. 2Q2014 includes the result from the total equity return swap. | |||

2

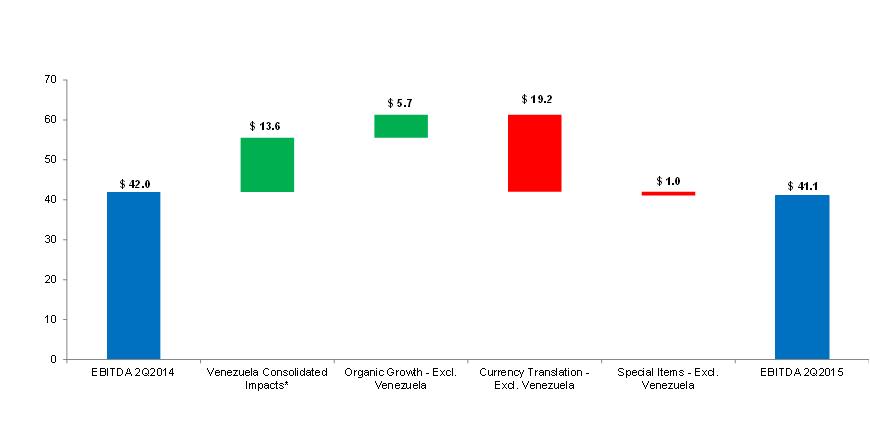

As reported Adjusted EBITDA ($ million)

Breakdown of main variations contributing to 2Q15 Adjusted EBITDA

*Net impact of Special Items (-$3.1 million), Currency Translation (-$13.9 million) and Organic Growth ($30.6 million).

Reported Adjusted EBITDA for the second quarter decreased 2.2% as organic growth achieved in each of the operating divisions was more than offset by currency translation impacts, primarily in Brazil, Venezuela and Argentina, as well as a negative variance in special items.

The Adjusted EBITDA margin improved by more than 80 basis points to 5.4%, supported by margin expansion at the operating division level as well as the non-recurrence of inventory write-downs recorded in the 2Q14 related to the transition to a weaker foreign exchange rate in Venezuela.

As reported, consolidated G&A dropped by 12.6%, or $9.7 million. On a constant currency basis, G&A increased by 7.1% year-over-year, or $5.5 million in absolute terms.

3

Consolidated – excluding Venezuela

| Figure

2. AD Holdings Inc Consolidated - Excluding Venezuela: Key Financial Results (In millions of U.S. dollars, except as noted) |

| 2Q14 (a) |

Special

Items (b) |

Currency

Translation (c) |

Organic

Growth (d) |

2Q15 (a+b+c+d) |

% As Reported | % Organic | |

| Total Restaurants (Units) | 1,939 | 1,986 | 2.4% | ||||

| Sales by Company-operated Restaurants | 830.5 | (169.2) | 62.3 | 723.6 | -12.9% | 7.5% | |

| Revenues from franchised restaurants | 33.6 | (8.1) | 4.3 | 29.7 | -11.6% | 12.6% | |

| Total Revenues | 864.2 | (177.3) | 66.5 | 753.4 | -12.8% | 7.7% | |

| Systemwide Comparable Sales | 4.9% | ||||||

| Adjusted EBITDA | 59.2 | (1.0) | (19.2) | 5.7 | 44.8 | -24.5% | 9.8% |

| Adjusted EBITDA Margin | 6.9% | 5.9% | |||||

| Net income (loss) attributable to AD | (3.0) | 7.2 | (10.6) | 19.8 | 13.3 | NM | NM |

| No. of shares outstanding (thousands) | 210,117 | 210,447 | |||||

| EPS (US$/Share) | -0.01 | 0.06 |

Excluding the Venezuelan operation, as reported revenues declined by 12.8% mainly due to the depreciation of the Brazilian real, while organic revenues rose 7.7% in the second quarter. Systemwide comparable sales increased 4.9% due to average check growth, partially offset by a decline in traffic of less than 1.0%. As reported Adjusted EBITDA contracted 24.5%, but increased 9.8% in organic terms. The Adjusted EBITDA margin declined more than 90 basis points to 5.9% due to lower operating results coupled with a negative variance derived from adjustments to EBITDA, on a year-over-year basis.

Non-operating Results

Non-operating results for the second quarter reflected a non-cash $3.7 million foreign currency exchange gain, versus a loss of $35.5 million last year, mainly due to the appreciation of the Brazilian real (BRL) from the previous quarter end, which generated a gain on intercompany balances, partially offset by a loss related to the BRL-denominated long-term debt. Net interest expense was $2.0 million lower year-over-year, totaling $16.9 million in the quarter.

The Company reported an income tax benefit of $6.5 million for the quarter, compared to an expense of $6.3 million in the prior year.

Second quarter net income attributable to the Company totaled $7.0 million, compared to a loss of $99.0 million in the same period of 2014, which was largely explained by the transition to a weaker foreign exchange rate in Venezuela during 2Q14.

The Company reported earnings per share of $0.03 in the second quarter of 2015, compared to a loss of $0.47 in the previous corresponding period. Total weighted average shares for the second quarter of 2015 were 210,447,373 as compared to 210,116,897 in the second quarter of 2014, reflecting the issuance of shares as a result of the partial vesting of restricted share units.

4

Analysis by Division:

Brazil Division

| Figure

3. Brazil Division: Key Financial Results (In millions of U.S. dollars, except as noted) | |||||||

| 2Q14 (a) |

Special

Items (b) |

Currency

Translation (c) |

Organic

Growth (d) |

2Q15 (a+b+c+d) |

% As Reported | % Organic | |

| Total Restaurants (Units) | 824 | 871 | 5.7% | ||||

| Total Revenues | 459.1 | (132.7) | 24.4 | 350.8 | -23.6% | 5.3% | |

| Systemwide Comparable Sales | 1.9% | ||||||

| Adjusted EBITDA | 55.2 | 0.0 | (16.9) | 6.1 | 44.4 | -19.5% | 11.1% |

| Adjusted EBITDA Margin | 12.0% | 12.7% | |||||

Brazil’s as reported revenues decreased by 23.6%, as a 37.7% year-over-year average depreciation of the Brazilian real more than offset a low-single digit increase in comparable sales and the contribution of new restaurant openings. Excluding the depreciation of the Brazilian real, organic revenues increased 5.3% year-over-year. Systemwide comparable sales increased by 1.9%, supported by average check growth and slightly positive traffic.

While the consumption environment in Brazil remains weak, traffic levels benefited from a favorable year-over-year comparison in the second half of June due to the FIFA World Cup last year and successful promotional activities. The Company’s marketing activities in the quarter continued to focus on promotions with a strong track record of success and included the launch of the Monopoly promotion and the Super/Mega/Grand Big Mac campaign, which helped mitigate the soft consumer environment in the country. The second quarter marketing calendar also included the Crispy Tasty sandwich and the McFlurry Oreo in the Dessert category. Also in the quarter, the Company launched the successful Minions campaign in the Happy Meal, reaffirming the Company’s commitment to the family business.

The net addition of 47 restaurants during the last 12-month period, of which over 60% were free-standing units that deliver a full experience to the Company’s customers, contributed $18.8 million to revenues on a constant currency basis during the quarter.

As reported Adjusted EBITDA contracted 19.5%, but increased 11.1% in organic terms. The Adjusted EBITDA margin improved more than 60 basis points to 12.7% as efficiencies in G&A and Payroll costs more than offset higher F&P and Occupancy and Other Operating Expenses as a percentage of sales.

5

NOLAD

| Figure

4. NOLAD Division: Key Financial Results (In millions of U.S. dollars, except as noted) | |||||||

| 2Q14 (a) |

Special

Items (b) |

Currency

Translation (c) |

Organic

Growth (d) |

2Q15 (a+b+c+d) |

% As Reported | % Organic | |

| Total Restaurants (Units) | 509 | 511 | 0.4% | ||||

| Total Revenues | 96.7 | (7.5) | 2.1 | 91.2 | -5.6% | 2.2% | |

| Systemwide Comparable Sales | -0.2% | ||||||

| Adjusted EBITDA | 6.0 | 0.0 | (0.1) | 2.2 | 8.1 | 34.8% | 36.5% |

| Adjusted EBITDA Margin | 6.2% | 8.8% | |||||

NOLAD’s as reported revenues decreased by 5.6% year-over-year, mainly due to the 18% year-over-year average depreciation of the Mexican peso. However, on an organic basis, revenues increased 2.2% year-over-year. Systemwide comparable sales were broadly flat as average check growth was counterbalanced by a decline in traffic. Traffic levels benefited from a favorable year-over-year comparison in the second half of June due to the FIFA World Cup last year.

Marketing initiatives comprised promotions for Children’s Day in Mexico and “Magic Straws” in Costa Rica and Panama. Marketing initiatives in the quarter also included the Super Mac and Mega Mac promotion in Costa Rica and Panama and the Adventure Time property in the Happy Meal. McMio, which is a new menu platform in Mexico that enables customers to create their own personalized menu combinations, is now almost completely rolled out.

The net addition of 2 restaurants during the last 12-month period contributed $2.2 million to revenues in constant currency.

As reported Adjusted EBITDA increased by 34.8%, or 36.5% on an organic basis. NOLAD’s operational excellence is reflected in the division’s Adjusted EBITDA margin improvement in seven of the last eight quarters while maintaining superior customer service levels. The more than 260 basis points margin increase to 8.8% was due to efficiencies in Payroll costs and Occupancy & Other Operating Expenses, combined with lower G&A as a percentage of sales more than offset higher F&P costs as a percentage of sales.

6

SLAD

| Figure

5. SLAD Division: Key Financial Results (In millions of U.S. dollars, except as noted) | |||||||

| 2Q14 (a) |

Special

Items (b) |

Currency

Translation (c) |

Organic

Growth (d) |

2Q15 (a+b+c+d) |

% As Reported | % Organic | |

| Total Restaurants (Units) | 378 | 383 | 1.3% | ||||

| Total Revenues | 203.3 | (24.7) | 42.2 | 220.8 | 8.6% | 20.7% | |

| Systemwide Comparable Sales | 21.0% | ||||||

| Adjusted EBITDA | 18.8 | 0.0 | (2.6) | 6.2 | 22.4 | 19.1% | 33.1% |

| Adjusted EBITDA Margin | 9.2% | 10.1% | |||||

SLAD’s as reported revenues increased by 8.6%, or 20.7% in organic terms, versus the prior year quarter. Currency translation was impacted by the 11.2% average decline of the Argentine peso versus the same period last year. Systemwide comparable sales increased 21.0%, driven by average check growth.

While traffic in the division was approximately flat, primarily impacted by a challenging macroeconomic environment in Argentina, it also benefited from a favorable year-over-year comparison in the second half of June due to last year’s FIFA World Cup. The Company’s marketing initiatives in the second quarter were designed to stimulate traffic and included the “Billetazos” promotion in key countries, the inclusion of the Triple Cheeseburger in the affordability platform, as well as the “Adventure Time” Happy Meal.

The net addition of 5 restaurants during the last 12-month period contributed $1.4 million to revenues in constant currency in the quarter.

As reported Adjusted EBITDA increased 19.1% and rose 33.1% in organic terms. The Adjusted EBITDA margin expanded 90 basis points to 10.1%, driven by efficiencies in F&P, Payroll costs and G&A expenses, partially offset by higher Occupancy & Other Operating Expenses as a percentage of sales and also higher occupancy expenses from franchised restaurants.

7

Caribbean Division

| Figure

6. Caribbean Division: Key Financial Results (In millions of U.S. dollars, except as noted) | |||||||

| 2Q14 (a) |

Special

Items (b) |

Currency

Translation (c) |

Organic

Growth (d) |

2Q15 (a+b+c+d) |

% As Reported | % Organic | |

| Total Restaurants (Units) | 364 | 355 | -2.5% | ||||

| Total Revenues | 158.8 | (85.9) | 23.3 | 96.1 | -39.5% | 14.7% | |

| Systemwide Comparable Sales | 20.3% | ||||||

| Adjusted EBITDA | (10.2) | (3.1) | (14.6) | 28.6 | 0.6 | 106.3% | 214.3% |

| Adjusted EBITDA Margin | -6.4% | 0.7% | |||||

The Caribbean division’s as reported revenues declined by 39.5%, due to the remeasurement of the results of the Venezuelan operation at a weaker year-over-year average exchange rate. Excluding this factor, organic revenues rose 14.7% year-over-year. Systemwide comparable sales increased by 20.3%, as inflation-driven growth in average check more than offset a decrease in traffic. The division continues to be affected by challenging macroeconomic and political environments in Venezuela and Puerto Rico. Key marketing initiatives during the quarter included the “Almuerzo Colombiano”, among others.

The Company is focused on long term, profitable growth as well as offering well-located and inviting restaurants to its guests. As part of that strategy, the Company closed 10 underperforming restaurants, against 1 opening, in the Caribbean Division over the last 12-month period. The combined contribution to constant currency revenues of the restaurants that were closed and opened was $0.6 million.

As reported Adjusted EBITDA was $0.6 million, compared with negative $10.2 million in the prior year period. The Adjusted EBITDA margin was 0.7%, versus negative 6.4% in the second quarter of 2014. The improvement reflects a materially lower impact from the change in the foreign exchange rate used to remeasure the Venezuelan operation. Special items impacting Adjusted EBITDA included the recognition of a $3.1 million royalty waiver for the Venezuelan operation from McDonald’s Corporation in the second quarter of last year.

8

Caribbean Division – excluding Venezuela

| Figure

7. Caribbean Division - Excluding Venezuela: Key Financial Results (In millions of U.S. dollars, except as noted) | |||||||

| 2Q14 (a) |

Special

Items (b) |

Currency

Translation (c) |

Organic

Growth (d) |

2Q15 (a+b+c+d) |

% As Reported | % Organic | |

| Total Restaurants (Units) | 228 | 221 | -3.1% | ||||

| Total Revenues | 105.0 | (12.4) | (2.2) | 90.5 | -13.8% | -2.1% | |

| Systemwide Comparable Sales | -4.3% | ||||||

| Adjusted EBITDA | 3.8 | 0.0 | (0.7) | 1.3 | 4.3 | 15.0% | 34.4% |

| Adjusted EBITDA Margin | 3.6% | 4.8% | |||||

As reported revenues in the Caribbean division excluding Venezuela decreased by 13.8% versus the prior-year period, mainly due to the depreciation of the Colombian peso and the Euro. Excluding currency movements, organic revenues declined 2.1% and were affected by the ongoing tough macroeconomic and political environment in Puerto Rico. Comparable sales decreased by 4.3%, largely due to traffic declines in Puerto Rico.

As reported Adjusted EBITDA improved 15.0%, or 34.4% on an organic basis. The Adjusted EBITDA margin increased by 120 basis points to 4.8% as efficiencies in G&A, Payroll, and Occupancy and Other Operating Expenses more than offset higher F&P as a percentage of sales.

| New Unit Development | |||||

| Figure 8. Total Restaurants (eop)* | |||||

| June 2015 |

March 2015 |

December 2014 |

September 2014 |

June 2014 | |

| Brazil | 871 | 867 | 866 | 833 | 824 |

| NOLAD | 511 | 512 | 513 | 511 | 509 |

| SLAD | 383 | 382 | 383 | 380 | 378 |

| Caribbean | 355 | 358 | 359 | 362 | 364 |

| TOTAL | 2,120 | 2,119 | 2,121 | 2,086 | 2,075 |

| LTM Net Openings | 45 | 50 | 59 | 93 | 104 |

| * Considers Company-operated and franchised restaurants at period-end | |||||

The Company completed 72 new restaurant openings for the twelve month period ended June 30, 2015, resulting in a total of 2,120 restaurants. Also in the period, the Company added 229 Dessert Centers and 8 McCafés, bringing the totals to 2,549 and 332, respectively.

Balance Sheet & Cash Flow Highlights

Cash and cash equivalents were $83.2 million at June 30, 2015. The Company’s total financial debt (including derivative instruments) was $755.1 million. Net debt was $671.9 million and the Net Debt/Adjusted EBITDA ratio was 2.8x at June 30, 2015.

Net cash provided by operating activities was $33.8 million in the second quarter of 2015, while cash used in financing activities amounted to $6.0 million. During the quarter, capital expenditures totaled $22.2 million.

9

First Half 2015

For the six months ended June 30, 2015, the Company’s revenues declined by 16.3% to $1,534.1 million. On an organic basis however, revenues grew by 10.2%. Adjusted EBITDA was $82.9 million, a 10.2% decrease compared to the first half of 2014. On an organic basis, Adjusted EBITDA increased by 62.6%, largely explained by the one-time charges that the Company registered in 1H14 as a result of the foreign exchange rate change in Venezuela. The year-to-date consolidated net loss amounted to $21.3 million, compared with a loss of $119.6 million in the first half of 2014. The net loss in 1H15 includes the following impacts the Company registered in the first quarter, which resulted from the transition to the SIMADI rate in Venezuela: (i) an FX loss of $8.0 million, (ii) an impairment charge of $7.8 million, and (iii) inventory write down of $3.3 million recorded in the first quarter, among others.

Excluding the Venezuelan operation, the Company’s revenues declined by 10.3%, but increased by 7.3% on an organic basis. Adjusted EBITDA declined by 22.6%, as reported, and increased by 2.2%, on an organic basis. The reported Adjusted EBITDA margin contracted by almost 100 basis points to 6.1%, as leverage in payroll costs was more than offset by higher F&P and G&A as a percentage of revenues.

10

2015 Guidance/Outlook Revision

Consistent with the Company’s long term strategy to improve the profitability of the existing restaurant base and given the challenging operating environment in many of its markets, the Company has reviewed its short-term capital expenditure plans. As a result, the Company is revising its 2015 full year guidance for restaurant openings and now expects to open approximately 30 new restaurants.

The Company, however, is maintaining its capital expenditures guidance range of $90.0 to $120.0 million for the year. More of the Company’s capital expenditures are now allocated to restaurant re-imaging and system upgrades at the restaurant level to further improve operating efficiencies and provide a modern and progressive restaurant experience to its guests.

Quarter Highlights & Recent Developments

Amendment to the Restaurant Opening Plan for 2014-2016

Under the Master Franchise Agreement (MFA), the Company is required to agree with McDonald’s on a restaurant opening plan and a reinvestment plan for each three-year period during the term of the MFA. The restaurant opening plan specifies the minimum number of new restaurants to be opened in the territories during the applicable three-year period, while the reinvestment plan specifies the amount the Company must spend reimaging and/or upgrading restaurants during the applicable three-year period.

As part of the reinvestment plan with respect to the current three-year period (commenced on January 1, 2014), the Company committed to open a minimum of 250 new restaurants and to reinvest an aggregate of at least $180 million.

The Company recently reached an agreement with McDonald’s Corporation to amend the 2014-2016 opening plan, mainly in order to adjust this plan to the current economic and political realities of the region. Under this agreement, the Company has committed to opening a minimum of 150 new restaurants over the three-year period, down from the original 250.

Importantly, the Company and McDonald’s Corporation agreed to maintain the 3-year reinvestment plan of at least $180 million.

Covenants under the MFA

The MFA requires the Company, among other obligations, to maintain a minimum fixed charge coverage ratio of at least 1.50x, as well as a maximum leverage ratio of 4.25x.

The Company was not in compliance with the ratio requirements for certain periods during 2014 and for the first two quarters of 2015. As of June 30, 2015, the fixed charge coverage ratio was 1.45x and the leverage ratio was 4.61x. For that reason, on July 17, 2015, McDonald’s Corporation granted the Company an extension of the limited waiver, through and including December 31, 2015, during which time the Company will not be required to comply with the financial ratios set forth in the MFA.

11

Revolving Credit Facility with Bank of America, N.A.

On July 30, 2015, the Company renewed the revolving credit facility with Bank of America, N.A. for up to $50 million, maturing on August 3, 2016. Under the new agreement, the Company will be required to comply with a consolidated net indebtedness to EBITDA ratio no greater than 3.5x on the last day of any quarter (versus the previous covenant ratio of 3.0x). As of June 30, 2015, this ratio was 2.92x. For more details on the revolving credit facility with Bank of America, N.A., please refer to Note 4 of the Company’s Financial Statements filed today with the S.E.C.

Key Management Changes

Sergio Alonso has been appointed the Company’s new Chief Executive Officer. He will succeed Chairman and Chief Executive Officer Woods Staton, who will remain as Executive Chairman.

Marcelo Rabach, who currently serves as Divisional President of the North Latin America Division (NOLAD), will succeed Mr. Alonso and is promoted to Chief Operating Officer.

Rogério Barreira, who currently serves as the Vice President of Operations in Brazil, will succeed Mr. Rabach as President of NOLAD. Mr. Barreira holds a Master of Business Administration from the Fundação Getúlio Vargas in São Paulo, Brazil.

The aforementioned management changes will be effective October 1, 2015.

|

Investor Relations Contact Daniel Schleiniger Arcos Dorados – IR Director daniel.schleiniger@ar.mcd.com +54 11 4711 2287 www.arcosdorados.com/ir |

Media Contact MBS Value Partners Katja Buhrer katja.buhrer@mbsvalue.com +1 917 969 3438 |

12

Definitions:

Systemwide comparable sales: growth refers to the change, measured in constant currency, in our Company-operated and franchised restaurant sales in one period from a comparable period for restaurants that have been open for thirteen months or longer. While sales by our franchisees are not recorded as revenues by us, we believe the information is important in understanding our financial performance because these sales are the basis on which we calculate and record franchised revenues, and are indicative of the financial health of our franchisee base.

Constant currency: basis refers to amounts calculated using the same exchange rate over the periods under comparison to remove the effects of currency fluctuations from this trend analysis.

Organic: To better discern underlying business trends, this release uses non-GAAP financial measures that segregate year-over-year growth into three categories: (i) currency translation, (ii) special items and (iii) organic growth. (i) Currency translation reflects the impact on growth of the appreciation or depreciation of the local currencies in which we conduct our business against the US dollar (the currency in which our financial statements are prepared). (ii) Special items include the impact of events that management does not consider part of the underlying performance of the business. (iii) Organic growth reflects the underlying growth of the business excluding the effect from currency translation and special items.

About Arcos Dorados

Arcos Dorados is the world’s largest McDonald’s franchisee in terms of systemwide sales and number of restaurants, operating the largest quick service restaurant (“QSR”) chain in Latin America and the Caribbean. It has the exclusive right to own, operate and grant franchises of McDonald’s restaurants in 20 Latin American and Caribbean countries and territories, including Argentina, Aruba, Brazil, Chile, Colombia, Costa Rica, Curaçao, Ecuador, French Guyana, Guadeloupe, Martinique, Mexico, Panama, Peru, Puerto Rico, St. Croix, St. Thomas, Trinidad & Tobago, Uruguay and Venezuela. The Company operates or franchises 2,120 McDonald’s-branded restaurants with over 95,000 employees serving approximately 4.3 million customers a day, as of June 30, 2015. Recognized as one of the best companies to work for in Latin America, Arcos Dorados is traded on the New York Stock Exchange (NYSE: ARCO). To learn more about the Company, please visit the Investors section of our website: www.arcosdorados.com

Cautionary Statement on Forward-Looking Statements

This press release contains forward-looking statements. The forward-looking statements contained herein include statements about the Company’s business prospects, its ability to attract customers, its affordable platform, its expectation for revenue generation and its outlook and guidance for 2015. These statements are subject to the general risks inherent in Arcos Dorados' business. These expectations may or may not be realized. Some of these expectations may be based upon assumptions or judgments that prove to be incorrect. In addition, Arcos Dorados' business and operations involve numerous risks and uncertainties, many of which are beyond the control of Arcos Dorados, which could result in Arcos Dorados' expectations not being realized or otherwise materially affect the financial condition, results of operations and cash flows of Arcos Dorados. Additional information relating to the uncertainties affecting Arcos Dorados' business is

13

contained in its filings with the Securities and Exchange Commission. The forward-looking statements are made only as of the date hereof, and Arcos Dorados does not undertake any obligation to (and expressly disclaims any obligation to) update any forward-looking statements to reflect events or circumstances after the date such statements were made, or to reflect the occurrence of unanticipated events.

Use of Non-GAAP Financial Measures

In addition to financial measures prepared in accordance with the general accepted accounting principles (GAAP), within this press release and the accompanying tables, we use a financial measure titled ‘Adjusted EBITDA’. We use Adjusted EBITDA to facilitate operating performance comparisons from period to period. Adjusted EBITDA is defined as our operating income plus depreciation and amortization plus/minus the following losses/gains included within other operating expenses, net and within general and administrative expenses in our statement of income: gains from sale or insurance recovery of property and equipment, write-offs of property and equipment, impairment of long-lived assets, one-time expenses related to G&A optimization plan, stock-based compensation in connection with the Company’s initial public listing, and the ADBV Long-Term Incentive Plan incremental compensation from modification.

We believe Adjusted EBITDA facilitates company-to-company operating performance comparisons by backing out potential differences caused by variations such as capital structures (affecting net interest expense and other financial charges), taxation (affecting income tax expense) and the age and book depreciation of facilities and equipment (affecting relative depreciation expense), which may vary for different companies for reasons unrelated to operating performance.

14

Second Quarter & First Half 2015 Consolidated Results

(In thousands of U.S. dollars, except per share data)

| Figure

9. Second Quarter & First Half 2015 Consolidated Results (In thousands of U.S. dollars, except per share data) |

|||||

| For Three-Months ended | For Six-Months ended | ||||

| June 30, | June 30, | ||||

| 2015 | 2014 | 2015 | 2014 | ||

| REVENUES | |||||

| Sales by Company-operated restaurants | 728,702 | 881,387 | 1,472,173 | 1,759,445 | |

| Revenues from franchised restaurants | 30,299 | 36,535 | 61,886 | 73,971 | |

| Total Revenues | 759,001 | 917,922 | 1,534,059 | 1,833,416 | |

| OPERATING COSTS AND EXPENSES | |||||

| Company-operated restaurant expenses: | |||||

| Food and paper | (260,557) | (318,647) | (520,018) | (634,369) | |

| Payroll and employee benefits | (153,325) | (192,232) | (314,068) | (381,801) | |

| Occupancy and other operating expenses | (210,004) | (252,126) | (426,555) | (504,245) | |

| Royalty fees | (37,298) | (41,127) | (75,300) | (82,513) | |

| Franchised restaurants - occupancy expenses | (13,864) | (15,380) | (29,090) | (31,097) | |

| General and administrative expenses | (67,675) | (77,399) | (133,146) | (144,575) | |

| Other operating expenses, net | (2,372) | (59,290) | (16,591) | (72,321) | |

| Total operating costs and expenses | (745,095) | (956,201) | (1,514,768) | (1,850,921) | |

| Operating income (loss) | 13,906 | (38,279) | 19,291 | (17,505) | |

| Net interest expense | (16,873) | (18,852) | (33,197) | (35,809) | |

| (Loss) gain from derivative instruments | (52) | 42 | (125) | 52 | |

| Foreign currency exchange results | 3,686 | (35,451) | (20,012) | (55,898) | |

| Other non-operating income (expense), net | (118) | (173) | (164) | (491) | |

| Income (loss) before income taxes | 549 | (92,713) | (34,207) | (109,651) | |

| Income tax benefit (expense) | 6,470 | (6,264) | 13,057 | (9,963) | |

| Net income (loss) | 7,019 | (98,977) | (21,150) | (119,614) | |

| Less: Net income attributable to non-controlling interests | (46) | (9) | (110) | (2) | |

| Net income (loss) attributable to Arcos Dorados Holdings Inc. | 6,973 | (98,986) | (21,260) | (119,616) | |

| (Loss) earnings per share information ($ per share): | |||||

| Basic net income per common share | $ 0.03 | $ (0.47) | $ (0.10) | $ (0.57) | |

| Weighted-average number of common shares outstanding-Basic | 210,447,373 | 210,116,897 | 210,332,347 | 209,992,850 | |

| Adjusted EBITDA Reconciliation | |||||

| Operating income | 13,906 | (38,279) | 19,291 | (17,505) | |

| Depreciation and amortization | 28,164 | 29,368 | 55,860 | 57,384 | |

| Operating charges excluded from EBITDA computation | (1,016) | 50,868 | 7,756 | 52,401 | |

| Adjusted EBITDA | 41,054 | 41,957 | 82,907 | 92,280 | |

| Adjusted EBITDA Margin as % of total revenues | 5.4% | 4.6% | 5.4% | 5.0% | |

15

Second Quarter & First Half 2015 Results by Division

(In thousands of U.S. dollars)

| Figure

10. Second Quarter & First Half 2015 Consolidated Results by Division (In thousands of U.S. dollars) |

|||||||||

| 2Q | 1H | ||||||||

| Three-Months ended | % Incr. | Constant | Six-Months ended | % Incr. | Constant | ||||

| June 30, | / | Currency | June 30, | / | Currency | ||||

| 2015 | 2014 | (Decr) | Incr/(Decr)% | 2015 | 2014 | (Decr) | Incr/(Decr)% | ||

| Revenues | |||||||||

| Brazil | 350,844 | 459,137 | -23.6% | 5.3% | 716,774 | 887,702 | -19.3% | 4.2% | |

| Caribbean | 96,126 | 158,757 | -39.5% | 14.7% | 196,708 | 346,395 | -43.2% | 17.4% | |

| NOLAD | 91,223 | 96,683 | -5.6% | 2.2% | 177,766 | 189,362 | -6.1% | 1.0% | |

| SLAD | 220,808 | 203,345 | 8.6% | 20.7% | 442,811 | 409,957 | 8.0% | 21.2% | |

| TOTAL | 759,001 | 917,922 | -17.3% | 10.0% | 1,534,059 | 1,833,416 | -16.3% | 10.2% | |

| Operating (loss) Income | |||||||||

| Brazil | 29,666 | 39,675 | -25.2% | 3.4% | 55,977 | 70,867 | -21.0% | 1.9% | |

| Caribbean | (6,045) | (63,793) | -90.5% | -115.2% | (22,528) | (75,487) | 70.2% | 108.5% | |

| NOLAD | 1,491 | (1,951) | -176.4% | -144.5% | 1,171 | (3,575) | 132.8% | 99.8% | |

| SLAD | 18,048 | 13,347 | 35.2% | 51.5% | 38,187 | 30,750 | 24.2% | 41.1% | |

| Corporate and Other | (29,254) | (25,557) | 14.5% | 19.7% | (53,516) | (40,060) | -33.6% | -48.3% | |

| TOTAL | 13,906 | (38,279) | -136.3% | -207.7% | 19,291 | (17,505) | 210.2% | 457.5% | |

| Adjusted EBITDA | |||||||||

| Brazil | 44,396 | 55,179 | -19.5% | 11.1% | 84,619 | 100,725 | -16.0% | 8.5% | |

| Caribbean | 645 | (10,202) | -106.3% | -249.2% | (1,057) | (14,164) | 92.5% | 286.2% | |

| NOLAD | 8,058 | 5,976 | 34.8% | 36.5% | 14,237 | 11,590 | 22.8% | 23.8% | |

| SLAD | 22,358 | 18,766 | 19.1% | 33.1% | 47,403 | 41,018 | 15.6% | 30.8% | |

| Corporate and Other | (34,403) | (27,762) | 23.9% | 28.0% | (62,295) | (46,889) | -32.9% | -44.5% | |

| TOTAL | 41,054 | 41,957 | -2.2% | 76.7% | 82,907 | 92,280 | -10.2% | 47.3% | |

| Figure 11. Average Exchange Rate per Quarter* | ||||||

| Brazil | Mexico | Argentina | Venezuela | |||

| 2Q15 | 3.07 | 15.32 | 8.95 | 197.86 | ||

| 2Q14 | 2.23 | 12.99 | 8.05 | 23.37 | ||

| * Local $ per 1 US$ | ||||||

16

Summarized Consolidated Balance Sheets

(In thousands of U.S. dollars)

| Figure

12. Summarized Consolidated Balance Sheets (In thousands of U.S. dollars) | |||

| June 30 | December 31 | ||

| 2015 | 2014 | ||

| ASSETS | |||

| Current assets | |||

| Cash and cash equivalents | 83,181 | 139,030 | |

| Accounts and notes receivable, net | 67,297 | 83,003 | |

| Other current assets (1) | 218,000 | 225,163 | |

| Total current assets | 368,478 | 447,196 | |

| Non-current assets | |||

| Property and equipment, net | 990,769 | 1,116,281 | |

| Net intangible assets and goodwill | 51,036 | 57,864 | |

| Deferred income taxes | 90,867 | 75,319 | |

| Other non-current assets (2) | 85,520 | 98,120 | |

| Total non-current assets | 1,218,192 | 1,347,584 | |

| Total assets | 1,586,670 | 1,794,780 | |

| LIABILITIES AND EQUITY | |||

| Current liabilities | |||

| Accounts payable | 182,266 | 220,337 | |

| Taxes payable (3) | 95,781 | 120,763 | |

| Accrued payroll and other liabilities | 86,745 | 112,072 | |

| Other current liabilities (4) | 31,969 | 37,580 | |

| Provision for contingencies | 648 | 777 | |

| Financial debt (5) | 53,549 | 49,642 | |

| Deferred income taxes | 816 | 895 | |

| Total current liabilities | 451,774 | 542,066 | |

| Non-current liabilities | |||

| Accrued payroll and other liabilities | 18,312 | 18,440 | |

| Provision for contingencies | 9,912 | 11,427 | |

| Financial debt (6) | 718,121 | 761,080 | |

| Deferred income taxes | 4,315 | 4,180 | |

| Total non-current liabilities | 750,660 | 795,127 | |

| Total liabilities | 1,202,434 | 1,337,193 | |

| Equity | |||

| Class A shares of common stock | 371,793 | 365,701 | |

| Class B shares of common stock | 132,915 | 132,915 | |

| Additional paid-in capital | 10,584 | 15,974 | |

| Retained earnings | 223,531 | 244,791 | |

| Accumulated other comprehensive losses | (355,243) | (302,467) | |

| Total Arcos Dorados Holdings Inc shareholders’ equity | 383,580 | 456,914 | |

| Non-controlling interest in subsidiaries | 656 | 673 | |

| Total equity | 384,236 | 457,587 | |

| Total liabilities and equity | 1,586,670 | 1,794,780 | |

(1) Includes "Other receivables", "Inventories", "Prepaid expenses and other current assets", "Deferred income taxes", and "Collateral deposits".

(2) Includes "Miscellaneous", "Collateral deposits", "Derivative instruments" and "McDonald´s Corporation indemnification for contingencies".

(3) Includes "Income taxes payable" and "Other taxes payable".

(4) Includes "Royalties payable to McDonald´s Corporation" and "Interest payable".

(5) Includes "Short-term debt", "Current portion of long-term debt" and "Derivative instruments".

(6) Includes "Long-term debt, excluding current portion".

17

Consolidated Financial Ratios

(In thousands of U.S. dollars, except ratios)

| Figure

13. Consolidated Financial Ratios (In thousands of U.S. dollars, except ratios) |

||

| June 30 | December 31 | |

| 2015 | 2014 | |

| Cash & cash equivalents | 83,181 | 139,030 |

| Total Financial Debt (i) | 755,077 | 801,205 |

| Net Financial Debt (ii) | 671,896 | 662,175 |

| Total Financial Debt / LTM Adjusted EBITDA ratio | 3.1 | 3.2 |

| Net Financial Debt / LTM Adjusted EBITDA ratio | 2.8 | 2.6 |

(i)Total financial debt includes short-term debt, long-term

debt and derivative instruments (including the asset portion of derivatives amounting to $16.6 million and $9.5 million as a reduction

of financial debt as of June 30, 2015 and December 31, 2014, respectively).

(ii) Total financial debt less cash and cash equivalents.

18