UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

FORM 10-Q

(Mark One)

þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended July 31, 2012

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

COMMISSION FILE NUMBER: 333-152002

DAULTON CAPITAL CORP.

(Name of Registrant as specified in its charter)

| NEVADA | 30-0459858 | |

| (State or other jurisdiction of incorporation of organization) | (I.R.S. Employer Identification No.) |

Level 13- 40 Creek St

Brisbane QLD Australia 4000

(Address of principal executive office)

(888) 408-9402

(Registrant’s telephone number)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o |

|

Non-accelerated filer (Do not check if smaller reporting company) |

o | Smaller reporting company | þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes o No þ

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date. 4,418,240,003 shares of common stock are issued and outstanding as of January 18, 2013.

| 1 |

DAULTON CAPITAL CORP.

FORM 10-Q/A

July 31, 2012

TABLE OF CONTENTS

| Page No. | ||||

| PART I. - FINANCIAL INFORMATION | ||||

| Item 1. | Financial Statements. | 4 | ||

| Consolidated Balance Sheets as of July 31, 2012 (Unaudited) and April 30, 2012 | 4 | |||

| Consolidated Statements of Operations and Comprehensive Income (loss) for the Three Months Ended July 31, 2012 and 2011 (Unaudited) | 5 | |||

| Consolidated Statements of Changes in Stockholder’s Equity (Deficit) - For the Period from May 28, 2010 (Inception) to July 31, 2012 (Unaudited) | 6 | |||

| Consolidated Statements of Cash Flows for the Three Months Ended July 31, 2012 and 2011 (Unaudited) | 7 | |||

| Notes to Unaudited Consolidated Financial Statements. | 8-16 | |||

| Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations. | 21 | ||

| Item 3 | Quantitative and Qualitative Disclosures About Market Risk. | 26 | ||

| Item 4 | Controls and Procedures. | 26 | ||

PART II - OTHER INFORMATION | ||||

| Item 1. | Legal Proceedings. | 27 | ||

| Item 1A. | Risk Factors. | 27 | ||

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds. | 27 | ||

| Item 3. | Defaults Upon Senior Securities. | 27 | ||

| Item 4. | Mine Safety Disclosures. | 27 | ||

| Item 5. | Other Information. | 27 | ||

| Item 6. | Exhibits. | 27 | ||

EXPLANATORY NOTE

The purposes of this Amendment No. 1 on Form 10–Q/A to the quarterly report on Form 10–Q for the quarter ended July 31, 2012, filed with the Securities and Exchange Commission on September 21, 2012 (the “Form 10–Q”), is as follows:

Management determined that as of July 31, 2012 and April 30, 2012 and for the periods ended July 31, 2012 and 2011, the consolidated financial statements did not properly reflect the reorganization and recapitalization of the Daulton Capital Corp. On May 22, 2012, the Company, Grimsby Investments Limited (“Grimsby”), and the stockholders of Grimsby (“Grimsby Shareholders”) entered into a Share Exchange. Upon closing of the transaction contemplated under the Share Exchange, as amended, on May 22, 2012, the Grimsby Shareholders (4 entities) transferred all of the issued and outstanding capital stock of Grimsby to us in exchange for an aggregate of 4.148 billon shares of our common stock and a commitment to pay royalties of $7,500,000 to two original founding stockholders of Grimsby, one of which is an officer and director of the Company, as amended retroactively in August 2012 for an original $150 million debt to the four original founding stockholders of Grimsby. Such exchange caused Grimsby to become our wholly-owned subsidiary.

The Share Exchange should have been accounted for as a reverse-merger and recapitalization since the stockholders of Grimsby obtained voting and management control of the Company. Grimsby was the acquirer for financial reporting purposes and Daulton was the acquired company. Consequently, the assets and liabilities and the operations reflected in the historical financial statements prior to the Exchange Agreement should be those of Grimsby and recorded at the historical cost basis of Grimsby, and the consolidated financial statements after completion of the Share Exchange should have included the assets and liabilities of both Grimsby and the Company and the Company’s consolidated operations from the closing date of the Share Exchange.

Accordingly, we restated our unaudited interim consolidated balance sheets as of July 31, 2012 and the consolidated statements of operations and comprehensive income (loss) and our consolidated statements of cash flows for the periods ended July 31, 2012 and 2011. Additionally, we revised all of our disclosures in the notes to the consolidated financial statements and management’s discussion and analysis.

This Amendment No. 1 to the Form 10-Q for the period ended July 31, 2012 contains currently dated certifications as Exhibits 31.1, 31.2, 32.1 and 32.2. We modified and updated all of our disclosures presented in the Form 10-Q as previously filed and reflected events occurring after the filing of the original Form 10-Q and included modified and updates disclosures for subsequent events.

| 2 |

FORWARD LOOKING STATEMENTS

This report contains forward-looking statements regarding our business, financial condition, results of operations and prospects. Words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates” and similar expressions or variations of such words are intended to identify forward-looking statements, but are not deemed to represent an all-inclusive means of identifying forward-looking statements as denoted in this report. Additionally, statements concerning future matters are forward-looking statements.

Although forward-looking statements in this report reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by us. Consequently, forward-looking statements are inherently subject to risks and uncertainties and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, those specifically addressed under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our report on Form 8-K/A as filed with the Securities and Exchange Commission on January 22, 2013, in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Form 10-Q/A and in other reports that we file with the SEC. You are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this report.

We file reports with the SEC. The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us. You can also read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You can obtain additional information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report, except as required by law. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this quarterly report, which are designed to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

| 3 |

PART 1 - FINANCIAL INFORMATION

Item 1. Financial Statements.

ARX GOLD CORPORATION AND SUBSIDIARIES

(FORMERLY DAULTON CAPITAL CORP.)

(A DEVELOPMENT STAGE COMPANY)

CONSOLIDATED BALANCE SHEETS

| July 31, | April 30, | |||||||

| 2012 | 2012 | |||||||

| (Unaudited) | ||||||||

| (As Restated) | ||||||||

| ASSETS | ||||||||

| Current Assets: | ||||||||

| Cash | $ | 5,625 | $ | – | ||||

| Due from related party | 851 | 850 | ||||||

| Total Current Assets | 6,476 | 850 | ||||||

| Total Assets | $ | 6,476 | $ | 850 | ||||

| LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT) | ||||||||

| Current Liabilities: | ||||||||

| Loans payable | $ | 5,100 | $ | – | ||||

| Accounts payable | 64,045 | – | ||||||

| Accrued expenses | 20,068 | 64 | ||||||

| Due to related party | 527 | – | ||||||

| Total Current Liabilities | 89,740 | 64 | ||||||

| Total Liabilities | 89,740 | 64 | ||||||

| COMMITMENTS AND CONTINGENCIES (Note 8) | ||||||||

| Stockholders' Equity (Deficit): | ||||||||

| Common stock $0.001 par value; 5,000,000,000 shares authorized; 4,413,240,003 and 4,148,000,000 issued and outstanding at July 31, 2012 and April 30, 2012, respectively | 4,413,240 | 4,148,000 | ||||||

| Additional paid-in capital | (4,325,025 | ) | (4,084,239 | ) | ||||

| Deficit accumulated during development stage | (171,571 | ) | (63,077 | ) | ||||

| Accumulated other comprehensive income | 92 | 102 | ||||||

| Total Stockholders' Equity (Deficit) | (83,264 | ) | 786 | |||||

| Total Liabilities and Stockholders' Equity (Deficit) | $ | 6,476 | $ | 850 | ||||

See accompanying notes to the consolidated financial statements.

| 4 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(FORMERLY DAULTON CAPITAL CORP.)

(A DEVELOPMENT STAGE COMPANY)

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS)

| For the Three Months Ended July 31, | For the Three Months Ended July 31, | For the Period from May 28, 2010 (Inception) to July 31, | ||||||||||

| 2012 | 2011 | 2012 | ||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | ||||||||||

| (As Restated) | (As Restated) | (As Restated) | ||||||||||

| REVENUES | $- | $- | $- | |||||||||

| OPERATING EXPENSES: | ||||||||||||

| Compensation | – | – | 62,826 | |||||||||

| Professional fees | 106,063 | – | 106,063 | |||||||||

| General and administrative | 2,431 | 32 | 2,682 | |||||||||

| Total Operating Expenses | 108,494 | 32 | 171,571 | |||||||||

| LOSS FROM OPERATIONS | (108,494 | ) | (32 | ) | (171,571 | ) | ||||||

| NET LOSS | $ | (108,494 | ) | $ | (32 | ) | $ | (171,571 | ) | |||

| COMPREHENSIVE LOSS: | ||||||||||||

| NET LOSS | $ | (108,494 | ) | $ | (32 | ) | $ | (171,571 | ) | |||

| OTHER COMPREHENSIVE INCOME(LOSS): | ||||||||||||

| Unrealized foreign currency translation Income (loss) | (10 | ) | 2 | 92 | ||||||||

| COMPREHENSIVE LOSS | $ | (108,504 | ) | $ | (30 | ) | $ | (171,479 | ) | |||

| Net Loss per Common Share (Basic and Diluted) | $ | – | $ | – | ||||||||

| Weighted Average Shares Outstanding:- Basic and Diluted | 4,349,813,046 | 4,148,000,000 | ||||||||||

See accompanying notes to the consolidated financial statements.

| 5 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(FORMERLY DAULTON CAPITAL CORP.)

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY (DEFICIT)

(A DEVELOPMENT STAGE COMPANY)

(AS RESTATED)

For the Period from May 28, 2010 (Inception) to July 31, 2012

| Common Stock | Additional Paid-in | Deficit Accumulated During Development | Accumulated Other Comprehensive | Total Stockholders' Equity | ||||||||||||||||||||

| Shares | Amount | Capital | Stage | Income (Loss) | (Deficit) | |||||||||||||||||||

| Balance, May 28, 2010 (Inception) | – | $ | – | $ | – | $ | – | $ | – | $ | – | |||||||||||||

| Common stock issued to founders | 4,148,000,000 | 4,148,000 | (4,148,000 | ) | – | – | – | |||||||||||||||||

| Cash contributed by founders | – | – | 420 | – | – | 420 | ||||||||||||||||||

| Net loss for period | – | – | – | (96 | ) | – | (96 | ) | ||||||||||||||||

| Comprehensive income | – | – | – | – | 113 | 113 | ||||||||||||||||||

| Balance, April 30, 2011 | 4,148,000,000 | 4,148,000 | (4,147,580 | ) | (96 | ) | 113 | 437 | ||||||||||||||||

| Cash contributed by founders | – | – | 515 | – | – | 515 | ||||||||||||||||||

| Stock-based compensation | – | – | 62,826 | – | – | 62,826 | ||||||||||||||||||

| Net loss for year | – | – | – | (62,981 | ) | – | (62,981 | ) | ||||||||||||||||

| Comprehensive loss | – | – | – | – | (11 | ) | (11 | ) | ||||||||||||||||

| Balance, April 30, 2012 | 4,148,000,000 | 4,148,000 | (4,084,239 | ) | (63,077 | ) | 102 | 786 | ||||||||||||||||

| Recapitalization of Company | 265,240,003 | 265,240 | (285,490 | ) | – | – | (20,250 | ) | ||||||||||||||||

| Contributed services | – | – | 44,704 | – | – | 44,704 | ||||||||||||||||||

| Net loss for the three months ended July 31, 2012 | – | – | – | (108,494 | ) | – | (108,494 | ) | ||||||||||||||||

| Comprehensive income | – | – | – | – | (10 | ) | (10 | ) | ||||||||||||||||

| Balance, July 31, 2012 (Unaudited) | 4,413,240,003 | $ | 4,413,240 | $ | (4,325,025 | ) | $ | (171,571 | ) | $ | 92 | $ | (83,264 | ) | ||||||||||

See accompanying notes to the consolidated financial statements.

| 6 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(FORMERLY DAULTON CAPITAL CORP.)

(A DEVELOPMENT STAGE COMPANY)

CONSOLIDATED STATEMENTS OF CASH FLOWS

| For the Three Months Ended July 31, | For the Three Months Ended July 31, | For the Period from May 28, 2010 (Inception) to July 31, | ||||||||||

| 2012 | 2011 | 2012 | ||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | ||||||||||

| (As Restated) | (As Restated) | (As Restated) | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||||||

| Net loss | $ | (108,494 | ) | $ | (32 | ) | $ | (171,571 | ) | |||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||||||

| Stock-based compensation | – | – | 62,826 | |||||||||

| Contributed services | 44,704 | – | 44,704 | |||||||||

| Changes in assets and liabilities: | ||||||||||||

| Due from related party | – | 11 | (815 | ) | ||||||||

| Accounts payable | 63,784 | – | 63,784 | |||||||||

| Accrued expenses | 4 | 10 | 68 | |||||||||

| NET CASH USED IN OPERATING ACTIVITIES | (2 | ) | (11 | ) | (1,004 | ) | ||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||||||

| Proceeds from loans | 5,100 | – | 5,100 | |||||||||

| Advances from related party | 520 | – | 520 | |||||||||

| Shareholder contribution | – | – | 935 | |||||||||

| NET CASH PROVIDED BY FINANCING ACTIVITIES | 5,620 | – | 6,555 | |||||||||

| Effect of Exchange Rate Changes on Cash | 7 | – | 74 | |||||||||

| Net Increase (Decrease) in Cash | 5,625 | (11 | ) | 5,625 | ||||||||

| Cash, Beginning of Period | – | 11 | – | |||||||||

| Cash, End of Period | $ | 5,625 | $ | – | $ | 5,625 | ||||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | ||||||||||||

| Cash paid for interest | $ | – | $ | – | $ | – | ||||||

| Cash paid for income taxes | $ | – | $ | – | $ | – | ||||||

| NON-CASH INVESTING AND FINANCING ACTIVITIES: | ||||||||||||

| Increase in accounts payable in connection with recapitalization | $ | 250 | $ | – | $ | 250 | ||||||

| Increase in accrued expenses in connection with recapitalization | $ | 20,000 | $ | – | $ | 20,000 | ||||||

| Common stock issued to founders | $ | – | $ | – | $ | 4,148,000 | ||||||

See accompanying notes to the consolidated financial statements.

| 7 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

Note 1 - Organization and nature of operations

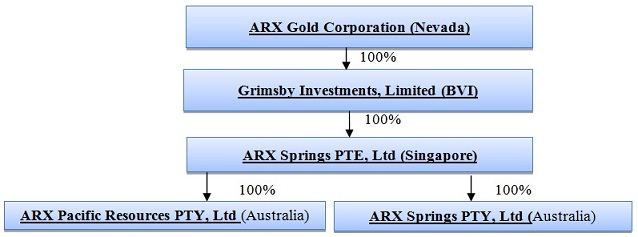

ARX Gold Corporation, formerly Daulton Capital Corp., (“ARX Gold”) was incorporated under the laws of the State of Nevada July 8, 2008. On May 22, 2012, ARX Gold, Grimsby Investments Limited (“Grimsby”), a company incorporated under the law of the British Virgin Islands on March 8, 2012, and the stockholders of Grimsby (“Grimsby Shareholders”) entered into a Share Exchange. Upon closing of the transaction contemplated under the Share Exchange, as amended, on May 22, 2012, the Grimsby Shareholders (4 entities) transferred all of the issued and outstanding capital stock of Grimsby to ARX Gold in exchange for an aggregate of 4.148 billon shares of the common stock of ARX Gold and a commitment to pay royalties of $7,500,000 to two original founding stockholders of Grimsby, as amended retroactively in August 2012 for an original $150 million debt to the four original founding stockholders of Grimsby. Such exchange caused Grimsby to become a wholly-owned subsidiary of ARX Gold. ARX Gold and Grimsby with its subsidiaries are collectively referred to as “the Company”.

The Share Exchange was accounted for as a reverse-merger and recapitalization since the stockholders of Grimsby obtained voting and management control of ARX Gold. Grimsby was the acquirer for financial reporting purposes and ARC Gold was the acquired company. Consequently, the assets and liabilities and the operations reflected in the historical financial statements prior to the Exchange Agreement will be those of Grimsby and was recorded at the historical cost basis of Grimsby, and the consolidated financial statements after completion of the Share Exchange included the assets and liabilities of both Grimsby and ARX Gold and the Company’s consolidated operations from the closing date of the Share Exchange.

On May 25, 2012, Daulton Capital Corp. changed its name to Celframe ARX Resources Corp. and on October 16, 2012, Celframe ARX Resources Corp. changes its name to ARX Gold Corporation.

On March 26, 2012, agents of Grimsby established ARX Springs Pte, Ltd., (“ARX Pte”), a company incorporated in Singapore, in anticipation of a future restructuring of the Company. At the time of its incorporation, ARX Pte had no operations, assets or stockholders.

On April 12, 2012, the one founding stockholder of ARX Springs Pty. Ltd a (“ARX Springs”), formed on November 11, 2011, and the two founding stockholders of ARX Pacific Resources Pty Ltd. (“ARX Pacific”), formed on May 28, 2010, transferred 100% of their respective ownerships in such companies to ARX Pte.

On May 15, 2012, in connection with a reorganization of Grimsby, 100% of the founders’ shares of ARX Pte were issued to Grimsby and Grimsby issued its founders shares to four entities. On May 22, 2012, immediately after the Share Exchange, the Company’s organizational structure of the Company is as follows:

Pursuant to certain mining rights agreements (see Note 3), ARX Pacific and ARX Springs, together referred to as the “ARX Companies”, have the rights to mine and extract gold and other materials from certain properties in Australia as described in Note 3.

| 8 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 2 - Summary of significant accounting policies

Basis of presentation

Management acknowledges its responsibility for the preparation of the accompanying interim financial statements which reflect all adjustments, consisting of normal recurring adjustments, considered necessary in its opinion for a fair statement of its financial position and the results of its operations for the interim period presented. These financial statements should be read in conjunction with the summary of significant accounting policies and notes to financial statements included in the Company’s filing of Form 8-K/A as filed with the Securities and Exchange Commission. The accompanying unaudited consolidated financial statements for ARX Gold Corporation have been prepared in accordance with accounting principles generally accepted in the United States of America (the “U.S.”) for interim financial information and with the instructions to Form 10-Q and Article 8-03 of Regulation S-X. Operating results for interim periods are not necessarily indicative of results that may be expected for the fiscal year as a whole.

As a result of the Company's focus on gold exploration, the Company is considered a development stage company as defined in ASC 915 “Development Stage Entities”. Activities during the development stage include implementation of the Company’s business plan, reorganization activities and fund raising. The Company plans on raising capital to implement its business plan and to begin development activities.

Going concern

As reflected in the accompanying consolidated financial statements, the Company had a net loss and net cash used in operations of $108,494 and $2, respectively, for the three months ended July 31, 2012 and a working capital deficit, stockholders’ deficit, and a deficit accumulated during development stage of $83,264, $83,264, and $171,571, respectively, at July 31, 2012 and has no revenues. The ability of the Company to continue as a going concern is dependent on the Company’s ability to raise additional capital, implement its business plan, and generate revenues. The consolidated financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern. The Company plans on raising capital though the sale of equity or debt instruments to commence operations.

Principles of consolidation

The consolidated financial statements are prepared in accordance with generally accepted accounting principles in the United States of America ("US GAAP") and present the consolidated financial statements of the Company and its wholly-owned subsidiaries as of July 31, 2012. In the preparation of consolidated financial statements of the Company, intercompany transactions and balances are eliminated in consolidation.

| 9 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 2 - Summary of significant accounting policies (continued)

Details of the Company’s subsidiaries are as follows:

| Name | Domicile and date of incorporation | Registered capital | Effective ownership | Principal activities | ||||

| Grimsby Investments Limited | British Virgin Islands March 8, 2012 |

$100 | 100% | Holding company | ||||

| ARX Springs Pte. | Republic of Singapore March 26, 2012 |

Singapore dollars (“S$”) 100,000 | 100% | Holding company | ||||

| ARX Springs Pty. Ltd. | Australia November 11, 2011 |

Australian dollars (“AUS$”) 30,000 | 100% | Pursuant to various agreements, ARX Springs has the right to explore, mine and extract gold and other minerals from certain properties. | ||||

| ARX Pacific Resources Pty. Ltd. | Australia May 28, 2010 |

AUS$ 1,000 | 100% | Pursuant to various agreements, ARX Pacific has the right to explore, mine and extract gold and other minerals from certain properties. |

Use of estimates

The preparation of the consolidated financial statements in conformity with generally accepted accounting principles in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from these estimates.

Fair value of financial instruments

The Company adopted the guidance of Accounting Standards Codification (“ASC”) 820 for fair value measurements which clarifies the definition of fair value, prescribes methods for measuring fair value, and establishes a fair value hierarchy to classify the inputs used in measuring fair value as follows:

| * | Level 1-Inputs are unadjusted quoted prices in active markets for identical assets or liabilities available at the measurement date. |

| * | Level 2-Inputs are unadjusted quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets and liabilities in markets that are not active, inputs other then quoted prices that are observable, and inputs derived from or corroborated by observable market data. |

| * | Level 3-Inputs are unobservable inputs which reflect the reporting entity’s own assumptions on what assumptions the market participants would use in pricing the asset or liability based on the best available information. |

The carrying amounts reported in the balance sheets for cash, due from related parties, and other current assets, accounts payable, and accrued expenses and due to related parties approximate their fair market value based on the short-term maturity of these instruments. The Company did not have any non-financial assets or liabilities that are measured at fair value on a recurring basis as of July 31, 2012 and April 30, 2012.

| 10 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 2 - Summary of significant accounting policies (continued)

Fair value of financial instruments (continued)

ASC 825-10 “Financial Instruments”, allows entities to voluntarily choose to measure certain financial assets and liabilities at fair value (fair value option). The fair value option may be elected on an instrument-by-instrument basis and is irrevocable, unless a new election date occurs. If the fair value option is elected for an instrument, unrealized gains and losses for that instrument should be reported in earnings at each subsequent reporting date. The Company did not elect to apply the fair value option to any outstanding instruments.

Cash and cash equivalents

For purposes of the consolidated statements of cash flows, the Company considers all highly liquid instruments purchased with a maturity of three months or less and money market accounts to be cash equivalents.

Mining property acquisition and exploration costs

The Company follows ASC 930 “Extraction Activities – Mining” in accounting for mining costs. Costs of lease, acquisition, exploration, carrying and retaining unproven mineral lease properties are expensed as incurred. The Company has chosen to expense all mineral acquisition and exploration costs as incurred given that it is still in the development stage. Once the Company has identified proven and probable reserves in its investigation of its properties and upon development of a plan for operating a mine, it would capitalize future costs until production is established. When a property reaches the production stage, the related capitalized costs will be depleted, using the units-of-production method over the estimated life of the probable-proven reserves. When the Company has capitalized mineral properties, these properties will be periodically assessed for impairment of value and any diminution in value. To date, the Company has not established the commercial feasibility of any exploration prospects; therefore, all costs are being expensed. During the three months ended July 31, 2012 and 2011, the Company did not incur any exploration costs.

Environmental Matters

Our operations are subject to evolving government environmental laws and regulations related to the discharge of materials into the environment. Our process is not expected to produce harmful levels of emissions or waste by-products. However, these laws and regulations would require us to remove or mitigate the environmental effects of the disposal or release of substances at our site should they occur. Compliance with such laws and regulations can be costly. Additionally, governmental authorities may enforce the laws and regulations with a variety of civil and criminal enforcement measures, including monetary penalties and remediation requirements. We are not aware of any area of non-compliance with governmental environmental laws and regulations as of the date of this report.

Asset retirement obligations

The Company follows the provisions of ASC 410, Asset Retirement and Environmental Obligations, which establishes standards for the initial measurement and subsequent accounting for obligations associated with the sale, abandonment or other disposal of long-lived tangible assets arising from the acquisition, construction or development and for normal operations of such assets. The Company did not have any asset retirement obligation at April 30, 2012 and 2011.

Impairment of long-lived assets

In accordance with ASC Topic 360, the Company reviews long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of the assets may not be fully recoverable, or at least annually. The Company recognizes an impairment loss when the sum of expected undiscounted future cash flows is less than the carrying amount of the asset. The amount of impairment is measured as the difference between the asset’s estimated fair value and its book value. The Company did not record any impairment charges for the three months ended July 31, 2012 and 2011.

| 11 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 2 - Summary of significant accounting policies (continued)

Advertising

Advertising is expensed as incurred and is included in selling expenses on the accompanying consolidated statements of operations. The Company did not incur advertising expenses during the three months ended July 31, 2012 and 2011, respectively.

Income taxes

The Company is governed by the income tax laws of the United States, Australia, the Republic of Singapore, and the British Virgin Islands. The Company accounts for income tax using the liability method prescribed by ASC 740, “Income Taxes”. Under this method, deferred tax assets and liabilities are determined based on the difference between the financial reporting and tax bases of assets and liabilities using enacted tax rates that will be in effect in the year in which the differences are expected to reverse. The Company records a valuation allowance to offset deferred tax assets if based on the weight of available evidence, it is more-likely-than-not that some portion, or all, of the deferred tax assets will not be realized. The effect on deferred taxes of a change in tax rates is recognized as income or loss in the period that includes the enactment date.

The Company applied the provisions of ASC 740-10-50, “Accounting for Uncertainty in Income Taxes”, which provides clarification related to the process associated with accounting for uncertain tax positions recognized in our financial statements. Audit periods remain open for review until the statute of limitations has passed. The completion of review or the expiration of the statute of limitations for a given audit period could result in an adjustment to the Company’s liability for income taxes. Any such adjustment could be material to the Company’s results of operations for any given quarterly or annual period based, in part, upon the results of operations for the given period. As of July 31, 2012 and April 30, 2012, the Company had no uncertain tax positions, and will continue to evaluate for uncertain positions in the future.

Foreign currency translation

The accompanying consolidated financial statements are presented in U.S. dollars (“USD”). The reporting currency of the Company is the USD. The functional currency of the ARX Companies is the Australian dollar and the functional currency of ARX Pte is the Singapore dollar. Results of operations and cash flows are translated at average exchange rates during the period, assets and liabilities are translated at the spot exchange rate at the end of the period, and equity is translated at historical exchange rates. As a result, amounts relating to assets and liabilities reported on the statements of cash flows may not necessarily agree with the changes in the corresponding balances on the balance sheets. Translation adjustments resulting from the process of translating the local currency financial statements into U.S. dollars are included in determining comprehensive income. The foreign currency translation adjustment included in comprehensive income (loss) for the three months ended July 31, 2012 and 2011 amounted to $(10) and $2, respectively.

Assets and liabilities denominated in foreign currencies are translated into the functional currency at the exchange rates prevailing at the balance sheet date with any transaction gains and losses that arise from exchange rate fluctuations on transactions denominated in a currency other than the functional currency included in the results of operations as incurred.

As of July 31, 2012 and April 30, 2012 and for the three months ended July 31, 2012 and 2011, the exchange rates used to translate amounts in Australian dollars and Singapore dollars into USD for the purposes of preparing the consolidated financial statements were as follows:

| 12 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 2 - Summary of significant accounting policies (continued)

Foreign currency translation (continued)

| AUS $ | SGD $ | ||||||||||

| July 31, 2012 | July 31, 2011 | April 30, 2012 | July 31, 2012 | July 31, 2011 | April 30, 2012 | ||||||

| Exchange rate on balance sheet dates | |||||||||||

| USD : AUS$: SGD$ exchange rate | 1.0479 | 1.0997 | 1.0471 | 0.8017 | - | 0.8086 | |||||

| Average exchange rate for the period | |||||||||||

| USD : AUS$: SGD$ exchange rate | 1.0086 | 1.0691 | 1.0436 | 0.7913 | - | 0.7931 | |||||

Stock-based compensation

Stock-based compensation is accounted for based on the requirements of the Share-Based Payment Topic of ASC 718 which requires recognition in the consolidated financial statements of the cost of employee and director services received in exchange for an award of equity instruments over the period the employee or director is required to perform the services in exchange for the award (presumptively, the vesting period). The ASC also requires measurement of the cost of employee and director services received in exchange for an award based on the grant-date fair value of the award.

Pursuant to ASC Topic 505-50, for share-based payments to consultants and other third-parties, compensation expense is determined at the “measurement date.” The expense is recognized over the vesting period of the award. Until the measurement date is reached, the total amount of compensation expense remains uncertain. The Company initially records compensation expense based on the fair value of the award at the reporting date.

Net loss per share of common stock

Basic net loss per common share is computed by dividing net loss available to common stockholders by the weighted average number of shares of common stock outstanding during the period. Diluted net loss per common share is computed by dividing net loss by the weighted average number of shares of common stock, common stock equivalents and potentially dilutive securities outstanding during each period. As of July 31, 2012 and 2011 and April 30, 2012, the Company did not have any potentially dilutive common shares.

Accumulated other comprehensive income

Comprehensive income is comprised of net income and all changes to stockholders' equity, except those due to investments by stockholders, changes in paid-in capital and distributions to stockholders. For the Company, comprehensive income (loss) for the three months ended July 31, 2012 and 2011 included net loss and unrealized gains (losses) from foreign currency translation adjustments.

Related party transactions

A related party is generally defined as (i) any person that holds 10% or more of the Company's securities including such person's immediate families, (ii) the Company's management, (iii) someone that directly or indirectly controls, is controlled by or is under common control with the Company, or (iv) anyone who can significantly influence the financial and operating decisions of the Company. A transaction is considered to be a related party transaction when there is a transfer of resources or obligations between related parties.

| 13 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 2 - Summary of significant accounting policies (continued)

Recent accounting pronouncements

Accounting standards that have been issued or proposed by FASB that do not require adoption until a future date are not expected to have a material impact on the consolidated financial statements upon adoption.

NOTE 3 – MINING RIGHTS

ARX Springs Project

On March 6, 2012 and as amended on March 31, 2012, the Company’s subsidiaries, ARX Springs and ARX Pacific entered into Stage Tribute Agreements (the “Stage Tribute Agreements”) with Riverstone Resources Pty Ltd. (“Riverstone”). The Stage Tribute Agreements were made pursuant to the terms of an agreement dated February 27, 2012 between Riverstone and BRI Microfine Pty Ltd., a related party (See Note 4) (the “Riverstone Master Agreement”). The Stage Tribute Agreements grant the exclusive right to the ARX Companies to explore, mine and extract gold and other extracted products on the ARX Springs Project properties located in the Wide Bay Burnett Region in central Queensland, Australia. The ARX Springs Project overall covers approximately 16 km² of surface area and the mining project is part of a larger area for which Riverstone owns and operates an extractive industries business.

The two ARX Companies will jointly operate at the ARX Springs site, and Phase 1 of the mining processing at ARX Springs under the respective Stage Tribute Agreements will mine a surface area of 600 ha. Under the terms of the Riverstone Master Agreement between BRI, a related party and Riverstone, phase 2 of the mining process at the ARX Springs Project may commence at any time and does not require work on phase 1 to be completed. ARX Companies must pay to Riverstone a production royalty of 19% of the value of production extracted and processed from the first 100 ha surface area of the ARX Springs Project treated and 15% of the value of production extracted and processed from the surface area of the project which exceeds 100ha.

During the term of the Stage Tribute Agreements, Riverstone solely or jointly with one or both of the ARX Companies (and either of the ARX Companies solely or jointly with Riverstone) may apply for extensions and additional mining licenses from the Queensland Mines and Resources Department. During all terms of the mining license and any additional mining licenses the holders of all ARX Springs mining license and additional mining licenses shall be obliged to comply with the regulations applicable and to meet the obligations imposed by the Mineral Resource Act of 1989 (Queensland). If the mining license or additional mining licenses, at any time are cancelled, the ARX Companies may lose the right to mine and process at the ARX Springs Project. Riverstone may terminate the Stage Tribute Agreements on prior notice to the ARX Companies if ARX Companies are in breach of the agreements but termination cannot be affected without the ARX Companies being first permitted to remedy any alleged breach and any disputes between Riverstone and the ARX Companies will be subject to mediation and if mediation is unsuccessful will be submitted to arbitration. Riverstone may terminate the Stage Tribute Agreements by giving three month’s notice by March 5, 2037, with provision to extend dates if required, or after the resources have been fully mined and processed, whichever occurs first. The initial ten hectare surface area of the ARX Springs Project must be mined and processed by March 5, 2025.

| 14 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 3 – MINING RIGHTS (continued)

The ARX Companies are obliged to take out business liability and employee insurances which shall be effected when mining processing commences.

Prior to undertaking any ground disturbing work on the ARX Springs Project, the ARX Companies must, in the ordinary course of the mining business obtain the approval of the Queensland Department of Mines on a proposed work plan. The agreements with Riverstone require consultation with Riverstone on the form of any proposed work plan to ensure it is not likely to interfere with the activities of Riverstone. The ARX companies solely or jointly with Riverstone may proceed to obtain all necessary regulatory approvals for any proposed work plan according to standard industry mining practice in the State of Queensland as governed by the Mineral Resource Act 1989.

The ARX Companies will be responsible for all rehabilitation works on the properties, as required by the Queensland Mines and Resources Department, and any other governmental or other authorities in relation to exploration or mining activities carried out by the ARX Companies. Prior to the commencement of work the Queensland Mines and Resources Department will assess a value of a rehabilitation bond and the value of the rehabilitation bond will have to be paid by the ARX companies. There is no reason known to Riverstone or ARX Companies why the bond will not be assessed according to current Queensland Mines and Resources Department guidelines but the actual amount of the rehabilitation bond is not yet known.

During the term of the Stage Tribute Agreements, Riverstone shall take all action necessary to keep the ARX Project in good standing. Riverstone will be obliged to protect the land areas and the Mining License and Riverstone shall make any required payments to the Department of Mines and Resources or such other department of the government of Queensland Australia responsible for the administration of the Mineral Resource Act of 1989 (Queensland) in order to maintain its rights to explore and, if warranted, to develop its property. If Riverstone fails to meet these obligations, the Company may lose the right to explore for gold and other extracted products on the property. In general terms the Arx Companies are entitled under their agreements to act on their own behalf to protect the land and site and the mining leases and to pay royalties to Queensland Mines Department if they decide to do so by potential threats or risks to the project or rights.

NOTE 4 - RELATED PARTY TRANSACTIONS

Technology Sub-license Agreement

On November 24, 2011, the Company’s subsidiary, ARX Springs, entered into a Technology Sub-license Agreements (the “Technology Agreement”) with BRI Microfine Pty Ltd. (“BRI”), a company incorporated in Australia and owned by the Company’s CEO and by a principal stockholder/founder of the Company. Pursuant to the Technology Agreement, BRI granted to ARX Springs an exclusive non-assignable, non-transferrable sub license to use the BRI’s technology with the ARX Spring Project for the term of the project. BRI’s technology is a chemical leaching process which has been shown to concentrate gold, particularly in a microfine (finer than 5 microns) state, from concentrates, ores, tailings, solutions and other friable or pulverized materials. As consideration of the Sub-license agreement, the Company shall pay a royalty to BRI calculated as a percentage of the gross value of extracted product on a sliding scale based on tonnes processed ranging from 15% down to 10%. BRI in its discretion may at any time allow a rebate to AR Springs of any royalty payable.

BRI, at the cost of the Company, and in accordance with the requirements of the Company, will construct at the ARX Springs Project site alluvial material processing production plants. Additionally, BRI will arrange for the application of software systems for operations and metallurgical reporting and information systems to be installed in all alluvial material processing production plants for the ARX Spring project. The Company shall pay BRI invoices for the provision of software systems and metallurgical reporting and information systems and construction of alluvial material processing production plants.

| 15 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 4 - RELATED PARTY TRANSACTIONS (continued)

Due from related party

The Company received from and provided advances to BRI. These advances are unsecured and payable on demand. At July 31, 2012 and April 30, 2012, amounts due from BRI amounted to $851 and $850, respectively.

Due to related party

The Company received working capital advances from a former officer and shareholder. These advances are unsecured and payable on demand. At July 31, 2012 and April 30, 2012, amounts due to this former officer and shareholder amounted to $527 and $0, respectively.

Royalty commitment

In August 2012, in connection with an amendment to the Share Exchange dated May 22, 2012, the Company entered into a royalty agreement (the “Royalty Agreement”) with two original founding stockholders of Grimsby (one of which is an officer and director of the Company), who received shares in the Share Exchange. Pursuant to the Royalty Agreement, the Company agreed, at the discretion of the Company’s board of directors, to pay these parties up to $7,500,000 in royalties from gross profits derived from the sales of all minerals and other products recovered from the ARX Spring Project.

NOTE 5 - LOANS PAYABLE

During the three months ended July 31, 2012, a shareholder advanced the Company $5,100 for working capital purposes. The advances are non-interest bearing, are unsecured and are payable on demand.

note 6 – STOCKHOLDERS’ EQUITY

Cash contributed by founders

For the year ended April 30, 2012 and for the period from May 28, 2010 (inception) to April 30, 2011, the original stockholders of ARX Pacific contributed capital to ARX Pacific of $515 and $420, respectively.

Stock-based compensation

On November 11, 2011, the Company issued 30,000 shares of ARX Spring’s common stock to ARX Springs original founders for services rendered. As there was no determinable fair value of founder’s shares, the Company valued these common shares at a nominal value of AUS$1.00 per common share. In connection with issuance of these common shares, the Company recorded stock-based compensation of $30,780.

On May 15, 2012 and accounted for on March 8, 2012, pursuant to recapitalization accounting, the Company issued 100 shares of Grimsby common stock to Grimsby’s original founders for services rendered. As there was no determinable fair value of founder’s shares, the Company valued these common shares at a nominal value of $1.00 per common share. In connection with issuance of these common shares, the Company recorded stock-based compensation of $100. This 100 share issuance quantity has also been retroactively reflected back to inception of the Company.

| 16 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

note 6 – STOCKHOLDERS’ EQUITY (continued)

On March 26, 2012, the Company issued 40,280 shares of ARX Pte common stock to ARX Pte original founders for services rendered. As there was no determinable fair value of founder’s shares, the Company valued these common shares at a nominal value of S$1.00 per common share. In connection with issuance of these common shares, the Company recorded stock-based compensation of $31,946.

On May 22, 2012, in connection with the share exchange agreement, the Company issued 4,148,000,000 shares if its common stock to the Grimsby shareholders (See Note 1).

Other contributed capital

In connection with consulting services performed for the Company by a third party in the amount of $44,704, BRI agreed to pay for these services on behalf of the Company. Accordingly, the Company recorded contributed capital of $44,704.

NOTE 7 - CONCENTRATIONS

Reliance on contractual agreements

The Company’s business is dependent on agreements with an unrelated party (see Note 3) and a related party (see Note 4).

Concentrations of credit risk

Financial instruments which potentially subject the Company to concentrations of credit risk consist principally of cash. At July 31, 2012 and April 30, 2012, all of the Company’s cash is maintained with banks in Australia and Singapore. The Company has not experienced any losses in such accounts and believes it is not exposed to any risks on its cash in bank accounts.

Concentration in a geographic area

The Company will operate in the mining industry and the operations will be concentrated in Australia (See Note 3).

NOTE 8 – COMMITMENTS AND CONTINGENCIES

On June 18, 2012, the Company entered into a Placement Agent Agreement with Khandwala Securities Limited (“KSL”) (the “Placement Agent”), whereby KSL was to act as exclusive Placement Agent, perform due diligence, and conduct other business development activities for a period of six months. In accordance with the Placement Agent Agreement, the Company shall pay KSL 5% of funds raised up to $50 million. Additionally, the Company agreed to pay Placement Agent $250,000 with $100,000 due upon signing of the Placement Agreement, $100,000 on completion of due diligence and submission of an information memorandum and $50,000 upon the Company’s sign–off of a placement memorandum and information statement. To date, KSL had not submitted any information statement or placement memorandum. Accordingly, the Company believes that only $100,000 may be due pursuant to the Placement Agent Agreement with $40,000 of that amount earned and accrued by the Company as of July 31, 2012.

By agreement made 18th June 2012 between Grimsby Investments Ltd and Salam International Ltd the parties entered into a conditional Gold Forward Sales contract which is subject to a condition of completion of due diligence by the buyer (Salam). Under the contract the buyer proposed buying gold bullion for US $105 million. The agreement required first gold delivery by the Company to commence 270 days after the effective date. The parties have confirmed the agreement remains in force and of full effect. The parties have agreed to extend both the time of completion of due diligence until the 28th February 2013 and the effective date specified in the agreement to 28 February 2013 with the consequence that subject to due diligence, the time for first delivery of gold by the Company is extended to 270 days after 1st March 2013. The parties have acknowledged that the contract is conditional upon satisfactory due diligence by the buyer. There is no obligation on the company nor is there any potential penalty on the company for any failure to deliver gold while the gold forward sales contract remains conditional on due diligence and on payment by the buyer to the company of a $5 million cash deposit. The deposit is not required to be paid until the buyer is satisfied with its due diligence investigations.

In August 2012, in connection with an amendment to the Share Exchange dated May 22, 2012, Daulton entered into a royalty agreement (the “Royalty Agreement”) with two original founding stockholders of Grimsby (one of which is an officer and director of the Company), who received shares in the Share Exchange. Pursuant to the Royalty Agreement, the Company agreed, at the discretion of the Company’s board of directors, to pay these parties up to $7,500,000 in royalties from gross profits derived from the sales of all minerals and other products recovered from the ARX Spring Project.

| 17 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 9 - SUBSEQUENT EVENTS

Common stock

In September 2012, the Company sold 5,000,000 shares of its common stock for proceeds of $225,000.

Loans payable

During the three months ended October 31, 2012, a shareholder advanced the Company $68,500 for working capital purposes. The advances are non-interest bearing, are unsecured and are payable on demand.

Acquisition of Costa Rica Mine

By agreement dated 31st October 2012 and by addendum agreement dated 21st November 2012 between the Company, Ascot Mining Ltd and Veritas Gold CR SA the parties agreed to terms of purchase by the Company from Ascot of 50% of the issued shares of Veritas. The terms of the purchase by the Company require delivery of 200 million common shares to Ascot and a $2,500,000 loan (completion advance) from the Company to Veritas as working capital and expansion capital for Chassoul Mine , Costa Rica. The Company has the right in its absolute discretion to arrange that the completion advance may be delivered by Musketeer Holdings Corp ( a shareholder in the company) in substitution for the Company subject to the primary obligation remaining with the Company. The parties have confirmed the agreement remains in force and of full effect and have agreed to extend the earlier completion date of 30 November 2012 to an extended completion date for the purchase to on or before 20 February 2013 or such other date as the parties may agree in writing. No party to the agreement is subject to any penalty by reason the purchase has not yet completed.

NOTE 10 – RESTATEMENT

The Company’s consolidated financial statements have been restated as of July 31, 2012 and for the three months ended July 31, 2012 and 2011. Management determined that as of July 31, 2012 and for the periods ended July 31, 2012 and 2011, the consolidated financial statements did not properly reflect the reorganization and recapitalization of the Company. On May 22, 2012, the Company, Grimsby, and the Grimsby Shareholders entered into a Share Exchange. Upon closing of the transaction contemplated under the Share Exchange, as amended, on May 22, 2012, the Grimsby Shareholders (four entities) transferred all of the issued and outstanding capital stock of Grimsby to the Company in exchange for an aggregate of 4.148 billon shares of the Company’s common stock and for a commitment to pay royalties of $7,500,000 to two original founding stockholders of Grimsby (one of which is an officer and director of the Company), as amended retroactively in August 2012 for an original $150 million debt to the four original founding stockholders of Grimsby. Such exchange caused Grimsby to become our wholly-owned subsidiary.

The Share Exchange should have been accounted for as a reverse-merger and recapitalization since the stockholders of Grimsby obtained voting and management control of the Company. Grimsby was the acquirer for financial reporting purposes and Daulton was the acquired company. Consequently, the assets and liabilities and the operations reflected in the historical financial statements prior to the Exchange Agreement should be those of Grimsby and recorded at the historical cost basis of Grimsby, and the consolidated financial statements after completion of the Share Exchange should have included the assets and liabilities of both Grimsby and the Company and the Company’s consolidated operations from the closing date of the Share Exchange.

| 18 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 10 – RESTATEMENT (continued)

Accordingly, the Company restated its unaudited interim consolidated balance sheets as of July 31, 2012 and the consolidated statements of operations and comprehensive income (loss) and its consolidated statements of cash flows for the periods ended July 31, 2012 and 2011. Additionally, the Company revised all of its disclosures in the notes to the consolidated financial statements and management’s discussion and analysis. The effect of correcting these errors in the Company’s (a) unaudited consolidated balance sheet at July 31, 2012; (b) unaudited consolidated statement of operations for the three months ended July 31, 2012 and 2011; and (c) unaudited consolidated statement of cash flows for the three months ended July 31, 2012 and 2011 are shown in the tables as follows:

| Consolidated Balance Sheet data | July 31, 2012 (Unaudited) | |||||||||||||||

| As previously filed | Adjustments to Restate | As Restated | ||||||||||||||

| Total Assets | $ | 4,173,056 | $ | (4,166,580 | ) | (a) | $ | 6,476 | ||||||||

| Total Current Liabilities | 114,570 | (24,830 | ) | (a) | 89,740 | |||||||||||

| Total Liabilities | 114,570 | (24,830 | ) | 89,740 | ||||||||||||

| Stockholders’ Equity | ||||||||||||||||

| Preferred stock ($0.001 par value; 5,000,000 shares authorized; none issued and outstanding) | – | – | – | |||||||||||||

| Common stock ($0.001 par value; 5,000,000,000 shares authorized; 4,413,240,003 shares issued and outstanding) | 4,413,240 | – | 4,413,240 | |||||||||||||

| Additional paid-in capital. | 989,137 | (5,314,162 | ) | (a) | (4,325,025 | ) | ||||||||||

| Subscription payable | 20,000 | (20,000 | ) | (a) | – | |||||||||||

| Deficit accumulated during the development stage | (1,363,891 | ) | 1,192,320 | (a) | (171,571 | ) | ||||||||||

| Accumulated other comprehensive income | – | 92 | 92 | |||||||||||||

| Total Stockholders’ Equity (Deficit) | 4,058,486 | (4,141,750 | ) | (83,264 | ) | |||||||||||

| Total Liabilities and Stockholders’ Equity (Deficit) | $ | 4,173,056 | $ | (4,166,580 | ) | $ | 6,476 | |||||||||

| (a) | To reflect properly reflect the recapitalization of the Company. |

| Consolidated Statement of Operations Data | For the Three Months Ended July 31, 2012 (Unaudited) | ||||||||||

| As previously filed | Adjustments to Restate | As Restated | |||||||||

| Revenues | $ | - | $ | — | $ | - | |||||

| Operating expenses | 227,730 | (119,236) | 108,494 | ||||||||

| Net Loss | $ | (227,730 | ) | $ | (119,236) | $ | (108,494) | ||||

| Comprehensive Loss | $ | (227,730 | ) | $ | (119,226) | $ | (108,504) | ||||

| Net Loss per Common Share: | |||||||||||

| Basic and diluted | $ | (0.00 | ) | $ | - | $ | (0.00) | ||||

| Weighted Average Common Shares Outstanding: | |||||||||||

| Basic and diluted | 3,448,587,829 | 4,349,813,046 | |||||||||

| (a) | To properly reflect the recapitalization of the Company. |

| 19 |

ARX GOLD CORPORATION AND SUBSIDIARIES

(Formerly Daulton Capital Corp.)

(A DEVELOPMENT STAGE COMPANY)

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

JULY 31, 2012

NOTE 10 – RESTATEMENT (continued)

| Consolidated Statement of Cash Flows | For the Three Months Ended July 31, 2012 (Unaudited) | |||||||||||||||

| As previously filed | Adjustments to Restate | As Restated | ||||||||||||||

| Cash used in operating activities | $ | (27,730 | ) | $ | 27,728 | $ | (2 | ) | ||||||||

| Cash used in financing activities | 27,730 | (22,110 | ) | 5,620 | ||||||||||||

| Effect of exchange rate changes on cash | – | 7 | (d) | 7 | ||||||||||||

| Net increase in cash | – | 5,625 | (e) | 5,625 | ||||||||||||

| 20 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following plan of operation provides information which management believes is relevant to an assessment and understanding of our results of operations and financial condition. The discussion should be read along with our financial statements and notes thereto. This section includes a number of forward-looking statements that reflect our current views with respect to future events and financial performance. Forward-looking statements are often identified by words like believe, expect, estimate, anticipate, intend, project and similar expressions, or words which, by their nature, refer to future events. You should not place undue certainty on these forward-looking statements. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our predictions.

Plan of Operations

We have commenced limited operations and we will require outside capital to implement our business model.

We were incorporated under the laws of the State of Nevada July 8, 2008 as formerly Daulton Capital Corp. On May 25, 2012, Daulton Capital Corp. changed its name to Celframe ARX Resources Corp. and on October 16, 2012, Celframe ARX Resources Corp. changes its name to ARX Gold Corporation (“ARX Gold”).

On May 22, 2012, ARX Gold, Grimsby Investments Limited (“Grimsby”), a company incorporated under the law of the British Virgin Islands on March 8, 2012, and the stockholders of Grimsby (“Grimsby Shareholders”) entered into a Share Exchange. Upon closing of the transaction contemplated under the Share Exchange, as amended, on May 22, 2012, the Grimsby Shareholders (4 entities) transferred all of the issued and outstanding capital stock of Grimsby to ARC Gold in exchange for an aggregate of 4.148 billion shares of the common stock of ARX Gold and a commitment to pay royalties of $7,500,000 to two original founding stockholders of Grimsby, as amended retroactively in August 2012 for an original $150 million to the four original founding stockholders of Grimsby. Such exchange caused Grimsby to become a wholly-owned subsidiary of ARX Gold. ARX Gold and Grimsby with its subsidiaries are collectively referred to as “the Company”.

The Share Exchange was accounted for as a reverse-merger and recapitalization since the stockholders of Grimsby obtained voting and management control of ARX Gold. Grimsby was the acquirer for financial reporting purposes and ARC Gold was the acquired company. Consequently, the assets and liabilities and the operations reflected in the historical financial statements prior to the Exchange Agreement will be those of Grimsby and was recorded at the historical cost basis of Grimsby, and the consolidated financial statements after completion of the Share Exchange included the assets and liabilities of both Grimsby and ARX Gold and the Company’s consolidated operations from the closing date of the Share Exchange.

On March 26, 2012, agents of Grimsby established ARX Springs Pte, Ltd., (“ARX Pte”), a company incorporated in Singapore, in anticipation of a future restructuring of the Company. At the time of its incorporation, ARX Pte had no operations, assets or stockholders.

On April 12, 2012, the one founding stockholder of ARX Springs Pty. Ltd a (“ARX Springs”), formed on November 11, 2011, and the two founding stockholders of ARX Pacific Resources Pty Ltd. (“ARX Pacific”), formed on May 28, 2010, transferred 100% of their respective ownerships in such companies to ARX Pte.

On May 15, 2012, in connection with a reorganization of Grimsby, 100% of the founders’ shares of ARX Pte were issued to Grimsby and Grimsby issued its founders shares to 4 entities.

| 21 |

On May 22, 2012, immediately after the Share Exchange, our organizational structure is as follows:

Pursuant to certain mining rights agreements, ARX Pacific and ARX Springs, together referred to as the “ARX Companies”) have the rights to mine and extract gold and other materials from certain properties in Australia.

ARX Springs Project

On March 6, 2012 and as amended on March 31, 2012, our subsidiaries, ARX Springs and ARX Pacific entered into Stage Tribute Agreements (the “Stage Tribute Agreements”) with Riverstone Resources Pty Ltd. (“Riverstone”). The Stage Tribute Agreements were made pursuant to the terms of an agreement dated February 27, 2012 between Riverstone and BRI Microfine Pty Ltd., a related party (See Note 4) (the “Riverstone Master Agreement”). The Stage Tribute Agreements grant the exclusive right to the ARX Companies to explore, mine and extract gold and other extracted products on the ARX Springs Project properties located in the Wide Bay Burnett Region in central Queensland, Australia. The ARX Springs Project overall covers approximately 16 km² of surface area and the mining project is part of a larger area for which Riverstone owns and operates an extractive industries business.

The two ARX Companies will jointly operate at the ARX Springs site, and Phase 1 of the mining processing at ARX Springs under the respective Stage Tribute Agreements will mine a surface area of 600 ha. Under the terms of the Riverstone Master Agreement between BRI, a related party and Riverstone, phase 2 of the mining process at the ARX Springs Project may commence at any time and does not require work on phase 1 to be completed. ARX Companies must pay to Riverstone production royalty of 19% of the value of production extracted and processed from the first 100 ha surface area of the ARX Springs Project treated and 15% of the value of production extracted and processed from the surface area of the project which exceeds 100ha.

Limited Operating History

We have generated a limited financial history and have not previously demonstrated that we will be able to expand our business. Our business is subject to risks inherent in growing an enterprise, including limited capital resources and possible rejection of our business model and/or sales methods.

Critical Accounting Policies and Estimates

While our significant accounting policies are more fully described in Note 2 to our financial statements for the three months ended July 31, 2012, we believe that the following accounting policies are the most critical to aid you in fully understanding and evaluating this management discussion and analysis.

| 22 |

Our financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. We continually evaluate our estimates, including those related to the accounting for and recovery of long-lived assets including mining rights, income taxes, and the valuation of equity transactions. We base our estimates on historical experience and on various other assumptions that we believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Any future changes to these estimates and assumptions could cause a material change to our reported amounts of revenues, expenses, assets and liabilities. Actual results may differ from these estimates under different assumptions or conditions. We believe the following critical accounting policies affect our more significant judgments and estimates used in the preparation of the financial statements.

Mining property acquisition and exploration costs

We follow ASC 930 “Extraction Activities – Mining” in accounting for mining costs. Costs of lease, acquisition, exploration, carrying and retaining unproven mineral lease properties are expensed as incurred. We have chosen to expense all mineral acquisition and exploration costs as incurred given that it is still in the development stage. Once we have identified proven and probable reserves in our investigation of our properties and upon development of a plan for operating a mine, we will capitalize future costs until production is established. When a property reaches the production stage, the related capitalized costs will be depleted, using the units-of-production method over the estimated life of the probable-proven reserves. When we have capitalized mineral properties, these properties will be periodically assessed for impairment of value and any diminution in value. To date, we have not established the commercial feasibility of any exploration prospects; therefore, all costs are being expensed.

Environmental Matters

Our operations are subject to evolving government environmental laws and regulations related to the discharge of materials into the environment. Our process is not expected to produce harmful levels of emissions or waste by-products. However, these laws and regulations would require us to remove or mitigate the environmental effects of the disposal or release of substances at our site should they occur. Compliance with such laws and regulations can be costly. Additionally, governmental authorities may enforce the laws and regulations with a variety of civil and criminal enforcement measures, including monetary penalties and remediation requirements. We are not aware of any area of non-compliance with governmental environmental laws and regulations as of the date of this report.

Asset retirement obligations

We follow the provisions of ASC 410, Asset Retirement and Environmental Obligations, which establishes standards for the initial measurement and subsequent accounting for obligations associated with the sale, abandonment or other disposal of long-lived tangible assets arising from the acquisition, construction or development and for normal operations of such assets.

Impairment of long-lived assets

In accordance with ASC Topic 360, we review long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of the assets may not be fully recoverable, or at least annually. We recognize an impairment loss when the sum of expected undiscounted future cash flows is less than the carrying amount of the asset. The amount of impairment is measured as the difference between the asset’s estimated fair value and its book value.

| 23 |

Foreign currency translation

The accompanying consolidated financial statements are presented in U.S. dollars (“USD”). The reporting currency of the Company is the USD. The functional currency of the ARX Companies is the Australian dollar and the functional currency of ARX Pte is the Singapore dollar. Results of operations and cash flows are translated at average exchange rates during the period, assets and liabilities are translated at the unified exchange rate at the end of the period, and equity is translated at historical exchange rates. As a result, amounts relating to assets and liabilities reported on the statements of cash flows may not necessarily agree with the changes in the corresponding balances on the balance sheets. Translation adjustments resulting from the process of translating the local currency financial statements into U.S. dollars are included in determining comprehensive income.

Assets and liabilities denominated in foreign currencies are translated into the functional currency at the exchange rates prevailing at the balance sheet date with any transaction gains and losses that arise from exchange rate fluctuations on transactions denominated in a currency other than the functional currency are included in the results of operations as incurred.

Stock-based compensation

We account for stock-based instruments issued to employees in accordance with ASC Topic 718. ASC Topic 718 requires companies to recognize in the statement of operations the grant-date fair value of stock options and other equity based compensation issued to employees. We account for non-employee share-based awards in accordance with ASC Topic 505-50.

Recent accounting pronouncements

Accounting standards that have been issued or proposed by FASB that do not require adoption until a future date are not expected to have a material impact on the financial statements upon adoption.

Results of Operations

For the Three Months Ended July 31, 2012 and 2011

Revenues

Since inception, we had $0 in revenue.

Operating Expenses

For the three months ended July 31, 2012 and 2011, operating expenses amounted to $108,494 and $32, respectively. Changes in operating expenses consisted of the following:

| Three Months Ended July 31, | ||||||||

| 2012 | 2011 | |||||||

| Professional fees | $ | 106,063 | $ | – | ||||

| Other selling, general and administrative | 2,431 | 32 | ||||||

| $ | 108,494 | $ | 32 | |||||

| * | For the three months ended July 31, 2012, professional fees were $106,063. During the three months ended July 31, 2012, we incurred business development and consulting fees of $44,704 related to the preparation of an exploration report on the ARX Springs Project. Additionally, we incurred $40,000 in connection with due diligence and capital raising activities, and accounting and legal fees of $21,359. We did not incur professional fees during the three months ended July 31, 2011. We expect professional fees to increase as we incur significant costs associated with our public company reporting requirements, costs associated with newly applicable corporate governance requirements, and other rules implemented by the Securities and Exchange Commission. |

| 24 |

| * | For the three months ended July 31, 2012, general and administrative expenses which included bank service charges and other office related expenses increased by $2,399 as compared to the three months ended July 31, 2011. We expect general and administrative expenses to increase as we increase our operations. |

Net Loss

As a result of the factors described above, our net loss for the three months ended July 31, 2012 and 2011 was $108,494 and $32, or a net loss per common share of $0.00 and $0.00 (basic and diluted), respectively.

Liquidity and Capital Resources

Liquidity is the ability of a company to generate funds to support its current and future operations, satisfy its obligations, and otherwise operate on an ongoing basis. To date, we have funded our operations through the sale of our common stock. Our primary uses of cash have been for compensation, and professional fees. All funds received have been expended in the furtherance of growing the business and establishing brand portfolios. The following trends are reasonably likely to result in a material decrease in our liquidity over the near to long term:

| · | An substantial increase in working capital requirements to finance our mining operations, |

| · | Addition of administrative and professional personnel as the business grows, |

| · | The cost of being a public company, and |

| · | Capital expenditures on excavation, mining and other equipment |

| · | Payment of royalties upon commencement of production. |

At July 31, 2012, we had a cash balance of $5,625. Since inception we have funded our operations as follows:

| ● | In 2010, we borrowed funds from a shareholder amounting to $5,100 to fund our operating expenses, pay our obligations, and for working capital purposes. |

| ● | In September 2012, we issued 5,000,000 shares of common stock for proceeds of $225,000. |