Exhibit 99.1

OBSIDIAN ENERGY LTD.

Annual Information Form

for the year ended December 31, 2017

March 6, 2018

TABLE OF CONTENTS

| Page | ||||

| GLOSSARY OF TERMS |

3 | |||

| CONVENTIONS |

4 | |||

| ABBREVIATIONS |

5 | |||

| OIL AND GAS INFORMATION ADVISORIES |

5 | |||

| CONVERSIONS |

6 | |||

| EFFECTIVE DATE OF INFORMATION |

6 | |||

| SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS |

6 | |||

| GENERAL AND ORGANIZATIONAL STRUCTURE |

9 | |||

| DESCRIPTION OF OUR BUSINESS |

10 | |||

| CAPITALIZATION OF OBSIDIAN ENERGY |

16 | |||

| DIRECTORS AND EXECUTIVE OFFICERS OF OBSIDIAN ENERGY |

18 | |||

| AUDIT COMMITTEE DISCLOSURES |

23 | |||

| DIVIDENDS AND DIVIDEND POLICY |

25 | |||

| MARKET FOR SECURITIES |

26 | |||

| INDUSTRY CONDITIONS |

27 | |||

| RISK FACTORS |

37 | |||

| MATERIAL CONTRACTS |

58 | |||

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS |

60 | |||

| TRANSFER AGENTS AND REGISTRARS |

60 | |||

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS |

60 | |||

| INTERESTS OF EXPERTS |

60 | |||

| ADDITIONAL INFORMATION |

61 | |||

| APPENDIX A – RESERVES DATA AND OTHER OIL AND GAS INFORMATION | ||||

| Appendix A-1 – Report of Management and Directors on Reserves Data and Other Information |

||||

| Appendix A-2 – Report on Reserves Data |

||||

| Appendix A-3 – Statement of Reserves Data and Other Oil and Gas Information |

||||

| APPENDIX B – MANDATE OF THE AUDIT COMMITTEE | ||||

2

GLOSSARY OF TERMS

The following is a glossary of certain terms used in this Annual Information Form.

“ABCA” means the Business Corporations Act (Alberta), R.S.A. 2000, C. B-9, as amended, including the regulations promulgated thereunder.

“Annual Information Form” means this annual information form dated March 7, 2018.

“Board” or “Board of Directors” means the board of directors of Obsidian Energy.

“Common Shares” means common shares in the capital of Obsidian Energy.

“Engineering Report” means the report prepared by Sproule dated January 29, 2018 where they evaluated one hundred percent of the crude oil, natural gas and natural gas liquids reserves of Obsidian Energy and the net present value of future net revenue attributable to those reserves effective as at December 31, 2017.

“Form 40-F” means our Annual Report on Form 40-F for the fiscal year ended December 31, 2017 filed with the SEC.

“Gross” or “gross” means:

| (a) | in relation to our interest in production or reserves, our “company gross reserves”, which are our working interest (operating or non-operating) share before deduction of royalties and without including any royalty interests of ours; |

| (b) | in relation to wells, the total number of wells in which we have an interest; and |

| (c) | in relation to properties, the total area of properties in which we have an interest. |

“Handbook” means the Chartered Professional Accountant Canada Handbook, as amended from time to time.

“IFRS” means International Financial Reporting Standards, being the standards and interpretations issued by the International Accounting Standards Board, as amended from time to time. The changeover date to IFRS was January 1, 2011 with retrospective adoption from January 1, 2010 onwards. For periods relating to financial years beginning on or after January 1, 2011, Canadian generally accepted accounting principles applicable to publicly accountable enterprises is determined with reference to Part I of the Handbook, which is IFRS.

“MD&A” means management’s discussion and analysis.

“Net” or “net” means:

| (a) | in relation to our interest in production or reserves, our working interest (operating or non-operating) share after deduction of royalty obligations, plus our royalty interests in production or reserves; |

| (b) | in relation to our interest in wells, the number of wells obtained by aggregating our working interest in each of our gross wells; and |

| (c) | in relation to our interest in a property, the total area in which we have an interest multiplied by the working interest we own. |

“NI 51-101” means National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities.

3

“Non-Resident” means: (i) a person who is not a resident of Canada for the purposes of the Tax Act; or (ii) a partnership that is not a Canadian partnership for the purposes of the Tax Act.

“NYSE” means the New York Stock Exchange.

“Obsidian Energy”, the “Company”, the “Corporation”, “we”, “us” or “our” each mean Obsidian Energy Ltd., a corporation existing under the ABCA. Where the context requires, these terms also include all of Obsidian Energy’s Subsidiaries on a consolidated basis. The Company completed a corporate name change in June 2017 from Penn West Petroleum Ltd. (“Penn West”) pursuant to obtaining the requisite shareholder approval.

“OPEC” means the Organization of the Petroleum Exporting Countries.

“SEC” means the United States Securities and Exchange Commission.

“Senior Notes” means our guaranteed, secured senior notes consisting of US$84 million principal amount of notes, as described under the heading “Capitalization of Obsidian Energy – Debt Capital – Senior Notes”.

“Shareholders” means holders of our Common Shares.

“Sproule” means Sproule Associates Limited, independent petroleum consultants of Calgary, Alberta.

“Subsidiaries” has the meaning ascribed thereto in the Securities Act (Ontario) and, for greater certainty, includes all corporations and partnerships owned, controlled or directed, directly or indirectly, by Obsidian Energy.

“Tax Act” means the Income Tax Act (Canada), R.S.C. 1985, C. 1 (5th Supp.), as amended, including the regulations promulgated thereunder, as amended from time to time.

“TSX” means the Toronto Stock Exchange.

“undeveloped land” and “unproved property” each mean a property or part of a property to which no reserves have been specifically attributed.

“United States” or “U.S.” means the United States of America.

CONVENTIONS

Certain terms used herein are defined in the “Glossary of Terms”. Certain other terms used herein but not defined herein are defined in NI 51-101 and, unless the context otherwise requires, shall have the same meanings herein as in NI 51-101.

All dollar amounts in this document are expressed in Canadian dollars, except where otherwise indicated. References to “$” or “Cdn$” are to Canadian dollars, references to “US$” are to United States dollars, references to “£” are to pounds sterling, and references to “€” are to Euros. On March 6, 2018, the exchange rate based on the noon rate as reported by WM/Reuters, was Cdn$1.00 equals US$0.776.

All financial information herein has been presented in accordance with IFRS.

4

ABBREVIATIONS

|

Oil and Natural Gas Liquids |

Natural Gas | |||||

| bbl | barrel or barrels | GJ | gigajoule | |||

| bbl/d | barrels per day | GJ/d | gigajoules per day | |||

| Mbbl | thousand barrels | Mcf | thousand cubic feet | |||

| MMbbl | million barrels | MMcf | million cubic feet | |||

| NGLs | natural gas liquids | Bcf | billion cubic feet | |||

| MMboe | million barrels of oil equivalent | Mcf/d | thousand cubic feet per day | |||

| Mboe | thousand barrels of oil equivalent | MMcf/d | million cubic feet per day | |||

| boe/d | barrels of oil equivalent per day | m3 MMbtu |

cubic metres million British thermal units | |||

| Other |

||

| AECO | the Alberta benchmark price for natural gas. | |

| BOE or boe | barrel of oil equivalent, using the conversion factor of 6 Mcf of natural gas being equivalent to one barrel of oil. | |

| WTI | West Texas Intermediate, the reference price paid in United States dollars at Cushing, Oklahoma for crude oil of standard grade. | |

| API | American Petroleum Institute. | |

| °API | the measure of the density or gravity of liquid petroleum products derived from a specific gravity. | |

| psi | pounds per square inch. | |

| MM$ | million dollars. | |

| MW | megawatt. | |

| MWh | megawatt hour. | |

| CO2 | carbon dioxide. | |

OIL AND GAS INFORMATION ADVISORIES

Where any disclosure of reserves data is made in this Annual Information Form (including the Appendices hereto) that does not reflect all of the reserves of Obsidian Energy, the reader should note that the estimates of reserves and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves and future net revenue for all properties, due to the effects of aggregation.

All production and reserves quantities included in this Annual Information Form (including the Appendices hereto) have been prepared in accordance with Canadian practices and specifically in accordance with NI 51-101. These practices are different from the practices used to report production and to estimate reserves in reports and other materials filed with the SEC by United States companies. Nevertheless, as part of Obsidian Energy’s Form 40-F for the year ended December 31, 2017, filed with the SEC, Obsidian Energy has disclosed proved reserves quantities using the standards contained in SEC Regulation S-X, and the standardized measure of discounted future net cash flows relating to proved oil and gas reserves determined in accordance with the U.S. Financial Accounting Standards Board, “Disclosures About Oil and Gas Producing Activities”, which disclosure complies with the SEC’s rules for disclosing oil and gas reserves.

References in this Annual Information Form to land and properties held, owned, acquired or disposed by us, or in respect of which we have an interest, refer to land or properties in respect of which we have a lease or other contractual right to explore for, develop, exploit and produce hydrocarbons underlying such land or properties.

5

Boes may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf: 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency conversion ratio of 6:1, utilizing a conversion on a 6:1 basis is misleading as an indication of value.

CONVERSIONS

The following table sets forth certain conversions between Standard Imperial Units and the International System of Units (or metric units).

| To Convert From |

To |

Multiply By | ||||

| Mcf |

cubic metres | 28.174 | ||||

| cubic metres |

cubic feet | 35.494 | ||||

| bbl |

cubic metres | 0.159 | ||||

| cubic metres |

bbl | 6.293 | ||||

| feet |

metres | 0.305 | ||||

| metres |

feet | 3.281 | ||||

| miles |

kilometres | 1.609 | ||||

| kilometres |

miles | 0.621 | ||||

| acres |

hectares | 0.405 | ||||

| hectares |

acres | 2.500 | ||||

| gigajoules (at standard) |

MMbtu | 0.948 | ||||

| MMbtu (at standard) |

gigajoules | 1.055 | ||||

| gigajoules (at standard) |

Mcf | 1.055 | ||||

EFFECTIVE DATE OF INFORMATION

Except where otherwise indicated, the information in this Annual Information Form is presented as at the end of Obsidian Energy’s most recently completed financial year, being December 31, 2017.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

In the interest of providing our securityholders and potential investors with information regarding Obsidian Energy, including management’s assessment of Obsidian Energy’s future plans and operations, certain statements contained and incorporated by reference in this document constitute forward-looking statements or information (collectively “forward-looking statements”). Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “budget”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “objective”, “aim”, “potential”, “target” and similar words suggesting future events or future performance. In addition, statements relating to “reserves” or “resources” are deemed to be forward-looking statements as they involve the implied assessment, based on certain estimates and assumptions, that the reserves and resources described exist in the quantities predicted or estimated and can be profitably produced in the future. In particular, this document and the documents incorporated by reference herein contain, without limitation, forward-looking statements pertaining to the following: the details of our 2018 capital budget and our average production guidance for 2018; the details of our ongoing acquisition, disposition, farm-out and financing strategy; our dividend policy; our expectations regarding the operational and financial impact that climate change regulations in the jurisdictions in which we operate will have on us; that the Corporation is unable to predict what additional legislation or amendment governments may enact in the future and what will need to be reported, remitted and in what time frame; that we are committed to mitigating the environmental impact from our operations, and to involving stakeholders throughout the exploration, development, production and abandonment process; that we will seek to drive improvement and to ensure compliance with our environmental policies; that we seek to communicate our commitment to environmental stewardship to our stakeholders in

6

order to always be held accountable; that we continue to work cooperatively with governments to develop an approach to deal with climate change issues that protects the industry’s competitiveness, limits the cost and administrative burden of compliance, and supports continued investment in the oil and gas sector; our belief that the trend towards heightened and additional standards in environmental legislation and regulation will continue and our expectation that we will be making increased expenditures as a result of the expansion of our operations and the adoption of new legislation relating to the protection of the environment; our commitment to mitigating the environmental impact from our operations and involving stakeholders throughout the exploration, development, production and abandonment process; our assessment of the operational and financial impacts that certain risks factors could have on us and the value of our Common Shares should such risk factors materialize; the quantity of our oil, natural gas liquids and natural gas reserves, the recoverability thereof, and the net present values of future net revenue to be derived from our reserves using forecast prices and costs, including the disclosure set forth in Appendix A-3 under “Statement of Reserves Data and Other Oil and Gas Information – Reserves Data”; the amount of royalties, operating costs, development costs, abandonment and reclamation costs and income taxes that we will incur in connection with the production of our reserves; our outlook for oil, natural gas liquids and natural gas prices; our expectations regarding future currency exchange rates and inflation rates; our expectations regarding funding the development of our reserves; our expectation that interest and other funding costs will not make the development of any of our properties uneconomic; our expectations regarding the timing for developing our proved undeveloped reserves and probable undeveloped reserves and the amount of future capital expenditures required to develop such reserves; our expectations regarding the significant economic factors and other significant uncertainties that could affect our reserves data; the number of net well bores, facilities and the length of pipeline in respect of which we expect to incur abandonment and reclamation costs and the total amount of such costs that we expect to incur and the timing thereof; the details of our exploration and development plans in each of our Cardium, Peace River, Viking and Deep Basin resource plays in 2018 and additional optimization activity in 2018; the expected lands that will be surrendered unless we qualify them in some manner; our expectations regarding when we will be required to pay income taxes; our production volume estimates for 2018; our intention to continue to actively identify and evaluate hedging opportunities in order to reduce our exposure to fluctuations in commodity prices and protect our future cash flows and capital programs; and the nature of, effectiveness of, and benefits to be derived from, our future marketing arrangements and risk management strategies.

With respect to forward-looking statements contained or incorporated by reference in this document, we have made assumptions regarding, among other things: 2018 prices of $55.00 per barrel WTI and $2.25 per Mcf AECO and a 2018 US$/Cdn$ foreign exchange rate of $1.28; that the Company does not dispose of additional material producing properties; the terms and timing of any anticipated asset dispositions or acquisitions; our ability to execute our long-term plan as described herein and in our other disclosure documents and the impact that the successful execution of such plan will have on us and our shareholders; the economic returns anticipated from expenditures on our assets; future crude oil, natural gas liquids and natural gas prices and differentials between light, medium and heavy oil prices and Canadian, WTI and world oil and natural gas prices; future capital expenditure levels and capital programs; future crude oil, natural gas liquids and natural gas production levels; the laws and regulations that we will be required to comply with, including laws and regulations relating to taxation, royalty regimes and environmental protection, and the continuance of those laws and regulations; that we will have the financial resources required to fund our capital and operating expenditures and requirements as needed; drilling results and the recoverability of our reserves; the estimates of our reserves volumes and the assumptions related thereto (including commodity prices and development costs) are accurate in all material respects; the amount of royalties, operating costs, development costs, abandonment and reclamation costs and income taxes that we will incur in connection with the production of our reserves; future exchange rates, inflation rates and interest rates; future debt levels; future income tax rates; the amount of tax pools available to us; the cost of expanding our property holdings; our ability to execute our capital programs as planned without significant adverse impacts from various factors beyond our control, including weather, infrastructure access and delays in obtaining regulatory approvals and third party consents; our ability to obtain equipment in a timely manner to carry out development activities and the costs thereof; our ability to market our oil and natural gas successfully to current and new customers; our ability to reduce our exposure to commodity price fluctuations and counterparty risks through our risk management programs; the impact of increasing competition; our ability to obtain financing on acceptable terms, that our conduct and results of operations will be consistent with expectations; our ability to add production and reserves through our development and exploitation activities;, if necessary; and that we will have the ability to develop our oil and gas properties in the manner currently contemplated. In addition, many of the forward-looking statements contained or incorporated by reference in this document are located proximate to assumptions that are specific to those forward-looking statements, and such

7

assumptions should be taken into account when reading such forward-looking statements: see in particular the assumptions identified in Appendix A-3 under “Statement of Reserves Data and Other Oil and Gas Information – Reserves Data” and “Statement of Reserves Data and Other Oil and Gas Information – Notes to Reserves Data Tables”.

Although Obsidian Energy believes that the expectations reflected in the forward-looking statements contained or incorporated by reference in this document, and the assumptions on which such forward-looking statements are made, are reasonable, there can be no assurance that such expectations will prove to be correct. Readers are cautioned not to place undue reliance on forward-looking statements included or incorporated by reference in this document, as there can be no assurance that the plans, intentions or expectations upon which the forward-looking statements are based will occur. By their nature, forward-looking statements involve numerous assumptions, known and unknown risks and uncertainties that contribute to the possibility that the predictions, forecasts, projections and other forward-looking statements contained herein will not be correct, which may cause our actual performance and financial results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by such forward-looking statements. These risks and uncertainties include, among other things: the possibility that we are unable to execute some or all of our ongoing asset acquisition or disposition programs on favourable terms or at all, whether due to the failure to receive requisite regulatory or other third party approvals or satisfy applicable closing conditions or for other reasons that we cannot anticipate; the possibility that we will not be able to successfully execute our long-term plan in part or in full, and the possibility that some or all of the benefits that we anticipate will accrue to us and our securityholders as a result of the successful execution of such plan do not materialize; the impact of weather conditions on seasonal demand; the impact of weather conditions on our ability to execute capital programs; the risk that we will be unable to execute our capital programs as planned without significant adverse impacts from various factors beyond our control, including weather, infrastructure access and delays in obtaining regulatory approvals and third party consents; risks inherent in oil and natural gas operations; uncertainties associated with estimating reserves and resources; competition for, among other things, capital, acquisitions of reserves, resources, undeveloped lands and skilled personnel; incorrect assessments of the value of acquisitions, including the historical acquisitions discussed herein; geological, technical, drilling and processing problems; general economic and political conditions in Canada, the U.S., Europe and globally, and in particular, the effect that those conditions have on commodity prices and our access to capital; industry conditions, including fluctuations in the price of crude oil, natural gas liquids and natural gas, price differentials for crude oil and natural gas produced in Canada as compared to other markets and transportation restrictions, including pipeline and railway capacity constraints; royalties payable in respect of our oil and natural gas production and changes to government royalty frameworks in jurisdictions in which we operate and the impact that such changes may have on us; changes in government regulation of the oil and natural gas industry, including environmental regulation; fluctuations in foreign exchange or interest rates; unanticipated operating events or environmental events that can reduce production or cause production to be shut-in or delayed, including extreme cold during winter months, wild fires and flooding; failure to obtain regulatory, industry partner and other third-party consents and approvals when required, including for acquisitions, dispositions, joint ventures, partnerships and mergers; failure to realize the anticipated benefits of dispositions, acquisitions, joint ventures and partnerships, including the historical dispositions, acquisitions, joint ventures and partnerships discussed herein; changes in taxation and other laws and regulations that affect us and our securityholders; the potential failure of counterparties to honour their contractual obligations; stock market volatility and market valuations; the ability of OPEC to control production and balance global supply and demand of crude oil at desired price levels; political uncertainty, including the risks of hostilities, in the petroleum producing regions of the world; delays in exploration and development activities if drilling and related equipment is unavailable or if access to drilling locations is restricted; the impact of pipeline interruptions and apportionments and the actions or inactions of third party operators; the possibility that we breach one or more of the financial covenants pursuant to our agreements with the syndicated banks and the holders of our senior, unsecured notes; and the other factors described under “Risk Factors” in this document and in Obsidian Energy’s public filings available in Canada at www.sedar.com and in the United States at www.sec.gov. Readers are cautioned that this list of risk factors should not be construed as exhaustive.

The forward-looking statements contained and incorporated by reference in this document speak only as of the date of this document. Except as expressly required by applicable securities laws, Obsidian Energy does not undertake any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The forward-looking statements contained and incorporated by reference in this document are expressly qualified by this cautionary statement.

8

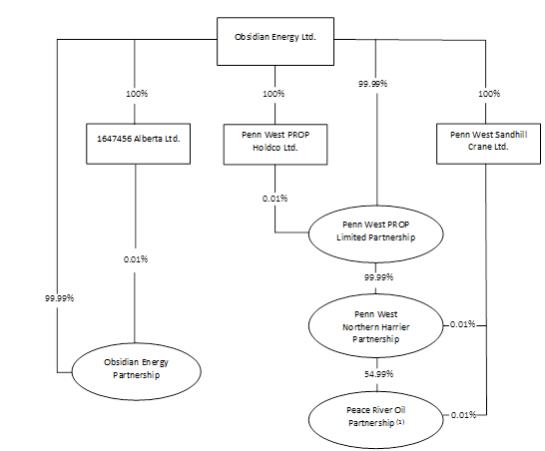

GENERAL AND ORGANIZATIONAL STRUCTURE

General

Obsidian Energy is a corporation amalgamated under the ABCA. Obsidian Energy’s head and registered office is located at Suite 200, 207 – 9th Avenue S.W., Calgary, Alberta, T2P 1K3.

Our Organizational Structure

The following diagram sets forth the organizational structure of Obsidian Energy and its material Subsidiaries as at the date hereof.

Notes:

| (1) | The remaining 45% interest in Peace River Oil Partnership is owned by Winter Spark Resources, Inc., an affiliate of China Investment Corporation. |

| (2) | Each of the entities identified in the diagram was incorporated, continued, formed or organized, as the case may be, under the laws of the Province of Alberta. |

9

DESCRIPTION OF OUR BUSINESS

Overview

Obsidian Energy is an intermediate-sized oil and gas producer with a well-balanced portfolio of high-quality assets based in Western Canada. Obsidian Energy is a company based on discipline, relentless passion for the work we do, and resolute accountability to our shareholders, our partners and the communities in which we operate. As at December 31, 2017, Obsidian Energy had 281 employees.

Reserves Data

See Appendices A-1, A-2 and A-3 for complete NI 51-101 oil and gas reserves disclosure for Obsidian Energy as at December 31, 2017.

General Development of the Business

The following is a description of the general development of Obsidian Energy’s business over the last three completed financial years.

Year Ended December 31, 2015

Board and Management Changes

Messrs. Raymond Crossley and William Friley joined the Board on March 6, 2015 and March 12, 2015, respectively. Effective March 12, 2015, Mr. Crossley was appointed as Chair of the Audit Committee and Mr. Friley was been appointed Chair of the Operations and Reserves Committee. In 2015, James Allard and James Smith retired from the Board.

In June 2015, Keith Luft (General Counsel and Senior Vice President, Corporate Services) retired from his position.

In 2015, as part of our ongoing effort to operate in a more efficient manner, the Company reduced its staffing levels by over 35 percent.

Amendments to Bank Facility and Senior Notes

In May 2015, the Company finalized amending agreements with the lenders under its syndicated bank facility and with the holders of its senior notes to, among other things, amend its financial covenants as follows:

| • | the maximum Senior Debt to EBITDA and Total Debt to EBITDA ratio will be less than or equal to 5:1 for the period January 1, 2015 through and including June 30, 2016, decreasing to less than or equal to 4.5:1 for the quarter ending September 30, 2016 and decreasing to less than or equal to 4:1 for the quarter ending December 31, 2016; |

| • | the Senior Debt to EBITDA ratio will decrease to less than or equal to 3:1 for the period from and after January 1, 2017; and |

| • | the Total Debt to EBITDA ratio will remain at less than or equal to 4:1 for all periods after September 30, 2016. |

The Company also agreed to the following:

| • | to temporarily grant floating charge security over all of its property in favor of the lenders and the noteholders on a pari passu basis, which security will be fully released upon the Company achieving both (i) a Senior Debt to EBITDA ratio of 3:1 or less for four consecutive quarters, and (ii) an investment grade rating on its senior secured debt; |

10

| • | to cancel the $500 million tranche of the Company’s existing $1.7 billion syndicated bank facility that was set to expire on June 30, 2016, the remaining $1.2 billion tranche of the syndicated bank facility remains available to the Company in accordance with the terms of the agreements governing such facility; |

| • | to temporarily reduce its quarterly dividend commencing in the first quarter of 2015 to $0.01 per share or less until the earlier of (i) the Senior Debt to EBITDA being less than 3:1 for two consecutive quarters ending on or after September 30, 2015, and (ii) March 30, 2017; and |

| • | until March 30, 2017, to use net proceeds from any asset dispositions to repay at par $650 million of the outstanding principal amounts owing to noteholders, with corresponding pro rata amounts from such asset dispositions to be used to repay any outstanding amounts drawn under its syndicated bank facility. As at December 31, 2015, Obsidian Energy has accumulated $800 million in net proceeds from asset dispositions that it has put towards its debt prepayments and syndicated bank facility. |

2015 Capital Expenditure Budget and Production and Funds Flow Guidance

In July 2015, the Company reduced its Canadian crude oil pricing assumption for the full year 2015 to $60.00 per barrel. Consequently, the Company updated its funds flow from operations guidance range from $500 - $550 million to $350 - $400 million and the capital budget reduced from $625 million to $575 million.

In September 2015, the Company announced that in response to continued and further significant changes in the commodity price environment, and in order to maintain financial flexibility, the Company’s capital budget had been reduced by approximately $75 million to $500 million, representing capital expenditures of approximately $245 million in the second half of 2015 with the revised 2015 production guideline range to be between 86,000 to 90,000 boe per day.

In November 2015, the Company refined the range of the annual production guidance to 85,000 to 87,000 boe per day. The capital budget for the year remained unchanged at $500 million.

Responding to the Commodity Price Environment

In September 2015, the Company provided an update in response to the commodity price environment which focused on limiting capital expenditures to funds flow from operation by year-end 2015, suspending the dividend, reducing board compensation and significantly reducing the cost structure though a 35 percent workforce reduction. For further details, see the Company’s news release dated September 1, 2015.

Change to Quarterly Dividend Payment and NYSE – Continued Listing Standard Notification

In September 2015, the Company announced a change to its quarterly dividend payment from $0.01 per Common Share to no dividend until further notice, effective after the 2015 third quarter dividend payable on October 15, 2015.

The Company also received notification from the NYSE in September 2015 that it had fallen below the NYSE’s continued listing standard, which requires a minimum average closing price of US$1.00 over a consecutive 30 trading day period. The Company regained compliance at the close of trading on November 30, 2015 since the average closing price of its common stock for the consecutive 30 trading days ended November 30, 2015 and the closing price of its common stock on November 30, 2015 both exceeded US$1.00. For further details, see the Company’s news release dated December 2, 2015.

Aggregate Acquisition and Disposition Activity

The Company completed non-core property dispositions of $800 million in 2015. Total production associated with the combined divestments was approximately 11,500 boe per day with production weighted approximately 20% toward natural gas. Divested assets were located in Alberta, Saskatchewan and Manitoba and represented non-core, base assets in the Company’s asset portfolio which had minimal capital allocated to them in the long-term plan. The net proceeds of the dispositions were used to repay a portion of the indebtedness outstanding under our bank facility and senior notes, as agreed to in the amending agreements.

11

Year Ended December 31, 2016

2016 Capital Expenditure Budget and Production

In January 2016, the Company announced its 2016 capital budget of $50 million. This capital budget was consistent with the strategy announced on September 1, 2015, which limited the total expenditures to funds flow from operations, in response to the weak commodity price environment. The Company’s average production guidance for 2016 was also set at 60,000 to 64,000 boe per day. In August 2016, the Company announced that due to the additional financial flexibility afforded the Company through the debt reduction efforts to date, that it would be resuming development in the Cardium and Alberta Viking in the second half of 2016 and therefore increasing the full year capital budget by approximately $40 million to $90 million, plus $15 million allocated to decommissioning expenditures. The Company’s average production guidance for 2016 was adjusted in November 2016, due to all the disposition activities, to 52,000 to 55,000 boe per day.

NYSE – Continued Listing Standard Notification

In January 2016, the Company received notification from the NYSE that it was no longer in compliance with one of the NYSE’s continued listing standards applicable to us because the average closing price of our Common Shares was less than US$1.00 per share over a consecutive 30-day trading period. Under the NYSE’s rules, the Company had a period of six months from the date of the NYSE notification to regain compliance with the NYSE’s price listing standard and avoid delisting. The Company regained compliance at the close of trading on June 30, 2016 since the average closing price of its common stock for the consecutive 30 trading days ended June 30, 2016 and the closing price of its common stock on June 30, 2016 both exceeded US$1.00. For further details, see the Company’s news release dated July 4, 2016.

Settlement of Class Action Lawsuit

In February 2016, the Company announced that it entered into agreements to settle all class action proceedings in Canada and United States against the Company related to damages alleged to have been incurred due to a decline in share price related to the restatement of certain of the Company’s historical financial statements and related MD&A in 2014. The settlement agreements provide for a payment of $53 million split evenly between Canadian and US investors that will be fully funded by insurance coverage maintained by the Company. As a result, the payment would not impact the Company’s cash or financial position. The settlements received the required court approval in each of Alberta, Ontario and Quebec and in New York, and all conditions to settlement have been satisfied. As a result of the approval of these settlements, there is no further exposure to the Company.

Board of Directors and Management Changes

Ms. Maureen Cormier Jackson joined the Board of Directors on March 8, 2016.

In October 2016, the Company announced that David Roberts (President and Chief Executive Officer) would be retiring from his position effective October 24, 2016 and that David French would succeed him.

In 2016, as part of our ongoing effort to operate in a more efficient manner, the Company reduced its staffing levels by over 40% percent.

12

Long Term Retention and Incentive Plan becomes Restricted Share Unit Plan

In March 2016, the Company announced that the Board had approved amendments to the Restricted Share Unit Plan (formerly the Long Term Retention and Incentive Plan) to allow for the administrators the discretion to make payments on future grants of restricted share units (formerly incentive awards) in either cash or Common Shares.

Termination of DRIP

In March 2016, the Company announced that the Board had decided to terminate the Obsidian Energy’s Dividend Reinvestment and Optional Common Share Purchase Plan, which had been suspended since December 2014, pursuant to the terms and conditions set forth in the plan.

Prepayment of Outstanding Debt

In September 2016, the Company offered $448 million of net proceeds received from dispositions during the year for prepayment of outstanding senior notes. The note holders accepted $437 million which was subsequently prepaid in October 2016. The remaining $11 million was used to repay indebtedness on our syndicated bank facility. This prepayment reduced the outstanding principal on our senior notes to approximately $139 million at that date, lowered the average interest rate on our debt, and reduced the number of noteholders from 36 down to two.

Aggregate Disposition Activity

The Company completed property dispositions of $1.4 billion in 2016 (including the sale of all its Saskatchewan assets for cash consideration of approximately $975 million – see the Company’s news release dated June 24, 2016 for further details). Total production associated with the combined divestments was approximately 30,000 boe per day with production weighted approximately 25% toward natural gas. These divested assets were located in Alberta, Saskatchewan and British Columbia and represented both non-core and core base assets in the Company’s asset portfolio. The net proceeds of the dispositions were used to repay a portion of the indebtedness outstanding under our bank facility and senior notes, as agreed to in the amending agreements.

Year Ended December 31, 2017

2017 Capital Expenditure Budget and Production

In January 2017, the Company announced its 2017 capital budget of $180 million (which includes $160 million in exploration and development capital and $20 million in decommissioning expenditures) and that it anticipated 2017 average production to be between 27,000 to 29,000 boe per day. In March 2017, Obsidian Energy announced it was increasing full year 2017 production guidance to 30,500 to 31,500 boe per day as a result of retaining certain assets in the outer Cardium and central Alberta that it potentially planned to sell. In August 2017, the Company reduced it full-year capital guidance to $160 million (which includes $145 million in exploration and development capital and $15 million in decommissioning expenditures) in response to sustained weak commodity prices. The Company kept its full-year production guidance unchanged at 30,500 to 31,500 boe per day.

Reduction to Senior Secured Debt

In January 2017, the Company announced that it had reduced the capacity available under its revolving syndicated bank facility to $600 million, from $1.2 billion. The reduced facility size was more appropriate for the Company after a meaningful debt reduction program throughout 2016 and a plan to fund future capital and other expenditures through funds flow from operations. This move was expected to save the Company approximately $2.5 million annually in reduced standby fees.

13

Board of Directors and Management Changes

In January 2017, David Dyck (Senior Vice President, Chief Financial Officer) and Gregg Gegunde (Senior Vice President, Exploration, Production & Delivery) retired from their positions and David Hendry was appointed Chief Financial Officer.

In August 2017, the Company’s Chair of the Board of Directors, Mr. Rick George, passed away. Mr. Gordon Ritchie joined the Board of Directors on December 1, 2017.

Aggregate Acquisition and Disposition Activity

In 2017, Obsidian Energy closed property dispositions for total proceeds of $110 million on properties located within British Columbia and the Swan Hills area of Alberta as well as certain royalty interests. Total production associated with the combined divestments was approximately 10,600 boe per day. The net proceeds of the dispositions were used to repay a portion of the indebtedness outstanding under our bank facility.

New Reserve-Based Credit Facility

In May 2017, the Company transitioned to a reserve-based syndicated revolving credit facility with a group of lenders. The credit facility had a borrowing base of $550 million, less the amount of outstanding pari passu senior notes outstanding. The initial revolving period of the credit facility ends on May 17, 2018, with an additional one year term out period, and is subject to a semi-annual borrowing base redetermination in May and November of each year.

Changes approved at the Annual General Meeting

In June 2017, in connection with the shareholder approval obtained at the annual general meeting of the Company, the Company: (i) changed its name to Obsidian Energy Ltd. and replaced its stock symbol with “OBE” on both the Toronto Stock Exchange and New York Stock Exchange; (ii) reduced the Company’s share capital for accounting purposes; and (iii) amended the restricted share unit plan to become the Restricted and Performance Share Unit Plan which allows for, among other things, the option for the Company to make payment on certain awards through the issuance of shares through treasury, purchase of shares on the open market or through payment with cash. The Company also changed the name of the partnership from Penn West Petroleum to Obsidian Energy Partnership at the same time.

SEC Law Suit

In June 2017, the Company announced that the U.S. Securities and Exchange Commission named the Company and three of its former employees in a law suit filed in the U.S. District Court for the Southern District of New York. The SEC’s complaint, based on those historic practices, alleges that Penn West (now Obsidian Energy) violated statutes which include Section 10(b), 13(b), 13(b)(2)(A) and 13(b)(2)(B) of the Securities Exchange Act of 1934 and certain related rules. The complaint requests the entry of injunctive relief preventing a reoccurrence of the practices and certain financial relief. In November 2017, the Company announced it had reached a settlement with the SEC regarding the law suit. Under the terms of the settlement, the Company, without admitting or denying any of the factual allegations in the SEC’s Complaint, agreed to pay a penalty of US$8.5 million. In addition, the Company was enjoined from future violations of certain provisions of U.S. securities legislation. Further details of the settlement and its consequences can be found in the Company’s press release dated November 15, 2017. The law suit would continue against the former Company employees named in the SEC Complaint.

NYSE – Continued Listing Standard Notification

In September 2017, the Company received notification from the NYSE that it was no longer in compliance with one of the NYSE’s continued listing standards applicable to us because the average closing price of our Common Shares was less than US$1.00 per share over a consecutive 30 day trading period. Under the NYSE’s rules, the Company had a period of six months from the date of the NYSE notification to regain compliance with the NYSE’s price listing standard and avoid delisting. The Company regained compliance at the close of trading on October 31, 2017 since the average closing price of its common stock for the consecutive 30 trading days ended October 31, 2017 and the closing price of its common stock on October 31, 2017 both exceeded US$1.00. For further details, see the Company’s news release dated November 1, 2017.

14

2018 Capital Expenditure Budget and Production

In November 2017, the Company announced its 2018 capital budget of $135 million which includes $86 million associated with development and existing wellbore optimization, $25 million of infrastructure and corporate capital, $10 million of decommissioning expenditures, and $14 million of capital associated with meeting the AER Directive 84 requirements for Hydrocarbon Emission Controls and Gas Conservation in the Peace River area. The capital budget would focus on the Company’s core areas of Cardium, PROP, Viking and Deep Basin. The Company’s average production guidance for 2018 was also set at 31,000 to 32,000 boe per day. The Company also announced its increased hedging levels for 2018. For further details, see the Company’s news release dated November 10, 2017.

2018 Developments

Board of Directors Changes

Mr. Edward H. Kernaghan joined the Board on January 3, 2018.

Mr. Jay W. Thornton was appointed as the Chair of the Board of Directors on February 22, 2018, replacing Mr. George Brookman who had been “Acting” Chair of the Board of Directors.

2018 Production Guidance and Disposition Activity

In January 2018, the Company closed an agreement to dispose of a significant portion of its non-core legacy assets located in central Alberta, in exchange for the assumption of abandonment and reclamation liabilities. Total production associated with the disposition is 2,200 boe per day. Additionally, the Company revised its average production guidance for 2018 to 29,000 to 30,000 boe per day.

Ongoing Acquisition, Disposition, Farm-Out and Financing Activities

Potential Acquisitions

Obsidian Energy continues to evaluate potential acquisitions of all types of petroleum and natural gas and other energy-related assets as part of its ongoing asset portfolio management program. At times, Obsidian Energy could be in the process of evaluating several potential acquisitions which individually or in the aggregate could be material. As of the date hereof, Obsidian Energy has not reached agreement on the price or terms of any potential material acquisitions. Obsidian Energy cannot predict whether any current or future opportunities will result in one or more acquisitions for Obsidian Energy.

Potential Dispositions and Farm-Outs

Obsidian Energy continues to evaluate potential dispositions of its petroleum and natural gas assets as part of its ongoing portfolio asset management program.

In addition, Obsidian Energy continues to consider potential farm-out opportunities with other industry participants in respect of its petroleum and natural gas assets in circumstances where Obsidian Energy believes it is prudent to do so based on, among other things, its capital program, development plan timelines and the risk profile of such assets. Obsidian Energy is normally in the process of evaluating several potential dispositions of its assets and farm-out opportunities at any one time, which individually or in the aggregate could be material. As of the date hereof, Obsidian Energy has not reached agreement on the price or terms of any potential material dispositions or farm-outs. Obsidian Energy cannot predict whether any current or future opportunities will result in one or more dispositions or farm-outs for Obsidian Energy.

15

Potential Financings

Obsidian Energy continuously evaluates its capital structure, liquidity and capital resources, and financing opportunities that arise from time to time. Obsidian Energy may in the future complete financings of Common Shares or debt (including debt which may be convertible into Common Shares) for purposes that may include the financing of acquisitions, the financing of Obsidian Energy’s operations and capital expenditures, and the repayment of indebtedness. As of the date hereof, Obsidian Energy has not reached agreement on the pricing or terms of any potential material financing. Obsidian Energy cannot predict whether any current or future financing opportunity will result in one or more material financings being completed.

Significant Acquisitions

Obsidian Energy did not complete an acquisition during its most recently completed financial year that was a significant acquisition for the purposes of Part 8 of National Instrument 51-102.

CAPITALIZATION OF OBSIDIAN ENERGY

Share Capital

The authorized capital of Obsidian Energy consists of an unlimited number of Common Shares without nominal or par value and 90,000,000 preferred shares without nominal or par value. A description of the share capital of Obsidian Energy is set forth below. This description is a summary only. Shareholders are encouraged to read the full text of such share provisions, which are available on SEDAR at www.sedar.com.

Common Shares

Shareholders are entitled to notice of, to attend and to one vote per Common Share held at any meeting of the shareholders of Obsidian Energy (other than meetings of a class or series of shares of Obsidian Energy other than the Common Shares).

Shareholders are entitled to receive dividends as and when declared by the Board of Directors on the Common Shares as a class, subject to prior satisfaction of all preferential rights to dividends attached to shares of other classes of shares of Obsidian Energy ranking in priority to the Common Shares in respect of dividends.

The holders of Common Shares are entitled in the event of any liquidation, dissolution or winding-up of Obsidian Energy, whether voluntary or involuntary, or any other distribution of the assets of Obsidian Energy among its Shareholders for the purpose of winding-up its affairs, and subject to prior satisfaction of all preferential rights to return of capital on dissolution attached to all shares of other classes of shares of Obsidian Energy ranking in priority to the Common Shares in respect of return of capital on dissolution, to share rateably, together with the holders of shares of any other class of shares of Obsidian Energy ranking equally with the Common Shares in respect of return of capital on dissolution, in such assets of Obsidian Energy as are available for distribution.

As at March 6, 2018, 504,340,988 Common Shares were issued and outstanding.

Preferred Shares

Preferred shares of Obsidian Energy may at any time or from time to time be issued in one or more series. Before any shares of a particular series are issued, the Board shall, by resolution, fix the number of shares that will form such series and shall, subject to the limitations set out in Obsidian Energy’s articles, by resolution fix the designation, rights, privileges, restrictions and conditions to be attached to the preferred shares of such series, including, but without in any way limiting or restricting the generality of the foregoing, the rate, amount or method of calculation of dividends thereon, the time and place of payment of dividends, the consideration for and the terms and conditions of any purchase for cancellation, retraction or redemption thereof, conversion or exchange rights (if any), and whether into or for securities of Obsidian Energy or otherwise, voting rights

16

attached thereto (if any), the terms and conditions of any share purchase or retirement plan or sinking fund, and restrictions on the payment of dividends on any shares other than preferred shares or payment in respect of capital on any shares in the capital of Obsidian Energy or creation or issue of debt or equity securities; the whole subject to filing of Articles of Amendment setting forth a description of such series, including the designation, rights, privileges, restrictions and conditions attached to the shares of such series. Notwithstanding the foregoing, other than in the case of a failure to declare or pay dividends specified in any series of preferred shares, the voting rights attached to the preferred shares shall be limited to one vote per preferred share at any meeting where the preferred shares and Common Shares vote together as a single class.

As at the date hereof, no preferred shares are issued and outstanding.

Debt Capital

Obsidian Energy has issued the Senior Notes and has a syndicated credit facility. A description of the debt capital of Obsidian Energy is set forth below. This description is a summary only. Shareholders are encouraged to read the full text of the agreements governing Obsidian Energy’s Senior Notes and credit facility, which are available on SEDAR at www.sedar.com.

Senior Notes

Obsidian Energy has issued the Senior Notes, which consist of US$84 million principal amount of notes. The Senior Notes are guaranteed by Obsidian Energy’s material subsidiaries, are secured and rank equally with our bank credit facilities. The following is a brief summary of certain of the material terms of each series of our Senior Notes.

| Series |

Currency / Principal Amount |

Interest Rate | Issue Date | Maturity Date | ||||||

| Series C |

US$5 million | 5.90 | % | May 31, 2007 | May 31, 2019 | |||||

| Series F |

US$24 million | 6.30 | % | May 29, 2008 | May 29, 2018 | |||||

| Series G |

US$4 million | 6.40 | % | May 29, 2008 | May 29, 2020 | |||||

| Series L |

US$8 million | 9.32 | % | May 5, 2009 | May 5, 2019 | |||||

| Series S |

US$10 million | 5.85 | % | March 16, 2010 | March 16, 2020 | |||||

| Series X |

US$13 million | 4.88 | % | December 2, 2010 and January 4, 2011 |

December 2, 2020 | |||||

| Series Y |

US$6 million | 4.98 | % | December 2, 2010 | December 2, 2022 | |||||

| Series Z |

US$2 million | 5.23 | % | December 2, 2010 and January 4, 2011 |

December 2, 2025 | |||||

| Series DD |

US$0.2 million | 4.23 | % | November 30, 2011 | November 30, 2018 | |||||

| Series EE |

US$12 million | 4.79 | % | November 30, 2011 | November 30, 2021 | |||||

17

Credit Facility

In May 2017, the Company transitioned to a reserve-based syndicated revolving credit facility with a group of lenders. The credit facility has a borrowing base of $550 million, less the amount of outstanding pari passu senior notes and outstanding pound sterling cross currency swap. The initial revolving period of the credit facility ends on May 17, 2018, with an additional one year term out period, and is subject to a semi-annual borrowing base redetermination in May and November of each year.

Additional Information

For additional information regarding our Senior Notes and our credit facility, see “Description of Our Business – General Development of the Business – Year Ended December 31, 2015, Year Ended December 31, 2016, Year Ended December 31, 2017 Developments and 2018 Development” in this Annual Information Form, Note 8 to our audited consolidated financial statements for the year ended December 31, 2017 (collectively, the “Financial Statement Disclosure”), and “Financing” and “Liquidity and Capital Resources” in our related MD&A (collectively, the “MD&A Disclosure”), both of which are available on SEDAR at www.sedar.com. The Financial Statement Disclosure and the MD&A Disclosure are both incorporated by reference into this Annual Information Form.

DIRECTORS AND EXECUTIVE OFFICERS OF OBSIDIAN ENERGY

The following table sets forth, as at March 6, 2018, the name, province and country of residence and positions and offices held for each of the directors and executive officers of Obsidian Energy, together with their principal occupations during the last five years. The directors of Obsidian Energy will hold office until the next annual meeting of Shareholders or until their respective successors have been duly elected or appointed.

18

| Name, Province and Country of Residence |

Positions and Offices Held with Obsidian Energy |

Principal Occupations during the Five Preceding Years | ||

| George H. Brookman(2)(4) Alberta, Canada |

Director since August 3, 2005 | Chief Executive Officer of West Canadian Industries Group Inc. (a digital printing and document management company). | ||

| John Brydson(1)(3) Connecticut, United States |

Director since June 4, 2014 | Private investor since 2012. From 2010 until the end of 2012, Chairman of Hestan Consulting Group, a full-service management consulting firm that he founded. Prior thereto, a Managing Director with Credit Suisse First Boston (now Credit Suisse). | ||

| Raymond Crossley(1)(4) Alberta, Canada |

Director since March 6, 2015 | Partner with PricewaterhouseCoopers LLP from 1996 until his retirement in March 2015, serving as the Managing Partner, Western Canada, from 2011 to 2013. Currently a director of Pure Technologies Ltd. and the Canada West Foundation. | ||

| David L. French Alberta, Canada |

Director, President and Chief Executive Officer since October 24, 2016 | President and Chief Executive Officer of Obsidian Energy since October 2016. Prior thereto, President and Chief Executive Officer of Bankers Petroleum Ltd. from April 2013 to October 2016. Vice-President, Business Development of Apache Corporation, January 2010 to April 2013. | ||

| William A. Friley(2)(3) Alberta, Canada |

Director since March 12, 2015 | President and CEO of Telluride Oil and Gas Ltd. and Skyeland Oils Ltd. On the board of directors of: OSUM Oil Sands Corp. (as the Chairman), Titan Energy Services, and Advanced Flow Technologies. He is also now the Chairman Emeritus to the Alberta Region board of the Nature Conservancy of Canada. | ||

| Maureen Cormier Jackson(1)(2) Alberta, Canada |

Director since March 8, 2016 | Independent businesswoman with over 35 years of executive, financial and operational expertise in the oil and gas industry. From 2012 and until her retirement in 2014, was Senior Vice President, Chief Process and Information Officer at Suncor Energy Inc. (“Suncor”). Her career spanned numerous roles at Suncor which provided experience in the areas of accounting and financial controls, environment, health and safety, and project management. Is also a director of Enerflex Ltd., the Founding Chair of the Wood Buffalo Community Foundation and serves on the Dean’s Advisory Board of Dean of Medicine at the University of Calgary. She was previously a director of a privately-owned family business for more than 15 years and has been involved in several non-profit organizations in various capacities during her career. Is a Chartered Professional Accountant and holds a Bachelor of Commerce from Memorial University. She also holds an ICD.D designation from the Institute of Corporate Directors. | ||

19

| Name, Province and Country of Residence |

Positions and Offices Held with Obsidian Energy |

Principal Occupations during the Five Preceding Years | ||

| Edward H. Kernaghan(3)(4) Ontario, Canada |

Director since January 3, 2018 | Mr. Kernaghan holds a Master of Science Degree from the University of Toronto. He is Senior Investment Advisor of Kernaghan & Partners Ltd., a brokerage firm. Mr. Kernaghan is also President of Principia Research Inc., a research and investment company, and of Kernwood Ltd., an investment holding company. | ||

| Gordon Ritchie(1)(2) Alberta, Canada |

Director since December 1, 2017 | Retired as Vice Chairman of RBC Capital Markets April 1, 2016 after 37 years with RBC. Previously, Mr. Ritchie served as Managing Director and Head of RBC’s Global E&P Energy Group, from 2000 to 2005; spent six years in New York where he served as President and Chief Executive Officer of RBC’s U.S. Broker/Dealer, RBC Dominion Securities Corporation, from 1993 to 1999; served as Managing Director of RBC’s International Corporate Finance Group based in London, England, from 1989 to 1993; and worked as Investment Banker and Energy Research Analyst in Calgary, from 1979 through 1988. | ||

| Jay W. Thornton(3)(4) Alberta, Canada |

Chairman of the Board and Director since June 26, 2013 | Mr. Thornton has over 27 years of oil and gas experience. Mr. Thornton held various operating and corporate executive positions with Shell Canada and Suncor Energy Inc. He is currently a director of North American Energy Partners Inc. and Tervita corporation, and previously a director with the Canadian Association of Petroleum Producers (CAPP). He is a graduate of McMaster university with an Honours degree in Economics. He is also completed the Institute of Corporate Directors (ICD) Education Program. | ||

| David Hendry Alberta, Canada |

Chief Financial Officer | Chief Financial Officer of Obsidian Energy since January 2017. Prior thereto, Vice President Finance at Obsidian Energy from May 2015 until December 2016. Prior thereto, Vice President Finance at Talisman Energy Inc. from May 2006 to April 2015. | ||

Notes:

| (1) | Member of the Audit Committee. |

| (2) | Member of the Human Resources and Compensation Committee. |

| (3) | Member of the Operations and Reserves Committee. |

| (4) | Member of the Governance Committee. |

20

As at the date hereof, the directors and executive officers of Obsidian Energy, as a group, beneficially owned, or controlled or directed, directly or indirectly, approximately 3.7 million Common Shares, or less than one percent of the issued and outstanding Common Shares.

Cease Trade Orders, Bankruptcies, Penalties or Sanctions

To the knowledge of Obsidian Energy, except as otherwise set forth herein, no director or executive officer of Obsidian Energy (nor any personal holding company of any of such persons) is, as of the date of this Annual Information Form, or was within ten years before the date of this Annual Information Form, a director, Chief Executive Officer or Chief Financial Officer of any company (including Obsidian Energy), that:

| (a) | was subject to a cease trade order (including a management cease trade order), an order similar to a cease trade order or an order that denied the relevant company access to any exemption under securities legislation, in each case that was in effect for a period of more than 30 consecutive days (collectively, an “Order”) that was issued while the director or executive officer was acting in the capacity as director, Chief Executive Officer or Chief Financial Officer; or |

| (b) | was subject to an Order that was issued after the director or executive officer ceased to be a director, Chief Executive Officer or Chief Financial Officer and which resulted from an event that occurred while that person was acting in the capacity as director, Chief Executive Officer or Chief Financial Officer. |

On July 29, 2014, Penn West announced that the Audit Committee of the Board was conducting a voluntary, internal review of certain of the Company’s accounting practices and that certain of the Company’s historical financial statements and related MD&A must be restated, which might result in the release of its second quarter 2014 financial results being delayed (which ultimately proved to be the case). Furthermore, the Company advised that its historical financial statements and related audit reports and MD&A should not be relied on. As a result, the Alberta Securities Commission issued a Management Cease Trade Order on August 5, 2014 (the “ASC MCTO”) against Messrs. Brookman, Brydson, and Thornton. On September 18, 2014, Penn West filed restated audited annual financial statements for the years ended December 31, 2013 and 2012, restated unaudited interim financial statements for the three months ended March 31, 2014 and 2013, restated MD&A for the year ended December 31, 2013 and the quarter ended March 31, 2014, and related amended documents. Penn West also filed its unaudited interim financial statements for the three and six month periods ended June 30, 2014 and 2013 and the related MD&A and management certifications. The ASC MCTO was revoked on September 23, 2014.

To the knowledge of Obsidian Energy, no director or executive officer of Obsidian Energy or shareholder holding a sufficient number of securities of Obsidian Energy to affect materially the control of Obsidian Energy (nor any personal holding company of any of such persons):

| (a) | is, as of the date of this Annual Information Form, or has been within the ten years before the date of this Annual Information Form, a director or executive officer of any company (including Obsidian Energy) that, while that person was acting in that capacity, or within a year of that person ceasing to act in that capacity, became bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency or was subject to or instituted any proceedings, arrangement or compromise with creditors or had a receiver, receiver manager or trustee appointed to hold its assets; or |

| (b) | has, within the ten years before the date of this Annual Information Form, become bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency, or become subject to or instituted any proceedings, arrangement or compromise with creditors, or had a receiver, receiver manager or trustee appointed to hold the assets of the director, executive officer or shareholder. |

To the knowledge of Obsidian Energy, no director or executive officer of Obsidian Energy or shareholder holding a sufficient number of securities of Obsidian Energy to affect materially the control of Obsidian Energy (nor any personal holding company of any of such persons), has been subject to:

| (a) | any penalties or sanctions imposed by a court relating to securities legislation or by a securities regulatory authority or has entered into a settlement agreement with a securities regulatory authority; or |

21

| (b) | any other penalties or sanctions imposed by a court or regulatory body that would likely be considered important to a reasonable investor in making an investment decision; |

provided that for the purposes of the foregoing, a late filing fee, such as a filing fee that applies to the late filing of an insider report, is not considered to be a “penalty or sanction”.

Conflicts of Interest

The Board of Directors approved an amendment to the Code of Business Conduct and Ethics (the “Code”) in July of 2015 which made the Code the applicable policy in regard to conflicts of interest (whereas previously there was also the Code of Ethics for Directors, Officers and Senior Financial Management). In general, the private investment activities of employees, directors and officers are not prohibited; however, should an existing investment pose a potential conflict of interest, the potential conflict is required by the Code to be disclosed to an officer or a member of Obsidian Energy’s legal department or to the Board of Directors. Any other activities posing a potential conflict of interest are also required by the Code to be disclosed to an officer or to a member of Obsidian Energy’s legal department. Any such potential conflicts of interests will be dealt with openly with full disclosure of the nature and extent of the potential conflicts of interests with Obsidian Energy. It is acknowledged in the Code that the directors may be directors or officers of other entities engaged in the oil and gas business, and that such entities may compete directly or indirectly with Obsidian Energy. Passive investments in public or private entities of less than one per cent of the outstanding shares will not be viewed as “competing” with Obsidian Energy. No executive officer or employee of Obsidian Energy should be a director, employee, contractor, consultant or officer of any entity that is or may be in competition with Obsidian Energy unless expressly authorized by an executive officer or the Board of Directors. Any director of Obsidian Energy who is a director or officer of, or who is otherwise actively engaged in the management of, or who owns an investment of one per cent or more of the outstanding shares, in public or private entities shall disclose such holding to the Board of Directors. In the event that any circumstance should arise as a result of such positions or investments being held or otherwise which in the opinion of the Board of Directors constitutes a conflict of interest which reasonably affects such person’s ability to act with a view to the best interests of Obsidian Energy, the Board of Directors will take such actions as are reasonably required to resolve such matters with a view to the best interests of Obsidian Energy. Such actions, without limitation, may include excluding such directors, officers or employees from certain information or activities of Obsidian Energy.

The ABCA provides that in the event that an officer or director is a party to, or is a director or an officer of, or has a material interest in any person who is a party to, a material contract or material transaction or proposed material contract or proposed material transaction, such officer or director shall disclose the nature and extent of his or her interest and shall refrain from voting to approve such contract or transaction.

As of the date hereof, Obsidian Energy is not aware of any existing or potential material conflicts of interest between Obsidian Energy or a Subsidiary of Obsidian Energy and any director or officer of Obsidian Energy or of any Subsidiary of Obsidian Energy.

Promoters

No person or company has been, within the two most recently completed financial years or during the current financial year, a “promoter” (as defined in the Securities Act (Ontario)) of Obsidian Energy or of a Subsidiary of Obsidian Energy.

22

AUDIT COMMITTEE DISCLOSURES

National Instrument 52-110 Audit Committees (“NI 52-110”) relating to audit committees has mandated certain disclosures for inclusion in this Annual Information Form. The text of the Audit Committee’s mandate is attached as Appendix B to this Annual Information Form.

Composition of the Audit Committee and Relevant Education and Experience

As of the date hereof, the members of the Audit Committee are Raymond Crossley (Chairman), John Brydson, Maureen Cormier Jackson and Gordon Ritchie, each of whom is independent and financially literate within the meaning of NI 52-110. The following comprises a brief summary of each member’s education and experience that is relevant to the performance of his or her responsibilities as an Audit Committee member.

John Brydson

Mr. Brydson has over 30 years of experience in the financial sector and has occupied senior roles in both major investment and commercial banks. Since 2012, Mr. Brydson has been a private investor. From 2010 until the end of 2012, he was Chairman of a small full-service management consulting firm, Hestan Consulting Group (“HCG”), which he founded. Prior to HCG, Mr. Brydson was a Managing Director with Credit Suisse First Boston, now Credit Suisse (“CS”), from 1995 until 2009, where he was in charge of the Multi-Product Event Trading group. He was also a Managing Director with Lehman Brothers in a similar function from 1983 until he joined CS. The early years of his career were spent as an equity analyst before joining Chase Manhattan Bank (“Chase”) in London in 1977. He transferred to the head office in New York in 1980 where he became a Vice President in the Project Finance Group, specializing in international projects in the energy, mining and metals sectors. He left Chase to join Lehman Brothers in 1983. Mr. Brydson holds an Honors Degree in Economics from Heriot-Watt University in Edinburgh, Scotland. Mr. Brydson served over 10 years as the President and a Board Member of The American Friends of Heriot-Watt University, a charitable organization, and remains on its Board.

Maureen Cormier Jackson

Ms. Cormier Jackson is an independent businesswoman with over 35 years of executive, financial and operational expertise in the oil and gas industry. From 2012 and until her retirement in 2014, Ms. Cormier Jackson was Senior Vice President, Chief Process and Information Officer at Suncor Energy Inc. (“Suncor”). Her career spanned numerous roles at Suncor which provided experience in the areas of accounting and financial controls, environment, health and safety, and project management. Ms. Cormier Jackson is also a director of Enerflex Ltd., the Founding Chair of the Wood Buffalo Community Foundation and serves on the Dean’s Advisory Board of Dean of Medicine at the University of Calgary. She was previously a director of a privately-owned family business for more than 15 years and has been involved in several non-profit organizations in various capacities during her career. Ms. Cormier Jackson is a Chartered Professional Accountant and holds a Bachelor of Commerce from Memorial University. She also holds an ICD.D designation from the Institute of Corporate Directors.

Raymond Crossley (Chairman)

Mr. Crossley is a corporate director. He serves as chair of the audit committee of Pure Technologies Ltd. Mr. Crossley has served as a member of the Financial Review Committee of the Alberta Securities Commission (“ASC”) and has been a member of the Financial Advisory Committee of the ASC. Mr. Crossley retired in 2015 from the accounting firm of PricewaterhouseCoopers (“PwC”) after serving for more than 33 years. He joined the firm in 1981 and had been a partner since 1996, working with a number of large publicly traded corporations operating in the natural resource and utilities sectors. Mr. Crossley served as an elected member of the Partnership Board (PwC’s governing body), from 2001-2005. From 2005-2011, Mr. Crossley was the Managing Partner of PwC’s Calgary office. From 2011-2013 Mr. Crossley acted as Managing Partner, Western Canada. Mr. Crossley is a member of the Chartered Professional Accountants of Alberta. He graduated from the University of Western Ontario with a degree in Economics and Political Science.

23

Gordon Ritchie

Mr. Ritchie retired in 2016, following a career spanning over 37 years with RBC Capital Markets LLC. From 2005 through 2016, Mr. Ritchie served as Vice Chairman, with primary responsibility for many of RBC’s top energy clients. During this period, Mr. Ritchie led teams completing many of the largest energy M&A and financing transactions in Canada, aggregating in excess of $200 billion. From 2000 through 2005, served as Managing Director and Head of the Global E&P Energy Group. Before that, Mr. Ritchie spent six years in New York where he served as President and Chief Executive Officer of RBC’s U.S. Broker/Dealer Operations (1993 to 1999); was Managing Director of RBC’s International Corporate Finance Group based in London, England (1989 to 1993); was Vice President, Corporate Finance in Calgary (1984 to 1988); and Energy Research Analyst (1979 to 1983). Throughout his career, Mr. Ritchie gained extensive experience in research and investment banking in Europe, the United States and Canada. Mr. Ritchie holds an MBA from the University of Western Ontario and a Bachelor of Arts (Economics) from the University of Alberta.

Pre-Approval Policies and Procedures for Audit and Non-Audit Services

The terms of the engagement of Obsidian Energy’s external auditors to provide audit services, including the budgeted fees for such audit services and the representations and disclaimer relating thereto, must be pre-approved by the entire Audit Committee.

With respect to any engagements of Obsidian Energy’s external auditors for non-audit services, Obsidian Energy must obtain the approval of the Audit Committee or the Chairman of the Audit Committee prior to retaining the external auditors to complete such engagement. If such pre-approval is provided by the Chairman of the Audit Committee, the Chairman must report to the Audit Committee on any non-audit service engagement pre-approved by him at the Audit Committee’s first scheduled meeting following such pre-approval. The fees for such non-audit services shall not exceed $50,000, either individually or in the aggregate, for a particular financial year without the approval of the Audit Committee.

If, after using its reasonable best efforts, Obsidian Energy is unable to contact the Chairman of the Audit Committee on a timely basis to obtain the pre-approval contemplated by the preceding paragraph, Obsidian Energy may obtain the required pre-approval from any other member of the Audit Committee, provided that any such Audit Committee member shall report to the Audit Committee on any non-audit service engagement pre-approved by him or her at the Audit Committee’s first scheduled meeting following such pre-approval and the fees for such services do not exceed $50,000 as noted above.

External Auditor Service Fees

The following table summarizes the fees billed to Obsidian Energy and Ernst & Young for external audit and other services during the periods indicated.

| Year |

Audit Fees(1) ($) |

Audit-Related Fees(2) ($) |

Tax Fees(3) ($) |

|||||||||

| 2017 |

811,000 | 39,000 | 16,000 | |||||||||

| 2016 |

992,000 | 75,750 | 5,800 | |||||||||

Notes:

| (1) | The aggregate fees billed by our external auditor in each of the last two fiscal years for audit services, including fees for the integrated audit of Obsidian Energy’s annual financial statements or services that are normally provided in connection with statutory and regulatory filings or engagements, reviews in connection with acquisitions and Sarbanes-Oxley Act related services, and review procedures on the unaudited interim consolidated financial statements. |