UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

|

|

¨

|

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

|

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2010

|

OR

|

|

o

|

TRANSITIONAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

o

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Date of event requiring this shell company report __________

For the transition period from __________ to __________

Commission file number: 333-126007

EFUTURE INFORMATION TECHNOLOGY INC.

(Exact name of Registrant as specified in its charter)

Cayman Islands

(Jurisdiction of incorporation or organization)

|

eFuture Information Technology Inc.

8F Topnew Tower

15 Guanghua Road

Chaoyang District

Beijing 100026, People’s Republic of China

86-10-51650988

(Address of principal executive offices)

|

|

Troe Wen, Secretary of the Board

Telephone: +(86 10) 5165-0988

Email: wenj@e-future.com.cn

Facsimile: +(86 10) 5293-7688

8F Topnew Tower, 15 Guanghua Road

Chaoyang District

Beijing, 100026, People’s Republic of China

|

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Ordinary shares, par value $0.0756 per share

|

|

NASDAQ Capital Market

|

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

As of December 31, 2010, there were 3,599,536 ordinary shares of the Registrant outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act). (Check one):

|

Large accelerated filer ¨

|

|

Accelerated filer ¨

|

|

Non-accelerated filer x

|

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

US GAAP x

|

|

International Financial Reporting Standards as issued by the International Accounting Standards Board ¨

|

|

Other ¨

|

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

TABLE OF CONTENTS

|

Item 1.

|

Identity of Directors, Senior Management and Advisers

|

1

|

|

|

Item 2.

|

Offer Statistics and Expected Timetable

|

1

|

|

|

Item 3.

|

Key Information

|

1

|

|

|

Item 4.

|

Information on the Company

|

13

|

|

|

Item 4A.

|

Unresolved Staff Comments

|

24

|

|

|

Item 5.

|

Operating and Financial Review and Prospects

|

24

|

|

|

Item 6.

|

Directors, Senior Management and Employees

|

40

|

|

|

Item 7.

|

Major Shareholder and Related Party Transactions

|

47

|

|

|

Item 8.

|

Financial Information

|

48

|

|

|

Item 9.

|

The Offer and Listing

|

48

|

|

|

Item 10.

|

Additional Information

|

49

|

|

|

Item 11.

|

Quantitative and Qualitative Disclosures about Market Risk

|

56

|

|

|

Item 12.

|

Description of Securities Other than Equity Securities

|

57

|

|

|

Item 13.

|

Defaults, Dividend Arrearages and Delinquencies

|

58

|

|

|

Item 14.

|

Material Modifications to the Rights of Securities Holders and Use of Proceeds

|

58

|

|

|

Item 15.

|

Controls and Procedures

|

58

|

|

|

Item 16.

|

[Reserved]

|

59

|

|

|

Item 16A.

|

Audit Committee Financial Expert

|

59

|

|

|

Item 16B.

|

Code of Ethics

|

60

|

|

|

Item 16C.

|

Principal Accountant Fees and Services

|

60

|

|

|

Item 16D.

|

Exemptions from the Listing Standards for Audit Committees

|

60

|

|

|

Item 16E.

|

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

|

60

|

|

|

Item 16F.

|

Change in Registrant’s Certifying Accountant

|

61

|

|

|

Item 16G.

|

Corporate Governance

|

61

|

|

|

Item 17.

|

Financial Statements

|

62

|

|

|

Item 18.

|

Financial Statements

|

62

|

|

|

Item 19.

|

Exhibits

|

62

|

In this Annual Report on Form 20-F, references to “dollars” and “$” are to United States dollars, references to “RMB”, “renminbi” or “yuan” are to the Chinese Yuan, and, unless the context otherwise requires, references to “eFuture,” “we,” “us” and “our” refer to eFuture Information Technology Inc., its consolidated subsidiaries and effectively controlled variable interest entities as defined in Part I of this Annual Report.

i

SPECIAL CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

Certain matters discussed in this report may constitute forward-looking statements for purposes of the Securities Act of 1933, as amended (the “Securities Act”), and the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from the future results, performance or achievements expressed or implied by such forward-looking statements. The words “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate,” and similar expressions are intended to identify such forward-looking statements. Our actual results may differ materially from the results anticipated in these forward-looking statements due to a variety of factors, including, without limitation, those discussed under “Item 3 - Key Information-Risk Factors,” “Item 4 - Information on the Company,” “Item 5 - Operating and Financial Review and Prospects,” and elsewhere in this report, as well as factors which may be identified from time to time in our other filings with the Securities and Exchange Commission (the “SEC”) or in the documents where such forward-looking statements appear. All written or oral forward-looking statements attributable to us are expressly qualified in their entirety by these cautionary statements.

The forward-looking statements contained in this report reflect our views and assumptions only as of the date this report is signed. Except as required by law, we assume no responsibility for updating any forward-looking statements.

ii

PART I

Unless the context requires otherwise, references in this report to “eFuture,” “the Company,” “we,” “us,” and “our” refer to eFuture Information Technology Inc., our wholly-owned subsidiary, eFuture (Beijing) Royalstone Information Technology Inc. (“eFuture Royalstone” or “eFuture Beijing”), and the effectively controlled two variable interest entities (“VIEs”), Beijing Wangku Hutong Information Technology Co., Ltd. (“Wangku”), acquired on May 14, 2008 and disposed on March 13, 2011, and Beijing Fuji Biaoshang Information Technology Co., Ltd. (“Biaoshang” or “bFuture”), acquired on October 24, 2007 and disposed on July 16, 2010.

|

Item 1.

|

Identity of Directors, Senior Management and Advisers

|

Not applicable.

|

Item 2.

|

Offer Statistics and Expected Timetable

|

Not applicable.

|

Item 3.

|

Key Information

|

|

A.

|

Selected Consolidated Financial Data

|

The following table presents the selected consolidated financial information for our company, which excludes the operating results for each years and balances as of each years ended of Biaoshang and Wangku because they are classified as discontinued operations. The selected consolidated statements of income data for the three years ended December 31, 2008, 2009 and 2010 and the consolidated balance sheet data as of December 31, 2009 and 2010 have been derived from our audited consolidated financial statements set forth in “Item 18 – Financial Statements”. The selected consolidated balance sheet data for the year ended December 31, 2008 have been derived from our audited consolidated balance sheet as of December 31, 2008, which is not included in this annual report. The selected consolidated statements of income data for the years ended December 31, 2006 and 2007 and the selected consolidated balance sheet data as of December 31, 2006 and 2007 have been derived from our audited consolidated financial statements for the years ended December 31, 2006 and 2007, which are not included in this annual report. Our historical results do not necessarily indicate results expected for any future periods. The selected consolidated financial data should be read in conjunction with, and are qualified in their entirety by reference to, our audited consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” below. Our audited consolidated financial statements are prepared and presented in accordance with Generally Accepted Accounting Principles in the United States of America, or U.S. GAAP .

|

RMB

|

USD

|

|||||||||||||||||||||||

|

For the Year

|

||||||||||||||||||||||||

|

For the Year Ended December 31,

|

Ended

|

|||||||||||||||||||||||

|

December 31,

|

||||||||||||||||||||||||

|

2006

|

2007

|

2008

|

2009

|

2010

|

2010

|

|||||||||||||||||||

|

Total Revenues

|

¥ | 47,843,530 | ¥ | 84,920,993 | ¥ | 129,546,655 | ¥ | 108,835,887 | ¥ | 151,902,684 | $ | 23,015,558 | ||||||||||||

|

Income (Loss) From Operations

|

7,976,967 | 5,914,486 | (6,882,703 | ) | (24,432,621 | ) | (21,732,821 | ) | (3,292,851 | ) | ||||||||||||||

|

Income (Loss) From Operations Per Ordinary Share

|

4.72 | 2.20 | (2.14 | ) | (7.27 | ) | (5.69 | ) | (0.85 | ) | ||||||||||||||

|

Net Income (Loss)

|

8,104,726 | (21,526,314 | ) | (4,478,112 | ) | (25,265,497 | ) | (17,323,421 | ) | (2,624,761 | ) | |||||||||||||

|

Basic Earnings (Loss) Per Share

|

4.80 | (8.01 | ) | (1.39 | ) | (7.51 | ) | (4.53 | ) | (0.69 | ) | |||||||||||||

|

Diluted Earnings (Loss) Per Share

|

4.43 | (8.01 | ) | (1.39 | ) | (7.51 | ) | (4.53 | ) | (0.69 | ) | |||||||||||||

1

|

RMB

|

USD

|

|||||||||||||||||||||||

|

As of December 31,

|

As of December 31,

|

|||||||||||||||||||||||

|

2006

|

2007

|

2008

|

2009

|

2010

|

2010

|

|||||||||||||||||||

|

Total Assets

|

¥ | 83,025,047 | ¥ | 208,884,779 | ¥ | 242,362,093 | ¥ | 231,747,618 | ¥ | 241,832,155 | $ | 36,641,235 | ||||||||||||

|

Total Current Liabilities

|

(18,476,058 | ) | (55,822,620 | ) | (96,806,490 | ) | (109,412,183 | ) | (102,375,657 | ) | (15,511,463 | ) | ||||||||||||

|

Long-term Liabilities

|

- | (49,849,390 | ) | (10,595,717 | ) | (7,970,483 | ) | (3,134,677 | ) | (474,951 | ) | |||||||||||||

|

Net Assets

|

64,548,989 | 103,212,769 | 134,959,886 | 114,364,952 | 136,321,821 | 20,654,821 | ||||||||||||||||||

|

Ordinary Shares

|

1,647,781 | 1,811,589 | 2,039,196 | 2,042,384 | 2,161,766 | 327,540 | ||||||||||||||||||

|

Number of Weighted-average Ordinary Shares

|

1,689,434 | 2,687,380 | 3,214,466 | 3,362,986 | 3,822,386 | 3,822,386 | ||||||||||||||||||

Exchange Rate Information

Our business is primarily conducted in China and all of our revenues are denominated in RMB. However, periodic reports made to shareholders will include current period amounts translated into U.S. dollars using the then current exchange rates, for the convenience of the readers. The conversion of RMB into U.S. dollars in this annual financial report is based on the noon buying rate in The City of New York for cable transfers of RMB as certified for customs purposes by the Federal Reserve Bank of New York. Unless otherwise noted, all translations from RMB to U.S. dollars and from U.S. dollars to RMB in this annual financial report were made at a rate of RMB6.6000 to US$1.00, the noon buying rate in effect as of December 31, 2010. We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, or at all. The government of the People’s Republic of China (the “PRC”) imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. The Company does not currently engage in currency hedging transactions. The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated.

|

Noon Buying Rate

|

||||||||||||||||

|

Period

|

Period-End

|

Average (1)

|

Low

|

High

|

||||||||||||

|

(RMB per U.S. dollar)

|

||||||||||||||||

|

2006

|

7.8041 | 7.9579 | 8.0702 | 7.8041 | ||||||||||||

|

2007

|

7.2946 | 7.6072 | 7.2946 | 7.8127 | ||||||||||||

|

2008

|

6.8225 | 6.9477 | 6.7800 | 7.2946 | ||||||||||||

|

2009

|

6.8259 | 6.8275 | 6.8244 | 6.8299 | ||||||||||||

|

2010

|

6.6000 | 6.7696 | 6.6000 | 6.8330 | ||||||||||||

|

December

|

6.6000 | 6.6497 | 6.6745 | 6.6000 | ||||||||||||

|

2011

|

||||||||||||||||

|

January

|

6.6017 | 6.5964 | 6.5809 | 6.6364 | ||||||||||||

|

February

|

6.5713 | 6.5761 | 6.5520 | 6.5965 | ||||||||||||

|

March

|

6.5483 | 6.5645 | 6.5483 | 6.5743 | ||||||||||||

|

April

|

6.4900 | 6.5267 | 6.4900 | 6.5477 | ||||||||||||

|

May

|

6.4786 | 6.4957 | 6.4786 | 6.5073 | ||||||||||||

|

June (through June 17, 2011)

|

6.4700 | 6.4785 | 6.4700 | 6.4830 | ||||||||||||

Source: Federal Reserve Statistical Release

|

(1)

|

Annual averages are calculated using the average of month-end rates of the relevant years. Monthly averages are calculated using the average of the daily rates during the relevant periods.

|

|

B.

|

Capitalization and Indebtedness

|

Not applicable.

2

|

C.

|

Reasons for the Offer and Use of Proceeds

|

Not applicable.

|

D.

|

Risk Factors

|

You should carefully consider all of the information in this Annual Report and, in particular, the risks outlined below. Any of the following risks could have a material adverse effect on our business, financial condition and results of operations.

Our management has determined that we have material weaknesses in our internal controls over financial reporting.

In connection with the preparation of our annual report on internal control over financial reporting, our management noted that our company has material weaknesses in our internal controls over financial reporting. Specifically, our management noted material weaknesses in our policies regarding (i) controls over the financial reporting processes, (ii) monthly and year end closing processes. See “Item 15. Controls and Procedures – Management’s Annual Report on Internal Control over Financial Reporting.”

We have taken steps to improve the controls in this area, such as hiring experienced personnel and training our accounting and administrative staff to ensure that they closely monitor the preparation of financial statements in accordance with the requirements of US GAAP and the disclosure of annual, current and other periodic reports pursuant to SEC and NASDAQ rules. We have also formalized and documented a set of internal audit processes to ensure that we maintain appropriate controls over financial reporting procedures. Despite these steps, we may experience reportable conditions and significant deficiencies in the future, which, if not remediated, may render us unable to detect in a timely manner misstatements that could occur in our financial statements in amounts that may be material.

Our company’s share price may be adversely affected by negative investor perceptions of small Chinese companies.

In the last year, many smaller U.S.-listed companies that operate primarily in China have seen the public value of their securities decrease significantly. One factor in such decreases has been the widespread allegation of fraud and unreliable financial reporting. Another factor has been a number of negative research reports published about Chinese companies, sometimes by parties that sell the securities short prior to publishing the research report in order to capitalize on subsequent share price decreases. The SEC and other agencies and self-regulatory organizations are looking into specific allegations of wrongdoing and monitoring U.S.-listed Chinese companies in general.

As a result of the actions by some Chinese companies and the media and governmental attention focused on all Chinese companies, the share prices of nearly all smaller Chinese companies like ours have been adversely affected, whether or not warranted in any particular case. If investors continue to lose confidence in smaller Chinese companies or if we are unable to differentiate our company in investors’ estimation from the problematic Chinese companies, then we expect that our share price will continue to be harmed.

A future issuance of our securities or a breach of agreements to which we are subject could lead to immediate and substantial dilution.

In connection with a financing we completed on March 13, 2007, we issued warrants to three funds affiliated with two institutional investors. These convertible notes and warrants contain certain anti-dilution language that could result in substantial dilution to our existing shareholders in the event we were determined to have violated them. This dilution would occur by repricing the warrants and recalculating the number of shares underlying the warrants. Even if an issuance did not trigger these anti-dilution provisions, an issuance of ordinary shares could nevertheless be completed at a level lower than some shareholder purchased their shares, leading to dilution of such shareholders.

3

We have generated a significant shareholders’ deficit, and we cannot provide any assurance that our business will be profitable in the future.

Though we achieved profitability from 2004 to 2006, we had an accumulated deficit of RMB86,011,313 as of December 31, 2010. As of December 31, 2010, our shareholders’ equity was RMB139,528,389. While we have achieved profitability in previous years, there can be no assurance that we will be able to continue our growth or profitability. Indeed, we had a net loss of RMB17,323,421 in the fiscal year ended December 31, 2010.

Our customers are Chinese companies engaged in the retail and consumer goods industries, and, consequently, our financial performance is dependent upon the economic conditions of these industries.

We have derived most of our revenues to date from software and services to the Chinese retail and consumer goods industries for manufacturers, distributors, logistics player and retailers, and our future growth is critically dependent on increased sales to these particular industries. The success of our customers is intrinsically linked to economic conditions in these industries, which in turn are subject to intense competitive pressures and are affected by overall economic conditions. We believe the license of our software solutions and the purchase of our related services is discretionary and generally involves a significant commitment of capital. As a result, although we believe our products can assist China’s retailers, distributors, wholesalers, and logistics companies in a competitive environment, demand for our products and services could be disproportionately affected by instability or downturns in the retailing, distribution, wholesaling and logistics industries, which may cause customers to exit the industry or delay, cancel or reduce any planned expenditures for information management systems and software products. We have previously experienced this effect in connection with the global financial crises and economic downturn, placed upon China’s retailing industry in recent years. There can be no assurance that we will be able to continue our historical revenue growth or sustain our profitability on a quarterly or annual basis or that our results of operations will not be adversely affected by continuing or future downturns in these industries. Any adverse change in the Chinese retail and consumer goods industries could adversely affect the level of software expenditure by the participants in these industries, which, in turn, could result in a material reduction in our sales.

Our recent service fee revenue growth will require our officers to manage our business efficiently while recruiting a significant number of new employees to assist in further development and implementation of our software.

In 2010, we had a great increase in service fee revenue. We intend to optimize our revenue mix by focusing on generating more service fee income through a wider range and different levels of service in the future. The growth in the size and complexity of our business has placed and is expected to continue to place a significant strain on our management and operations. Continued growth will require us to recruit and hire a substantial number of new employees, including consulting and product development personnel. In particular, our ability to undertake new projects and increase license revenues is substantially dependent on the availability of our consulting personnel to assist in the licensing and implementation of our software solutions. We will not be able to continue to increase our business at historical rates without adding significant numbers of personnel skilled in software implementation and integration. Although we have not incurred significant difficulty in the hiring and training of skilled employees to date, there can be no assurance that we will effectively locate, retain or train additional personnel in the future. If we do not sufficiently increase our integration and implementation workforce over time, we may be required to forego licensing opportunities. Our ability to compete effectively and to manage future growth, if any, also will depend on our ability to continue to implement and improve operational, financial and management information systems on a timely basis.

Historically, wages for comparably skilled technical and management personnel in the software solutions industry in China have been lower than in developed countries, such as in the U.S. or Europe. In recent years, wages in China’s software industry have increased and may continue to increase at faster rates. Wage increases will increase our cost of our products and services of the same quality and increase our cost of operations. As a result, our gross margin and profit margin may decline. In the long term, unless offset by increases in efficiency and productivity of our work force, wage increases may also result in increased prices for our solutions and services, making us potentially less competitive. Increases in wages, including an increase in the cash component of our compensation expenses, will increase our net cash outflow and our gross margin and profit margin may decline.

4

Our operating results may seasonally fluctuate, which could cause our results to fall short of expectations and may adversely affect the trading price of our ordinary shares.

Our business has historically experienced the highest revenue in the fourth quarter of each year, primarily due to a massive year-end capital purchases by customers. Such factors have resulted in 2010, 2009, and 2008 first quarter revenue being lower than revenue in the prior year’s fourth quarter. We believe that this trend will continue in the future and that our revenue will continue to peak in the fourth quarter of each year and decline from that level in the first quarter of the following year. As we continue to grow, we expect that the seasonality in our business may cause our operating results to fluctuate. Due to the foregoing factors, we believe that quarter to quarter comparisons of our results of operations may not be a good indication of our future performance and should not be overly relied upon. It is likely that our results of operations in some periods may be below the expectations of public market analysts and investors. In this event, the price of our ordinary shares will probably decline, perhaps significantly more in percentage terms than any corresponding decline in our operating results.

We are heavily dependent upon the services of technical and managerial personnel who develop and implement our one-stop front-end supply chain total solutions, and we may have to actively compete for their services.

We are heavily dependent upon our ability to attract, retain and motivate skilled technical, managerial and consulting personnel, especially highly skilled engineers involved in ongoing product development and consulting personnel. Our ability to install, maintain and enhance our front-end supply chain total solutions is substantially dependent upon our ability to locate, hire and train qualified personnel. Many of our technical, managerial and consulting personnel possess skills that would be valuable to all companies engaged in software development, and the Chinese software industry is characterized by a high level of employee mobility and aggressive recruiting of skilled personnel. Consequently, we expect that we will have to actively compete with other Chinese software developers for these employees. Our ability to profitably operate is substantially dependent upon our ability to locate, hire, train and retain our technical, managerial and consulting personnel. Although we have not experienced difficulty locating, hiring, training or retaining our employees to date, there can be no assurance that we will be able to retain our current personnel, or that we will be able to attract and assimilate other personnel in the future. If we are unable to effectively obtain and maintain skilled personnel, the quality of our software products and the effectiveness of installation and training could be materially impaired.

We may be subject to fines and legal sanctions if we or our employees who are PRC citizens fail to comply with recent PRC regulations relating to employee stock options granted by overseas listed companies to PRC citizens.

In March 2007, SAFE issued the Application Procedure for Foreign Exchange Administration for Domestic Individuals Participating in Employee Stock Holding Plans or Stock Option Plans of Overseas Listed Companies, also known as “Circular 78.” Under Circular 78, PRC individuals who participate in an employee stock option holding plan or a stock option plan of an overseas listed company are required, through a PRC domestic agent or PRC subsidiary of the overseas listed company, to register with SAFE and complete certain other procedures. We and our Chinese employees who have been granted restricted stock or stock options pursuant to our stock incentive plans are subject to Circular 78 because we are an overseas listed company. However, in practice, significant uncertainties exist with respect to the interpretation and implementation of Circular 78. We intend to submit the application for registration of our employee stock incentive plan as soon as possible. We or our Chinese employees may not be able to comply with, qualify under, or obtain any registration required by Circular 78. If we or our Chinese employees fail to comply with the provisions of Circular 78, we or they may be subject to fines and legal sanctions imposed by SAFE or other PRC governmental authorities, which could result in a material and adverse effect to our business operations and employee stock incentive plans.

Our business could suffer if our executives and directors compete against us and our non-competition agreements with them cannot be enforced.

If any of our management or key personnel joins a competitor or forms a competing company, we may lose customers, suppliers, know-how and key professionals and staff members. Each of our directors and executive officers has entered into employment agreements and confidentiality and non-competition agreements with us. However, if any dispute arises between our directors and officers and us, the non-competition provisions contained in their confidentiality and non-competition agreements may not be enforceable, especially in China, where most of these executive officers and key employees reside, on the ground that we have not provided adequate compensation to these executive officers for their non-competition obligations, which is required under the relevant PRC regulations.

5

We sell our services on a fixed-price, fixed-time basis, which exposes us to risks associated with cost overruns and delays.

We sell most of our services on a fixed-price, fixed-time basis. In contracts with our customers, we typically agree to pay late completion fines of up to 0.3% of the total contract value. In large scale projects, there are many factors beyond our control which could cause delays or cost overruns. In this event, we would be exposed to cost overruns and liability for late completion fines.

Competition within the Chinese market for our software products is significant.

We believe that while the Chinese market for front-end supply chain total solutions is subject to intense competition, the number of significant competitors is relatively limited, we effectively compete in our market, our competitors occupy a substantial competitive position. There can be no assurance that we will be able to effectively compete in our industry on an ongoing basis.

Our financial performance is dependent upon the sale and implementation of front-end supply chain total solutions and related services, a single, concentrated group of products.

We derive most of our revenues from the license and implementation of software applications for China’s retail and consumer goods industries and providing consulting services. The life cycle of our software is difficult to estimate due in large measure to the potential effect of new software, applications and enhancements (including those we introduce) on the maturation in the China’s retail and consumer goods industries industry. To the extent we are unable to continually improve our front-end supply chain total solutions to address the changing needs of the China’s retail and consumer goods industries market, we may experience a significant decline in the demand for our programs. In such a scenario, our revenues may significantly decline.

The market for front-end supply chain total solutions is intensely competitive.

Although we believe that we have principal competitive factors in our markets, a number of companies offer competitive products addressing certain of our target markets. In the enterprise systems market, we compete with in-house systems developed by our targeted customers and with third-party developers. In addition, we believe that new market entrants may attempt to develop fully integrated enterprise-level systems targeting the China’s retail and consumer goods industries. Many of our existing competitors, as well as a number of potential new competitors, have significantly greater financial, technical and marketing resources than we do. We cannot guarantee that we will be able to compete successfully against current or future competitors. As a result of this product concentration and uncertain product life cycles, we may not be as protected from new competition or industry downturns as a more diversified competitor.

Our financial performance is directly related to our ability to adapt to technological change and evolving standards when developing and improving our front-end supply chain total solutions.

The software development industry is subject to rapid technological change, changing customer requirements, frequent new product introductions and evolving industry standards that may render existing software obsolete. The life cycles of our software are difficult to estimate. Our software products must keep pace with technological developments, conform to evolving industry standards and address the increasingly sophisticated needs of Chinese retailers, wholesalers, distributors and logistics companies. In particular, we believe that we must continue to respond quickly to users’ needs for broad functionality. While we attempt to upgrade our software every one to two years, we cannot guarantee that our software will continue to enjoy market acceptance. To the extent we are unable to develop and introduce products in a timely manner, we believe that participants in the China’s retail and consumer goods industries will obtain products from our competitors promptly and our sales will correspondingly suffer. In addition, we strive to achieve compatibility between our products and retailing systems platforms that we believe are or will become popular and widely adopted. We invest substantial resources in development efforts aimed at achieving this compatibility. If we fail to anticipate or respond adequately to technology or market developments, we could incur a loss of competitiveness or revenue.

6

Asset impairment reviews may result in future write-downs.

Our accounting policies require us, among other things, to conduct annual reviews of goodwill, and to test intangible assets for impairment whenever events or changes in circumstances indicate that their carrying amount may not be recoverable. In connection with our business acquisitions, we make assumptions regarding estimated future cash flows and other factors to determine the fair value of goodwill and intangible assets. In assessing the related useful lives of those assets, we have to make assumptions regarding their fair value, our recoverability of those assets and our ability to successfully develop and ultimately commercialize acquired technology. If those assumptions change in the future when we conduct our periodic reviews in accordance with applicable accounting standards, we may be required to record impairment charges. It is possible that future reviews will result in further write-downs of goodwill and other intangible assets.

The financial soundness of our clients and vendors could affect our business and results of operations.

As a result of the disruptions in the financial markets and other macro-economic challenges currently affecting the economy of the United States and other parts of the world, our clients, subcontractors, suppliers and other vendors may experience cash flow concerns. As a result, clients may modify, delay or cancel plans to purchase our services and vendors may reduce their output, change terms of sales, or stop providing goods or services to us. Additionally, if clients’ or vendors’ operating and financial performance deteriorates, or if they are unable to make scheduled payments or obtain credit, clients may not be able to pay, or may delay payment of, accounts receivable owed to us and vendors may restrict credit or impose different payment terms, or stop providing goods or services to us. Any inability of current or potential clients to pay us for our services or any demands by vendors for different payment terms may adversely affect our earnings and cash flow. Furthermore, if one or more of our vendors stops providing goods or services to us, or interrupts its provision of goods or services to us, our business could be disrupted and we may incur higher costs.

We are substantially dependent upon our key personnel, particularly Adam Yan, our Chairman and Chief Executive Officer.

Our performance is substantially dependent on the performance of our executive officers and key employees. We do not have in place “key person” life insurance policies on any of our employees. The loss of the services of any of our executive officers or other key employees could substantially impair our ability to successfully implement our existing software and develop new programs and enhancements.

As a software-oriented business, our ability to operate profitably is directly related to our ability to develop and protect our proprietary technology.

We rely on a combination of trademark, trade secret, nondisclosure and copyright law to protect our front-end supply chain total solutions, which may afford only limited protection. Despite our efforts to protect our proprietary rights, unauthorized parties, including customers, may attempt to reverse engineer or copy aspects of our software products or to obtain and use information that we regard proprietary. Although we are currently unaware of any unauthorized use of our technology, in the future, we cannot guarantee that others will not use our technology without proper authorization.

Some of our software products are developed on third-party middleware software programs that are licensed by our customers from third parties, generally on a non-exclusive basis. Considering the fact that we believe that there are a number of widely available middleware programs available, we do not currently anticipate that our customers will experience difficulties obtaining these programs. The termination of any such licenses, or the failure of the third-party licensors to adequately maintain or update their products, could result in delay in our ability to ship certain of our products while we seek to implement technology offered by alternative sources. Nonetheless, while it may be necessary or desirable in the future to obtain other licenses, there can be no assurance that they will be able to do so on commercially reasonable terms or at all.

7

Our success and ability to compete depend substantially upon our intellectual property, which we protect through a combination of confidentiality arrangements and copyright. We enter into confidentiality agreements with most of our employees and consultants, and control access to, and distribution of, our documentation and other licensed information. Despite these precautions, it may be possible for a third party to copy or otherwise obtain and use our technology without authorization, or to develop similar technology independently. Since the Chinese legal system in general and the intellectual property regime in particular, are relatively weak, it is often difficult to enforce intellectual property rights in China.

In the future, we may receive notices claiming that we are infringing the proprietary rights of third parties. While we believe that we do not infringe and have not infringed upon the rights of others, we cannot guarantee that we will not become the subject of infringement claims or legal proceedings by third parties with respect to our current programs or future software developments. In addition, we may initiate claims or litigation against third parties for infringement of our proprietary rights or to establish the validity of our proprietary rights. Any such claims could be time consuming, result in costly litigation, cause product shipment delays or force us to enter into royalty or license agreements rather than dispute the merits of such claims, thereby impairing our financial performance by requiring us to pay additional royalties and/or license fees to third parties. We have never lost an infringement claim since our formation.

Our front-end supply chain total solutions may contain integration challenges, design defects or software errors that could be difficult to detect and correct.

Implementation of our software may involve a significant amount of systems developed by third parties. Although we have not experienced a material number of defects associated with our software to date, despite extensive testing, we may, from time to time, discover defects or errors in our software only after use by a customer. We may also experience delays in shipment of our software during the period required to correct such errors. In addition, we may, from time to time, experience difficulties relating to the integration of our software products with other hardware or software in the customer’s environment that are unrelated to defects in our software products. Such defects, errors or difficulties may cause future delays in product introductions and shipments, result in increased costs and diversion of development resources, require design modifications or impair customer satisfaction with our software. Since our software solutions are used by our customers to perform mission-critical functions, design defects, software errors, misuse of our products, incorrect data from external sources or other potential problems within or out of our control that may arise from the use of our products could result in financial or other damages to our customers. To date, however, we have not had significant difficulties integrating our software into our customers’ existing systems. We do not maintain product liability insurance. Although our license agreements with customers contain provisions designed to limit our exposure to potential claims as well as any liabilities arising from such claims, such provisions may not effectively protect us against such claims and the liability and costs associated therewith. To the extent we are found liable in a product liability case, we could be required to pay a substantial amount of damages to an injured customer, thereby impairing our financial condition.

We may not pay dividends.

We have not previously paid any cash dividends nor do we anticipate paying any dividends on our ordinary shares. Although we achieved profitability from 2004 to 2006, we cannot assure you that our operations will continue to result in sufficient revenues to enable us to operate at profitable levels or to generate positive cash flows. Indeed, we had net losses of RMB25,265,497 and RMB17,323,421 in the fiscal years ended December 31, 2009 and 2010, respectively. Furthermore, there is no assurance our Board of Directors will declare dividends even if we are profitable. Dividend policy is subject to the discretion of our Board of Directors and will depend on, among other things, our earnings, financial condition, capital requirements and other factors. Under Cayman Islands law, we may only pay dividends from profits or credit from the share premium account (the amount paid over par value, which is $0.0756), and we must be solvent before and after the dividend payment. If we determine to pay dividends on any of our ordinary shares in the future, as a holding company, we will be dependent on receipt of funds from our operating wholly- and partially-owned subsidiaries.

8

A slowdown in the Chinese economy may slow down our growth and profitability.

We cannot assure you that growth of the Chinese economy will be steady or that any slowdown will not have a negative effect on our business. Several years ago, the Chinese economy experienced deflation, which may recur in the foreseeable future. More recently, the Chinese government announced its intention to use macroeconomic tools and regulations to slow the rate of growth of the Chinese economy, the results of which are difficult to predict. Adverse changes in the Chinese economy will likely impact the financial performance of the retailing, distribution, logistics and manufacturing industries in China. Consequently, under such circumstances, our customers may opt to delay discretionary expenditures like those for our software, which, in turn, could result in a material reduction in our sales.

We do not have business interruption, litigation or natural disaster insurance.

The insurance industry in China is still at an early state of development. In particular PRC insurance companies offer limited business products. As a result, we do not have any business liability or disruption insurance coverage for our operations in China. Any business interruption, litigation or natural disaster may result in our business incurring substantial costs and the diversion of resources.

We may become a passive foreign investment company, which could result in adverse U.S. tax consequences to U.S. investors.

Based upon the nature of our business activities, we may be classified as a passive foreign investment company (“PFIC”) by the U.S. Internal Revenue Service (“IRS”) for U.S. federal income tax purposes. Such characterization could result in adverse U.S. tax consequences to you if you are a U.S. investor. For example, if we are a PFIC, a U.S. investor will become subject to burdensome reporting requirements. The determination of whether or not we are a PFIC is made on an annual basis and will depend on the composition of our income and assets from time to time. Specifically, we will be classified as a PFIC for U.S. tax purposes if either:

|

|

·

|

75% or more of our gross income in a taxable year is passive income; or

|

|

|

·

|

the average percentage of our assets by value in a taxable year which produce or are held for the production of passive income (which includes cash) is at least 50%.

|

The calculation of the value of our assets is based, in part, on the then market value of our ordinary shares, which is subject to change. In addition, the composition of our income and assets will be affected by how, and how quickly, we spend the cash we raised in our initial public offering. We cannot assure you that we will not be a PFIC for any taxable year.

Governmental control of currency conversion may affect the value of our ordinary shares.

The PRC government imposes controls on the convertibility of the Renminbi into foreign currencies and, in certain cases, the remittance of currency out of China. We receive substantially all of our revenues in Renminbi. Under our current corporate structure, our income is derived from dividend payments from our PRC subsidiaries. Shortages in the availability of foreign currency may restrict the ability of our PRC subsidiaries to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency denominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade-related transactions, can be made in foreign currencies without prior approval from the PRC State Administration of Foreign Exchange by complying with certain procedural requirements. However, approval from appropriate government authorities is required where Renminbi are to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of bank loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay dividends in foreign currencies to our shareholders.

9

Fluctuation in the value of the Renminbi may have a material adverse effect on the value of our ordinary shares.

The value of the Renminbi against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in political and economic conditions. The Renminbi is permitted to fluctuate within a narrow and managed band against a basket of certain foreign currencies. There remains significant international pressure on the PRC government to adopt an even more flexible currency policy, which could result in a further and more significant appreciation of the Renminbi against the U.S. dollar. We rely entirely on dividends and other fees paid to us by our subsidiaries in China. Any significant revaluation of Renminbi may materially and adversely affect our cash flows, revenues, earnings and financial position, and the value of, and any dividends payable on, our ordinary shares in U.S. dollars. For example, an appreciation of Renminbi against the U.S. dollar would make any new Renminbi denominated investments or expenditures more costly to us, to the extent that we need to convert U.S. dollars into Renminbi for such purposes. An appreciation of Renminbi against the U.S. dollar would also result in foreign currency translation losses for financial reporting purposes when we translate our U.S. dollar denominated financial assets into Renminbi, as the Renminbi is our reporting currency.

Changes in China’s political and economic policies could harm our business.

The economy of China has historically been a planned economy subject to governmental plans and quotas and has, in certain aspects, been transitioning to a more market-oriented economy. Although we believe that the economic reform and the macroeconomic measures adopted by the Chinese government have had a positive effect on the economic development of China, we cannot predict the future direction of these economic reforms or the effects these measures may have on our business, financial position or results of operations.

New labor laws in the PRC may adversely affect our results of operations.

As of December 31, 2010 we had approximately 740 employees in the PRC. On June 29, 2007, the PRC Government promulgated a new labour law, namely, the Labour Contract Law of the PRC, or the Labour Contract Law, which became effective on January 1, 2008. The Labor Contract Law establishes more restrictions and increases costs for employers to dismiss employees under certain circumstances, including specific provisions related to fixed-term employment contracts, non-fixed-term employment contracts, task-based employment, part-time employment, probation, consultation with the labor union and employee representative’s council, employment without a contract, dismissal of employees, compensation upon termination and for overtime work, and collective bargaining. According to the Labor Contract Law, unless otherwise provided by law, an employer is obliged to sign a labor contract with a non-fixed term with an employee if the employer continues to hire the employee after the expiration of two consecutive fixed-term labor contracts or if the employee has worked for the employer for ten consecutive years. Severance pay is required if a labor contract expires without renewal because the employer refuses to renew the labor contract or provides less favorable terms for renewal. In addition, under the Regulations on Paid Annual Leave for Employees, which became effective on January 1, 2008, employees who have served more than one year for an employer are entitled to a paid vacation ranging from 5 to 15 days, depending on the number of the employee’s working years at the employer. Employees who waive such vacation time at the request of employers shall be compensated for three times their regular salaries for each waived vacation day. As a result of these new measures designed to enhance labor protection, our labor costs are expected to increase, which may adversely affect our business and our results of operations. In addition, the PRC government in the future may enact further labor-related legislation that increases our labor costs and restricts our operations.

If PRC law were to phase out the preferential tax benefits currently being extended to qualified “High and New Technology Enterprises”, we would have to pay more taxes, which could have a material and adverse effect on our financial condition and results of operations.

According to the PRC Corporate Income Tax Law, or the CIT Law, which became effective on January 1, 2008, as further clarified by subsequent tax regulations implementing the CIT Law, foreign-invested enterprises and domestic enterprises are subject to corporate income tax, at a uniform rate of 25%. The CIT rate of enterprises established before March 16, 2007 that were eligible for preferential tax rates according to then effective tax laws and regulations will gradually transition to the uniform 25% CIT rate by January 1, 2013. In addition, certain enterprises may still benefit from a preferential tax rate of 15% under the CIT Law if they qualify as “high and new technology enterprises strongly supported by the state,” subject to certain general factors described in the CIT Law and the related regulations.

10

In December 2008, our subsidiary eFuture Beijing was designated as “High and New Technology Enterprises” under the CIT Law, which entitles it to a preferential CIT rate of 15% from 2008 to 2010. eFuture Beijing is in the process of applying for renewal of the preferential tax rate and anticipates that it will receive such renewal by the end of 2011. Because we believe that we are more likely than not to receive this renewal this year, we plan to reserve against tax liabilities at a rate of 15%. If it fails to maintain the “High and New Technology Enterprises” qualification, its applicable CIT rate may increase to up to 25%, which could have a material adverse effect on our results of operations. We cannot assure you that we will be able to maintain our current effective tax rate in the future.

Furthermore, we may apply for an exemption of the 5% business tax levied on our total revenues derived from our technology consulting services. If the PRC law were to phase out preferential tax benefits currently granted to “High and New Technology Enterprises” or if we ceased to qualify as such, we would be subject to the standard statutory tax rate, which currently is 25%, and we would be unable to obtain business tax refunds for our provision of technology consulting services.

China’s legal system embodies uncertainties that could adversely affect our ability to engage in the development and integration of the front-end supply chain total solutions.

Since 1979, the Chinese government has promulgated many new laws and regulations covering general economic matters. Despite this activity to develop a legal system, China’s system of laws is not yet complete. Even where adequate law exists in China, enforcement of existing laws or contracts based on existing law may be uncertain or sporadic, and it may be difficult to obtain swift and equitable enforcement or to obtain enforcement of a judgment by a court of another jurisdiction. The relative inexperience of China’s judiciary, in many cases, creates additional uncertainty as to the outcome of any litigation. In addition, interpretation of statutes and regulations may be subject to government policies reflecting domestic political changes. Noting that our business is substantially dependent upon laws protecting intellectual property rights, any ambiguity in the interpretation or implementation of such laws may negatively impact our business, its financial condition and results of operation. Our activities in China will also be subject to administration review and approval by various national and local agencies of China’s government. Because of the changes occurring in China’s legal and regulatory structure, we may not be able to secure the requisite governmental approval for our activities. Although we have obtained all required governmental approval to operate our business as currently conducted, to the extent we are unable to obtain or maintain required governmental approvals, the Chinese government may, in its sole discretion, prohibit us from conducting our business.

Shareholder rights under Cayman Islands law may differ materially from shareholder rights in the United States, which could adversely affect the ability of us and our shareholders to protect our and their interests.

Our corporate affairs are governed by our Amended and Restated Memorandum and Articles of Association, by the Companies Law (2007 Revision) and the common law of the Cayman Islands. The rights of shareholders to take action against the directors, actions by minority shareholders, and the fiduciary responsibilities of our directors to us under Cayman Islands law are to a large extent governed by the common law of the Cayman Islands. The common law in the Cayman Islands is derived in part from comparatively limited judicial precedent in the Cayman Islands as well as from English common law, the decisions of whose courts are of persuasive authority but are not binding on a court in the Cayman Islands. The rights of our shareholders and the fiduciary responsibilities of our directors under Cayman Islands law in this area may not be as clearly established as they would be under statutes or judicial precedent in existence in some jurisdictions in the United States. In particular, the Cayman Islands has a less developed body of securities laws as compared to the United States, and some states, such as Delaware, have more fully developed and judicially interpreted bodies of corporate laws. Moreover, our company could be involved in a corporate combination in which dissenting shareholders would have no rights comparable to appraisal rights which would otherwise ordinarily be available to dissenting shareholders of United States corporations. Also, our Cayman Islands counsel is not aware of a significant number of reported class actions or derivative actions having been brought in Cayman Islands courts. Such actions are ordinarily available in respect of United States corporations in U.S. courts. Finally, Cayman Islands companies may not have standing to initiate shareholder derivative action before the federal courts of the United States. As a result, our public shareholders may face different considerations in protecting their interests in actions against the management, directors or our controlling shareholders than would shareholders of a corporation incorporated in a jurisdiction in the United States, and our ability to protect our interests may be limited if we are harmed in a manner that would otherwise enable us to sue in a United States federal court.

11

As we are a Cayman Islands company and most of our assets are outside the United States, it will be extremely difficult to acquire jurisdiction and enforce liabilities against us and our officers, directors and assets based in China.

We are a Cayman Islands exempt company, and our corporate affairs are governed by our Amended and Restated Memorandum and Articles of Association and by the Cayman Islands Companies Law (2007 Revision) and other applicable Cayman Islands laws. Certain of our directors and officers reside outside of the United States. In addition, the Company’s assets are located outside the United States. As a result, it may be difficult or impossible to effect service of process within the United States upon our directors or officers and our subsidiaries, or enforce against any of them court judgments obtained in United States courts, including judgments relating to United States federal securities laws. In addition, there is uncertainty as to whether the courts of the Cayman Islands and of other offshore jurisdictions would recognize or enforce judgments of United States courts obtained against us predicated upon the civil liability provisions of the securities laws of the United States or any state thereof, or be competent to hear original actions brought in the Cayman Islands or other offshore jurisdictions predicated upon the securities laws of the United States or any state thereof. Furthermore, because the majority of our assets are located in China, it would also be extremely difficult to access those assets to satisfy an award entered against us in United States court.

You may face difficulties in protecting your interests, and your ability to protect your rights through the U.S. federal courts may be limited, because we are incorporated under Cayman Islands law, conduct most of our operations in China and most of our officers and directors reside outside the United States.

We are incorporated in the Cayman Islands, and conduct most of our operations in China through our subsidiaries in China. Most of our officers and directors reside outside the United States and some or all of the assets of those persons are located outside of the United States. It may be difficult or impossible for you to bring an original action against us or against these individuals in a Cayman Islands or Chinese court in the event that you believe that your rights have been infringed under the U.S. federal securities laws or otherwise. Even if you are successful in bringing an action of this kind, the laws of the Cayman Islands and of China may render you unable to enforce a judgment against our assets or the assets of our directors and officers. You would also find it difficult to enforce a U.S. court judgment based on the civil liability provisions of the U.S. federal securities laws, in the United States, the Cayman Islands or China, against us or our officers and directors.

Our corporate affairs are governed by our memorandum and articles of association and by the Companies Law, Cap. 22 (Law 3 of 1961, as consolidated and revised) and common law of the Cayman Islands. The rights of shareholders to take legal action against our directors and us, actions by minority shareholders and the fiduciary responsibilities of our directors to us under Cayman Islands law are to a large extent governed by the common law of the Cayman Islands. The common law of the Cayman Islands is derived in part from comparatively limited judicial precedent in the Cayman Islands as well as from English common law, which has persuasive, but not binding, authority on a court in the Cayman Islands. The rights of our shareholders and the fiduciary responsibilities of our directors under Cayman Islands law are not as clearly established as they would be under statutes or judicial precedents in the United States. In particular, the Cayman Islands has a less developed body of securities laws as compared to the United States, and provides significantly less protection to investors. In addition, Cayman Islands companies may not have standing to initiate a shareholder derivative action before the federal courts of the United States.

As a result of all of the above, our public shareholders may have more difficulty in protecting their interests through actions against us or our management, directors or major shareholders than would shareholders of a corporation incorporated in a jurisdiction in the United States.

There can be no guarantee that China will comply with the membership requirements of the World Trade Organization.

Due in part to the relaxation of trade barriers following World Trade Organization accession in January 2002, we believe China will become one of the world’s largest markets by the middle of the twenty-first century. As a result, we believe the Chinese market presents a significant opportunity for both domestic and foreign companies. With the Chinese accession to the World Trade Organization, Chinese industries are gearing up to face the new regimes that are required by World Trade Organization regulation. The Chinese government has begun to reduce its average tariff on imported goods. We believe that a tariff reduction on imported goods combined with increasing consumer demand in China may lead to increased demand for our logistics programs. China has also agreed that foreign companies will be allowed to import most products into any part of China. Current trading rights and distribution restrictions are to be phased out over a three-year period. In the sensitive area of intellectual property rights, China has agreed to implement the trade-related intellectual property agreement of the Uruguay Round. As our business is dependent upon the protection of our intellectual property in China and throughout the world, China’s decision to implement intellectual property protection standards that coordinate with other major economies is of critical importance to our business and its ability to generate profits. However, there can be no assurances that China will implement any or all of the requirements of its membership in the World Trade Organization in a timely manner, if at all.

12

High technology and emerging market shares have historically experienced extreme volatility and may subject you to losses.

The trading price of our shares may be subject to significant market volatility due to investor perceptions of investments relating to China. In addition, the high technology sector of the stock market frequently experiences extreme price and volume fluctuations, which have particularly affected the market prices of many software companies and which have often been unrelated to the operating performance of those companies.

|

Item 4.

|

Information on the Company

|

|

A.

|

History and Development of the Company

|

History

We were established as an offshore company incorporated in the Cayman Islands under the Cayman Islands Companies Law on November 2, 2000. eFuture (Beijing) Tornado Information Technology Inc. (“eFuture Tornado”), which was established as a domestic Chinese company in January 2000 in an effort to maintain intellectual property, has previously and will continue to conduct all of our software development operations as our wholly-owned subsidiary within China.

On October 31, 2006, we listed on the NASDAQ Capital Market under the symbol “EFUT.”

On August 28, 2007, following the successful acquisition of Guangzhou Royalstone System Integration Co. Ltd., eFuture Tornado was renamed “eFuture (Beijing) Royalstone Information Technology Inc.” (“eFuture Royalstone” or “eFuture Beijing”).

With the approval of our shareholders, we changed our name from “e-Future Information Technology Inc.” to “eFuture Information Technology Inc.” in 2008.

Our acquisition of Proadvancer Systems Inc. (“Proadvancer”) in April 2008 has enhanced our core business and enabled market leadership and significant share gains in China’s logistics market.

We acquired a majority stake in Beijing Fuji Biaoshang Information Technology Inc. in 2007 and effectively controlled 51% of the ownership in Beijing Wangku Hutong Information Technology Co., Ltd. in 2007 and 2008, respectively. Biaoshang and Wangku have been classified as discontinued operations for the year ended December 31, 2010, following eFuture’s announcements on August 31, 2010 and March 21, 2011, and completion on July 16, 2010 and March 13, 2011, respectively, of the sale of its 51% stakes in the two entities.

Our principal executive offices and headquarters in Beijing moved to the central business district in May of 2009, which is located at 8/F Topnew Tower, 15 Guanghua Road, Chaoyang Distinct, Beijing 100026, China. Our telephone number is +86 10 5293 7699, and our fax number is +86 10 5293 7688.

13

|

B.

|

Business Overview

|

General

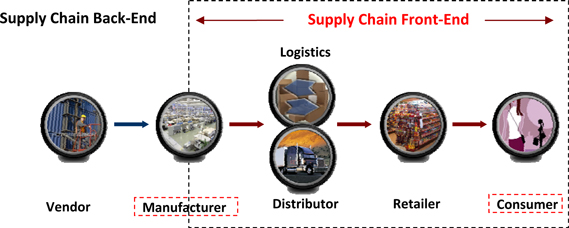

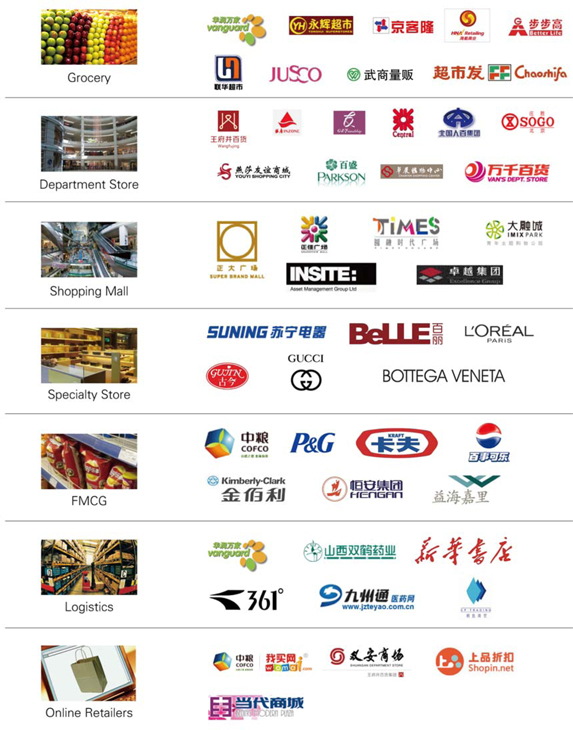

eFuture is a leading provider of software and services to China’s rapidly growing retail and consumer goods industries. eFuture offers one-stop, end-to-end integrated portfolio of software and services from factory to consumer on seven verticals: Fast Moving Consumer Goods (FMCG), Department Store, Shopping Mall, Grocery, Logistics, Specialty Store and Online Retailers.

Vision

Where is consumer, there is eFuture.

Mission

Creating a happy consumer world.

Our Market

eFuture’s software solutions and services are focused on the retail and consumer goods industries, and its customers are companies within these sectors. In China, retail sales accounted for almost 39.4% of GDP in 2010 and have shown a constant upward trend between 2003 and 2009, with a CAGR of 15.6%. In 2010, China’s retail sales reached RMB15.7 billion, representing a growth rate of 18.3% over 2009. The rapid growth of the retail and consumer goods industry in China has been driven by powerful macro-economic trends that continue today – increasing GDP, rapid urbanization, improving quality of life and increasing national disposable income. According to a report by IDC in May 2010, total expenditure on IT solutions in China’s retail industry was almost RMB1.65 billion in 2009.

Clients

eFuture’s clients include manufacturers, distributors, resellers, logistics companies and retailers. The Company’s client base encompasses global corporations such as Procter & Gamble, Pepsi, L’Oreal, Kimberly-Clark, Gucci and B&Q as well as leading Chinese companies. Its domestic client base includes over 30 companies that were ranked among China’s top 100 retailers during 2010, such as Suning, Shanghai Bailian-Lianhua, China Resources Vanguard and Beijing Wangfujing.

14

Growth Strategy

As a leading provider of software solutions and services in the retail and consumer goods industries in China, we have the following three growth strategies consisting of multiple organic and non-organic growth drivers:

15

|

|

·

|

Organic Growth - We aim to drive the long-term organic growth and profitability of our core software business and professional service by:

|

|

|

w

|

Strengthening our software core business while increasing more stable recurring service and consulting service revenues

|

|

|

w

|

Pursuing profitable growth by improving our delivery cost and operating expense structure

|

|

|

w

|

Using innovation to further broaden cloud service offerings

|

|

|

·

|

M&A – We aim to expand our business through our merger and acquisition strategy of targeted “fill-in” acquisitions. Our strategy is to actively pursue various M&A opportunities that complement organic growth by focusing on targets that will help us to achieve the following goals:

|

|

|

w

|

Diversify our product offering - Independent Software Vendors (ISV) with offerings complementary to our solutions, which focus on industries including fashion, auto, consumer electronics, drugstores and fast-moving consumer goods.

|

|

|

w

|

Broaden our regional coverage - ISVs with extensive coverage in South, East, and North China.

|

|

|

w

|

Penetrate the small and medium sized businesses (SMB) market - Companies with standardized, scalable product offerings that facilitate penetration into SMBs in tier 2 to tier 3 cities in China.

|

|

|

w

|

Create additional recurring revenue streams - Companies with products and services delivering a stable and recurring revenue stream, and which provide potential for growth.

|

Business Line

With strong brand recognition among international and local clients, eFuture provides one-stop, end-to-end integrated portfolio of software and services for the front-end supply chain from factory to consumer.

eFuture has three business lines: software, professional service and cloud service.

|

|

·

|

Software is eFuture’s core business. The Company’s software solutions include the management of merchandizing, distribution, warehousing, supply chain, customer relationship, logistics and point of sale. They are highly scalable and can be deployed individually or together with back-end systems. These solutions offer enhanced decision making and responsiveness to consumer demands, increased efficiency, and ultimately drive profit growth.

|

|

|

·

|

Professional service is eFuture’s fast growing business, and covers operations, delivery, consulting, maintenance and support services via the Company’s nationwide service centers and team of dedicated professionals.

|

|

|

·

|

Cloud service is eFuture’s seed business, and consists of cloud services based on cloud computing architecture, such as business to consumer (“B2C”) eCommerce and Salesforce Automation.

|

By solidifying our core software business, growing professional service revenues, and developing our cloud service offerings and capabilities, we have established a diverse platform which we believe will allow us to further expand our market share and generate consistent revenue in the coming years.

Software

Our software solutions are specifically designed to optimize demand processes from factory to consumer, and to address SCM, business processes, decision support, inventory optimization, collaborative planning and forecasting requirements. Our software solutions integrate industry know-how with predictive information technologies, consulting services and best practices to help our clients create, manage and fulfill customer demand.

Our solutions can be deployed individually to meet specific needs, or as part of a scalable and fully-integrated, end-to-end solution. Our software solutions consist of three independently deployable groups of products: Foundation Solutions, Collaborative Solutions and Intelligent Solutions, which range from internal and external collaborative process management to sophisticated business analysis.

16

Our Foundation Solutions are used to meet client needs for services such as retail management, point of sale (“POS”), distribution management, logistics management, warehouse management, vendor payment and control and loyalty card management. Our clients use several of our Foundation Solutions, depending on the type of customer and their needs.

Our Collaborative Solutions are used to meet client needs for services such as visual SCM and visual process management systems. Our clients use a variety of our Collaborative Solutions, depending on the type of customer and their needs.

Our Intelligent Solutions are used to meet client needs for services such as business intelligence, brand analysis, supplier relationship management and customer relationship management systems.

Professional Service

Our software professional service business includes recurring support services on existing software installations, delivery services, consulting services and outsourcing services.

Support Service is provided following the installation of our software solutions, as clients will typically require ongoing maintenance support and software upgrades to ensure the efficient operation of their system. These services are designed to assist our customers with integration issues and to answer questions that may arise.

Following a one-year regular maintenance program that is an element of our initial software installation, our customers may purchase three levels of annual continued maintenance services. Under our Regular and Silver plans, we generally provide these maintenance services over the telephone during regular business hours. For our customers who elect to purchase our Gold plan at a higher cost, we will provide these services at the customer’s location and on a real-time basis, if appropriate. Each level of maintenance offers customers different options to meet their particular needs.