UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[x] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2013

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________to ___________

Commission File Number: 000-54998

CONSUMER CAPITAL GROUP, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 26-2517432 | |

State or other jurisdiction of incorporation or organization |

(I.R.S. Employer Identification No.) | |

| 100 Park Avenue, 16th Floor, New York 10017 | 10017 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code:(212) 880-6400

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange on which registered: |

| None | None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.0001 per share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [x]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [x]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [x] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [x] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] | |

| Non-accelerated filer | [ ] | Smaller reporting company | [x] | |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [x]

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, as of the last business day of the registrant’s most recently completed second fiscal quarter was $28,311,006.

As of March 12, 2014, the registrant had 19,072,987 shares of common stock, par value $0.0001 per share, outstanding.

Documents incorporate by reference: None.

CONSUMER CAPITAL GROUP, INC.

ANNUAL REPORT ON FORM 10-K

| Page | ||||||

| PART I | ||||||

| ITEM 1. | Business | 1 | ||||

| ITEM 1A. | Risk Factors | 15 | ||||

| ITEM 1B. | Unresolved Staff Comments | 15 | ||||

| ITEM 2. | Properties | 15 | ||||

| ITEM 3. | Legal Proceedings | 16 | ||||

| ITEM 4. | Mine Safety Disclosures | 16 | ||||

| PART II | ||||||

| ITEM 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 16 | ||||

| ITEM 6. | Selected Financial Data | 18 | ||||

| ITEM 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 18 | ||||

| ITEM 7A. | Quantitative and Qualitative Disclosures About Market Risk | 22 | ||||

| ITEM 8. | Financial Statements and Supplementary Data | 23 | ||||

| ITEM 9. | Changes In and Disagreements With Accountants on Accounting and Financial Disclosure | 23 | ||||

| ITEM 9A. | Controls and Procedures | 23 | ||||

| ITEM 9B. | Other Information | 24 | ||||

| PART III | ||||||

| ITEM 10. | Directors, Executive Officers and Corporate Governance | 24 | ||||

| ITEM 11. | Executive Compensation | 27 | ||||

| ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 28 | ||||

| ITEM 13. | Certain Relationships and Related Transactions, and Director Independence | 29 | ||||

| ITEM 14. | Principal Accountant Fees and Services | 30 | ||||

| PART IV | ||||||

| ITEM 15. | Exhibits and Financial Statement Schedules | 31 | ||||

| Signatures | 34 | |||||

FORWARD-LOOKING STATEMENTS

Certain statements made in this Annual Report on Form 10-K are “forward-looking statements” made under the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 regarding the plans and objectives of management for future operations. Such statements involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. These statements use words such as “believe,” “expect,” “should,” “strive,” “plan,” “intend,” “estimate,” “anticipate” or similar expressions. The forward-looking statements included herein are based on our current beliefs, assumptions, and expectations, and are subject to numerous risks and uncertainties. You should carefully read the risk factor disclosure contained in “Item 1A. Risk Factors” of this Annual Report on Form 10-K, where we discuss many of the important factors currently known to management that could cause actual results to differ materially from those in our forward-looking statements. Our plans and objectives are based, in part, on assumptions of the continuing expansion of business. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions, and future business decisions, all of which are difficult or impossible to predict accurately, and many of which are beyond our control. Although we believe our assumptions underlying the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. These forward-looking statements are made as of the date of this report, and we assume no obligation to update these forward-looking statements whether as a result of new information, future events, or otherwise, other than as required by law. In light of these assumptions, risks, and uncertainties, the forward-looking events discussed in this report might not occur and actual results and events may vary significantly from those discussed in the forward-looking statements.

USE OF CERTAIN DEFINED TERMS

In this Report, unless otherwise noted or as the context otherwise requires: “the Company,” “we,” “us,” and “our” refers to the combined company Consumer Capital Group, Inc. and its subsidiaries and Variable Interest Entities.

PART I

Item 1. Business.

Overview

We are primarily engaged in two different businesses: e-commerce services and meat distribution. We operate an online retail platform in China at www.ccmus.com through Arki (Beijing) E-Commerce Technology Corp., our wholly owned subsidiary, and an online retail platform at www.ccgusa.com in the United States. We operate our meat distribution business through Beijing Beitun Trading Co., Ltd., our 51% owned subsidiary. In addition to e-commerce services and meat distribution, we have been working to develop a debit card business, through America Arki Fuxin Network Management Co. Ltd., our wholly owned subsidiary.

Corporate History

We were originally incorporated under the name “Mondas Minerals Corp.” in Delaware on April 25, 2008 and was engaged in the acquisition, exploration, and development of natural resource properties. The principal executive offices were previously located at 13983 West Stone Avenue, Post Falls, ID 83854.

We received our initial funding of $15,000 through the sale of common stock to our officer and director who purchased 1,500,000 shares of our common stock at $0.01 per share on May 13, 2008. In January 2010, we raised $1,457,818 from an offering of 1,000,000 shares pursuant to a registration statement on Form S-1 filed with the SEC under file number 333-152330, which became effective on January 5, 2010. The offering was completed on January 27, 2010.

We were an exploration stage company with no revenues or operating history prior to our merger on February 4, 2011 described below. We owned a 100% undivided interest in a mineral property, the Ram 1-4 Mineral Claims (known as the “Ram Property.”) The Ram Property consists of an area of 82.64 acres located in the Lida Quadrangle Area, Esmeralda County, Nevada. Title to the Ram Property was held by Mondas. Our plan of operation was to conduct mineral exploration activities on the property in order to assess whether it contains mineral deposits capable of commercial extraction.

As of December 31, 2010 and immediately prior to the merger transaction described below, we were an exploration stage company with nominal assets, no revenues, or operating history. On January 11, 2011, the Company changed its fiscal year end from June 30 to December 31.

On February 4, 2011, the Company acquired Consumer Capital Group, Inc., a California corporation (“CCG California”), a consumer e-commerce business with operations in the People’s Republic of China (“PRC”) in a reverse merger transaction (the “Merger”) pursuant to an Agreement and Plan of Merger (“Merger Agreement”) by and among the Company, the Company’s wholly owned subsidiary CCG Acquisition Corp., a Delaware corporation (“CCG Delaware”), CCG California, and Scott D. Bengfort.

In the Merger, CCG Delaware merged into CCG California with CCG California as the surviving corporation. As a result, CCG California became our wholly-owned subsidiary, and the subsidiaries of CCG Delaware including America Pine (Beijing) Bio-Tech, Inc., Arki (Beijing) E-Commerce Technology Corp., Beijing Beitun Trading Co., Ltd., and America Arki (Fuxin) Network Management Co. Ltd., all of which incorporated in China (together, the “PRC Subsidiaries”), became Mondas’s indirect subsidiaries. Arki (Beijing) E-Commerce Technology Corp. has a contractual relationship with America Arki Network Service Beijing Co., Ltd. (“Arki Network Service”), a PRC limited liability company, which is 100% owned by two of CCG California’s former major shareholders and officers. CCG California, the PRC Subsidiaries, and Arki Network Service are collectively referred to as the “CCG Group.”

On January 7, 2011, the Company formed a new wholly-owned subsidiary by the name of “Consumer Capital Group Inc.” (“CCG Name Sub”) in Delaware solely for purposes of changing its corporate name to “Consumer Capital Group Inc.” in conjunction with the closing of the Merger. On February 17, 2011, the Company changed its name to Consumer Capital Group Inc. pursuant to Certificate of Ownership filed with the Secretary of State of Delaware by merging CCG Name Sub into the Company with the Company surviving and CCG Name Sub ceasing to exist.

Under the Merger Agreement, the Company issued an aggregate of 17,777,778 shares of its common stock to the shareholders of CCG California immediately prior to the Merger (“CCG Shareholders”) at an exchange rate of one (1) share of our common stock for each 21.96 shares of CCG California common stock.

Immediately prior to the closing of the Merger, there were 2,500,000 issued and outstanding shares of the Company’s common stock, 60% of which were held by the then-principal stockholder, CEO, and sole director of the Company, Mr. Bengfort. As a part of the Merger, CCG California paid USD $335,000 in cash to Mr. Bengfort in exchange for his agreement to enter into various transaction agreements relating to the Merger, as well as the cancellation of 1,388,889 shares of the Company’s common stock directly held by him, constituting 92.6% of his pre-Merger holdings of the Company’s common stock.

In connection with the Merger, the mining rights held by the Company were assigned to Mr. Bengfort, and in turn, Mr. Bengfort personally assumed all liabilities of the Company existing immediately prior to the closing, under the terms of an Assignment and Assumption Agreement between the Company and Mr. Bengfort effective on the closing date of the Merger (the “Assignment and Assumption Agreement”). Mr. Bengfort also agreed to discharge and forego his rights to be repaid approximately $16,000, which the Company owed to him immediately prior to the closing of the Merger, along with all other claims against the Company, by executing a release agreement (“Release”) effective on the closing date of the Merger. Mr. Bengfort also agreed to be a party to the Merger Agreement, including various representations and warranties. Further, Mr. Bengfort executed an indemnification agreement (“Indemnification Agreement”) in favor of CCG California and its shareholders to indemnify them for any breach of the Merger Agreement or unpaid or unresolved liabilities of the Company that may materialize within a one year period after the closing. The closing of the Merger was on February 4, 2011.

In connection with the closing, Mr. Bengfort resigned from his role as the Company’s sole officer and director. New directors took office, and appointed new officers of the Company promptly following the closing of the Merger.

There was no trading of our shares prior to the Merger. Since the Merger, there has been limited trading of our shares. From and after the closing of the Merger, our primary operations now consist of the business and operations of the CCG Group, which are primarily conducted in the PRC.

Our current principal offices are located at 100 Park Avenue, 16th Floor, New York 10017. Our trading symbol on the Over-the-Counter Bulletin Board (the “OTCBB”) is CCGN. Our website address is www.ccgusa.com.

CCG HISTORY AND ORGANIZATION

The founders of the CCG Group are Jianmin Gao, Chief Executive Officer, Lingling Zhang, Wife of Chief Executive Officer, and Fei Gao, Son of Chief Executive Officer. The founders formed America Pine Group Inc. (“America Pine California”) in California on November 27, 2006. America Pine California was in the business of selling healthcare products imported from the United States of America to residents in the PRC. The founders formed America Pine Beijing in the PRC on March 21, 2007 as a wholly owned subsidiary of America Pine California to conduct operations for this business in the PRC. These operations ceased on February 5, 2010.

The founders formed Arki Beijing in the PRC on March 6, 2008 as a wholly owned subsidiary of America Pine California with an intention to develop the CCG Group’s current consumer e-commerce business.

On February 5, 2010, in connection with the execution of a Stock Right Transfer Agreement, America Pine California transferred all of its equity interests in both Arki Beijing and America Pine Beijing Consumer Capital Group, Inc., a California corporation and wholly owned subsidiary of the Company (“CCG California”), which was formed in California on October 14, 2009.

On November 26, 2010, CCG California formed Arki Fuxin as its wholly owned subsidiary.

On November 29, 2010, CCG California received approval from the Beijing Fangshan District Business Council in the PRC to acquire the controlling interest of Beitun Trading. Beitun Trading has a registered capital of RMB500,000 (approximately $80,250), of which RMB255,000 (approximately $40,928) was contributed by CCG and RMB245,000 (approximately $39,323) was contributed by Wei Guo. CCG currently owns 51% of Beitun Trading, and Wei Guo owns 49% of Beitun Trading.

On November 26, 2010, Arki Beijing, Arki Network Service, and its shareholders entered into contractual arrangements, and on December 2010, Arki Fuxin, Arki Network Service, and its shareholders entered into contractual arrangements, to operate the consumer e-commerce website. Arki Network Service is owned by CCG’s two largest shareholders, Mr. Jianmin Gao and Mr. Fei Gao. These arrangements are more fully described below.

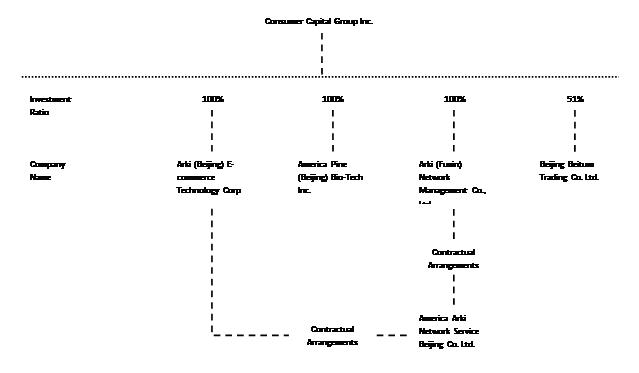

Corporate Structure

Contractual Arrangements with Arki Beijing, Arki Network Service, and Arki Fuxin

Our relationships with Arki Network Service, its stockholders, and Arki Beijing are governed by a series of contractual arrangements, as we (including our direct and indirect subsidiaries) do not own any equity interests in Arki Network Service. PRC law currently has limits on foreign ownership of certain companies. To comply with these restrictions, Arki Network Service and its shareholders entered into two sets of contractual arrangements with Arki Beijing and Arki Fuxin in November 2010:

Powers of Attorney. The equity owners irrevocably appointed Arki Beijing and Arki Fuxin to vote on their behalf on all matters they are entitled to vote on, including matters relating to the transfer of any or all of their respective equity interests in the entity and the appointment of the chief executive officer and other senior management members.

Share Pledge Agreements. The equity owners pledged their respective equity interests in the entity as a guarantee for the payment by the entity of consulting and services fees under the business cooperation agreements and repayment under the loan agreements.

Business Cooperation Agreement. Arki Beijing and Arki Fuxin provide the entity with technical support, consulting services, and other commercial services to Arki Network Service. The initial term of these agreements is ten years. In consideration for those services, Arki Network Service agrees to pay Arki Beijing and Arki Fuxin service fees. The service fees are eliminated upon consolidation.

Loan Agreements. Loans were granted to the equity owners of Arki Network Service by Arki Fuxin with the sole and exclusive purpose of providing funds necessary for its capitalization as required by the laws of the PRC.

Exclusive Option Agreements. Shareholders of Arki Network Service granted an option contract to Arki Beijing and Arki Fuxin to purchase their respective equity interests in the entity.

As of December 31, 2013, we conduct substantially all of our e-commerce business operations through Arki Fuxin, which holds substantial control over Arki Network Service’s operations through their contractual arrangements.

Current Corporate Structure

The following diagram illustrates our corporate structure:

Our Business

E-commerce

From and after the closing of the Merger, our primary operations now consist of the business and operations of the CCG Group, which are primarily conducted in the PRC. CCG is a holding company that, prior to December 2010, through Arki (Beijing) E-Commerce Technology Corp. (“Arki Beijing”) and its subsidiary, Arki Network Service, operated a consumer e-commerce business in the PRC. Beginning in December 2010, the e-commerce business operations are being conducted through America Arki (Fuxin) Network Management Co. Ltd., a PRC corporation (“Arki Fuxin”), Arki Network Service, and Arki Beijing through respective contractual arrangements among those parties. These contractual arrangements are necessary to comply with laws of the PRC limiting foreign ownership of companies that operate in the e-commerce space. Through such contractual arrangements, we have the ability to substantially influence Arki Network Service’s daily business operations and financial affairs, appoint its management, and approve all matters requiring stockholder approval.

CCG also owns 100% equity interests in America Pine (Beijing) Bio-Tech, Inc., a PRC corporation (“America Pine Beijing”), which currently does not have substantial operations.

Our online retail platforms allow third-party merchants to sell their general merchandise products directly to consumers in China and the United States. We charge third-party merchants a service fee of approximately 5% of the total purchase price with respect to their general merchandise sold through our website. We also receive advertising fees from third-party merchants if they advertise products through our website. To incentivize our customers, we give our member customers bonus points for each purchase, to be used for cash value in their next purchase. As our customers accumulate bonus points, they receive membership upgrade, special discounts and additional bonus points. Our member customers may also receive awards from our daily sweepstakes program. In 2013, we began to refocus our online retail platforms from selling general merchandise products to selling collections.

Our Consumer E-Commerce Website

In 2010, we launched our PRC-based nationwide online retailing platform at www.ccmus.com. The Company, through Arki Beijing, is primarily engaged in the development and operation of its nationwide online retailing platform “Chinese Consumer Market Network” at www.ccmus.com. In 2011, we launched our U.S. retail platform at www.ccgusa.com, but the business operation has been relatively small.

Our website provides consumer goods and services in the following 19 major categories:

| 1. | Nutrition and health supplements; | |

| 2. | Toys and games; | |

| 3. | Cosmetics and beauty; | |

| 4. | Consumer electronics; | |

| 5. | Culture and sports; | |

| 6. | Consumer services; | |

| 7. | Maternity and baby products; | |

| 8. | Clothes and shoes; | |

| 9. | Jewelry and accessories; | |

| 10. | Travel and tickets; | |

| 11. | Foreign goods; | |

| 12. | Office supplies; | |

| 13. | Household appliances; | |

| 14. | Luxury products; | |

| 15. | Home furnishings; | |

| 16. | Organic products; | |

| 17. | Education products; | |

| 18. | Kitchen appliances; and | |

| 19. | Crystal products; |

How the Website Works

Third-party merchants use our website to advertise and sell their goods, manage customer data, and track orders and shipments. Consumers shop online and pay for products and services through the system. Thus, we do not buy, hold, or sell any inventory.

The system escrows payments for the goods until the consumer uses the system to indicate that the order was satisfactorily fulfilled. Third-party merchants set the price of their products and services offered through our website. Third-party merchants, however, must include within their selling price a service fee for CCG and sometimes money for our points and reward program if applicable.

As of December 31, 2013, through our China website we offer products from 530 merchants and from our U.S. website we offer products and services from 20 merchants. We also have over 32,000 members in China and over 510 members in the U.S. These members purchase products and services offered through our website.

Members

Consumers who purchase products and services offered through our website are automatically enrolled as members. We offer our members in China a “Lucky Drawing” sweepstakes and members who purchase products or services are automatically enrolled in the drawing. The amount of the Lucky Drawing prize is based on the volume of purchases up to a maximum prize of RMB5,000. We believe this reward program motivates consumers to encourage their family and friends to purchase products and services through our website. This reward program is limited to our members in China.

In addition to this sweepstakes feature, we attract customers, build loyalty, and encourage repeat business by establishing membership levels based on total amount spent by each member. As members purchase more goods and services through the website, they attain higher levels of membership that entitle them to “bonus points” that can be applied toward future purchases. Earning additional points and attaining higher levels of membership also entitle members to additional sweepstakes opportunities. Again, this feature is limited to our members in China.

Merchants

Our website provides business-to-consumer e-commerce retail platform to manufacturers and distributors who wish to sell directly to Chinese consumers. Our platform eliminates most intermediate links and results in substantial channel cost savings. By providing direct access to our members, merchants attain an immediate and dramatic expansion of their retail exposure throughout the PRC. Merchants benefit from the online nature of business-to-consumer e-commerce transactions that facilitate fast and immediate receipt of orders, shorten accounts receivable periods, enhance cash flow, reduce cost of sales, and increase a seller’s operational capacity.

An important feature of our system is that, in addition to the Company managed sweepstakes and bonus points features, the platform allows merchants to offer incentive points to consumers who purchase their goods. Merchants may set the amount of the purchase price that consumers receive back as incentive points based on the consumer’s membership level and purchasing history with the seller. These incentive points constitute a strong marketing mechanism for the merchants and an indirect discount to consumers.

Technology

Our website is built on advanced e-commerce technologies. Its major modules and functionalities include:

| ● | front-end web application built on Microsoft ASP.NET technology, including the most advanced .NET 4.0 framework. |

| o | Support for Memberships, User Profiles, Security, and Encryption. | |

| o | Integrated performance enhancement, database, XML, and RSS. | |

| o | Support for real-time authentication, authorization, and validation. |

| ● | Shopping cart built on Microsoft ASP.NET technology using C# libraries with .NET user profiles, LINQ, and SQL Server database | |

| ● | Transaction engine built on Microsoft SQL Server and ASP.NET 4.0 technology with support for parallel computing and load balancing for enhanced efficient real-time transaction performances. | |

| ● | Secured order handling via https, authentication, authorization, and transaction logging. | |

| ● | Merchant interface web platform that enables merchants to share and route information through different departments, execute business transactions, and obtain real-time reports. | |

| ● | SQL Server Reporting Services. | |

| ● | Scalability. The system is designed to support very large numbers of concurrent transactions based on its .NET 4.0 parallel computing, load balancing, and SQL Server Enterprise capabilities, and grow well ahead of the transaction volume curve. | |

| ● | Lucky Drawing sweepstakes. The daily sweepstakes are conducted on the web platform by means of application features that promote user awareness, create program documentation, drive promotions, perform record reconciliations, and generate reporting and acknowledgment. | |

| ● | Bonus point incentive program. The system’s knowledge management module and a content management module are designed to support this and other incentive programs based on corporate strategic planning and marketing schedules. | |

| ● | Interface with banking and financial partners. The system fully integrates with our financial institution partners. |

Security

Our platform provides both merchants and members with complete financial, identity, authenticity, and delivery security. We hold payment for goods ordered through the system until the consumer confirms receipt and satisfaction with the goods received. Security is ensured by means of a multifactor account password and authentication system, multiple password-protected login protocols, and dynamic passwords, digital certificates, and other authentication mechanisms. The transaction security system further guarantees that both merchants and sellers are certified and registered on file in order to ensure the true identity of the parties. Each transaction is subject to verification by industry-leading proprietary monitoring algorithms to detect and eliminate fraudulent activities.

During the year ended December 31, 2013, we had a nominal revenue of $5,681 from our e-commerce segment. The decrease was primarily due to the diversion of attention of management from the existing operation of this segment as the Company is making changes to its current e-commerce business model. The Company is working to re-focus its e-commerce business on selling collections.

Meat Distribution

We own a 51% majority interest in an operating subsidiary, Beijing Beitun Trading Co., Ltd. (“Beitun Trading”). Beitun Trading, a PRC trade and distribution company, engages in the wholesale distribution of various food and meat products. It was established in April 24, 2000 and operates in the PRC. Its customers consist of restaurants and food producers located throughout the PRC.

Through Beijing Beitun Trading Co., Ltd., we purchase meats from suppliers and distribute them to restaurants and food producers in China.

Debit Card Program

We plan to launch a cobranded debit card program, where the Company authorizes certain merchants the right to issue cobranded debit cards and charges each participating merchant a percentage of transactions with that merchant. We plan to charge participating merchants a transaction fee of 1% to 5% for each purchase using our cobranded debit cards. We intend to give our cardholders cash rewards with their purchases through our online retail platform. The cardholder may use the debit card to make electronic payments on our website as well as to make purchases with merchants that have signed up with our program. In the past two years, we made efforts to collaborate with Bank of Fuxin to issue cobranded debit cards but the collaboration has become very minimum as of December 31, 2013. We are currently seeking to allay with some other bank(s) to explore our plan of issuing cobranded debit cards. We do not expect to start our debit card operation before the first half of 2014.

In order to promote distribution of these cards, the Company has signed a dealer agreement with China Unionpay, which is a card management company similar to Visa and Master Card. China Unionpay has POS machines all over China.

Our Industry

China’s Economy

China is experiencing a rapid increase in per capita income and household consumption. This is fueled, in part, by an active array of policies on the part of the Chinese government oriented toward increasing disposable income and shifting growth away from industrial development and toward domestic demand.

The E-Commerce Industry in China

According to the state China Internet Network Information Center (CNNIC), China’s population of internet users was 618 million in 2013 and, the population of online shoppers reached 302 million in 2013.

China’s government remains focused on continuing the development of the country’s consumer market. At the 2010 Economic Work Conference, the government stressed the need to further expand consumption demand and consumption capacity. China’s well-established policy to stimulate consumption includes extending the availability of consumer credit and enhancing the country’s retail and distribution systems.

Since 2010, the Chinese government has spent efforts to step up stimulus of the domestic consumption market and expand imports. According to CHINA DAILY, China also plans to continue to boost domestic consumption as a priority in its 12th Five-Year Plan (2011-2015). Boosting domestic consumption is a key theme in the five year plan and is likely to improve the outlook for consumer markets. According to the Five-Year Plan, China’s household income is expected to rise to $9 trillion in 2015 from $4 trillion in 2010. According to Credit Suisse, China’s domestic consumption is expected to rise to $15.94 trillion in 2020, up from $1.72 trillion in 2009.

The Pork Industry in China

Pork is China’s meat of choice, accounting for nearly three fourths of its meat consumption. According to Earth Policy Institute, on a per person basis, over the past five years, per capita pork consumption in China has grown by over 3 percent a year despite price increases.

In addition to a greater general preference for pork, urbanization and rapid income growth are working in parallel to create more demand for pork and processed pork products.

Competition

Our website operates in a rapidly growing e-commerce market across the PRC. We compete against both domestic and international e-commerce businesses as well as traditional retailers that are expanding into e-commerce. We believe our major competitors include, among others, the following:

| ● | TAOBAO.COM is China’s biggest online retailer. It follows the eBay model by facilitating consumer-to-consumer or business-to-consumer retail by means of a platform for businesses and individuals to open online retail stores. Taobao caters to bargain-hunting consumers. Most of their users are teenagers, college students, and white collar workers in big cities in the age group 20-35. | |

| ● | DANGDANG.COM is another big online retailer in China. It sells books and other media products and general merchandise that it sources from publishers, manufacturers, and distributors in China. It also has a marketplace program in which third-party merchants can sell general merchandise products alongside its products, and customers can purchase these products through the same checkout process. | |

| ● | PAIPAI.COM consists of a number of major channels, including women, men, online games, digital products, mobile phone, life, sports, students, special offers, mothers and babies, toys, superior quality products, and hotels. Its business model centers on fashionable and trendy brand offerings. | |

| ● | EACHNET.COM is eBay’s China e-commerce platform. |

Competitive Advantages and Disadvantages

We believe our e-commerce business model possesses a number of strategically significant strengths. Major competitors such as Taobao and Paipai cater predominantly to consumer-to-consumer transactions. In contrast, we focus on business-to-consumer e-commerce with full range of consumer goods and services, from clothing and consumer electronics to household appliances and home furnishings. We believe our sweepstakes and incentive programs are unique among China’s competing e-commerce offerings. For manufacturers and distributors, the platform provides comprehensive retail channel benefits and geographical breadth while permitting autonomy and flexibility in how sellers fulfill and ship goods to consumers. By concentrating on e-commerce technology, we avoid the overhead and operational difficulties of logistics and supply chains.

Our website is presently disadvantaged by its limited history in the marketplace and our need to recruit and train experienced personnel. In addition to the competition we face from other e-commerce businesses, we require time and resources to further integrate our banking, merchant, and consumer partners. At present, consumer-to-consumer represents the largest segment of China’s e-commerce market.

Marketing and Sales

In 2012, we began to cooperate with the China Education Foundation to promote our business during televised national graduation ceremonies of the PRC’s millions of college students. The promotion was minimal in 2013.

PRC Regulations

Online commerce in China is subject to a number of laws and regulations. This section summarizes all material PRC laws and regulations relevant to our business and operations in China and the key provisions of such regulations.

Corporate Laws and Industry Catalogue Relating to Foreign Investment

The establishment, operation, and management of corporate entities in China are governed by the Company Law of the PRC, or the Company Law, effective in 1994, as amended in 1999, 2004, and 2005, respectively. The Company Law is applicable to our PRC subsidiaries and affiliated PRC entity unless the PRC laws on foreign investment have stipulated otherwise.

The establishment, approval, registered capital requirement, and day-to-day operational matters of wholly foreign-owned enterprises (“WFOE”), such as our PRC subsidiary, Arki Network Service, are regulated by the WFOE Law of the PRC effective in 1986, as amended in 2000, and the Implementation Rules of the WFOE Law of the PRC effective in 1990, as amended in 2001.

Investment activities in the PRC by foreign investors are principally governed by the Guidance Catalogue of Industries for Foreign Investment, or the Catalogue, which was promulgated and is amended from time to time by the Ministry of Commerce and the National Development and Reform Commission. The Catalogue divides industries into three categories: encouraged, restricted, and prohibited. Industries not listed in the Catalogue are generally open to foreign investment unless specifically restricted by other PRC regulations.

Establishment of WFOEs is generally permitted in encouraged industries. Some restricted industries are limited to equity or contractual joint ventures, while in some cases Chinese partners are required to hold the majority interests in such joint ventures.

For example, sales and distribution of audio and video products are among the restricted categories, and only contractual joint ventures in which Chinese partners holding majority interests can engage in the distribution of audio and video products in China.

In addition, restricted category projects are also subject to higher-level government approvals. Foreign investors are not allowed to invest in industries in the prohibited category.

Regulations Relating to Telecommunications Services

In September 2000, the State Council issued the Regulations on Telecommunications of China (“the Telecommunications Regulations”), to regulate telecommunications activities in China. The telecommunications industry in China is governed by a licensing system based on the classifications of the telecommunications services set forth under the Telecommunications Regulations.

The Ministry of Industry and Information Technology (“MIIT”) together with the provincial-level communications administrative bureaus, supervises and regulates the telecommunications industry in China. The Telecommunications Regulations divide the telecommunications services into two categories: infrastructure telecommunications services and value-added telecommunications services. The operation of value-added telecommunications services is subject to the examination, approval, and the granting of licenses by MIIT or the provincial-level communications administrative bureaus. According to the Catalogue of Classification of Telecommunications Businesses effective in April 2003, provision of information services through the internet, such as the operation of our website, is classified as value-added telecommunications services.

Regulations Relating to Foreign Investment in Value-added Telecommunications Industry

According to the Administrative Rules for Foreign Investment in Telecommunications Enterprises issued by the State Council effective in January 2002, as amended in September 2008, a foreign investor may hold no more than a 50% equity interest in a value-added telecommunications services provider in China, and such foreign investor must have experience in providing value-added telecommunications services overseas and maintain a good track record.

The Circular on Strengthening the Administration of Foreign Investment in and Operation of Value-added Telecommunications Business (“the Circular”), issued by the former Ministry of Information Industry (“MII”) in July 2006, reiterated the regulations on foreign investment in telecommunications businesses, which require foreign investors to set up foreign-invested enterprises and obtain an internet content provider, or ICP, license to conduct any value-added telecommunications business in China. Under the Circular, a domestic company that holds an ICP license is prohibited from leasing, transferring, or selling the license to foreign investors in any form, and from providing any assistance, including providing resources, sites, or facilities, to foreign investors that conduct value-added telecommunications business illegally in China. Furthermore, certain relevant assets, such as the relevant trademarks and domain names that are used in the value-added telecommunications business must be owned by the local ICP license holder or its shareholders. The Circular further requires each ICP license holder to have the necessary facilities for its approved business operations and to maintain such facilities in the regions covered by its license. In addition, all value-added telecommunications service providers are required to maintain network and information security in accordance with the standards set forth under relevant PRC regulations. If an ICP license holder fails to comply with the requirements in the Circular and also fails to remedy such non-compliance within a specified period of time, MII or its local counterparts have the discretion to take administrative measures against such license holder, including revoking its ICP license. We believe Arki Network Service is in compliance with the Circular.

Regulations Relating to Internet Information Services and Content of Internet Information

In September 2000, the State Council issued the Administrative Measures on Internet Information Services (“the Internet Measures”), to regulate the provision of information services to online users through the internet. According to the Internet Measures, internet information services are divided into two categories: services of an operative nature and services of a non-operative nature. Our business conducted through our website involves operating internet information services, which requires us to obtain an ICP license. If an internet information service provider fails to obtain an ICP license, the relevant local branch of MII may levy fines, confiscate its income, or even block its website. Due to the PRC law restriction that foreign investors cannot hold more than a 50% equity interest in a value-added telecommunications services provider, we hold our ICP license through Arki Network Service. Arki Network Service currently holds an ICP license issued by Beijing Communications Administration, a local branch of MII. Our ICP license will expire in August 2015, and we will renew such license prior to its expiration date.

The Internet Measures further specify that the internet information services regarding, among others, news, publication, education, medical and health care, and pharmacy and medical appliances are required to be examined, approved, and regulated by the relevant authorities. Internet content providers are prohibited from providing services beyond that included in the scope of their business license or other required licenses or permits. Furthermore, the Internet Measures clearly specify a list of prohibited content. Internet content providers must monitor and control the information posted on their websites. We are subject to this rule as a result of our operation of our online marketplace program.

Regulations Relating to Privacy Protection

As an internet content provider, we are subject to regulations relating to protection of privacy. Under the Internet Measures, internet content providers are prohibited from producing, copying, publishing or distributing information that is humiliating or defamatory to others or that infringes the lawful rights and interests of others. Internet content providers that violate the prohibition may face criminal charges or administrative sanctions by PRC security authorities. In addition, relevant authorities may suspend their services, revoke their licenses or temporarily suspend or close down their websites. Furthermore, under the Administration of Internet Bulletin Board Services issued by the MII in November 2000, internet content providers that provide electronic bulletin board services must keep users’ personal information confidential and are prohibited from disclosing such personal information to any third party without the consent of the users, unless otherwise required by law. The regulation further authorizes relevant telecommunication authorities to order internet content providers to rectify any unauthorized disclosure. Internet content providers could be subject to legal liabilities if unauthorized disclosure causes damages or losses to internet users. However, the PRC government retains the power and authority to order internet content providers to provide the personal information of internet users if the users post any prohibited content or engage in illegal activities through the internet. We believe that we are currently in compliance with these regulations in all material aspects.

Regulations Relating to Taxation

In January 2008, the PRC Enterprise Income Tax Law (The “EIT” Law) took effect. The EIT applies a uniform 25% enterprise income tax rate to both foreign-invested enterprises and domestic enterprises, unless where tax incentives are granted to special industries and projects. Under the EIT Law and its implementation regulations, dividends generated from the business of a PRC subsidiary after January 1, 2008 and payable to its foreign investor may be subject to a withholding tax rate of 10% if the PRC tax authorities determine that the foreign investor is a non-resident enterprise, unless there is a tax treaty with China that provides for a preferential withholding tax rate. Distributions of earnings generated before January 1, 2008 are exempt from PRC withholding tax.

Under the EIT Law, an enterprise established outside China with “de facto management bodies” within China is considered a “resident enterprise” for PRC enterprise income tax purposes and is generally subject to a uniform 25% enterprise income tax rate on its worldwide income. A circular issued by the State Administration of Taxation in April 2009 regarding the standards used to classify certain Chinese-invested enterprises controlled by Chinese enterprises or Chinese enterprise groups and established outside of China as “resident enterprises” clarified that dividends and other income paid by such PRC “resident enterprises” will be considered PRC-source income and subject to PRC withholding tax, currently at a rate of 10%, when paid to non-PRC enterprise shareholders. This circular also subjects such PRC “resident enterprises” to various reporting requirements with the PRC tax authorities.

Under the implementation regulations to the EIT Law, a “de facto management body” is defined as a body that has material and overall management and control over the manufacturing and business operations, personnel and human resources, finances, and properties of an enterprise. In addition, the tax circular mentioned above specifies that certain PRC-invested overseas enterprises controlled by a Chinese enterprise or a Chinese enterprise group in the PRC will be classified as PRC resident enterprises if the following are located or residence in the PRC: senior management personnel and departments that are responsible for daily production, operation, and management; financial and personnel decision making bodies; key properties, accounting books, the company seal, and minutes of board meetings and shareholders’ meetings; and half or more of the senior management or directors having voting rights.

Regulations Relating to Foreign Exchange

Pursuant to the Regulations on the Administration of Foreign Exchange issued by the State Council and effective in 1996, as amended in January 1997 and August 2008, current account transactions, such as sale or purchase of goods, are not subject to PRC governmental control or restrictions. Certain organizations in the PRC, including foreign-invested enterprises, may purchase, sell, and/or remit foreign currencies at certain banks authorized to conduct foreign exchange business upon providing valid commercial documents. Approval of the PRC State Administration of Foreign Exchange (“SAFE”), however, is required for capital account transactions.

In August 2008, SAFE issued a circular on the conversion of foreign currency into Renminbi by a foreign-invested company that regulates how the converted Renminbi may be used. The circular requires that the registered capital of a foreign-invested enterprise converted into Renminbi from foreign currencies may only be utilized for purposes within its business scope. For example, such converted amounts may not be used for investments in or acquisitions of other PRC companies, unless specifically provided otherwise, which can inhibit the ability of companies to consummate such transactions. In addition, SAFE strengthened its oversight of the flow and use of the Renminbi registered capital of foreign-invested enterprises converted from foreign currencies. The use of such Renminbi capital may not be changed without SAFE’s approval, and may not in any case be used to repay Renminbi loans if the proceeds of such loans have not been utilized. Violations may result in severe penalties, such as heavy fines.

Regulations Relating to Labor

Pursuant to the PRC Labor Law effective in 1995 and the PRC Labor Contract Law effective in 2008, a written labor contract is required when an employment relationship is established between an employer and an employee. Other labor-related regulations and rules of the PRC stipulate the maximum number of working hours per day and per week as well as the minimum wages. An employer is required to set up occupational safety and sanitation systems, implement the national occupational safety and sanitation rules and standards, educate employees on occupational safety and sanitation, prevent accidents at work, and reduce occupational hazards.

In the PRC, workers dispatched by an employment agency are normally engaged in temporary, auxiliary, or substitute work. Pursuant to the PRC Labor Contract Law, an employment agency is the employer for workers dispatched by it and must perform an employer’s obligations toward them. The employment contract between the employment agency and the dispatched workers, and the placement agreement between the employment agency and the company that receives the dispatched workers must be in writing. Also, the company that accepts the dispatched workers must bear joint and several liabilities for any violation of the Labor Contract Law by the employment agencies arising from their contracts with dispatched workers. An employer is obligated to sign an indefinite term labor contract with an employee if the employer continues to employ the employee after two consecutive fixed-term labor contracts. The employer also has to pay compensation to the employee if the employer terminates an indefinite term labor contract. Except where the employer proposes to renew a labor contract by maintaining or raising the conditions of the labor contract and the employee is not agreeable to the renewal, an employer is required to compensate the employee when a definite term labor contract expires. Furthermore, under the Regulations on Paid Annual Leave for Employees issued by the State Council in December 2007 and effective as of January 2008, employees who have served an employer for more than one (1) year and less than ten years are entitled to a 5-day paid vacation, those whose service period ranges from 10 to 20 years are entitled to a 10-day paid vacation, and those who have served for more than 20 years are entitled to a 15-day paid vacation. An employee who does not use such vacation time at the request of the employer shall be compensated at three times their normal salaries for each waived vacation day.

Pursuant to the Regulations on Occupational Injury Insurance effective in 2004 and the Interim Measures concerning the Maternity Insurance for Enterprise Employees effective in 1995, PRC companies must pay occupational injury insurance premiums and maternity insurance premiums for their employees. Pursuant to the Interim Regulations on the Collection and Payment of Social Insurance Premiums effective in 1999 and the Interim Measures concerning the Administration of the Registration of Social Insurance effective in 1999, basic pension insurance, medical insurance, and unemployment insurance are collectively referred to as social insurance. Both PRC companies and their employees are required to contribute to the social insurance plans. Pursuant to the Regulations on the Administration of Housing Fund effective in 1999, as amended in 2002, PRC companies must register with applicable housing fund management centers and establish a special housing fund account in an entrusted bank. Both PRC companies and their employees are required to contribute to the housing funds. The PRC Subsidiaries and Arki Network Service are in process of applying for registration for social insurance and opening a housing fund account.

Regulations on Dividend Distribution

Wholly foreign-owned companies in the PRC may pay dividends only out of their accumulated profits after tax as determined in accordance with PRC accounting standards. Remittance of dividends by a wholly foreign-owned enterprise out of China is subject to examination by the banks designated by SAFE. Wholly foreign-owned companies may not pay dividends unless they set aside at least 10% of their respective accumulated profits after tax each year, if any, to fund certain reserve funds, until such time as the accumulative amount of such fund reaches 50% of the wholly foreign-owned company’s registered capital. In addition, these companies also may allocate a portion of their after-tax profits based on PRC accounting standards to staff welfare and bonus funds at their discretion. These reserve funds and staff welfare and bonus funds are not distributable as cash dividends.

Safe Regulations on Offshore Special Purpose Companies Held by PRC Residents or Citizens

Pursuant to the Notice on Relevant Issues Concerning Foreign Exchange Administration for PRC Residents to Engage in Financing and Inbound Investment via Overseas Special Purpose Vehicles, or Circular No. 75, issued in October 2005 by SAFE and its supplemental notices, PRC citizens or residents are required to register with SAFE or its local branch in connection with their establishment or control of an offshore entity established for the purpose of overseas equity financing involving a roundtrip investment whereby the offshore entity acquires or controls onshore assets or equity interests held by the PRC citizens or residents. In addition, such PRC citizens or residents must update their SAFE registrations when the offshore special purpose vehicle undergoes material events relating to increases or decreases in investment amount, transfers or exchanges of shares, mergers or divisions, long-term equity or debt investments, external guarantees, or other material events that do not involve roundtrip investments. Subsequent regulations further clarified that PRC subsidiaries of an offshore company governed by the SAFE regulations are required to coordinate and supervise the filing of SAFE registrations in a timely manner by the offshore holding company’s shareholders who are PRC citizens or residents. If these shareholders fail to comply, the PRC subsidiaries are required to report to the local SAFE branches. If the shareholders of the offshore holding company who are PRC citizens or residents do not complete their registration with the local SAFE branches, the PRC subsidiaries may be prohibited from distributing their profits and proceeds from any reduction in capital, share transfer or liquidation to the offshore company, and the offshore company may be restricted in its ability to contribute additional capital to its PRC subsidiaries. Moreover, failure to comply with the SAFE registration and amendment requirements described above could result in liability under PRC law for evasion of applicable foreign exchange restrictions.

M&A Rules

On August 8, 2006, six PRC regulatory agencies, including China Securities Regulatory Commission (“CSRC”), promulgated a rule entitled Provisions Regarding Mergers and Acquisitions of Domestic Enterprises by Foreign Investors (“the M&A Rules”) to regulate foreign investment in PRC domestic enterprises. The M&A rules, among other things, requires an overseas special purpose vehicle(“SPV”), formed for listing purposes through acquisitions of PRC domestic companies and controlled by PRC companies or individuals, to obtain the approval of CSRC prior to publicly listing their securities on an overseas stock exchange. We believe that while the CSRC generally has jurisdiction over overseas listings of SPVs like us, CSRC’s approval is not required for this offering given the fact that no provision in the M&A Rules classifies the respective contractual arrangements between Arki Network Service and Arki Beijing and between Arki Network Service and Arki Fuxin as a type of acquisition transaction falling under the M&A Rules. There remains some uncertainty as to how this regulation will be interpreted or implemented in the context of an overseas offering. If the CSRC or another PRC regulatory agency subsequently determines that approval is required for this offering, we may face sanctions by the CSRC or another PRC regulatory agency.

The M&A Rules also establish procedures and requirements that could make some acquisitions of Chinese companies by foreign investors more time-consuming and complex, including requirements in some instances that the Ministry of Commerce be notified in advance of any change-of-control transaction in which a foreign investor takes control of a Chinese domestic enterprise.

Safe Regulations on Employee Share Options

On March 28, 2007, SAFE promulgated the Application Procedure of Foreign Exchange Administration for Domestic Individuals Participating in Employee Share Holding Plan or Share Option Plan of Overseas Listed Company, or the Share Option Rule. Pursuant to the Share Option Rule, Chinese citizens who are granted share options by an overseas publicly listed company are required to register with SAFE through a Chinese agent or Chinese subsidiary of the overseas publicly listed company and complete certain other procedures. Our PRC employees who have been granted share options will be subject to these regulations. Failure of our PRC share option holders to complete their SAFE registrations may subject these PRC employees to fines and legal sanctions and may also limit our ability to contribute additional capital into our PRC subsidiaries and limit our PRC subsidiaries’ ability to distribute dividends to us.

Employees

As of March 4, 2014, we had approximately 18 full-time employees and no part-time employees.

Item 1A. Risk Factors.

Smaller reporting companies are not required to provide the information required by this item.

Item 1B. Unresolved Staff Comments.

Smaller reporting companies are not required to provide the information required by this item.

Item 2. Properties.

Our current principal executive offices are located at 100 Park Avenue, 16th Floor, New York 10017. The table below provides a general description of our offices and facilities, including those for our international operations:

| Location | Principal Activities | Area (sq. ft.) | Lease Expiration Date | |||||

| 100 Park Avenue, 16th Floor, New York 10017 | Company headquarters | 170 | Expires on October 31, 2014. | |||||

| No. 3B & 5, Floor 25, Unit 2503, No. 77, Jianguo Road Chaoyang District, Beijing People’s Republic of China | PRC operations headquarter Arki Beijing’s office | 7,065 | Expires on October 20, 2016. | |||||

The minimum future commitments under lease agreements payable as of December 31, 2013 are as follows:

| Year | Amount | |||||

| 2014 | $ | 569,026 | ||||

| 2015 | 540,576 | |||||

| 2016 | 435,464 | |||||

| Total | $ | 1,545,066 | ||||

Item 3. Legal Proceedings.

Except as set forth below, there are no material pending legal proceedings to which the Company, any executive officer, any owner of record or beneficially of more than five percent of any class of voting securities is a party or of which any of our property is the subject.

On May 23, 2012 three individuals filed claims for unpaid salaries against Arki Network Service Beijing Co., Ltd., our variable interest entity in China (“Arki Network”) with the BeiingChaoyang District Personnel Dispute Arbitration Commissions (“the Arbitration Commission”). On November 12, 2012, the Arbitration Commission found that Arki Network shall pay such three individuals a total $65,765 for unpaid salaries and a fine for hiring employees without an employment agreement. On November 21, 2012, Arki Network filed a claim with The People’s Court of Beijing Chao Yang Division (the “Chao Yang Division Court”) challenging the findings of the Arbitration Commission on the ground that there were no employment relationships between Arki Network and any of the discussed individuals. On August 20, 2013, the Chao Yang Division Court decided that the findings of the Arbitration Commission have no legal effect because there were no employment relationships between Arki Network and any of the discussed individuals. The three individuals have appealed the Chao Yang Division Court’s rulings to the Third Intermediate People’s Court of Beijing (the “Intermediate Court”). On November 19, 2013, the Intermediate Court issued its decision that the ruling of the Chao Yang Division Court stayed. As a result, the findings of the Arbitration Commission have no legal effect and Arki Network is not legally liable to the three individuals for any payment.

On June 12, 2012, an individual filed a claim against Arki Network with the Court for unpaid salaries. On December 12, 2012, the Court dismissed all the claims brought by such individual against Arki Network. Such individual did not appeal to a higher court within required time period. The decision by the Court on December 12, 2012 became effective and final on December 27, 2012.

Item 4. Mine Safety Disclosures

Not Applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases Of Equity Securities.

Market Information

Our common stock has been quoted on the OTC Bulletin Board under the symbol “MNDM” since April 1, 2010. Beginning on February 23, 2011, our symbol was changed to “CCGN”. The following table sets forth the range of the quarterly high and low bid price information for the years ended December 31, 2013 and 2012 as reported by the OTC Bulletin Board.

| Fiscal Year 2013 | High | Low | ||||||

| First Quarter | $ | 5.00 | $ | 2.50 | ||||

| Second Quarter | $ | 5.95 | $ | 3.15 | ||||

| Third Quarter | $ | 4.48 | $ | 2.30 | ||||

| Fourth Quarter | $ | 14.50 | $ | 3.05 | ||||

| Fiscal Year 2012 | High | Low | ||||||

| First Quarter | $ | 10.00 | $ | 3.60 | ||||

| Second Quarter | $ | 12.33 | $ | 9.00 | ||||

| Third Quarter | $ | 9.00 | $ | 3.50 | ||||

| Fourth Quarter | $ | 8.00 | $ | 1.50 | ||||

* The quotations of the closing prices reflect inter-dealer prices, without retail mark-up, markdown or commission, and may not necessarily represent actual transactions.

The market price of our common stock is subject to significant fluctuations in response to variations in our quarterly operating results, general trends in the market, and other factors, over many of which we have little or no control. In addition, broad market fluctuations, as well as general economic, business and political conditions, may adversely affect the market for our common stock, regardless of our actual or projected performance.

Holders of Our Common Stock

As of March 4, 2014, we had approximately 9,231 shareholders of record of our common stock.

Dividends

Under applicable PRC regulations, foreign-invested enterprises in the PRC may pay dividends only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, a foreign-invested enterprise in the PRC is required to set aside at least 10% of its after-tax profit (determined in accordance with PRC accounting standards) each year to its general reserves until the accumulative amount of such reserves reach 50% of its registered capital. These reserves are not distributable as cash dividends.

We have not paid dividends on our common stock and do not anticipate paying such dividends in the foreseeable future. We will rely on dividends from our PRC Operating Entities for our funds and PRC regulations (described above) may limit the amount of funds distributable to us from our PRC Operating Entities, which will affect our ability to declare any dividends.

Recent Sales of Unregistered Securities

On June 14, 2013, the Company entered into a Securities Purchase Agreement with Asher Enterprises, Inc. (“Asher Enterprises”) pursuant to which the Company sold and issued to Asher Enterprises a promissory note with a principal amount of $78,500 (the “Note”). The issuance of this Note was exempt from the registration requirements of the Securities Act, pursuant to Section 4(2) thereof as a transaction by an issuer not involving a public offering.

On January 21, 2014, Asher Enterprises converted $15,000 of convertible loan into 4,098 shares of common stock at conversion price of $3.66 per share. The issuance of these shares was exempt from the registration requirements of the Securities Act, pursuant to Section 4(2) thereof as a transaction by an issuer not involving a public offering.

Item 6. Selected Financial Data.

Smaller reporting companies are not required to provide the information required by this item.

Item 7. Management’s Discussion and Analysis of Financial Conditions and Results of Operations.

The following discussion and analysis of financial condition and results of operations relates to the operations and financial condition reported in the audited condensed consolidated financial statements of the Company for the fiscal years ended December 31, 2013 and 2012, and should be read in conjunction with such financial statements and related notes included in this report. Those statements in the following discussion that are not historical in nature should be considered to be forward looking statements that are inherently uncertain. Actual results and the timing of the events may differ materially from those contained in these forward looking statements due to a number of factors, including those discussed in the “Cautionary Note on Forward Looking Statements” set forth elsewhere in this Annual Report.

FORWARD-LOOKING STATEMENTS:

Certain statements made in this Annual Report on Form 10-K are “forward-looking statements” (within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934) regarding the plans and objectives of management for future operations. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. These statements use words such as “believe,” “expect,” “should,” “strive,” “plan,” “intend,” “estimate,” “anticipate” or similar expressions. The forward-looking statements included herein are based on current beliefs, assumptions, and are subject to numerous risks and uncertainties. You should carefully read the risk factor disclosure contained in “Item 1A. Risk Factors” of this Annual Report on Form 10-K, where we discuss many of the important factors currently known to management that could cause actual results to differ materially from those in our forward-looking statements. Our plans and objectives are based, in part, on assumptions of the continuing expansion of business. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions, and future business decisions, all of which are difficult or impossible to predict accurately, and many of which are beyond our control. Although we believe our assumptions underlying the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. These forward-looking statements are made as of the date of this report, and we assume no obligation to update these forward-looking statements whether as a result of new information, future events, or otherwise, other than as required by law. In light of these assumptions, risks, and uncertainties, the forward-looking events discussed in this report might not occur and actual results and events may vary significantly from those discussed in the forward-looking statements.

Overview

We are primarily engaged in two different businesses: e-commerce services and meat distribution. We operate an online retail platform in China at www.ccmus.com through Arki (Beijing) E-Commerce Technology Corp., our wholly owned subsidiary, and an online retail platform at www.ccgusa.com in the United States. We operate our meat distribution business through Beijing Beitun Trading Co., Ltd., our 51% owned subsidiary. In addition to e-commerce services and meat distribution, we have been working to develop a debit card business, through America Arki Fuxin Network Management Co. Ltd., our wholly owned subsidiary.

Our online retail platforms allow third-party merchants to sell their general merchandise products directly to consumers in China and the United States. We charge third-party merchants a service fee of approximately 5% of the total purchase price with respect to their general merchandise sold through our website. We also receive advertising fees from third-party merchants if they advertise products through our website. To incentivize our customers, we give our member customers bonus points for each purchase, to be used for cash value in their next purchase. As our customers accumulate bonus points, they receive membership upgrade, special discounts and additional bonus points. Our member customers may also receive awards from our daily sweepstakes program.

Through Beijing Beitun Trading Co., Ltd., we purchase meats from suppliers and distribute them to restaurants and food producers in China.

We collaborate with Bank of Fuxin to issue cobranded debit cards. We plan to charge participating merchants a transaction fee of 1% to 5% for each purchase using our cobranded debit cards. We intend to give our cardholders cash rewards with their purchases through our online retail platform. As of December 31, 2013, our cooperation with Fuxin becomes very minimum. We are seeking to collaborate with other banks for debit card business cooperation. We have not realized any revenue from this segment of business. We expect to start our debit card operation in 2014.

Results of Operations

Comparison of years ended December 31, 2013 and December 31, 2012

Revenues

We derive our revenues from our e-commerce business and meat distribution business. We have not generated any revenue from our debit card business. Our net revenues for the year ended December 31, 2013 decreased to $5,848,228 from $6,823,880 for the year ended December 31, 2012, a decrease of $972,652 or 14.3%. The following table sets forth a breakdown of our revenues for the periods indicated:

| Year ended December 31, | Increase (decrease) in | Increase (decrease) in | ||||||||||||||

| 2013 | 2012 | dollar amount | percentage | |||||||||||||

| Net revenue – e-commerce business | $ | 5,681 | $ | 1,153,389 | $ | (1,147,708 | ) | (99.5 | )% | |||||||

| Net revenue – meat distribution business | $ | 5,842,547 | $ | 5,670,491 | $ | 172,056 | 3.0 | % | ||||||||

| Net revenue – debit card business | $ | — | $ | — | $ | — | — | |||||||||

| Total Revenue | $ | 5,848,228 | $ | 6,823,880 | $ | (975,652 | ) | (14.3 | )% | |||||||

E-commerce Business

Our net revenues from e-commerce business for the year ended December 31, 2013 decreased to $5,681 from $1,153,389 for the year ended December 31, 2012, a decrease of $1,147,708 or 99.5%. The decrease was primarily due to the diversion of attention of management from the existing operation of this segment as the Company is making changes to its current e-commerce business model. The Company is working to re-focus its e-commerce business on selling collections.

Meat Distribution Business

Our net revenues from meat distribution business for the year ended December 31, 2013 increased to $5,842,547 in the year ended December 31, 2013 from $5,670,491 for the year ended December 31, 2012, an increase of $172,056 or 3.0%. The increase was attributed to increased demand in the year ended December 31, 2013.

Debit Card Business

Our debit card business has not generated any revenue as of December 31, 2013.

Cost of Sales

Cost of sales includes costs of our products, shipping charges from the suppliers and to our customers, and costs of packaging material associated with our meat distribution business. Cost and expenses associated with our e-commerce business, such as processing costs and transaction costs, are recognized as our selling expenses in our consolidated statements of operations and comprehensive income. Our cost of sales for the year ended December 31, 2013 increased to $5,767,654 from $5,595,790 for the year ended December 31, 2012, an increase of $171,864 or 3.1%. The increase was in line with the increase in revenues from the meat distribution business.

Gross Profit

Our gross profit for the year ended December 31, 2013 decreased to $80,574 from $1,228,090 for the year ended December 31, 2012, a decrease of $1,147,516 or 93.4%. The decrease was primarily due to a decrease in sales from e-commerce business. Our gross profit margin for the year ended December 31, 2013 decreased to 1.4% from 18.0% for the year ended December 31, 2012. The decrease of our gross profit margin was primarily due to an increase in percentage of revenues from the relatively low-profit margin meat distribution business.

Operating Expenses

Our operating expenses consist of selling expenses, and general and administrative expenses. Our total operating expenses for the year ended December 31, 2013 decreased to $1,045,509 from $2,561,388 for the year ended December 31, 2012, a decrease of $1,515,879 or 59.2%. The following table sets forth a breakdown of our operating expenses for the periods indicated:

| Year ended December 31, | Increase (decrease) in | Increase (decrease) in | ||||||||||||||

| 2013 | 2012 | dollar amount | percentage | |||||||||||||

| Selling expenses for e-commerce business | $ | 59,403 | $ | 937,080 | $ | (877,677 | ) | (93.7 | )% | |||||||

| Selling expenses for meat distribution business | $ | 53,504 | $ | 48,435 | $ | 5,069 | 10.5 | % | ||||||||

| Sub-total | $ | 112,907 | $ | 985,515 | $ | (872,608 | ) | (88.5 | )% | |||||||

| General & administrative expenses for e-commerce business | $ | 917,559 | $ | 1,556,555 | $ | (638,996 | ) | (41.1 | )% | |||||||

| General & administrative expenses for meat distribution business | $ | 15,043 | $ | 19,318 | $ | (4,275 | ) | (22.1 | )% | |||||||

| Sub-total | $ | 932,602 | $ | 1,575,873 | $ | (643,271 | ) | (40.8 | )% | |||||||

| Total | $ | 1,045,509 | $ | 2,561,388 | $ | (1,515,879 | ) | (59.2 | )% | |||||||

Selling expenses for the year ended December 31, 2013 decreased to $112,907 from $985,515 for the year ended December 31, 2012, a decrease of $872,608 or 88.5%. Selling expenses for the e-commerce business for the year ended December 31, 2013 decreased to $59,403 from $937,080 for the year ended December 31, 2012, a decrease of $877,677, or 93.7%. The decrease was in line with the decrease in sales in our e-commerce business. Selling expenses for the meat distribution business for the years ended December 31, 2013 and 2012 were $53,504 and $48,435, respectively. The selling expenses for the meat distribution business do not increase or decrease along with the increase or decrease in revenue, because the selling expenses mainly consist of non-commission based salaries for sales staff and shipping and handling expenses that only incur if a customer requests shipping instead of self picking-up.

General and administrative expenses for the year ended December 31, 2013 decreased to $932,602 from $1,575,873 for the year ended December 31, 2012, a decrease of $643,271, or 40.8%. The decrease was primarily due to a decrease of $420,000 in share-based compensation expenses.

Liquidity and Capital Resources

Cash flows

| Year ended December 31, | ||||||||

| Net cash generated from /(used in) | 2013 | 2012 | ||||||

| Operating activities | $ | (838,664 | ) | $ | (1,783,227 | ) | ||

| Investing activities | $ | — | $ | — | ||||

| Financing activities | $ | 763,724 | $ | 1,342,942 | ||||

| Net decrease in cash | $ | (72,562 | ) | $ | (445,565 | ) | ||

Operating Activities

The net cash used in operating activities was $838,664 for the year ended December 31, 2013, which was primarily due to our net loss of $699,793, an increase of inventories of $62,240, a decrease in accounts payable of $86,654, a decrease in payable to Caesar Capital Management Ltd. of $42,160, and an increase of advance to suppliers of $449,891, partially offset by a decrease of prepaid expenses of $72,262, and a decrease of accounts receivable of $446,068.