Endeavour Silver Corp.: Exhibit 99.1 - Filed by newsfilecorp.com

ANNUAL INFORMATION FORM

of

ENDEAVOUR SILVER CORP.

(the “Company” or “Endeavour”)

Suite #301 - 700 West Pender Street

Vancouver, British

Columbia, Canada, V6C 1G8

Phone: (604) 685-9775

Fax: (604) 685-9744

Dated: March 17, 2017

TABLE OF CONTENTS

| ITEM 1: |

PRELIMINARY NOTES

|

| 1.1 |

Incorporation of Documents by

Reference |

All financial information in this Annual Information Form

(“AIF”) has been prepared in accordance with International Financial Reporting

Standards (“IFRS”) as prescribed by the International Accounting Standards

Board.

The information provided in the AIF is supplemented by

disclosure contained in the documents listed below which are incorporated by

reference into this AIF. The documents listed below are not contained within,

nor attached to, this document but may be accessed at www.sedar.com or on the

Company’s website at www.edrsilver.com.

Type of

Document |

Effective Date /

Period Ended |

Date Filed /

Posted |

Document

name which may be viewed at

the SEDAR website at

www.sedar.com |

|

NI 43-101 Technical Report:

Updated Mineral Resource and

Reserve Estimates for the Guanacevi Project, Durango State, Mexico |

December 31, 2016 |

March 8, 2017 |

Technical Report (NI 43-101) – English

Qualification Certificate(s) and Consent(s) |

NI 43-101 Technical Report:

Updated

Mineral Resource and Reserve Estimates for the Bolañitos Project

Guanajuato State, Mexico |

December 31, 2016 |

March 8, 2017 |

Technical Report (NI 43-101) –

English Qualification Certificate(s) and Consent(s) |

NI 43-101 Technical Report:

Updated

Mineral Resource and Reserve Estimates for the El Cubo Project, Guanajuato

State, Mexico |

December 31, 2016 |

March 8, 2017 |

Technical Report (NI 43-101) –

English Qualification Certificate(s) and Consent(s) |

NI 43-101 Technical Report

Preliminary

Economic Assessment for the Terronera Project, Jalisco State, Mexico |

March 25, 2015 |

May 13, 2015 |

Technical Report (NI 43-101) –

English Qualification Certificate(s) and Consent(s)

|

References to “the Company” or “Endeavour” are to Endeavour

Silver Corp. and where applicable and as the context requires, include its

subsidiaries.

All information in this AIF is as of December 31, 2016 unless

otherwise indicated.

| 1.3 |

Forward-Looking Statements |

This AIF contains “forward-looking statements” within the

meaning of applicable Canadian securities legislation. Such forward-looking

statements concern the Company’s anticipated results and developments in the

Company’s operations in future periods, planned exploration and development of

its properties, plans related to its business and other matters that may occur

in the future. These statements relate to analyses and other information that

are based on expectations of future performance, including silver and gold

production and planned work programs.

Endeavour Silver Corp.

Statements concerning reserves and mineral resource estimates

may also be deemed to constitute forward-looking statements to the extent that

they involve estimates of the mineralization that will be encountered if the

property is developed and, in the case of mineral reserves, such statements

reflect the conclusion based on certain assumptions that the mineral deposit can

be economically exploited.

Any statements that express or involve discussions with respect

to predictions, expectations, beliefs, plans, projections, forecasts,

objectives, assumptions or future events or performance are not statements of

historical fact and may be forward-looking statements. Forward-looking

statements are subject to a variety of known and unknown risks, uncertainties

and other factors which could cause actual events or results to differ from

those expressed or implied by the forward-looking statements, including, without

limitation:

| • |

risks related to precious and base metal price

fluctuations; |

| • |

risks related to fluctuations in the currency markets

(particularly the Mexican peso, Canadian dollar and United States dollar);

|

| • |

risks related to the inherently dangerous activity of

mining, including conditions or events beyond our control, and operating

or technical difficulties in mineral exploration, development and mining

activities; |

| • |

uncertainty in our ability to fund the development of our

mineral properties or the completion of further exploration programs;

|

| • |

uncertainty as to actual capital costs, operating costs,

production and economic returns, and uncertainty that our development

activities will result in profitable mining operations; |

| • |

risks related to our reserves and mineral resource

figures being estimates based on interpretations and assumptions which may

result in less mineral production under actual conditions than is

currently estimated and to diminishing quantities or grades of mineral

reserves as properties are mined; |

| • |

risks related to changes in governmental regulations, tax

and labour laws and obtaining necessary licenses and permits; |

| • |

risks related to our business being subject to

environmental laws and regulations which may increase our costs of doing

business and restrict our operations; |

| • |

risks related to our mineral properties being subject to

prior unregistered agreements, transfers, or claims and other defects in

title; |

| • |

risks relating to inadequate insurance or inability to

obtain insurance; |

| • |

risks related to our ability to successfully integrate

acquisitions; |

| • |

uncertainty in our ability to obtain necessary financing;

|

| • |

risks related to increased competition that could

adversely affect our ability to attract necessary capital funding or

acquire suitable producing properties for mineral exploration in the

future; |

| • |

risks related to many of our primary properties being

located in Mexico, including political, economic, and regulatory

instability; and |

| • |

risks related to our officers and directors becoming

associated with other natural resource companies which may give rise to

conflicts of interests. |

This list is not exhaustive of the factors that may affect our

forward-looking statements. Should one or more of these risks and uncertainties

materialize, or should underlying assumptions prove incorrect, actual results

may vary materially from those described in the forward-looking statements. The

Company’s forward-looking statements are based on beliefs, expectations and

opinions of management on the date the statements are made and the Company does

not assume any obligation to update forward-looking statements if circumstances

or management’s beliefs, expectations or opinions change, except as required by

law. For the reasons set forth above, investors should not place undue reliance

on forward-looking statements.

2

Endeavour Silver Corp.

| 1.4 |

Currency and Exchange

Rates |

All dollar amounts in this AIF are expressed in U.S. dollars

(“U.S.$”) unless otherwise indicated. References to “Cdn.$” are to Canadian

dollars.

The high, low, average and closing noon rates for the United

States dollar in terms of Canadian dollars for each of the financial periods of

the Company ended December 31, 2016, December 31, 2015 and December 31, 2014, as

quoted by the Bank of Canada, were as follows:

| |

|

|

Year ended |

|

|

Year ended |

|

|

Year ended |

|

| |

|

|

December 31, 2016 |

|

|

December 31, 2015 |

|

|

December 31, 2014 |

|

| |

|

|

|

|

|

|

|

|

|

|

| |

High |

|

1.4589 |

|

|

1.3990 |

|

|

1.1643 |

|

| |

Low |

|

1.2544 |

|

|

1.1728 |

|

|

1.0614 |

|

| |

Average |

|

1.3248 |

|

|

1.2787 |

|

|

1.1045 |

|

| |

Closing |

|

1.3427 |

|

|

1.3840 |

|

|

1.1601 |

|

On December 30, 2016, the noon exchange rate for the United

States dollar in terms of Canadian dollars, as quoted by the Bank of Canada, was

U.S.$1.00 = Cdn.$1.3427 (Cdn.$1.00 = U.S.$0.7448) . On March 17, 2017, the daily

average exchange rate for the United States dollar in terms of Canadian dollars,

as quoted by the Bank of Canada, was U.S.$1.00 = Cdn.$1.3369 (Cdn.$1.00 =

U.S.$0.7480) .

| 1.5 |

Classification of Mineral Reserves and

Resources |

In this AIF, the definitions of proven and probable mineral

reserves, and measured, indicated and inferred mineral resources are those used

by the Canadian provincial securities regulatory authorities and conform to the

definitions utilized by the Canadian Institute of Mining, Metallurgy and

Petroleum, as the CIM Definition Standards on Mineral Resources and Mineral

Reserves adopted by the CIM Council, as amended.

| 1.6 |

Cautionary Note to U.S. Investors concerning Estimates

of Mineral Reserves and Measured, Indicated and Inferred Mineral

Resources |

This AIF has been prepared in accordance with the requirements

of the securities laws in effect in Canada, which differ from the requirements

of United States securities laws. The terms “mineral reserve”, “proven mineral

reserve” and “probable mineral reserve” are Canadian mining terms as defined in

accordance with the Canadian Securities Administrators’ National Instrument

43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) and the

Canadian Institute of Mining, Metallurgy and Petroleum as the CIM Definition

Standards on Mineral Resources and Mineral Reserves adopted by the CIM Council,

as amended. These definitions differ materially from the definitions in SEC

Industry Guide 7 under the United States Securities Act of 1933, as amended.

Under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study

is required to report reserves, the three-year historical average price is used

in any reserve or cash flow analysis to designate reserves and the primary

environmental analysis or report must be filed with the appropriate governmental

authority.

3

Endeavour Silver Corp.

In addition, the terms “mineral resource”, “measured mineral

resource”, “indicated mineral resource” and “inferred mineral resource” are

defined in and required to be disclosed by NI 43-101; however, these terms are

not defined terms under SEC Industry Guide 7 and are normally not permitted to

be used in reports and registration statements filed with the SEC. Investors are

cautioned not to assume that any part or all of mineral deposits in these

categories will ever be converted into SEC Industry Guide 7 reserves. “Inferred

mineral resources” have a great amount of uncertainty as to their existence, and

great uncertainty as to their economic and legal feasibility. It cannot be

assumed that all or any part of an inferred mineral resource will ever be

upgraded to a higher category. Under Canadian rules, estimates of inferred

mineral resources may not form the basis of feasibility or pre-feasibility

studies, except in rare cases. Investors are cautioned not to assume that all or

any part of an inferred mineral resource exists or is economically or legally

mineable. Disclosure of “contained ounces” in a resource is permitted disclosure

under Canadian regulations; however, the SEC normally only permits issuers to

report mineralization that does not constitute “reserves” by SEC Industry Guide

7 standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this AIF contain

descriptions of our mineral deposits that may not be comparable to similar

information made public by U.S. companies subject to the reporting and

disclosure requirements under the United States federal securities laws and the

rules and regulations thereunder, including SEC Industry Guide 7.

| ITEM 2: |

CORPORATE STRUCTURE

|

| 2.1 |

Name, Address and

Incorporation |

The Company was incorporated under the laws of the Province of

British Columbia on March 11, 1981 under the name, “Levelland Energy &

Resources Ltd”. Effective August 27, 2002 the Company changed its name to

“Endeavour Gold Corp.”, consolidated its share capital on the basis of four old

common shares for one new common share and increased its share capital to

100,000,000 common shares without par value. On September 13, 2004, the Company

changed its name to “Endeavour Silver Corp.”, transitioned from the Company

Act (British Columbia) to the Business Corporations Act (British

Columbia) and increased its authorized share capital to unlimited common shares

without par value.

The Company’s principal business office is located at:

Suite 301 - 700 West Pender Street

Vancouver, British Columbia

Canada, V6C 1G8

and its registered and records office is located at:

19th Floor, 885 West Georgia

Street

Vancouver, British Columbia

Canada, V6C 3H4

4

Endeavour Silver Corp.

The Company conducts its business primarily in Mexico through

subsidiary companies. The following table lists the Company’s material direct

and indirect subsidiaries, their jurisdiction of incorporation, and percentage

owned by the Company directly or indirectly.

| |

|

|

|

|

|

Percentage |

|

| |

|

|

|

|

|

owned directly |

|

| Name of

Company |

|

|

Incorporated |

|

|

or indirectly |

|

| |

|

|

|

|

|

|

|

| Endeavour Gold Corporation, S.A. de C.V.

|

|

|

Mexico |

|

|

100% |

|

| EDR Silver de Mexico S.A. de C.V. SOFOM ENR |

|

|

Mexico |

|

|

100% |

|

| Minera Plata Adelante, S.A. de C.V. |

|

|

Mexico |

|

|

100% |

|

| Minera Santa Cruz Garibaldi S.A. de C.V. |

|

|

Mexico |

|

|

100% |

|

| Refinadora Plata Guanacevi, S.A. de C.V.

|

|

|

Mexico |

|

|

100% |

|

| Mina Bolañitos S.A de C.V. |

|

|

Mexico |

|

|

100% |

|

| Compania Minera del Cubo S.A. de C.V. |

|

|

Mexico |

|

|

100% |

|

| Minas Lupycal S.A. de C.V. |

|

|

Mexico |

|

|

100% |

|

| Minera Oro Silver de Mexico S.A. de C.V.

|

|

|

Mexico |

|

|

100% |

|

| Minera Plata Carina S.P.A. |

|

|

Chile |

|

|

100% |

|

| Oro Silver Resources Ltd. |

|

|

British Columbia, Canada |

|

|

100% |

|

| Endeavour Zilver S.A.R.L. |

|

|

Luxembourg |

|

|

100% |

|

| ITEM 3: |

GENERAL DEVELOPMENT OF THE BUSINESS

|

The Company is a Canadian mineral company engaged in the

evaluation, acquisition, exploration, development and exploitation of precious

metal properties in Mexico and Chile. The Company has three producing

silver-gold mines in Mexico: the Guanacevi Mine in Durango acquired in 2004, the

Bolañitos Mine in Guanajuato acquired in 2007 and the El Cubo Mine in Guanajuato

acquired in 2012. In addition to operating these three mines, the Company is

advancing three exploration and development projects in Mexico: the Terronera

property in Jalisco acquired in 2010 that is now in the pre-feasibility stage,

the permitted El Compas property and La Plata plant in Zacatecas acquired in

2016, and the prospective Parral properties in Chihuahua acquired in 2016.

2016

Equity Financings

Further to a short form base shelf prospectus filed by the

Company in July 2014 to qualify the distribution of up to Cdn$200 million of

common shares and various other securities of the Company and a corresponding

registration statement filed in the United States, the Company filed a

prospectus supplement in November 2015 for an at-the-market offering of up to

U.S.$16.5 million value of common shares of the Company on the New York Stock

Exchange through Cowen and Company, LLC acting as sole agent (the “2015 ATM

Offering”). During 2016, the Company sold under the 2015 ATM Offering 7,218,125

common shares at an average price of $2.13 per share for proceeds of $14.9

million, net of commission. Together with common shares sold in 2015, the

Company issued a total of 8,017,694 common shares under the 2015 ATM Offering

for net proceeds of $16.0 million.

5

Endeavour Silver Corp.

Further to a short form base shelf prospectus filed by the

Company in May 2016 to qualify the distribution of up to Cdn.$200 million of

common shares and various other securities of the Company and a corresponding

registration statement filed in the United States, the Company filed a

prospectus supplement in May 2016 for an at-the-market offering of up to U.S.$40

million value of common shares of the Company on the New York Stock Exchange

through Cowen and Company, LLC acting as sole agent (the “2016 ATM Offering”).

From launch to July 2016, the Company sold 10,245,347 common shares under the

2016 ATM Offering at an average price of $3.90 per share for proceeds of $38.9

million, net of commission. The Company will determine, at its sole discretion,

the timing and number of common shares of the Company to be further sold under

the 2016 ATM Offering.

Credit Facility Amendments

The Company had entered into a $75 million secured revolving

term credit facility (the “Credit Facility”) with The Bank of Nova Scotia

(“Scotiabank”) pursuant to a credit agreement made as of July 24, 2012. In 2013,

the Company extended the maturity of the Credit Facility from July 24, 2015

until July 24, 2016. Under the terms of the Credit Facility, the credit limit

available was reduced to $50 million on July 24, 2013 and, was further reduced

to $25 million on July 24, 2015. The Company entered into an amended and

restated credit agreement with Scotiabank, dated January 27, 2016, as amended by

a first amending agreement dated March 3, 2016, a second amending agreement

dated March 31, 2016 and a third amending agreement dated April 15, 2016

(collectively, the “Amended Credit Agreement”) whereby the Company and

Scotiabank agreed to the conversion of $22 million which was then outstanding

under the Credit Facility into a two-year term loan amortized quarterly and

expiring December 31, 2017. The Company repaid $3 million on signing of the

original Amended Credit Agreement and is to repay $2.5 million under the Amended

Credit Agreement each quarter. The interest rate margin on the Credit Facility

is 4.5% over LIBOR. The Credit Facility is principally secured by a pledge of

the Company’s equity interests in its material operating subsidiaries, including

Refinadora Plata Guanaceví SA de CV, Minas Bolañitos SA de CV and Compania

Minera del Cubo SA de CV. The Amended Credit Agreement contains a number of

covenants that impose financial or operating restrictions on the Company,

including a provision that “Tangible Net Worth of the Company” for the purposes

of the loan under the Amended Credit Agreement must be greater than U.S.$45.9

million. At December 31, 2016, the Company had $9 million outstanding under the

Credit Facility.

Acquisition of El Compas Project

On May 27, 2016, the Company issued 2,147,239 common shares of

the Company to Canarc Resource Corp. (“Canarc”) and assumed Canarc’s obligation

to pay an aggregate of 165 troy ounces of gold to Marlin Gold Mining Ltd. to

acquire a 100% interest in Canarc’s wholly-owned subsidiary, Oro Silver

Resources Ltd, which owned the El Compas project in Zacatecas, Mexico through

its wholly owned Mexican subsidiary, Minera Oro Silver de Mexico SA de CV

(“Minera Oro Silver”). The El Compas project consists of 28 concessions fully

permitted for mining with 22 concessions subject to a 1.5% net smelter return

royalty and six concessions subject to a 3.0% net smelter return royalty. Minera

Oro Silver also holds a five year operating lease, renewable for an additional

five years, on a 500 tpd ore processing plant located in Zacatecas, Mexico for a

total annual lease cost of MXN 1.6 million (approximately $90,000), adjusted

annually for inflation. The plant is currently not operational and will require

capital investment to restore to an operational state. Preliminary capital

investment estimates are $6.5 million to $7.5 million to recommence operations

at the plant. The Company and Carnac have a common director in Bradford Cooke.

6

Endeavour Silver Corp.

Acquisition of Parral Properties

On October 31, 2016, the Company issued 1,198,083 common shares

of the Company to Silver Standard Resources Inc. (“Silver Standard”) in

connection with the acquisition from Silver Standard of a 100% interest in the

Parral properties located in Chihuahua, Mexico. Under the terms of the Company’s

agreement with Silver Standard, the Company is to spend U.S.$2 million on

exploration over the two-year period following the closing date. On completing

this exploration expenditure, Endeavour will have one year to deliver a NI

43-101 technical report, including a resource estimate, and issue an additional

U.S.$200,000 in common shares of the Company to Silver Standard for each

1,000,000 ounces of silver delineated in measured and indicated resources on the

San Patricio and La Palmilla properties within the Parral properties, based on

the 10-day average closing price of Endeavour’s common shares on the New York

Stock Exchange prior to the earlier of delivery of the NI 43-101 report and

October 31, 2019.

2015

Equity Financing

In 2015, pursuant to the 2015 ATM Offering, the Company issued

799,569 common shares of the Company at an average price of $1.43 per share for

net proceeds of $1.1 million.

2014

Credit Facility Amendment

As mentioned under “2016 Developments-Credit Facility

Amendments”, the Credit Facility with Scotiabank was reduced to $25 million on

July 24, 2015.

| 3.2 |

Significant Acquisitions |

No significant acquisitions for which disclosure is required

under Part 8 of National Instrument 51-102 were completed by the Company during

its most recently completed financial year.

| ITEM 4: |

DESCRIPTION OF THE BUSINESS

|

Business of the Company

The Company’s principal business activities are the evaluation,

acquisition, exploration, development and exploitation of mineral properties.

The Company produces silver-gold from its underground mines at Guanacevi,

Bolañitos and El Cubo in Mexico. The Company also has interests in certain

exploration properties in Mexico and Chile.

Since 2002, the Company’s business strategy has been to focus

on acquiring advanced-stage silver mining properties in Mexico. Mexico, despite

its long and prolific history of metal production, appears to be relatively

under-explored using modern exploration techniques and offers promising

geological potential for precious metals exploration and production.

7

Endeavour Silver Corp.

The Company’s Guanaceví and Bolañitos mines acquired in 2004

and 2007, respectively, demonstrate its business model of acquiring fully built

and permitted silver mines that were about to close for lack of ore. By bringing

the money and expertise needed to find new silver ore-bodies, Endeavour

successfully re-opened and expanded these mines to develop their full potential.

In 2012, the Company acquired the El Cubo silver-gold mine which came with

substantial reserves and resources. The benefit of acquiring fully built and

permitted mining and milling infrastructure is that, if new exploration efforts

are successful, the mine development cycle from discovery to production only

takes a matter of months instead of the several years normally required in the

traditional mining business model.

In addition to operating the Guanaceví, Bolañitos and El Cubo

mines, the Company is advancing exploration and development of its Terronera, El

Compas and Parral properties located in Mexico. The Company is also exploring a

number of other properties towards achieving its goal to become a premier senior

producer in the silver mining sector.

The Company’s business is not materially affected by

intangibles such as licences, patents and trademarks, nor is it significantly

affected by seasonal changes. Other than as disclosed in this AIF, the Company

is not aware of any aspect of its business which may be affected in the current

financial year by renegotiation or termination of contracts.

Foreign Operations

As the Company’s producing mines and mineral exploration

interests are principally located in Mexico, the Company’s business is dependent

on foreign operations. As a developing economy, operating in Mexico has certain

risks. See “Risk Factors – Foreign Operations”.

Employees

As at December 31, 2016, the Company had approximately 14

employees based in its Vancouver corporate office and employed through its

Mexican subsidiaries approximately 1,627 full and part-time employees in Mexico.

Additional consultants are also retained from time to time for specific

corporate activities, development and exploration programs.

Environmental Protection

The Company’s environmental permit requires that it reclaim

certain land it disturbs during mining operations. Significant reclamation and

closure activities include land rehabilitation, decommissioning of buildings and

mine facilities, ongoing care and maintenance and other costs. Although the

ultimate amount of the reclamation and rehabilitation costs to be incurred

cannot be predicted with certainty, the total undiscounted amount of probability

weighted estimated cash flows required to settle the Company’s estimated

obligations is $2.1 million for the Guanacevi mine operations, $1.8 million for

the Bolañitos mine operations and $4.0 million for the El Cubo mine operations.

Community, Environmental and Corporate Safety Policies

Endeavour is focused on the improvement of sustainability

programs for all stakeholders and understands that such programs contribute to

the long-term benefit of the Company and society at large. Sustainability

programs implemented by the Company range from improving the Company’s safety

policies and practices; supporting health programs for the Company’s employees

and the local communities; enhancing environmental stewardship and reclamation;

sponsoring educational scholarships and job skills training programs; sponsoring

community cultural events and infrastructure improvements; and supporting

charitable causes.

8

Endeavour Silver Corp.

The Company’s ability to generate revenues and profits from its

mineral properties, or any other mineral property it may acquire, is dependent

upon a number of factors, including, without limitation, the following risk

factors.

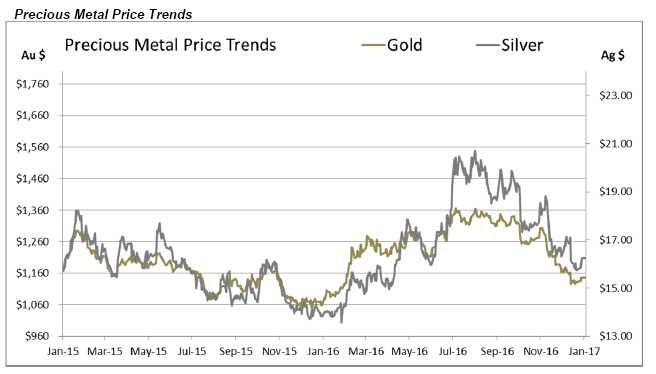

Precious and Base Metal Price Fluctuations

The profitability of the precious metal operations in which the

Company has an interest will be significantly affected by changes in the market

prices of precious metals. Prices for precious metals fluctuate on a daily

basis, have historically been subject to wide fluctuations and are affected by

numerous factors beyond the control of the Company such as the level of interest

rates, the rate of inflation, central bank transactions, world supply of the

precious metals, foreign currency exchange rates, international investments,

monetary systems, speculative activities, international economic conditions and

political developments. The exact effect of these factors cannot be accurately

predicted, but the combination of these factors may result in the Company not

receiving adequate returns on invested capital or the investments retaining

their respective values. Declining market prices for these metals could

materially adversely affect the Company’s operations and profitability.

Fluctuations in the price of consumed commodities

Prices and availability of commodities consumed or used in

connection with exploration, development and mining, such as natural gas,

diesel, oil, electricity, cyanide and other re-agents fluctuate and affect the

costs of production at our operations. These fluctuations can be unpredictable,

can occur over short periods of time and may have a materially adverse impact on

our operating costs or the timing and costs of various projects. Our general

policy is not to hedge our exposure to changes in prices of the commodities that

we use in our business.

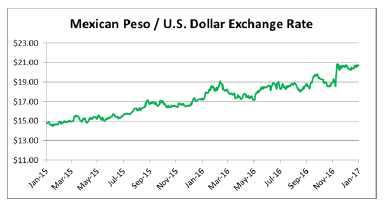

Foreign Exchange Rate Fluctuations

Operations

in Mexico and Canada are subject to foreign currency exchange fluctuations. The

Company raises its funds through equity issuances which are priced in Canadian

dollars, and the majority of the exploration costs of the Company are

denominated in United States dollars and Mexican pesos. The Company may suffer

losses due to adverse foreign currency fluctuations.

Competitive Conditions

Significant

competition exists for natural resource acquisition opportunities. As a result

of this competition, some of which is with large, well established mining

companies with substantial capabilities and significant financial and technical

resources, the Company may be unable to either compete for or acquire rights to

exploit additional attractive mining properties on terms it considers

acceptable. Accordingly, there can be no assurance that the Company will be able

to acquire any interest in additional projects that would yield reserves or

results for commercial mining operations.

Operating Hazards and Risks

Mining operations

generally involve a high degree of risk, which even a combination of experience,

knowledge and careful evaluation may not be able to overcome. These risks

include, but are not limited to, the following: environmental hazards,

industrial accidents, third party accidents, unusual or unexpected geological

structures or formations, fires, power outages, labour disruptions, floods,

explosions, cave-ins, land-slides, acts of God, periodic interruptions due to

inclement or hazardous weather conditions, earthquakes, war, rebellion,

revolution, delays in transportation, inaccessibility to property, restrictions

of courts and/or government authorities, other restrictive matters beyond the

reasonable control of the Company, and the inability to obtain suitable or

adequate machinery, equipment or labour and other risks involved in the

operation of mines.

9

Endeavour Silver Corp.

Operations in which the Company has a direct or indirect

interest will be subject to all the hazards and risks normally incidental to

exploration, development and production of precious and base metals, any of

which could result in work stoppages, delayed production and resultant losses,

increased production costs, asset write downs, damage to or destruction of mines

and other producing facilities, damage to life and property, environmental

damage and possible legal liability for any or all damages. The Company may

become subject to liability for pollution, cave-ins or hazards against which it

cannot insure or against which it may elect not to insure. Any compensation for

such liabilities may have a material, adverse effect on the Company’s financial

position.

Our property, business interruption and liability insurance may

not provide sufficient coverage for losses related to these or other hazards.

Insurance against certain risks, including certain liabilities for environmental

pollution, may not be available to us or to other companies within the industry

at reasonable terms or at all. In addition, our insurance coverage may not

continue to be available at economically feasible premiums, or at all. Any such

event could have a material adverse effect on our business.

Mining Operations

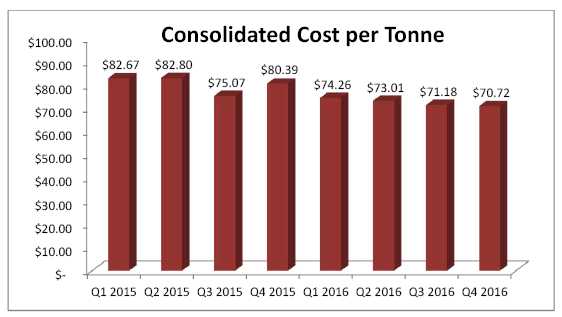

The capital costs required

by the Company’s projects may be significantly higher than anticipated. Capital

and operating costs, production and economic returns, and other estimates

contained in the Company’s current technical reports, may differ significantly

from those provided for in future studies and estimates and from management

guidance, and there can be no assurance that the Company’s actual capital and

operating costs will not be higher than currently anticipated. In addition,

delays to construction and exploration schedules may negatively impact the net

present value and internal rates of return of the Company’s mineral properties

as set forth in the applicable technical report. Similarly, there can be no

assurance that historical rates of production, grades of ore processed, rates of

recoveries or mining cash costs will not experience fluctuations or differ

significantly from current levels over the course of the mining operations

conducted by the Company.

In addition, there can be no assurance that the Company will be

able to continue to extend the production from its current operations through

exploration and drilling programs.

Infrastructure

Mining, processing,

development and exploration activities depend, to one degree or another, on

adequate infrastructure. Reliable roads, bridges, power sources and water supply

are important determinants, which affect capital and operating costs. The lack

of availability on acceptable terms or the delay in the availability of any one

or more of these items could prevent or delay exploitation or development of the

Company’s projects. If adequate infrastructure is not available in a timely

manner, there can be no assurance that the exploitation or development of the

Company’s projects will be commenced or completed on a timely basis, if at all;

the resulting operations will achieve the anticipated production volume, or the

construction costs and ongoing operating costs associated with the exploitation

and/or development of the Company’s advanced projects will not be higher than

anticipated. In addition, unusual or infrequent weather phenomena, sabotage,

government or other interference in the maintenance or provision of such

infrastructure could adversely affect the Company’s operations and

profitability.

Exploration and Development

There is no

assurance given by the Company that its exploration and development programs and

properties will result in the discovery, development or production of a

commercially viable ore body or yield new reserves to replace or expand current

reserves.

10

Endeavour Silver Corp.

The business of exploration for minerals and mining involves a

high degree of risk. Few properties that are explored are ultimately developed

into producing mines. At this time, other than the mineral reserves on the

Company’s Guanacevi Mines Project, Bolañitos Mines Project and El Cubo Mine,

none of the Company’s properties have any defined ore-bodies with proven

reserves.

The economics of developing silver, gold and other mineral

properties are affected by many factors including capital and operating costs,

variations of the tonnage and grade of ore mined, fluctuating mineral markets,

and such other factors as government regulations, including regulations relating

to royalties, allowable production, importing and exporting of minerals and

environmental protection. Depending on the prices of silver, gold or other

minerals produced, the Company may determine that it is impractical to commence

or continue commercial production.

Substantial expenditures are required to discover an ore-body,

to establish reserves, to identify the appropriate metallurgical processes to

extract metal from ore, and to develop the mining and processing facilities and

infrastructure. The marketability of any minerals acquired or discovered may be

affected by numerous factors which are beyond the Company’s control and which

cannot be accurately foreseen or predicted, such as market fluctuations,

conditions for precious and base metals, the proximity and capacity of milling

and smelting facilities, and such other factors as government regulations,

including regulations relating to royalties, allowable production, importing and

exporting minerals and environmental protection. In order to commence

exploitation of certain properties presently held under exploration concessions,

it is necessary for the Company to apply for an exploitation concession. There

can be no guarantee that such a concession will be granted. Unsuccessful

exploration or development programs could have a material adverse impact on the

Company’s operations and profitability.

Calculation of Reserves and Resources and Precious Metal

Recoveries

There is a degree of uncertainty attributable to the

calculation and estimation of reserves and resources and their corresponding

metal grades to be mined and recovered. Until reserves or resources are actually

mined and processed, the quantities of mineralization and metal grades must be

considered as estimates only. Any material change in the quantity of mineral

reserves, mineral resources, grades and recoveries may affect the economic

viability of the Company’s properties.

Decreases in the market price of silver or gold may

render the mining of reserves uneconomic.

The mineral resource and

reserve figures included in the AIF and the documents incorporated by reference

are estimates, which are, in part, based on forward-looking information, and no

assurance can be given that the indicated level of silver and gold will be

produced. Factors such as metal price fluctuations, increased production costs

and reduced recovery rates may render the present proven and probable reserves

unprofitable to develop at a particular site or sites for periods of time.

The NI 43-101 technical reports in respect of the Guanacevi

Mines, the Bolanitos Mines and the El Cubo Mine assume the following metal

prices: $16.29 per ounce for silver and $1,195 per ounce for gold. The Terronera

PEA assumes the following metal prices in the base case plan: $18 per ounce for

silver and $1,260 per ounce for gold. Mineral reserve and resource estimates

would be lower than estimated to the extent that actual metal prices are lower

than assumed.

11

Endeavour Silver Corp.

Replacement of Reserves and Resources

The

Guanaceví, Bolañitos and El Cubo mines are the Company’s only current sources of

mineral production. Current life-of-mine plans provide for a defined production

life for mining at the Company’s mines. The Bolañitos mine has an expected mine

life of less than two years based on current proven and probable reserves and

production levels. If the Company’s mineral reserves and resources are not

replaced either by the development or discovery of additional reserves and/or

extension of the life-of-mine at its current operating mines or through the

acquisition or development of an additional producing mine, this could have an

adverse impact on the Company’s future cash flows, earnings, financial

performance and financial condition, including as a result of requirements to

expend funds for reclamation and decommissioning.

Acquisition Strategy

As part of the Company’s

business strategy, it has sought and will continue to seek new mining and

development opportunities in the mining industry. In pursuit of such

opportunities, it may fail to select appropriate acquisition candidates,

negotiate appropriate acquisition terms, conduct sufficient due diligence to

determine all related liabilities or to negotiate favourable financing terms.

The Company may encounter difficulties in transitioning the business, including

issues with the integration of the acquired businesses or its personnel into the

Company. The Company cannot assure that it can complete any acquisition or

business arrangement that it pursues, or is pursuing, on favourable terms, or

that any acquisitions or business arrangements completed will ultimately benefit

its business.

Integration of New Acquisitions

The Company’s

success at completing any acquisitions will depend on a number of factors,

including, but not limited to: identifying acquisitions which fit the Company’s

strategy; negotiating acceptable terms with the seller of the business or

property to be acquired; and obtaining approval from regulatory authorities in

the jurisdictions of the business or property to be acquired.

The positive effect on the Company’s results arising from past

and future acquisitions will depend on a variety of factors, including, but not

limited to: assimilating the operations of an acquired business or property in a

timely and efficient manner including the existing work force, union

arrangements and existing contracts; maintaining the Company’s financial and

strategic focus while integrating the acquired business or property;

implementing uniform standards, controls, procedures and policies at the

acquired business, as appropriate; and to the extent that the Company makes an

acquisition outside of markets in which it has previously operated, conducting

and managing operations in a new operating environment and under a new

regulatory regime where it has no direct experience.

Past and future business or property acquisitions could place

increased pressure on the Company’s cash flow if such acquisitions involve cash

consideration or the assumption of obligations requiring cash payments. The

integration of the Company’s existing operations with any acquired business will

require significant expenditures of time, attention and funds. Achievement of

the benefits expected from consolidation would require the Company to incur

significant costs in connection with, among other things, implementing financial

and planning systems. The Company may not be able to integrate the operations of

a recently acquired business or restructure the Company’s previously existing

business operations without encountering difficulties and delays. In addition,

this integration may require significant attention from the Company’s management

team, which may detract attention from the Company’s day-to-day operations. Over

the short-term, difficulties associated with integration could have a material

adverse effect on the Company’s business, operating results, financial condition

and the price of the Company’s common shares. In addition, the acquisition of

mineral properties may subject the Company to unforeseen liabilities, including

environmental liabilities.

12

Endeavour Silver Corp.

Foreign Operations

The Company’s operations

are currently conducted through subsidiaries principally in Mexico and, as such,

its operations are exposed to various levels of political, economic and other

risks and uncertainties which could result in work stoppages, blockades of the

Company’s mining operations and appropriation of assets. Some of the Company’s

operations are located in areas where Mexican drug cartels operate. These risks

and uncertainties vary from region to region and include, but are not limited

to, terrorism; hostage taking; local drug gang activities; military repression;

expropriation; extreme fluctuations in currency exchange rates; high rates of

inflation; labour unrest; the risks of war or civil unrest; renegotiation or

nullification of existing concessions, licenses, permits and contracts; illegal

mining; changes in taxation policies; restrictions on foreign exchange and

repatriation; and changing political conditions, currency controls and

governmental regulations that favour or require the awarding of contracts to

local contractors or require foreign contractors to employ citizens of, or

purchase supplies from, a particular jurisdiction.

Local opposition to mine development projects could arise in

Mexico, and such opposition could be violent. There can be no assurance that

such local opposition will not arise with respect to the Company’s Mexican

operations. If the Company were to experience resistance or unrest in connection

with its Mexican operations, it could have a material adverse effect on its

operations and profitability. To the extent the Company acquires mineral

properties in jurisdictions other than Mexico, it may be subject to similar and

additional risks with respect to its operations in those jurisdictions.

Government Regulation

The Company’s

operations, exploration and development activities are subject to extensive

foreign federal, state and local laws and regulations governing such matters as

environmental protection, management and use of toxic substances and explosives,

management of natural resources, health, exploration and development of mines,

production and post-closure reclamation, safety and labour, mining law reform,

price controls import and export laws, taxation, maintenance of claims, tenure,

government royalties and expropriation of property. There is no assurance that

future changes in such regulation, if any, will not adversely affect the

Company’s operations. The activities of the Company require licenses and permits

from various governmental authorities.

The costs associated with compliance with these laws and

regulations are substantial and possible future laws and regulations, changes to

existing laws and regulations and more stringent enforcement of current laws and

regulations by governmental authorities, could cause additional expenses,

capital expenditures, restrictions on or suspensions of the Company’s operations

and delays in the development of its properties. Moreover, these laws and

regulations may allow governmental authorities and private parties to bring

lawsuits based upon damages to property and injury to persons resulting from the

environmental, health and safety practices of the Company’s past and current

operations, or possibly even those actions of parties from whom the Company

acquired its mines or properties, and could lead to the imposition of

substantial fines, penalties or other civil or criminal sanctions. The Company

retains competent and well trained individuals and consultants in jurisdictions

in which it does business, however, even with the application of considerable

skill the Company may inadvertently fail to comply with certain laws. Such

events can lead to financial restatements, fines, penalties, and other material

negative impacts on the Company.

Mexican Foreign Investment and Income Tax Laws

In December 2012, the Mexican government amended federal labour laws

with respect to the use of service companies, subcontracting arrangements and

the obligation to compensate employees with appropriate profit-sharing in

Mexico. While the Company believes it is probable that these amended labour laws

will not result in any material obligation or additional profit-sharing

entitlements for its Mexican employees, there can be no assurance that this will

continue to be the case.

Any developments or changes in such legal, regulatory or

governmental requirements as described above or otherwise are beyond the control

of the Company and may adversely affect its business.

13

Endeavour Silver Corp.

Mexican Tax Assessments

As disclosed under

“Item 11: Legal Proceedings”, a subsidiary of the Company in Mexico has received

a tax assessment from Mexican fiscal authorities. The Company filed an appeal

against the June 2016 tax assessment on the basis certain items rejected by the

courts were included in the new tax assessment, while a number of deficiencies

exist within the assessment. If the Company is unsuccessful, this could

negatively impact the Company’s financial position and create difficulties for

the Company in dealing with Mexican fiscal authorities in the future.

Included in the Company’s consolidated financial statements,

are net assets of $595,000, including $42,000 in cash, held by MSCG. Following

the Tax Court’s rulings, MSCG is in discussions with the tax authorities with

regards to the shortfall of assets within MSCG to settle its estimated tax

liability. An alternative settlement option would be to transfer the shares and

assets of MSCG to the tax authorities. As of December 31, 2016, the Company

recognized an allowance for transferring the shares and assets of MSCG amounting

to $595,000. The Company is currently assessing MSCG’s settlement options based

on on-going court proceedings and discussion with the tax authorities.

Obtaining and Renewing of Government Permits

In the ordinary course of business, the Company is required to

obtain and renew government permits for the operation and expansion of existing

operations or for the development, construction and commencement of new

operations. Obtaining or renewing the necessary governmental permits is a

complex and time-consuming process involving numerous jurisdictions and possibly

involving public hearings and costly undertakings on the Company’s part. The

duration and success of the Company’s efforts to obtain and renew permits are

contingent upon many variables not within its control including the

interpretation of applicable requirements implemented by the permitting

authority.

The Company may not be able to obtain or renew permits that are

necessary to its operations, or the cost to obtain or renew permits may exceed

what the Company believes it can recover from a given property once in

production. Any unexpected delays or costs associated with the permitting

process could delay the development or impede the operation of a mine, which

could adversely impact the Company’s operations and profitability.

Environmental Factors

All phases of the

Company’s operations are subject to environmental regulation in the various

jurisdictions in which it operates. Environmental legislation is evolving in a

manner which will require stricter standards and enforcement, increased fines

and penalties for non-compliance, more stringent environmental assessments of

proposed projects and a heightened degree of responsibility for companies and

their officers, directors and employees. There is no assurance that any future

changes in environmental regulation will not adversely affect the Company’s

operations. The costs of compliance with changes in government regulations have

the potential to reduce the profitability of future operations. Environmental

hazards that may have been caused by previous or existing owners or operators

may exist on the Company’s mineral properties, but are unknown to the Company at

present.

14

Endeavour Silver Corp.

Title to Assets

Although the Company has or

will receive title opinions for any properties in which it has a material

interest, there is no guarantee that title to such properties will not be

challenged or impugned. The Company has not conducted surveys of the claims in

which it holds direct or indirect interests and, therefore, the precise area and

location of such claims may be in doubt. The Company’s claims may be subject to

prior unregistered agreements or transfers or native land claims and title may

be affected by unidentified or unknown defects.

The Company has conducted as thorough an investigation as

possible on the title of properties that it has acquired or will be acquiring to

be certain that there are no other claims or agreements that could affect its

title to the concessions or claims. If title to the Company’s properties is

disputed, it may result in the Company paying substantial costs to settle the

dispute or clear title and could result in the loss of the property, which

events may affect the economic viability of the Company.

Employee Recruitment and Retention

Recruiting

and retaining qualified personnel is critical to the Company’s success. The

Company is dependent on the services of key executives including the Company’s

President and Chief Executive Officer and other highly skilled and experienced

executives and personnel focused on managing the Company’s interests. The number

of persons skilled in acquisition, exploration, development and operation of

mining properties are limited and competition for such persons is intense. As

the Company’s business activity grows, the Company will require additional key

financial, administrative and mining personnel as well as additional operations

staff. We could experience increases in our recruiting and training costs and

decreases in our operating efficiency, productivity and profit margins. If we

are not able to attract, hire and retain qualified personnel, the efficiency of

our operations could be impaired, which could have an adverse impact on the

Company’s future cash flows, earnings, financial performance and financial

condition.

Potential Conflicts of Interest

The directors

and officers of the Company may serve as directors and/or officers of other

public and private companies, and may devote a portion of their time to manage

other business interests. This may result in certain conflicts of interest.

To the extent that such other companies may participate in

ventures in which the Company is also participating, such directors and officers

of the Company may have a conflict of interest in negotiating and reaching an

agreement with respect to the extent of each company’s participation. The laws

of British Columbia, Canada, require the directors and officers to act honestly,

in good faith, and in the best interests of the Company and its shareholders.

However, in conflict of interest situations, directors and officers of the

Company may owe the same duty to another company and will need to balance the

competing obligations and liabilities of their actions.

There is no assurance that the needs of the Company will

receive priority in all cases. From time to time, several companies may

participate together in the acquisition, exploration and development of natural

resource properties, thereby allowing these companies to: (i) participate in

larger properties and programs; (ii) acquire an interest in a greater number of

properties and programs; and (iii) reduce their financial exposure to any one

property or program. A particular company may assign, at its cost, all or a

portion of its interests in a particular program to another affiliated company

due to the financial position of the company making the assignment.

In determining whether or not the Company will participate in a

particular program and the interest therein to be acquired by it, it is expected

that the directors and officers of the Company will primarily consider the

degree of risk to which the Company may be exposed and its financial position at

that time.

15

Endeavour Silver Corp.

Third Party Reliance

The Company’s rights to

acquire interests in certain mineral properties have been granted by third

parties who themselves may hold only an option to acquire such properties. As a

result, the Company may have no direct contractual relationship with the

underlying property holder.

Absolute Assurance on Financial Statements

We

prepare our financial reports in accordance with accounting policies and methods

prescribed by IFRS. In the preparation of financial reports, management may need

to rely upon assumptions, make estimates or use their best judgment in

determining the financial condition or results of operations of the Company.

Significant accounting details are described in more detail in the notes to our

annual consolidated financial statements for the year ended December 31, 2016.

In order to have a reasonable level of assurance that financial transactions are

properly authorized, assets are safeguarded against unauthorized or improper use

and transactions are properly recorded and reported, we have implemented and

continue to analyze our internal control systems for financial reporting.

Although we believe our financial reporting and financial statements are

prepared with reasonable safeguards to ensure reliability, we cannot provide

absolute assurance in that regard.

General Economic Conditions

The volatile

global economic environment has created market uncertainty and volatility in

recent years. Instability in the market for metal commodities has been

experienced since April 2013, and continues today. These macro-economic events

negatively affected the mining and minerals sectors in general, and the

Company’s market capitalization has been significantly reduced in periods of

market instabilities. Any sudden or rapid destabilization of global economic

conditions could impact the Company's ability to obtain equity or debt financing

in the future on terms favorable to the Company or at all. In such an event, the

Company's operations and financial condition could be adversely impacted.

The Company assesses on a quarterly basis the carrying values

of its mineral properties. Should market conditions and commodity prices worsen

and persist in a worsened state for a prolonged period of time, an impairment of

the Company’s mineral properties may be required.

Substantial Volatility of Share Price

The

market prices for the securities of mining companies, including our own, have

historically been highly volatile. The market has from time to time experienced

significant price and volume fluctuations that are unrelated to the operating

performance of any particular company. In addition, because of the nature of our

business, certain factors such as our announcements and the public’s reaction,

our operating performance and the performance of competitors and other similar

companies, fluctuations in the market prices of our resources, government

regulations, changes in earnings estimates or recommendations by research

analysts who track our securities or securities of other companies in the

resource sector, general market conditions, announcements relating to

litigation, the arrival or departure of key personnel and the risk factors

described in this AIF can have an adverse impact on the market price of the

Common Shares.

Any negative change in the public’s perception of

Endeavour’s prospects could cause the price of our securities, including the

price of our Common Shares, to decrease dramatically. Furthermore, any negative

change in the public’s perception of the prospects of mining companies in

general could depress the price of our securities, including the price of our

Common Shares, regardless of our results. Following declines in the market price

of a company’s securities, securities class-action litigation is often

instituted. Litigation of this type, if instituted, could result in substantial

costs and a diversion of our management’s attention and resources.

16

Endeavour Silver Corp.

Need for additional financing

The Company’s

current cash and cash-flows may not be sufficient to pursue additional

exploration, development or discovery of additional reserves, extension to

life-of-mines or new acquisitions and, therefore, the Company may require

additional financing. Additional financing may not be available on acceptable

terms, if at all. The Company may need additional financing by way of private or

public offerings of equity or debt or the sale of project or property interests

in order to have sufficient working capital for its business objectives, as well

as for general working capital purposes.

The success and the pricing of any such capital raising and/or

debt financing will be dependent upon the prevailing market conditions at that

time. There can be no assurance that financing will be available to the Company

or, if it is available, that it will be offered on acceptable terms. If

additional financing is raised through the issuance of equity or convertible

debt securities of the Company, this may negatively impact the price of the

Common Shares and could result in dilution to shareholders and the interests of

shareholders in the net assets of the Company may be diluted.

Differences in U.S. and Canadian reporting of mineral

reserves and resources

The Company’s mineral reserve and resource

estimates are not directly comparable to those made in filings subject to SEC

reporting and disclosure requirements as the Company generally reports mineral

reserves and resources in accordance with Canadian practices. These practices

are different from those used to report mineral reserve and resource estimates

in reports and other materials filed with the SEC. It is Canadian practice to

report measured, indicated and inferred resources, which are not permitted in

disclosure filed with the SEC by United States issuers. Under SEC rules,

mineralization may not be classified as a "reserve" unless the determination has

been made that the mineralization could be economically and legally produced or

extracted at the time the reserve determination is made. United States investors

are cautioned not to assume that all or any part of measured or indicated

resources will ever be converted into reserves.

Further, "inferred mineral resources" have a great amount of

uncertainty as to their existence and as to whether they can be mined legally or

economically. Disclosure of "contained ounces" is permitted disclosure under

Canadian regulations; however, the SEC only permits issuers to report

mineralization that does not constitute “reserves” by SEC Industry Guide 7

standards "as in-place tonnage and grade without reference to unit of metal

measures.

Accordingly, information concerning descriptions of

mineralization, reserves and resources contained in this AIF, or in the

documents incorporated herein by reference, may not be comparable to information

made public by United States companies subject to the reporting and disclosure

requirements of the SEC.

Material weaknesses in the internal control over

financial reporting

The Company documented and tested, during its

most recent fiscal year, its internal control procedures in order to satisfy the

requirements of Section 404 of the U.S. Sarbanes-Oxley Act (“SOX”)

requires an annual assessment by management of the effectiveness of the

Company’s internal control over financial reporting and an attestation report by

the independent auditor addressing this assessment. The Company may fail to

achieve and maintain the adequacy of its internal control over financial

reporting as such standards are modified, supplemented, or amended from time to

time, and the Company may not be able to ensure that it can conclude on an

ongoing basis that it has effective internal control over financial reporting in

accordance with Section 404 of SOX. The Company’s failure to satisfy the

requirements of Section 404 of SOX on an ongoing, timely basis could result in

the loss of investor confidence in the reliability of the Company’s financial

statements, which in turn could harm the business and negatively affect the

trading price of the Common Shares. In addition, any failure to implement

required new or improved controls, or difficulties encountered in their

implementation, could harm the Company’s operating results or cause us to fail

to meet reporting obligations.

17

Endeavour Silver Corp.

Future acquisitions of companies may also provide the Company

with challenges in implementing the required processes, procedures and controls

in its acquired operations. Acquired companies may not have disclosure controls

and procedures or internal control over financial reporting that are as thorough

or effective as those required by securities laws currently applicable the

Company.

No evaluation can provide complete assurance that the internal

control over financial reporting will detect or uncover all failures of persons

within the Company to disclose material information required to be reported. The

effectiveness of the Company’s controls and procedures could also be limited by

simple errors or faulty judgments. In addition, as the Company expands, the

challenges involved in implementing appropriate internal control over financial

reporting will increase and will require that it continue to improve the

internal control over financial reporting. Although the Company intends to

devote substantial time and incur substantial costs, as necessary, to ensure

ongoing compliance, it cannot be certain that it will be successful in complying

with Section 404 of SOX.

Credit Facility with Scotiabank

The Company’s

Credit Facility with Scotiabank requires the Company to make certain interest

payments, provide a first-ranking security interest over all of its assets and

also contains a number of covenants that impose significant operating and

financial restrictions on the Company and may limit the Company’s ability to

engage in acts that may be in its long-term best interest.

If the Company’s cash flows and cash and cash equivalents are

insufficient to fund its debt service obligations, including repayment or

renewal of the Credit Facility at the end of its term, the Company could face

liquidity problems and could be forced to seek amendments to the Credit

Facility, or reduce or delay investments and capital expenditures, dispose of

material assets or operations, seek additional debt or equity capital or

restructure or refinance the Company’s indebtedness, including the Credit

Facility. The Company may not be able to affect any such alternative measures on

commercially reasonable terms or at all and, even if successful, those

alternatives may not allow the Company to meet its scheduled debt service

obligations. There can be no certainty that the Company will be able to repay or

renew the Credit Facility at maturity and the failure to do so would have a

material adverse effect on the Company.

In addition, a breach of the covenants under the Credit

Facility could result in an event of default under the applicable indebtedness.

Such a default may allow the creditors to accelerate the related debt, and may

result in the acceleration of any other debt to which a cross acceleration or

cross default provision applies. In the event a lender accelerates the repayment

of the Company’s borrowings, the Company may not have sufficient assets to repay

its indebtedness. The security interests provided by the Company under the

Credit Facility may adversely affect the Company’s ability to secure other types

of financing. As a result of the security interests granted to Scotiabank, any

default under the Credit Facility, including any covenants thereunder, could

result in the loss of the Company’s entire interest in its material assets.

Lack of Dividends

The Company has never

declared or paid any dividends on the Common Shares. So long as the Company’s

Amended Credit Agreement with Scotiabank and related security documentation are

in effect, the Company is restricted from declaring and paying any dividends.

Endeavour otherwise intends, for the foreseeable future, to retain its future

earnings, if any, to finance its exploration activities and further development

and the expansion of the business. The payment of future dividends, if any, will

be reviewed periodically by the Board of Directors of Endeavour and will depend

upon, among other things, conditions then existing including earnings, financial

conditions, cash on hand, financial requirements to fund our exploration

activities, development and growth, and other factors that the Board may

consider appropriate in the circumstances.

18

Endeavour Silver Corp.

Claims Under U.S. Securities Laws

The

enforcement by investors of civil liabilities under the federal securities laws

of the United States may be affected adversely by the fact that the Company is

incorporated under the laws of British Columbia, Canada, that the independent

chartered public accountants who have audited the Company’s financial statements

and some or all of the Company’s directors and officers may be residents of

Canada or elsewhere, and that all or a substantial portion of the Company’s

assets and said persons are located outside the United States. As a result, it

may be difficult for holders of the Company’s common shares to effect service of

process within the United States upon people who are not residents of the United

States or to realize in the United States upon judgments of courts of the United

States predicated upon civil liabilities under the federal securities laws of

the United States

Financial Instruments

From time to time, the

Company may use certain financial instruments to manage the risks associated

with changes in silver prices, interest rates and foreign currency exchange

rates. The use of financial instruments involves certain inherent risks

including, among other things: (i) credit risk, the risk of default on amounts

owing to the Company by the counterparties with which Company has entered into

such transaction; (ii) market liquidity risk, the risk that the Company has

entered into a position that cannot be closed out quickly, either by liquidating

such financial instrument or by establishing an offsetting position; and (iii)

unrealized mark-to-market risk, the risk that, in respect of certain financial

instruments, an adverse change in market prices for commodities, currencies or

interest rates will result in the Company incurring an unrealized mark-to-market

loss in respect of such derivative products.

Financial Reporting Standards

The Company

prepares its financial reports in accordance with IFRS. In preparation of

financial reports, management may need to rely upon assumptions, make estimates

or use their best judgment in determining the financial condition of the

Company. Significant accounting policies are described in more detail in the

Company’s audited financial statements. In order to have a reasonable level of

assurance that financial transactions are properly authorized, assets are

safeguarded against unauthorized or improper use, and transactions are properly

recorded and reported, the Company has implemented and continues to analyze its

internal control systems for financial reporting. Although the Company believes

its financial reporting and financial statements are prepared with reasonable

safeguards to ensure reliability, the Company cannot provide absolute assurance.

Information Systems and Cyber Security

Our

operations depend, in part, upon information technology systems. Our information

technology systems are subject to disruption, damage or failure from a number of

sources, including, but not limited to, hacking, computer viruses, security

breaches, natural disasters, power loss, vandalism, theft and defects in design.

Any of these and other events could result in information technology systems

failures, operational delays, production downtimes, destruction or corruption of

data, security breaches or other manipulation or improper use of our data,

systems and networks, any of which could have adverse effects on our reputation,

business, results of operations, financial condition and share price.

Our risk and exposure to these matters cannot be fully

mitigated because of, among other things, the evolving nature of these threats.

As a result, cyber security and the continued development and enhancement of

controls, processes and practices designed to protect our systems, computers,

software, data and networks from attack, damage or unauthorized access remain a

priority. As cyber threats continue to evolve, we may be required to expend

additional resources to continue to modify or enhance protective measures or to

investigate and remediate any security vulnerabilities.

19

Endeavour Silver Corp.

| 4.3 |

Asset-Backed Securities

Outstanding |

The Company has not issued any asset-backed securities.

Summary of Mineral Reserves and Mineral Resources

Estimates

The following tables summarize as at December 31, 2016 the

Company’s estimated Mineral Reserves and Mineral Resources on its material

mineral properties, all of which are wholly owned. Information in the following

tables and the notes thereto are extracted from the respective technical reports

on the material properties referred to under the description of each property

below.

| Silver-Gold Reserves & Resources (as of December 31,

2016) |

| Reserves |

Tonnes |

Ag g/t |

Au g/t |

Ag oz |

Au oz |

| Guanaceví |

87,000 |

247 |

0.49 |

686,200 |

1,400 |

| Bolanitos |

157,000 |

90 |

2.84 |

456,700 |

14,300 |

| El Cubo |

409,000 |

154

|

1.99 |

2,028,900 |

26,200 |

| Total Proven |

653,000 |

151 |

2.00 |

3,171,800 |

41,900 |

| Guanacevi |

508,000 |

262 |

0.64 |

4,285,200 |

10,500 |

| Bolanitos |

238,000 |

104 |

1.81 |

798,300 |

13,800 |

| El Cubo |

453,000 |

159

|

1.71 |

2,311,100 |

24,900 |

| Total Probable |

1,199,000 |

192 |

1.28 |

7,394,600 |

49,200 |

| Total Proven

& Probable |

1,852,000 |

177 |

1.53 |

10,566,400 |

91,100 |

| Resources |

Tonnes

|

Ag g/t

|

Au g/t

|

Ag oz |

Au oz

|

| Guanaceví |

69,000 |

248 |

0.47 |