Exhibit 99.1

![]()

ANNUAL INFORMATION FORM

March 29, 2019

MAG Silver Corp.

Suite 770 – 800 West Pender Street

Vancouver, BC, Canada V6C 2V6

An copy of this Annual Information Form for the

year ended December 31, 2018 may be obtained upon request

from the Corporate Secretary of MAG Silver Corp. at the above

address or from the company’s web site:

www.magsilver.com

Table of Contents

| INTRODUCTORY NOTES | 3 |

| Date of Information | 3 |

| Cautionary Statement on Forward-Looking Information | 3 |

| Currency and Exchange Rates | 7 |

| Metric Equivalents | 8 |

| Financial Data in this AIF | 8 |

| Defined Terms | 8 |

| Cautionary Statement Regarding Non-IFRS Measures | 8 |

| CORPORATE STRUCTURE | 8 |

| Intercorporate Relationships | 9 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 10 |

| Three Year History | 11 |

| DESCRIPTION OF THE BUSINESS | 16 |

| General | 16 |

| Principal Markets | 17 |

| Adjacent Property Disclosure | 17 |

| Cautionary Note to Investors Concerning Estimates of Mineral Resources | 17 |

| Technical Information | 18 |

| Passive Foreign Investment Company | 18 |

| Employees | 18 |

| Competitive Conditions | 18 |

| Economic Dependence | 18 |

| CARRYING ON BUSINESS IN MEXICO | 19 |

| RISK FACTORS | 23 |

| MINERAL PROJECTS | 45 |

| Cinco de Mayo Property | 63 |

| DIVIDENDS | 64 |

| DESCRIPTION OF CAPITAL STRUCTURE | 64 |

| Common Shares | 64 |

| Shareholder Rights Plan | 64 |

| MARKET FOR SECURITIES | 64 |

| Trading Price and Volume | 64 |

| Prior Sales | 65 |

| DIRECTORS AND OFFICERS | 66 |

| Name, Occupation and Security Holding as at March 25, 2019 | 66 |

| Cease trade orders, bankruptcies, penalties or sanctions | 69 |

| Conflicts of Interest | 70 |

| Audit Committee | 71 |

| Compensation Committee | 73 |

| Corporate Governance and Nomination Committee | 73 |

| Disclosure Committee | 73 |

| Health, Safety, Environmental, Community Committee | 74 |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 74 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 74 |

| TRANSFER AGENTS AND REGISTRARS | 75 |

| MATERIAL CONTRACTS | 75 |

| INTERESTS OF EXPERTS | 76 |

| ADDITIONAL INFORMATION | 76 |

| Schedule “A” | 77 |

| Schedule “B” | 83 |

2

INTRODUCTORY NOTES

In this Annual Information Form (“AIF”), unless the context otherwise dictates, “we”, “MAG” or the “Company” refers to MAG Silver Corp. and its subsidiaries.

Date of Information

All information in this AIF is as of December 31, 2018 unless otherwise indicated.

Documents Incorporated By Reference

The information provided in this AIF is supplemented by disclosure contained in the documents listed below which are incorporated by reference into this AIF. These documents must be read together with this AIF. The documents listed below are not contained within, nor attached to this document. The documents may be accessed by the reader at the following locations:

|

Type of Document

|

Effective Date / Period Ended

|

Date Filed / Posted

|

Document name which may be viewed at the SEDAR website at www.sedar.com

|

| MAG Silver Juanicipio NI 43-101 Technical Report (Amended and Restated), Zacatecas State, Mexico | October 21, 2017 (Amended January 19, 2018) | January 19, 2018 |

Amended and Restated Technical Report (43-101) – English

Qualification Certificate(s) and Consent(s) |

Cautionary Statement on Forward-Looking Information

This AIF and the documents incorporated by reference herein contain forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of Canadian securities laws. Such forward-looking statements and information include, but are not limited to:

| • | the future price of silver, gold, lead, zinc and copper; |

| • | the estimation of mineral resources; |

| • | preliminary economic estimates relating to the Juanicipio Project (as defined herein); |

| • | estimates of the time and amount of future silver, gold, lead, zinc and copper production for specific operations; |

| • | estimated future exploration and development expenditures and other expenses for specific operations; |

| • | permitting timelines; |

| • | the Company’s expectations regarding impairments of mineral properties; |

| • | the expected timeline for the Feasibility Study (as defined herein) and expected differences in approach, recommendations and conclusions of the Feasibility Study as compared to the 2017 PEA; |

| • | the anticipated timing of a formal ‘production decision’ at Minera Juanicipio (as defined herein); |

| • | the expected timeline to production at the Juanicipio Project publicly reported by Fresnillo; |

3

| • | the Company’s expectations regarding the sufficiency of its capital resources and requirements for additional capital; |

| • | litigation risks; |

| • | currency fluctuations; |

| • | environmental risks and reclamation cost; and |

| • | changes to governmental laws and regulations. |

When used in this AIF, any statements that express or involve discussions with respect to predictions, beliefs, plans, projections, objectives, assumptions or future events of performance (often but not always using words or phrases such as “anticipate”, “believe”, “estimate”, “expect”, “intend”, “plan”, “strategy”, “goals”, “objectives”, “project”, “potential” or variations thereof or stating that certain actions, events, or results “may”, “could”, “would”, “might” or “will” be taken, occur, or be achieved, or the negative of any of these terms and similar expressions), as they relate to the Company or management, are intended to identify forward-looking statements and information. Such statements reflect the Company’s current views with respect to future events and are subject to certain known and unknown risks, uncertainties and assumptions.

Many factors could cause actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements and information, including, among others:

| · | the potential for no commercially mineable deposits due to the speculative nature of the Company’s business; |

| · | none of the properties in which the Company has an interest having any mineral reserves; |

| · | the Company’s has properties in the exploration stage, and most exploration projects do not result in commercially mineable deposits; |

| · | estimates of mineral resources being based on interpretation and assumptions which are inherently imprecise; |

| · | no guarantee of surface rights for the Company’s mineral properties; |

| · | no guarantee of the Company’s ability to obtain all necessary licenses and permits that may be required to carry out exploration and development of its mineral properties and business activities; |

| · | risks related to the properties in which the Company has an interest being located in foreign jurisdictions, including Mexico, which may be subject to political instability, governmental relations and increased police and military enforcement action against criminal activities; |

| · | the effect of global economic and political instability on the Company’s business; |

4

| · | risks related to maintaining a positive relationship with the communities in which the Company operates; |

| · | risks related to the Company’s ability to finance substantial expenditures required for commercial operations on its mineral properties; |

| · | the Company’s history of losses and no revenues from operations; |

| · | risks related to the Company’s ability to arrange additional financing, and possible loss of the Company’s interests in its properties due to a lack of adequate funding; |

| · | risks related to the Juanicipio Project; |

| · | risks related to access and availability of infrastructure, power and water; |

| · | risks related to ground water levels at the Juanicipio Project; |

| · | risks related to a lack of access to a skilled workforce; |

| · | risks related to the Juanicipio Project mine plan and mine design and the contemplated development timeline to production; |

| · | risks relating to the capital requirements for the Juanicipio Project and the timeline to production; |

| · | risks related to the conclusions and recommendations of the Feasibility Study (as defined herein); |

| · | risks related to the Feasibility Study’s impact on the Juanicipio Project mine plan and mine design; |

| · | risks related to the Company’s decision to participate in the development of the Juanicipio Project upon a production decision; |

| · | risks related to title, challenge to title, or potential title disputes regarding the Company’s mineral properties; |

| · | risks related to the Company being a minority shareholder of Minera Juanicipio; |

| · | risks related to disputes with joint venture partners; |

| · | risks related to the influence of the Company’s significant shareholders over the direction of the Company’s business; |

| · | the potential for legal proceedings to be brought against the Company; |

| · | risks related to environmental regulations; |

| · | the highly competitive nature of mineral exploration industry; |

| · | risks related to equipment shortages, access restrictions and lack of infrastructure on the Company’s mineral properties; |

5

| · | the Company’s dependence upon key personnel, some of whom may not have entered into written agreements with the Company, and other qualified management; |

| · | the Company’s dependence on certain related party service providers (Minera Cascabel S.A. de C.V. (“Cascabel”) and IMDEX Inc. (“IMDEX”)) to supervise operations in Mexico; |

| · | the Company’s dependence on Fresnillo plc (“Fresnillo”) to attract, train and retain qualified personnel; |

| · | risks related to directors being, or becoming, associated with other natural resource companies which may give rise to conflicts of interest; |

| · | currency fluctuations (particularly the C$/U.S.$ and U.S.$/Mexican Peso exchange rates) and inflationary pressures; |

| · | risks related to mining operations generally; |

| · | risks related to fluctuation of mineral prices and marketability; |

| · | the Company being subject to anti-corruption laws, human rights laws, Mexican foreign investment laws, income tax laws and Mexican laws; |

| · | the Company being subject to Canadian disclosure practices concerning its mineral resources which allow for more disclosure than is permitted for domestic U.S. reporting companies; |

| · | risks related to maintaining adequate internal control over financial reporting; |

| · | funding and property commitments that may result in dilution to the Company’s shareholders; |

| · | the volatility of the price of the Company’s Common Shares; |

| · | the uncertainty of maintaining a liquid trading market for the Company’s Common Shares; |

| · | the Company being a “passive foreign investment company” which may have adverse U.S. federal income tax consequences for U.S. shareholders; |

| · | the difficulty of U.S. litigants effecting service of process or enforcing any judgments against the Company, as the Company, its principals and assets are located outside of the United States; |

| · | all of the Company’s mineral property assets being located outside of Canada; |

| · | risks related to the decrease of the market price of the Common Shares if the Company’s shareholders sell substantial amounts of Common Shares; |

| · | risks related to dilution to existing shareholders if stock options are exercised; |

6

| · | risks related to dilution to existing shareholders if deferred share units, restricted share units or performance share units are converted into Common Shares of the Company; |

| · | the history of the Company with respect to not paying dividends and anticipation of not paying dividends in the foreseeable future; and |

| · | the absence of a market through which the Company’s securities, other than Common Shares, may be sold. |

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein. This list is not exhaustive of the factors that may affect any of the Company’s forward-looking statements and information. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of the Company or other future events or conditions may differ materially from those reflected in the forward-looking statements and information due to a variety of risks, uncertainties and other factors, including without limitation, those referred to in this AIF under the heading “Risk Factors” and documents incorporated by reference herein. The Company’s forward-looking statements and information are based on the reasonable beliefs, expectations and opinions of management on the date the statements are made and, other than as required by applicable securities laws, the Company does not assume any obligation to update forward-looking statements and information if circumstances or management’s beliefs, expectations or opinions should change. For the reasons set forth above, investors should not attribute undue certainty to or place undue reliance on forward-looking statements and information.

Currency and Exchange Rates

All dollar amounts referred to in this AIF are expressed in United States dollars (“U.S.$”) except where indicated otherwise. The Company’s accounts are based on a U.S.$ functional currency and are reported in a U.S.$ presentation currency. All references to “dollars” are “$” are to U.S.$ except where indicated otherwise. All references to “pesos” are to Mexican pesos. The Company incurs expenditures primarily in U.S.$, and to a lesser extent in Canadian dollars (“C$”), and pesos.

The following table sets forth the rate of exchange for the C$ expressed in U.S.$ in effect at the end of the periods indicated, the average of exchange rates in effect on the last day of each month during such periods, and the high and low exchange rates during such periods based on the noon rate of exchange as reported by the Bank of Canada for conversion of Canadian dollars into United States dollars:

| Canadian dollars, as expressed in U.S. dollars | Year Ended December 31, | ||

| 2018 | 2017 | 2016 | |

| Rate at end of period | $0.7456 | $0.7971 | $0.7448 |

| Average rate for period | $0.7438 | $0.7701 | $0.7548 |

| High for period | $0.8039 | $0.8245 | $0.7972 |

| Low for period | $0.7438 | $0.7276 | $0.6854 |

The rate of exchange on March 25, 2019 as reported by the Bank of Canada for the conversion of Canadian dollars into United States dollars was C$1.00 equals U.S.$0.7452.

The following table sets forth the rate of exchange for the Mexican Peso expressed in U.S.$ in effect at the end of the periods indicated, the average of exchange rates in effect on the last day of each month during such periods, and the high and low exchange rates during such periods based on the exchange rate published by Banco de Mexico in the Official Journal of the Federation to settle liabilities denominated in foreign currency payable in Mexico, for conversion of Mexican Pesos into United States dollars (“Official Closing Rate”):

7

| Mexican pesos, as expressed in U.S. dollars | Year Ended December 31, | ||

| 2018 | 2017 | 2016 | |

| Rate at end of period | $0.0509 | $0.0506 | $0.0484 |

| Average rate for period | $0.0520 | $0.0529 | $0.0533 |

| High for period | $0.0556 | $0.0572 | $0.0582 |

| Low for period | $0.0483 | $0.0456 | $0.0475 |

The Official Closing Rate of exchange on March 25, 2019 as reported by the Banco de Mexico for the conversion of Mexican Pesos into United States dollars was $1.00 Pesos equals U.S.$0.0522.

Metric Equivalents

For ease of reference, the following factors for converting Imperial measurements into metric equivalents are provided:

| To convert from Imperial | To metric | Multiply by |

| Acres | Hectares | 0.404686 |

| Tons | Tonnes | 0.907185 |

| Troy Ounces/ton (“opt”) | Grams/Tonne (“g/t”) | 34.2857 |

Financial Data in this AIF

Financial information reported in this AIF is in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

Defined Terms

A glossary of certain terms used in this AIF is attached as Schedule “B”. Terms used and not defined in this AIF that are defined in National Instrument 51-102 - Continuous Disclosure Obligations shall bear that definition. Other definitions are set out in National Instrument 14-101 - Definitions.

Cautionary Statement Regarding Non-IFRS Measures

This AIF includes certain terms or performance measures commonly used in the mining industry that are not defined under IFRS, including cash cost per ounce of silver. These terms and measures do not have a standardized meaning prescribed by IFRS. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Non-IFRS measures should be read in conjunction with the Company’s financial statements.

CORPORATE STRUCTURE

MAG Silver Corp. was originally incorporated under the Company Act (British Columbia) on April 21, 1999 under the name “583882 B.C. Ltd.” On June 28, 1999, in anticipation of becoming a capital pool company, the Company changed its name to “Mega Capital Investments Inc.” On April 22, 2003, the Company changed its name to “MAG Silver Corp.” to reflect its new business upon the completion of its qualifying transaction on the TSX Venture Exchange. Effective March 29, 2004, the Company Act (British Columbia) was replaced by the Business Corporations Act (British Columbia). Accordingly, on July 27, 2005, the Company transitioned under the Business Corporations Act (British Columbia) and adopted new articles and concurrently increased its authorized capital from 1,000,000,000 Common Shares to an unlimited number of Common Shares without par value and an unlimited number of Preferred Shares without par value.

The Company’s head office is located at Suite 770, 800 West Pender Street, Vancouver, British Columbia, Canada, V6C 2V6. The Company’s registered office is located at 2600 – 595 Burrard Street, Vancouver, British Columbia Canada, V7X 1L3.

8

Intercorporate Relationships

The following chart illustrates the Company’s significant subsidiaries, including the jurisdiction of incorporation of each company and its properties.

(1) The Company is the registered owner of 99.99% of the issued Class I shares of Minera Pozo Seco S.A. de C.V. (“Pozo Seco”), a corporation incorporated under the laws of Mexico. The remaining 0.01% of the issued Class I shares of Pozo Seco are held by Dan MacInnis, a director of the Company, on behalf of the Company.

9

(2) The Company is the registered owner of 99.99% of the issued Class I shares of Minera Los Lagartos, S.A. DE C.V. (“Lagartos”), a corporation incorporated under the laws of Mexico. The remaining 0.01% of the issued Class I shares of Lagartos are held by Dan MacInnis, a director of the Company, on behalf of the Company.

(3) Lagartos is the registered owner of a 44% interest in Minera Juanicipio, S.A. De C.V. (“Minera Juanicipio”), a corporation incorporated under the laws of Mexico, which holds the joint ventured Juanicipio Project (the “Juanicipio Joint Venture”) with Fresnillo, a London Stock Exchange listed company controlled by Industrias Peñoles, S.A. De C.V. (“Peñoles”), which holds the remaining 56% interest in Minera Juanicipio.

The following table lists the subsidiaries of the Company and a company in which MAG holds a significant interest, together with the jurisdiction of incorporation and the direct or indirect percentage ownership by the Company of each such subsidiary:

| Name | Percentage of Ownership | Jurisdiction of Organization |

| Minera Los Lagartos, S.A. DE C.V. | 100%(1) | Mexican Republic |

| Minera Juanicipio, S.A. DE C.V. | 44%(2) | Mexican Republic |

| 0890887 B.C. Ltd. | 100%(3) | Canada |

| 0892249 B.C. Ltd. | 100%(3) | Canada |

| DSUB0890887 Cooperatief U.A. | 100%(4) | Netherlands |

| STPF B.V. | 100%(5) | Netherlands |

| Minera Pozo Seco S.A. DE C.V. | 100%(6) | Mexico |

Notes:

| (1) | On October 9, 2005 the assets of Lexington Capital Group Inc., previously a subsidiary of the Company, were merged with Lagartos, so that all of the Company’s interests in the Juanicipio claim were held by Lagartos. |

| (2) | 44% interest is owned by Lagartos, which in turn is wholly owned by the Company. |

| (3) | 0890887 B.C. Ltd., and 0892249 B.C. Ltd., were incorporated on September 21, 2010 and September 28, 2010, respectively and are wholly owned by the Company. |

| (4) | DSUB0890887 Cooperatief U.A. was incorporated on October 11, 2010 in the jurisdiction of the Netherlands, and is wholly owned by 0890887 B.C. Ltd. and 0892249 B.C. Ltd. |

| (5) | STPF B.V. was acquired by DSUB0890887 Cooperatief U.A. on October 12, 2010. |

| (6) | Minera Pozo Seco was incorporated in Mexico on September 27, 2010. |

GENERAL DEVELOPMENT OF THE BUSINESS

MAG is a company based in Vancouver, British Columbia, Canada focused on the acquisition, exploration and development of mineral exploration properties, with its primary focus being silver projects located primarily in the Americas. The Company’s Common Shares trade on the Toronto Stock Exchange (“TSX”) and the NYSE American under the symbol MAG. The Company is a “reporting issuer” in the Provinces of British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, Nova Scotia, New Brunswick, Prince Edward Island and Newfoundland and Labrador and is a reporting “foreign issuer” in the United States of America.

10

Juanicipio Project

The Company’s principal and material property is its 44% interest in the Juanicipio Joint Venture, an exploration and development project (the “Juanicipio Project”) located in Mexico. Although a formal production decision has not been made on the Juanicipio project, on October 28, 2013, underground development commenced and has been ongoing since, along with continued exploration drilling on the property. The Company’s share of Juanicipio exploration and development costs are funded primarily through its 44% interest in Minera Juanicipio, and to a lesser extent, costs are incurred directly by MAG related to project oversight (of the ongoing development and of the field and drilling programs executed).

Other Projects

The Company has concession rights in other non-material properties to which the exploration is managed directly by MAG. Exploration on these interests (when undertaken) is managed through contracted service providers (exploration companies, drilling companies, assay companies, etc.) as the Company has no direct employees outside of Canada.

All the work in Mexico is overseen and supervised at industry market rates, by Cascabel and IMDEX, related companies to MAG (see “INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS” below). There was no active exploration on any of the properties in Mexico in 2018.

Cinco de Mayo

The Company owns 100% of the mineral concessions comprising the Cinco de Mayo Property. The property is located approximately 190 kilometres northwest of the city of Chihuahua, in northern Chihuahua State, Mexico, and covers approximately 25,113 hectares. The primary concessions of the Cinco de Mayo Property were acquired by way of an option agreement dated February 26, 2004, and the property remains subject to a 2.5% net smelter returns royalty to a related party (see “INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS” below). The project consists of four major mineralized zones: the Upper Manto silver-lead-zinc inferred resource; the Pegaso deep discovery; the non-core Pozo Seco high grade molybdenum-gold resource; and the surrounding Cinco de Mayo exploration area.

In late 2012, certain members of the local Ejido challenged the Company’s surface right access to the property and have prevented the Company from obtaining the surface access permission required as part of a Federal Government exploration permit process. The Company has been unable to negotiate a renewed surface access agreement with the Ejido, and a full impairment was recognized on the property in the year ended December 31, 2016.

The Company believes that the Cinco de Mayo Project has significant geological potential and will continue to maintain its mineral concessions in good standing. Efforts to regain surface access are ongoing, although the Company has no current plans to conduct any geological exploration programs on the property.

Three Year History

Year Ended December 31, 2016

On March 1, 2016, the Company closed a bought deal public offering and issued 8,905,000 common shares at $7.30 per share for gross proceeds of $65,006,500, and on March 4, 2016, the Company closed the associated over-allotment option which was fully exercised by the underwriters, and issued a further 1,335,750 common shares at a price of $7.30 for additional gross proceeds of $9,750,975.

11

As at December 31, 2016, the Company had working capital of $139,141,858 including cash and term deposits of $138,346,996.

Operational highlights of 2016 for the Juanicipio Project include the following summary.

Development

MAG and Fresnillo continued to progress the Juanicipio Project in accordance with the recommendations of the 2014 Juanicipio Technical Report, with the development focused primarily on the ramp decline advancing towards the main Valdecañas Vein of the property. The entry portal, surface explosives magazines, surface offices and associated infrastructure were completed, and the ramp decline advanced with drilling and blasting. The ramp and ancillary passage development advance rate remained at or exceeding the levels envisioned in the 2014 Juanicipio Technical Report (115 metres per month), and the ramp reached the uppermost reaches of the Valdecañas Vein in December 2016 and footwall development commenced thereafter.

Exploration

The deep drilling programs to further delineate the extent of the new Deep Zone that were approved and commenced in the second half of 2015, were completed in 2016. On August 15, 2016, drill results were released and confirmed the extension of wide high-grade mineralization from the Deep Zone discovery on the Minera Juanicipio joint venture property. The drilling also resulted in the discovery of the “Anticipada Vein”, a newly recognized vein of unclear geometry lying about 100 metres into the hanging wall of the East Vein.

In April 2016, the Joint Venture Technical Committee approved a supplemental $1,200,000 budget (MAG’s 44% share is $528,000) for additional 2016 deep and shallow in-fill drilling as well as protection and exploration holes along and ahead of the path of the decline as it approached the Valdecañas Vein. This supplemental drill program was for a combined 8,900 metres of surface and underground drilling, and continued through year end into 2017.

Year Ended December 31, 2017

On November 28, 2017, the Company completed a non-brokered private placement and issued 4,599,641 common shares at $10.47 per share for gross proceeds of $48,158,241.

As at December 31, 2017, the Company had working capital of $159,905,996 including cash and term deposits of $160,395,108.

Operational highlights of 2017 for the Juanicipio Project include the following summary.

2017 PEA

A new Mineral Resource estimate and Preliminary Economic Assessment was announced on November 7, 2017 and the resulting MAG Silver Juanicipio NI 43-101 Technical Report was filed on December 18, 2017 with an Amendment and Restated report filed on January 19, 2018 (the “2017 PEA”). The studies were commissioned by MAG and carried out by AMC Mining Consultants (Canada) Ltd. (“AMC”). Based on the 2017 PEA, the Company viewed the Juanicipio Project as a robust, high-grade, high-margin underground silver project exhibiting low development risks. The 2017 PEA incorporated major overall project upgrades highlighted by the delineation and provision for mining of greatly expanded Indicated and Inferred Mineral Resources in the recently discovered (2015) “Deep Zone”. The volume of these new base metal-rich Deep Zone Resources contributed to a significant expansion of project scope and enhancements to most aspects of the mine design; the most important being an increase of the planned production rate to 4,000 tonnes per day (“tpd”). Within the expanded scope of the 2017 PEA the Juanicipio Project was now projected to produce a payable total of 183 million silver ounces, 750 thousand gold ounces, 1.3 billion pounds of zinc and 812 million pounds of lead over an initial 19 years of mine life, with an opportunity to consider and assess the recoverability of copper as well. (see ‘Juanicipio Project’ in ‘MINERAL PROJECTS’ below).

12

The economic analysis in the 2017 PEA is preliminary in nature and is based, in part, on Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves. There is no certainty that a Preliminary Economic Assessment will be realized (see “Risk Factors” below).

Feasibility Study

An independent feasibility study to be prepared by AMC, was commissioned by Minera Juanicipio in the second half of 2017 (the “Feasibility Study”). The Feasibility Study will not include Inferred Mineral Resources in the mine plan, and it is therefore expected to have a shorter mine life than envisioned in the 2017 PEA. In addition, the Feasibility Study is expected to be based on more detailed engineering and may have changes in scope. As a result, the Feasibility Study is expected to contain an incremental increase in the estimated initial capital cost. With these and other possible scope changes, the project’s modeled economics are expected to decrease as compared to those in the 2017 PEA (see ‘Risk Factors’ below). This study is a requirement of the Minera Juanicipio Shareholders’ Agreement in order to make a formal production decision. Upon its completion, Minera Juanicipio is expected to present the Feasibility Study to both its Board and the respective Joint Venture partner Boards for formal development consideration and approval.

Development

The decline ramp reached the uppermost reaches of the main Valdecañas Vein in December 2016 and footwall development commenced thereafter into 2017. Ramp-related surface installations, offices and associated infrastructure were completed, and construction of additional ventilation raises was on-going. Midway through 2017, underground development was intensified to allow for the planned increase in processing capacity to 4,000 tpd. Additional development contractors were engaged in the year by Minera Juanicipio, and a twinning of the access decline was undertaken and advanced rapidly with the intent of providing expanded capacity for hauling mineralized rock and waste.

Exploration

Drilling of the Deep Zone continued through 2017, and the Zone effectively remained open to depth and laterally along its entire strike length to the Joint Venture boundary in both directions.

Assays from 13 exploration and infill drill holes from the Deep Zone were released in the first quarter of 2017, which along with previously announced results from 14 earlier holes (27 holes total) have:

| · | confirmed that continuous mineralization extends below the Valdecañas Bonanza Zone in both the East and West Veins; |

13

| · | revealed a substantial widening of this deeper mineralization into a well-defined dilatant zone under both veins; |

| · | improved definition of the new “Anticipada” or “Vant” Vein, within the vein system; and, |

| · | combined to indicate that a major ore-fluid input point underlies the Overlap Zone between the East and West veins |

A significantly expanded Mineral Resource estimate for the base metal-rich Deep Zone was included in the 2017 PEA (see ‘Juanicipio Project’ in ‘MINERAL PROJECTS’ below).

A 20,000-metre 2017 exploration drill program commenced in July 2017 to test various targets within the Juanicipio property boundaries and to continue drilling the Deep Zone. Dr. Peter Megaw, the Company’s Chief Exploration Officer, and the MAG exploration team were involved with Fresnillo in selecting drill targets for this program. To the end of 2017, approximately 9,000 metres were drilled, primarily in-fill drilling and assays were pending at year end.

Year Ended December 31, 2018

As at December 31, 2018, the Company had working capital of $129,315,792 including cash and cash equivalents of $130,180,392.

Total Juanicipio Project expenditures incurred and capitalized directly by Minera Juanicipio (on a 100% basis) for the year ended December 31, 2018 amounted to $45.9 million.

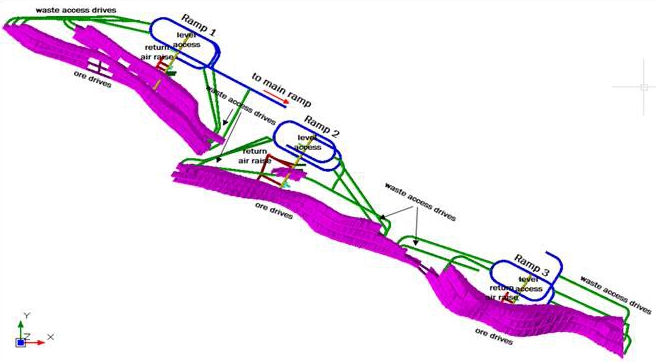

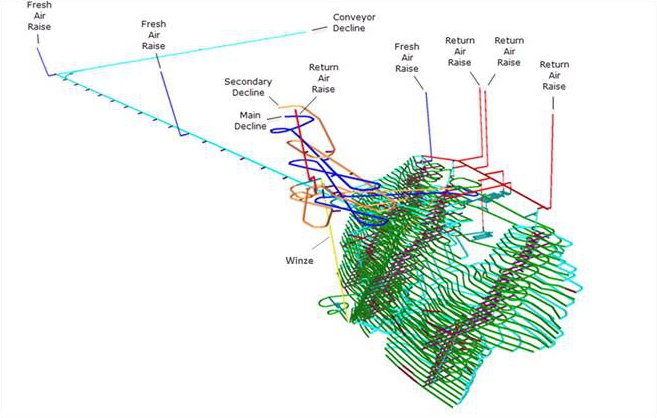

UNDERGROUND DEVELOPMENT – Juanicipio Project

The twinning of the original access decline was considered necessary to provide expanded capacity for hauling additional mineralized rock and waste stemming from the planned increase in processing capacity to 4,000 tpd. The twin ramp was started in 2017 and completed in the second half of 2018 and is accessible through a second entry portal for the mine also completed in 2018. The twin ramps will allow for streamlined underground traffic flow and increased safety through the mine having a second egress. The three ramps into the mineralized envelope are designed to provide access to the mineralized material and form initial stopes within the mine and are required to facilitate the planned increase in mining rate to 4,000 tpd.

Development in 2018 was focused on:

| • | advancing the three internal spiral footwall ramps at depth to be used to further access the full strike length of the Valdecañas Vein system; |

| • | excavating and constructing the underground crushing chamber; |

| • | advancing the conveyor ramp to the planned surface processing facility; |

| • | integrating additional ventilation and other associated underground infrastructure; and, |

| • | progressing the construction of surface infrastructure facilities. |

As of 2017, Minera Juanicipio has intensified underground development by engaging additional development contractors. The underground development metres achieved in 2017 and 2018 reflect the increased number of contractors and accelerated activity:

14

| Period |

Development Metres (excluding ventilation raises) |

%age of total metres advanced achieved to date |

| Oct 28, 2013 – December 31, 2016 | 5,307 | 30% |

| January 1 – December 31, 2017 | 5,634 | 32% |

| January 1 – December 31, 2018 | 6,630 | 38% |

| Cumulative Total to December 31, 2018 | 17,571 | 100% |

The underground development in the year ended December 31, 2018 totaled 6,630 metres advanced, and accounts for 38% of the total underground development advanced on the project to the end of December 31, 2018. Total underground development at Juanicipio to the end of December 31, 2018 was in excess of 17.5 kilometres.

Concurrent with the ongoing underground development, detailed engineering continues for the internal shaft and other mine infrastructure, and mill-site preparation is underway. According to the operator, Fresnillo, negotiations with suppliers of processing equipment and development contractors have begun and respective contractual commitments of $23.1 million (equipment) and $69.5 million (development contractors) have been committed to as at December 31, 2018.

Feasibility Study

An independent feasibility study is a requirement of the Minera Juanicipio Shareholders’ Agreement in order to formally approve the project. As noted above, AMC was therefore commissioned by Minera Juanicipio in late 2017 to prepare such a study and a draft remains under review by both Joint Venture partners. Upon approval of the Feasibility Study by the Technical Committee, Minera Juanicipio is expected to present the study to both its Board and the respective Joint Venture partner Boards for formal development consideration and approval. MAG expects to support the development of the project.

By regulatory definition, a feasibility study cannot include Inferred Mineral Resources in the mine plan. The Feasibility Study will therefore only be based on Minera Juanicipio’s Indicated Mineral Resources and will include more detailed engineering. These factors may lead to changes in the project’s scope as compared to that of the 2017 PEA. Without Inferred Mineral Resources in the mine plan, the Feasibility Study will reflect a shorter mine life than envisioned in the 2017 PEA and the study is expected to contain an incremental increase in the estimated initial capital cost. With these and other possible scope changes, the project’s modeled economics are expected to decrease as compared to those in the 2017 PEA (see ‘Risk Factors’ below).

Exploration

Drilling designed with the intention to both convert the Inferred Resources included in the Deep Zone into Indicated Resources, and to further trace the Deep Zone laterally and to depth, was ongoing throughout 2018. Directional drilling equipment that arrived to site in December 2017, and was in full use (being rotated between three separate “mother holes”) for most of 2018 with the exception of a short period when it was returned to the border for import permit renewal. This specialized equipment enables drilling a series of precisely aimed and angled deflection holes off of a single “mother hole” drilled to 800-1,000 metres of depth. This more efficient drilling method results in fewer lost holes and improves the precision and accuracy in deep grid drilling on the 100 x 100 metre pattern required for Indicated Resource definition. It is comparable to conventional drilling on a time and cost basis, but the ability to minimize the uncontrolled deflection of conventional deep drilling helps eliminate many wasted holes. In the second half of 2018, drilling also commenced on the western extension of the Juanicipio Vein as part of the exploration program to pursue other high priority drill targets within the Juanicipio property. These targets were formulated at a late March 2018 Minera Juanicipio exploration meeting, attended on behalf of the Company by Dr. Peter Megaw and Lyle Hansen, the Chief Exploration Officer and Geotechnical Director, respectively.

15

At the end of 2018, exploration drilling under the current drill program totalled approximately 46,060 metres of completed drilling with all assays pending.

Current Fiscal Year (Subsequent to December 31, 2018)

The Juanicipio Project remains the Company’s primary focus in 2019. On site at the project, underground and other development actively continues with emphasis on: developing the three internal spiral footwall ramps at depth to access the full strike length of the Valdecañas Vein system; excavating and constructing the underground crushing chamber; advancing the conveyor ramp from both ends to and from the planned mill site (with the box cut for the underground conveyor exit portal now complete); integrating additional ventilation and other associated underground infrastructure, and progressing the construction of surface infrastructure facilities.

As well, the partners of Minera Juanicipio are currently reviewing a draft EPCM agreement which defines the specific terms by which Fresnillo will oversee the construction of the process plant and associated surface infrastructure. An Operator Services agreement is also under review by the partners which will become effective upon commercial production being achieved. And finally, both lead and zinc off-take agreements are being reviewed by the partners.

Subsequent to the year end, the Company reported assays for a 48-hole (46,060 m) diamond drill program on the Juanicipio Joint Venture Property completed in late 2018 (see two Press Releases dated March 4, 2019). The program was designed to expand and infill the wide, high-grade Deep Zone Mineral Resource estimate outlined in the Company’s 2017 PEA. The drill results reported extend and confirm continuity to depth of high-grade mineralization in the East and West Valdecañas Vein Deep Zones and in the Anticipada Vein. Drilling also coincidentally discovered the new Pre-Anticipada vein in the hangingwall above the system.

On March 4, 2019, the Company also reported the discovery of the northeast (“NE”) oriented ‘Venadas Vein” within the Juanicipio property (See Press Releae dated March 4, 2019). The Company believes this new Venadas Vein discovery is the first ever mineralized vein in the Fresnillo district oriented at a high angle (NE) to the historically mined northwest (“NW”) oriented veins. The Venadas Vein intercepts lie at a very high-level in the vein zoning model, suggesting considerable depth potential. As well, other much larger NE structures with intense surface alteration are known farther afield within the Juanicipio property and are now priority exploration targets. None have ever been directly drilled.

For more information on the Company’s progress and intentions for its material property please refer to the “Mineral Projects” section below.

DESCRIPTION OF THE BUSINESS

General

The Company is in the mineral acquisition, exploration and development business. The Company is in the exploration and development stage and there is no assurance that a commercially viable mineral deposit exists on any of its properties. In the case of the Company’s primary asset, the Juanicipio Project, although a Feasibility Study is in process as noted above, as of the current date, Minera Juanicipio has not completed a pre-feasibility study or feasibility study on the project, and accordingly, there is no estimate of mineral reserves. Rather, the decision to commence development of the Juanicipio Project in late 2013 was based upon a preliminary economic assessment of the project, which is preliminary in nature and is based, in part, on Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the economic results presented in a preliminary economic assessment will be realized (see “Risks Relating to the Development of the Juanicipio Project” below).

16

Principal Markets

The Company is a reporting issuer in the Provinces of British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, Nova Scotia, New Brunswick, Prince Edward Island and Newfoundland and Labrador and is a reporting “foreign issuer” in the United States of America.

The Company’s Common Shares were listed and posted for trading on the TSX Venture Exchange (formerly CDNX) on April 19, 2000 under the symbol “MGA”. Concurrent with the Company’s name change to MAG Silver Corp. on April 22, 2003, the trading symbol was changed to “MAG”. On July 9, 2007, the Company’s Common Shares were listed on the American Stock Exchange (then the NYSE MKT and now the NYSE American) under the symbol “MVG”. On October 5, 2007, the Company delisted from the TSX Venture Exchange concurrent with its listing on the TSX, with the Company’s Common Shares continuing to trade under the symbol “MAG”. On June 27, 2016, the Company changed its symbol on the NYSE MKT (now the NYSE American) from “MVG” to “MAG”.

Adjacent Property Disclosure

The staff of the United States Securities and Exchange Commission (the “SEC”) take the position that mining and mineral exploration companies, in their filings with the SEC, should describe only those mineral deposits that the companies themselves can economically and legally extract or produce. This AIF contains information regarding adjacent properties on which we have no right to explore or mine, and is considered by management to be of material importance to the Company and its land holdings in the area. Investors are cautioned that mineral deposits on adjacent properties do not necessarily indicate and certainly do not prove the existence, nature or extent of mineral deposits on our properties.

Cautionary Note to Investors Concerning Estimates of Mineral Resources

This AIF uses the terms "Indicated Mineral Resources" and “Inferred Mineral Resources”. MAG advises investors that although these terms comply with Canadian reporting standards under NI 43-101, the SEC does not recognize these terms and U.S. companies are generally not permitted to disclose resources in documents that they file with the SEC. Furthermore, disclosure of “contained ounces” is permitted under Canadian regulations; however, the SEC permits issuers to report mineralization that does not constitute “reserves” by SEC standards only as in place tonnage and grade without reference to unit measures.

Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. In addition, "Inferred Mineral Resources" have a great amount of uncertainty as to their existence, and economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resources will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources are considered too speculative geologically to have the economic considerations applied to them to enable them to be categorized as mineral resources and, accordingly, may not form the basis of feasibility or pre-feasibility studies, or economic studies except for a Preliminary Economic Assessment as defined under NI 43-101. Investors are cautioned not to assume that part or all of an Inferred Mineral Resource exists, or is economically or legally mineable indicated and inferred mineral resources that are not mineral resources do not have demonstrated economic viability.

17

Technical Information

Unless otherwise indicated, scientific or technical information in this AIF is based on information prepared by employees of MAG or its joint venture partners, as applicable, under the supervision of, or that has been reviewed and approved by, Dr. Peter Megaw, Ph.D., C.P.G., who is a “Qualified Person” as defined in NI 43-101. A “Qualified Person” means an individual who is an engineer or geoscientist with at least five years of experience in mineral exploration, mine development or operation or mineral project assessment, or any combination of these, has experience relevant to the subject matter of the mineral project, and is a member in good standing of a professional association.

Passive Foreign Investment Company

The Company believes it is a Passive Foreign Investment Company (“PFIC”) as that term is defined in Section 1297 of the Internal Revenue Code of 1986, as amended. Consequently, this classification may result in adverse tax consequences for U.S. holders of the Company’s Common Shares. For an explanation of these effects on taxation, U.S. shareholders and prospective U.S. holders of the Company’s Common Shares are encouraged to consult their own tax advisers.

Employees

The Company’s business is administered from its head office in Vancouver, British Columbia, Canada. As of December 31, 2018, the Company had seven full time employees (excluding directors), two consultants, and one part time employee.

Specialized Skill and Knowledge

Many aspects of MAG’s business require specialized skill and knowledge. Such skills and knowledge include the areas of geology, engineering, accounting and mine planning. MAG has found that it has been able to locate and retain such employees when needed.

Competitive Conditions

Competition in the mineral exploration and production industry is intense. The Company competes with a number of large, established mining companies with greater financial resources and technical facilities, for the acquisition and development of mineral concessions, claims, leases and other interests, as well as for the recruitment and retention of qualified employees and consultants and the equipment required to continue the Company’s exploration activities.

Economic Dependence

The Juanicipio Project, in which the Company owns a 44% joint venture interest, is considered the only material property of the Company. The Company’s interest in the Juanicipio Project is held through its indirect 44% ownership of Minera Juanicipio, and is governed by the terms of the Shareholders Agreement with Fresnillo which holds the other 56% interest. As a minority stakeholder in the Project, the Company is subject to various risks (see “Risks Related to Minority Interest Investment in the Juanicipio Project” below).

Please consult the Company's public filings at www.sedar.com and www.sec.gov for further, more detailed information concerning these matters.

18

CARRYING ON BUSINESS IN MEXICO

The Company’s current property interests are primarily located in Mexico. A summary of the regulatory regime material to the business and affairs of the Company is provided below.

Mining Regulations

The exploration and exploitation of minerals in Mexico may be carried out by Mexican citizens or Mexican companies incorporated under Mexican law by means of obtaining concessions (currently covering exploration and exploitation). Concessions are granted by the Mexican federal government for a period of fifty years from the date of their recording in the Public Registry of Mining. The term of mining concessions previously issued by the Mexican federal government (for exploration and/or exploitation) was automatically extended by the enactment of the 2006 amendments to the Mexican Mining Law. Likewise, due to such amendments, the holders of mining concessions for exploration were automatically authorized to carry out not only exploration work, but also exploitation works.

Holders of concessions may, within the five years prior to the expiration of such concessions, apply for their renewal for the same period of time. Failure to apply prior to the expiration of the term of the concession will result in termination of the concession. Concessions are subject to annual work requirements and payment of mining duties which are assessed and levied on a semi-annual basis. Such concessions may be transferred or assigned by their holders, but such transfers or assignments must comply with the requirements established by the Mexican Mining Law and be registered before the Public Registry of Mining in order to be valid against third parties. Such recordation has to be requested within the fifteen business days following the execution or notarization of the corresponding assignment of rights agreement.

Although the Law of Foreign Investment (Ley de Inversión Extranjera) provides that mineral concessions may also be obtained by foreign citizens or foreign corporations, the Mexican Mining Law provides that such concessions may only be granted to Mexican citizens or Mexican corporations. Thus, foreign citizens or corporations may only obtain mineral concessions through the establishment of a subsidiary in Mexico. Foreign investment in Mexican companies must comply with certain requirements set forth in the Law of Foreign Investment.

The Mexican Mining Law does not require payment of finder’s fees or royalties to the Government, except for: i) a mining royalty fee of 7.5% and the 0.5% extraordinary governmental fee on precious metals, (see below “Income Tax Regime Effective January 1, 2014); and ii) a discovery premium or economic consideration in connection with claims or allotments contracted directly from the Mexican Geological Service that have been awarded pursuant to a public bid process. None of the property interests held by Lagartos or Minera Pozo Seco are under such fee regimes at the present time. However, holders of mining concessions are required to pay mining concession fees which are assessed and levied on a semi-annual basis, and that increase over time the longer the concessions are held.

Foreign Investment Regulation

Foreign investment regulation in Mexico is primarily governed by the Law of Foreign Investment and its Regulations. Foreign investment of up to 100% in Mexican mining companies is permitted. Companies with foreign investment in their capital stock must be registered with the National Registry of Foreign Investment which is maintained by the Ministry of Economy, and file certain reports and notices, including in certain circumstances, and under a criteria determined by the Law of Foreign Investment an annual report and/or quarterly reports with respect to the operations carried out during the preceding fiscal year which is necessary in order to renew their certificate of recordation with such Registry.

19

Environmental Regulations

Mexico has federal, state and municipal laws and regulations, as well as international agreements related to the protection of the environment and natural resources (“Environmental Laws”), including laws and regulations concerning water pollution, air pollution, noise pollution, hazardous substances and forest protection. The main federal Environmental Law in Mexico is the Ley General del Equilibrio Ecológico y la Protección al Ambiente (the “General Law of Ecological Balance and Environmental Protection” or the “General Law”), pursuant to which general environmental rules and policies have been promulgated addressing air pollution, hazardous substances and environmental impact among various others.

Another federal law particularly relevant for the mining sector is the Ley General para la Gestión Integral de los Residuos (the “General Law for Integrated Waste Management”) and its regulations the Reglamento de la Ley General para la Prevención y Gestión Integral de los Residuos (the “Regulations to the General Law for Integrated Waste Prevention and Management”), which regulate the generation, handling, transportation, storage and final disposal of hazardous waste, as well as the import and export of hazardous materials and hazardous wastes, and assign liability for ownership and possession of contaminated sites and for contaminating activities. The Ley General de Desarrollo Forestal Sustentable and its regulations (the “Forestry Protection Laws”) are also relevant, as they address reforestation obligations and compensation measures on projects which may have a deforestation impact, which may include mining projects.

On June 7, 2013, the Ley Federal de Responsabilidad Ambiental (Federal Law of Environmental Liability) was enacted, under which any person or entity that directly or indirectly (for action or omission) causes damage to the environment, will be held liable and obliged to: i) repair the damage, or in the event that such repair is not possible; ii) pay compensatory damages, subject to a corresponding judicial, administrative or criminal proceeding.

Applicable Environmental Laws contemplate the creation and regulation of Natural Protected Areas (Areas Naturales Protegidas) which along with Ecological Ordinance Programs (Programas de Ordenamiento Ecológico) constitute two of the main instruments that will regulate the use of land in the areas within their jurisdiction, including restrictions on certain activities and sectors, such as the mining sector.

In addition, there are a series of “Mexican Official Norms” which are technical standards issued by competent regulatory authorities, pursuant to the Ley General de Metrología y Normalización and to other laws that include the aforementioned Environmental Laws, which establish standards relating to air emissions, waste water discharges, the generation, handling and disposal of hazardous wastes (including specific Mexican Official Norms for the handling of mining tailings, which are considered mining hazardous wastes) and noise control, among others. There are Mexican Official Norms regarding soil contamination (mainly with total petroleum hydrocarbons and heavy metals) and waste management (the “Ecological Standards”). Of particular importance to the mining sector are Mexican Official Norms NOM-120-SEMARNAT-2011 regulating environmental protection of mining activities in certain zones, and NOM-141-SEMARNAT-2003 which addresses certain aspects of tailings (jales de minería) from mining activities, among other Ecological Standards applicable to mining activities.

The Secretaría de Medio Ambiente y Recursos Naturales (the “Ministry of the Environment and Natural Resources” or “SEMARNAT”, for its initials in Spanish) is the federal agency in charge of establishing and overseeing environmental regulation at the federal level, including the General Law and federal statutes and the Environmental Laws, as well as the Ecological Standards. On enforcement matters the SEMARNAT acts mainly through the “Procuraduría Federal de Protección al Ambiente” (the “Federal Bureau of Environmental Protection” or “PROFEPA”, for its initials in Spanish) and in certain cases through other governmental entities under its control, such as the Comisión Nacional del Agua (or National Water Commission).

20

Environmental Laws also regulate environmental protection in the mining industry in Mexico. In order to comply with these laws, a series of permits, licenses and authorizations must be obtained by a concession holder during the exploration and exploitation stages of a mining project. Generally, these permits and authorizations are issued on a timely basis after the completion of an application and the fulfillment of the necessary requirements by a concession holder. Additionally, periodic reporting of hazardous wastes and federal air emissions and federal waste water discharges to Federal authorities is required under the Environmental Laws. To the best of the Company’s knowledge, all of the Company’s property interests are currently in compliance with the Environmental Laws.

In the exploration stage, the cost of complying with such Environmental Laws is included in the exploration budget. Until such time as the Company conducts larger more invasive procedures, such as trenching or bulk sampling, there is only nominal cost associated with compliance with the Environmental Laws. The Company’s programs are not yet sufficiently advanced to allow an estimate of the future cost of such environmental compliance.

Currency

The official monetary unit of Mexico is the Mexican peso. The currency exchange rate freely floats and the country has no currency exchange restrictions. Nevertheless, following the devaluation of the Mexican peso in December, 1994, uncertainties continue with respect to the financial situation of Mexico. See “Risk Factors” below, specifically those risk factors dealing with currency fluctuation and inflation.

The following table presents a five-year history of the average annual exchange rates to convert one United States dollar into Mexican pesos, calculated by using the average of the exchange rates on the last day of each month during the given year.

| Year | Average Exchange Rate (Mxn peso/US$) |

| 2018 | 19.2432 |

| 2017 | 18.9232 |

| 2016 | 18.6774 |

| 2015 | 15.8299 |

| 2014 | 13.3609 |

Value Added Tax (“VAT”) also known as “IVA”

In Mexico, VAT is charged on the sale of goods, rendering of services, lease of goods and importation of the majority of goods and services at a rate of 16%. Proprietors selling goods or services must collect VAT on behalf of the government. Goods or services purchased incur a credit for VAT paid. The resulting net VAT is then remitted to, or collected from, the Government of Mexico through a formalized filing process.

The Company has traditionally held a VAT receivable balance due to the expenditures it incurs whereby VAT is paid to the vendor or service provider. Collections of these receivables from the Government of Mexico often take months and sometimes years to recover, but the Company has to date been able to recover all of its VAT paid.

Amendments were made to Mexican VAT legislation, effective January 1, 2017, that may impact the Company’s future ability to recover VAT paid after January 1, 2017. Although still subject to interpretation and confirmation of intent from the Mexican government, companies in a pre-operative/exploration stage may have to satisfy additional criteria in order to claim valid refunds. The Company’s IVA paid that falls into this category, is not material or significant to the Company’s overall operations.

21

The 2017 changes are not expected to have any impact on Minera Juanicipio and its ability to recover VAT paid, given the expectation it will be in production by 2020.

Income Tax Regime Effective January 1, 2014

The Mexican Senate approved Tax Reform changes in Mexico that became effective January 1, 2014, that in part, adversely affect operating mining companies in Mexico. The changes affecting the Mexican mining industry include: the elimination of a planned reduction in the corporate tax rate from 30% to 28% by 2015 (corporate tax rate will remain 30% indefinitely); a mining royalty fee of 7.5% on income before tax, depreciation, and interest; an extraordinary governmental fee on precious metals, including gold and silver, of 0.5% of gross revenues; and, changes affecting the timing of various expense deductions for tax purposes. Once Minera Juanicipio or any of the Company’s other properties are in production, they will be subjected to this tax regime. Possible tax planning opportunities may exist to reduce the impact of the tax changes. Managements’ assessment of the tax reform changes is that they do not have an impact on the viability of the Juanicipio Project, and the changes have been fully reflected in the 2017 PEA.

Under the new tax regime, mining concession holders that fail to develop mining works in accordance with the Mining Law, during a consecutive two year period within the first eleven years of the term of the concession, will pay on a semi-annual basis an additional mining fee equivalent to 50% to the maximum current mining duty. If the failure to carry out works remains unchanged, starting on the twelfth year, the additional fee will be doubled.

An additional component of the Mexican tax reform also includes a 10% dividend tax, to be withheld on all dividends paid to foreign residents of Mexico over financial earnings which also form part of the after-taxed net earnings account generated as of January 1, 2014. With the existing Canadian-Mexico tax treaties, this dividend tax rate will be reduced to 5%. Prior to the tax reform, there was no dividend withholding tax on dividends paid from Mexico to Canadian corporations out of tax paid earnings.

Tax Law for the State of Zacatecas.

On December 31, 2016, the Government of the State of Zacatecas published the Tax Law for the State of Zacatecas (Ley de Hacienda del Estado de Zacatecas, the “Zacatecas Tax Law”), which came into effect on January 1, 2017.

As provided for in the Zacatecas Tax Law, certain so called “environmental duties” were established for operations carried out within the State of Zacatecas. Such new duties are the following:

| I. | Duty for Environmental Remediation in the Extraction of Minerals (Remediación Ambiental en la Extracción de Minerales). This duty applies for the extraction activities of the soil and sub-soil of materials that constitute deposits of the same nature to the materials of the soil, through open-pit processes. This duty does not apply to the substances and minerals subject to the Mining Law (i.e., substances and minerals subject to provisions of Article 4 of the Mining Law, such as gold, silver, lead, zinc, copper, etc.). |

| II. | Duty for Emissions of Gases to the Atmosphere (De la Emisión de Gases a la Atmósfera). This duty applies to emissions caused to the atmosphere of certain substances generated in productive processes. |

22

| III. | Duty for Emissions of Pollutants to the Soil, Sub-soil and Water (De la Emisión de Contaminantes al Suelo, Subsuelo y Agua). This duty applies to those pollutants deposited, scrapped or released to the soil, subsoil or water deposits. |

| IV. | Duty for the Deposit or Storage of Waste (Del Impuesto al Depósito o Almacenamiento de Residuos). This duty applies to the deposit or storage of waste in public or private landfills. |

In addition, the Zacatecas Tax Law also includes certain other amendments and adjustments to pre-existing taxes in Zacatecas such as the payroll tax.

Minera Juanicipio’s operations are located in the State of Zacatecas, and this new tax law will apply to the Juanicipio development once it is in production. Managements’ assessment of this tax however, is that it will not have an impact on the viability of the Juanicipio Project.

Other general tax amendments are referred to in the “Mexican Foreign Investment and Income Tax Laws apply to the Company” section in Risk Factors below.

RISK FACTORS

The exploration, development and mining of natural resources are highly speculative in nature and are subject to significant risks. The risk factors noted below do not necessarily comprise all those faced by the Company. Additional risks and uncertainties not presently known to the Company or that the Company currently considers immaterial may also impair the business, operations and future prospects of the Company. If any of the following risks actually occur, the business of the Company may be harmed and its financial condition and results of operations may suffer significantly, along with a possible significant decline in the value and/or share price of the Company’s publicly traded stock.

The Company’s securities should be considered a highly speculative investment and investors should carefully consider all of the information disclosed in the Company’s Canadian and U.S. regulatory filings prior to making an investment in the Company. Without limiting the foregoing, the following risk factors should be given special consideration when evaluating an investment in the Company’s securities.

Risks Relating to the Company’s Business Operations

Mineral exploration and development is a highly speculative business and most exploration projects do not result in the discovery of commercially mineable deposits.

Exploration for minerals is a highly speculative venture necessarily involving substantial risk. The expenditures made by the Company described herein may not result in discoveries of commercial quantities of minerals. The failure to find an economic mineral deposit on any of the exploration concessions in which the Company has an interest will have a negative effect on the Company.

None of the properties in which the Company has an interest has any mineral reserves.

Currently, there are no mineral reserves (within the meaning of NI 43-101) on any of the properties in which the Company has an interest. Only those mineral deposits that the Company can economically and legally extract or produce, based on a comprehensive evaluation of cost, grade, recovery and other factors, are considered mineral reserves. The resource estimates contained in the 2017 PEA are indicated and inferred resource estimates only and no assurance can be given that any particular level of recovery of silver or other minerals from mineralized material will in fact be realized or that an identified mineralized deposit will ever qualify as a commercially mineable mineral deposit. In particular, inferred mineral resources have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. Further, the economic assessment contained in the 2017 PEA is preliminary in nature, and actual capital costs, operating costs, production, economic returns and other estimates contained in studies or estimates prepared by or for the Company may differ from those described therein and herein, and there can be no assurance that actual costs will not be higher than anticipated. Substantial additional work, including mine design and mining schedules, metallurgical flow sheets and process plant designs, would be required in order to determine if any economic deposits exist on the Company’s properties. Additional expenditures may be required to establish mineral reserves through drilling and metallurgical and other testing techniques. The costs, timing and complexities of upgrading the mineralized material to proven or probable reserves may be greater than the value of the Company’s reserves on a mineral property and may require the Company to write-off the costs capitalized for that property in its financial statements. The Company cannot provide any assurance that future feasibility studies will establish mineral reserves at its properties. The failure to establish mineral reserves could restrict the Company’s ability to successfully implement its strategies for long-term growth.

23

Most exploration projects do not result in commercially mineable deposits.

The Company’s property interests are primarily at the exploration stage, with none of the Company’s properties have known commercial quantities of minerals. Development of mineral properties involves a high degree of risk and few properties that are explored are ultimately developed into producing mines. The commercial viability of a mineral deposit is dependent upon a number of factors which are beyond the Company’s control, including the attributes of the deposit, commodity prices, government policies and regulation and environmental protection. Fluctuations in the market prices of minerals may render resources and deposits containing relatively lower grades of mineralization uneconomic. Further exploration or delineation will be required before a final evaluation as to the economic and legal feasibility of any of the Company’s properties is determined. Even if the Company completes its exploration programs and is successful in identifying mineral deposits, it will have to spend substantial funds on further drilling and engineering studies before it will know if it has a commercially viable mineral deposit. Most exploration projects do not result in the discovery of commercially mineable mineral deposits.

Estimates of reserves and resources, mineral deposits and production costs can be affected by such factors as environmental permit regulations and requirements, indigenous communities’ rights, weather, environmental factors, unforeseen technical difficulties, unusual or unexpected geological formations and work interruptions. As a result, there is a risk such estimates are inaccurate. For example, the 2017 PEA includes a resource estimate prepared by AMC in accordance with NI 43-101. The grade of precious and base metals ultimately discovered may differ from the indicated drilling results. If the grade of the resource was lower, there would be a negative impact on the economics of the Juanicipio Project. There can be no assurance that precious metals recovered in small-scale tests will be duplicated in large-scale tests under on-site conditions or in production scale. The probability of an individual prospect ever having reserves is extremely remote. If a property does not contain any reserves, any funds spent on exploration of that property will be lost. The failure of the Company to find an economic mineral deposit on any of its exploration concessions will have a negative effect on the Company.

Estimates of mineral resources are based on interpretation and assumptions and are inherently imprecise.

The mineral resource figures referred to in the 2017 PEA, this AIF and the documents incorporated herein by reference have been determined and valued based on assumed future prices, cut-off grades and operating costs. However, until mineral deposits are actually mined and processed, any mineral resources must be considered as estimates only. Fresnillo prepares its own internal resources estimates annually in respect of the Juanicipio Project and such estimates may be materially different from those relied upon by the Company. Any such estimates are expressions of judgment based on knowledge, mining experience, analysis of drilling results and industry practices. Estimates can be imprecise and depend upon geological interpretation and statistical inferences drawn from drilling and sampling analysis, which may prove to be unreliable. In addition, the grade and/or quantity of precious metals ultimately recovered may differ from that indicated by drilling results. There can be no assurance that precious and base metals recovered in small-scale tests will be duplicated in large-scale tests under on-site conditions or in production scale. The grade of the reported mineral resource estimates are uncertain in nature and it is uncertain whether further technical studies will result in an upgrade to them. Further drilling on the mineralized zones is required to complement the current bulk sample and add confidence in the continuity of mineralized zones in comparison to the current block model. Any material change in the quantity of mineralization, grade or mineralization to waste ratio or extended declines in market prices for silver and precious metals may render portions of the Company’s mineralization uneconomic and result in reduced reported mineralization. Any material reductions in estimates of mineralization, or of the Company’s ability to extract this mineralization, could have a material adverse effect on the Company’s results of operations or financial condition.

24

Rights to use the surface of the Company’s mineral properties are not guaranteed.

The mineral properties in which the Company has an interest are generally located in remote and relatively uninhabited areas. Some properties, like the Juanicipio Project, are near towns and other habitations, but there are currently no areas of interest to the Company within its mineral concessions that are overlain by significant habitation or industrial users. However, there are potential overlapping surface usage issues in some areas. Some surface rights are owned by local communities or “Ejidos” and some surface rights are owned by private ranching or residential interests. The Company will be required to negotiate the acquisition of surface rights in those areas where it may wish to develop mining operations. In some areas the Company has been required or is in the process of negotiating compensation for surface rights holders in order to secure right of access. In some areas, surface right compensation has been negotiated and is awaiting formal government expropriation in its favour. The Company’s interest in a property or project could be adversely affected by an inability to obtain surface access permissions, or by challenges, regardless of merit, to existing surface access agreements.

With respect to the Company’s Cinco de Mayo Property, the Company has been unable to negotiate a renewed surface agreement with the local Ejido controlling the surface access to key portions of the property and a full impairment was recognized on the property in the year ended December 31, 2016.

There is no guarantee that licenses and permits required by the Company or Minera Juanicipio to conduct business will be obtained, which may result in an impairment or loss in the Company’s mineral properties.

The Company’s and Minera Juanicipio’s current and anticipated future operations, including further exploration, development activities and commencement of production on the Company’s properties, require permits from various national, provincial, territorial and local governmental authorities. The Company and Minera Juanicipio may not be able to obtain all necessary licenses and permits that may be required to carry out exploration, development and mining operations at their projects. In addition, the grant of required licenses and permits may be delayed for reasons outside the Company’s and Minera Juanicipio’s control. For example, the Company has been prevented from obtaining the Soil Use Change Permit required for the Cinco de Mayo Property due to the opposition from certain members of the local Ejido described above. In addition, development permitting delays resulting from a Mexican government changeover in 2012 and 2013 delayed the start of the decline development at the Juanicipio Project. Failure to obtain such licenses and permits on a timely basis, or failure to comply with the terms of any such licenses and permits that the Company and Minera Juanicipio do obtain, may adversely affect their respective business as the Company and Minera Juanicipio would be unable to legally conduct their intended exploration, development or mining work, which may result in increased costs, delay in activities or the Company or Minera Juanicipio losing its interest in its mineral properties.

25

The properties in which the Company has an interest are located primarily in Mexico.