| ProShares Ultra Investment Grade Corporate |

Ultra Investment Grade Corporate

Important Information About the Fund

ProShares Ultra Investment Grade Corporate (the "Fund") seeks investment results for a single day only, not for longer periods. A "single day" is measured from the time the Fund calculates its net asset value ("NAV") to the time of the Fund's next NAV calculation. The return of the Fund for periods longer than a single day will be the result of each day's returns compounded over the period, which will very likely differ from two times (2x) the return of the Markit iBoxx $ Liquid Investment Grade Index (the "Index") for that period. For periods longer than a single day, the Fund will lose money when the level of the Index is flat over time, and it is possible that the Fund will lose money over time even if the level of the Index rises. Longer holding periods, higher index volatility and greater leverage each exacerbate the impact of compounding on a fund's returns. During periods of higher index volatility, the volatility of the Index may affect the Fund's return as much as or more than the return of the Index.

The percentage change of the Fund's NAV each day may differ, perhaps significantly, from two times (2x) the percentage change of the Index on such day. This is due primarily to (a) the impact of a limited trading market in the component Index bonds on the calculation of the Index, and (b) the time difference in calculation of the Index (3:00 p.m.) and valuation of the Fund (4:00 p.m.).

The Fund is different from most exchange-traded funds in that it seeks leveraged returns relative to the Index and only on a daily basis. The Fund also is riskier than similarly benchmarked exchange-traded funds that do not use leverage. Accordingly, the Fund may not be suitable for all investors and should be used only by knowledgeable investors who understand the potential consequences of seeking daily leveraged investment results. Shareholders should actively monitor their investments. |

| Investment Objective |

| The Fund seeks daily investment results, before fees and expenses, that correspond to two times (2x) the daily performance of the Index. The Fund does not seek to achieve its stated investment objective over a period of time greater than a single day. |

| Fees and Expenses of the Fund |

| The table below describes the fees and expenses that you may pay if you buy or hold shares of the Fund. “Acquired Fund Fees and Expenses” are expenses incurred indirectly by the Fund through its ownership of shares in other investment companies, such as exchange-traded funds (“ETFs”). ETF expenses are similar to the expenses paid for any operating company held by the Fund. They are not direct costs paid by Fund shareholders and are not used to calculate the Fund’s NAV. They have no impact on the costs associated with Fund operations. |

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment) |

|

|

| Example: |

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other funds.

The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of each period. The example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same, except that the fee waiver/expense reimbursement is assumed only to pertain to the first year. Although your actual cost may be higher or lower, based on these assumptions your approximate costs would be: |

|

Expense Example

(USD $)

|

1 Year

|

3 Years

|

5 Years

|

10 Years

|

|

ProShares Ultra Investment Grade Corporate

|

105 |

772 |

1,464 |

3,310 |

|

| The Fund pays transaction and financing costs associated with transacting in securities and derivatives. In addition, investors may pay brokerage commissions on their purchases and sales of the Fund’s shares. These costs are not reflected in the example or the table above. |

| Portfolio Turnover |

| The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when the Fund’s shares are held in a taxable account. These costs, which are not reflected in Annual Fund Operating Expenses or in the example above, affect the Fund’s performance. During the most recent fiscal year end, the Fund’s annual portfolio turnover rate was 0% of the average value of its entire portfolio. This portfolio turnover rate is calculated without regard to cash instrument or derivatives transactions. If such transactions were included, the Fund’s portfolio turnover rate would be significantly higher. |

| Principal Investment Strategies |

The Fund invests in a combination of debt securities, exchange-traded funds and derivatives that ProShare Advisors believes, in combination, should have similar daily return characteristics as two times (2x) the daily return of the Index. The Index is a modified market-value weighted index designed to provide a balanced representation of U.S. dollar-denominated investment grade corporate bonds publicly offered in the United States by means of including the most liquid investment grade corporate bonds available as determined by the index provider. Currently, the bonds eligible for inclusion in the Index include U.S. dollar-denominated corporate bonds publicly offered in the United States that are issued by companies domiciled in the U.S., Bermuda, Canada, Cayman Islands, Western Europe or Japan; are rated investment grade by Moody's Investors Service, Inc., Fitch, Inc. or Standard and Poor's Financial Services, LLC; are from issuers with at least $3 billion par outstanding; have at least $750 million of outstanding face value; and have at least three years remaining to maturity. There is no limit to the number of issues in the Index. Index rebalances occur monthly. The Index is published under the Bloomberg ticker symbol "IBOXIG."

The types of securities and derivatives that the Fund will principally invest in are set forth below. The Fund may invest up to 85% of its assets in debt securities, ETFs, or a combination thereof. Cash balances arising from the use of derivatives will typically be held in money market instruments. - Debt Securities — Debt securities are fixed income securities, which may include foreign sovereign, sub-sovereign and supranational bonds, as well as any other obligations of any rating or maturity such as foreign and domestic investment grade corporate debt securities and lower-rated corporate debt securities.

- Exchange-Traded Funds (ETFs) — The Fund may invest in shares of other ETFs, which are registered investment companies that are traded on stock exchanges and hold assets such as stocks or bonds.

- Derivatives — The Fund invests in derivatives, which are financial instruments whose value is derived from the value of an underlying asset (including ETFs), interest rate or index. The Fund invests in derivatives as a substitute for investing directly in debt in order to gain leveraged exposure to the Index. These derivatives principally include:

- Swap Agreements — Contracts entered into primarily with major global financial institutions for a specified period ranging from a day to more than one year. In a standard "swap" transaction, two parties agree to exchange the return (or differentials in rates of return) earned or realized on particular predetermined investments or instruments. The gross return to be exchanged or "swapped" between the parties is calculated with respect to a "notional amount," e.g., the return on or change in value of a particular dollar amount invested in a "basket" of securities representing a particular index.

- Money Market Instruments — The Fund invests in short-term cash instruments that have a remaining maturity of 397 days or less and exhibit high quality credit profiles, including:

- U.S. Treasury Bills — U.S. government securities that have initial maturities of one year or less, and are supported by the full faith and credit of the United States.

- Repurchase Agreements — Contracts in which a seller of securities, usually U.S. government securities or other money market instruments, agrees to buy them back at a specified time and price. Repurchase agreements are primarily used by the Fund as a short-term investment vehicle for cash positions.

ProShare Advisors uses a mathematical approach to investing. Using this approach, ProShare Advisors determines the type, quantity and mix of investment positions that the Fund should hold to approximate on a daily basis the performance of two times (2x) the Index. The Fund may gain exposure to only a representative sample of the securities in the Index, which exposure is intended to have aggregate characteristics similar to those of the Index, and may invest in securities or financial instruments not contained in the Index. ProShare Advisors does not invest the assets of the Fund in securities or derivatives based on ProShare Advisors' view of the investment merit of a particular security, instrument, or company, other than for cash management purposes, nor does it conduct conventional research or analysis (other than in determining counterparty creditworthiness), or forecast market movement or trends, in managing the assets of the Fund. The Fund seeks to remain fully invested at all times in securities and/or derivatives that, in combination, provide leveraged exposure to the Index without regard to market conditions, trends or direction. The Fund seeks investment results for a single day only as calculated from NAV to NAV, not for longer periods.

At the close of the markets each trading day, the Fund will seek to position its portfolio so that its exposure to the Index is consistent with the Fund's investment objective. The Index's movements during the day will affect whether the Fund's portfolio needs to be repositioned. For example, if the Index has risen on a given day, net assets of the Fund should rise. As a result, the Fund's exposure will need to be increased. Conversely, if the Index has fallen on a given day, net assets of the Fund should fall. As a result, the Fund's exposure will need to be decreased.

Because of daily rebalancing and the compounding of each day's return over time, the return of the Fund for periods longer than a single day will be the result of each day's returns compounded over the period, which will very likely differ from two times (2x) the return of the Index over the same period. The Fund will lose money when the level of the Index is flat over time, and it is possible that the Fund will lose money over time even if the level of the Index rises, as a result of daily rebalancing, the Index's volatility and the effects of compounding. See "Principal Risks", below.

The Fund will concentrate its investments in a particular industry or group of industries to approximately the same extent as the Index is so concentrated. As of the close of business on June 30, 2012, the Index was concentrated in the financial services industry group, which comprised approximately 33% of the market capitalization of the Index.

Please see “Investment Objectives, Principal Investment Strategies and Related Risks” in the Fund’s full Prospectus for additional details. |

| Principal Risks |

You could lose money by investing in the Fund. - Risk Associated with the Use of Derivatives — The Fund uses investment techniques, such as investing in derivatives, that may be considered aggressive. Investing in derivatives may expose the Fund to greater risks than investing directly in the reference asset(s) underlying those derivatives, such as counterparty risk, liquidity risk and increased correlation risk (each as discussed below). When the Fund uses derivatives, there may be imperfect correlation between the value of the reference asset(s) and the derivative, which may prevent the Fund from achieving its investment objective. Moreover, with respect to the use of swap agreements, if the Index has a dramatic intraday move that causes a material decline in the Fund's net assets, the terms of a swap agreement between the Fund and its counterparty may permit the counterparty to immediately close out the transaction with the Fund. In that event, the Fund may be unable to enter into another swap agreement or invest in other derivatives to achieve the desired exposure consistent with the Fund's investment objective. This, in turn, may prevent the Fund from achieving its investment objective, even if the Index reverses all or a portion of its intraday move by the end of the day. Any financing, borrowing and other costs associated with using derivatives may also have the effect of lowering the Fund's return.

- Leverage Risk — The Fund obtains investment exposure in excess of its assets in seeking to achieve its investment objective—a form of leverage—and will lose more money in market environments adverse to its daily objective than a similar fund that does not employ such leverage. The use of such leverage could result in the total loss of an investor's investment. For example, because the Fund includes a multiplier of two times (2x) the Index, a single day movement in the Index approaching 50% at any point in the day could result in the total loss of a shareholder's investment if that movement is contrary to the investment objective of the Fund, even if the Index subsequently moves in an opposite direction, eliminating all or a portion of the earlier movement. This would be the case with any such single day movements in the Index, even if the Index maintains a level greater than zero at all times.

- Compounding Risk — As a result of compounding and because the Fund has a single day investment objective, the Fund's performance for periods greater than a single day is likely to be either greater than or less than the Index performance times the stated multiple in the Fund objective, before accounting for fees and fund expenses. Compounding affects all investments, but has a more significant impact on a leveraged fund. Particularly during periods of higher Index volatility, compounding will cause results for periods longer than a single day to vary from two times (2x) the return of the Index. This effect becomes more pronounced as volatility increases. Fund performance for periods greater than a single day can be estimated given any set of assumptions for the following factors: a) Index performance; b) Index volatility; c) period of time; d) financing rates associated with leveraged exposure; e) other Fund expenses; and f) dividends or interest paid with respect to securities in the Index. The chart below illustrates the impact of two principal factors—Index volatility and Index performance—on Fund performance. The chart shows estimated Fund returns for a number of combinations of Index volatility and Index performance over a one-year period. Performance shown in the chart assumes: (a) no Fund expenses; and (b) borrowing/lending rates (to obtain leveraged exposure) of zero percent. If Fund expenses and/or actual borrowing/lending rates were reflected, the Fund's performance would be lower than shown.

Areas shaded darker represent those scenarios where the Fund can be expected to return less than two times (2x) the performance of the Index. For periods longer than a single day, the Fund will lose money when the level of the Index is flat and can even lose money when the level of the Index rises. Estimated Fund Returns | | | | | | | | | | | | | | | | | | | | | | | | | Index

Performance | | | One Year Volatility Rate | | One

Year

Index | | Two

times

(2x) the

One

Year

Index | | | 10% | | | 25% | | | 50% | | | 75% | | | 100% | | | | | | | | | | -60% | | | -120% | | | | -84.2% | | | | -85.0% | | | | -87.5% | | | | -90.9% | | | | -94.1% | | | | | | | | | | -50% | | | -100% | | | | -75.2% | | | | -76.5% | | | | -80.5% | | | | -85.8% | | | | -90.8% | | | | | | | | | | -40% | | | -80% | | | | -64.4% | | | | -66.2% | | | | -72.0% | | | | -79.5% | | | | -86.8% | | | | | | | | | | -30% | | | -60% | | | | -51.5% | | | | -54.0% | | | | -61.8% | | | | -72.1% | | | | -82.0% | | | | | | | | | | -20% | | | -40% | | | | -36.6% | | | | -39.9% | | | | -50.2% | | | | -63.5% | | | | -76.5% | | | | | | | | | | -10% | | | -20% | | | | -19.8% | | | | -23.9% | | | | -36.9% | | | | -53.8% | | | | -70.2% | | | | | | | | | | 0% | | | 0% | | | | -1.0% | | | | -6.1% | | | | -22.1% | | | | -43.0% | | | | -63.2% | | | | | | | | | | 10% | | | 20% | | | | 19.8% | | | | 13.7% | | | | -5.8% | | | | -31.1% | | | | -55.5% | | | | | | | | | | 20% | | | 40% | | | | 42.6% | | | | 35.3% | | | | 12.1% | | | | -18.0% | | | | -47.0% | | | | | | | | | | 30% | | | 60% | | | | 67.3% | | | | 58.8% | | | | 31.6% | | | | -3.7% | | | | -37.8% | | | | | | | | | | 40% | | | 80% | | | | 94.0% | | | | 84.1% | | | | 52.6% | | | | 11.7% | | | | -27.9% | | | | | | | | | | 50% | | | 100% | | | | 122.8% | | | | 111.4% | | | | 75.2% | | | | 28.2% | | | | -17.2% | | | | | | | | | | 60% | | | 120% | | | | 153.5% | | | | 140.5% | | | | 99.4% | | | | 45.9% | | | | -5.8% | | The foregoing table is intended to isolate the effect of Index volatility and Index performance on the return of the Fund. For example, the Fund may incorrectly be expected to achieve a -40% return on a yearly basis if the Index return were -20%, absent the effects of compounding. However, as the table shows, with Index volatility of 50%, the Fund could be expected to return -50.2% under such a scenario. The Fund's actual returns may be significantly greater or less than the returns shown above as a result of any of the factors discussed above or in "Principal Risks—Correlation Risk" below. The Index's annualized historical volatility rate for the five-year period ended June 30, 2012 was 6.42%. The Index's highest June to June volatility rate during the five-year period was 11.49% (June 30, 2009). The Index's annualized performance for the five-year period ended June 30, 2012 was 8.32%. Historical Index volatility and performance are not indications of what the Index volatility and performance will be in the future. For additional graphs and charts demonstrating the effects of Index volatility and Index performance on the long-term performance of the Fund, see "Principal Risks of Geared Funds and the Impact of Compounding" in the Fund's full Prospectus and "Special Note Regarding the Correlation Risks of Geared Funds" in the Fund's Statement of Additional Information. - Correlation Risk — A number of factors may affect the Fund's ability to achieve a high degree of correlation with the Index, and there can be no guarantee that the Fund will achieve a high degree of correlation. Failure to achieve a high degree of correlation may prevent the Fund from achieving its investment objective.

The percentage change of the Fund's NAV each day may differ, perhaps significantly, from two times (2x) the percentage change of the Index on such day. This is due primarily to (a) the impact of a limited trading market in the component Index bonds on the calculation of the Index, and (b) the time difference in calculation of the Index (3:00 pm) and the valuation of the Fund (4:00 pm). In order to achieve a high degree of correlation with the Index, the Fund seeks to rebalance its portfolio daily to keep exposure consistent with its investment objective. Being materially over-or under-exposed to the Index may prevent the Fund from achieving a high degree of correlation with the Index. Market disruptions or closure, regulatory restrictions or extreme market volatility will adversely affect the Fund's ability to adjust exposure to requisite levels. The target amount of portfolio exposure is impacted dynamically by the Index's movements. Because of this, it is unlikely that the Fund will have perfect exposure (i.e., 2x) to the Index at the end of each day and the likelihood of being materially over- or under-exposed is higher on days when the Index level is volatile near the close of the trading day. A number of other factors may also adversely affect the Fund's correlation with the Index, including fees, expenses, transaction costs, financing costs associated with the use of derivatives, income items, valuation methodology, accounting standards and disruptions or illiquidity in the markets for the securities or financial instruments in which the Fund invests. The Fund may not have investment exposure to all bonds in the Index, or its weighting of investment exposure to such bonds may be different from that of the Index. In addition, the Fund may invest in securities or financial instruments not included in the Index. The Fund may also be subject to large movements of assets into and out of the Fund, potentially resulting in the Fund being over- or under-exposed to the Index. Activities surrounding Index reconstitutions or other Index rebalancing events may hinder the Fund's ability to meet its daily investment objective on or around that day. - Counterparty Risk — The Fund will be subject to credit risk (i.e., the risk that a counterparty is unwilling or unable to make timely payments to meet its contractual obligations) with respect to the amount it expects to receive from counterparties to derivatives and repurchase agreements entered into by the Fund. If a counterparty becomes bankrupt or fails to perform its obligations, the value of your investment in the Fund may decline.

- Debt Instrument Risk — The Fund may invest in, or seek exposure to, debt instruments. Debt instruments may have varying levels of sensitivity to changes in interest rates, credit risk and other factors. Many types of debt instruments are subject to prepayment risk, which is the risk that the issuer of the security will repay principal prior to the maturity date. Debt instruments allowing prepayment may offer less potential for gains during a period of declining interest rates, as the Fund may be required to reinvest at lower interest rates. In addition, changes in the credit quality of the issuer of a debt instrument can also affect the price of a debt instrument, as can an issuer's default on its payment obligations. Such factors may cause the value of an investment in the Fund to change. Also, the securities of certain U.S. government agencies, authorities or instrumentalities are neither issued by nor guaranteed as to principal and interest by the U.S. government, and may be exposed to more credit risk than securities issued by and guaranteed as to principal and interest by the U.S. government. All U.S. government securities are subject to credit risk. Because of the rising U.S. government debt burden, it is possible that the U.S. government may not be able to meet its financial obligations or that securities issued by the U.S. government may experience credit downgrades. Such a credit event may also adversely impact the financial markets.

- Early Close/Late Close/Trading Halt Risk — An exchange or market may close early, close late or issue trading halts on specific securities, or the ability to buy or sell certain securities or derivatives may be restricted, which may result in the Fund being unable to buy or sell certain securities or derivatives. In such circumstances, the Fund may be unable to rebalance its portfolio, may be unable to accurately price its investments and/or may incur substantial trading losses.

- Exposure to Foreign Investments Risk — Exposure to securities of foreign issuers may provide the Fund with increased risk. Various factors related to foreign investments may negatively impact the Index's performance, such as: i) fluctuations in the value of the applicable foreign currency; ii) differences in securities settlement practices; iii) uncertainty associated with evidence of ownership of investments in countries that lack centralized custodial services; iv) possible regulation of, or other limitations on, investments by U.S. investors in foreign investments; v) potentially higher brokerage commissions; vi) the possibility that a foreign government may withhold portions of interest and dividends at the source; vii) taxation of income earned in foreign countries or other foreign taxes imposed; viii) foreign exchange controls, which may include suspension of the ability to transfer currency from a foreign country; ix) less publicly available information about foreign issuers; x) changes in the denomination currency of a foreign investment; and xi) less certain legal systems in which the Fund might encounter difficulties or be unable to pursue legal remedies. Foreign investments also may be more susceptible to political, social, economic and regional factors than might be the case with U.S. securities.

- Financial Services Industry Risk — The Fund is subject to risks faced by companies in the financial services economic sector to the same extent as the Index is so concentrated, including: extensive governmental regulation and/or nationalization that affects the scope of their activities, the prices they can charge and the amount of capital they must maintain; adverse effects from increases in interest rates; effects on profitability by loan losses, which usually increase in economic downturns; the severe competition to which banks, insurance, and financial services companies may be subject; and increased inter-industry consolidation and competition in the financial sector. Further, such stocks in the Index may underperform fixed income investments and stock market indexes that track other markets, segments and sectors.

- Geographic Concentration Risk — Because the Fund focuses its investments in particular foreign countries or geographic regions, it may be more volatile than a more geographically diversified fund. The performance of the Fund will be affected by the political, social and economic conditions in those foreign countries and geographic regions and subject to the related risks.

- Interest Rate Risk — Interest rate risk is the risk that debt securities or certain financial instruments may fluctuate in value due to changes in interest rates. Commonly, investments subject to interest rate risk will decrease in value when interest rates rise and increase in value when interest rates decline. The value of securities with longer maturities may fluctuate more in response to interest rate changes than securities with shorter maturities.

- Intraday Price Performance Risk — The Fund is rebalanced at or about the time of its NAV calculation. As such, the intraday position of the Fund will generally be different from the Fund's stated investment objective corresponding to two times (2x) the Index. When shares are bought intraday, the performance of the Fund's shares relative to the Index until the Fund's next NAV calculation time will generally be greater than or less than the Fund's stated multiple.

- Risks of Investing in Exchange-Traded Funds (ETFs) — Investing in other investment companies, such as ETFs, subjects the Fund to those risks affecting the underlying ETFs, such as risks that the investment management strategy of the ETF may not produce its intended results (management risk) and the risk that the ETF could lose money over short periods due to short-term market movements and over longer periods during market downturns (market risk). In addition, investing in ETFs involve the risk that an ETF's performance may not track the performance of the index or markets that the ETF is designed to track, which may result in losses to such ETF and, ultimately, the Fund. Moreover, the Fund will incur its pro rata share of the expenses of the underlying ETF's expenses.

- Liquidity Risk — In certain circumstances, such as the disruption of the orderly markets for the securities or derivatives in which the Fund invests, the Fund might not be able to acquire or dispose of certain holdings quickly or at prices that represent true market value in the judgment of ProShare Advisors. Markets for the securities or derivatives in which the Fund invests may be disrupted by a number of events, including but not limited to economic crises, natural disasters, new legislation, or regulatory changes inside or outside of the U.S. For example, regulation limiting the ability of certain financial institutions to invest in certain securities would likely reduce the liquidity of those securities. Such situations may prevent the Fund from limiting losses, realizing gains or achieving a high correlation with the Index.

- Market Risk — The Fund is subject to market risks that will affect the value of its shares, including adverse issuer, political, regulatory, market or economic developments, as well as developments that impact specific economic sectors, industries or segments of the market.

- Market Price Variance Risk — The Fund's shares are listed for trading on the NYSE Arca and can be bought and sold in the secondary market at market prices. The market prices of shares will fluctuate in response to changes in NAV and supply and demand for shares. ProShare Advisors cannot predict whether shares will trade above, below or at their NAV. Given the fact that shares can be created and redeemed in Creation Units, as defined below, ProShare Advisors believes that large discounts or premiums to the NAV of shares should not be sustained. The Fund's investment results are measured based upon the daily NAV of the Fund. Investors purchasing and selling shares in the secondary market may not experience investment results consistent with those experienced by investors creating and redeeming directly with the Fund.

- Non-Diversification Risk — The Fund is classified as "non-diversified" under the Investment Company Act of 1940, and has the ability to invest a relatively high percentage of its assets in the securities of a small number of issuers susceptible to a single economic, political or regulatory event, or in derivative instruments with a single counterparty if ProShare Advisors determines that doing so is the most efficient means of meeting the Fund's investment objective. This makes the performance of the Fund more susceptible to adverse impact to an issuer or counterparty than a diversified fund might be. This risk may be particularly acute when the Index is comprised of a small number of securities.

- Portfolio Turnover Risk — Daily rebalancing of Fund holdings, which is required to keep leverage consistent with a single day investment objective, will cause a higher level of portfolio transactions than compared to most exchange-traded funds. Additionally, active market trading of the Fund's shares may cause more frequent creation or redemption activities that could, in certain circumstances, increase the number of portfolio transactions. High levels of transactions increase brokerage costs and may result in increased taxable capital gains.

- Valuation Risk — In certain circumstances, portfolio securities may be valued using techniques other than market quotations. The value established for a portfolio security may be different from what would be produced through the use of another methodology or if it had been priced using market quotations. Portfolio securities that are valued using techniques other than market quotations, including "fair valued" securities, may be subject to greater fluctuation in their value from one day to the next than would be the case if market quotations were used. In addition, there is no assurance that a Fund could sell a portfolio security for the value established for it at any time, and it is possible that a Fund would incur a loss because a portfolio security is sold at a discount to its established value.

- Valuation Time Risk — The Fund typically values its portfolio at 4:00 p.m. (Eastern Time). The closing levels of the securities that comprise the Index are, in certain cases, calculated earlier or later than the time the Fund typically values its portfolio.

Moreover, the Fund's shares trade on the NYSE Arca from 9:30 a.m. to 4:00 p.m. (Eastern time). The derivatives (and/or reference assets on which the derivatives are based) held by the Fund, however, may have different fixing or settlement times. Consequently, liquidity in the derivatives (and/or their reference assets) may be reduced after such fixing or settlement times. Accordingly, during the time when the NYSE Arca is open but after the applicable fixing or settlement times, trading spreads and the resulting premium or discount on the Fund's shares may widen, and, therefore, increase the difference between the market price of the Fund's shares and the NAV of such shares. Please see "Investment Objectives, Principal Investment Strategies and Related Risks" in the Fund's full Prospectus for additional details. |

| Investment Results |

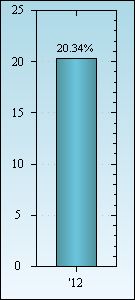

| The bar chart below shows the Fund’s investment results during its first full calendar year of operations, and the table shows how the Fund’s average annual total returns for various periods compare with a broad measure of market performance. This information provides some indication of the risks of investing in the Fund. Past results (before and after taxes) are not predictive of future results. Updated information on the Fund’s results can be obtained by visiting ProShares.com. |

| Annual Returns as of December 31 |

|

Best Quarter (ended 9/30/2012): 8.76%

Worst Quarter (ended 12/31/2012): 0.81%

The year-to-date return as of the most recent quarter,

which ended December 31, 2012, was 20.34%. |

Average Annual Total Returns

As of December 31, 2012 |

|

Average Annual Total Returns

|

One Year

|

Since Inception

|

Inception Date

|

|

ProShares Ultra Investment Grade Corporate

|

|

20.34% |

21.19% |

Apr. 13,

2011 |

|

ProShares Ultra Investment Grade Corporate After Taxes on Distributions

|

|

20.34% |

21.19% |

|

|

ProShares Ultra Investment Grade Corporate After Taxes on Distributions and Sale of Shares

|

|

13.22% |

18.19% |

|

|

ProShares Ultra Investment Grade Corporate Markit iBoxx $ Liquid Investment Grade Index

|

[1] |

11.85% |

11.57% |

|

|

Average annual total returns are shown on a before- and after-tax basis for the Fund. After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold shares through tax-deferred arrangements, such as a retirement account. After-tax returns may exceed the return before taxes due to a tax benefit from realizing a capital loss on a sale of shares.

Annual returns are required to be shown and should not be interpreted as suggesting that the Fund should or should not be held for longer periods of time. The Fund may not be suitable for all investors and should only be used by knowledgeable investors who understand the potential consequences of seeking daily leveraged results (i.e., 2x). Shareholders should actively monitor their investments. |