| Oppenheimer SteelPath MLP Income Fund | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Oppenheimer SteelPath MLP Income Fund |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Investment Objectives/Goals |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The investment objective of Oppenheimer SteelPath MLP Income Fund (the “Fund” or “Income Fund”) is to generate a high level of inflation-protected current income, primarily through investments in the larger, more liquid energy Master Limited Partnerships (“MLPs”). |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Fees and Expenses of the Fund |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. You may qualify for front-end sales charge discounts if you and your family invest, or agree to invest in the future, at least $50,000 in the Oppenheimer SteelPath Funds. More information about these and other discounts is available from your financial professional and in “The Funds’ Share Classes” starting on page 67 of this Prospectus and in “Additional Information Regarding Sales Charges” starting on page 60 of the Fund’s Statement of Additional Information. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Shareholder Fees (fees paid directly from your investment) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Example |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be: |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

You would pay the following expenses if you did not redeem your shares: |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Portfolio Turnover |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the fiscal year ended November 30, 2012, the Fund’s portfolio turnover rate was 29% of the average value of its portfolio. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Principal Investment Strategies of the Fund |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Under normal circumstances, the Fund seeks to achieve its investment objective by investing at least 90% of its net assets in the equity securities of MLPs. The MLP securities in which the Fund invests are common units representing limited partnership interests of energy infrastructure MLPs. The Fund principally invests in larger, more liquid energy MLPs that derive the majority of their revenue from energy infrastructure assets and energy related assets or activities, including businesses: (i) involved in the gathering, transporting, processing, treating, terminalling, storing, refining, distributing, mining or marketing of natural gas, natural gas liquids, crude oil, refined products or coal (“Midstream MLPs”), (ii) primarily engaged in the acquisition, exploitation and development of crude oil, natural gas and natural gas liquids (“Upstream MLPs”), (iii) that process, treat, and refine natural gas liquids and crude oil (“Downstream MLPs”), and (iv) engaged in owning, managing, and transporting alternative energy infrastructure assets, including alternative fuels such as ethanol, hydrogen and biodiesel (“Other Energy MLPs”). While the Fund principally invests in larger, more liquid MLPs, it may invest in MLPs of all market capitalization ranges. The Fund also may invest in securities issued by open- and closed-end investment companies, including money market funds, and the retail shares of actively managed and index exchange-traded funds (“ETFs”), as well as cash and cash equivalents. The Fund is non-diversified, which means that it may invest in a limited number of issuers.

MLPs are publicly traded partnerships engaged in the transportation, storage, processing, refining, marketing, exploration, production, and mining of minerals and natural resources. By confining their operations to these specific activities, their interests, or units, are able to trade on public securities exchanges exactly like the shares of a corporation, without entity level taxation. Of the MLPs that the Advisor follows, approximately two-thirds trade on the New York Stock Exchange (“NYSE”) and the rest trade on the NYSE Amex Equities (“Amex”) or NASDAQ Stock Market (“NASDAQ”). MLPs’ disclosures are regulated by the Securities and Exchange Commission (“SEC”) and MLPs must file Form 10-Ks, Form 10-Qs, and notices of material changes like any publicly traded corporation. The Fund provides access to a product that issues a single Form 1099 to its shareholders thereby removing the obstacles of federal and state filings (because shareholders do not receive any Schedule K-1) and, for certain tax-exempt shareholders, unrelated business taxable income (“UBTI”) filings, while providing portfolio transparency, liquidity and daily net asset value (“NAV”).

The Advisor relies on its disciplined investment process in determining investment selection and weightings. This process includes a comparison of quantitative and qualitative value factors that are developed through the Advisor’s proprietary analysis and valuation models. To determine whether an investment meets its criteria, the Advisor generally will perform a detailed fundamental analysis of the underlying businesses owned and operated by potential MLP portfolio companies. The Advisor seeks to invest in MLPs which have, among other characteristics, sound business fundamentals, a strong record of cash flow growth, distribution continuity, a solid business strategy, a respected management team and which are not overly exposed to changes in commodity prices. The Advisor will sell investments if it determines that any of the above-mentioned characteristics have changed materially from its initial analysis, or that quantitative or qualitative value factors indicate that an investment is no longer earning a return commensurate with its risk.

Through this process, the Advisor seeks to manage the Fund’s portfolio to include MLPs that produce the greatest potential for the Advisor to achieve a high level of inflation protected current income and modest capital appreciation over the long-term. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Principal Risks of Investing in the Fund |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

The Fund’s principal risks are discussed below. The value of the Fund’s investments may increase or decrease, sometimes dramatically, which will cause the value of the Fund’s shares to increase or decrease. As a result, you may lose money on your investment in the Fund, and there can be no assurance that the Fund will achieve its investment objective. The Fund is not a complete investment program.

Concentration Risk. Under normal circumstances, the Fund concentrates its investments in MLPs and the energy infrastructure industry. A fund that invests primarily in a particular sector could experience greater volatility than funds investing in a broader range of industries.

Deferred Tax Risk. The Fund is classified for federal tax purposes as a taxable regular corporation or so-called Subchapter “C” corporation. As a “C” corporation, the Fund is subject to U.S. federal income tax on its taxable income at the graduated rates applicable to corporations (currently at a maximum rate of 35%) as well as state and local income taxes. An investment strategy whereby a fund elects to be taxed as a regular corporation, or “C” corporation, rather than as a regulated investment company for U.S. federal income tax purposes, is a relatively recent strategy for open-end registered investment companies such as the Fund. This strategy involves complicated accounting, tax, NAV and share valuation aspects that would cause the Fund to differ significantly from most other open-end registered investment companies. This could result in unexpected and potentially significant accounting, tax and valuation consequences for the Fund and for its shareholders. In addition, accounting, tax and valuation practices in this area are still developing, and there may not always be a clear consensus among industry participants as to the most appropriate approach. This could result in changes over time in the practices applied by the Fund, which, in turn, could have significant adverse consequences on the Fund and it shareholders.

As a “C” corporation, the Fund accrues deferred income taxes for any future tax liability associated with (i) that portion of MLP distributions considered to be a tax-deferred return of capital and for any net operating gains as well as (ii) capital appreciation of its investments. The Fund’s accrued deferred tax liability will be reflected each day in the Fund’s NAV. The Fund’s current and deferred tax liability, if any, will depend upon the Fund’s net investment gains and losses and realized and unrealized gains and losses on investments and therefore may vary greatly from year to year and from day to day depending on the nature of the Fund’s investments, the performance of those investments and general market conditions. The Fund will rely to some extent on information provided by the MLPs, which may not be timely, to estimate deferred tax liability and/or asset balances. From time to time, the Fund may modify the estimates or assumptions regarding its deferred tax liability and/or asset balances as new information becomes available. The Fund’s estimates regarding its deferred tax liability and/or asset balances are made in good faith; however, the daily estimate of the Fund’s deferred tax liability and/or asset balances used to calculate the Fund’s NAV may vary dramatically from the Fund’s actual tax liability.

The following example illustrates two hypothetical trading days of the Fund and the tax effect upon the daily NAV compared to the individual securities. The examples assume a 36.7% deferred tax calculation (maximum corporate tax rate of 35% in effect for 2012 plus estimated state tax rate of 1.7%, net of federal benefit). They do not reflect the impact, if any, of any valuation allowances on deferred tax assets that management may deem appropriate.

Deferred Tax Calculation

Actual income tax expense, if any, will be incurred over many years, depending upon whether and when investment gains and losses are realized, the then-current basis of the Fund’s assets and other factors. Upon the sale of an MLP security, the Fund will be liable for previously deferred taxes, if any. As a result, the Fund’s actual tax liability could have a material impact on the Fund’s NAV.

Equity Securities of MLPs Risk. MLP common units, like other equity securities, can be affected by macro-economic and other factors affecting the stock market in general, expectations of interest rates, investor sentiment towards an issuer or certain market sector, changes in a particular issuer’s financial condition, or unfavorable or unanticipated poor performance of a particular issuer (in the case of MLPs, generally measured in terms of distributable cash flow). Prices of common units of individual MLPs, like the prices other equity securities, also can be affected by fundamentals unique to the partnership or company, including earnings power and coverage ratios.

Industry Specific Risk. The MLPs in which the Fund invests also are subject to risks specific to the industry they serve, including the following:

Investment Companies and ETFs Risk. Investments in the securities of ETFs and other investment companies, including money market funds, may involve duplication of advisory fees and certain other expenses. By investing in an ETF or another investment company, a Fund becomes a shareholder of that ETF or other investment company. As a result, Fund shareholders indirectly bear a Fund’s proportionate share of the fees and expenses paid by the ETF or other investment company, in addition to the fees and expenses Fund shareholders directly bear in connection with the Fund’s own operations. As a shareholder, a Fund must rely on the ETF or other investment company to achieve its investment objective. If the ETF or other investment company fails to achieve its investment objective, the value of a Fund’s investment will decline, adversely affecting the Fund’s performance. In addition, because ETFs are listed on national stock exchanges and are traded like stocks listed on an exchange, ETF shares potentially may trade at a discount or a premium. Investments in ETFs are also subject to brokerage and other trading costs, which could result in greater expenses to a Fund. Additionally, despite the short maturities and high credit quality of a money market fund’s investments, increases in interest rates and deteriorations in the credit quality of the instruments a Fund has purchased may reduce the Fund’s yield and can cause the price of a money market security to decrease.

Issuer Risk. The value of a security may decline for a number of reasons which directly relate to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s products or services.

Liquidity Risk. Although common units of MLPs trade on the NYSE, Amex, and NASDAQ, certain MLP securities may trade less frequently than those of larger companies due to their smaller capitalizations. In the event certain MLP securities experience limited trading volumes, the prices of such MLPs may display abrupt or erratic movements at times. Additionally, it may be more difficult for the Fund to buy and sell significant amounts of such securities without an unfavorable impact on prevailing market prices. As a result, these securities may be difficult to dispose of at a fair price at the times when the Advisor believes it is desirable to do so. The Fund’s investment in securities that are less actively traded or over time experience decreased trading volume may restrict its ability to take advantage of other market opportunities or to dispose of securities. This also may affect adversely the Fund’s ability to make dividend distributions to you. The Fund will not purchase or otherwise acquire any security if, as a result, more than 15% of its net assets would be invested in illiquid investments.

Market Risk. The securities markets may move down, sometimes rapidly and unpredictably, based on overall economic conditions and other factors. The market value of a security may decline due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. A security’s market value also may decline because of factors that affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry.

MLP Risk. Investments in securities of MLPs involve risks that differ from investments in common stock, including risks related to limited control and limited rights to vote on matters affecting the MLP, risks related to potential conflicts of interest between the MLP and the MLP’s general partner, cash flow risks, dilution risks and risks related to the general partner’s right to require unit holders to sell their common units at an undesirable time or price.

MLP Tax Risk. MLPs do not pay U.S. federal income tax at the partnership level. Rather, each partner is allocated a share of the partnership’s income, gains, losses, deductions and expenses. A change in current tax law, or a change in the underlying business mix of a given MLP, could result in an MLP being treated as a corporation for U.S. federal income tax purposes, which would result in such MLP being required to pay U.S. federal income tax on its taxable income. The classification of an MLP as a corporation for U.S. federal income tax purposes would have the effect of reducing the amount of cash available for distribution by the MLP. Thus, if any of the MLPs owned by the Fund were treated as a corporation for U.S. federal income tax purposes, it could result in a reduction in the value of the Fund’s investment, and consequently your investment in the Fund and lower income.

Non-Diversification Risk. The Fund is a non-diversified investment company under the 1940 Act. Accordingly, the Fund may invest a greater portion of its assets in a more limited number of issuers than a diversified fund. An investment in the Fund may present greater risk to an investor than an investment in a diversified portfolio because changes in the financial condition or market assessment of a single issuer, or the effects of a single economic, political or regulatory event, may cause greater fluctuations in the value of the Fund’s shares.

Regulatory Risk. The Fund is subject to the risk that changes in the laws, regulations and/or related interpretations relating to the Fund’s tax treatment as a “C” corporation or investments in MLPs or other instruments could increase the Fund’s expenses or otherwise impact a Fund’s ability to implement its investment strategy.

Reliance on the Advisor Risk. The Fund’s ability to achieve its investment objective is dependent on the Advisor’s ability to identify profitable investment opportunities for the Fund. The Advisor was established in 2009 and neither the Advisor nor the portfolio managers responsible for managing the Fund’s portfolio had managed a mutual fund prior to that time. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Past Performance |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

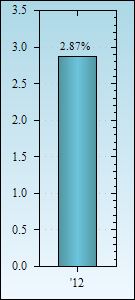

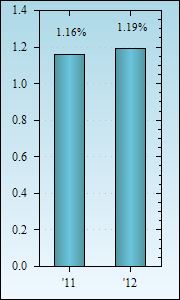

The accompanying bar chart and table provide an indication of the risks of investing in the Fund. The bar chart below shows how the total return of the Fund’s Class Y shares have varied from year to year. The returns in the bar chart do not reflect any applicable sales charges. If sales charges were reflected, returns would be lower than those shown. The table shows the average annual total returns of each class of the Fund that has been in operation for at least one full calendar year, and also compares the Fund’s performance with the average annual total returns of a broad-based market index. Unlike the returns in the bar chart, the returns in the table reflect the maximum applicable sales charges.

The performance data quoted here represents past performance. Past performance is no guarantee of future results. Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end please call 888.614.6614. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Oppenheimer SteelPath MLP Income Fund For the calendar year ended December 31 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Calendar Year ended December 31

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Average annual total returns (for periods ended December 31, 2012) |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The after-tax returns are shown only for Class Y shares, are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and the after-tax returns shown are not relevant to investors who hold their fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns for classes other than Class Y will vary from returns shown for Class Y. Performance information for Class I shares (first offered June 28, 2013) will be provided after those shares have one full calendar year of performance. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||