UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

for the fiscal year ended December 31, 2013.

or

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

for the transition period from to .

Commission file number: 001-34371

United States Short Oil Fund, LP

(Exact name of registrant as specified in its charter)

| Delaware | 26-2939256 | |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

1999 Harrison Street, Suite 1530

Oakland, California 94612

(Address of principal executive offices) (Zip code)

(510) 522-9600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Shares of United States Short Oil Fund, LP | NYSE Arca, Inc. | |

| (Title of each class) | (Name of exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

The aggregate market value of the registrant’s shares held by non-affiliates of the registrant as of June 30, 2013 was: $18,065,000.

The registrant had 350,00 outstanding shares as of March 24, 2014.

DOCUMENTS INCORPORATED BY REFERENCE:

None.

UNITED STATES SHORT OIL FUND, LP

Table of Contents

| Page | ||

| Part I. | ||

| Item 1. Business. | 1 | |

| Item 1A. Risk Factors. | 28 | |

| Item 1B. Unresolved Staff Comments. | 38 | |

| Item 2. Properties. | 38 | |

| Item 3. Legal Proceedings. | 39 | |

| Item 4. Mine Safety Disclosures. | 39 | |

| Part II. | ||

| Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. | 39 | |

| Item 6. Selected Financial Data. | 40 | |

| Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. | 40 | |

| Item 7A. Quantitative and Qualitative Disclosures About Market Risk. | 59 | |

| Item 8. Financial Statements and Supplementary Data. | 61 | |

| Item 9. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure. | 98 | |

| Item 9A. Controls and Procedures. | 98 | |

| Item 9B. Other Information. | 98 | |

| Part III. | ||

| Item 10. Directors, Executive Officers and Corporate Governance. | 98 | |

| Item 11. Executive Compensation. | 103 | |

| Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | 103 | |

| Item 13. Certain Relationships and Related Transactions, and Director Independence. | 104 | |

| Item 14. Principal Accountant Fees and Services. | 104 | |

| Part IV. | ||

| Item 15. Exhibits and Financial Statement Schedules. | 105 | |

| Exhibit Index. | 105 | |

| Signatures. | 107 |

Part I

| Item 1. | Business. |

What is DNO?

The United States Short Oil Fund, LP (“DNO”) is a Delaware limited partnership organized on June 30, 2008. DNO maintains its main business office at 1999 Harrison Street, Suite 1530, Oakland, California 94612. DNO is a commodity pool that issues limited partnership interests (“shares”) traded on the NYSE Arca, Inc. (the “NYSE Arca”). It operates pursuant to the terms of the Second Amended and Restated Agreement of Limited Partnership dated as of March 1, 2013 (as amended from time to time, the “LP Agreement”), which grants full management control to its general partner, United States Commodity Funds LLC (“USCF”).

The investment objective of DNO is for the daily changes in percentage terms of its shares’ per share net asset value (“NAV”) to inversely reflect the daily changes in percentage terms of the spot price of West Texas Intermediate (“WTI”) light, sweet crude oil delivered to Cushing, Oklahoma, as measured by the daily changes in the price of the futures contract for WTI light, sweet crude oil traded on the New York Mercantile Exchange (the “NYMEX”), that is the near month contract to expire, except when the near month contract is within two weeks of expiration, in which case it will be measured by the futures contract that is the next month contract to expire (the “Benchmark Futures Contract”), less DNO’s expenses. It is not the intent of DNO to be operated in a fashion such that the per share NAV will equal, in dollar terms, the inverse of the spot price of WTI light, sweet crude oil or any particular futures contract based on WTI light, sweet crude oil. It is not the intent of DNO to be operated in a fashion such that its per share NAV will reflect the inverse of the percentage change of the price of any particular futures contract as measured over a time period greater than one day. USCF believes that it is not practical to manage the portfolio to achieve such an investment goal when investing in Futures Contracts (as defined below) and Other Crude Oil-Related Investments (as defined below). DNO’s shares began trading on September 24, 2009. USCF is the general partner of DNO and is responsible for the management of DNO.

Who is USCF?

USCF is a single member limited liability company that was formed in the state of Delaware on May 10, 2005. USCF maintains its main business office at 1999 Harrison Street, Suite 1530, Oakland, California 94612. USCF is a wholly-owned subsidiary of Wainwright Holdings, Inc., a Delaware corporation (“Wainwright”). Mr. Nicholas Gerber (discussed below) controls Wainwright by virtue of his ownership or control of a majority of Wainwright’s shares. Wainwright is a holding company that previously owned an insurance company organized under Bermuda law (which has been liquidated) and a registered investment adviser firm named Ameristock Corporation, which has been distributed to the Wainwright shareholders. USCF is a member of the National Futures Association (the “NFA”) and registered as a commodity pool operator (“CPO”) with the Commodity Futures Trading Commission (the “CFTC”) on December 1, 2005 and as a Swaps Firm on August 8, 2013.

USCF also serves as general partner or sponsor of the United States Oil Fund, LP (“USO”), the United States Natural Gas Fund, LP (“UNG”), the United States 12 Month Oil Fund, LP (“USL”), the United States Gasoline Fund, LP (“UGA”), the United States Diesel-Heating Oil Fund, LP (“UHN”), the United States 12 Month Natural Gas Fund, LP (“UNL”), the United States Brent Oil Fund, LP (“BNO”), the United States Commodity Index Fund (“USCI”), the United States Copper Index Fund (“CPER”), the United States Agriculture Index Fund (“USAG”) and the United States Metals Index Fund (“USMI”). USO, UNG, USL, UGA, UHN, UNL, BNO, USCI, CPER, USAG and USMI are actively operating funds and all are listed on the NYSE Arca. All funds listed previously are referred to collectively herein as the “Related Public Funds.” The Related Public Funds are subject to reporting requirements under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). For more information about each of the Related Public Funds, investors in DNO may call 1.800.920.0259 or visit www.unitedstatescommodityfunds.com or the U.S. Securities and Exchange Commission’s (the “SEC”) website at www.sec.gov.

| 1 |

USCF previously filed registration statements to register shares of the United States Sugar Fund (“USSF”), the United States Natural Gas Double Inverse Fund (“UNGD”), the United States Gasoil Fund (“USGO”) and the United States Asian Commodities Basket Fund (“UAC”), each of which is a series of the United States Commodity Funds Trust I, and the US Golden Currency Fund (“HARD”), a series of the United States Currency Funds Trust. On December 30, 2013, USCF withdrew the registration statements for USSF, UNGD, USGO and UAC effective December 31, 2013. On January 27, 2014, USCF withdrew the registration statement for HARD. HARD was never available to the public and at the time of withdrawal, HARD was still in the process of review by various regulatory agencies which have regulatory authority over USCF and HARD.

USCF is required to evaluate the credit risk of DNO to the futures commission merchant (“FCM”), oversee the purchase and sale of DNO’s shares by certain authorized purchasers (“Authorized Purchasers”), review daily positions and margin requirements of DNO and manage DNO’s investments. USCF also pays the fees of ALPS Distributors, Inc., which serves as the marketing agent for DNO (the “Marketing Agent”), and Brown Brothers Harriman & Co. (“BBH&Co.”), which serves as the administrator (the “Administrator”) and the custodian (the “Custodian”) for DNO.

Limited partners have no right to elect USCF as the general partner on an annual or any other continuing basis. If USCF voluntarily withdraws as general partner, however, the holders of a majority of DNO’s outstanding shares (excluding for purposes of such determination shares owned, if any, by the withdrawing USCF and its affiliates) may elect its successor. USCF may not be removed as general partner except upon approval by the affirmative vote of the holders of at least 66 and 2/3 percent of DNO’s outstanding shares (excluding shares owned, if any, by USCF and its affiliates), subject to the satisfaction of certain conditions set forth in the LP Agreement.

The business and affairs of USCF are managed by a board of directors (the “Board”), which is comprised of three management directors (the “Management Directors”), some of whom are also its executive officers, and three independent directors who meet the independent director requirements established by the NYSE Arca Equities Rules and the Sarbanes-Oxley Act of 2002. The Management Directors have the authority to manage USCF pursuant to its LLC Agreement, as amended from time to time. Through its Management Directors, USCF manages the day-to-day operations of DNO. The Board has an audit committee which is made up of the three independent directors (Peter M. Robinson, Gordon L. Ellis and Malcolm R. Fobes III). For additional information relating to the audit committee, please see “Item 10. Directors, Executive Officers and Corporate Governance – Audit Committee” in this annual report on Form 10-K.

How Does DNO Operate?

An investment in the shares is intended to allow both retail and institutional investors to easily gain inverse or negative exposure to the crude oil market in a cost-effective manner. The shares are also expected to provide additional means for diversifying an investor’s investments or hedging exposure to changes in crude oil prices.

The net assets of DNO consist primarily of investments in short positions in futures contracts for WTI light, sweet crude oil, other types of crude oil, diesel-heating oil, gasoline, natural gas and other petroleum-based fuels that are traded on the NYMEX, ICE Futures or other U.S. and foreign exchanges (collectively, “Futures Contracts”) and, to a lesser extent, in order to comply with regulatory requirements or in view of market conditions, other crude oil-related investments such as cash-settled options on Futures Contracts, forward contracts for crude oil, cleared swap contracts and non-exchange traded (“over-the-counter”) transactions that are based on the price of crude oil and other petroleum-based fuels, Futures Contracts and indices based on the foregoing (collectively, “Other Crude Oil-Related Investments”). Market conditions that USCF currently anticipates could cause DNO to invest in Other Crude Oil-Related Investments include those allowing DNO to obtain greater liquidity or to execute transactions with more favorable pricing. For convenience and unless otherwise specified, Futures Contracts and Other Crude Oil-Related Investments collectively are referred to as “Crude Oil Interests” in this annual report on Form 10-K. DNO invests substantially the entire amount of its assets in Futures Contracts while supporting such investments by holding the amounts of its margin, collateral and other requirements relating to these obligations in short-term obligations of the United States of two years or less (“Treasuries”), cash and cash equivalents. The daily holdings of DNO are available on DNO’s website at www.unitedstatescommodityfunds.com.

| 2 |

The investment objective of DNO is for the daily changes in percentage terms of its shares’ per share NAV to inversely reflect the daily changes in percentage terms of the spot price of WTI light, sweet crude oil delivered to Cushing, Oklahoma, as measured by the daily changes in the price of the futures contract on light, sweet crude oil traded on the NYMEX that is the near month contract to expire, except when the near month contract is within two weeks of expiration, in which case it will be measured by the futures contract that is the next month contract to expire (the “Benchmark Futures Contract”), less DNO’s expenses. It is not the intent of DNO to be operated in a fashion such that its per share NAV will equal, in dollar terms, the inverse of the spot price of WTI light sweet crude oil or any particular futures contract based on WTI light sweet crude oil. It is not the intent of DNO to be operated in a fashion such that its per share NAV will reflect the inverse of the percentage change of the price of any particular futures contract as measured over a time period greater than one day. DNO may invest in interests other than the Benchmark Futures Contract (as defined below) to comply with accountability levels and position limits. For a detailed discussion of accountability levels and position limits, see “Item 1. Business – What are Futures Contracts?” below in this annual report on Form 10-K.

USCF employs a “neutral” investment strategy in order to inversely track changes in the price of the Benchmark Futures Contract regardless of whether the price goes up or goes down. DNO’s “neutral” investment strategy is designed to permit investors generally to purchase and sell DNO’s shares for the purpose of taking short positions indirectly in crude oil in a cost-effective manner, and/or to permit participants in the crude oil or other industries to hedge the risk of losses in their crude oil-related transactions. Accordingly, depending on the investment objective of an individual investor, the risks generally associated with taking short positions in crude oil and/or the risks involved in hedging may exist. In addition, an investment in DNO involves the risk that the changes in the price of DNO’s shares will not accurately track the inverse of the changes in the Benchmark Futures Contract and that changes in the Benchmark Futures Contract will not closely correlate with the inverse of changes in the spot price of WTI light sweet crude oil.

The Benchmark Futures Contract is changed from the near month contract to the next month contract over a four-day period. Each month the Benchmark Futures Contract changes starting at the end of the day on the date two weeks prior to expiration of the near month contract for that month. During the first three days of the period, the applicable value of the Benchmark Futures Contract is based on a combination of the near month contract and the next month contract as follows: (1) day 1 consists of 75% of the then near month contract’s price plus 25% of the price of the next month contract, divided by 75% of the near month contract’s prior day’s price plus 25% of the price of the next month contract, (2) day 2 consists of 50% of the then near month contract’s price plus 50% of the price of the next month contract, divided by 50% of the near month contract’s prior day’s price plus 50% of the price of the next month contract, and (3) day 3 consists of 25% of the then near month contract’s price plus 75% of the price of the next month contract, divided by 25% of the near month contract’s prior day’s price plus 75% of the price of the next month contract. On day 4, the Benchmark Futures Contract is the next month contract to expire at that time and that contract remains the Benchmark Futures Contract until the beginning of the following month’s change in the Benchmark Futures Contract over a four-day period.

On each day during the four-day period, USCF anticipates it will “roll” DNO’s positions in Crude Oil Interests by closing, or selling, a percentage of DNO’s positions in Crude Oil Interests and reinvesting the proceeds from closing those positions in new Crude Oil Interests that reflect the change in the Benchmark Futures Contract.

The anticipated dates that the monthly four-day roll period will commence are posted on DNO’s website at www.unitedstatescommodityfunds.com, and are subject to change without notice.

DNO’s total portfolio composition is disclosed on its website each business day that the NYSE Arca is open for trading. The website disclosure of portfolio holdings is made daily and includes, as applicable, the name and value of each Crude Oil Interest, the specific types of Other Crude Oil-Related Investments and characteristics of such Other Crude Oil-Related Investments, the name and value of each Treasury and cash equivalent, and the amount of cash held in DNO’s portfolio. DNO’s website is publicly accessible at no charge. DNO’s assets used for margin and collateral are held in segregated accounts pursuant to the Commodity Exchange Act (the “CEA”) and CFTC regulations.

Effective February 29, 2012, the shares issued by DNO may only be purchased by Authorized Purchasers and only in blocks of 50,000 shares called Creation Baskets. The amount of the purchase payment for a Creation Basket is equal to the aggregate NAV of the shares in the Creation Basket. Similarly, only Authorized Purchasers may redeem shares and only in blocks of 50,000 shares called Redemption Baskets. Prior to February 29, 2012, Authorized Purchasers could only purchase or redeem shares in blocks of 100,000 shares. The amount of the redemption proceeds for a Redemption Basket is equal to the aggregate NAV of shares in the Redemption Basket. The purchase price for Creation Baskets and the redemption price for Redemption Baskets are the actual NAV calculated at the end of the business day when a request for a purchase or redemption is received by DNO. The NYSE Arca publishes an approximate per share NAV intra-day based on the prior day’s per share NAV and the current price of the Benchmark Futures Contract, but the price of Creation Baskets and Redemption Baskets is determined based on the actual per share NAV calculated at the end of the day.

| 3 |

While DNO issues shares only in Creation Baskets, shares are listed on the NYSE Arca and investors may purchase and sell shares at market prices like any listed security.

What is DNO’s Investment Strategy?

In managing DNO’s assets, USCF does not use a technical trading system that issues buy and sell orders. USCF instead employs a quantitative methodology whereby each time a Creation Basket is sold, USCF takes corresponding short positions in Crude Oil Interests, such as the Benchmark Futures Contract, that have an aggregate market value that approximates the amount of Treasuries and/or cash received upon the issuance of the Creation Basket.

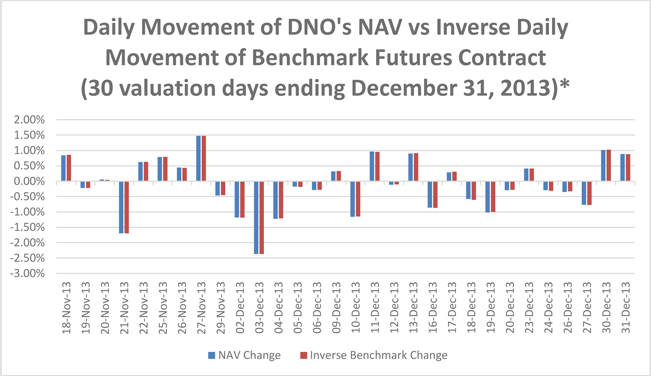

By remaining invested as fully as possible in short positions in Futures Contracts or Other Crude Oil-Related Investments, USCF believes that the daily changes in percentage terms in DNO’s NAV will continue to closely inversely track the daily changes in percentage terms in the price of the Futures Contracts. USCF believes that certain arbitrage opportunities result in the price of the shares traded on the NYSE Arca closely tracking the per share NAV of DNO. Additionally, Futures Contracts traded on the NYMEX have closely tracked the spot price of crude oil. Based on these expected interrelationships, USCF believes that the daily changes in the price of DNO’s shares traded on the NYSE Arca have closely tracked and will continue to closely track the inverse of the daily changes in the spot price of WTI light, sweet crude oil. For performance data relating to DNO’s ability to track benchmark, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Tracking DNO’s Benchmark” in this annual report on Form 10-K.

USCF endeavors to place DNO’s trades in Futures Contracts and Other Crude Oil-Related Investments and otherwise manage DNO’s investments so that “A” will be within plus/minus 10 percent of “B”, where:

| • | A is the average daily change in DNO’s per share NAV for any period of 30 successive valuation days; i.e., any NYSE Arca trading day as of which DNO calculates its NAV; and | ||

| • | B is the inverse of the average daily percentage change in the price of the Benchmark Futures Contract over the same period. |

USCF believes that market arbitrage opportunities will cause the daily changes in DNO’s share price on the NYSE Arca to closely track the inverse of the daily changes in DNO’s NAV per share. USCF believes that the net effect of these two expected relationships and the relationships described above between DNO’s NAV and the Benchmark Futures Contract will be that the daily changes in the price of DNO’s shares on the NYSE Arca will closely track, in percentage terms, the inverse of the daily changes in the spot price of WTI light, sweet crude oil, less DNO’s expenses. For performance data relating to DNO’s ability to track its benchmark, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Tracking DNO’s Benchmark” in this annual report on Form 10-K.

The specific Futures Contracts sold depend on various factors, including a judgment by USCF as to the appropriate diversification of DNO’s investments in futures contracts with respect to the month of expiration, and the prevailing price volatility of particular contracts. While USCF has made significant investments in NYMEX Futures Contracts, for various reasons, including the ability to enter into the precise amount of exposure to the crude oil market, position limits or other regulatory requirements limiting DNO’s holdings, and market conditions, it may invest in Futures Contracts traded on other exchanges or invest in Other Crude Oil-Related Investments. To the extent that DNO invests in Other Crude Oil-Related Investments, it would prioritize investments in contracts and instruments that are economically equivalent to the Benchmark Futures Contract, including cleared swaps that satisfy such criteria, and then, to a lesser extent, it would invest in other types of cleared swaps and other contracts, instruments and non-cleared swaps, such as swaps in the over-the-counter market. If DNO is required by law or regulation, or by one of its regulators, including a futures exchange, to reduce its position in the Futures Contracts to the applicable position limit or to a specified accountability level or if market conditions dictate it would be more appropriate to invest in Other Crude Oil-Related Investments, a substantial portion of DNO’s assets could be invested in accordance with such priority in Other Crude Oil-Related Investments that are intended to replicate the return on the Benchmark Futures Contract. As DNO’s assets reach higher levels, it is more likely to exceed position limits, accountability levels or other regulatory limits and, as a result, it is more likely that it will invest in accordance with such priority in Other Crude Oil-Related Investments at such higher levels. In addition, market conditions that USCF currently anticipates could cause DNO to invest in Other Crude Oil-Related Investments include those allowing DNO to obtain greater liquidity or to execute transactions with more favorable pricing. See “Item 1. Business – Regulation” in this annual report on Form 10-K for a discussion of the potential impact of regulation on DNO’s ability to invest in over-the-counter transactions and cleared swaps.

| 4 |

USCF may not be able to fully invest DNO’s assets in the Futures Contracts having an aggregate notional amount exactly equal to DNO’s NAV. For example, as standardized contracts, the Futures Contracts are for a specified amount of a particular commodity, and DNO’s NAV and the proceeds from the sale of a Creation Basket are unlikely to be an exact multiple of the amounts of those contracts. As a result, in such circumstances, DNO may be better able to achieve the exact amount of exposure to changes in price of the Benchmark Futures Contract through the use of Other Crude Oil-Related Investments, such as over-the-counter contracts that have better correlation with changes in price of the Benchmark Futures Contract.

DNO anticipates that to the extent it invests in Futures Contracts other than contracts on WTI light sweet crude oil (such as futures contracts for diesel-heating oil, natural gas, and other petroleum-based fuels) and Other Crude Oil-Related Investments, it will enter into various non-exchange-traded derivative contracts to hedge the short-term price movements of such Futures Contracts and Other Crude Oil-Related Investments against the current Benchmark Futures Contract.

USCF does not anticipate letting DNO’s Futures Contracts expire and taking, or making, delivery of the underlying commodity. Instead, USCF closes existing positions, e.g., when it changes the Benchmark Futures Contract or Other Crude-Oil Related Investments or it otherwise determines it would be appropriate to do so and reinvests the proceeds in new Futures Contracts or Other Crude-Oil Related Interests. Positions may also be closed out to meet orders for Redemption Baskets and in such case proceeds for such baskets will not be reinvested.

What is the Crude Oil Market and the Petroleum-Based Fuel Market?

DNO may take short positions in Futures Contracts traded on the NYMEX that are based on WTI light, sweet crude oil. It may also take short positions in contracts on other exchanges, including the ICE Futures and the Singapore Exchange. The contracts provide for delivery of several grades of domestic and internationally traded foreign crudes, and, among other things, serve the diverse needs of the physical market. In Europe, Brent crude oil is the standard for futures contracts and is primarily traded on the ICE Futures. Brent crude oil is the price reference for two-thirds of the world’s traded oil. The ICE Brent Futures is a deliverable contract with an option to cash settle which trades in units of 1,000 barrels (42,000 U.S. gallons). The ICE Futures also offers a WTI crude oil futures contract which trades in units of 1,000 barrels. The WTI crude oil futures contract is cash settled against the prevailing market price for U.S. light, sweet crude oil.

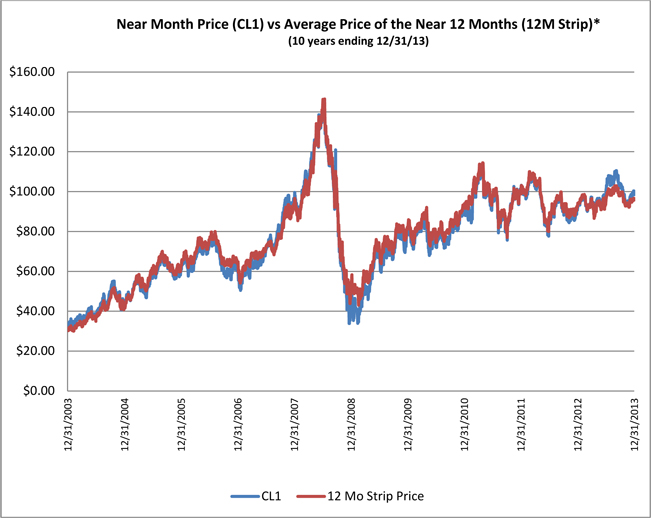

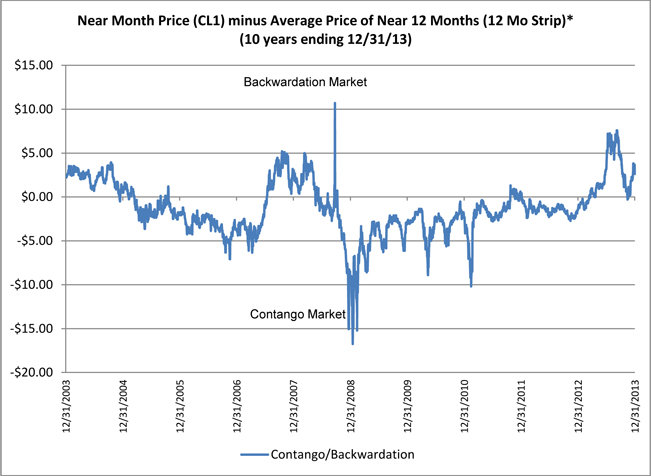

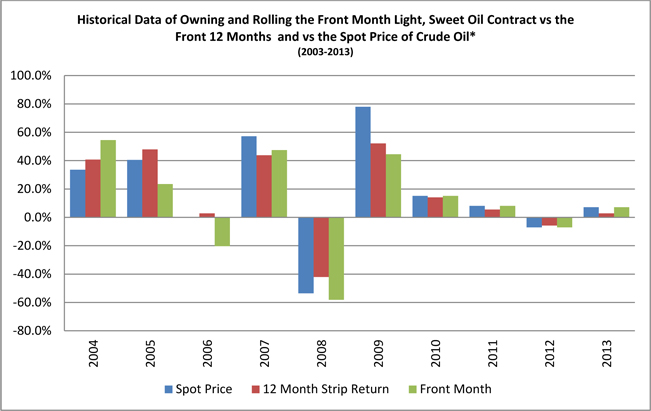

WTI Light, Sweet Crude Oil. Crude oil is the world’s most actively traded commodity. The futures contracts for WTI light, sweet crude oil that are traded on the NYMEX are the world’s most liquid forum for crude oil trading, as well as the world’s largest volume futures contract trading on a physical commodity. Due to the liquidity and price transparency of WTI light, sweet crude oil futures contracts, they are used as a principal international pricing benchmark. The futures contracts for WTI light, sweet crude oil trade on the NYMEX in units of 1,000 U.S. barrels and, if not closed out before maturity, will result in delivery of oil to Cushing, Oklahoma, which is also accessible to the international spot markets by two major interstate petroleum pipeline systems.

Demand for petroleum products by consumers, as well as agricultural, manufacturing and transportation industries, determines demand for crude oil by refiners. Since the precursors of product demand are linked to economic activity, crude oil demand will tend to reflect economic conditions. However, other factors such as weather also influence product and crude oil demand.

| 5 |

Crude oil supply is determined by both economic and political factors. Oil prices (along with drilling costs, availability of attractive prospects for drilling, taxes and technology, among other factors) determine exploration and development spending, which influence output capacity with a lag. In the short run, production decisions by the Organization of Petroleum Exporting Countries (“OPEC”) also affect supply and prices. Oil export embargoes and the current conflicts in the Middle East represent other routes through which political developments move the market. It is not possible to predict the aggregate effect of all or any combination of these factors.

Diesel-Heating Oil. Diesel-heating oil, also known as No. 2 fuel oil, accounts for 25% of the yield of a barrel of crude oil, the second largest “cut” from oil after gasoline. The heating oil futures contract listed and traded on the NYMEX trades in units of 42,000 gallons (1,000 barrels) and is based on delivery in the New York harbor, the principal cash market center. The ICE Futures also offers a Heating Oil Futures Contract which trades in units of 42,000 U.S. gallons (1,000 barrels). The Heating Oil Futures Contract is cash-settled against the prevailing market price for heating oil delivered to the New York Harbor.

Gasoline. Gasoline is the largest single volume refined product sold in the U.S. and accounts for almost half of national oil consumption. The gasoline futures contract listed and traded on the NYMEX trades in units of 42,000 gallons (1,000 barrels) and is based on delivery at petroleum products terminals in the New York harbor, the major East Coast trading center for imports and domestic shipments from refineries in the New York harbor area or from the Gulf Coast refining centers. The price of gasoline has historically been volatile.

Natural Gas. Natural gas accounts for almost a quarter of U.S. energy consumption. The natural gas futures contract listed and traded on the NYMEX trades in units of 10,000 million British thermal units and is based on delivery at the Henry Hub in Louisiana, the nexus of 16 intra- and interstate natural gas pipeline systems that draw supplies from the region’s prolific gas deposits. The pipelines serve markets throughout the U.S. East Coast, the Gulf Coast, the Midwest, and up to the Canadian border. The price of natural gas has historically been volatile.

What are Futures Contracts?

Futures Contracts are agreements between two parties. One party agrees to buy a commodity such as crude oil from the other party at a later date at a price and quantity agreed upon when the contract is made. Futures Contracts are traded on futures exchanges, including the NYMEX. For example, the Benchmark Futures Contract is traded on the NYMEX in units of 42,000 U.S. gallons (1,000 barrels). Futures Contracts traded on the NYMEX are priced by floor brokers and other exchange members both through an “open outcry” of offers to purchase or sell the contracts and through an electronic, screen-based system that determines the price by matching electronically offers to purchase and sell. Additional risks of investing in or taking short positions in Futures Contracts are included in “Item 1A. Risk Factors” in this annual report on Form 10-K.

Impact of Accountability Levels, Position Limits and Price Fluctuation Limits. Futures contracts include typical and significant characteristics. Most significantly, the CFTC and U.S. designated contract markets such as the NYMEX have established accountability levels and position limits on the maximum net long or net short futures contracts in commodity interests that any person or group of persons under common trading control (other than as a hedge, which an investment by DNO is not) may hold, own or control. The net position is the difference between an individual or firm’s open long contracts and open short contracts in any one commodity. In addition, most U.S.-based futures exchanges, such as the NYMEX, limit the daily price fluctuation for futures contracts. Currently, the ICE Futures imposes position and accountability limits that are similar to those imposed by U.S.-based futures exchanges and also limits the maximum daily price fluctuation, while some other non-U.S. futures exchanges have not adopted such limits.

The accountability levels for the Benchmark Futures Contract and other Futures Contracts traded on U.S. based futures exchanges, such as the NYMEX, are not a fixed ceiling, but rather a threshold above which the NYMEX may exercise greater scrutiny and control over an investor’s positions. The current accountability level for investments for any one-month in the Benchmark Futures Contract is 10,000 net contracts. In addition, the NYMEX imposes an accountability level for all months of 20,000 net futures contracts for WTI light, sweet crude oil. In addition, the ICE Futures maintains the same accountability levels, position limits and monitoring authority for its light, sweet crude oil contract as the NYMEX. If DNO and the Related Public Funds exceed these accountability levels for investments in the futures contract for WTI light, sweet crude oil, the NYMEX and ICE Futures will monitor such exposure and may ask for further information on their activities, including the total size of all positions, investment and trading strategy, and the extent of liquidity resources of DNO and the Related Public Funds. If deemed necessary by the NYMEX and/or ICE Futures, DNO could be ordered to reduce its aggregate position back to the accountability level. As of December 31, 2013, DNO held short positions in 104 Crude Oil Futures CL Contracts traded on the NYMEX. DNO did not hold short positions on ICE Futures as of December 31, 2013. For the year ended December 31, 2013, DNO did not exceed accountability levels on the NYMEX or ICE Futures.

| 6 |

Position limits differ from accountability levels in that they represent fixed limits on the maximum number of futures contracts that any person may hold and cannot allow such limits to be exceeded without express CFTC authority to do so. In addition to accountability levels and position limits that may apply at any time, the NYMEX and ICE Futures impose position limits on contracts held in the last few days of trading in the near month contract to expire. It is unlikely that DNO will run up against such position limits because DNO’s investment strategy is to close out its positions and “roll” from the near month contract to expire to the next month contract during a four-day period beginning two weeks from expiration of the contract. For the year ended December 31, 2013, DNO did not exceed any position limits imposed by the NYMEX and ICE Futures.

On November 5, 2013, the CFTC proposed a rulemaking that would establish specific limits on speculative positions in 28 physical commodity futures and option contracts as well as swaps that are economically equivalent to such contracts in the agriculture, energy and metals markets (the “Position Limit Rules”). On the same date, the CFTC proposed another rule addressing the circumstances under which market participants would be required to aggregate their positions with other persons under common ownership or control (the “Proposed Aggregation Requirements”). Specifically, the Position Limit Rules would, among other things: identify which contracts are subject to speculative position limits; set thresholds that restrict the number of speculative positions that a person may hold in a spot month, individual month, and all months combined; create an exemption for positions that constitute bona fide hedging transactions; impose responsibilities on designated contract markets (“DCMs”) and swap execution facilities (“SEFs”) to establish position limits or, in some cases, position accountability rules; and apply to both futures and swaps across four relevant venues: over-the-counter (“OTC”), DCMs, SEFs as well as non-U.S. located platforms. Furthermore, until such time as the Position Limit Rules are adopted, the regulatory architecture in effect prior to the adoption of the Position Limit Rules will govern transactions in commodities and related derivatives (collectively, “Referenced Contracts”). Under that system, the CFTC enforces federal limits on speculation in agricultural products (e.g., corn, wheat and soy), while futures exchanges enforce position limits and accountability levels for agricultural and certain energy products (e.g., oil and natural gas). As a result, DNO may be limited with respect to the size of its investments in any commodities subject to these limits. Finally, subject to certain narrow exceptions, the Position Limit Rules require the aggregation, for purposes of the position limits, of all positions in the 28 Referenced Contracts held by a single entity and its affiliates, regardless of whether such position existed on U.S. futures exchanges, non-U.S. futures exchanges, in cleared swaps or in over-the-counter swaps. Under the CFTC’s existing position limits requirements and the Position Limit Rules, a market participant is generally required to aggregate all positions for which that participant controls the trading decisions with all positions for which that participant has a 10 percent or greater ownership interest in an account or position, as well as the positions of two or more persons acting pursuant to an express or implied agreement or understanding. At this time, it is unclear how the Proposed Aggregation Requirements may affect DNO, but it may be substantial and adverse. By way of example, the Proposed Aggregation Requirements in combination with the Position Limit Rules may negatively impact the ability of DNO to meet its investment objectives through limits that may inhibit USCF’s ability to sell additional Creation Baskets of DNO. See “Commodity Interest Markets” – “Regulation” in this annual report on Form 10-K for additional information.

Price Volatility. The price volatility of Futures Contracts generally has been historically greater than that for traditional securities such as stocks and bonds. Price volatility often is greater day-to-day as opposed to intra-day. Futures Contracts tend to be more volatile than stocks and bonds because price movements for crude oil are more currently and directly influenced by economic factors for which current data is available and are traded by crude oil futures traders throughout the day. Because DNO invests a significant portion of its assets in short positions in Futures Contracts, the assets of DNO, and therefore the prices of DNO shares, may be subject to greater volatility than traditional securities.

| 7 |

Marking-to-Market Futures Positions. Futures Contracts are marked to market at the end of each trading day and the margin required with respect to such contracts is adjusted accordingly. This process of marking-to-market is designed to prevent losses from accumulating in any futures account. Therefore, if DNO’s futures positions have declined in value, DNO may be required to post “variation margin” to cover this decline. Alternatively, if DNO futures positions have increased in value, this increase will be credited to DNO’s account.

Why Does DNO Purchase and Sell Futures Contracts?

DNO’s investment objective is to have the daily changes in percentage terms of its shares’ per share NAV inversely reflect the daily changes in percentage terms of the spot price of WTI light, sweet crude oil delivered to Cushing, Oklahoma, as measured by the changes in the price of the futures contract on WTI light, sweet crude oil as traded on the NYMEX that is the near month contract to expire, except when the near month contract is within two weeks of expiration, in which case the futures contract will be the next month contract to expire, less DNO’s expenses. DNO seeks to have its aggregate NAV approximate at all times the aggregate market value of the Futures Contracts and Other Crude Oil-Related Investments it holds.

In connection with taking short positions in Futures Contracts and Other Crude Oil-Related Investments, DNO holds Treasuries, cash and/or cash equivalents that serve as segregated assets supporting DNO’s positions in Futures Contracts and Other Crude Oil-Related Investments. For example, the purchase of a Futures Contract with a notional value of $10 million would not require DNO to pay $10 million upon entering into the contract; rather, only a margin deposit, generally of 5% to 30% of the stated value of the Futures Contract, would be required. To secure its Futures Contract obligations, DNO would deposit the required margin with the FCM and would separately hold, through its Custodian or FCM, Treasuries, cash and/or cash equivalents in an amount equal to the balance of the current market value of the contract, which at the contract’s inception would be $10 million minus the amount of the margin deposit, or $8.5 million (assuming a 15% margin).

As a result of the foregoing, typically 5% to 30% of DNO’s assets are held as margin in segregated accounts with a FCM. In addition to the Treasuries and cash it posts with the FCM for the Futures Contracts it owns, DNO may hold, through the Custodian, Treasuries, cash and/or cash equivalents that can be posted as additional margin or as other collateral to support its over-the-counter contracts. DNO earns income from the Treasuries and/or cash equivalents that it purchases, and on the cash it holds through the Custodian or FCM. DNO anticipates that the earned income will increase the NAV and limited partners’ capital contribution accounts. DNO reinvests the earned income, holds it in cash, or uses it to pay its expenses. If DNO reinvests the earned income, it makes investments that are consistent with its investment objective.

What are the Trading Policies of DNO?

Liquidity

DNO invests only in Futures Contracts and Other Crude Oil-Related Investments that, in the opinion of USCF, are traded in sufficient volume to permit the ready taking and liquidation of positions in these financial interests and Other Crude Oil-Related Investments that, in the opinion of USCF, may be readily liquidated with the original counterparty or through a third party assuming the position of DNO.

Spot Commodities

While the WTI light sweet crude oil Futures Contracts traded on the NYMEX can be physically settled, DNO does not intend to take or make physical delivery. DNO may from time to time trade in Other Crude Oil-Related Investments, including contracts based on the spot price of crude oil.

Leverage

USCF endeavors to have the value of DNO’s Treasuries, cash and cash equivalents, whether held by DNO or posted as margin or other collateral, at all times approximate the aggregate market value of its obligations under its Futures Contracts and Other Crude Oil-Related Investments. Commodity pools’ trading positions in futures contracts or other related investments are typically required to be secured by the deposit of margin funds that represent only a small percentage of a futures contract’s (or other commodity interest’s) entire market value. While USCF has not and does not intend to leverage DNO’s assets, it is not prohibited from doing so under the LP Agreement.

| 8 |

Borrowings

Borrowings are not used by DNO unless DNO is required to borrow money in the event of physical delivery, DNO trades in cash commodities, or for short-term needs created by unexpected redemptions.

Over-the-Counter Derivatives (Including Spreads and Straddles)

In addition to Futures Contracts, there are also a number of listed options on the Futures Contracts on the principal futures exchanges. These contracts offer investors and hedgers another set of financial vehicles to use in managing exposure to the crude oil market. Consequently, DNO may purchase options on crude Futures Contracts on these exchanges in pursuing its investment objective.

In addition to the Futures Contracts and options on the Futures Contracts, there also exists an active non-exchange-traded market in derivatives tied to crude oil. These derivatives transactions (also known as over-the-counter contracts) are usually entered into between two parties in private contracts. Unlike most of the exchange-traded Futures Contracts or exchange-traded options on the Futures Contracts, each party to such contract bears the credit risk of the other party, i.e., the risk that the other party may not be able to perform its obligations under its contract. To reduce the credit risk that arises in connection with such contracts, DNO will generally enter into an agreement with each counterparty based on the Master Agreement published by the International Swaps and Derivatives Association, Inc. (“ISDA”) that provides for the netting of its overall exposure to its counterparty.

USCF assesses or reviews, as appropriate, the creditworthiness of each potential or existing counterparty to an over-the-counter contract pursuant to guidelines approved by USCF’s Board.

DNO may enter into certain transactions where an over-the-counter component is exchanged for a corresponding futures contract (“Exchange for Risk” or “EFR” transaction.) These EFR transactions may expose DNO to counterparty risk during the interim period between the execution of the over-the-counter component and the exchange for a corresponding futures contract. Generally, the counterparty risk from the EFR transaction will exist only on the day of execution.

DNO may employ spreads or straddles in its trading to mitigate the differences in its investment portfolio and its goal of tracking the price of the Benchmark Futures Contract. DNO would use a spread when it chooses to take simultaneous long and short positions in futures written on the same underlying asset, but with different delivery months.

During the 12 month reporting period ended December 31, 2013, DNO limited its derivatives activities to Futures Contracts and EFR transactions.

Pyramiding

DNO has not and will not employ the technique, commonly known as pyramiding, in which the speculator uses unrealized profits on existing positions as variation margin for the purchase or sale of additional positions in the same or another commodity interest.

Who are the Service Providers?

In its capacity as the Custodian for DNO, BBH&Co. may hold DNO’s Treasuries, cash and/or cash equivalents pursuant to a custodial agreement. BBH&Co. is also the registrar and transfer agent for the shares. In addition, in its capacity as Administrator for DNO, BBH&Co. performs certain administrative and accounting services for DNO and prepares certain SEC, NFA and CFTC reports on behalf of DNO. USCF pays BBH&Co.’s fees for these services.

| 9 |

BBH&Co.’s principal business address is 50 Post Office Square, Boston, MA 02110-1548. BBH&Co., a private bank founded in 1818, is neither a publicly held company nor insured by the Federal Deposit Insurance Corporation. BBH&Co. is authorized to conduct a commercial banking business in accordance with the provisions of Article IV of the New York State Banking Law, New York Banking Law §§160–181, and is subject to regulation, supervision, and examination by the New York State Department of Financial Services. BBH&Co. is also licensed to conduct a commercial banking business by the Commonwealths of Massachusetts and Pennsylvania and is subject to supervision and examination by the banking supervisors of those states.

DNO also employs ALPS Distributors, Inc. as the Marketing Agent. USCF pays the Marketing Agent an annual fee. In no event may the aggregate compensation paid to the Marketing Agent and any affiliate of USCF for distribution-related services in connection with the offering of shares exceed ten percent (10%) of the gross proceeds of the offering.

ALPS’s principal business address is 1290 Broadway, Suite 1100, Denver, CO 80203. ALPS is the marketing agent for DNO. ALPS is a broker-dealer registered with the Financial Industry Regulatory Authority (“FINRA”) and a member of the Securities Investor Protection Corporation.

On October 8, 2013, USCF entered into a Futures and Cleared Derivatives Transactions Customer Account Agreement with RBC Capital Markets, LLC (“RBC Capital” or “RBC”) to serve as DNO’s FCM, effective October 10, 2013. Prior to October 10, 2013, UBS Securities LLC (“UBS Securities”) was DNO’s FCM. This agreement requires RBC Capital to provide services to DNO, as of October 10, 2013, in connection with the purchase and sale of Futures Contracts and Other Crude Oil-Related Investments that may be purchased or sold by or through RBC Capital for DNO’s account. For the period October 10, 2013 and after, DNO pays RBC Capital commissions for executing and clearing trades on behalf of DNO. Prior to October 10, 2013, DNO paid UBS Securities commissions for executing and clearing trades on behalf of DNO.

RBC Capital’s primary address is 500 West Madison Street, Suite 2500, Chicago, Illinois 60661. UBS Securities’ principal business address is 677 Washington Blvd., Stamford, Connecticut 06901. From DNO’s commencement of trading to October 10, 2013, UBS Securities was a futures clearing broker for DNO. Effective October 10, 2013, RBC Capital became the futures clearing broker for DNO. Both RBC Capital and UBS Securities are registered in the U.S. with FINRA as a broker-dealer and with the CFTC as a FCM. RBC Capital and UBS Securities are members of various U.S. futures and securities exchanges.

RBC is a large broker-dealer subject to many different complex legal and regulatory requirements. As a result, certain of RBC’s regulators may from time to time conduct investigations, initiate enforcement proceedings and/or enter into settlements with RBC with respect to issues raised in various investigations. RBC complies fully with its regulators in all investigations being conducted and in all settlements it reaches. In addition, RBC is and has been subject to a variety of civil legal claims in various jurisdictions, a variety of settlement agreements and a variety of orders, awards and judgments made against it by courts and tribunals, both in regard to such claims and investigations. RBC complies fully with all settlements it reaches and all orders, awards and judgments made against it.

RBC has been named as a defendant in various legal actions, including arbitrations, class actions and other litigation including those described below, arising in connection with its activities as a broker-dealer. Certain of the actual or threatened legal actions include claims for substantial compensatory and/or punitive damages or claims for indeterminate amounts of damages. RBC is also involved, in other reviews, investigations and proceedings (both formal and informal) by governmental and self-regulatory agencies regarding RBC’s business, including among other matters, accounting and operational matters, certain of which may result in adverse judgments, settlements, fines, penalties, injunctions or other relief.

RBC contests liability and/or the amount of damages, as appropriate, in each pending matter. In view of the inherent difficulty of predicting the outcome of such matters, particularly in cases where claimants seek substantial or indeterminate damages or where investigations and proceedings are in the early stages, RBC cannot predict the loss or range of loss, if any, related to such matters; how or if such matters will be resolved; when they will ultimately be resolved; or what the eventual settlement, fine, penalty or other relief, if any, might be. Subject to the foregoing, RBC believes, based on current knowledge and after consultation with counsel, that the outcome of such pending matters will not have a material adverse effect on the consolidated financial condition of RBC.

| 10 |

On March 11, 2013, the New Jersey Bureau of Securities entered a consent order settling an administrative complaint against RBC, which alleged that RBC failed to follow its own procedures with respect to monthly account reviews and failed to maintain copies of the monthly account reviews with respect to certain accounts that James Hankins Jr. maintained at the firm in violation of N.J.S.A. 49:3-58(a)(2)(xi) and 49:3-59(b). Without admitting or denying the findings of fact and conclusions of law, RBC consented to a civil monetary penalty of $150,000 (of which $100,000 was suspended as a result of the firm’s cooperation) and to pay disgorgement of $300,000.

On May 2, 2012, the Massachusetts Securities Division entered a consent order settling an administrative complaint against RBC, which alleged that RBC recommended unsuitable products to its brokerage and advisory clients and failed to supervise its registered representatives’ sales of inverse and leveraged ETFs in violation of Section 204(a)(2) of the Massachusetts Uniform Securities Act (“MUSA”). Without admitting or denying the allegations of fact, RBC consented to permanently cease and desist from violations of MUSA, pay restitution of $2.9 million to the investors who purchased the inverse and leveraged ETFs and pay a civil monetary penalty of $250,000.

On September 27, 2011, the SEC commenced and settled an administrative proceeding against RBC for willful violations of Sections 17(a)(2) and 17(a)(3) of the 1933 Act for negligently selling collateralized debt obligations to five Wisconsin school districts despite concerns about the suitability of the product. The firm agreed to pay disgorgement of $6.6 million, prejudgment interest of $1.8 million, and a civil monetary penalty of $22 million.

On February 24, 2009, the SEC commenced and settled an administrative proceeding against RBC for willful violations of Section 15B(c)(1) of the 1934 Act and Municipal Securities Rulemaking Board Rules G-17, G-20 and G-27, related to municipal expenses in connection with ratings agency trips. The firm was censured and paid a civil monetary penalty of $125,000.

On June 9, 2009, the SEC commenced and settled a civil action against RBC for willful violations of Section 15(c) of the 1934 Act, in connection with auction rate securities (ARS). The firm agreed to repurchase ARS owned by certain retail customers and to use best efforts to provide ineligible customers opportunities to liquidate ARS, and other ancillary relief.

Please see RBC’s Form BD for more details.

RBC Capital will act only as clearing broker for DNO and as such will be paid commissions for executing and clearing trades on behalf of DNO. Prior to October 10, 2013, UBS Securities acted only as clearing broker for DNO and as such was paid commissions for executing and clearing trades on behalf of DNO. Neither RBC Capital nor UBS Securities has passed upon the adequacy or accuracy of this annual report on Form 10-K. Neither RBC Capital nor UBS Securities will act in any supervisory capacity with respect to USCF or participate in the management of USCF or DNO.

Neither RBC Capital nor UBS Securities is affiliated with DNO or USCF. Therefore, neither USCF nor DNO believes that there are any conflicts of interest with RBC Capital and UBS Securities or their trading principals arising from their acting as DNO’s FCM.

Currently, USCF does not employ commodity trading advisors for the trading of DNO contracts. USCF currently does, however, employ a trading advisor for USCI, CPER, USAG and USMI, SummerHaven Investment Management, LLC (“SummerHaven”). If, in the future, USCF does employ commodity trading advisors for DNO, it will choose each advisor based on arm’s-length negotiations and will consider the advisor’s experience, fees and reputation.

Fees of DNO

Fees and Compensation Arrangements with USCF and Non-Affiliated Service Providers(1)

| Service Provider | Compensation Paid by USCF | |

| BBH&Co., Custodian and Administrator |

Minimum amount of $75,000 annually for its custody, fund accounting and fund administration services rendered to all funds, as well as a $20,000 annual fee for its transfer agency services. In addition, an asset-based charge of (a) 0.06% for the first $500 million of DNO’s and the Related Public Funds’ combined net assets, (b) 0.0465% for DNO’s and the Related Public Funds’ combined net assets greater than $500 million but less than $1 billion, and (c) 0.035% once DNO’s and the Related Public Funds’ combined net assets exceed $1 billion.(2) | |

| ALPS Distributors, Inc., Marketing Agent | 0.06% on DNO’s assets up to $3 billion and 0.04% on DNO’s assets in excess of $3 billion. |

| (1) | USCF pays this compensation. |

| (2) | The annual minimum amount will not apply if the asset-based charge for all accounts in the aggregate exceeds $75,000. USCF also will pay transaction charge fees to BBH&Co., ranging from $7.00 to $15.00 per transaction for each Fund. |

| 11 |

Compensation to USCF

DNO is contractually obligated to pay USCF a management fee based on 0.60% per annum on its average daily total net assets. Fees are calculated on a daily basis (accrued at 1/365 of the applicable percentage of total net assets on that day) and paid on a monthly basis. Total net assets are calculated by taking the current market value of DNO’s total assets and subtracting any liabilities.

Fees and Compensation Arrangements between DNO and Non-Affiliated Service Providers(3)

| Service Provider | Compensation Paid by DNO | |

| UBS Securities LLC, Futures Commission Merchant | Approximately $3.50 per buy or sell; charges may vary | |

| RBC Capital Markets, LLC, Futures Commission Merchant | Approximately $3.50 per buy or sell; charges may vary |

| (3) | DNO pays this compensation. |

New York Mercantile Exchange Licensing Fee(4)

| Assets | Licensing Fee | ||

| Prior to October 19, 2011: | |||

| First $1,000,000,000 | 0.04% of NAV | ||

| After the first $1,000,000,000 | 0.02% of NAV | ||

| On and after October 20, 2011: | 0.015% on all net assets |

| (4) | Fees are calculated on a daily basis (accrued at 1/365 of the applicable percentage of NAV on that day) and paid on a monthly basis. DNO is responsible for its pro rata share of the assets held by DNO and the Related Public Funds, other than BNO, USCI, CPER, USAG and USMI. |

| 12 |

Expenses Paid or Accrued by DNO from Inception through December 31, 2013 in dollar terms:

| Expenses: | Amount in Dollar Terms | |||

| Amount Paid or Accrued to USCF: | $ | 378,024 | ||

| Amount Paid or Accrued in Portfolio Brokerage Commissions: | $ | 74,475 | ||

| Other Amounts Paid or Accrued(5): | $ | 800,195 | ||

| Total Expenses Paid or Accrued: | $ | 1,252,694 | ||

| Expenses Waived(6): | $ | (688,736 | ) | |

| Total Expenses Paid or Accrued Excluding Expenses Waived(6): | $ | 563,958 | ||

| (5) | Includes expenses relating to legal fees, auditing fees, printing expenses, licensing fees, tax reporting fees, prepaid insurance expenses and miscellaneous expenses and fees and expenses paid to the independent directors of USCF. |

| (6) | USCF has voluntarily agreed to pay certain expenses typically borne by DNO, to the extent that such expenses exceeded 0.15% (15 basis points) of DNO’s NAV, on an annualized basis, through at least June 30, 2014. USCF has no obligation to continue such payments into subsequent periods. |

Expenses Paid or Accrued by DNO from Inception through December 31, 2013 as a Percentage of Average Daily Net Assets:

| Expenses: | Amount as a Percentage of Average Daily Net Assets |

||

| Amount Paid or Accrued to USCF: | 0.60% annualized | ||

| Amount Paid or Accrued in Portfolio Brokerage Commissions: | 0.12% annualized | ||

| Other Amounts Paid or Accrued(7): | 1.27% annualized | ||

| Total Expenses Paid or Accrued: | 1.99% annualized | ||

| Expenses Waived(8): | (1.09)% annualized | ||

| Total Expenses Paid or Accrued Excluding Expenses Waived(8): | 0.90% annualized |

| (7) | Includes expenses relating to legal fees, auditing fees, printing expenses, licensing fees, tax reporting fees, prepaid insurance expenses and miscellaneous expenses and fees and expenses paid to the independent directors of USCF. |

| (8) | USCF has voluntarily agreed to pay certain expenses typically borne by DNO, to the extent that such expenses exceeded 0.15% (15 basis points) of DNO’s NAV, on an annualized basis, through at least June 30, 2014. USCF has no obligation to continue such payments into subsequent periods. |

Other Fees. DNO also pays the fees and expenses associated with its tax accounting and reporting requirements. These fees were approximately $140,000 for the fiscal year ended December 31, 2013. In addition, DNO is responsible for paying its portion of the directors’ and officers’ liability insurance for DNO and the Related Public Funds and the fees and expenses of the independent directors who also serve as audit committee members of DNO and the Related Public Funds organized as limited partnerships and, as of July 8, 2011, the Related Public Funds organized as a series of a Delaware statutory trust. DNO shares the fees and expenses on a pro rata basis with each Related Public Fund, as described above, based on the relative assets of each Related Public Fund computed on a daily basis. These fees and expenses for the year ended December 31, 2013 were $555,465 for DNO and the Related Public Funds. DNO’s portion of such fees and expenses for the year ended December 31, 2013 was $3,907.

Form of Shares

Registered Form. Shares are issued in registered form in accordance with the LP Agreement. The Administrator has been appointed registrar and transfer agent for the purpose of transferring shares in certificated form. The Administrator keeps a record of all limited partners and holders of the shares in certificated form in the registry (the “Register”). USCF recognizes transfers of shares in certificated form only if done in accordance with the LP Agreement. The beneficial interests in such shares are held in book-entry form through participants and/or accountholders in the Depository Trust Company (“DTC”).

| 13 |

Book Entry. Individual certificates are not issued for the shares. Instead, shares are represented by one or more global certificates, which are deposited by the Administrator with DTC and registered in the name of Cede & Co., as nominee for DTC. The global certificates evidence all of the shares outstanding at any time. Shareholders are limited to: (1) participants in DTC such as banks, brokers, dealers and trust companies (“DTC Participants”), (2) those who maintain, either directly or indirectly, a custodial relationship with a DTC Participant (“Indirect Participants”), and (3) those banks, brokers, dealers, trust companies and others who hold interests in the shares through DTC Participants or Indirect Participants, in each case who satisfy the requirements for transfers of shares. DTC Participants acting on behalf of investors holding shares through such participants’ accounts in DTC will follow the delivery practice applicable to securities eligible for DTC’s Same-Day Funds Settlement System. Shares are credited to DTC Participants’ securities accounts following confirmation of receipt of payment.

DTC. DTC has advised DNO as follows: It is a limited purpose trust company organized under the laws of the State of New York and is a member of the Federal Reserve System, a “clearing corporation” within the meaning of the New York Uniform Commercial Code and a “clearing agency” registered pursuant to the provisions of Section 17A of the Exchange Act. DTC holds securities for DTC Participants and facilitates the clearance and settlement of transactions between DTC Participants through electronic book-entry changes in accounts of DTC Participants.

Calculating Per Share NAV

DNO’s per share NAV is calculated by:

| • | Taking the current market value of its total assets; |

| • | Subtracting any liabilities; and |

| • | Dividing that total by the total number of outstanding shares. |

The Administrator calculates the per share NAV of DNO once each NYSE Arca trading day. The per share NAV for a particular trading day is released after 4:00 p.m. New York time. Trading during the core trading session on the NYSE Arca typically closes at 4:00 p.m. New York time. The Administrator uses the NYMEX closing price (determined at the earlier of the close of the NYMEX or 2:30 p.m. New York time) for the Futures Contracts traded on the NYMEX, but calculates or determines the value of all other DNO investments (including Futures Contracts not traded on the NYMEX, Other Crude-Oil Related Investments and Treasuries), using market quotations, if available, or other information customarily used to determine the fair value of such investments as of the earlier of the close of the NYSE Arca or 4:00 p.m. New York time, in accordance with the current Administrative Agency Agreement among BBH&Co., DNO and USCF. “Other information” customarily used in determining fair value includes information consisting of market data in the relevant market supplied by one or more third parties including, without limitation, relevant rates, prices, yields, yield curves, volatilities, spreads, correlations or other market data in the relevant market; or information of the types described above from internal sources if that information is of the same type used by DNO in the regular course of its business for the valuation of similar transactions. The information may include costs of funding, to the extent costs of funding are not and would not be a component of the other information being utilized. Third parties supplying quotations or market data may include, without limitation, dealers in the relevant markets, end-users of the relevant product, information vendors, brokers and other sources of market information.

In addition, in order to provide updated information relating to DNO for use by investors and market professionals, the NYSE Arca calculates and disseminates throughout the core trading session on each trading day an updated indicative fund value. The indicative fund value is calculated by using the prior day’s closing per share NAV of DNO as a base and updating that value throughout the trading day to reflect changes in the most recently reported trade price for the active light, sweet Futures Contracts on the NYMEX. The prices reported for those Futures Contract months are adjusted based on the prior day’s spread differential between settlement values for the relevant contract and the spot month contract. In the event that the spot month contract is also the Benchmark Futures Contract, the last sale price for that contract is not adjusted. The indicative fund value share basis disseminated during NYSE Arca core trading session hours should not be viewed as an actual real time update of the per share NAV, because the per share NAV is calculated only once at the end of each trading day based upon the relevant end of day values of DNO’s investments.

| 14 |

The indicative fund value is disseminated on a per share basis every 15 seconds during regular NYSE Arca core trading session hours of 9:30 a.m. New York time to 4:00 p.m. New York time. The normal trading hours of the NYMEX are 10:00 a.m. New York time to 2:30 p.m. New York time. This means that there is a gap in time at the beginning and the end of each day during which DNO’s shares are traded on the NYSE Arca, but real-time NYMEX trading prices for crude oil Futures Contracts traded on the NYMEX are not available. During such gaps in time, the indicative fund value will be calculated based on the end of day price of such Futures Contracts from the NYMEX’s immediately preceding trading session. In addition, other Futures Contracts, Other Crude-Oil Related Investments and Treasuries held by DNO will be valued by the Administrator, using rates and points received from client-approved third party vendors (such as Reuters and WM Company) and advisor quotes. These investments will not be included in the indicative fund value.

The NYSE Arca disseminates the indicative fund value through the facilities of CTA/CQ High Speed Lines. In addition, the indicative fund value is published on the NYSE Arca’s website and is available through on-line information services such as Bloomberg and Reuters.

Dissemination of the indicative fund value provides additional information that is not otherwise available to the public and is useful to investors and market professionals in connection with the trading of DNO shares on the NYSE Arca. Investors and market professionals are able throughout the trading day to compare the market price of DNO and the indicative fund value. If the market price of DNO shares diverges significantly from the indicative fund value, market professionals will have an incentive to execute arbitrage trades. For example, if DNO appears to be trading at a discount compared to the indicative fund value, a market professional could buy DNO shares on the NYSE Arca and sell short crude oil Futures Contracts. Such arbitrage trades can tighten the tracking between the market price of DNO and the indicative fund value and thus can be beneficial to all market participants.

Creation and Redemption of Shares

DNO creates and redeems shares from time to time, but only in one or more Creation Baskets or Redemption Baskets. The creation and redemption of baskets are only made in exchange for delivery to DNO or the distribution by DNO of the amount of Treasuries and any cash represented by the baskets being created or redeemed, the amount of which is based on the combined NAV of the number of shares included in the baskets being created or redeemed determined after 4:00 p.m. New York time on the day the order to create or redeem baskets is properly received.

Authorized Purchasers are the only persons that may place orders to create and redeem baskets. Authorized Purchasers must be: (1) registered broker-dealers or other securities market participants, such as banks and other financial institutions, that are not required to register as broker-dealers to engage in securities transactions as described below, and (2) DTC Participants. To become an Authorized Purchaser, a person must enter into an Authorized Purchaser Agreement with USCF on behalf of DNO. The Authorized Purchaser Agreement provides the procedures for the creation and redemption of baskets and for the delivery of the Treasuries and any cash required for such creations and redemptions. The Authorized Purchaser Agreement and the related procedures attached thereto may be amended by USCF, without the consent of any shareholder or Authorized Purchaser. From July 1, 2011 through December 31, 2013 (and continuing at least through May 1, 2014), the applicable transaction fee paid by Authorized Purchasers was $350 to DNO for each order they place to create or redeem one or more baskets; prior to July 1, 2011, this fee was $1,000. Authorized Purchasers who make deposits with DNO in exchange for baskets receive no fees, commissions or other form of compensation or inducement of any kind from either DNO or USCF, and no such person will have any obligation or responsibility to DNO or USCF to effect any sale or resale of shares. As of December 31, 2013, 13 Authorized Purchasers had entered into agreements with USCF on behalf of DNO. During the year ended December 31, 2013, DNO issued 27 Creation Baskets and redeemed 28 Redemption Baskets.

Certain Authorized Purchasers are expected to be capable of participating directly in the physical crude oil market and the crude oil futures market. In some cases, Authorized Purchasers or their affiliates may from time to time buy crude oil or sell crude oil or Crude Oil Interests and may profit in these instances. USCF believes that the size and operation of the crude oil market make it unlikely that an Authorized Purchaser’s direct activities in the crude oil or securities markets will significantly affect the price of crude oil, Crude Oil Interests, or the price of the shares.

| 15 |

Each Authorized Purchaser is required to be registered as a broker-dealer under the Exchange Act and is a member in good standing with FINRA, or exempt from being or otherwise not required to be registered as a broker-dealer or a member of FINRA, and qualified to act as a broker or dealer in the states or other jurisdictions where the nature of its business so requires. Certain Authorized Purchasers may also be regulated under federal and state banking laws and regulations. Each Authorized Purchaser has its own set of rules and procedures, internal controls and information barriers as it determines is appropriate in light of its own regulatory regime.

Under the Authorized Purchaser Agreement, USCF has agreed to indemnify the Authorized Purchasers against certain liabilities, including liabilities under the Securities Act of 1933, as amended (the “Securities Act”), and to contribute to the payments the Authorized Purchasers may be required to make in respect of those liabilities.

The following description of the procedures for the creation and redemption of baskets is only a summary and an investor should refer to the relevant provisions of the LP Agreement and the form of Authorized Purchaser Agreement for more detail, each of which is incorporated by reference into this annual report on Form 10-K.

Creation Procedures

On any business day, an Authorized Purchaser may place an order with the Marketing Agent to create one or more baskets. For purposes of processing purchase and redemption orders, a “business day” means any day other than a day when any of the NYSE Arca, the NYMEX or the NYSE is closed for regular trading. Purchase orders must be placed by 12:00 p.m. New York time or the close of regular trading on the NYSE Arca, whichever is earlier. The day on which the Marketing Agent receives a valid purchase order is referred to as the purchase order date.

By placing a purchase order, an Authorized Purchaser agrees to deposit Treasuries, cash, or a combination of Treasuries and cash, as described below. Prior to the delivery of baskets for a purchase order, the Authorized Purchaser must also have wired to the Custodian the non-refundable transaction fee due for the purchase order. Authorized Purchasers may not withdraw a creation request.

The manner by which creations are made is dictated by the terms of the Authorized Purchaser Agreement. By placing a purchase order, an Authorized Purchaser agrees to (1) deposit Treasuries, cash, or a combination of Treasuries and cash with the Custodian, and (2) if required by USCF in its sole discretion, enter into or arrange for a block trade, an exchange for physical or exchange for swap, or any other over-the-counter energy transaction (through itself or a designated acceptable broker) with DNO for the purchase of a number and type of futures contracts at the closing settlement price for such contracts on the purchase order date. If an Authorized Purchaser fails to consummate (1) and (2), the order shall be cancelled. The number and type of contracts specified shall be determined by USCF, in its sole discretion, to meet DNO’s investment objective and shall be purchased as a result of the Authorized Purchaser’s purchase of shares.

Determination of Required Deposits

The total deposit required to create each basket (“Creation Basket Deposit”) is the amount of Treasuries and/or cash that is in the same proportion to the total assets of DNO (net of estimated accrued but unpaid fees, expenses and other liabilities) on the purchase order date as the number of shares to be created under the purchase order is in proportion to the total number of shares outstanding on the purchase order dates. USCF determines, directly in its sole discretion or in consultation with the Administrator, the requirements for Treasuries and the amount of cash, including the maximum permitted remaining maturity of a Treasury and proportions of Treasury and cash that may be included in deposits to create baskets. The Marketing Agent will publish such requirements at the beginning of each business day. The amount of cash deposit required is the difference between the aggregate market value of the Treasuries required to be included in a Creation Basket Deposit as of 4:00 p.m. New York time on the date the order to purchase is properly received and the total required deposit.

Delivery of Required Deposits

An Authorized Purchaser who places a purchase order is responsible for transferring to DNO’s account with the Custodian the required amount of Treasuries and cash by the end of the third business day following the purchase order date. Upon receipt of the deposit amount, the Administrator directs DTC to credit the number of baskets ordered to the Authorized Purchaser’s DTC account on the third business day following the purchase order date. The expense and risk of delivery and ownership of Treasuries until such Treasuries have been received by the Custodian on behalf of DNO shall be borne solely by the Authorized Purchaser.

| 16 |