UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

(Mark One)

|

|

|

R

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the Fiscal Year Ended January 29, 2011

|

|

|

or

|

|

|

£

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission File Number: 001-31314

_______________

AÉROPOSTALE, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

No. 31-1443880

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

incorporation or organization)

|

Identification No.)

|

|

112 West 34th Street, 22nd floor

|

|

|

New York, NY

|

10120

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code:

(646) 485-5410

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

Common Stock, $0.01 par value

|

New York Stock Exchange

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes R No £

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes £ No R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to the filing requirements for at least the past 90 days. Yes R No £

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. R

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filed”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer R

|

Accelerated filer £

|

|

Non-accelerated filer £

|

Smaller reporting company £

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No R

The aggregate market value of voting stock held by non-affiliates of the registrant as of July 31, 2010 was $2,656,929,516.

81,776,929 shares of Common Stock were outstanding at March 18, 2011.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement, to be filed with the Securities and Exchange Commission within 120 days after the end of the registrant’s fiscal year covered by this Annual Report on Form 10-K, with respect to the Annual Meeting of Stockholders to be held on June 16, 2011, are incorporated by reference into Part III of this Annual Report on Form 10-K. This report consists of 56 sequentially numbered pages. The Exhibit Index is located at sequentially numbered page 54.

AÉROPOSTALE, INC.

| 3 | ||

| 10 | ||

| 14 | ||

| 15 | ||

| 15 | ||

| 15 | ||

| 16 | ||

| 18 | ||

| 19 | ||

| 26 | ||

| 27 | ||

| 51 | ||

| 51 | ||

| 51 | ||

| 52 | ||

| 52 | ||

| 52 | ||

| 52 | ||

| 52 | ||

| 53 | ||

| 54 | ||

| 55 | ||

As used in this Annual Report on Form 10-K, unless the context otherwise requires, all references to “we”, “us”, “our”, “Aéropostale” or the “Company’ refer to Aéropostale, Inc., and its subsidiaries. The term “common stock” means our common stock, $0.01 par value. Our website is located at www.aeropostale.com (this and any other references in this Annual Report on Form 10-K to Aéropostale.com is solely a reference to a uniform resource locator, or URL, and is an inactive textual reference only, not intended to incorporate the website into this Annual Report on Form 10-K). On our website, we make available, as soon as reasonably practicable after electronic filing with the Securities and Exchange Commission, our annual reports on Form 10-K, quarterly reports on Form 10-Q, annual Proxy filings and current reports on Form 8-K, and any amendments to those reports. All of these reports are provided to the public free of charge.

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements involve certain risks and uncertainties, including statements regarding our strategic direction, prospects and future results. Certain factors, including factors outside of our control, may cause actual results to differ materially from those contained in the forward-looking statements. The risk factors included in Part I, Item 1A should be read in connection with evaluating our business and future prospects. All forward looking statements included in this report are based on information available to us as of the date hereof, and we assume no obligation to update or revise such forward-looking statements to reflect events or circumstances that occur after such statements are made.

Overview

Aéropostale, Inc., a Delaware corporation, was originally incorporated as MSS-Delaware, Inc. on September 1, 1995 and on February 1, 2000 changed its name to Aéropostale, Inc.. Aéropostale, Inc. is a primarily mall-based, specialty retailer of casual apparel and accessories, principally targeting 14 to 17 year-old young women and men through its Aéropostale stores and 7 to 12 year-old kids through its P.S. from Aéropostale stores. The Company provides customers with a focused selection of high quality fashion and fashion basics at compelling values in an innovative and exciting store environment. Aéropostale maintains control over its proprietary brands by designing, sourcing, marketing and selling all of its own merchandise. Aéropostale products can only be purchased in Aéropostale stores and online at www.aeropostale.com. P.S. from Aéropostale products can be purchased in P.S. from Aéropostale stores, in certain Aéropostale stores including our new Times Square store in New York City and online at www.ps4u.com. As of January 29, 2011, we operated 965 Aéropostale stores, consisting of 906 stores in 49 states and Puerto Rico, 59 stores in Canada, as well as 47 P.S. from Aéropostale stores in 13 states. In addition, pursuant to a Licensing Agreement, one of our international licensees operated 10 Aéropostale stores in the United Arab Emirates as of January 29, 2011. During March 2011, we announced that we had signed a second licensing agreement. The licensee to this agreement is expected to open approximately 25 stores in Singapore, Malaysia and Indonesia over the next five years.

The Aéropostale brand was established by R.H. Macy & Co., Inc., as a department store private label initiative, in the early 1980’s targeting men in their twenties. Macy’s subsequently opened the first mall-based Aéropostale specialty store in 1987. Over the next decade, Macy’s, and then Federated Department Stores, Inc. (now Macy’s, Inc.), expanded Aéropostale to over 100 stores. In August 1998, Federated sold its specialty store division to Aéropostale management and Bear Stearns Merchant Banking. In May of 2002, Aéropostale management took the Company public through an initial public offering and listed our common stock on the New York Stock Exchange.

Our Aéropostale concept provides the customer with a focused selection of high-quality, active-oriented, fashion and fashion basic merchandise at compelling values. We strive to create a fun, high-energy shopping experience through the use of creative visual merchandising, colorful in-store signage, popular music and an enthusiastic well-trained sales force. Our average Aéropostale store is generally smaller than that of our mall-based competitors. We believe this enables us to achieve higher sales productivity and project a sense of greater action and excitement in the store.

P.S. from Aéropostale offers casual clothing and accessories focusing on elementary school kids between the ages of 7 and 12. The P.S. brand draws from the core competencies of Aéropostale, offering the customer trend-right merchandise at compelling values. The innovative store format strives to be a fun, playful and inviting shopping experience for both the parent and child. We maintain control of our proprietary brands by designing and sourcing all of our merchandise. Our P.S. from Aéropostale products are sold only at our stores and online through our e-commerce websites, www.ps4u.com and www.aeropostale.com.

Our fiscal year ends on the Saturday nearest to January 31. Fiscal 2010 was the 52-week period ended January 29, 2011; fiscal 2009 was the 52-week period ended January 30, 2010, and fiscal 2008 was the 52-week period ended January 31, 2009. Fiscal 2011 will be the 52-week period ending January 28, 2012.

Executive Transition

In December 2010, we announced that Thomas P. Johnson, then our Co-Chief Executive Officer, had been appointed our Chief Executive Officer, effective December 1, 2010. Mr. Johnson also continues to serve as a member of our Board of Directors. At that same time, we also announced that Mindy C. Meads had departed from the Company, ending her tenure as both Co-Chief Executive Officer and as a director.

Effective February 2010, Julian Geiger, our Chairman and then Chief Executive Officer elected to end his service as our Chief Executive Officer. Mr. Geiger continues to serve as Chairman of our Board of Directors and as a part-time advisor to the Company. Also effective in February 2010, Ms. Meads and Mr. Johnson were each promoted to the position of Co-Chief Executive Officer and appointed to our Board of Directors, and Michael J. Cunningham was promoted to the position of President and Chief Financial Officer.

Growth Strategy

Store Productivity. We seek to generate sales growth by increasing sales per square foot, increasing average unit retail and increasing transactions. In an effort to accomplish that growth, we invest in strategic initiatives such as enhancing our supply chain and store productivity technologies. We currently have over 170 stores in our chain operating at over $800 sales per square foot, compared to the total chain average of $626 per square foot. We recognize the opportunity to increase the square footage in a number of these highly productive locations, where appropriate, with the expectation that we will be able to generate additional sales growth.

New Aéropostale stores. We consider the merchandise in our stores as having broad appeal that continues to provide us with new store expansion opportunities. Over the last three fiscal years we opened 163 new Aéropostale stores. We plan to continue our growth by opening a total of approximately 28 new Aéropostale stores during fiscal 2011. We plan to open stores both in markets where we currently operate, as well as in new markets (see the section “Stores — Store design and environment” below).

New P.S. from Aéropostale stores. During fiscal 2009, we launched “P.S. from Aéropostale” by opening our first 14 stores in five states. As of January 29, 2011, we operated 47 P.S. from Aéropostale stores in 13 states. We plan to open approximately 20 additional P.S. from Aéropostale stores during fiscal 2011. As part of our growth strategy for P.S. from Aéropostale, we plan to expand our size offerings to increase our targeted customer base, increase the mix of fashion offerings and maximize e-commerce opportunities.

E-commerce. We launched our Aéropostale e-commerce business in May 2005. The Aéropostale on-line store is accessible at our website, www.aeropostale.com. P.S. from Aéropostale merchandise can be purchased online at www.aeropostale.com or www.ps4u.com. A third party provides fulfillment services for our e-commerce business, including warehousing our inventory and fulfilling our customers’ sales orders. We purchase, manage and own the inventory sold through our website and we recognize revenue from the sale of these products when the customer receives the merchandise.

International. During fiscal 2008, we signed our first international licensing agreement. As licensor we receive guaranteed minimum annual royalty payments from the licensee throughout the term of the agreement, as well as certain support and administrative fees. The licensee has opened 10 Aéropostale brand retail stores in the United Arab Emirates since fiscal 2009, and expects to open approximately three additional stores during fiscal 2011. During March 2011, we announced that we had signed a second licensing agreement. The licensee under this agreement is expected to open approximately 25 stores in Singapore, Malaysia and Indonesia over the next five years. We assume no inventory risk on the merchandise sold in our licensee’s stores and we do not own or lease the underlying real estate where the stores operate. In addition, our international licensing agreements contain other customary terms and conditions governing our business relationship with the licensees. We will continue to evaluate additional international opportunities.

Stores

Existing stores. We locate our stores primarily in shopping malls, outlet centers and, to a much lesser degree, lifestyle and off-mall shopping centers, all located in geographic areas with the highest possible concentrations of our target customers. We generally locate our stores in mall locations near popular teen gathering spots, such as food courts and other teen-oriented retailers. We have opened three street level stores in the New York City area. In November 2010, we opened a 19,000 square foot Aéropostale flagship store in the Times Square section of New York City. We highlight and offer both Aéropostale and P.S. from Aéropostale products in the Times Square store. We expect this flagship store to play an important role in creating an international awareness of the Aéropostale brand and image.

During fiscal 2009, we completed the closure of our 14 store Jimmy’Z concept that was launched in 2005. Jimmy’Z Surf Co., Inc., a wholly owned subsidiary of Aéropostale, Inc., was a contemporary lifestyle brand targeting trend-aware young women and men aged 18 to 25.

As of January 29, 2011, we operated 965 Aéropostale stores consisting of 906 stores in 49 states and Puerto Rico, 59 stores in Canada, as well as 47 P.S. from Aéropostale stores in 13 states. In addition, pursuant to a Licensing Agreement, our international licensee operated 10 Aéropostale stores in the United Arab Emirates as of January 29, 2011, which are excluded from the table below.

|

United States

|

Number of

Aéropostale

Stores

|

Number of

P.S from Aéropostale

Stores

|

Total

Number

Stores

|

|||||||||

|

Alabama

|

17 | 1 | 18 | |||||||||

|

Arizona

|

17 | — | 17 | |||||||||

|

Arkansas

|

8 | — | 8 | |||||||||

|

California

|

78 | 1 | 79 | |||||||||

|

Colorado

|

15 | — | 15 | |||||||||

|

Connecticut

|

11 | 2 | 13 | |||||||||

|

Delaware

|

4 | 2 | 6 | |||||||||

|

Florida

|

59 | — | 59 | |||||||||

|

Georgia

|

27 | 3 | 30 | |||||||||

|

Hawaii

|

3 | — | 3 | |||||||||

|

Idaho

|

5 | — | 5 | |||||||||

|

Illinois

|

34 | — | 34 | |||||||||

|

Indiana

|

23 | — | 23 | |||||||||

|

Iowa

|

12 | — | 12 | |||||||||

|

Kansas

|

8 | — | 8 | |||||||||

|

Kentucky

|

10 | — | 10 | |||||||||

|

Louisiana

|

15 | 1 | 16 | |||||||||

|

Maine

|

4 | — | 4 | |||||||||

|

Maryland

|

18 | — | 18 | |||||||||

|

Massachusetts

|

26 | 2 | 28 | |||||||||

|

Michigan

|

33 | — | 33 | |||||||||

|

Minnesota

|

16 | 1 | 17 | |||||||||

|

Mississippi

|

8 | — | 8 | |||||||||

|

Missouri

|

16 | — | 16 | |||||||||

|

Montana

|

3 | — | 3 | |||||||||

|

North Carolina

|

26 | 1 | 27 | |||||||||

|

North Dakota

|

4 | — | 4 | |||||||||

|

Nebraska

|

5 | — | 5 | |||||||||

|

New Hampshire

|

7 | — | 7 | |||||||||

|

New Jersey

|

25 | 13 | 38 | |||||||||

|

New Mexico

|

3 | — | 3 | |||||||||

|

Nevada

|

7 | — | 7 | |||||||||

|

New York

|

50 | 11 | 61 | |||||||||

|

Ohio

|

38 | — | 38 | |||||||||

|

Oklahoma

|

7 | — | 7 | |||||||||

|

Oregon

|

8 | — | 8 | |||||||||

|

Pennsylvania

|

53 | 3 | 56 | |||||||||

|

Puerto Rico

|

4 | — | 4 | |||||||||

|

Rhode Island

|

2 | — | 2 | |||||||||

|

South Carolina

|

15 | — | 15 | |||||||||

|

South Dakota

|

2 | — | 2 | |||||||||

|

Tennessee

|

20 | — | 20 | |||||||||

|

Texas

|

72 | 6 | 78 | |||||||||

|

Utah

|

12 | — | 12 | |||||||||

|

Vermont

|

2 | — | 2 | |||||||||

|

Virginia

|

27 | — | 27 | |||||||||

|

Washington

|

21 | — | 21 | |||||||||

|

West Virginia

|

7 | — | 7 | |||||||||

|

Wisconsin

|

18 | — | 18 | |||||||||

|

Wyoming

|

1 | — | 1 | |||||||||

|

Canada

|

||||||||||||

|

Alberta

|

9 | — | 9 | |||||||||

|

British Columbia

|

8 | — | 8 | |||||||||

|

New Brunswick

|

3 | — | 3 | |||||||||

|

Newfoundland

|

1 | — | 1 | |||||||||

|

Nova Scotia

|

1 | — | 1 | |||||||||

|

Ontario

|

37 | — | 37 | |||||||||

|

Total

|

965 | 47 | 1,012 | |||||||||

The following table highlights the number of Aéropostale, Jimmy’Z and P.S. from Aéropostale stores opened and closed since the beginning of fiscal 2008:

|

|

Aéropostale

Stores

Opened

|

P.S. from

Aéropostale

Stores

Opened

|

Aéropostale

Stores

Closed

|

Jimmy’Z

Stores Closed

|

Total

Number of

Stores at End

of Period

|

|||||||||||||||

|

Fiscal 2008

|

89 | — | — | 3 | 914 | |||||||||||||||

|

Fiscal 2009

|

39 | 14 | 4 | 11 | 952 | |||||||||||||||

|

Fiscal 2010

|

35 | 33 | 8 | — | 1,012 | |||||||||||||||

Store design and environment. Our Aéropostale stores average approximately 3,700 square feet and our P.S. from Aéropostale stores average approximately 3,400 square feet. We design our stores in an effort to create an energetic shopping environment, featuring powerful in-store promotional signage, creative visuals and popular music. The enthusiasm of our associates is integral to our store environment. Our stores feature display windows that provide high visibility for mall traffic. Our strategy is to create fresh and exciting merchandise presentations by updating our floor sets numerous times throughout the year. Visual merchandising directives are initiated at the corporate level in order to maintain consistency throughout all of our stores.

Store management. Our Aéropostale stores along with our P.S. from Aéropostale stores are organized by region and further broken down into districts. A regional manager or a group district manager manages each of our 13 regions and each region encompasses approximately eight to 10 districts. Each district is managed by a district manager and encompasses approximately seven to 10 individual stores. Our corporate headquarters directs the merchandise assortments, merchandise pricing, store layout, inventory management and in-store visuals for all of our stores.

Expansion opportunities and store site selection. We focus on opening new stores in an effort to further penetrate the existing markets we are already in, as well as to enter new markets. We plan to continue increasing our store base during fiscal 2011 by opening approximately 28 new Aéropostale stores and 20 P.S. from Aéropostale stores (see the section “Growth Strategy” above).

In selecting a specific store site, we generally target high traffic locations in malls, outlet centers and, to a much lesser degree, lifestyle and off-mall shopping centers, with suitable demographics and favorable lease economics. Our primary site evaluation criteria include average sales per retail square foot, co-tenancies, traffic patterns and occupancy costs.

For new Aéropostale stores opened in fiscal 2010, excluding our street level stores, our average net investment was approximately $557,000 per store location, which included capital expenditures adjusted for landlord contributions and initial inventory at cost, net of payables. For new P.S. from Aéropostale stores opened in fiscal 2010, our average net investment was approximately $549,000 (see the section “Store design and environment” above for a further discussion).

Pricing

We believe that a key component of our success is our ability to understand what our customers desire and what they can afford. Our merchandise, which we believe is of comparable quality to that of our primary competitors, is generally priced lower than our competitors’ merchandise. We conduct promotions in our stores throughout the year generally lasting anywhere from two to four weeks in length.

Design and Merchandising

Our design and merchandising teams focus on designing merchandise that meets the demands of our customers’ lifestyles. We maintain separate design and merchandising groups for each of our brands and within those brands, for each of the young women’s and young men’s product lines.

Design. We offer a focused collection of apparel, including graphic t-shirts, tops, bottoms, sweaters, jeans, outerwear and accessories. Our “design-driven, merchant-modified” philosophy, in which our designers’ visions are refined by our merchants’ understanding of the current market for our products, helps to ensure that our merchandise styles reflect the latest trends while not becoming too fashion-forward for our customers’ tastes. Much of our merchandise features our brands’ logos. We believe that our Aéropostale logo apparel appeals to our customers and reinforces our brand image.

Merchandising and Planning. Our merchandising organization, together with our planning organization, determines the quantities of units needed for each product category. By monitoring sales of each style and color and employing our flexible sourcing capabilities, we are able to adjust our merchandise assortments to capitalize upon emerging trends. In fiscal 2008, we began a phased implementation of assortment planning and allocation systems. In fiscal 2009, we implemented the latest phase of our allocation system and in fiscal 2010 we supplemented that system with an order optimization component, which allowed us to further improve our inventory position at the store level. In fiscal 2011, we expect to begin the implementation of an integrated assortment planning tool.

Sourcing

We seek to employ a sourcing strategy that expedites our speed to market and allows us to respond quickly to our customers’ preferences. We believe that we have developed strong relationships with our vendors, some of who rely upon us for a significant portion of their overall business.

During fiscal 2010, we sourced approximately 85% of our merchandise from our top five merchandise vendors. Most of our vendors maintain sourcing offices in the United States, with the majority of their production factories located in Asia and Central America. In an effort to minimize currency risk, all payments to our vendors and sourcing agents are made in U.S. dollars. We engage a third party independent contractor to visit the production facilities that supply us with our products. This independent contractor performs audits at each factory and as a result, assesses the compliance of the facility with, among other things, local and United States labor laws and regulations as well as fair trade and business practices.

Marketing and Advertising

We utilize numerous initiatives to increase our brand recognition and promote our merchandise assortment. We view our stores as the primary means to communicate our message and provide our brand experience. Our marketing efforts are focused on in-store communications, promotions and internal as well as external advertising. We expand, test and modify our marketing efforts based on focus groups, surveys and consumer feedback.

We believe that the enthusiasm and commitment of our store-level employees are key elements in enhancing our brand with our target customers. We also view the use of our logo on our merchandise as a means for expanding our brand awareness and visibility. We market in-store with large images in the store-front windows and at the checkout area. In addition, we have information alongside product displays and other touch points such as shopping bags. We also conduct select external advertising during key selling periods. Our advertisements appear in publications and in malls and on the radio on a regional basis. Periodically, we also partner with select third parties such as magazines, television shows and musical bands, to create marketing programs which we believe will be appealing to our customers.

Our websites, www.aeropostale.com and www.ps4u.com support all of our internet marketing and promotional initiatives and also offer a large portion of our merchandise assortment for purchase. We maintain a database of our customers and send emails and distribute information on special offers and promotions on a frequent basis. In addition, we support our brand through social media outlets such as Facebook and Twitter.

Distribution

To support our stores in the United States and Puerto Rico, we maintain two distribution centers to process merchandise and warehouse inventory needed to replenish our stores. We lease a 315,000 square foot distribution center facility in South River, New Jersey. We also lease a second distribution facility in Ontario, California with 360,000 square feet of space. The staffing and management of these distribution facilities is outsourced to a third party provider that operates each distribution facility and processes our merchandise. This third party provider employs personnel, some of whom are represented by a labor union. There have been no work stoppages or disruptions since the inception of our relationship with this third party provider in 1991, and we believe that the third party provider has a good relationship with its employees. In addition, a third party provides fulfillment services for our e-commerce business, including warehousing our inventory and fulfilling our customers’ sales orders. In addition, we outsource the shipment of our merchandise through third party transportation providers. These third parties ship our merchandise from our distribution facilities to our stores.

During fiscal 2009, we entered into an agreement with a third party to perform distribution services for our stores in Canada. The distribution center is located in Etobicoke, Ontario, Canada, and is independently owned and operated. This third party distribution center receives, processes and warehouses our merchandise for all of our stores in Canada. Unlike in the United States however, we do not lease the facility and we are not the only company with product in this warehouse. Prior to opening this facility, all of our products destined for our stores in Canada were first shipped to the United States and processed through our South River, New Jersey distribution center.

We continue to invest in systems and automation to improve processing efficiencies, automate functions that were previously performed manually and to support our store growth. Our distribution facilities utilize automated sortation materials handling equipment to receive, process and ship goods to our stores. These facilities also serve our other warehousing needs, such as storage of new store merchandise, floor set merchandise and packaging supplies.

Information Systems

Our management information systems provide a full range of retail, financial and merchandising applications. We utilize industry specific software systems to provide various functions related to point-of-sale, inventory management, supply chain, planning and replenishment, and financial reporting. We continue to invest in technology to align our systems with our business model and to support our continuing growth. For example, since fiscal 2008 we have been implementing in phases, new planning and allocation systems, as discussed above. During fiscal 2010, we completed implementing a data warehouse system to enhance our business intelligence reporting capabilities. During fiscal 2011, we plan to complete the implementation of a workforce management system that we began in fiscal 2010, which we believe will improve our labor scheduling at the store level. We expect to continue to invest strategically in our infrastructure in the future.

Trademarks

We own, through certain of our wholly owned subsidiaries, federal trademark registrations in the U.S. Patent and Trademark Office for our principal marks AÉROPOSTALE®, AÉRO®, 87®, P.S. FROM AÉROPOSTALE™, P.S.09® and other related marks for clothing, a variety of accessories, including sunglasses, belts, socks and hats, and as a service mark for retail clothing stores, as well as state registrations for these marks. We also have certain registrations pending for trademarks and service marks for clothing, retail stores and online services. Additionally, we have applied for or have already obtained a registration for the AÉROPOSTALE®, P.S. FROM AÉROPOSTALE™, and related marks in over 85 foreign countries. We plan to continue this focus on expanding our international registrations of our marks in the future.

We continue to maintain certain registrations of our JIMMY’Z® brand and related marks in the United States for clothing and related goods and services.

We regard our trademarks and other proprietary intellectual property as valuable assets of the Company that we continually maintain and protect.

Competition

The apparel market is highly competitive. We compete with a wide variety of retailers including other specialty stores, department stores, mail order retailers and mass merchandisers. Specifically, our Aéropostale brand competes primarily with other teen apparel retailers including, but not limited to, Abercrombie & Fitch®, American Eagle Outfitters®, Hollister®, Old Navy®, and Pacific Sunwear®. Our P.S. from Aéropostale brand competes primarily with other retailers such as Justice® and The Children’s Place®, as well as department stores, mail order retailers and mass merchandisers. Retailers in our sector compete primarily on the basis of design, price, quality, service and product assortment.

Employees

As of January 29, 2011, we employed 4,160 full-time and 13,668 part-time employees. We employed 673 of our employees at our corporate offices and in the field, and 17,155 at our store locations. The number of part-time employees fluctuates depending on our seasonal needs. None of our employees are represented by a labor union and we consider our relationship with our employees to be good.

Seasonality

Our business is highly seasonal, and historically we have realized a significant portion of our sales, net income and cash flows in the second half of the year, attributable to the impact of the back-to-school selling season in the third quarter, and the holiday selling season in our fourth quarter. As a result, our working capital requirements fluctuate during the year, increasing in mid-summer in anticipation of the third and fourth quarters. Our business is also subject, at certain times, to calendar shifts which may occur during key selling times such as school holidays, Easter and regional fluctuations in the calendar during the back-to-school selling season.

Available Information

We maintain internet websites, www.aeropostale.com and www.ps4u.com, through which access is available free of charge to our annual reports on Form 10-K, quarterly reports on Form 10-Q, Proxy Statements and current reports on Form 8-K, and all amendments of these reports filed, or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, after they are filed with the Securities and Exchange Commission.

Our Corporate Governance Guidelines and the charters for our Audit Committee, Nominating and Corporate Governance Committee and Compensation Committee may also be found on our internet websites at www.aeropostale.com or www.ps4u.com. In addition, our websites contain the Charter for our Lead Independent Director and Code of Business Conduct and Ethics, which is our code of ethics and conduct for our directors, officers and employees. Any waivers to our Code of Business Conduct and Ethics will be promptly disclosed on our websites.

In fiscal 2010, our Chief Executive Officer certified, in accordance with section 303.12(a) of the NYSE Listed Company Manual, that he was not aware of any violation by us of the NYSE’s corporate governance listing standards as of the date of such certification.

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements involve certain risks and uncertainties, including statements regarding our strategic direction, prospects and future results. Certain factors, including factors outside of our control, may cause actual results to differ materially from those contained in the forward-looking statements. The following risk factors should be read in connection with evaluating our business and future prospects. All forward looking statements included in this report are based on information available to us as of the date hereof, and we assume no obligation to update or revise such forward-looking statements to reflect events or circumstances that occur after such statements are made. Such uncertainties include, among others, the following factors:

The effect of economic pressures and other business factors

The global economic crisis continues to cause a great deal of uncertainty. This market uncertainty continues to result in a lack of consumer confidence and spending. The success of our operations depends, to a significant extent, upon a number of factors relating to discretionary consumer spending, including economic conditions affecting disposable consumer income such as employment, housing, consumer debt, interest rates, increases in energy costs and consumer confidence. There can be no assurance that consumer spending will not be further negatively affected by general or local economic conditions, thereby adversely impacting our results of operations and continued growth.

Our ability to react to raw material cost increases, labor and energy prices

Global inflationary economic conditions, as well as increases in our product costs, such as raw materials, labor and fuel, will reduce our overall profitability. Specifically, fluctuations in the price of cotton that is used in the manufacture of merchandise we purchase from our suppliers have begun to negatively impact our cost of goods. In addition, any reduction in merchandise available to us or any significant increase in the costs to produce that merchandise would have a material adverse effect on our results of operations. We have strategies in place to mitigate the rising cost of raw materials and our overall profitability depends on the success of those strategies. Additionally, increases in other costs, including labor and energy, could adversely impact our results of operations as well.

Our sales and operations may be adversely affected by unfavorable local, regional or national economic conditions.

Our business is sensitive to consumer spending patterns and preferences. Various economic conditions affect the level of disposable income consumers have available to spend on the merchandise we offer including employment, interest rates, taxation, energy costs, the availability of consumer credit, consumer confidence in future economic conditions and general business conditions. Accordingly, consumer purchases of discretionary items and retail products, including our products, may decline during recessionary periods, and also may decline at other times when changes in consumer spending patterns affect us unfavorably. Therefore, our growth, sales and profitability may be adversely affected by economic conditions on a local, regional and/or national level. In addition, any significant decreases in shopping mall traffic could also have a material adverse effect on our results of operations.

If we are unable to identify and respond to consumers’ fashion preferences, domestically and/or internationally, in a timely manner, our profitability would decline.

We may not be able to keep pace with the rapidly changing fashion trends, both domestically and/or internationally, and consumer tastes inherent in the teen apparel industry. We produce casual, comfortable apparel, a majority of which displays the “Aéropostale”, “Aéro” or “P.S. from Aéropostale” logo. There can be no assurance that fashion trends will not move away from casual clothing or that we will not have to alter our design strategy to reflect changes in consumer preferences. Failure to anticipate, identify or react appropriately to changes in styles, trends, desired images or brand preferences could have a material adverse effect on our results of operations.

Our ability to attract customers to our stores depends heavily on the success of the shopping malls in which we are located.

In order to generate customer traffic, we must locate our stores in prominent locations within successful shopping malls. We cannot control the development of new shopping malls, the availability or cost of appropriate locations within existing or new shopping malls, or the success of individual shopping malls. A significant decrease in shopping mall traffic could have a material adverse effect on our results of operations. Additionally, the loss of an anchor or other significant tenant in a shopping mall in which we have a store, or the closure of a significant number of shopping malls in which we have stores, either by a single landlord with a large portfolio of malls, or by a number of smaller individual landlords, may have a material adverse effect on our results of operations.

Fluctuations in comparable store sales and quarterly results of operations may cause the price of our common stock to decline substantially.

Our comparable store sales and quarterly results of operations have fluctuated in the past and are likely to continue to fluctuate in the future. Our comparable store sales and quarterly results of operations are affected by a variety of factors, including:

|

|

•

|

actions of our competitors or mall anchor tenants;

|

|

|

•

|

changes in general economic conditions and consumer spending patterns;

|

|

|

•

|

fashion trends;

|

|

|

•

|

changes in our merchandise mix;

|

|

|

•

|

the effectiveness of our inventory management;

|

|

|

•

|

calendar shifts of holiday or seasonal periods;

|

|

|

•

|

the timing of promotional events; and

|

|

|

•

|

weather conditions.

|

If our comparable store sales fail to meet the expectations of investors, then the market price of our common stock could decline substantially. You should refer to the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for more information.

A significant decrease in sales during peak shopping seasons could have an adverse effect on our financial condition and results of operations.

Our net sales and net income are disproportionately higher from August through January each year due to increased sales from back-to-school and holiday shopping. Sales during this period cannot be used as an accurate indicator for our annual results. Our net sales and net income from February through July are typically lower due to, in part, the traditional retail slowdown immediately following the winter holiday season. Any significant decrease in sales during the back-to-school and winter holiday seasons would have a material adverse effect on our financial condition and results of operations. In addition, in order to prepare for the back-to-school and holiday shopping seasons, we must order and keep in stock significantly more merchandise than we would carry during other parts of the year. Any unanticipated decrease in demand for our products during these peak shopping seasons could require us to sell excess inventory at a substantial markdown, which could reduce our net sales and gross margins and negatively impact our profitability. Additionally, our business is also subject, at certain times, to calendar shifts which may occur during key selling times such as school holidays, Easter and regional fluctuations in the calendar during the back-to-school selling season.

Our continued expansion plan is dependent on a number of factors which, if not implemented, could delay or prevent the successful opening of new stores and our entry into new markets.

Unless we continue to do the following, we may be unable to open new stores successfully and, in turn, our continued growth would be impaired:

|

|

•

|

identify suitable markets and sites for new store locations;

|

|

|

•

|

negotiate acceptable lease terms;

|

|

|

•

|

hire, train and retain competent store personnel;

|

|

|

•

|

foster current relationships and develop new relationships with vendors that are capable of supplying a greater volume of merchandise;

|

|

|

•

|

manage inventory and distribution effectively to meet the needs of new and existing stores on a timely basis;

|

|

|

•

|

expand our infrastructure to accommodate growth; and

|

|

|

•

|

generate sufficient operating cash flows or secure adequate capital on commercially reasonable terms to fund our expansion plans.

|

There are a finite number of suitable locations and malls within the United States and Canada in which to locate our stores. If we are unable to locate additional suitable locations to open new stores successfully and/or enter new markets, then there will be an adverse effect on the rate of our revenue and earnings growth.

We rely on a small number of vendors to supply a significant amount of our merchandise.

During fiscal 2010, we sourced approximately 85% of our merchandise from our top five merchandise vendors. During fiscal 2009, we sourced approximately 81% of our merchandise from our top five merchandise vendors. Our relationships with our suppliers generally are not on a long-term contractual basis and do not provide assurances on a long-term basis as to adequate supply, quality or acceptable pricing. Most of our suppliers could discontinue selling to us at any time. If one or more of our significant suppliers were to sever their relationship with us, we may not be able to obtain replacement products in a timely manner, which would have a material adverse effect on our sales, financial condition and results of operations. In addition, we do not own or operate any of our own manufacturing facilities and therefore we depend upon independent third party vendors to manufacture all of the merchandise we sell in our stores. If any of our vendors, especially our primary vendors which manufacture the majority of our merchandise, ship orders to us late, do not meet our quality standards, or otherwise fail to deliver us product in accordance with our plans, then there would be a material adverse effect on our results of operations.

Our foreign sources of production may not always be reliable, which may result in a disruption in the flow of new merchandise to our stores.

The large majority of the merchandise we purchase is manufactured overseas. We do not have any long-term merchandise supply contracts with our vendors and the imports of our merchandise by our vendors are subject to existing or potential duties, tariffs and quotas. We also face a variety of other risks generally associated with doing business in foreign markets and importing merchandise from abroad, such as: (i) political instability; (ii) enhanced security measures at foreign and United States ports, which could delay delivery of goods; (iii) imposition of new legislation relating to import quotas that may limit the quantity of goods which may be imported into the United States from countries in a region within which we do business; (iv) imposition of additional or greater duties, taxes, and other charges on imports; (v) delayed receipt or non-delivery of goods due to the failure of our vendors to comply with applicable import regulations; and (vi) delayed receipt or non-delivery of goods due to unexpected or significant port congestion or labor unrest at United States ports. Any disruption to our vendors and our foreign sources of production due to any of the factors listed above or due to other unforeseeable events or circumstances could have a material adverse effect on our results of operations.

Failure of new business concepts would have a negative effect on our results of operations.

We expect that the introduction of new brand concepts, such as the launch in fiscal 2009 of our new store brand concept P.S. from Aéropostale, as well as other new business opportunities, such as international expansion, will play an important role in our overall growth strategy. Our ability to succeed with a new brand concept requires significant expenditures and management attention. Additionally, any new brand is subject to certain risks including customer acceptance, competition, product differentiation, the ability to attract and retain qualified personnel, including management and designers, diversion of management’s attention from our core Aéropostale business and the ability to obtain suitable sites for new stores. Our experience with our Jimmy’Z brand, which we have now closed, demonstrates that there can be no assurance that new brands will grow or become profitable.

Our business could suffer if a manufacturer fails to use acceptable labor practices.

Our sourcing agents and independent manufacturers are required to operate in compliance with all applicable foreign and domestic laws and regulations. While our vendor operating guidelines promote ethical business practices for our vendors and suppliers, we do not control these manufacturers or their labor practices. The violation of labor or other laws by an independent manufacturer, or by one of the sourcing agents, or the divergence of an independent manufacturer’s or sourcing agent’s labor practices from those generally accepted as ethical in the United States, could interrupt, or otherwise disrupt the shipment of finished products or damage our reputation. Any of these, in turn, could have a material adverse effect on our financial condition and results of operations. To help mitigate this risk, we engage a third party independent contractor to visit the production facilities from which we receive our products. This independent contractor assesses the compliance of the facility with, among other things, local and United States labor laws and regulations as well as foreign and domestic fair trade and business practices.

The unexpected loss of the services of key personnel could have a material adverse effect on our business.

Our key executive officers have substantial experience and expertise in the retail industry and have made significant contributions to the growth and success of our brands. The unexpected loss of the services of one or more of these individuals could adversely affect us. Specifically, if we were to unexpectedly lose the services of Thomas P. Johnson, our Chief Executive Officer, or Michael J. Cunningham, our President, our business could be adversely affected. In addition, departures of any other senior executives or key performers in the Company could also adversely affect our operations.

A substantial interruption in our information systems could have a material adverse effect on our business.

We depend on the security and integrity of electronic data and our management information systems for many aspects of our business. We may be materially adversely affected if our management information systems are disrupted or compromised or we are unable to improve, upgrade, maintain, and expand our management information systems.

We rely on third parties to manage our distribution centers and transport our merchandise to our stores; a disruption of our distribution activities could have a material adverse effect on our business.

The efficient operation of our stores is dependent on our ability to distribute, in a timely manner, our merchandise to our store locations throughout the United States and Canada. We currently lease and maintain two, third party, independently operated distribution facilities, one in South River, New Jersey, and the other in Ontario, California. These distribution centers manage, collectively, the receipt, storage, sortation, packaging and distribution of virtually all of our merchandise. In addition, we also utilize a third distribution center, located in Canada, which is independently owned and operated.

These third parties employ personnel represented by labor unions. Although there have been no work stoppages or disruptions since the inception of our relationships with these third party providers, there can be no assurance that work stoppages or disruptions will not occur in the future. We also use separate third party transportation companies to deliver our merchandise from our distribution centers to our stores. Any failure by any of these third parties to respond adequately to our warehousing, distribution and transportation needs would have a material adverse effect on our results of operations.

Failure to comply with regulatory requirements could have a material adverse effect on our business.

As a public company, we are subject to numerous regulatory requirements. Our policies, procedures and internal controls are designed to comply with all applicable laws and regulations, including those imposed by the Sarbanes-Oxley Act of 2002, the Securities and Exchange Commission (“SEC”) and the NYSE. Failure to comply with such laws and regulations could have a material adverse effect on our reputation, financial condition and on the market price of our common stock.

We rely on a third party to manage the web-hosting, operation, warehousing and order fulfillment for our e-commerce business; any disruption of these activities could have a material adverse effect on our e-commerce business.

We rely on one third party, GSI Commerce, Inc. (“GSI”), to host our e-commerce website, warehouse all of the inventory sold through our e-commerce website, and fulfill all of our e-commerce sales to our customers. GSI also performs additional services for us supporting our e-commerce business. Any significant interruption in the operations of GSI, over which we have no control, could have a material adverse effect on our e-commerce business.

Failure to protect our trademarks adequately could negatively impact our brand image and limit our ability to penetrate new markets.

We believe that our key trademarks AÉROPOSTALE®, AERO® and 87® and our new store concept brand, P.S. FROM AÉROPOSTALE™ and variations thereof, are integral to our logo-driven design strategy. We have obtained federal registrations of or have pending applications for these trademarks in the United States and have applied for or obtained registrations in most foreign countries in which our vendors are located, as well as elsewhere. We use these trademarks in many constantly changing designs and logos even though we have not applied to register every variation or combination thereof for adult clothing and related accessories. There can be no assurance that the registrations we own and have obtained will prevent the imitation of our products or infringement of our intellectual property rights by others. If any third party imitates our products in a manner that projects lesser quality or carries a negative connotation, our brand image could be materially adversely affected.

There can be no assurance that others will not try to block the manufacture, export or sale of our products as a violation of their trademarks or other proprietary rights. Other entities may have rights to trademarks that contain portions of our marks or may have registered similar or competing marks for apparel and accessories in foreign countries in which our vendors are located. There may also be other prior registrations in other foreign countries of which we are not aware. Accordingly, it may not be possible, in those few foreign countries where we were not able to register our marks, to enjoin the manufacture, sale or exportation of AÉROPOSTALE or P.S. FROM AÉROPOSTALE branded goods to the United States. If we were unable to reach a licensing arrangement with these parties, our vendors may be unable to manufacture our products in those countries. Our inability to register our trademarks or purchase or license the right to use our trademarks or logos in these jurisdictions could limit our ability to obtain supplies from or manufacture in less costly markets or penetrate new markets should our business plan change to include selling our merchandise in those jurisdictions outside the United States.

The effects of war, acts of terrorism, natural disasters or other unforeseen wide-scale events could have a material adverse effect on our operating results and financial condition.

The continued threat of terrorism and the associated heightened security measures and military actions in response to acts of terrorism has disrupted commerce and has intensified uncertainties in the U.S. economy. Any further acts of terrorism or a future war may disrupt commerce and undermine consumer confidence, which could negatively impact our sales revenue by causing consumer spending and/or mall traffic to decline. Furthermore, an act of terrorism or war, or the threat thereof, or any other natural disaster that results in unforeseen interruptions of commerce, could negatively impact our business by interfering with our ability to obtain merchandise from our vendors.

None

We lease all of our store locations. Most of our stores are located in shopping malls throughout the U.S. and Canada. Most of our store leases have a term of ten years and require us to pay additional rent based on specified percentages of sales after we achieve specified annual sales thresholds. Generally, our store leases do not contain extension options. Our store leases typically include a pre-opening period of approximately 60 days that allows us to take possession of the property to construct the store. Typically rent payment commences when the stores open. We recognize rent expense in our consolidated financial statements on a straight-line basis over the non-cancelable term of each individual underlying lease, commencing when we take possession of the property. Generally, our leases allow for termination by us after a certain period of time if sales at that site do not exceed specified levels.

Our new flagship store in Times Square, New York City, and our other two street stores in New York City, have lease terms of fifteen years.

We lease 89,000 square feet of office space at 112 West 34th Street in New York, New York. The facility is used as our corporate headquarters and for our design, sourcing and production teams. These leases expire in 2015 and 2016.

We also lease 40,000 square feet of office space at 201 Willowbrook Boulevard in Wayne, New Jersey. This facility is used as administrative offices for finance, operations and information systems personnel. This lease expires in 2012 and provides us with a five year option to extend at the end of the initial term. We are currently evaluating other alternatives to exercising this option.

In addition, we lease a 315,000 square foot distribution and warehouse facility in South River, New Jersey. This lease expires in 2021. We also lease a second 360,000 square foot distribution facility in Ontario, California. This lease expires in 2015. These facilities are used to warehouse inventory needed to replenish and back-stock all of our stores, as well as to serve our general warehousing needs.

In January 2008, we learned that the Securities and Exchange Commission (the “SEC”) had issued a formal order of investigation with respect to matters arising from the activities of Christopher L. Finazzo, our former Executive Vice President and Chief Merchandising Officer. On September 16, 2010, we were advised by the SEC that they had concluded their investigation as it related to the company, with no further action being taken.

We are also party to various litigation matters and proceedings in the ordinary course of business. In the opinion of our management, dispositions of these matters are not expected to have a material adverse impact on our financial position, results of operations or cash flows.

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is traded on the New York Stock Exchange under the symbol “ARO”. The following table sets forth the range of high and low sales prices of our common stock as reported on the New York Stock Exchange since February 2, 2009.

|

|

Market Price

|

|||||||

|

|

High

|

Low

|

||||||

|

Fiscal 2010

|

||||||||

|

4th quarter

|

$ | 27.03 | $ | 23.04 | ||||

|

3rd quarter

|

28.57 | 21.30 | ||||||

|

2nd quarter

|

30.88 | 27.14 | ||||||

|

1st quarter

|

32.08 | 21.89 | ||||||

| Fiscal 2009 | ||||||||

|

4th quarter

|

$ | 25.50 | $ | 19.30 | ||||

|

3rd quarter

|

29.47 | 23.43 | ||||||

|

2nd quarter

|

25.48 | 20.67 | ||||||

|

1st quarter

|

22.65 | 13.78 | ||||||

As of March 18, 2011, there were 60 stockholders of record. However, when including others holding shares in broker accounts under street name, we estimate the shareholder base at approximately 28,999.

All stock prices in the above table were adjusted for the three-for-two stock split on all shares of our common stock that was distributed on March 5, 2010.

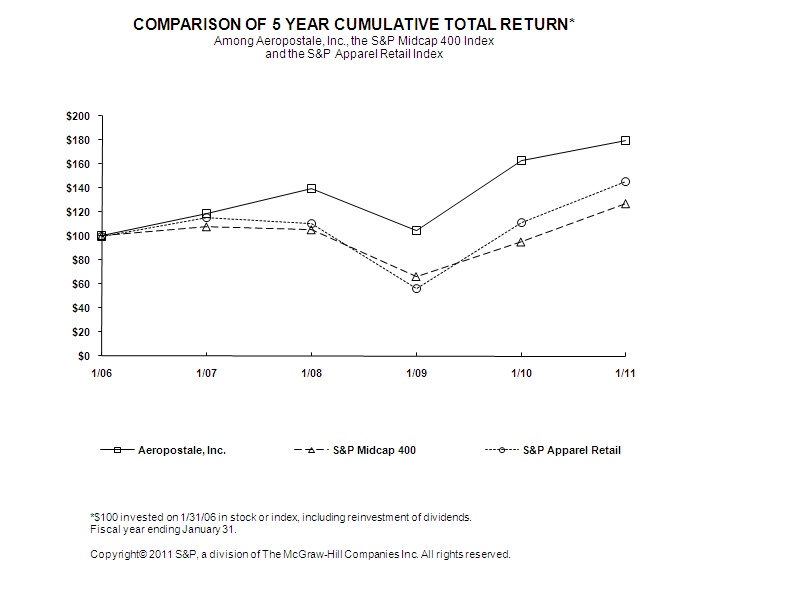

PERFORMANCE GRAPH

The following graph shows the changes, for the period commencing January 29, 2006 and ended January 28, 2011 (the last trading day during fiscal 2010), in the value of $100 invested in shares of our common stock, the Standard & Poor’s MidCap 400 Composite Stock Price Index (the “S&P MidCap 400 Index”) and the Standard & Poor’s Apparel Retail Composite Index (the “S&P Apparel Retail Index”). The plotted points represent the closing price on the last trading day of the fiscal year indicated.

| 1/06 | 1/07 | 1/08 | 1/09 | 1/10 | 1/11 | |||||||||||||||||||

|

Aéropostale, Inc.

|

$ | 100 | $ | 119 | $ | 140 | $ | 105 | $ | 163 | $ | 180 | ||||||||||||

|

S&P Midcap 400

|

$ | 100 | $ | 108 | $ | 106 | $ | 67 | $ | 95 | $ | 127 | ||||||||||||

|

S&P Apparel Retail

|

$ | 100 | $ | 115 | $ | 110 | $ | 56 | $ | 111 | $ | 146 |

We have not paid a dividend on our common stock during our last three fiscal years, and we do not have any current intention to pay a dividend on our common stock.

We repurchase our common stock from time to time under a stock repurchase program. On November 11, 2010, our Board of Directors approved a $300.0 million increase in repurchase availability under the program, bringing total repurchase authorization, since inception of the program, to $1.15 billion. The repurchase program may be modified or terminated by the Board of Directors at any time, and there is no expiration date for the program. The extent and timing of repurchases will depend upon general business and market conditions, stock prices, opening and closing of our stock trading window, and liquidity and capital resource requirements going forward. Our purchases of treasury stock for the fourth quarter of fiscal 2010 and remaining availability pursuant to our share repurchase program were as follows:

|

Period

|

Total Number

of Shares

(or Units)

Purchased

|

Average

Price Paid

per Share

|

Total Number of

Shares Purchased

as Part of Publicly

Announced Plans

or Programs

|

Approximate Dollar

Value of Shares

that may yet be

Purchased Under the

Plans or Programs

(a) (b)

|

||||||||||||

|

(In thousands)

|

||||||||||||||||

|

October 31 to November 27, 2010

|

2,647,000 | $ | 24.97 | 2,647,000 | $ | 330,475 | ||||||||||

|

November 28, 2010 to January 1, 2011

|

900,000 | 24.20 | 900,000 | $ | 308,692 | |||||||||||

|

January 2 to January 29, 2011

|

2,500,000 | 25.34 | 2,500,000 | $ | 245,337 | |||||||||||

|

Total

|

6,047,000 | $ | 25.01 | 6,047,000 | ||||||||||||

__________

|

(a)

|

The repurchase program may be modified or terminated by the Board of Directors at any time, and there is no expiration date for the program.

|

|

(b)

|

Includes additional $300.0 million of repurchase availability that was approved on November 11, 2010.

|

The following selected financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and with our consolidated financial statements and other financial information appearing elsewhere in this document:

|

Fiscal Year Ended

|

||||||||||||||||||||

|

|

January 29,

2011

|

January 30,

2010

|

January 31,

2009

|

February 2,

2008 (1)

|

February 3,

2007 (2) (3)

|

|||||||||||||||

|

(In thousands, except per share and store data)

|

||||||||||||||||||||

|

Statements of Income Data:

|

||||||||||||||||||||

|

Net sales

|

$ | 2,400,434 | $ | 2,230,105 | $ | 1,885,531 | $ | 1,590,883 | $ | 1,413,208 | ||||||||||

|

Gross profit, as a percent of sales

|

36.9 | % | 38.0 | % | 34.7 | % | 34.8 | % | 32.2 | % | ||||||||||

|

SG&A, as a percent of sales

|

20.8 | % | 20.8 | % | 21.5 | % | 21.7 | % | 20.5 | % | ||||||||||

|

Income from operations, as a percent of sales

|

16.1 | % | 17.2 | % | 13.2 | % | 12.8 | % | 11.9 | % | ||||||||||

|

Net income, as a percent of sales

|

9.6 | % | 10.3 | % | 7.9 | % | 8.2 | % | 7.5 | % | ||||||||||

|

Net income

|

$ | 231,339 | $ | 229,457 | $ | 149,422 | $ | 129,197 | $ | 106,647 | ||||||||||

|

Diluted earnings per common share (4)

|

$ | 2.49 | $ | 2.27 | $ | 1.47 | $ | 1.15 | $ | 0.88 | ||||||||||

|

Selected Operating Data:

|

||||||||||||||||||||

|

Number of stores open at end of period

|

1,012 | 952 | 914 | 828 | 742 | |||||||||||||||

|

Comparable store sales increase

|

1 | % | 10 | % | 8 | % | 3 | % | 2 | % | ||||||||||

|

Comparable average unit retail change

|

(4 | )% | 3 | % | 2 | % | (3 | )% | 3 | % | ||||||||||

|

Average net sales per store (in thousands)

|

$ | 2,267 | $ | 2,243 | $ | 2,042 | $ | 1,932 | $ | 1,924 | ||||||||||

|

Average square footage per store

|

3,659 | 3,601 | 3,594 | 3,546 | 3,540 | |||||||||||||||

|

Net store sales per average square foot

|

$ | 626 | $ | 624 | $ | 572 | $ | 545 | $ | 543 | ||||||||||

|

|

As of

|

|||||||||||||||||||

|

|

January 29,

2011

|

January 30,

2010

|

January 31,

2009

|

February 2,

2008

|

February 3,

2007

|

|||||||||||||||

|

(In thousands)

|

||||||||||||||||||||

|

Balance Sheet Data:

|

||||||||||||||||||||

|

Working capital

|

$ | 253,463 | $ | 288,177 | $ | 218,444 | $ | 87,300 | $ | 233,995 | ||||||||||

|

Total assets

|

773,197 | 792,309 | 657,919 | 514,169 | 581,164 | |||||||||||||||

|

Long-term liabilities

|

124,458 | 115,980 | 127,422 | 119,506 | 104,250 | |||||||||||||||

|

Total debt

|

— | — | — | — | — | |||||||||||||||

|

Retained earnings (5)

|

389,764 | 922,790 | 693,333 | 543,911 | 414,916 | |||||||||||||||

|

Total stockholder’s equity

|

432,637 | 434,489 | 355,060 | 197,276 | 312,116 | |||||||||||||||

__________

|

(1)

|

Includes initial gift card breakage income of $7.7 million ($4.8 million, after tax, or $0.05 per diluted share) and other operating income of $4.1 million ($2.6 million, after tax, or $0.03 per diluted share) as a result of an agreement with Christopher L. Finazzo, our former Executive Vice President and Chief Merchandising Officer, partially offset by an asset impairment charge of $9.0 million ($5.7 million, after tax, or $0.05 per diluted share).

|

|

|

(2)

|

Includes $7.4 million ($4.5 million, after tax, or $0.03 per diluted share), net of professional fees, representing concessions, primarily from South Bay Apparel Inc., to us for prior purchases of merchandise and other operating income of $2.1 million ($1.3 million, after tax, or $0.01 per diluted share) from the resolution of a dispute with a vendor regarding the enforcement of our intellectual property rights.

|

|

|

(3)

|

53-week fiscal year.

|

|

|

(4)

|

In March 2010, we completed a three-for-two stock split on all shares of our common stock. All share and per share amounts presented in the consolidated financial statements were retroactively adjusted for the common stock split, as were all previously reported periods contained herein.

|

|

|

(5)

|

On October 20, 2010, we retired 47.5 million shares of our treasury stock. These shares remain as authorized stock; however they are now considered unissued. In accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 505, “Equity” (“ASC 505”), the treasury stock retirement resulted in a reduction of the following on our consolidated balance sheet: common stock by $0.4 million, treasury stock by $764.8 million and retained earnings by $764.4 million. There was no effect on total stockholders’ equity position as a result of the retirement.

|

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations Introduction

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements involve certain risks and uncertainties, including statements regarding our strategic direction, prospects and future results. Certain factors, including factors outside of our control, may cause actual results to differ materially from those contained in the forward-looking statements. The risk factors included in Part I, Item 1A should be read in connection with evaluating our business and future prospects. All forward looking statements included in this report are based on information available to us as of the date hereof, and we assume no obligation to update or revise such forward-looking statements to reflect events or circumstances that occur after such statements are made.

Overview

Aéropostale, Inc. and its subsidiaries is a primarily mall-based, specialty retailer of casual apparel and accessories, principally targeting 14 to 17 year-old young women and men through its Aéropostale stores and 7 to 12 year-old kids through its P.S. from Aéropostale stores. The Company provides customers with a focused selection of high quality fashion and fashion basics at compelling values in an innovative and exciting store environment. Aéropostale maintains control over its proprietary brands by designing, sourcing, marketing and selling all of its own merchandise. Aéropostale products can only be purchased in Aéropostale stores and online at www.aeropostale.com. P.S. from Aéropostale products can only be purchased in P.S. from Aéropostale stores, certain Aéropostale stores and online at www.ps4u.com. As of January 29, 2011, we operated 965 Aéropostale stores consisting of 906 stores in 49 states and Puerto Rico, 59 stores in Canada, as well as 47 P.S. from Aéropostale stores in 13 states. In addition, pursuant to a Licensing Agreement, one of our international licensees operated 10 Aéropostale stores in the United Arab Emirates as of January 29, 2011. During March 2011, we announced that we had signed a second licensing agreement. The licensee to this agreement is expected to open approximately 25 stores in Singapore, Malaysia and Indonesia over the next five years.

During December 2010, Thomas P. Johnson, Co-Chief Executive Officer, was named the Company’s Chief Executive Officer. Mr. Johnson also continues to serve as a member of our Board of Directors. Also during December 2010, Mindy C. Meads departed from the Company, ending her tenure as both Co-Chief Executive Officer and as a director.

Our fiscal year ends on the Saturday nearest to January 31. Fiscal 2010 was the 52-week period ended January 29, 2011; fiscal 2009 was the 52-week period ended January 30, 2010, and fiscal 2008 was the 52-week period ended January 31, 2009. Fiscal 2011 will be the 52-week period ending January 28, 2012.

The discussion in the following section is on a consolidated basis, unless indicated otherwise.

Fiscal 2010 Highlights

We achieved net sales of $2.4 billion during fiscal 2010, an increase of $170.3 million or 8% from fiscal 2009. Gross profit, as a percentage of net sales, decreased by 1.1 percentage points for fiscal 2010. Selling, general and administrative expense, or SG&A, as a percentage of net sales, remained consistent in fiscal 2010. The effective tax rate was 40.2% for fiscal 2010, compared with 40.1% for fiscal 2009. Net income for fiscal 2010 was $231.3 million, or $2.49 per diluted share, compared with net income of $229.5 million, or $2.27 per diluted share, for fiscal 2009.

As of January 29, 2011, we had working capital of $253.5 million, cash and cash equivalents of $265.6 million, no short-term investments and no debt outstanding. Merchandise inventories increased by 9% on a per retail square foot basis as of January 29, 2011 compared to last year. Cash flows from operating activities were $263.7 million for fiscal 2010. We operated 1,012 total stores as of January 29, 2011, an increase of 6% from the same period last year.

During fiscal 2010, we repurchased 10.3 million shares of our common stock for $257.5 million, as compared to repurchases of 7.6 million shares for $174.3 million during fiscal 2009. Program to date, we repurchased 53.0 million shares for $904.0 million, at an average price of $17.06 per share. We have approximately $245.3 million of repurchase authorization remaining as of January 29, 2011 under the $1.15 billion share repurchase program.

Key Performance Measures

We use a number of key indicators of financial condition and operating performance to evaluate the performance of our business, including the following:

|

|

Fiscal Year Ended

|

|||||||||||

|

|

January 29,

2011

|

January 30,

2010

|

January 31,

2009

|

|||||||||

|

Net sales (in millions)

|

$ | 2,400.4 | $ | 2,230.1 | $ | 1,885.5 | ||||||

|

Total store count at end of period

|

1,012 | 952 | 914 | |||||||||

|

Comparable store count at end of period

|

918 | 878 | 811 | |||||||||

|

Net sales growth

|

8 | % | 18 | % | 19 | % | ||||||

|

Comparable store sales growth

|

1 | % | 10 | % | 8 | % | ||||||

|

Comparable average unit retail change

|

(4 | )% | 3 | % | 2 | % | ||||||

|

Comparable units per sales transaction change

|

4 | % | 4 | % | 3 | % | ||||||

|

Comparable sales transaction growth

|

2 | % | 4 | % | 4 | % | ||||||

|

Net store sales per average square foot

|

$ | 626 | $ | 624 | $ | 572 | ||||||

|

Average net sales per store (in thousands)

|

$ | 2,267 | $ | 2,243 | $ | 2,042 | ||||||

|

Gross profit (in millions)

|

$ | 886.2 | $ | 847.1 | $ | 654.2 | ||||||

|

Income from operations (in millions)

|

$ | 386.8 | $ | 382.7 | $ | 248.3 | ||||||

|

Diluted earnings per share

|

$ | 2.49 | $ | 2.27 | $ | 1.47 | ||||||

|

Average store square footage growth over comparable period

|

6 | % | 7 | % | 12 | % | ||||||

|

Change in total inventory at end of period

|

18 | % | 5 | % | (7 | )% | ||||||

|

Change in inventory per retail square foot at end of period

|

9 | % | (2 | )% | (17 | )% | ||||||

|

Percentages of net sales by category

|

||||||||||||

|

Women’s

|

69 | % | 70 | % | 71 | % | ||||||

|

Men’s

|

31 | % | 30 | % | 29 | % | ||||||

Results of Operations

The following table sets forth our results of operations expressed as a percentage of net sales. We also use this information to evaluate the performance of our business:

|

|

Fiscal Year Ended

|

|||||||||||

|

January 29,

2011

|

January 30,

2010

|

January 31,

2009

|

||||||||||

|

Net sales

|

100.0 | % | 100.0 | % | 100.0 | % | ||||||

|

Gross profit

|

36.9 | 38.0 | 34.7 | |||||||||

|

SG&A

|

20.8 | 20.8 | 21.5 | |||||||||

|

Income from operations

|

16.1 | 17.2 | 13.2 | |||||||||

|

Income before income taxes

|

16.1 | 17.2 | 13.2 | |||||||||

|

Income taxes

|

6.5 | 6.9 | 5.3 | |||||||||

|

Net income

|

9.6 | % | 10.3 | % | 7.9 | % | ||||||

Sales

Net sales consist of sales from comparable stores, non-comparable stores, and from our e-commerce business. A store is included in comparable store sales after 14 months of operation. We consider a remodeled or relocated store with more than a 25% change in square feet to be a new store. Prior period sales from stores that have closed are not included in comparable store sales, nor are sales from our e-commerce business.