Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2011 or

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission file number: 001-34289

World Energy Solutions, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 04-3474959 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

446 Main Street

Worcester, Massachusetts 01608

(Address of principal executive offices)

(508) 459-8100

(Registrant’s telephone number, including area code)

|

Securities registered under Section 12(b) of the Act: |

Name of each exchange on which registered: | |

| Common Stock, $0.0001 par value | NASDAQ Capital Market |

Securities registered under Section 12(g) of the Act:

None

Indicate by checkmark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by checkmark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by checkmark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ |

Smaller reporting company | x | |||

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the common stock held by non-affiliates of the registrant based on the last sale price of such stock as reported by the NASDAQ Capital Market on June 30, 2011 (the last business day of the Registrant’s most recently completed second fiscal quarter) was $30,705,583.

As of March 2, 2012, the registrant had 11,874,259 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for the Annual Meeting of Stockholders to be held on May 17, 2012, are incorporated by reference into Part III of this Report.

Table of Contents

World Energy Solutions, Inc.

Form 10-K

For the Year Ended December 31, 2011

FORWARD-LOOKING STATEMENTS

This Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, which statements involve risks and uncertainties. These statements relate to our future plans, objectives, expectations and intentions. These statements may be identified by the use of words such as “may”, “could”, “would”, “should”, “will”, “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” and similar expressions. Our actual results and timing of certain events could differ materially from those discussed in these statements. Factors that could contribute to these differences include but are not limited to, those discussed under “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, and elsewhere in this Report. The cautionary statements made in this Report should be read as being applicable to all forward-looking statements wherever they appear in this Report.

Table of Contents

Overview

World Energy Solutions, Inc. (“World Energy” or the “Company”) offers a range of energy management solutions to commercial and industrial businesses, institutions, utilities, and governments to reduce their overall energy costs. The Company comes to market with a holistic approach to energy management helping customers a) contract for the lowest price for energy, b) engage in energy efficiency projects to minimize quantity used and c) maximize available rebate and incentive programs. The Company made its mark on the industry with an innovative approach to procurement via its state-of-the-art online auction platforms, the World Energy Exchange®, the World Green Exchange® and the World DR Exchange®. With recent investments and acquisitions, World Energy is building out its energy efficiency practice—offering technology-enabled solutions such as online audits of facilities to identify retrofit options and project management services for retrofit implementation, believing this practice will also enable more cross-selling opportunities for commodity auctions. The Company is also taking its suite of solutions to the rapidly growing small- and medium-sized customer markets.

World Energy provides energy management services utilizing state-of-the-art technology and the experience of a seasoned team to bring lower energy costs to its customers. The Company uses a simple equation

E = P*Q-i

to help customers understand the holistic nature of the energy management problem. Total energy cost (E) is a function of Energy Price (P) times the Quantity of Energy Consumed (Q), minus any rebates or incentives (i) the customer can earn. This approach not only makes energy management more approachable for customers, simplifying what has become an increasingly dynamic and complex problem, it also highlights the inter-related nature of the energy management challenge. The Company asserts that point solution vendors may optimize one of the three elements, but it takes looking at the problem holistically to unlock the most savings.

In April 2010, we filed an S-3 registration statement with the Securities and Exchange Commission, or SEC, using a “shelf” registration, or continuous offering, process. Under this shelf registration process, we may, from time to time, issue and sell any combination of preferred stock, common stock or warrants, either separately or in units, in one or more offerings with a maximum aggregate offering price of $20,000,000, including the U.S. dollar equivalent if the public offering of any such securities is denominated in one or more foreign currencies, foreign currency units or composite currencies. In April 2011 we issued 1.5 million shares of common stock utilizing this shelf registration to several accredited institutional investors at $3.60 per share, yielding net proceeds of approximately $5.3 million. We intend to use this shelf registration for future offerings when prices and equity markets are beneficial to us.

The net proceeds raised to date were applied in the third and fourth quarters of 2011 to make three acquisitions. We purchased the book of energy contracts from Co-eXprise, Inc., expanding our customer base in the auction market, particularly in the government space. We acquired the assets and certain liabilities of Northeast Energy Solutions, LLC, a small efficiency shop based in Connecticut. Finally we acquired the assets and certain liabilities of GSE Consulting, LP, a mid-market broker principally serving the Texas market. These acquisitions strengthen our leadership position in energy auctions, supplement our emerging expansion efforts into the efficiency space, and provide us with strong base in the growing small- and medium-sized customer marketplaces of the energy brokerage industry.

The Retail Energy Industry

Retail Electricity Deregulation

The electricity industry in the United States is governed by both federal and state laws and regulations, with the federal government having jurisdiction over the sale and transmission of electricity at the wholesale level in interstate commerce, and the states having jurisdiction over the sale and distribution of electricity at the retail level.

The federal government regulates the electricity wholesale and transmission business through the Federal Energy Regulatory Commission, or FERC, which draws its jurisdiction from the Federal Power Act, and from other legislation such as the Public Utility Regulatory Policies Act of 1978, the Energy Policy Act of 1992, and the Energy Policy Act of 2005, or EPA 2005. FERC has comprehensive and plenary jurisdiction over the rates and terms for sales of power at wholesale, and over the organization, governance and financing of the companies engaged in such sales. States regulate the sale of electricity at the retail level within their respective jurisdictions, in accordance with individual state laws which can vary widely in material respects. Restructuring of the retail electricity industry in the United States began in the mid-1990s, when certain state legislatures restructured their electricity markets to create competitive markets that enable energy consumers to purchase electricity from competitive energy suppliers.

1

Table of Contents

Prior to the restructuring of the retail electricity industry, the electricity market structure in the United States consisted of vertically integrated utilities which had a near monopoly over the generation, transmission and distribution of electricity to retail energy consumers. In states that have embraced electricity restructuring, the generation component (i.e., the source of the electricity) has become more competitive while the energy delivery functions of transmission and distribution remain as monopoly services provided by the incumbent local utility and subject to comprehensive rate regulation. In other words, in these states, certain retail energy consumers (specifically, those served by investor-owned utilities and not by municipal power companies or rural power cooperatives) can choose their electricity supplier but must still rely upon their local utility to deliver that electricity to their home or place of business.

The structure and, ultimately, the success level of industry restructuring has been determined on a state by state basis. There have been three general models for electricity industry restructuring: (i) delayed competition, (ii) phased-in competition, and (iii) full competition. The delayed competition model consists of the state passing legislation authorizing competitive retail electricity markets (i.e., customer choice of electric energy supplier), however, no action is taken by the state regulatory authority charged with utility industry oversight within such state to change the incumbent utility rates for electric energy to encourage competition. The phased-in competition model consists of the state passing legislation authorizing competitive retail electricity markets together with a gradual change of the incumbent utility’s retail electric rates to encourage the competitive supply of electricity over time. The full competition model consists of the state passing legislation authorizing competitive retail electricity markets together with an immediate change to the incumbent local utilities’ retail electric rates that results in the whole commercial, industrial and government, or CIG, electricity market in such state being competitive immediately.

Energy consumers who choose to switch electricity suppliers can either do it themselves by contacting competitive energy suppliers directly, or indirectly, by engaging aggregators, brokers or consultants, collectively referred to as ABCs, to assist them with their electricity procurement.

Energy Suppliers: These entities take title to power and resell it directly to energy consumers. These are typically well-funded entities, which service both energy consumers directly and also work with ABCs, to contract with energy consumers. Presently, we estimate there are over 150 competitive suppliers, several of which operate on a national level and are registered in nearly all of the 16 states and the District of Columbia that permit CIG energy consumers to choose their electricity supplier and have deregulated pricing to create competitive markets. Of the 16 deregulated states, 13 have fully viable competitive markets.

Aggregators, Brokers and Consultants: ABCs facilitate transactions by having competitive energy suppliers compete against each other in an effort to get their energy customers the lowest price. This group generally uses manual request for proposal, or RFP, processes that are labor intensive, relying on phone, fax and email solicitations. We believe that the online RFP process is superior to the traditional paper-based RFP process as it involves a larger number of energy suppliers, can accommodate a larger number of bids within a shorter time span, and allows for a larger amount of contract variations including various year terms, territories and energy usage patterns.

Online Brokers: Online brokers are a subset of the ABCs. These entities use online platforms to run electronic RFP processes in an effort to secure the lowest prices for their energy customers by having competitors bid against one another. We believe that we are among the pioneering companies brokering electricity online and we are not aware of any competitor that has brokered more electricity online than we have.

Retail Natural Gas

The natural gas industry in the United States is governed by both federal and state laws and regulations, with the federal government having jurisdiction over the transmission of natural gas in interstate commerce, and the states having jurisdiction over the sale and distribution at the retail level.

The federal government regulates the natural gas transmission business through FERC which draws its jurisdiction from the Natural Gas Act, and from other legislation such as the EPA 2005. FERC has comprehensive and plenary jurisdiction over the rates and terms for transmission of gas in interstate commerce, and over the organization, governance and financing of the companies engaged in such transmission. States regulate the distribution and sale of gas at the retail level within their respective jurisdictions, in accordance with individual state laws which can vary widely in material respects.

The natural gas market in the United States is deregulated in most states and offers retail energy consumers access to their choice of natural gas commodity supplier.

Following a period of heavy regulation, the gas industry was deregulated in three phases as a result of legislation enacted in 1978 followed by multiple orders of FERC. The expected result of this deregulation was to stimulate competition in the natural gas industry down the pipeline to the distribution level.

At the retail level, reforms and restructuring have taken place on a state by state basis, with varying nuances to the restructuring in different states. For example, state commissions have allowed local distribution companies to offer unbundled transportation service to large customers; occasionally to provide flexible pricing in competitive markets; and to engage in other competitive activities.

2

Table of Contents

Today, we estimate that utilities in over 40 states permit retail natural gas consumers to choose their natural gas commodity suppliers. In most instances, the local distribution utility still delivers the commodity to the consumers’ premises, even if a different supplier is selected to provide the commodity. The level of competitive choice available to retail CIG energy consumers has increased, with a wide range of products and a significant number of suppliers participating in both retail and wholesale transactions.

Demand Response

The electric power industry in North America faces enormous challenges to keep pace with the expected increase in demand for electricity and to manage the increased amount of intermittent renewable energy resources that are expected to be connected to the power grid in the future. Because electricity cannot be economically stored using commercially available technology today, it must be generated, delivered and consumed at the moment that it is needed by end-use customers. Maintaining a reliable electric power grid therefore requires real-time balancing between supply and demand. Power generation, transmission and distribution facilities are built to capacity levels that can service the maximum amount of anticipated demand plus a reserve margin intended to serve as a buffer to protect the system in critical periods of peak demand or unexpected events such as failure of a power plant or major transmission line. However, under-investment in generation, transmission and distribution infrastructure in recent years in key regions, coupled with a dramatic growth in electricity consumption over that same time period, has led to an increased frequency of voltage reductions—commonly known as brownouts—and blackouts, and periodically prevents the transport of power to constrained areas during periods of peak demand, which can affect reliability and cause significant economic impacts.

As the electric power industry confronts these challenges, demand response (DR) has emerged as an important solution to help address the imbalance in electric supply and demand. For example, the EPA 2005 declared it the official policy of the United States to encourage demand response and the adoption of devices that enable it. In addition, the Energy Independence and Security Act of 2007 ordered the FERC to conduct a nationwide assessment of demand response potential and create a national action plan to promote demand response at the federal level and support individual states in their own demand response initiatives.

Our customers in the DR market are energy consumers that agree to curtail their electricity consumption when requested by Regional Transmission Organizations (“RTOs”) or Independent System Operators (“ISOs”) during times of peak demand. We bring together these energy consumers with Curtailment Service Providers (“CSPs”) to auction off the energy consumers capacity. CSPs compete against each in a forward auction, bidding up the percentage of the demand response revenue that the energy consumer will receive from a specific DR program.

Energy Efficiency

There is an increasing emphasis on energy efficiency as an important aspect of national energy policy, smart grid solutions and facility management best practices. For example, the White House estimates that commercial buildings consumed roughly 20 percent of all energy in the U.S. in 2010. Additionally Pike Research, a leading industry analyst firm, estimates that if all commercial buildings underwent efficiency retrofits (noting that 80% of all commercial buildings are more than 10 years old), the payout would be on the order of $41.1 billion each year.

Large drivers of the overall efficiency market include the national Better Buildings initiative, which aims for 20% efficiency gains in commercial buildings by 2020 through cost-effective upgrades, and New York City’s Greener, Greater Buildings Plan aimed at reducing energy consumption by existing buildings, which account for 70-80% of the City’s total greenhouse gas emissions.

Several utilities offer incentive programs that encourage efficiency as well. These programs collect an efficiency surcharge from each customer in their territories, and then provide rebate programs that offset the costs of approved energy retrofits for lighting, mechanical and HVAC systems.

With our recent investments, extensive base of federal and state government clients, growing footprint in the commercial property space, and large channel partner network that includes leading energy service companies, we expanded our presence in the energy efficiency market with our acquisition of Northeast Energy Solutions, LLC (“NES”) in October 2011. NES focuses on turn-key electrical and mechanical energy efficiency measures serving commercial, industrial and institutional customers.

Wholesale Energy

The wholesale electricity market is the competitive market that connects generators (sellers) with utilities, electricity retailers and intermediaries (buyers) who purchase electricity to re-sell on the retail market. We estimate that total wholesale purchases of electric power in 2011 was over 4.1 billion MWh. Natural gas is an important input fuel for generators, and U.S. consumption of natural gas in 2010 exceeded 24 trillion cubic feet.

The U.S. wholesale electricity market emerged in the late 1970s when independent power producers, or IPPs, and other non-utilities entered the electricity generation market, although the market was restricted until the early 1990s when competitive constraints were removed. These new generation entities began to compete directly with traditional utilities and offered customers more than one choice to obtain electricity. Today, participants in the wholesale market include IPPs, traditional utilities, and intermediary power marketers. In addition, banks, traders, and brokers participate in the wholesale market.

3

Table of Contents

IPPs and traditional utilities comprise the generation portion of the wholesale market. Many employ internal sales forces to assist in the sale and distribution of their power, enabling them to participate as both buyers and sellers within the wholesale market. However, a growing number of IPPs and utilities have found it easier and more cost effective to sell their generation through power marketing services, which has contributed to the power marketers’ increased role within the market. Power marketers utilize several different platforms to purchase power from generators for distribution, which include paper RFPs, phone brokerage, electronic exchanges and auctions.

Our customers in the wholesale market can be either buyers or sellers and can include utilities and municipal utilities that buy power or natural gas to fill in gaps in their portfolios or to consume in their generation facilities, and retail marketers who buy natural gas and power to resell to retail customers. If the customer is a buyer, we will run a reverse (descending price) auction to secure a lower price. If the customer is a seller, we will run a forward (ascending price) auction to secure a higher price.

Environmental Commodities

Concerns about global warming have spawned a number of initiatives to reduce greenhouse gas emissions. The most widely adopted of these initiatives is the Kyoto Protocol pursuant to which many countries in Europe, Asia and elsewhere have created carbon cap and trade systems. In carbon cap and trade programs, carbon dioxide emission caps are established and producers of these emissions can buy or sell credits in order to meet their required allocations. While the United States did not ratify the Kyoto Protocol, there are a number of initiatives in the U.S. at the regional, state and local levels aimed at limiting greenhouse gas emissions, the most robust of which is the Regional Greenhouse Gas Initiative (“RGGI”).

In August 2008, we were awarded a two-year contract with RGGI, subsequently extended for an additional two-year period, which is the first mandatory, market based effort in the United States to reduce greenhouse gas emissions. RGGI selected our World Green Exchange® to sell allowances for the emitting of carbon dioxide emissions from the power sector. In accordance with this contract the Company has conducted quarterly auctions for RGGI over a three-and-half-year period and will conduct additional quarterly auctions through July 2012. We successfully completed fourteen quarterly auctions for RGGI through December 31, 2011.

Company Strategy and Operations

Overview

World Energy offers a range of energy management solutions to commercial and industrial businesses, institutions, utilities, and governments to reduce their overall energy costs. The Company comes to market with a holistic approach to energy management helping customers a) contract for the lowest price for energy, b) engage in energy efficiency projects to minimize quantity used and c) maximize available rebate and incentive programs. The Company made its mark on the industry with an innovative approach to procurement via its state-of-the-art online auction platforms, the World Energy Exchange®, the World Green Exchange® and the World DR Exchange®. With recent investments and acquisitions, World Energy is building out its energy efficiency practice—offering technology-enabled solutions such as online audits of facilities to identify retrofit options and project management services for retrofit implementation, believing this practice will also enable more cross-selling opportunities for commodity auctions. The Company is also taking its suite of solutions to the growing small- and medium-sized customer marketplaces.

World Energy provides energy management services utilizing state-of-the-art technology and the experience of a seasoned management team to bring lower energy costs to its customers. The company uses a simple equation

E = P*Q-i

to help customers to understand the holistic nature of the energy management problem. Total energy cost (E) is a function of Energy Price (P) times the Quantity of Energy Consumed (Q), minus any rebates or incentives (i) the customer can earn. This approach not only makes energy management more approachable for customers, simplifying what has become an increasingly dynamic and complex problem, it also highlights the inter-related nature of the energy management challenge. The Company asserts that point solution vendors may optimize one of the three elements, but it takes looking at the problem holistically to unlock the most savings. We help customers optimize this equation by applying the Seven Levers of Energy Management™—Planning, Sourcing, Risk Management, Efficiency, Sustainability, Incentives and Monitoring.

These Seven Levers are supported by state of the art technology developed or licensed by the Company. We have developed three online auction platforms, the World Energy Exchange®, the World Green Exchange® and, most recently, the World DR Exchange®. On the World Energy Exchange® energy consumers in North America are able to negotiate for the purchase or sale of electricity, natural gas and other energy resources from competing energy suppliers which have agreed to participate on our auction platform in a given event. On the World Green Exchange®, buyers and sellers negotiate for the purchase or sale of environmental commodities such as Renewal Energy Certificates (RECs), Verified Emissions Reductions (VERs) and Certified

4

Table of Contents

Emissions Reductions (CERs). On the World DR Exchange®, CSPs and energy consumers are brought together in highly-structured auction events designed to yield price transparency, heighten competition, and maximize the energy consumers’ share of demand response revenues.

We bring bidders and listers together in our online marketplaces, often with the assistance of our channel partners, who identify and work with customers to consummate transactions. Our exchanges are comprised of a series of software modules that automate our comprehensive procurement process including:

| • | energy and environmental commodities sourcing management — a database of suppliers and contacts; |

| • | lead management — a module to track prospective customers through the sales process; |

| • | deal and task management — a module to list, assign and track steps to complete a procurement successfully; |

| • | market intelligence — databases of information related to market rules and pricing trends for markets; |

| • | request for proposal, or RFP, development — a module to create RFPs with a variety of terms and parameters; |

| • | conducting auctions — underlying software to manage the bidding and timing of an auction and display the results; |

| • | portfolio management — a database of contracts, sites, accounts and usage; |

| • | risk management – monitoring, triggering and messaging tools; |

| • | commission reporting — a system to display forecasted and actual commissions due to channel partners; and |

| • | receivables management — a system to upload data received from suppliers and track payment receipt. |

Our technology-based solution is attractive to channel partners as it provides them with a business automation platform to enhance their growth, profitability and customer satisfaction. Channel partners are important to our business because these entities offer our auction platforms to enhance their service offerings to their customers. By accessing our market intelligence and automated auction platform, channel partners significantly contribute to our transaction volume, and in return we pay them a fixed percentage of the revenue we receive from winning bidders (i.e., energy suppliers and other buyers). This third party commission structure is negotiated in advance within the channel partner agreement based on a number of factors, including expected volume, effort required in the auction process and competitive factors.

As a requirement to bid in an auction (which is described in greater detail below), bidders must enter into an agreement to pay our fee if they execute a contract as a result of the auction. Following an auction event, our employees continue to work with the energy consumer and other listers or collectively, the customer, and bidder through the contract negotiation process and, accordingly, we are aware of whether a contract between the customer and bidder is consummated. If a contract is entered into between a customer and bidder using our auction platforms, we are compensated based upon a fixed fee, or commission rate, that is built into the price of the commodity. This approach is attractive to both the customer and bidder as there is no fee charged to either party if the brokering process does not result in a contract. Our fees are based on the total amount of the commodity transacted between the customer and bidder multiplied by our contractual commission rate. We have master agreements with our bidders, whereby bidders are allowed to bid on customer requirements in exchange for agreeing to pay the fee that we have negotiated with the customer. In order to participate in any specific auction, bidders are required to acknowledge and agree to our fee on our online platform prior to participating in that auction.

Retail Electricity Transactions

For retail electricity transactions, monthly revenue is based on actual usage data obtained from the energy supplier for a given month or, to the extent actual usage data is not available, based on the estimated amount of electricity delivered to the energy consumer for that month. While the number of contracts closed via the World Energy Exchange® in any given period can fluctuate widely due to a number of factors, this revenue recognition method provides for a relatively predictable revenue stream, as revenue is based on energy consumers’ actual historical energy usage profile. However, monthly revenue can still vary from our expectations because usage is affected by a number of variables which cannot always be accurately predicted, such as the weather and the general business conditions affecting our energy consumers.

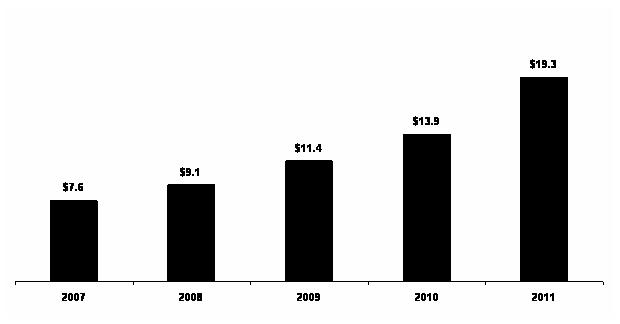

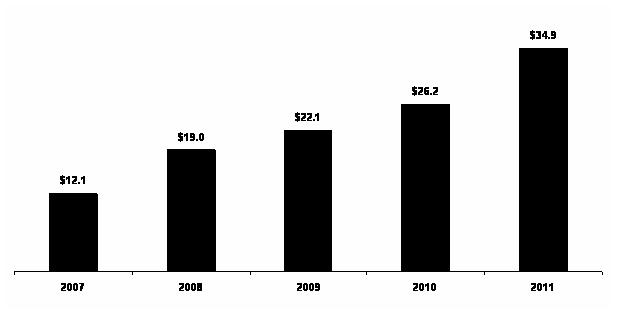

Contracts between energy consumers and energy suppliers are signed for a variety of term lengths, with a one-year contract term being typical for commercial and industrial energy consumers, and government contracts typically having two to three year, and occasionally five-year terms. Backlog relates to contracts in force on a given date representing transactions between bidders and listers on our platform related to commodity brokerage assuming listers consume energy at their historical levels or deliver credits at expected levels. The chart below displays our annualized and total backlog from year-end 2007 through 2011. Total backlog represents the revenue that we would derive over the remaining life of those contracts. Annualized backlog represents the revenue that we would derive from those contracts within the twelve months following the date on which the backlog is

5

Table of Contents

calculated. For any particular contract, annualized backlog is calculated by multiplying the energy consumer’s historical usage by our fixed contractual commission rate. This metric is not intended as an estimate of overall future revenues, since it does not purport to include revenues that may be earned during the relevant backlog period from new contracts or renewals of contracts that expire during such period. In addition, annualized backlog does not represent guaranteed future revenues, and to the extent actual usage under a particular contract varies from historical usage, our revenues under such contract will differ from the amount included in backlog.

In addition to retail electricity contracts, we have ongoing contractual arrangements with retail natural gas customers under which we deliver certain energy management and auction administration services for which we receive a monthly fee. Total and annualized backlog as at December 31, 2011 includes monthly management fees related to natural gas contracts of $1.0 million that have expected revenue associated with them from January 1, 2012 through December 31, 2012. These contracts can be terminated within 30 days notice per the terms of the contracts and, therefore, backlog does not include any revenue from expected contract renewals or expected fees beyond December 31, 2012.

Annualized Backlog

(in millions)

Total Backlog

(in millions)

6

Table of Contents

Because the calculation of backlog is a calculation of a contracted commission rate multiplied by a historical energy usage figure and our management contracts are cancelable by our natural gas customers, our backlog may not necessarily be indicative of future results. Annualized backlog should not be viewed in isolation or as a substitute for our historical revenues presented in the financial statements included in this Form 10-K. Events that may cause future revenues from contracts in force to differ materially from our annualized backlog include the events that may affect energy usage, such as overall business activity levels, changes in energy consumers’ businesses, weather patterns and other factors described under “Risk Factors”. The Company also recognizes revenue from certain mid-market transactions as cash is received from the energy supplier.

Retail Natural Gas Transactions

There are two primary fee components to our retail natural gas services—transaction fees and management fees. Transaction fees are billed to and paid by the energy supplier awarded business on the platform. Transaction fees for natural gas and electricity awards are established prior to award and are the same for each supplier. For the majority of our natural gas transactions, we invoice the supplier upon the conclusion of the transaction based on the estimated energy volume transacted for the entire award term multiplied by the transaction fee. Management fees are paid by our energy consumers and are generally billed on a monthly basis for services rendered based on terms and conditions included in contractual arrangements. While substantially all of our retail natural gas transactions are accounted for in accordance with this policy, a certain percentage is accounted for as the natural gas is consumed by the customer.

Demand Response Transactions

Demand response transaction fees are recognized when we have received confirmation from the CSP that the energy consumer has performed under the applicable RTO or ISO program requirements. The energy consumer is either called to perform during an actual curtailment event or is required to demonstrate its ability to perform in a test event during the performance period. For the PJM Interconnection (“PJM”), an RTO that coordinates the movement of wholesale electricity in all or parts of 13 states and the District of Columbia, the performance period is June through September in a calendar year. Test results are submitted to PJM by the CSPs and we receive confirmation of the energy consumers’ performance in the fourth quarter. CSPs typically pay us ratably on a quarterly basis throughout the demand response fiscal (June to May) year. As a result, a portion of the revenue we recognize is reflected as unbilled accounts receivable.

Wholesale Transactions

Wholesale transaction fees are invoiced upon the conclusion of the auction based on a fixed fee. These revenues are not tied to future energy usage and are recognized upon the completion of the online auction. For reverse auctions where our customers bid for a consumer’s business, the fees are paid by the bidder. For forward auctions where a lister is selling energy, the fees are typically paid by the lister. While substantially all wholesale transactions are accounted for in this fashion, a small percentage of our wholesale revenue is accounted for as the electricity or gas is delivered.

Environmental Commodity Transactions

Environmental commodity transaction fees are accounted for utilizing two primary methods. For regulated allowance programs like RGGI, fees are paid by the lister and are recognized as revenue quarterly as auctions are completed and approved. For all other environmental commodity transactions both the lister and the bidder pay a transaction fee and revenue is recognized upon the consummation of the underlying transaction as credits are delivered by the lister and payment is made by the bidder.

Energy Efficiency Services

The Company generally recognizes revenues for energy efficiency services when persuasive evidence of an arrangement exists, delivery has occurred, the price is fixed or determinable and collectability is reasonably assured. Due to the short-term nature of projects (typically two to three weeks), the Company utilizes the completed-contract method. Revenues are recognized based upon factors such as passage of title, installation, payments and customer acceptance.

The Brokerage Process

Our brokerage process is supported by a variety of modules designed with the goal to find the best possible price while providing step-by-step process management and detailed documentation prior to, during and following the auction. Our process includes data collection and analysis, establishing the benchmark price, conducting multiple auction events to enable testing of various term and price combinations and assisting in contract completion. We create an audit trail of all the steps taken in a given transaction. Specific web pages track all information provided to energy suppliers including energy supplier calls, supplier invitations, usage profiles and desired contract parameters.

At the commencement of the process, non-government energy consumers will enter into a procurement services agreement with us pursuant to which we are appointed as the brokerage service provider to solicit and obtain bids for the supply of energy or environmental commodities and to assist in the procurement of these commodities. Government energy consumers will send out a

7

Table of Contents

solicitation at the commencement of the brokerage process which sets out the contract terms. Only bidders that are qualified under the solicitation may participate in the auction. Bidders who wish to bid on the provision of energy or environmental commodities to such customers must partake in our brokerage process and cannot contract with customers outside of our brokerage process.

For retail energy, the procurement services agreement authorizes us to retrieve the energy consumer’s energy usage history from the utility serving its accounts. We utilize the usage history to identify and analyze the energy consumer’s energy needs and to run a rate and tariff model which calculates the utility rate for that energy consumer’s facilities. This price is used as a benchmark price to beat for the auction event. For other customers or commodities, the benchmark price may be negotiated or calculated in another manner.

Prior to conducting the auction, the auction parameters, including target price, supplier preferences, contract terms, payment terms and product mix, as applicable, are discussed with the customer and agreed upon. Approximately two to five days prior to the auction, we will post RFPs with these auction parameters on our World Energy Exchange®, World DR Exchange® or World Green Exchange® and alert the potential bidders. Additionally, bidders are provided with information about the customer, historical energy usage information relating to the energy consumer’s facilities (if retail customers), and the desired contract parameters, several days in advance of the auction as part of the RFP. This advanced notice gives the bidders the opportunity to analyze the value of a potential deal and the creditworthiness of the customer. We believe that, using this information along with the auction parameters described in the RFP, the bidders develop a bidding strategy for the auction.

The auction is run on the World Energy Exchange®, World DR Exchange® or the World Green Exchange®, depending on the commodity auctioned. The auction creates a competitive bidding environment that is designed to cause bidders to deliver better prices in response to other competitive bids. Specifically, bidders enter an auction by submitting an opening bid at or better than the suggested opening bid posted on the RFP. After they enter the auction and assess the bidding activity, bidders may begin testing the competition by submitting a bid better than the then-leading bid. They do this presumably to test their pricing and to gauge the relative level of competition for the deal. There is typically a modest level of bidding and counter-bidding activity among bidders until the final 30 seconds of the auction when bidding activity tends to increase. In the final seconds, all bidders see the then-leading bid and must make a judgment as to how aggressively to submit their last bid in order to win the deal. At this point in the auction, bidders make their final bid without knowledge of what any other bidders are bidding. We call this a final “blind” bid.

Typically, a number of auctions tailored to the customer’s specific needs will be held. Our exchanges provide rapid results and can accommodate a multitude of permutations for offers, including various year terms, quantities, load factors and green power requirements. For commercial and industrial customers or project owners, we typically run two to six auction events per procurement and for large government aggregations that generally are more complex, we typically run 20 to 40 auction events. Each auction event usually lasts 15 minutes or less. Included as part of any auction transaction are date and time stamping of bids, comparison of each bid with benchmark prices, as well as automated stop times, which ensure the integrity of auction events. The exchanges are also periodically synchronized to the atomic clock which is intended to ensure that auction start and stop times are precise.

Following an auction, the auction results are analyzed and if the auction has been successful, we assist the customer with the contracting process with the winning bidder which is typically finalized within one hour of the closing of the last auction event. In the case of a commercial energy consumer, we facilitate any remaining discussion between the leading energy supplier and the energy consumer relating to the energy supplier’s contract terms that were not addressed in establishing the auction parameters. In the case of government energy consumers, the energy suppliers have seen and, in general, have agreed to the form of supply contract being required by the government energy consumer. Accordingly, the time period between the end of the auction and the execution of a contract is usually shorter than in the case of non-government energy consumers. Not all auctions result in awarded contracts.

For retail energy transactions, the incumbent local utility serving a given location is typically obligated to deliver the commodity to the customer’s premises from the location where the supplier delivers electricity energy into that local utility’s delivery system. However, the energy supplier is responsible for enrolling the energy consumer’s account with the applicable local utility and the energy supplier remains liable for any costs resulting from the physical loss of energy during transmission and delivery to the customer’s premises. We never buy, sell or take title to the energy products or environmental commodities on our auction platforms.

We typically interface directly with the customer throughout the brokerage process. However, if a channel partner is involved, the channel partner will often perform one or more of the following functions: working with a customer to sign a procurement services agreement, interacting with the customer relating to World Energy analyses, supporting the decision-making, and interfacing with the customer during the contracting process. However, even if a channel partner is involved, we are still primarily responsible for tasks such as interacting with utilities to obtain an energy consumer’s usage history, performing analyses, creating RFPs, interfacing with bidders, and scheduling, conducting and monitoring auctions and collecting the commission earned from the bidder.

8

Table of Contents

Growth Strategy

Our overall objective is to leverage our preeminent position as the exchange of choice for executing transactions in energy, energy related services and environmental commodities to be a leader in the energy management space.

We seek to achieve our objective by expanding our community of channel partners, customers and bidders on our exchange, strengthening and expanding long-term relationships with government agencies, broadening our product offerings, making strategic acquisitions, and growing our sales force. Key elements of our strategy are as follows:

Leveraging New Products such as Demand Response, Risk Management and Efficiency. We continue to expand our offerings either organically (World DR Exchange) or via acquisition (risk management via Energy Gateway and efficiency via Northeast Energy Solutions), and sell them to new prospects or existing customers via our sales force and channel network.

Continuing to Develop Channel Partner Relationships. A significant amount of the customers using our auction platforms have been introduced to us through our channel partners. Our plan is to focus on developing and increasing our number of channel partner relationships in an effort to expand the base of customers using our auction platforms. We have consistently increased the number of channel partners since 2007 from 42 to 187 at December 31, 2011.

Strengthening and Expanding Long-term Relationships with Government Agencies. We intend to continue to build on the relationships we have established with federal, state and local government agencies. We expect that our expertise in brokering cost-saving energy contracts for government agencies will continue to be in demand as contract terms expire and governments look to contract for low energy prices in a competitive market.

Expand our Share in the Natural Gas Market. While our core competence has traditionally been in electricity brokerage for retail energy consumers, we significantly expanded our share of the natural gas market with our 2007 acquisition of EnergyGateway, LLC. This acquisition provided us with additional staff, natural gas expertise and a post-and-respond software solution to add to our auction capability. We expect this combination to continue to strengthen our natural gas offering and present cross-selling opportunities.

Continue to expand in the Wholesale Market. An important rationale for our initial public offering was to enter the wholesale market where we had initial success in 2006. We have grown our customer base from 12 in 2007 to 81 as of December 31, 2011, of which forty-nine have contributed to revenue to date.

Push into the Mid-Market: We see the mid-market as being a viable growth opportunity, and with our acquisition of GSE Consulting we added a base of expertise that can enable us to take their Texas footprint and expand it nationally.

Making Strategic Acquisitions. From time to time, we also pursue strategic acquisitions to help us expand geographically, add expertise and product depth, provide accretive revenue and profit streams or a combination of two or more of the above. We believe with our public currency and automated systems that we are a logical entity to roll up the industry.

Bidders, Listers and Channel Partners

Bidders. Our success is heavily dependent on our bidder relationships, the credibility of our bidders and the integrity of the auction process. Bidders include over 280 competitive electricity and natural gas suppliers and over 190 wholesale electricity suppliers registered on the World Energy Exchange®, representing a majority of all suppliers in the deregulated electricity and natural gas markets. To date, there are over 150 registered bidders on the World Green Exchange®. Of the registered energy suppliers, approximately 160 had active contracts with energy consumers that were brokered through our World Energy Exchange® as of December 31, 2011. Two of these bidders accounted for 23% and 22% in the aggregate of our revenue for the years ended December 31, 2011 and 2010, respectively. In order to participate in an auction event, bidders must register with us by either entering into a standard-form agreement pursuant to which the bidder is granted a license to access our auction platform and bid at auction events or by qualifying to participate in an auction pursuant to a government solicitation. Our national standard form agreement is typically for an indefinite term, may be terminated by either party upon 30 days prior written notice, is non-exclusive, non-transferable and cannot be sublicensed. Under our standard-form agreement or the government solicitation, the bidder agrees to pay us a commission, which varies from contract to contract and is based on a set rate per energy unit consumed by the lister.

Listers. Listers using our auction platform to procure energy, demand response and environmental commodities include government agencies, commercial and industrial energy consumers, utilities, municipal utilities, environmental commodity project owners, financial institutions and brokers. Government energy consumers have complex energy needs in terms of both scope and scale, which we believe can best be met with a technology-based solution such as our exchanges. Additionally, the automated nature of our exchanges is designed to support protest free auctions. We have brokered energy for the General Services Administration (“GSA”) and over 25 federal agencies, and numerous county and state governments including the 10 Northeast and Mid-Atlantic states participating in RGGI.

Our contracts for the online energy procurements with these governmental entities are typically for multiple years ranging from

9

Table of Contents

two to five years. During this contractual period, the governmental entity may run various auctions for different locations or agencies that fall under their purview. As a result, revenue from these customers could extend beyond the actual contractual term. As additional states open their electricity markets to competition and suppliers enter those markets creating a competitive landscape, we plan to actively market our services to them. These contracts do not require that the government energy consumer use our services and, as is typical in government procurements, contain termination for convenience and fiscal funding clauses. If a contract was terminated for convenience, it would typically not have any bearing on energy delivered through the termination date.

None of the energy consumers using our auction platform accounted for 10% or more of our aggregate revenue for the years ended December 31, 2011 and 2010, respectively.

Direct Sales. Retail targets of direct sales efforts are typically large companies with facilities in many geographic locations including hotel chains, property management firms, big box retailers, supermarkets, department stores, drug stores, convenience stores, restaurant chains, financial services firms and manufacturers across various industries. We also are pursuing utilities, municipal utilities, and retail energy providers in the wholesale market, and project owners, customers seeking to meet compliance obligations, and brokers in the environmental commodities markets.

Channel Partners. We also target customers through our channel partner model. These are firms with existing client relationships with certain customers that would benefit from the addition of an online procurement solution. Channel partners consist of a diverse array of companies including energy service companies, demand side consultants and manufacturers, ABCs and strategic sourcing companies, but in the most general terms they are resellers or distributors. As of December 31, 2011, we had entered into agreements with 187 channel partners that are currently engaged in efforts to source potential transactions to our exchanges, although not all have sourced a transaction for which an auction has been completed. Upon identifying opportunities with new channel partners, we enter into a channel partner agreement that grants the channel partner a non-exclusive right to sell our procurement process typically for a term of one year, which renews automatically unless terminated upon 30 days written notice. The channel partner receives a commission based generally on the amount of involvement of the channel partner in the procurement process.

Competition

Customers have a broad array of options when purchasing energy or environmental commodities. Retail energy consumers can either purchase energy directly from the utility at the utility’s rate or purchase energy in the deregulated market through one of the following types of entities: competitive energy suppliers, ABCs and online brokers. We compete with competitive energy suppliers, ABCs and other online brokers for energy consumers that are seeking an alternative to purchasing directly from the utility. Demand response customers typically negotiate demand response services directly with CSPs. Wholesale customers typically buy from generators, traders, traditional brokers who use phone-based methods, or bid-ask exchanges. Environmental commodity customers typically buy or sell directly through bilateral transactions, brokers, traders or bid-ask exchanges. Energy Efficiency Services customers typically use small to medium size lighting companies for their lighting efficiency measure. These lighting companies outsource any mechanical efficiency measures to small heating, ventilation, air condition (HVAC) contractors.

Technology

The auction platform that powers our exchanges is comprised of a scalable transaction processing architecture and web-based user interface. The auction platform is primarily based on internally developed proprietary software, but also includes third party components for user interface elements and reporting. The auction platform supports the selling and buying processes including bid placements, bidder registration and management, channel partner management, deal process management, contract management, site management, collection and commission management, and reporting. The auction platform maintains current and historical data online for all of these components.

Our technology systems are monitored and upgraded as necessary to accommodate increasing levels of traffic and transaction volume on the website. However, future upgrades or additional technology licensing may be required to ensure optimal performance of our auction platform services. See “Risk Factors” at Item 1A. To provide maximum uptime and system availability, our auction platform is hosted in a multi-tiered, secure, and reliable fault tolerant environment which includes backup power supply to computer equipment, climate control, as well as physical security to the building and data center. In the event of a major system component failure, such as a system motherboard, spare servers are available.

We strive to offer a high level of data security in order to build the confidence in our services among customers and to protect the participants’ private information. Our security infrastructure has been designed to protect data from unauthorized access, both physically and over the Internet. The most sensitive data and hardware of the exchanges reside at the data centers.

Seasonality

Our revenue is subject to seasonality and fluctuations during the year primarily as a result of weather conditions and its impact on the demand for energy. The majority of our revenue is generated from the commissions we receive under any given energy contract, which is tied to the energy consumer’s consumption of energy. Therefore, revenue from natural gas consumption tends

10

Table of Contents

to be strongest during the winter months due to the increase in heating usage, and revenue from electricity consumption tends to be strongest during the summer months due to the increase in air conditioning usage. Our revenue is also subject to fluctuations within any given season, depending on the severity of weather conditions — during a particularly cold winter or an unseasonably warm summer, energy consumption will rise. In addition, transaction revenue in the natural gas and wholesale markets for which we invoice upon completion of the respective transaction tends to be higher in the first and fourth quarters when utilities and natural gas customers make their annual natural gas buys.

Intellectual Property

We enter into confidentiality and non-disclosure agreements with third parties with whom we conduct business in order to limit access to and disclosure of our proprietary information.

We operate our platform under the trade names “World Energy Exchange®” and “World Green Exchange®”. We own the following registered trademarks in the United States: World Energy Solutions®, World Green Exchange®, World DR Exchange® and World Energy Exchange®. We also own the following domain names: worldenergy.com, wesplatform.com, wexch.com, worldenergyexchange.com, echoicenet.com, e-choicenet.com, worldenergysolutions.com, worldenergysolutions.net, worldenergy.biz, worldgreenexchange.com, worldgreenexchange.biz, worldgreenexchange.info, worldgreenexchange.us, worldpowerexchange.com, and worldenergysolutionsinc.com. To protect our intellectual property, we rely on a combination of copyright and trade secret laws and the domain name dispute resolution system.

Our corporate name and certain of our trade names may not be eligible for protection if, for example, they are generic or in use by another party. We may be unable to prevent competitors from using trade names or corporate names that are confusingly similar or identical to ours.

We do not have any patents and if we are unable to protect our copyrights, trade secrets or domain names, our business could be adversely affected. Others may claim in the future that we have infringed their intellectual property rights.

Personnel

As of December 31, 2011, we had eighty-two employees consisting of three members of senior management, forty sales and marketing employees, two information technology employees, twenty-nine supply desk employees and eight administrative employees. In addition, we rely on a number of consultants and other advisors. The extent and timing of any increase in staffing will depend on the availability of qualified personnel and other developments in our business. None of the employees are represented by a labor union, and we believe that we have good relationships with our employees.

Company Information

We commenced operations through an entity named Oceanside Energy, Inc., or Oceanside, which was incorporated under the laws of the State of Delaware on September 3, 1996. We incorporated World Energy Solutions, Inc. under the laws of the State of Delaware under the name “World Energy Exchange, Inc.” on June 22, 1999, and on October 31, 1999, Oceanside became a wholly-owned subsidiary of World Energy Solutions, Inc. and was subsequently dissolved. On December 21, 2006, we incorporated a 100% owned subsidiary, World Energy Securities Corp., under the laws of the Commonwealth of Massachusetts.

Our registered and principal office is located at 446 Main Street, Worcester, Massachusetts, 01608, United States of America, and our telephone number is (508) 459-8100. Our website is located at www.worldenergy.com.

You should carefully consider the risks and uncertainties described below before deciding to invest in shares of our common stock. If any of the following risks or uncertainties actually occurs, our business, prospects, financial condition and operating results would likely suffer, possibly materially. In that event, the market price of our common stock could decline and you could lose all or part of your investment.

Risks Related to Our Business

We currently derive a substantial amount of our revenue from the brokerage of electricity, and as a result our business is highly susceptible to factors affecting the electricity market over which we have no control.

We derived approximately 69% of our revenue during 2011 from the brokerage of electricity. Although our reliance on the brokerage of electricity has diminished as we implemented our strategy to expand into other markets, we believe that our revenue will continue to be highly dependent on the level of activity in the electricity market for the near future. Transaction volume in the electricity market is subject to a number of variables, such as consumption levels, pricing trends, availability of supply and other variables. We have no control over these variables, which are affected by geopolitical events such as war, threat of war, terrorism, civil unrest, political instability, environmental or climatic factors and general economic conditions. We are particularly

11

Table of Contents

vulnerable during periods when energy consumers perceive that electricity prices are at elevated levels since transaction volume is typically lower when prices are high relative to regulated utility prices. Accordingly, if electricity transaction volume declines sharply, our results will suffer.

Our business is heavily influenced by how much regulated utility prices for energy are above or below competitive market prices for energy and, accordingly, any changes in regulated prices or cyclicality or volatility in competitive market prices heavily impacts our business.

When energy prices increase in competitive markets above the price levels of the regulated utilities, energy consumers are less likely to lock-in to higher fixed price contracts in the competitive markets and so they are less likely to use our auction platform. Accordingly, reductions in regulated energy prices can negatively impact our business. Any such reductions in regulated energy prices over a large geographic area or over a long period of time would have a material adverse effect on our business, prospects, financial condition and results of operations. Similarly, cyclicality or volatility in competitive market prices that have the effect of driving those prices above the regulated utility prices will make our auction platform less useful to energy consumers and will negatively impact our business.

Our costs will continue to increase as we expand our business and our revenue may not increase proportionately, resulting in operating losses in the future.

We have significantly increased our operating expenses as we expanded our brokerage capabilities to offer additional energy-related products, increased our sales and marketing efforts, developed our administrative organization and made acquisitions. For the year ended December 31, 2011 we had net income of approximately $0.5 million. As we continue to invest in our business, we may incur operating losses. In addition, our budgeted expense levels are based, in significant part, on our expectations as to future revenue and are largely fixed in the short term. As a result, we may be unable to adjust spending in a timely manner to compensate for any unexpected shortfall in revenue which could compound those losses in any given fiscal period.

We continue to expand our business through the acquisition of other businesses and technologies which will present special risks.

We continue to expand our business in certain areas through the acquisition of businesses, technologies, products and services from other businesses. Acquisitions involve a number of special problems, including:

| • | the need to incur additional indebtedness, issue stock or use cash in order to complete the acquisition; |

| • | difficulty integrating acquired technologies, operations and personnel with the existing business; |

| • | diversion of management attention in connection with both negotiating the acquisitions and integrating the assets; |

| • | strain on managerial and operational resources as management tries to oversee larger operations; |

| • | the funding requirements for acquired companies may be significant; |

| • | exposure to unforeseen liabilities of acquired companies; |

| • | increased risk of costly and time-consuming litigation, including stockholder lawsuits; and |

| • | potential issuance of securities in connection with an acquisition with rights that are superior to the rights of our common stockholders, or which may have a dilutive effect on our common stockholders. |

We may not be able to successfully address these problems. Our future operating results will depend to a significant degree on our ability to successfully integrate acquisitions and manage operations while also controlling expenses and cash burn.

A prolonged recession, instability in the financial markets, and insufficient financial sector liquidity, could negatively impact our business.

The consequences of a prolonged recession could include a lower level of economic activity and uncertainty regarding energy prices and the capital and commodity markets. A lower level of economic activity could result in a decline in energy consumption and further weakened commodity markets, which could adversely affect our revenues and future growth. Economic downturns or periods of high energy supply costs typically lead to reductions in energy consumption and increased conservation measures. Instability in the financial markets as a result of a recession or otherwise, as well as insufficient financial sector liquidity, also could affect the cost of capital and our ability to raise capital.

We have limited operating experience and a history of operating losses, which may make it difficult for you to evaluate our business and prospects.

We have a limited operating history upon which you can evaluate our business and prospects. We began assisting in energy transactions in 2001 and introduced our current auction model in April of that same year. Further, while we did generate net income in 2011, we have a history of losses and, at December 31, 2011, we had an accumulated deficit of approximately $21.6 million. You must consider our business, financial history and prospects in light of the risks and difficulties we face as an early stage company with a limited operating history.

12

Table of Contents

Our success depends on the widespread adoption of purchasing electricity from competitive sources.

Our success depends, in large part, on the willingness of CIG energy consumers to embrace competitive sources of supply, and on the ability of our energy suppliers to consistently source electricity at competitive rates. In most regions of North America, energy consumers have either no or relatively little experience purchasing electricity in a competitive environment. Although electricity consumers in deregulated regions have been switching from incumbent utilities to competitive sources, there can be no assurance that the trend will continue. In a majority of states and municipalities, including some areas which are technically “deregulated”, electricity is still provided by the incumbent local utility at subsidized rates or at rates that are too low to stimulate meaningful competition by other providers. In addition, extreme price volatility could delay or impede the widespread adoption of competitive markets. To the extent that competitive markets do not continue to develop rapidly our prospects for growth will be constrained. Also, there can be no assurance that trends in government deregulation of energy will continue or will not be reversed. Increased regulation of energy would significantly damage our business.

The online brokerage of energy and environmental commodities is a relatively new and emerging market and it is uncertain whether our auction model will gain widespread acceptance.

The emergence of competition in the energy and environmental commodities markets is a relatively recent development, and industry participants have not yet achieved consensus on how to most efficiently take advantage of the competitive environment. We believe that as the online energy brokerage industry matures, it is likely to become dominated by a relatively small number of competitors that can offer access to the largest number of competitive suppliers and consumers. Brokerage exchanges with the highest levels of transaction volume will likely be able to offer bidders lower transaction costs and offer listers better prices, which we believe will increasingly create competitive barriers for smaller online brokerage exchanges. For us to capitalize on our position as an early entrant into this line of business, we will need to generate widespread support for our auction platform and continue to rapidly expand the scale of our operations. Other online auction or non-auction strategies may prove to be more attractive to the industry than our auction model. If an alternative brokerage exchange model becomes widely accepted in the electricity industry and/or the environmental commodities brokerage industry we participate in, our business will be adversely affected.

Even if our auction brokerage model achieves widespread acceptance as the preferred means to transact energy and environmental products, we may be unsuccessful in competing against current and future competitors.

We expect that competition for online brokerage of energy and environmental products will intensify in the near future in response to expanding restructured energy markets that permit consumer choice of energy sources and as technological advances create incentives to develop more efficient and less costly energy procurement in regional and global markets. The barriers to entry into the online brokerage marketplace are relatively low, and we expect to face increased competition from traditional off-line energy brokers, other established participants in the energy industry, online services companies that can launch online auction services that are similar to ours and demand response and energy management service providers.

Many of our competitors and potential competitors have longer operating histories, better brand recognition and significantly greater financial resources than we do. The management of some of these competitors may have more experience in implementing their business plan and strategy and they may have pre-existing commercial or other relationships with large listers and/or bidders which would give them a competitive advantage. We expect that as competition in the online marketplace increases, brokerage commissions for the energy and environmental commodities industries will decline, which could have a negative impact on the level of brokerage fees we can charge per transaction and may reduce the relative attractiveness of our exchange services. We expect that our costs relating to marketing and human resources may increase as our competitors undertake marketing campaigns to enhance their brand names and to increase the volume of business conducted through their exchanges. We also expect many of our competitors to expend financial and other resources to improve their network and system infrastructure to compete more aggressively. Our inability to adequately address these and other competitive pressures would have a material adverse effect on our business, prospects, financial condition and results of operations.

If we are unable to rapidly implement some or all of our major strategic initiatives, our ability to improve our competitive position may be negatively impacted.

Our strategy is to improve our competitive position by implementing certain key strategic initiatives in advance of competitors, including the following:

| • | leveraging new products such as demand response and efficiency; |

| • | continue to develop channel partner relationships; |

| • | strengthen and expand long-term relationships with government agencies; |

| • | move “downstream” into the small- and medium-sized customer segment; |

| • | target other energy-related markets; |

| • | target utilities in order to broker energy-related products for them; and |

| • | make strategic acquisitions. |

While we have made significant progress in pursuing these initiatives, we cannot assure you that we will be successful in executing against any of these key strategic initiatives, or that our time to market will be sooner than that of competitors. Some of

13

Table of Contents

these initiatives relate to new services or products for which there are no established markets, or in which we lack experience and expertise. If we are unable to continue to implement some or all of our key strategic initiatives in an effective and timely manner, our ability to improve our competitive position may be negatively impacted, which would have a material adverse effect on our business and prospects.

We depend on the services of our senior executives and other key personnel, the loss of whom could negatively affect our business.

Our future performance will depend substantially on the continued services of our senior management and other key personnel, including our chief information officer, senior vice president of operations and our market directors. If any one or more of these persons leave their positions and we are unable to find suitable replacement personnel in a timely and cost efficient manner, our business may be disrupted and we may not be able to achieve our business objectives, including our ability to manage our growth and successfully implement our strategic initiatives. We do not have long-term employment agreements with any of our senior management or other key personnel and we do not have a non-competition agreement with our current chief executive officer.

We must also continue to seek ways to retain and motivate all of our employees through various means, including through enhanced compensation packages. In addition, we will need to hire more employees as we continue to implement our key strategy of building on our market position and expanding our business. Competition for qualified personnel in the areas in which we compete remains strong and the pool of qualified candidates is limited. Our failure to attract, hire and retain qualified staff on a cost efficient basis would have a material adverse effect on our business, prospects, financial condition, results of operations and ability to successfully implement our growth strategies.

We do not have contracts for fixed volumes with the bidders who use our auction platform and we depend on a small number of key bidders, and the partial or complete loss of one or more of these bidders as a participant on our auction platform could undermine our ability to execute effective auctions.

We do not have contracts for fixed volumes with any of the bidders who use our auction platform. Two of these bidders accounted for 23% and 22% in the aggregate of our revenue for the years ended December 31, 2011 and 2010, respectively. The loss of these or other significant bidders will negatively impact our operations, particularly in the absence of our ability to locate additional national bidders. We do not have agreements with any of these bidders preventing them from directly competing with us or utilizing competing services.

We depend on a small number of key listers for a significant portion of our revenue, many of which are government entities that have no obligation to use our auction platform or continue their relationship with us, and the partial or complete loss of business of one or more of these consumers could negatively affect our business.