UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2017

¨ Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ________ to ________

Commission File Number: 000-50058

PRA Group, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 75-3078675 | |||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||

120 Corporate Boulevard, Norfolk, Virginia | 23502 | (888) 772-7326 | ||

(Address of principal executive offices) | (Zip Code) | (Registrant's Telephone No., including area code) | ||

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $0.01 par value per share | NASDAQ Global Select Market | |

(Title of Class) | (Name of Exchange on which registered) | |

Securities registered pursuant to Section 12(g) of the Act:

None |

(Title of Class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES þ NO ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Act. YES ¨ NO þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES þ NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES þ NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or emerging growth company. See the definitions of "large accelerated filer", "accelerated filer", "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one): Large accelerated filer þ Accelerated filer ¨ Non-accelerated filer ¨ (Do not check if a smaller reporting company) Smaller reporting company ¨ Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO þ

The aggregate market value of the common stock held by non-affiliates of the registrant as of June 30, 2017 was $1,657,180,835 based on the $37.90 closing price as reported on the NASDAQ Global Select Market.

The number of shares of the registrant's Common Stock outstanding as of February 23, 2018 was 45,225,425.

Documents incorporated by reference: Portions of the Registrant's definitive Proxy Statement for its 2018 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K.

Table of Contents

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

2

Table of Contents

continued | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

Item 16. | ||

Signatures | ||

3

Cautionary Statements Pursuant to Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995:

This report contains forward-looking statements within the meaning of the federal securities laws. These forward-looking statements involve risks, uncertainties and assumptions that could cause our results to differ materially from those expressed or implied by such forward-looking statements. All statements, other than statements of historical fact, are forward-looking statements, including statements regarding overall cash collection trends, gross margin trends, operating cost trends, liquidity and capital needs and other statements of expectations, beliefs, future plans and strategies, anticipated events or trends, and similar expressions concerning matters that are not historical facts. The risks, uncertainties and assumptions referred to above may include the following:

• | a prolonged economic recovery or a deterioration in the economic or inflationary environment in the Americas or Europe, including the interest rate environment; |

• | changes in the credit or capital markets, which affect our ability to borrow money or raise capital; |

• | our ability to replace our nonperforming loans with additional portfolios; |

• | our ability to purchase nonperforming loans at appropriate prices; |

• | changes in, or interpretations of, federal, state, local, or foreign laws or the administrative practices of various bankruptcy courts, which may impact our ability to collect on our nonperforming loans; |

• | our ability to collect sufficient amounts on our nonperforming loans; |

• | the possibility that we could incur significant allowance charges on our finance receivables; |

• | changes in, or interpretations of, bankruptcy or collection laws that could negatively affect our business, including by causing an increase in certain types of bankruptcy filings involving liquidations, which may cause our collections to decrease; |

• | our ability to manage risks associated with our international operations; |

• | changes in tax laws regarding earnings of our subsidiaries located outside of the United States ("U.S."); |

• | the impact of the Tax Cuts and Jobs Act (the "Tax Act") including interpretations and determinations by tax authorities; |

• | the possibility that we could incur goodwill or other intangible asset impairment charges; |

• | adverse effects from the vote by the United Kingdom ("UK") to leave the European Union ("EU"); |

• | adverse outcomes in pending litigations or administrative proceedings; |

• | our loss contingency accruals may not be adequate to cover actual losses; |

• | the possibility that class action suits and other litigation could divert our management's attention and increase our expenses; |

• | the possibility that we could incur business or technology disruptions or cyber incidents; |

• | our ability to collect and enforce our nonperforming loans may be limited under federal, state, local and foreign laws; |

• | our ability to comply with existing and new regulations of the collection industry, the failure of which could result in penalties, fines, litigation, damage to our reputation, or the suspension or termination of or required modification to our ability to conduct our business; |

• | investigations or enforcement actions by governmental authorities, including the Consumer Financial Protection Bureau ("CFPB"), which could result in changes to our business practices, negatively impact our portfolio purchasing volume, make collection of account balances more difficult or expose us to the risk of fines, penalties, restitution payments, and litigation; |

• | the possibility that compliance with foreign and U.S. laws and regulations that apply to our international operations could increase our cost of doing business in international jurisdictions; |

• | our ability to raise the funds necessary to repurchase the convertible senior notes or to settle conversions in cash; |

• | our ability to maintain, renegotiate or replace our credit facilities; |

• | changes in interest or exchange rates, which could reduce our net income, and the possibility that future hedging strategies may not be successful, which could adversely affect our results of operations and financial condition, as could our failure to comply with hedge accounting principles and interpretations; and |

• | the risk factors discussed herin and in our other filings with the Securities and Exchange Commission (the "SEC"). |

You should assume that the information appearing in this Annual Report on Form 10-K (this "Form 10-K") is accurate only as of the date it was issued. Our business, financial condition, results of operations and prospects may have changed since that date.

You should carefully consider the factors listed above and review the "Risk Factors" section beginning on page 9, as well as the "Management's Discussion and Analysis of Financial Condition and Results of Operations" section beginning on page 23 and the "Business" section beginning on page 5.

Our forward-looking statements could be wrong in light of these and other risks, uncertainties and assumptions. The future events, developments or results described in, or implied by, this Form 10-K could turn out to be materially different. Except as required by law, we assume no obligation to publicly update or revise our forward-looking statements after the date of this Form 10-K and you should not expect us to do so.

4

Investors should also be aware that while we do, from time to time, communicate with securities analysts and others, we do not selectively disclose to them any material nonpublic information or other confidential commercial information. Accordingly, stockholders should not assume that we agree with any statement or report issued by any analyst regardless of the content of the statement or report. We do not, by policy, confirm forecasts or projections issued by others. Thus, to the extent that reports issued by securities analysts contain any projections, forecasts or opinions, such reports are not our responsibility.

PART I

Item 1. Business.

General

Headquartered in Norfolk, Virginia and incorporated in Delaware, we are a global financial and business services company with operations in the Americas and Europe.

Our primary business is the purchase, collection and management of portfolios of nonperforming loans. The accounts we acquire are primarily the unpaid obligations of individuals owed to credit grantors, which include banks and other types of consumer, retail, and auto finance companies. We acquire portfolios of nonperforming loans in two broad categories: Core and Insolvency. Our Core operation specializes in purchasing and collecting nonperforming loan accounts, which we purchased at a substantial discount to face value since either the credit grantor and/or other third-party collection agencies have been unsuccessful in collecting the full balance owed. Our Insolvency operation consists primarily of purchasing and collecting on nonperforming loan accounts where the customer is involved in a bankruptcy proceeding.

We also provide the following fee-based services:

• | Class action claims recovery services and purchases; |

• | Servicing of consumer bankruptcy accounts in the U.S.; and |

• | To a lesser extent, contingent collections of nonperforming loans in Europe and South America. |

We sold our government services business in January 2017 and PRA Location Services, LLC ("PLS") in June 2017.

We have one reportable segment, accounts receivable management, based on similarities among the operating units, including the nature of the products and services, the nature of the production processes, the types or classes of customers for our products and services, the methods used to distribute our products and services, and the nature of the regulatory environment.

We were initially formed as Portfolio Recovery Associates, L.L.C., a Delaware limited liability company, on March 20, 1996. We formed Portfolio Recovery Associates, Inc. in August 2002 in order to become a publicly traded company and our common stock began trading on the NASDAQ Global Select Market ("NASDAQ") on November 8, 2002. We continued to diversify our business by acquiring Aktiv Kapital AS ("Aktiv"), a Norway-based company specializing in the acquisition and servicing of nonperforming loans throughout Europe and Canada, on July 16, 2014, and subsequently changed our legal name on October 23, 2014 from Portfolio Recovery Associates, Inc. to PRA Group, Inc. We expanded into South America on August 3, 2015 by acquiring 55% of the equity interest in RCB Investimentos S.A. ("RCB"), a servicing platform of nonperforming loans in Brazil, with the remaining 45% of the equity interest owned by the executive team and previous owners of RCB. On April 26, 2016, we completed our public tender offer to purchase 100% of the shares of DTP S.A. ("DTP"), a Polish-based debt collection company, further building our in-house collection efforts in Poland.

All references in this Form 10-K to the "PRA Group," "our," "we," "us," the "Company" or similar terms are to PRA Group, Inc. and its subsidiaries.

Nonperforming Loan Portfolio Purchases

To identify buying opportunities, we maintain an extensive marketing effort with our senior officers contacting known and prospective sellers of nonperforming loans. From these sellers, we have purchased a variety of nonperforming loans including Visa® and MasterCard® credit cards, private label and other credit cards, installment loans, lines of credit, deficiency balances of various types, legal judgments, and trade payables. Sellers of nonperforming loans include major banks, credit unions, consumer finance companies, telecommunication providers, retailers, utilities, automobile finance companies, student loan companies, and other debt owners. The price at which we acquire portfolios depends on the age of the portfolio, whether it is a Core or Insolvency portfolio, geographic distribution, our historical experience with a certain asset type or credit grantor and other similar factors.

5

Nonperforming Loan Portfolio Purchasing Process

We acquire portfolios of nonperforming loans from credit grantors through auctions and negotiated sales. In an auction process, the seller will assemble a portfolio of nonperforming loans and will seek purchase prices from specifically invited potential purchasers. In a privately negotiated sale process, the credit grantor will contact one or more purchasers directly, receive a bid, and negotiate the terms of sale. In either case, typically, invited purchasers will have already successfully completed a qualification process that can include the seller's review of any or all of the following: the purchaser's experience, reputation, financial standing, operating procedures, business practices, and compliance oversight.

We acquire portfolios of nonperforming loans through either single portfolio transactions, referred to as spot sales, or through the pre-arranged purchase of multiple portfolios over time, referred to as forward flow sales. Under a forward flow contract, we agree to purchase nonperforming loans from credit grantors on a periodic basis, at a price equal to a set percentage of face value of the nonperforming loans over a specified time period, generally from three to twelve months.

Nonperforming Loan Portfolio Collection Operations

Call Center Operations

In higher volume markets, our collection efforts leverage internally staffed call centers. In some newer markets or in markets that have less consistent debt purchasing patterns, most notably outside the U.S., we may utilize external vendors to do some of this work. Whether the accounts are being worked internally or externally, we utilize our proprietary analysis to proportionally direct work efforts to those customers most likely to pay. The analysis driving those decisions relies on various models and variables that have the highest correlation to profitable collections from call activity.

Legal Recovery - Core Portfolios

An important component of our collections effort involves our legal recovery operations and the judicial collection of accounts of customers who we believe have the ability, but not the willingness, to resolve their obligations. There are some markets in which the collection process follows a prescribed time-sensitive and sequential set of legal actions, but in the majority of instances, we use models and analysis and select those accounts reflecting a high propensity to pay in a legal environment. Depending on the balance of the receivable and the applicable local collection laws, we determine whether to commence legal action to judicially collect on the receivable. The legal process can take an extended period of time and can be costly, but when accounts are selected properly it also usually generates net cash collections that likely would not have been realized otherwise. We use a combination of internal staff (attorney and support), and external staff to pursue legal collections under certain circumstances.

Insolvency Operations

Insolvency Operations in the U.S. manages customer filings under the U.S. Bankruptcy Code on debtor accounts derived from two sources: (1) our purchased pools of bankrupt accounts and (2) our Core purchased pools of nonperforming loans that have filed for bankruptcy or insolvency protection after being acquired by us. We file proofs of claim ("POCs") or claim transfers and actively manage these accounts through the entire life cycle of the insolvency proceeding in order to substantiate our claims and ensure that we participate in any distributions to creditors. Outside of the U.S., this work is primarily outsourced to third parties.

Insolvency accounts in the U.S. are typically those filed under Chapter 13 of the U.S. Bankruptcy Code, have an associated payment plan that generally ranges from three to five years in duration and can be acquired at any stage in the bankruptcy plan life cycle. Portfolios sold close to the filing of the bankruptcy plan will generally take months to generate cash flow; however, aged portfolios sold years after the filing of the bankruptcy plan will typically generate cash flows immediately. Non-U.S. insolvency accounts may have some slight differences, but generally operate in a similar manner. In Canada, we purchase Consumer Proposal, Consumer Credit Counseling and Bankrupt Accounts. In the UK, we purchase Individual Voluntary Arrangements, Company Voluntary Arrangements, Trust Deeds and Bankrupt Accounts. In Germany, we acquire consumer bankruptcies, which may also consist of small business loans with a personal guarantee.

Fee-Based Services

In addition to the purchase, collection and management of portfolios of nonperforming loans, we provide fee-based services including class action claims recovery purchasing and servicing through Claims Compensation Bureau, LLC ("CCB"); contingent collection of nonperforming loans through PRA Group Europe and RCB; and third-party servicing of bankruptcy accounts in the U.S.

6

Seasonality

Although our business is not impacted significantly by seasonality, cash collections in the Americas tend to be higher in the first and second quarters of the year and lower in the third and fourth quarters of the year; by contrast, cash collections in Europe tend to be higher in the third and fourth quarters of the year. Customer payment patterns are affected by seasonal employment trends, income tax refunds and holiday spending habits geographically.

Competition

Purchased portfolio competition comes from both third-party contingent fee collection agencies and other purchasers of debt that manage their own nonperforming loans or outsource such servicing. Our primary competitors in our fee-for-service business are providers of outsourced receivables management services. Regulatory complexity and burdens, combined with seller preference for experienced portfolio purchasers create significant barriers to successful entry for new competitors. While both markets remain competitive, the contingent fee industry is more fragmented than the purchased portfolio industry.

We face bidding competition in our acquisition of nonperforming loans and in obtaining placements for our fee-for-service businesses. We also compete on the basis of reputation, industry experience and performance. We believe that our competitive strengths include our disciplined and proprietary underwriting process, the extensive data set we have developed as a result of reselling substantially no portfolios since 2002 and inhouse collections, our ability to bid on portfolios at appropriate prices, our reputation from previous portfolio purchase transactions, our ability to close transactions in a timely fashion, our strong relationships with grantors of receivables, our team of well-trained collectors who provide quality customer service while complying with applicable collection laws, and our ability to efficiently and effectively collect on various asset types.

Compliance

Our approach to compliance is multifaceted and comprehensive, and includes the following:

• | our Code of Conduct, which applies to all directors, officers and employees, is available at the Investor Relations page of our website at www.pragroup.com; |

• | compliance and ethics training for our directors, officers and employees; |

• | a confidential telephone and email hotline and web-based portals to report suspected compliance violations, fraud, financial reporting, accounting, and auditing matters and other acts that may be illegal and/or unethical; |

• | regular and annual testing by our compliance and internal audit departments of controls embedded in business processes designed to foster compliance with laws, regulations and internal policy; and |

• | regular evaluation of the legislative and regulatory environment, monitoring of statutory and regulatory changes and relevant case law, so that operations personnel are aware of and in compliance with the laws and judicial decisions that may impact their job duties. |

Regulation

We are subject to a variety of federal, state, local, and foreign laws that establish specific guidelines and procedures that debt collectors must follow when collecting customer accounts, including laws relating to the collection, use, retention, security and transfer of personal information. It is our policy to comply with the provisions of all applicable federal, state, local and foreign laws in all of our activities even though there are frequent changes in these laws and regulations, in their interpretation and application and inconsistencies from jurisdiction to jurisdiction. Our failure to comply with these laws could result in enforcement action against us, the payment of significant fines and penalties, restrictions upon our operations or our inability to recover amounts owed to us. Significant laws and regulations applicable to our business include the following:

• | Fair Debt Collection Practices Act ("FDCPA"), which imposes certain obligations and restrictions on the practices of debt collectors, including specific restrictions regarding the time, place and manner of the communications. |

• | Fair Credit Reporting Act ("FCRA"), which obligates credit information providers to verify the accuracy of information provided to credit reporting agencies and investigate consumer disputes concerning the accuracy of such information. |

• | Gramm-Leach-Bliley Act, which requires that certain financial institutions, including collection agencies, develop policies to protect the privacy of consumers' private financial information and provide notices to consumers advising them of their privacy policies. |

7

• | Electronic Funds Transfer Act, which regulates electronic fund transfer transactions, including a consumer’s right to stop payments on a pre-approved fund transfer and right to receive certain documentation of the transaction. |

• | Telephone Consumer Protection Act ("TCPA"), which, along with similar state laws, places certain restrictions on users of certain automated dialing equipment and pre-recorded messages that place telephone calls to consumers. |

• | Servicemembers Civil Relief Act ("SCRA"), which gives U.S. military service personnel relief from credit obligations they may have incurred prior to entering military service, and may also apply in certain circumstances to obligations and liabilities incurred by a servicemember while serving on active duty. |

• | Health Insurance Portability and Accountability Act, which provides standards to protect the confidentiality of patients' personal healthcare and financial information in the U.S. |

• | U.S. Bankruptcy Code, which prohibits certain contacts with consumers after the filing of bankruptcy petitions and dictates what types of claims will or will not be allowed in a bankruptcy proceeding and how such claims may be discharged. |

• | Americans with Disabilities Act, which requires that telecommunications companies operating in the U.S. take steps to ensure functionally equivalent services are available for their consumers with disabilities, and requires accommodation of consumers with disabilities, such as the implementation of telecommunications relay services. |

• | U.S. Foreign Corrupt Practices Act ("FCPA"), United Kingdom Bribery Act ("UK Bribery Act") and Other Applicable Legislation. Our operations outside the U.S. are subject to the FCPA, which prohibits U.S. companies and their agents and employees from providing anything of value to a foreign official for the purposes of influencing any act or decision of these individuals in order to obtain an unfair advantage or help obtain or retain business. Although similar to the FCPA, the UK Bribery Act is broader in scope and covers bribes given to or received by any person with improper intent. |

• | Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-Frank Act"), which restructured the regulation and supervision of the financial services industry in the U.S. and created the CFPB. The CFPB has rulemaking, supervisory, and enforcement authority over larger consumer debt collectors. The Dodd-Frank Act, along with the Unfair, Deceptive, or Abusive Acts or Practices ("UDAAP") provisions included therein, and the Federal Trade Commission Act, prohibit unfair, deceptive, and/or abusive acts and practices. |

• | Foreign data protection and privacy laws, which include relevant country specific legislation in the United Kingdom and other European countries where we operate that regulate the processing of information relating to individuals, including the obtaining, holding, use or disclosure of such information; the Personal Information Protection and Electronic Documents Act, which aims to protect personal information that is collected, used or disclosed in certain circumstances for purposes of electronic commerce in Canada; and the EU Data Protection Directive, which will be replaced by the General Data Protection Regulation, effective as of May 25, 2018, which regulates the processing and free movement of personal data within the EU and transfer of such data outside the EU. |

• | Consumer Credit Act 1974 (and its related regulations), Unfair Terms in Consumer Contracts Regulations of 1999 and the Financial Conduct Authority's consumer credit conduct of business rules, which apply to our international operations and govern consumer credit agreements. |

In addition, certain of our EU subsidiaries are subject to capital adequacy and liquidity requirements as prescribed by the Swedish Financial Supervisory Authority ("SFSA").

On September 9, 2015, Portfolio Recovery Associates, LLC ("PRA"), our wholly owned subsidiary, entered into a consent order with the CFPB, settling a previously disclosed investigation of certain debt collection practices of PRA (the "Consent Order"). PRA entered into the Consent Order for settlement purposes, without admitting the truth of the allegations, other than the jurisdictional facts. Among other things, the Consent Order required PRA to: (i) vacate 837 judgments obtained after the applicable statute of limitations, refund $860,607 in payments received on account of such judgments and waive the remaining $3.4 million in judgment balances; (ii) refund $18.2 million in Litigation Department Calls Restitution, as defined in the Consent Order; and (iii) pay an $8.0 million civil money penalty to the CFPB.

Employees

As of December 31, 2017, we employed 5,154 full-time equivalents globally. We believe that our relations with our employees are generally satisfactory. While none of our North American employees are represented by a union or covered by a collective bargaining agreement, in Europe we work closely with a number of Works Councils, and in countries where it is the customary local practice, such as Finland and Spain, we have collective bargaining agreements.

8

Available Information

We make available on or through our website, www.pragroup.com, certain reports that we file with or furnish to the SEC in accordance with the Securities Exchange Act of 1934, as amended (the "Exchange Act"). These include our Annual Reports on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act ("SEC Filings"). We make this information available on our website free of charge as soon as reasonably practicable after we electronically file the information with or furnish it to the SEC. The information that is filed with the SEC may be read or copied at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. In addition, information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at: www.sec.gov.

The information contained on, or that can be accessed through our website, is not, and shall not be deemed to be, a part of this Form 10-K or incorporated into any other filings we make with the SEC.

Reports filed with, or furnished to, the SEC are also available free of charge upon request by contacting our corporate office at:

PRA Group, Inc.

Attn: Investor Relations

120 Corporate Boulevard, Suite 100

Norfolk, Virginia 23502

Item 1A. Risk Factors.

An investment in our Company involves risk, including the possibility that the value of the investment could fall substantially. The following are risks that could materially affect our business, results of operations, financial condition, liquidity, cash flows, and the value of, and return on, an investment in our Company.

Risks related to our operations and industry

A prolonged economic recovery or deterioration in the economic or inflationary environment in the Americas or Europe could have an adverse effect on our business and results of operations.

Our performance may be adversely affected by economic, political or inflationary conditions in any market in which we operate. These conditions could include regulatory developments, changes in global or domestic economic policy, legislative changes, the sovereign debt crises experienced in several European countries and the uncertainty on the future of the EU as a result of the United Kingdom's departure from the EU. Deterioration in economic conditions, a prolonged economic recovery, or a significant rise in inflation could cause personal bankruptcy and insolvency filings to increase, and the ability of consumers to pay their debts could be adversely affected. This may in turn adversely impact our business and financial results. Deteriorating economic conditions or a prolonged recovery could also adversely impact the businesses to which we provide fee-based services, which could reduce our fee income and cash flow.

If global credit market conditions and the stability of global banks deteriorate, it could negatively impact the generation of comprehensive receivable buying opportunities and our business, financial results and ability to succeed in foreign markets could be adversely affected. If conditions in major credit markets deteriorate, the amount of consumer or commercial lending and financing could be reduced, thus decreasing the volume of nonperforming loans available for our purchase.

Other factors associated with the economy that could influence our performance include the financial stability of the lenders on our bank loans and credit facilities and our access to capital and credit. The financial turmoil that adversely affected the banking system and financial markets in recent years resulted in the tightening of credit markets. Although there has been some improvement, a worsening of current conditions could have a negative impact on our business, including a decrease in the value of our financial investments and the insolvency of lending institutions, including the lenders on our bank loans and credit facilities, resulting in our difficulty in or inability to obtain credit. These and other economic factors could have an adverse effect on our financial condition and results of operations.

9

We may not be able to continually replace our nonperforming loans with additional portfolios sufficient to operate efficiently and profitably, and/or we may not be able to purchase nonperforming loans at appropriate prices.

To operate profitably, we must acquire and service a sufficient amount of nonperforming loans to generate revenue that exceeds our expenses. Fixed costs such as salaries and other compensation expense constitute a significant portion of our overhead and, if we do not replace the nonperforming loan portfolios we service with additional portfolios, we may have to reduce the number of our collection personnel. We would then have to rehire collection staff if we subsequently obtain additional portfolios. These practices could lead to:

• | low employee morale; |

• | fewer experienced employees; |

• | higher training costs; |

• | disruptions in our operations; |

• | loss of efficiency; and |

• | excess costs associated with unused space in our facilities. |

The availability of nonperforming loan portfolios at prices that generate an appropriate return on our investment depends on a number of factors both within and outside of our control, including the following:

• | the continuation of high levels of consumer debt obligations; |

• | sales of nonperforming loan portfolios by debt owners; and |

• | competitive factors affecting potential purchasers and credit grantors of receivables. |

Furthermore, heightened regulation of the credit card and consumer lending industry or changing credit origination strategies may result in decreased availability of credit to consumers, potentially leading to a future reduction in nonperforming loans available for purchase from debt owners. Conversely, lower regulatory barriers with respect to debt buyers could lead to increased participants in the debt collection industry, which could, in turn, impact the supply of nonperforming loans available for purchase. We cannot predict how our ability to identify and purchase nonperforming loans and the quality of those nonperforming loans would be affected if there were a shift in lending practices, whether caused by changes in the regulations or accounting practices applicable to debt owners or debt buyers, a sustained economic downturn or otherwise.

Moreover, there can be no assurance that debt owners will continue to sell their nonperforming loans consistent with recent levels or at all, or that we will be able to bid competitively for those portfolios. Because of the length of time involved in collecting on acquired portfolios and the variability in the timing of our collections, we may not be able to identify trends and make changes in our purchasing strategies in a timely manner. If we are unable to maintain our business or adapt to changing market needs as well as our current or future competitors, we may experience reduced access to nonperforming loan portfolios at appropriate prices and, therefore, reduced profitability.

Currently, a number of large banks that historically sold nonperforming loans in the U.S. are not selling such debt. This includes sellers of bankrupt accounts, some of whom have elected to stop selling such accounts because they believe that regulatory guidance concerning sales of bankruptcy accounts is ambiguous. Should these conditions worsen, it could negatively impact our ability to replace our nonperforming loans with additional portfolios sufficient to operate profitably.

We may not be able to collect sufficient amounts on our nonperforming loans to fund our operations.

Our principal business consists of acquiring and liquidating nonperforming loans that consumers or others have failed to pay. The debt owners have typically made numerous attempts to recover on their receivables, often using a combination of in-house recovery efforts and third-party collection agencies. These nonperforming loans are difficult to collect, and we may not collect a sufficient amount to cover our investment and the costs of running our business.

10

For financial reporting purposes, we utilize the interest method of revenue recognition for determining our income recognized on finance receivables, which is based on an analysis of projected cash flows that may prove to be less than anticipated and could lead to the incurrence of allowance charges which would reduce our net finance receivables income.

We utilize the interest method to determine income recognized on finance receivables under the guidance of Financial Accounting Standards Board ("FASB") Accounting Standards Codification 310-30, "Loans and Debt Securities Acquired with Deteriorated Credit Quality" ("ASC 310-30"). Under this method, pools of receivables we acquire are modeled upon their projected cash flows. A yield is then established which, when applied to the unamortized purchase price of the receivables, results in the recognition of income at a constant yield relative to the remaining balance in the pool. Each pool is analyzed regularly to assess the actual performance compared to that derived from our models. Under ASC 310-30, rather than lowering the estimated yield if the collection estimates are not received or projected to be received, the carrying value of a pool would be written down to maintain the then current yield and is shown as a reduction in revenue in the consolidated income statements with a corresponding valuation allowance offsetting finance receivables, net, on the consolidated balance sheets. As a result, if the accuracy of the modeling process deteriorates or there is a significant decline in anticipated future cash flows, we could incur reductions in future revenues resulting from additional allowance charges, which could reduce our profitability in a given period.

Our collections may decrease if certain types of insolvency proceedings and bankruptcy filings involving liquidations increase.

Various economic trends and potential changes to existing legislation may contribute to an increase in the amount of personal bankruptcy and insolvency filings. Under certain of these filings, a debtor's assets may be sold to repay creditors, but because most of the receivables we collect through our collections operations are unsecured, we typically would not be able to collect on those receivables. Although our insolvency collections business could benefit from an increase in personal bankruptcies and insolvencies, we cannot ensure that our collections operations business would not decline with an increase in personal insolvencies or bankruptcy filings or changes in related regulations or practices. If our actual collection experience with respect to a nonperforming or insolvent bankrupt receivables portfolio is significantly lower than the total amount we projected when we purchased the portfolio, our financial condition and results of operations could be adversely impacted.

Our international operations expose us to risks which could harm our business, results of operations and financial condition.

A significant portion of our operations is conducted outside the U.S. This could expose us to adverse economic, industry and political conditions that may have a negative impact on our ability to manage our existing operations or pursue alternative strategic transactions, which could have a negative effect on our business, results of operations and financial condition.

The global nature of our operations expands the risks and uncertainties described elsewhere in this section, including the following:

• | changes in local political, economic, social and labor conditions in the markets in which we operate, including Europe, Brazil and Canada; |

• | foreign exchange controls on currency conversion and the transfer of funds that might prevent us from repatriating cash earned in countries outside the U.S. in a tax-efficient manner; |

• | currency exchange rate fluctuations, currency restructurings, inflation or deflation, and our ability to manage these fluctuations through a foreign exchange risk management program; |

• | different employee/employer relationships, laws and regulations and existence of employment tribunals and Works Councils; |

• | laws and regulations imposed by foreign governments, including those governing data security, sharing and transfer; |

• | potentially adverse tax consequences resulting from changes in tax laws in the foreign jurisdictions in which we operate or challenges to our interpretations and application of complex international tax laws; |

• | logistical, communications and other challenges caused by distance and cultural and language differences, each making it harder to do business in certain jurisdictions; |

• | risks related to crimes, strikes, riots, civil disturbances, terrorist attacks, wars and natural disasters; |

• | volatility of global credit markets and the availability of consumer credit and financing in our international markets; |

• | uncertainty as to the enforceability of contract and intellectual property rights under local laws; |

11

• | the potential of forced nationalization of certain industries, or the impact on creditors' rights, consumer disposable income levels, flexibility and availability of consumer credit, and the ability to enforce and collect aged or charged-off debts stemming from foreign governmental actions, whether through austerity or stimulus measures or initiative, intended to control or influence macroeconomic factors such as wages, unemployment, national output or consumption, inflation, investment, credit, finance, taxation or other economic drivers; |

• | the presence of varying levels of business corruption in international markets and the effect of various anti-corruption and other laws on our foreign operations; |

• | the impact on our day-to-day operations and our ability to staff our international operations given our high employee turnover rates, changing labor conditions and long-term trends towards higher wages in developed and emerging international markets as well as the potential impact of union organizing efforts; |

• | potential damage to our reputation due to non-compliance with foreign and local laws; and |

• | the complexity and necessity of using non-U.S. representatives, consultants and other third-party vendors. |

Furthermore, our future tax expense could be affected by changes in the mix of earnings in countries with differing statutory tax rates, changes in the valuation of deferred tax assets and liabilities, or changes in tax laws or their interpretation. The determination of the provision for income taxes and other tax liabilities regarding our global operations requires significant judgment. Although we believe our estimates are reasonable, the ultimate tax outcome may differ from the amounts recorded in our financial statements and may adversely affect our financial results in the period(s) for which such determination is made.

Our tax filings are subject to audit by domestic and foreign tax authorities. These audits may result in assessments of additional taxes, adjustments to the timing of taxable income or deductions, or re-allocations of income among tax jurisdictions.

Any one of these factors could adversely affect our business, results of operations and financial condition.

The impact of the Tax Act, including interpretations and determinations by taxing authorities, could have an adverse effect on our financial condition and results of operations.

On December 22, 2017, the President of the United States of America signed the Tax Act, which includes a broad range of tax reform provisions affecting businesses, including a reduction in the U.S. federal corporate tax rate from 35% to 21%; a one-time transition tax on certain unrepatriated earnings of foreign subsidiaries; generally eliminating U.S. federal income taxes on dividends from foreign subsidiaries; requiring a current inclusion in U.S. federal taxable income of certain earnings of controlled foreign corporations referred to as Global Intangible Low-Taxed Income; creating the base erosion anti-abuse tax, a new minimum tax; creating a new limitation on deductible interest expense; and increased limitations on the deductibility of executive compensation. The Tax Act will impact our effective tax rate for fiscal years 2018 and beyond. The new law makes broad and complex changes to the U.S. tax code and we expect to see future regulatory, administrative or legislative guidance. While we expect that the lowering of the U.S. federal tax rate will have a positive impact on our worldwide effective tax rate, we are analyzing the Tax Act to determine the full impact of the new tax law. To the extent any future guidance differs from our preliminary interpretation of the law, it could have a material effect on our financial position and results of operations.

In addition, many countries in the EU and around the world have adopted and/or proposed changes to current tax laws. Further, organizations such as the Organization for Economic Cooperation and Development have published actions that, if adopted by countries where we do business, could increase our tax obligations in those countries. Due to the scale of our U.S. and international business activities, many of these enacted and proposed changes to the taxation of our activities could increase our worldwide effective tax rate and harm our financial position and results of operations.

Goodwill or other intangible asset impairment charges could negatively impact our net income and stockholders' equity.

We have recorded a significant amount of goodwill as a result of our acquisitions. Goodwill is not amortized, but is tested for impairment at the reporting unit level. Goodwill is required to be tested for impairment annually and between annual tests if events or circumstances indicate that it is more likely than not that the fair value of a reporting unit is less than its carrying amount. There are numerous risks that may cause the fair value of a reporting unit to fall below its carrying amount, which could lead to the recognition of goodwill impairment. These risks include, but are not limited to, adverse changes in macroeconomic conditions, the business climate, or the market for the entity's products or services; significant variances between actual and expected financial results; negative or declining cash flows; lowered expectations of future results; failure to realize anticipated synergies from acquisitions; significant expense increases; a more likely-than-not expectation of selling or disposing all or a portion of a reporting unit; the loss of key personnel; an adverse action or assessment by a regulator; and a sustained decrease in the Company's share price.

12

Our goodwill impairment testing involves the use of estimates and the exercise of judgment, including judgments regarding expected future business performance and market conditions. Significant changes in our assessment of such factors, including the deterioration of market conditions, could affect our assessment of the fair value of one or more of our reporting units and could result in a goodwill impairment charge in a future period.

Other intangible assets, such as client and customer relationships, non-compete agreements and trademarks, are amortized. Risks such as those that could lead to the recognition of goodwill impairment, could also lead to the recognition of other intangible asset impairment.

The vote by the UK to leave the EU, and the ultimate exit of the UK from the EU, could adversely impact our business, results of operations and financial condition.

On June 23, 2016, the UK voted to leave the EU. Although the vote had no binding legal effect, it adversely impacted global markets and resulted in a decline in the value of the British pound as compared to the U.S. dollar and other currencies. The UK's exit negotiations with the EU officially began in June 2017. It is expected that the UK's actual exit from the EU, or Brexit, will take place in March 2019. However, perceptions concerning the impact of the UK's withdrawal from the EU may adversely affect business activity, political stability and economic conditions in the UK, the EU and globally, which could in turn adversely affect European or worldwide political, regulatory, economic and financial market conditions.

As of December 31, 2017, the total estimated remaining collections ("ERC") of our UK portfolios constituted approximately 17% of our consolidated ERC. We expect volatility in exchange rates in the short term as the UK negotiates its exit from the EU. A weaker British pound compared to the U.S. dollar during a reporting period could cause local currency results of our UK operations to be translated into fewer U.S. dollars. In the longer term, any impact from Brexit on our business, results of operations and financial condition will depend on the final terms negotiated by the UK and the EU, including arrangements concerning taxes and financial services regulation.

Our loss contingency accruals may not be adequate to cover actual losses.

We are involved in judicial, regulatory, and arbitration proceedings or investigations concerning matters arising from our business activities. We believe that we have adopted reasonable compliance policies and procedures and believe we have meritorious defenses in all material litigation pending against us. However, there can be no assurance as to the ultimate outcome. We establish accruals for potential liability arising from legal proceedings when it is probable that such liability has been incurred and the amount of the loss can be reasonably estimated. We may still incur legal costs for a matter even if we have not accrued a liability. In addition, actual losses may be higher than the amount accrued for a certain matter, or in the aggregate. An unfavorable resolution of a legal proceeding or claim could adversely impact our business, financial condition, results of operations, or liquidity. For more information, refer to the "Litigation and Regulatory Matters" section of Note 14 to our Consolidated Financial Statements included in Item 8 of this Form 10-K ("Note 14").

Class action suits and other litigation could divert our management's attention from operating our business and increase our expenses.

Grantors, nonperforming loan purchasers and third-party collection agencies and attorneys in the consumer credit industry are frequently subject to putative class action lawsuits and other litigation. Claims include failure to comply with applicable laws and regulations and improper or deceptive origination and servicing practices. An unfavorable outcome in a class action suit or other litigation could adversely affect our results of operations, financial condition, cash flows and liquidity. Even when we prevail or the basis for the litigation is groundless, considerable time, energy and resources may be needed to respond, and such class action lawsuits or other litigation could adversely affect our results of operations, financial condition and cash flows.

The occurrence of cyber incidents, or a deficiency in our cyber-security, could negatively impact our business by disrupting our operations, compromising or corrupting our confidential information or damaging our image, all of which could negatively impact our business and financial results.

Our business is highly dependent on our ability to process and monitor a large number of transactions across markets and in multiple currencies. As our geographical reach expands, maintaining the security of our systems and infrastructure becomes more significant. Privacy laws in the U.S., Europe and elsewhere govern the collection and transmission of personal data. As our reliance on technology has increased, so have the risks posed to our systems, both internal and those we have outsourced. Our three primary risks that could directly result from the occurrence of a cyber incident are operational interruption, damage to our image, and private data exposure. Private data may include customer information, our employees' personally identifiable information, or proprietary business information such as underwriting and collections methodologies. We have implemented solutions, processes, and procedures to help mitigate these risks, but these measures, as well as our organization's increased awareness of our risk of a cyber incident do not guarantee that our business, reputation or financial results will not be negatively impacted by such an incident.

13

However, should such a cyber incident occur, we may be required to expend significant additional resources to notify affected consumers, modify our protective measures or to investigate and remediate vulnerabilities or other exposures. Additionally, we may be subject to fines, penalties, litigation costs and settlements and financial losses that may not be fully covered by our cyber insurance.

Risks associated with governmental regulation and laws

Our ability to collect and enforce our nonperforming loans may be limited under federal, state and foreign laws, regulations and policies.

The businesses conducted by our operating subsidiaries are subject to licensing and regulation by governmental and regulatory bodies in the many jurisdictions in which we operate. Federal and state laws and the laws and regulations of the foreign countries in which we operate may limit our ability to collect on and enforce our rights with respect to our nonperforming loans regardless of any act or omission on our part. Some laws and regulations applicable to credit issuers may preclude us from collecting on nonperforming loans we purchase if the credit issuer previously failed to comply with applicable laws in generating or servicing those receivables. Collection laws and regulations also directly apply to our business. Such laws and regulations are extensive and subject to change. A variety of state, federal and international laws and regulations govern the collection, use, retention, transmission, sharing and security of consumer data. Consumer protection and privacy protection laws, changes in the ways that existing rules or laws are interpreted or enforced and any procedures that may be implemented as a result of regulatory consent orders may adversely affect our ability to collect on our nonperforming loans and may harm our business. Our failure to comply with laws or regulations applicable to us could limit our ability to collect on our receivables, which could reduce our profitability and harm our business.

Failure to comply with government regulation of the collections industry could result in penalties, fines, litigation, damage to our reputation or the suspension or termination of our ability to conduct our business.

The collections industry throughout the markets in which we operate is governed by various laws and regulations, many of which require us to be a licensed debt collector. Our industry is also at times investigated by regulators and offices of state attorneys general, and subpoenas and other requests or demands for information may be issued by governmental authorities who are investigating debt collection activities. These investigations may result in enforcement actions, fines and penalties, or the assertion of private claims and lawsuits. If any such investigations result in findings that we or our vendors have failed to comply with applicable laws and regulations, we could be subject to penalties, litigation losses and expenses, damage to our reputation, or the suspension or termination of, or required modification to, our ability to conduct collections, which would adversely affect our business, results of operations and financial condition.

In a number of jurisdictions, we must maintain licenses to perform debt recovery services and must satisfy related bonding requirements. Our failure to comply with existing licensing requirements, changing interpretations of existing requirements, or adoption of new licensing requirements, could restrict our ability to collect in certain jurisdictions, subject us to increased regulation, increase our costs, or adversely affect our ability to collect our receivables.

Some laws, among other things, also may limit the interest rate and the fees that a credit grantor may impose on our consumers, limit the time in which we may file legal actions to enforce consumer accounts, and require specific account information for certain collection activities. In addition, local requirements and court rulings in various jurisdictions also may affect our ability to collect.

Regulations and statutes applicable to our industry further provide that, in some cases, consumers cannot be held liable for, or their liability may be limited with respect to, charges to their debt or credit card accounts that resulted from unauthorized use of their credit. These laws, among others, may limit our ability to recover amounts owing with respect to the receivables, whether or not we committed any wrongful act or omission in connection with the account.

If we fail to comply with any applicable laws and regulations discussed above, such failure could result in penalties, litigation losses and expenses, damage to our reputation, or otherwise impact our ability to conduct collections efforts, which could adversely affect our business, results of operations and financial condition.

Investigations or enforcement actions by governmental authorities may result in changes to our business practices; negatively impact our receivables portfolio purchasing volume; make collection of receivables more difficult; or expose us to the risk of fines, penalties, restitution payments and litigation.

Our debt collection activities and business practices are subject to review from time to time by various governmental authorities and regulators, including the CFPB, which may commence investigations or enforcement actions or reviews targeted at businesses in the financial services industry. These reviews may involve governmental authority consideration of individual consumer complaints, or could involve a broader review of our debt collection policies and practices. Such investigations could lead to

14

assertions by governmental authorities that we are not complying with applicable laws or regulations. In such circumstances, authorities may request or seek to impose a range of remedies that could involve potential compensatory or punitive damage claims, fines, restitution payments, sanctions or injunctive relief, that if agreed to or granted, could require us to make payments or incur other expenditures that could have an adverse effect on our financial position. The CFPB has the authority to obtain cease and desist orders (which can include orders for restitution or rescission of contracts, as well as other kinds of affirmative relief), recover costs, and impose monetary penalties (ranging from $5,000 per day to over $1 million per day, depending on the nature and gravity of the violation). In addition, where a company has violated Title X of the Dodd-Frank Act or CFPB regulations implemented thereunder, the Dodd-Frank Act empowers state attorneys general and other state regulators to bring civil actions to remedy violations under state law. Government authorities could also request or seek to require us to cease certain of our practices or institute new practices. Negative publicity relating to investigations or proceedings brought by governmental authorities could have an adverse impact on our reputation, could harm our ability to conduct business with industry participants, and could result in financial institutions reducing or eliminating sales of receivables portfolios to us which would harm our business and negatively impact our results of operations. Moreover, changing or modifying our internal policies or procedures, responding to governmental inquiries and investigations and defending lawsuits or other proceedings could require significant efforts on the part of management and result in increased costs to our business. In addition, such efforts could divert management's full attention from our business operations. All of these factors could have an adverse effect on our business, results of operations, and financial condition.

The CFPB has issued civil investigative demands to many companies that it regulates, and is currently examining practices regarding the collection of consumer debt. In September 2015, we entered into the Consent Order with the CFPB settling a previously disclosed investigation of certain debt collection practices of PRA. The Consent Order resulted in the payment of $19 million in consumer refunds and an $8 million penalty. In addition, we were required to cease collection of approximately $3 million of consumer debt and modify some of our collections practices. Although we have implemented the requirements of the Consent Order, there can be no assurance that additional litigation or new industry regulations currently under consideration by the CFPB would not have an adverse effect on our business, results of operations, and financial condition. In addition, the CFPB monitors our compliance with the Consent Order and could make a determination that we have failed to adhere to our obligations. Such a determination could result in additional inquiries, penalties or liabilities, which could have an adverse effect on our business, results of operations, and financial condition.

Compliance with complex and evolving foreign and U.S. laws and regulations that apply to our international operations could increase our cost of doing business in international jurisdictions.

We operate on a global basis with offices and activities in a number of jurisdictions throughout the Americas and Europe. We face increased exposure to risks inherent in conducting business internationally, including compliance with complex foreign and U.S. laws and regulations that apply to our international operations, which could increase our cost of doing business in international jurisdictions. These laws and regulations include those related to taxation and anti-corruption laws such as the FCPA, the UK Bribery Act and other local laws prohibiting corrupt payments to governmental officials. Given the complexity of these laws, there is a risk that we may inadvertently breach certain provisions of these laws, such as through the negligent behavior of an employee or our failure to comply with certain formal documentation requirements. Violations of these laws and regulations by us, any of our employees or our third-party vendors, either inadvertently or intentionally, could result in fines and penalties, criminal sanctions, restrictions on our operations and limits on our ability to offer our products and services in one or more countries. Violations of these laws could also adversely affect our business, brand, international expansion efforts, ability to attract and retain employees and results of operations.

Risks associated with indebtedness

We utilize bank loans, credit facilities and convertible notes to finance our business activities, which could negatively impact our liquidity and business operations if we are unable to retain, renegotiate, expand or replace our bank loans and credit facilities or raise the necessary funds to repurchase the convertible notes.

As described in Note 6 to our Consolidated Financial Statements included in Item 8 of this Form 10-K, our sources of financing include a North American credit facility, a European multicurrency revolving credit facility and convertible senior notes. The credit facilities contain financial and other restrictive covenants, including restrictions on how we operate our business and our ability to pay dividends to our stockholders. Failure to satisfy any one of these covenants could result in negative consequences including the following:

• | acceleration of outstanding indebtedness; |

• | exercise by our lenders of rights with respect to the collateral pledged under certain of our outstanding indebtedness; |

• | our inability to continue to purchase nonperforming loans needed to operate our business; or |

15

• | our inability to secure alternative financing on favorable terms, if at all. |

If we are unable to retain, renegotiate, expand or replace our credit facilities, including as a result of failure to satisfy the restrictive covenants contained in them, our liquidity and business operations could be impacted negatively.

We have additional indebtedness in the form of Convertible Senior Notes due 2020 and 2023 (collectively the "Notes") and may not have the ability to raise the funds necessary to repurchase the Notes upon a fundamental change or to settle conversions in cash. Our ability to make scheduled payments of the principal of, to pay interest on, or to refinance our indebtedness, including the Notes, or to make cash payments in connection with any conversion of the Notes depends on our future performance, which is subject to economic, financial, competitive and other factors beyond our control. Our ability to refinance our indebtedness will depend on the capital markets and our financial condition at that time. We may not be able to engage in any of these activities or engage in these activities on desirable terms, which could result in a default on our debt obligations. In addition, in the event the conditional conversion features of the Notes are triggered, holders of the Notes are entitled to convert the Notes into shares of our common stock at any time during specified periods at their option, subject to the terms of the indenture governing the Notes. Upon conversion, unless we elect to deliver solely shares of our common stock to settle such conversion (other than paying cash in lieu of delivering any fractional shares of our common stock), we will be required to make cash payments in respect of the Notes. However, we may not have enough available cash or be able to obtain financing at the time we are required to repurchase Notes surrendered to settle conversions in cash, and our ability to repurchase the Notes or pay cash upon conversion may be limited by law. Any issuance of shares of our common stock upon conversion of the Notes would dilute the ownership interest of our stockholders.

We may be restricted from paying cash upon conversion of the Notes, repurchasing the Notes for cash when required and repaying the Notes at maturity or upon acceleration following an event of default under the Notes unless we repay all amounts outstanding under, and terminate, our North American Credit Agreement, and our future indebtedness may contain limitations on our ability to pay cash upon conversion of the Notes and on our ability to repurchase the Notes.

The terms of our North American Credit Agreement prohibit us from paying cash upon conversion of the Notes, repurchasing the Notes for cash when required upon the occurrence of a fundamental change and repaying the Notes at maturity or upon acceleration following an event of default under the indenture governing the Notes if a default or an event of default exists on the date of such required payment, repurchase or repayment, as applicable, or certain other conditions are not met, including pro forma compliance with the financial covenants and having “Sufficient Liquidity” (described below). As a result, we will be restricted from making such payments unless the default or event of default under our North American Credit Agreement is cured or waived, such conditions are met and/or we repay all amounts then outstanding under, and terminate, our North American Credit Agreement.

In addition, under our North American Credit Agreement our ability to settle conversions of the Notes in cash requires that immediately prior to any such conversion, our cash and cash equivalents (including our availability under our domestic and multi-currency revolving facilities under our North American Credit Agreement) be at least 115% of the sum of the principal amount of the Notes to be paid in cash (“Sufficient Liquidity”). The terms of any additional indebtedness incurred as permitted by our North American Credit Agreement may contain similar or more onerous restrictions than the foregoing.

Our failure to repurchase Notes, to pay, when due, cash upon conversion of the Notes or repay the Notes at maturity or upon acceleration following an event of default under the indenture governing the Notes would constitute a default under the indenture governing the Notes. A default under the indenture may constitute a default under our North American Credit Agreement.

Changes in interest rates could increase our interest expense and reduce our net income.

Our revolving credit facilities bear interest at variable rates. Increases in interest rates could increase our interest expense which would, in turn, lower our earnings. From time to time, we may enter into hedging transactions to mitigate our interest rate risk on all or a portion of our debt. Hedging strategies rely on assumptions and projections. If these assumptions and projections prove to be incorrect or our hedges do not adequately mitigate the impact of changes in interest rates, we may experience volatility in our earnings that could adversely affect our results of operations and financial condition.

Item 1B. Unresolved Staff Comments.

None.

16

Item 2. Properties.

Our corporate headquarters and primary domestic operations facility are located in Norfolk, Virginia. In addition, we have operational centers, all of which are leased except the facilities in Kansas and Tennessee, in the following locations in the Americas and Europe:

Americas | ||||

- Birmingham, Alabama | - Jackson, Tennessee | |||

- Burlington, North Carolina | - London, Ontario, Canada | |||

- Hampton, Virginia | - North Richland Hills, Texas | |||

- Henderson, Nevada | - San Diego, California | |||

- Hutchinson, Kansas | - São Paulo, Brazil | |||

Europe | ||||

- Bromley, United Kingdom | - Madrid, Spain | |||

- Duisburg, Germany | - Oslo, Norway | |||

- Eisenstadt, Austria | - Padova, Italy | |||

- Helsinki, Finland | - Uppsala, Sweden | |||

- Kilmarnock, United Kingdom | - Warsaw, Poland | |||

- Luxembourg, Luxembourg | - Zug, Switzerland | |||

We also lease several less significant facilities in various locations throughout the Americas and Europe, which are not listed above. We do not consider any specific leased or owned facility to be material to our operations. We believe that equally suitable alternative facilities are available throughout our geographic market areas.

Item 3. Legal Proceedings.

We and our subsidiaries are from time to time subject to a variety of routine legal and regulatory claims, inquiries and proceedings, most of which are incidental to the ordinary course of our business. We initiate lawsuits against customers and are occasionally countersued by them in such actions. Also, customers, either individually, as members of a class action, or through a governmental entity on behalf of customers, may initiate litigation against us in which they allege that we have violated a state or federal law in the process of collecting on an account. From time to time, other types of lawsuits are brought against us.

Refer to Note 14 for information regarding legal proceedings in which we are involved.

Item 4. Mine Safety Disclosures.

Not applicable.

17

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Price Range of Common Stock

Our common stock is traded on NASDAQ under the symbol "PRAA." The following table sets forth the high and low sales price for our common stock, as reported by NASDAQ, for the periods indicated.

2017 | 2016 | ||||||

High | Low | High | Low | ||||

Quarter ended March 31, | $42.70 | $31.75 | $35.98 | $20.00 | |||

Quarter ended June 30, | $38.45 | $30.95 | $34.15 | $22.51 | |||

Quarter ended September 30, | $40.15 | $25.72 | $34.99 | $21.93 | |||

Quarter ended December 31, | $36.00 | $26.85 | $39.70 | $23.15 | |||

Based on information provided by our transfer agent and registrar, as of February 16, 2018, there were 54 holders of record and 38,830 beneficial owners of our common stock.

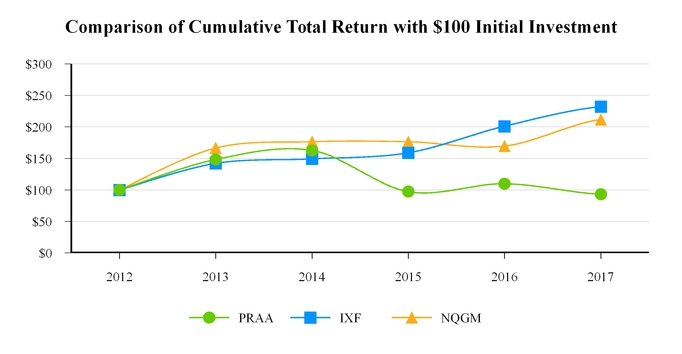

Stock Performance

The following graph and subsequent table compares from December 31, 2012 to December 31, 2017, the cumulative stockholder returns assuming an initial investment of $100 in our common stock (PRAA), the stocks comprising the NASDAQ Financial 100 (IXF) and the stocks comprising the NASDAQ Global Market Composite Index (NQGM) at the beginning of the period. Any dividends paid during the five year period are assumed to be reinvested.

Ticker | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |||||||||||||||||||

PRA Group, Inc. | PRAA | $ | 100 | $ | 148 | $ | 163 | $ | 97 | $ | 110 | $ | 93 | ||||||||||||

NASDAQ Financial 100 | IXF | $ | 100 | $ | 142 | $ | 149 | $ | 159 | $ | 201 | $ | 232 | ||||||||||||

NASDAQ Global Market Composite Index | NQGM | $ | 100 | $ | 167 | $ | 177 | $ | 176 | $ | 170 | $ | 212 | ||||||||||||

The comparisons of stock performance shown above are not intended to forecast or be indicative of possible future performance of our common stock. We do not make or endorse any predictions as to our future stock performance.

18

Dividend Policy

Our board of directors sets our dividend policy. We do not currently pay regular dividends on our common stock and did not pay dividends in the three years ended December 31, 2017; however, our board of directors may determine in the future to declare or pay dividends on our common stock. Under the terms of our credit facilities, cash dividends may not exceed $20 million in any fiscal year without the consent of our lenders. Any future determination as to the declaration and payment of dividends will be at the discretion of our board of directors and will depend on then existing conditions, including our results of operations, financial condition, contractual restrictions, capital requirements, business prospects and other factors that our board of directors may consider relevant.

Recent Sales of Unregistered Securities

None.

Securities Authorized for Issuance Under Equity Compensation Plans

For information regarding securities authorized for issuance under equity compensation plans see Note 9 to our Consolidated Financial Statements included in Item 8 of this Form 10-K.

Share Repurchase Programs

On October 22, 2015, our board of directors authorized a share repurchase program to purchase up to $125 million of our outstanding shares of common stock.

During the second quarter of 2017, we repurchased approximately $44.9 million of our outstanding shares of common stock which concluded the program.

19

Item 6. Selected Financial Data.

The following selected financial data should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" included in Item 7 of this Form 10-K and our Consolidated Financial Statements and the related notes thereto included in Item 8 of this Form 10-K . Certain prior year amounts have been reclassified for consistency with the current period presentation.

Consolidated Income Statement, Operating and Other Financial Data Amounts in thousands, except per share amounts | |||||||||||||||||||

Years Ended December 31, | |||||||||||||||||||

Income Statement Data: | 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||

Revenues: | |||||||||||||||||||

Income recognized on finance receivables, net | $ | 780,803 | $ | 745,119 | $ | 865,122 | $ | 807,474 | $ | 663,546 | |||||||||

Fee income | 24,916 | 77,381 | 64,383 | 65,675 | 71,532 | ||||||||||||||

Other revenue | 7,855 | 8,080 | 12,513 | 7,820 | 57 | ||||||||||||||

Total revenues | 813,574 | 830,580 | 942,018 | 880,969 | 735,135 | ||||||||||||||

Operating expenses: | |||||||||||||||||||

Compensation and employee services | 273,033 | 258,846 | 268,345 | 234,531 | 192,474 | ||||||||||||||

Legal collection expenses | 119,398 | 132,202 | 129,456 | 139,161 | 124,551 | ||||||||||||||

Agency fees | 35,530 | 44,922 | 32,188 | 16,399 | 5,901 | ||||||||||||||

Outside fees and services | 62,792 | 63,098 | 65,155 | 55,821 | 31,615 | ||||||||||||||

Communication | 33,132 | 33,771 | 33,113 | 33,085 | 28,161 | ||||||||||||||

Rent and occupancy | 14,823 | 15,710 | 14,714 | 11,509 | 8,311 | ||||||||||||||

Depreciation and amortization | 19,763 | 24,359 | 19,874 | 18,414 | 14,417 | ||||||||||||||