As filed with the Securities and Exchange Commission on January [*], 2018

Registration No. 333-219893

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

BTCS Inc.

(Exact name of registrant as specified in its charter)

| Nevada | 7372 | 90-1096644 | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification Number) |

9466 Georgia Avenue #124

Silver Spring, MD 20901

(202) 430-6576

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Charles W. Allen

Chief Executive Officer

BTCS Inc.

9466 Georgia Avenue #124

Silver Spring, MD 20901

(202) 430-6576

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a copy to:

Michael D. Harris Esq.

Nason, Yeager, Gerson, White & Lioce, P.A.

3001 PGA Blvd., Suite 305

Palm Beach Gardens, FL 33410

(561) 471-3507

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] | |

| Non-accelerated filer [ ] (Do not check if a smaller reporting company) | Smaller reporting company [X] | |

| Emerging growth company [ ] |

If an emerging growth company, indicate by checkmark if the registrant has not elected to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. [ ]

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered(1) | Proposed Maximum Offering Price per Share(2) | Proposed Maximum Aggregate Offering Price(2) | Amount of Registration Fee(3) | ||||||||||||

| Common Stock, par value $0.001 per share, issuable upon exercise of outstanding Series A warrants | 15,873,600 | $ | 0.1111 | $ | 1,763,557 | $ | 0 | |||||||||

| Common Stock, par value $0.001 per share, issuable upon exercise of outstanding Additional warrants | 15,714,288 | $ | 0.111 | $ | 1,745,857 | $ | 0 | |||||||||

| Common Stock, par value $0.001 per share, issuable upon exercise of outstanding Bonus warrants | 15,714,288 | $ | 0.111 | $ | 1,745,857 | $ | 0 | |||||||||

| Common Stock, par value $0.001 per share, issuable upon exercise of outstanding Series B warrants | 12,942,000 | $ | 0.11 | $ | 1,423,620 | $ | 0 | |||||||||

| Common Stock, par value $0.001 per share, issuable upon exercise of outstanding Series C-1 Convertible Preferred Stock and Common Stock issued upon the conversion of Series C S-1 Convertible Preferred Stock | 12,942,000 | $ | 0.11 | $ | 1,423,620 | $ | 0 | |||||||||

| Common Stock, par value $0.001 per share | 8,695,456 | $ | - | $ | - | $ | - | |||||||||

| Total (3) | 81,881,632 | - | $ | - | $ | 0 | ||||||||||

| (1) | Pursuant to Rule 416 under the Securities Act of 1933, as amended, the shares being registered hereunder include such indeterminate number of shares of Common Stock, as may be issuable with respect to the shares being registered hereunder as a result of stock splits, stock dividends or similar transactions. |

| (2) | The proposed maximum offering price per share and the proposed maximum aggregate offering price have been estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rules 457(c) under the Securities Act of 1933 on the basis of the average of the bid and asked price of our Common Stock on the OTC Markets on August 8, 2017, a date within five days prior to the date of the filing of this registration statement, for 47,302,176 shares of Common Stock, and on November 24, 2017, a date within five days prior to the date of the filing of this amendment to the Company’s registration statement, for 30,879,744 shares of Common Stock. |

| (3) | A registration fee of $609.09, for 47,302,176 shares of Common Stock, was paid by the Company in connection with the initial filing of the Company’s Form S-1 registration statement on August 10, 2017 and an additional $422.90 was paid in connection with the S-1/A filed on November 29, 2017. |

The registrant hereby amends this registration statement on such date or date(s) as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Commission acting pursuant to said Section 8(a) may determine.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED January [*], 2018 |

81,881,632 Shares of Common Stock

BTCS Inc.

We are registering an aggregate of 81,881,632 shares of Common Stock, $0.001 par value per share of BTCS Inc., for resale by certain of our shareholders identified in this prospectus. The 81,881,632 shares of Common Stock or the Resale Shares consist of (i) 15,873,600 shares of Common Stock underlying outstanding Series A warrants exercisable at $0.085 per share, (ii) 15,714,288 shares of Common Stock underlying outstanding Additional Warrants exercisable at $0.085 per share, (iii) 15,714,288 shares of Common Stock underlying outstanding Bonus Warrants exercisable at $0.17 per share, (iv) 12,942,000 shares of Common Stock underlying outstanding Series B Warrants exercisable at $0.135 per share, (v) 10,000,800 shares of Common Stock underlying outstanding Series C-1 Convertible Preferred Stock and 2,941,200 shares of Common Stock issued upon the conversion of Series C-1 Preferred Stock, (vi) 4,295,456 shares of Common Stock owned by our executive officers, and (vii) 4,400,000 shares of Common Stock. Please see the section entitled “Selling Shareholders” beginning at page 53 of this prospectus.

The shareholders identified in the “Selling Shareholders” section may offer to sell the Resale Shares at fixed prices, at prevailing market prices at the time of sale, at varying prices or at negotiated prices, and will pay all brokerage commissions and discounts attributable to the sale of such shares. They will receive all of the net proceeds from the offering of their shares.

The Resale Shares may be sold by the shareholders identified in the “Selling Shareholders” section to or through underwriters or dealers, directly to purchasers or through agents designated from time to time. For additional information regarding the methods of sale you should refer to the section entitled “Plan of Distribution” in this prospectus.

Our Common Stock is presently quoted on the OTCQB under the symbol “BTCS”. On January 16, 2018, the last reported sale price for our Common Stock on the OTCQB was $0.128 per share.

Our business and an investment in our securities involve a high degree of risk. See “Risk Factors” beginning on page 3 of this prospectus for a discussion of information that you should consider before investing in our securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is _______ __, 2018

| i |

TABLE OF CONTENTS

You should rely only on information contained in this prospectus. We have not authorized anyone to provide you with information that is different from that contained in this prospectus. The selling shareholder is not offering to sell or seeking offers to buy shares of common stock in jurisdictions where offers and sales are not permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock.

| ii |

GLOSSARY OF DEFINED TERMS AND INDUSTRY DATA

In this prospectus, each of the following quoted terms has the meanings set forth after such term:

“bitcoin” — A type of a Digital Asset based on an open source math-based protocol existing on the Bitcoin Network and utilizing cryptographic security.

“Bitcoin Exchange”— An electronic marketplace where exchange participants may trade, buy and sell bitcoins based on bid-ask trading. The largest Bitcoin Exchanges are online and typically trade on a 24-hour basis, publishing transaction price and volume data.

“Bitcoin Exchange Market” — The global bitcoin exchange market for the trading of bitcoins, which consists of transactions on electronic Bitcoin Exchanges.

“Bitcoin Network” — The online, end-user-to-end-user network hosting the public transaction ledger, known as the Blockchain, and the source code comprising the basis for the math-based protocols and cryptographic security governing the Bitcoin Network.

“Blockchain” — The public transaction ledger of the Bitcoin Network on which miners or mining pools solve algorithmic equations allowing them to add records of recent transactions (called “blocks”) to the chain of transactions in exchange for an award of bitcoins from the Bitcoin Network and the payment of transaction fees, if any, from users whose transactions are recorded in the block being added.

“CEA” — Commodity Exchange Act of 1936, as amended.

“CFTC” — The US Commodity Futures Trading Commission, an independent agency with the mandate to regulate commodity futures and option markets in the United States.

“Code” — The US Internal Revenue Code of 1986, as amended.

“Digital Asset” — Collectively, all digital assets based upon a computer-generated math-based and/or cryptographic protocol that may, among other things, be used to buy and sell goods or pay for services. Bitcoins represent one type of Digital Asset.

“Digital Security” — A type of Digital Asset that is offered by a promoter as an investment contract, which is a type of security defined by Section 2(a)(1) of the Securities Act.

“DDoS Attack” — Distributed denial of service attacks are coordinated hacking attempts to disrupt websites, web servers or computer networks in which an attacker bombards an online target with a large quantity of external requests, thus precluding the target from processing requests from genuine users.

“Exchange Act” — The Securities Exchange Act of 1934, as amended.

“FDIC” — The Federal Deposit Insurance Corporation.

“FinCEN” — The Financial Crimes Enforcement Network, a bureau of the US Department of the Treasury.

“FINRA” — The Financial Industry Regulatory Authority, Inc., which is the primary regulator in the United States for broker-dealers.

“Fiat Currency” — Currency that a government has declared to be legal tender, but is not backed by a physical commodity. The value of fiat money is derived from the relationship between supply and demand rather than the value of the material that the money is made of.

“IRS” — The US Internal Revenue Service, a bureau of the US Department of the Treasury.

“Mining” — The process by which Bitcoins are created involving programmers solving complex math problems with the computers in the Bitcoin Network.

| iii |

“SEC” — The US Securities and Exchange Commission.

“Securities Act” — The Securities Act of 1933, as amended.

“SIPC” — The Securities Investor Protection Corporation.

“Transaction Verification Services” — Is equivalent to Mining.

“Warrants” refers to the Series A Warrants, Additional Warrants, Bonus Warrants, and Series B Warrants.

Industry Data

This prospectus also includes estimates of market size and industry data that we obtained from industry publications and surveys and internal company sources. The industry publications and surveys used by management to determine market size and industry data contained in this prospectus have been obtained from sources believed to be reliable.

| iv |

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our Common Stock, you should carefully read this entire prospectus, including our financial statements and the related notes and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in each case included elsewhere in this prospectus.

Unless the context otherwise requires, references to “we,” “our,” “us,” “BTCS,” or the “Company” in this prospectus mean BTCS Inc., on a combined basis with its wholly-owned subsidiary, BTCS Digital Manufacturing, as applicable.

Introduction

We are an early entrant in the Digital Asset market and one of the first U.S. publicly traded companies to be involved with Digital Assets and blockchain technologies.

Our Business

Subject to additional financing, the Company plans to create a portfolio of Digital Assets including bitcoin and other “protocol tokens” to provide investors a diversified pure-play exposure to the bitcoin and blockchain industries. The Company intends to acquire Digital Assets and Digital Securities through: open market purchases and may participate in initial Digital Asset offerings (often referred to as initial coin offerings). The Company has not participated in any initial coin offerings as it believes most of the offerings entail the offering of Digital Securities and require registration under the Securities Act and under state securities laws. Since about July 2017, initial coin offerings using Digital Securities have been (or should be) limited to accredited investors. Because we cannot qualify as an accredited investor, there will only be a limited number of initial coin offerings in which we can participate. Additionally, the Company may acquire Digital Assets by resuming its transaction verification services business through outsourced data centers and earning rewards in Digital Assets by securing their respective blockchains. The Company will carefully review its purchases of Digital Securities to avoid violating the Investment Company Act of 1940 (the “Investment Company”) and seek to reduce potential liabilities under the federal securities laws. See “Risk Factors” at page 3 and “Business” at pages 33-46.

Digital asset blockchains are typically maintained by a network of participants which run servers which secure their blockchain. The market is rapidly evolving and there can be no assurances that we will be competitive with industry participants that have or may have greater resources than us.

Blockchain Technology and Digital Asset Initiatives

We are also focused on Digital Assets and blockchain technologies. Subject to additional financing, we plan to continue to evaluate other strategic opportunities in this rapidly evolving sector in an effort to enhance shareholder value.

Transaction Verification Service Business (Digital Asset mining e.g. bitcoin, Suspended)

We believe that with additional funding we may be able to resume our transaction verification services business (Digital Asset mining e.g. bitcoin) and believe this may provide revenue growth. If we are successful in resuming our transaction verification services business, we anticipate utilizing outsourced data centers and may diversify operations by securing other blockchains in addition to bitcoins. If we resume our mining operations, we do not intend to actively trade the Digital Assets but rather hold them for our own account and sell them for U.S. dollars or other currencies including virtual currencies.

Transaction verification entails running ASIC (application-specific integrated circuit) servers or other specialized servers which solve a set of prescribed complex mathematical calculations in order to add a block to a blockchain and thereby confirm Digital Asset transactions. A party which is successful in adding a block to the blockchain, is awarded a fixed number of Digital Assets for our effort.

Going Concern

Because of recurring operating losses, net operating cash flow deficits, and an accumulated deficit, our independent auditors have indicated in their report on our December 31, 2016 financial statements that there is substantial doubt about our ability to continue as a going concern.

| 1 |

Summary of The Offering

| Resale Shares: | 81,881,632 shares of Common Stock (the “Resale Shares”), consisting of: (i) 15,873,600 shares of Common Stock issuable upon exercise of outstanding Series A Warrants exercisable at $0.085 per share; (ii) 15,714,288 shares of Common Stock issuable upon exercise of outstanding Additional Warrants exercisable at $0.085 per share; (iii) 15,714,288 shares of Common Stock issuable upon exercise of outstanding Bonus Warrants exercisable at $0.17 per share; and (iv) 12,942,000 shares of Common Stock issuable upon exercise of outstanding Series B Warrants exercisable at $0.135 per share, (v) 10,000,800 shares of Common Stock underlying outstanding Series C-1 Convertible Preferred Stock and 2,941,200 shares of Common Stock issued upon the conversion of Series C-1 Preferred Stock, (vi) 4,295,456 shares of Common Stock owned by our executive officers, and (vii) 4,400,000 shares of Common Stock. The Series A, Additional, and Bonus Warrants were issued in a private placement that closed on May 25, 2017. The Series C-1 Convertible Preferred Stock and the Series B Warrants were issued in a private placement that closed in October 2017. See “Private Placements.” The Selling Shareholders include our executive officers. |

|||

| Common Stock outstanding before and after this offering: |

Common Stock outstanding prior to offering: 368,219,169 shares Common Stock offered by the Selling Shareholders: 81,881,632 shares Common Stock outstanding immediately following the offering: 438,464,145 shares. (1) |

|||

| Use of proceeds: | We will not receive any proceeds from the sale of shares in this offering by the Selling Shareholders. However, if any of the Warrants are exercised for cash, we will receive the proceeds, and we plan to use such proceeds for general corporate purposes including compensation to our management. | |||

| Risk factors: | See “Risk Factors” beginning on page 3 of this prospectus and the other information included in this prospectus for a discussion of factors you should carefully consider before investing in our securities. | |||

| OTCQB trading symbol | BTCS |

| (1) | The number of outstanding shares after the offering assumes: i) the 60,244,176 Resale Shares issuable upon the exercise of outstanding warrants are exercised for cash, and ii) 10,000,800 Resale Shares issuable upon the conversion of Series C-1 Convertible Preferred Stock is converted. |

Unless we indicate otherwise, all information in this prospectus:

| ● | is based on 368,219,169 shares of Common Stock issued and outstanding as of January 16, 2018; |

||

| ● | excludes 60,244,176 shares of our Common Stock, being registered in this prospectus, issuable upon exercise of outstanding warrants at a weighted average exercise price of $0.118 per share as of January 16, 2018; and excludes i) 10,000,800 shares of our Common Stock issuable upon the conversion of Series C-1 Convertible Preferred Stock, and ii) 1,820,458 shares of Common Stock underlying warrants not being registered in this Prospectus. |

| 2 |

Any investment in our Common Stock involves a high degree of risk. Investors should carefully consider the risks described below and all of the information contained in this prospectus before deciding whether to purchase our Common Stock. Our business, financial condition and results of operations could be materially adversely affected by these risks if any of them actually occur. This prospectus also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks we face as described below and elsewhere in this prospectus.

Risks Related to Our Company

We need to secure additional financing.

We anticipate that we will incur operating losses for the foreseeable future. Our cash burn rate is approximately $80,000 per month. As of January 16, 2018, we had $231,000 in available cash and approximately $620,587 of Digital Assets. The price of the Digital Assets are subject to wide fluctuations.

Our available cash and Digital Assets as of the date of this prospectus are expected to be only sufficient to last through December 2018 . We require additional funds for our anticipated operations. If we are not successful in securing additional financing, we may be required to delay significantly, reduce the scope of or eliminate our business activities, downsize our general and administrative infrastructure, or seek alternative measures to avoid bankruptcy.

Our auditors have issued a “going concern” audit opinion.

Our independent auditors have indicated in their report on our December 31, 2016 (and we expect that they will do so for their report for 2017) financial statements that there is substantial doubt about our ability to continue as a going concern. A “going concern” opinion indicates that the financial statements have been prepared assuming we will continue as a going concern and do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets, or the amounts and classification of liabilities that may result if we do not continue as a going concern. Therefore, you should not rely on our consolidated balance sheet as an indication of the amount of proceeds that would be available to satisfy claims of creditors, and potentially be available for distribution to shareholders, in the event of liquidation.

We have a limited operating history and a history of operating losses, and expect to incur significant additional operating losses.

We have a limited operating history. Therefore, there is limited historical financial information upon which to base an evaluation of our performance. Our prospects must be considered in light of the uncertainties, risks, expenses, and difficulties frequently encountered by companies in their early stages of operations. We have generated net losses of $44.3 million and $10.0 million for the years ended December 31, 2016 and 2015, respectively. We expect to incur additional net losses over the next several years as we seek to expand operations. The amount of future losses and when, if ever, we will achieve profitability are uncertain. If we are unsuccessful at executing on our business plan, our business, prospects, and results of operations may be materially adversely affected.

We have an evolving business model.

As Digital Assets and blockchain technologies become more widely available, we expect the services and products associated with them to evolve. Very recently, the Securities and Exchange Commission (the “SEC”) issued a Report that promoters that use initial coin offerings or token sales to raise capital may be engaged in the offer and sale of securities in violation of the Securities Act and the Securities Exchange Act of 1934 (the “Exchange Act”). This may cause us to potentially change our future business in order to comply fully with the federal securities laws as well as applicable state securities laws. As a result, to stay current with the industry, our business model may need to evolve as well. From time to time we may modify aspects of our business model relating to our product mix and service offerings. We cannot offer any assurance that these or any other modifications will be successful or will not result in harm to the business. We may not be able to manage growth effectively, which could damage our reputation, limit our growth and negatively affect our operating results.

| 3 |

The loss of our executive officers Charles Allen, our Chairman, Chief Executive Officer and Chief Financial Officer, and Michal Handerhan, our Chief Operating Officer, could have a material adverse effect on us.

Our continued success depends solely on the continued services of our executive officers, particularly Charles Allen, our Chairman, Chief Executive Officer and Chief Financial Officer, and Michal Handerhan, our Chief Operating Officer, who have extensive market knowledge and long-standing industry relationships. In particular, our reputation among and our relationships with key Digital Asset industry leaders are the direct result of a significant investment of time and effort by these individuals to build our credibility in a highly specialized industry. Occasionally, members of senior management or key employees may find it necessary to take a leave of absence due to medical or other causes. The loss of services of either Charles Allen or Michal Handerhan, could diminish our business and growth opportunities and our relationships with key leaders in the Digital Asset industry and could have a material adverse effect on us.

The loss of Charles Allen, our Chairman, Chief Executive Officer and Chief Financial Officer, and Michal Handerhan, our Chief Operating Officer, would have a material adverse effect on us.

After December 2018 we will not have sufficient funds to make payroll and compensate either Charles Allen or Michal Handerhan, if either are unwilling to continue working without pay and choose to leave it could have a material adverse effect on us.

The simultaneous loss of services of both Charles Allen and Michal Handerhan, would result in the Company having no officers or employees and would subsequently cease all operations which would have a material adverse effect on us. See the second risk factor below on the loss of our executive officers and employees.

Because Michal Handerhan our Chief Operating Officer has notified the Company that in the event of the departure of Charles Allen, our Chairman, Chief Executive Officer and Chief Financial Officer from the Company he may terminate his employment and may resign as an officer and director of the Company, which would have a material adverse effect on us.

We have no other officers and only two other directors. The simultaneous loss of Charles Allen, our Chairman, Chief Executive Officer and Chief Financial Officer, and Michal Handerhan, our Chief Operating Officer, would have a material adverse effect on us. Their Employment Agreements permit them to resign for Good Reason which includes non-payment of salaries. This would result in the Company owing them $435,000 and would leave the Company without officers or employees which may have a material adverse effect upon us.

Charles Allen, our Chairman, Chief Executive Officer and Chief Financial Officer and Michal Handerhan our Chief Operating Officer have both notified the Company that in the event the Company is unable to consummate the proposed merger with an Australian entity they intend to terminate their employment and resign as officers and directors of the Company. In January 2018 our officers indicated that due to delays with the proposed merger they have agreed to stay on for a limited time to evaluate other strategic alternatives for the Company; if they are to leave it would have a material adverse effect on us.

We have no other officers and only two other directors. The simultaneous loss of Charles Allen, our Chairman, Chief Executive Officer and Chief Financial Officer, and Michal Handerhan, our Chief Operating Officer, would have a material adverse effect on us. See the risk factor immediately below on the loss of our executive officers and employees.

If Charles Allen and Michal Handerhan are not available as officers and employees, we may lack officers and employees who have experience in the blockchain industry, which will adversely affect our future prospects.

Messrs. Charles Allen and Michal Handerhan are our sole officers and employees. Each has experience in the blockchain industry including mining. Each of them are also the officers and directors of Global Bit Ventures Inc. (“GBV”) which has entered into a series of agreements to be acquired by Marathon Patent Group, Inc. (“Marathon”), subject to shareholder approval and customary closing conditions. If this merger closes, Messrs. Allen and Handerhan have agreed to become the Chief Executive Officer and President, respectively, of Marathon which will present a conflict of interest with the business of the Company. It is likely that due to time constraints, they will resign as officers and employees after a transition period. Pending their resignations, our independent directors would be required to assess corporate opportunities. For this reason, their duties with Marathon may adversely affect the Company. It is possible that they may remain as directors of the Company. Presently, the Company’s active business is the managing of our Digital Asset portfolio and seeking to acquire an operating company in the blockchain industry. Our previously announced merger with an Australian company is not progressing due to the failure of the Australian company to deliver audited financials and requested due diligence items and currently takes little time and effort of our officers. However, our officers are spending time pursuing another acquisition. We presently have no agreement to acquire any other business. Because of conflicts for their time, we may be hampered in our acquisition efforts. Our informal plan is for Mr. David Garrity, an experienced financial executive and an independent director of the Company is expected to become Chief Executive Officer and potentially Chief Financial Officer. We have no agreement with Mr. Garrity and cannot assure you that he will accept full-time employment. Further, Mr. Garrity has limited experience in the blockchain industry. For these reasons, if the Marathon merger closes, we may be adversely affected.

If the Marathon GBV merger fails to close o ur Chairman, Chief Executive Officer and Chief Financial Officer, Charles Allen ’s involvement with GBV may create a continuing , conflict of interest. In the event such position and interest results in a conflict of interest between us and GBV , Mr. Allen could potentially make decisions that are not in the best interest of the shareholders of the Company.

Our Chairman, Chief Executive Officer and Chief Financial Officer, Charles Allen, is involved in other companies including his position and interest in GBV, a blockchain company. If the Marathon GBV merger fails to close, Mr. Allen may face continuing conflicts of interest between the Company and GBV. The conflicts include time and the potentially competing interests of two companies in the same industry. Our Board of Directors and Mr. Allen will attempt to minimize such conflicts. In determining whether or not our interest conflict with those of Mr. Allen’s, our disinterested directors will primarily consider legal advice concerning corporate opportunities, the potential benefits to us, the degree of risk to which we may be exposed and our financial position at that time. We will rely upon the role of Mr. David Garrity and Jonathan Read, our two non-employee directors to evaluate corporate opportunities and the time Mr. Allen spends on our interests. However, as discussed at page 48 under the heading “Conflicts of Interest,” Mr. Read is Chief Executive Officer and Chairman of another company which has invested in and is seeking to enter into the blockchain industry. While Mr. Garrity presently has no conflicts to our knowledge, he may acquire them in the future and he may not want to continue as the only director without potential conflicts of interest. Other than as indicated, the Company has no other procedures or mechanisms to deal with conflicts of interest. It is possible that the existence of the potential conflict or decisions made in connection with such conflicts could adversely affect the price of our Common Stock and could cause the price to be less than it might have been if the conflicts did not exist or were avoided. Mr. Allen currently devotes no less than twenty-five hours per week to GBV, however as a result of the Company’s past inability to compensate Mr. Allen at generally accepted market levels and its historic failure to either make payroll or make payroll on a timely basis, Mr. Allen may choose to devote a substantial amount of his time to his involvement with other companies which may have a material adverse effect on us.

| 4 |

From July 1, 2017 to October 24, 2017 we did not have sufficient funds to make payroll and compensate Charles Allen, as a result Mr. Allen elected to devote a substantial amount of his time to his involvement with other companies which may have a material adverse effect on us.

With our small size and lack of financial resources, we may not be able to recruit independent directors. Because our officers may be subject to potential lawsuits brought by shareholders on behalf of the Company, they may be hesitant to take actions which could benefit us and they may be more likely to resign. Ultimately, we may be adversely harmed as the result of such potential conflicts.

If the Marathon GBV merger fails to close our Chief Operating Officer, Michal Handerhan’s involvement with GBV may create a continuing, conflict of interest. In the event such position and interest results in a conflict of interest between us and GBV, Mr. Handerhan could potentially make decisions that are not in the best interest of the shareholders of the Company.

Our Chief Operating Officer, Michal Handerhan, is involved in other companies including his position and interest in GBV, a blockchain company. If the Marathon GBV merger fails to close, Mr. Handerhan may face continuing conflicts of interest between the Company and GBV. The conflicts include time and the potentially competing interests of two companies in the same industry. Our Board of Directors and Mr. Handerhan will attempt to minimize such conflicts. In determining whether or not our interest conflict with those of Mr. Handerhan’s, our disinterested directors will primarily consider legal advice concerning corporate opportunities, the potential benefits to us, the degree of risk to which we may be exposed and our financial position at that time. We will rely upon the role of Mr. David Garrity and Jonathan Read, our two non-employee directors to evaluate corporate opportunities and the time Mr. Handerhan spends on our interests. However, as discussed at page 48 under the heading “Conflicts of Interest,” Mr. Read is Chief Executive Officer and Chairman of another company which has invested in and is seeking to enter into the blockchain industry. While Mr. Garrity presently has no conflicts to our knowledge, he may acquire them in the future and he may not want to continue as the only director without potential conflicts of interest. Other than as indicated, the Company has no other procedures or mechanisms to deal with conflicts of interest. It is possible that the existence of the potential conflict or decisions made in connection with such conflicts could adversely affect the price of our Common Stock and could cause the price to be less than it might have been if the conflicts did not exist or were avoided. Mr. Handerhan currently devotes no less than twenty-five hours per week to GBV, however as a result of the Company’s past inability to compensate Mr. Handerhan at generally accepted market levels and its historic failure to either make payroll or make payroll on a timely basis, Mr. Handerhan may choose to devote a substantial amount of his time to his involvement with other companies which may have a material adverse effect on us.

From July 1, 2017 to October 24, 2017 we did not have sufficient funds to make payroll and compensate Michal Handerhan, as a result Mr. Handerhan has chosen to devote a substantial amount of his time to his involvement with other companies which may have a material adverse effect on us.

With our small size and lack of financial resources, we may not be able to recruit independent directors. Because our officers may be subject to potential lawsuits brought by shareholders on behalf of the Company, they may be hesitant to take actions which could benefit us and they may be more likely to resign. Ultimately, we may be adversely harmed as the result of such potential conflicts.

Any inability to attract and retain additional personnel could affect our ability to successfully grow our business.

Our future success depends on our ability to identify, attract, hire, train, retain and motivate other highly-skilled technical, managerial, editorial, merchandising, marketing and customer service personnel. Competition for such personnel is intense. Our failure to retain and attract the necessary technical, managerial, editorial, merchandising, marketing, and customer service personnel could harm our business.

We may need to implement additional finance and accounting systems, procedures and controls as we grow our business and organization and to satisfy new reporting requirements.

We are required to comply with a variety of reporting, accounting and other rules and regulations. Compliance with existing requirements is expensive. We may need to implement additional finance and accounting systems, procedures and controls to satisfy our reporting requirements and such further requirements may increase our costs and require additional management time and resources. Our internal control over financial reporting is determined to be ineffective. Such failure could cause investors to lose confidence in our reported financial information, negatively affect the market price of our Common Stock, subject us to regulatory investigations and penalties, and adversely impact our business and financial condition.

Changes in accounting standards and subjective assumptions, estimates and judgments by management related to complex accounting matters could significantly affect our financial results.

Generally accepted accounting principles and related accounting pronouncements, implementation guidelines and interpretations with regard to a wide range of matters that are relevant to our business, including but not limited to revenue recognition, estimating valuation allowances and accrued liabilities (including allowances for returns, credit card chargebacks, doubtful accounts and obsolete and damaged inventory), internal use software and website development (acquired and developed internally), accounting for income taxes, valuation of long-lived and intangible assets and goodwill, stock-based compensation and loss contingencies, are highly complex and involve many subjective assumptions, estimates and judgments by our management. Changes in these rules or their interpretation or changes in underlying assumptions, estimates or judgments by our management could significantly change our reported or expected financial performance.

| 5 |

If we fail to accurately forecast our expenses and revenues, our business, prospects, financial condition and results of operations may suffer and the price of our securities may decline.

The rapidly evolving nature of our industry and the constantly evolving nature of our business, make forecasting operating results difficult. We plan to upgrade and further expand the components of our infrastructure. We may experience difficulties with upgrades of our infrastructure, and may incur increased expenses as a result of these difficulties. As a result of these potential expenditures on our infrastructure, our ability to reduce spending may become limited. Therefore, any significant shortfall in the revenues for which we have built and are continuing to build our infrastructure would likely harm our business.

Natural disasters and geo-political events could adversely affect our business.

Natural disasters, including hurricanes, cyclones, typhoons, tropical storms, floods, earthquakes and tsunamis, weather conditions, including winter storms, droughts and tornados, whether as a result of climate change or otherwise, and geo-political events, including civil unrest or terrorist attacks, that affect us or other service providers could adversely affect our business.

Since there has been limited precedence set for financial accounting of Digital Assets other than Digital Securities, it is unclear how we will be required to account for Digital Asset transactions in the future.

Since there has been limited precedence set for the financial accounting of Digital Assets other than Digital Securities, it is unclear how we will be required to account for Digital Asset transactions or assets. Furthermore, a change in regulatory or financial accounting standards could result in the necessity to restate our financial statements. Such a restatement could negatively impact our business, prospects, financial condition and results of operation.

We are subject to the information and reporting requirements of the Exchange Act), and other federal securities laws, including compliance with the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”).

The costs of preparing and filing annual and quarterly reports and other information with the Securities and Exchange Commission and furnishing audited reports to shareholders will cause our expenses to be higher than they would have been if we were privately held. It may be time consuming, difficult and costly for us to develop, implement and maintain the internal controls and reporting procedures required by the Sarbanes-Oxley Act. We may need to hire additional financial reporting, internal controls and other finance personnel in order to develop and implement appropriate internal controls and reporting procedures.

If we fail to establish and maintain an effective system of internal control, we may not be able to report our financial results accurately or to prevent fraud. Any inability to report and file our financial results accurately and timely could harm our reputation and adversely impact the trading price of our Common Stock. During our assessment of the effectiveness of internal control over financial reporting as of December 31, 2016, management identified a significant deficiency in our disclosure controls and procedures which may lead to a failure to prevent or detect misstatements.

Effective internal control is necessary for us to provide reliable financial reports and prevent fraud. If we cannot provide reliable financial reports or prevent fraud, we may not be able to manage our business as effectively as we would if an effective control environment existed, and our business and reputation with investors may be harmed. As a result, our small size and any current internal control deficiencies may adversely affect our financial condition, results of operation and access to capital. During our assessment of the effectiveness of internal control over financial reporting as of December 31, 2016, management identified a significant deficiency related to presence of weakness in our disclosure control and procedure resulting from limited internal audit functions. Because of our inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with any policies and procedures may deteriorate.

| 6 |

Public company compliance may make it more difficult to attract and retain officers and directors.

The Sarbanes-Oxley Act and rules implemented by the Securities and Exchange Commission have required changes in corporate governance practices of public companies. As a public company, we expect these rules and regulations to increase our compliance costs in 2016 and beyond and to make certain activities more time consuming and costly. The impact of the SEC’s July 25, 2017 report on Digital Securities (the “Report”) will increase our compliance and legal costs. More recently, the SEC’s Chairman commented that most initial coin offerings (a type of Digital Asset) involve the offer of a Digital Security. As a public company, we also expect that these rules and regulations may make it more difficult and expensive for us to obtain director and officer liability insurance and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract and retain qualified persons to serve on our board of directors or as executive officers, and to maintain insurance at reasonable rates, or at all.

Our stock price may be volatile.

The market price of our Common Stock is likely to be highly volatile and could fluctuate widely in price in response to various factors, many of which are beyond our control, including the following:

| ● | changes in our industry including changes which adversely affect bitcoin and other Digital Assets; |

| ● | competitive pricing pressures; |

| ● | continued volatility in the stock prices of Digital Assets issuers; |

| ● | continued volatility in the price of bitcoin and other Digital Assets; |

| ● | our ability to obtain working capital financing; |

| ● | additions or departures of key personnel including our executive officers; |

| ● | sales of our Common Stock; |

| ● | conversion of our Series B Preferred Stock and the subsequent sale of the underlying Common Stock; |

| ● | conversion of our Series C-1 Convertible Preferred Stock and the subsequent sale of the underlying Common Stock; |

| ● | exercise of our warrants and the subsequent sale of the underlying Common Stock; |

| ● | our ability to execute our business plan; |

| ● | operating results that fall below expectations; |

| ● | loss of any strategic relationship; |

| ● | regulatory developments; and |

| ● | economic and other external factors. |

In addition, the securities markets have from time to time experienced significant price and volume fluctuations that are unrelated to the operating performance of particular companies. These market fluctuations may also materially and adversely affect the market price of our Common Stock. As a result, you may be unable to resell your shares at a desired price.

| 7 |

We have not paid cash dividends in the past and do not expect to pay dividends in the future. Any return on investment may be limited to the value of our Common Stock.

We have never paid cash dividends on our Common Stock and do not anticipate doing so in the foreseeable future. The payment of dividends on our Common Stock will depend on earnings, financial condition and other business and economic factors affecting us at such time as our board of directors may consider relevant. If we do not pay dividends, our Common Stock may be less valuable because a return on your investment will only occur if our stock price appreciates.

There is currently a limited trading market for our Common Stock and we cannot ensure that one will be sustained.

Our shares of Common Stock are not traded on a national securities exchange, and the price, may not reflect our actual or perceived value. There can be no assurance that there will be an active market for our shares of Common Stock in the future. The market liquidity will be dependent on the perception of our operating business, among other things. We may, in the future, take certain steps, including utilizing investor awareness campaigns, press releases, road shows and conferences to increase awareness of our business and any steps that we might take to bring us to the awareness of investors may require we compensate consultants with cash and/or stock. There can be no assurance that there will be any awareness generated or the results of any efforts will result in any impact on our trading volume. Consequently, investors may not be able to liquidate their investment at a price that reflects the value of the business and trading may be at an inflated price relative to the performance of our company due to, among other things, availability of sellers of our shares. The price of our Common Stock has been highly volatile. Because there may be a low price for our shares of Common Stock and because of our involvement in the Digital Asset business, many brokerage firms or clearing firms may not be willing to effect transactions in the securities or accept our shares for deposit in an account. Even if an investor finds a broker willing to effect a transaction in the shares of our Common Stock, the combination of brokerage commissions, transfer fees, taxes, if any, and any other selling costs may exceed the selling price. Further, many lending institutions will not permit the use of low priced shares of Common Stock as collateral for any loans.

Because our Common Stock does not trade on a national securities exchange, the prices of our Common Stock may be more volatile and lower than if we were listed.

Our Common Stock trades on the OTCQB operated by OTC Markets. This market is not a national securities exchange. While our Common Stock trading has been relatively active, generally the OTCQB does not have the same level of activity as a national securities exchange like Nasdaq. Most institutions will not purchase a security unless it is on a national securities exchange. In addition, they do not purchase stocks that trade below $5 per share. We may, in the future, take certain steps, including utilizing investor awareness campaigns, press releases, road shows and conferences to increase awareness of our business and any steps that we might take to bring us to the awareness of investors may require we compensate consultants with cash and/or stock. There can be no assurance that there will be any awareness generated or the results of any efforts will result in any impact on our trading volume. Consequently, investors may not be able to liquidate their investment or liquidate it at a price that reflects the value of the business and trading may be at an inflated price relative to the performance of our company due to, among other things, availability of sellers of our shares.

Our Common Stock is deemed a “penny stock,” which would make it more difficult for our investors to sell their shares.

Our Common Stock is subject to the “penny stock” rules adopted under Section 15(g) of the Exchange Act. The penny stock rules generally apply to companies whose Common Stock is not listed on the Nasdaq Stock Market or other national securities exchange or trades at less than $5.00 per share. These rules require, among other things, that brokers who trade penny stock to persons other than “established customers” complete certain documentation, make suitability inquiries of investors and provide investors with certain information concerning trading in the security, including a risk disclosure document and quote information under certain circumstances. Many brokers have decided not to trade penny stocks because of the requirements of the penny stock rules and, as a result, the number of broker-dealers willing to act as market makers in such securities is limited. If we remain subject to the penny stock rules for any significant period, it could have an adverse effect on the market, if any, for our securities. Because our Common Stock is subject to the penny stock rules, investors will find it more difficult to dispose of our securities.

| 8 |

Sales by our significant shareholders could have an adverse effect on the market price of our stock.

Several of our shareholders own significant portions of our preferred stock convertible into Common Stock, and Warrants exercisable for Common Stock. If one or more of our significant shareholders were to sell all or a material number of shares of Common Stock currently available to be sold and the additional shares of Common Stock, upon effectiveness of a registration statement we are required to file (or expiration of the six-month Rule 144 period), the market price of our Common Stock could be negatively impacted. These shares plus the shares of Common Stock issuable upon conversion of preferred stock and on the exercise of warrants creates a circumstance commonly referred to as an “overhang” and in anticipation of exercises the market price of our Common Stock could fall. Investors should be aware that they could experience significant short-term volatility in our stock if such shareholders decide to sell all or a portion of their holdings of our Common Stock at once or within a short period of time. The existence of an overhang, whether or not sales have occurred or are occurring, also could make more difficult our ability to raise additional financing through the sale of equity or equity-related securities in the future at a time and price that we deem reasonable or appropriate.

Our articles of incorporation allow for our board to create new series of preferred stock without further approval by our shareholders, which could adversely affect the rights of the holders of our Common Stock.

Our board of directors has the authority to fix and determine the relative rights and preferences of preferred stock. Our board of directors also has the authority to issue preferred stock without further shareholder approval. As a result, our board of directors could authorize the issuance of a series of preferred stock that would grant to holders the preferred right to our assets upon liquidation, the right to receive dividend payments before dividends are distributed to the holders of Common Stock and the right to the redemption of the shares, together with a premium, prior to the redemption of our Common Stock. In addition, our board of directors could authorize the issuance of a series of preferred stock that has greater voting power than our Common Stock or that is convertible into our Common Stock, which could decrease the relative voting power of our Common Stock or result in dilution to our existing shareholders.

Substantial future sales of our Common Stock by us or by our existing shareholders could cause our stock price to fall.

Additional equity financings or other share issuances by us, including shares issued in connection with strategic alliances and corporate partnering transactions, could adversely affect the market price of our Common Stock. Sales by existing shareholders of a large number of shares of our Common Stock in the public market or the perception that additional sales could occur could cause the market price of our Common Stock to drop.

If the Selling Shareholders exercise their Warrants or we engage in future securities offerings, our shareholders will experience future dilution.

If the Selling Shareholders exercise their Warrants including those which the Resale Shares underlie, our existing shareholders will incur substantial dilution. In order to raise capital, we plan to offer additional shares of our Common Stock or other securities convertible into or exchangeable for our Common Stock. We have no plans as to the type of security or price or the potential number of shares of Common Stock. Although no assurances can be given that we will issue any Common Stock or Common Stock equivalents or consummate a financing, in the event we do, or in the event we sell shares of Common Stock or other securities convertible into shares of our Common Stock in the future, additional and substantial dilution will occur.

| 9 |

We may be accused of infringing intellectual property rights of third parties.

We may be subject to legal claims of alleged infringement of the intellectual property rights of third parties. The ready availability of damages, royalties and the potential for injunctive relief has increased the defense litigation costs of patent infringement claims, especially those asserted by third parties whose sole or primary business is to assert such claims. Such claims, even if not meritorious, may result in significant expenditure of financial and managerial resources, and the payment of damages or settlement amounts. Additionally, we may become subject to injunctions prohibiting us from using software or business processes we currently use or may need to use in the future, or requiring us to obtain licenses from third parties when such licenses may not be available on financially feasible terms or terms acceptable to us or at all. In addition, we may not be able to obtain on favorable terms, or at all, licenses or other rights with respect to intellectual property we do not own in providing ecommerce services to other businesses and individuals under commercial agreements.

Use of social media may adversely impact our reputation.

There has been a marked increase in use of social media platforms and similar devices, including weblogs (blogs), social media websites, and other forms of Internet-based communications which allow individual access to a broad audience of consumers and other interested persons. Consumers value readily available information concerning retailers, manufacturers, and their goods and services and often act on such information without further investigation, authentication and without regard to its accuracy. The availability of information on social media platforms and devices is virtually immediate as is its impact. Social media platforms and devices immediately publish the content their subscribers and participants post, often without filters or checks on accuracy of the content posted. The opportunity for dissemination of information, including inaccurate information, is virtually limitless. Information concerning or affecting us may be posted on such platforms and devices at any time. Information posted may be inaccurate and adverse to us, and it may harm our business. The harm may be immediate without affording us an opportunity for redress or correction. Such platforms also could be used for the dissemination of trade secret information or compromise of other valuable company assets, any of which could harm our business.

Risks Related to the Bitcoin Network and Bitcoins

The following risks relate to our proposed business and the effects upon us assume we obtain financing in a sufficient amount to re-enter this business.

The further development and acceptance of the Bitcoin Network and other Digital Asset systems, which represent a new and rapidly changing industry, are subject to a variety of factors that are difficult to evaluate. The slowing or stopping of the development or acceptance of the Bitcoin Network may adversely affect an investment in our Company.

Digital Assets such as bitcoins that may be used, among other things, to buy and sell goods and services are a new and rapidly evolving industry of which the Bitcoin Network is a prominent, but not unique, part. The growth of the Digital Assets industry in general, and the Bitcoin Network in particular, is subject to a high degree of uncertainty. The factors affecting the further development of the Digital Assets industry, as well as the Bitcoin Network, include:

| ● | continued worldwide growth in the adoption and use of bitcoins and other Digital Assets; |

| ● | government and quasi-government regulation of bitcoins and other Digital Assets and their use, or restrictions on or regulation of access to and operation of the Bitcoin Network or similar Digital Assets systems; |

| ● | the maintenance and development of the open-source software protocol of the Bitcoin Network; |

| ● | changes in consumer demographics and public tastes and preferences; |

| ● | the availability and popularity of other forms or methods of buying and selling goods and services, including new means of using fiat currencies; |

| ● | general economic conditions and the regulatory environment relating to Digital Assets; and |

| ● | the impact of regulators focusing on Digital Assets and Digital Securities and the costs associated with such regulatory oversight. |

| 10 |

A decline in the popularity or acceptance of the Bitcoin Network could adversely affect an investment in us.

If We Acquire Digital Securities, Even Unintentionally, We May Violate the Investment Company Act and Incur Potential Third Party Liabilities

We expect that if we obtain sufficient financing, we will increase our portfolio of Digital Assets including bitcoins and Digital Securities. As this prospectus discloses, there is an increased regulatory examination of Digital Assets and Digital Securities. This has led to regulatory and enforcement activities. In order to limit our acquisition of Digital Securities to stay within the 40% threshold, we will examine the manner in which Digital Assets were initially marketed to determine if they may be deemed Digital Securities and subject to federal and state securities laws. Even if we conclude that a particular Digital Asset is not a security under the Securities Act, certain states including California take a stricter view of the term “investment contract” which means the Digital Asset may have violated applicable state securities laws. This will result in increased compliance costs and legal fees. If our examination of a Digital Asset is incorrect, we may incur regulatory penalties and private investor liabilities since Section 5 of the Securities Act is a strict liability statute much like selling spoiled milk and state securities laws generally impose liability for negligence for misrepresentations.

If We Complete Our Recently Announced Merger with an Australian Company, We May Incur Unknown Liabilities Under United States and Foreign Laws.

On August 21, 2017 we announced that we had entered into a non-binding letter of intent to merge with an existing Australian company engaged in various aspects of the Digital Assets business. See “Business” at page 33. Because the Australian company has ownership in a Digital Assets exchange and acquired Digital Assets, if the merger is completed we could encounter liability at the subsidiary level for their acts prior to the effectiveness of the merger. Although we have been advised by the Australian company that they have raised money from offshore investors, they have not attempted to comply with Regulation S under the Securities Act which has a stricter standard. If BCG is alleged to have violated Section 5 of the Securities Act it could be found liable for rescission of investments found to have been made in violation of Section 5 and could face an enforcement action from the SEC. Because there has been some public concerns raised about U.S. bitcoin exchanges, there is the potential for liability by their operation of an offshore bitcoin exchange. Although we intend to request indemnification for such liabilities, we cannot assure you that the definitive agreement will have such indemnification. Moreover, our only practical remedy may be to reduce the securities we issue in the merger. However, it is the view of the SEC that indemnification under the securities laws is unenforceable as against public policy. Further, if the proposed merger closes, we will be required to closely monitor BCG’s operations to insure compliance with local laws.

Because the Australian Company has not been diligent in providing due diligence materials or completing its required audit, we may not complete the acquisition.

Our acquisition of the Australian company is subject to satisfactory completion of our due diligence process, receipt of audited financial statements and agreement on a definitive agreement. We have not received material compliance with our due diligence requests nor have we seen customary progress with the audit. We also have strong differences concerning the contents of the agreement specifically the representations and warranties that the Australian company would provide us. As a result, we have been pursuing other possible acquisitions in lieu of acquiring the Australian company. We can provide no assurances or guarantees that we will be able to consummate the planned merger or any other acquisition, which may adversely affect an investment in us.

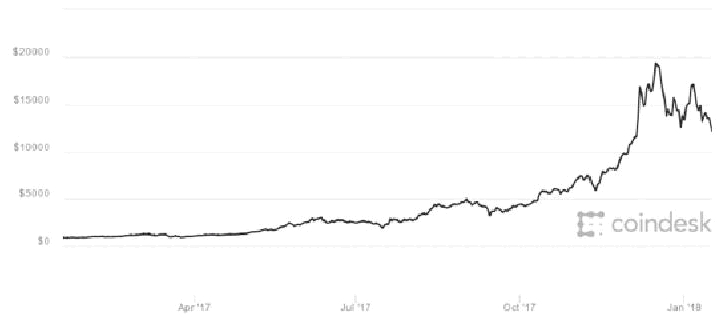

Currently, there is relatively small use of bitcoins in the retail and commercial marketplace in comparison to relatively large use by speculators, thus contributing to price volatility that could adversely affect an investment in us.

As relatively new products and technologies, bitcoins and the Bitcoin Network have only recently become widely accepted as a means of payment for goods and services by many major retail and commercial outlets, and use of bitcoins by consumers to pay such retail and commercial outlets remains limited. Conversely, a significant portion of bitcoin demand is generated by speculators and investors seeking to profit from the short- or long-term holding of bitcoins. A lack of expansion by bitcoins into retail and commercial markets, or a contraction of such use, may result in increased volatility or a reduction in the price of bitcoin, either of which could adversely impact an investment in us.

Significant Bitcoin Network contributors could propose amendments to the Bitcoin Network’s protocols and software that, if accepted and authorized by the Bitcoin Network, could adversely affect an investment in us.

A small group of individuals contribute to the Bitcoin Core project on Github. This group of contributors is currently headed by Wladimir J. van der Laan, the current lead maintainer. These individuals can propose refinements or improvements to the Bitcoin Network’s source code through one or more software upgrades that alter the protocols and software that govern the Bitcoin Network and the properties of bitcoin, including the irreversibility of transactions and limitations on the mining of new bitcoin. Proposals for upgrades and discussions relating thereto take place on online forums. For example, there is an ongoing debate regarding altering the Blockchain by increasing the size of blocks to accommodate a larger volume of transactions. Although some proponents support an increase, other market participants oppose an increase to the block size as it may deter miners from confirming transactions and concentrate power into a smaller group of miners. To the extent that a significant majority of the users and miners on the Bitcoin Network install such software upgrade(s), the Bitcoin Network would be subject to new protocols and software that may adversely affect an investment in the Shares. In the event a developer or group of developers proposes a modification to the Bitcoin Network that is not accepted by a majority of miners and users, but that is nonetheless accepted by a substantial plurality of miners and users, two or more competing and incompatible Blockchain implementations could result. This is known as a “hard fork.” In such a case, the “hard fork” in the Blockchain could materially and adversely affect the perceived value of bitcoin as reflected on one or both incompatible Blockchains, that may adversely affect an investment in us.

Bitcoin has recently forked and additional forks may occur in the future which may affect the value of bitcoin held by the Company.

On August 1, 2017 bitcoin’s blockchain was forked and Bitcoin Cash was created. The fork resulted in a new blockchain being created with a shared history, and a new path forward. Bitcoin Cash has a block size of 8mb and other technical changes. On October 24, 2017, bitcoin’s blockchain was forked and Bitcoin Gold was created. The fork resulted in a new blockchain being created with a shared history, and new path forward, Bitcoin Gold has a different proof of work algorithm and other technical changes. The value of the newly created Bitcoin Cash and Bitcoin Gold may or may not have value in the long run and may affect the price of bitcoin if interest is shifted away from bitcoin to the newly created Digital Assets. The value of bitcoin after the creation of a fork is subject to many factors including the value of the fork product, market reaction to the creation of the fork product, and the occurrence of forks in the future. As such, the value of bitcoin could be materially reduced if existing and future forks have a negative effect on bitcoin’s value.

The open-source structure of the Bitcoin Network protocol means that the contributors to the protocol are generally not directly compensated for their contributions in maintaining and developing the protocol. A failure to properly monitor and upgrade the protocol could damage the Bitcoin Network and an investment in us.

The Bitcoin Network operates based on an open-source protocol maintained by contributors, largely on the Bitcoin Core project on GitHub. As an open source project, Bitcoin is not represented by an official organization or authority. As the Bitcoin Network protocol is not sold and its use does not generate revenues for contributors, contributors are generally not compensated for maintaining and updating the Bitcoin Network protocol. Although the MIT Media Lab’s Digital Currency Initiative funds the current maintainer Wladimir J. van der Laan, among others, this type of financial incentive is not typical. The lack of guaranteed financial incentive for contributors to maintain or develop the Bitcoin Network and the lack of guaranteed resources to adequately address emerging issues with the Bitcoin Network may reduce incentives to address the issues adequately or in a timely manner. This may adversely affect an investment in us.

| 11 |

If a malicious actor or botnet obtains control in excess of 50 percent of the processing power active on the Bitcoin Network, it is possible that such actor or botnet could manipulate the Blockchain in a manner that adversely affects an investment in us.

If a malicious actor or botnet (a volunteer or hacked collection of computers controlled by networked software coordinating the actions of the computers) obtains a majority of the processing power dedicated to mining on the Bitcoin Network, it may be able to alter the Blockchain on which the Bitcoin Network and all bitcoin transactions rely by constructing alternate blocks if it is able to solve for such blocks faster than the remainder of the miners on the Bitcoin Network can add valid blocks. In such alternate blocks, the malicious actor or botnet could control, exclude or modify the ordering of transactions, though it could not generate new bitcoins or transactions using such control. Using alternate blocks, the malicious actor could “double-spend” its own bitcoins (i.e., spend the same bitcoins in more than one transaction) and prevent the confirmation of other users’ transactions for so long as it maintains control. To the extent that such malicious actor or botnet does not yield its majority control of the processing power on the Bitcoin Network or the bitcoin community does not reject the fraudulent blocks as malicious, reversing any changes made to the Blockchain may not be possible. Such changes could adversely affect an investment in us.

In late May and early June 2014, a mining pool known as GHash.io approached and, during a 24- to 48-hour period in early June may have exceeded, the threshold of 50 percent of the processing power on the Bitcoin Network. To the extent that GHash.io did exceed 50 percent of the processing power on the network, reports indicate that such threshold was surpassed for only a short period, and there are no reports of any malicious activity or control of the Blockchain performed by GHash.io. Furthermore, the processing power in the mining pool appears to have been redirected to other pools on a voluntary basis by participants in the GHash.io pool, as had been done in prior instances when a mining pool exceeded 40 percent of the processing power on the Bitcoin Network. The approach to and possible crossing of the 50 percent threshold indicate a greater risk that a single mining pool could exert authority over the validation of bitcoin transactions. To the extent that the bitcoin ecosystem, including the Core Developers and the administrators of mining pools, do not act to ensure greater decentralization of bitcoin mining processing power, the feasibility of a malicious actor obtaining in excess of 50 percent of the processing power on the Bitcoin Network (e.g., through control of a large mining pool or through hacking such a mining pool) will increase, which may adversely impact an investment in us.

If the award of bitcoin for solving blocks and transaction fees for recording transactions are not sufficiently high to incentivize miners, miners may cease expending hashrate to solve blocks and confirmations of transactions on the Blockchain could be slowed temporarily. A reduction in the hashrate expended by miners on the Bitcoin Network could increase the likelihood of a malicious actor obtaining control in excess of fifty percent (50%) of the aggregate hashrate active on the Bitcoin Network or the Blockchain, potentially permitting such actor to manipulate the Blockchain in a manner that adversely affects an investment in us.

As the award of new bitcoin for solving blocks declines, and if transaction fees are not sufficiently high, miners may not have an adequate incentive to continue mining and may cease their mining operations. The current fixed reward for solving a new block is twelve and a half (12.5) bitcoin per block; the reward decreased from twenty-five (25) bitcoin in July 2016. It is estimated that it will halve again in about four (4) years. This reduction may result in a reduction in the aggregate hashrate of the Bitcoin Network as the incentive for miners will decrease. Moreover, miners ceasing operations would reduce the aggregate hashrate on the Bitcoin Network, which would adversely affect the confirmation process for transactions (i.e., temporarily decreasing the speed at which blocks are added to the Blockchain until the next scheduled adjustment in difficulty for block solutions) and make the Bitcoin Network more vulnerable to a malicious actor obtaining control in excess of fifty (50) percent of the aggregate hashrate on the Bitcoin Network. Periodically, the Bitcoin Network has adjusted the difficulty for block solutions so that solution speeds remain in the vicinity of the expected ten (10) minute confirmation time targeted by the Bitcoin Network protocol. The Company believes that from time to time there will be further considerations and adjustments to the Bitcoin Network regarding the difficulty for block solutions. More significant reductions in aggregate hashrate on the Bitcoin Network could result in material, though temporary, delays in block solution confirmation time. Any reduction in confidence in the confirmation process or aggregate hashrate of the Bitcoin Network may negatively impact the value of bitcoin, which will adversely impact an investment in us.

| 12 |

To the extent that the profit margins of Bitcoin mining operations are not high, operators of Bitcoin mining operations are more likely to immediately sell bitcoins earned by mining in the Bitcoin Exchange Market, resulting in a reduction in the price of bitcoins that could adversely impact an investment in us.

Over the past two years, Bitcoin Network mining operations have evolved from individual users mining with computer processors, graphics processing units and first generation ASIC servers. Currently, new processing power brought onto the Bitcoin Network is predominantly added by incorporated and unincorporated “professionalized” mining operations. Professionalized mining operations may use proprietary hardware or sophisticated ASIC machines acquired from ASIC manufacturers. They require the investment of significant capital for the acquisition of this hardware, the leasing of operating space (often in data centers or warehousing facilities), incurring of electricity costs and the employment of technicians to operate the mining farms. As a result, professionalized mining operations are of a greater scale than prior Bitcoin Network miners and have more defined, regular expenses and liabilities. These regular expenses and liabilities require professionalized mining operations to more immediately sell bitcoins earned from mining operations on the Bitcoin Exchange Market, whereas it is believed that individual miners in past years were more likely to hold newly mined bitcoins for more extended periods. The immediate selling of newly mined bitcoins greatly increases the supply of bitcoins on the Bitcoin Exchange Market, creating downward pressure on the price of bitcoins.