2019

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

OR

Commission file number:

(Exact name of registrant as specified in its charter)

(I.R.S. Employer

,

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code:

-

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading symbols

Name of each exchange on which registered

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the

Act. [ ] Yes [x]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was

required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [x]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be

submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for

such shorter period that the registrant was required to submit such files). [x]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a

smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,”

“accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

[x] Accelerated filer [ ] Non-accelerated filer [ ]

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended

transition period for complying with any new or revised financial accounting standards provided pursuant to Section

13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). [ ] Yes [x]

The aggregate market value of common stock held by non-affiliates of the registrant on June 28, 2019, the last

business day of the registrant’s most recently completed second fiscal quarter, based on the closing price on that date

of $61.00, was $

The registrant had

Documents incorporated by reference:

Portions of the Proxy Statement for the Annual Meeting of Stockholders to be held on May 12, 2020 (Part III)

TABLE OF CONTENTS

Page

Commonly Used Abbreviations……………………………………………………………………….

1

Item

PART I

1 and 2.

Business and Properties ......................................................................................................

2

Corporate Structure ........................................................................................................

2

Segment and Geographic Information ...........................................................................

2

Alaska .......................................................................................................................

4

Lower 48 ...................................................................................................................

6

Canada ......................................................................................................................

9

Europe and North Africa ...........................................................................................

10

Asia Pacific and Middle East ....................................................................................

12

Other International ....................................................................................................

17

Competition ...................................................................................................................

19

General ...........................................................................................................................

19

1A.

Risk Factors ........................................................................................................................

21

1B.

Unresolved Staff Comments ...............................................................................................

28

3.

Legal Proceedings ...............................................................................................................

28

4.

Mine Safety Disclosures .....................................................................................................

28

Information About our Executive Officers .........................................................................

29

PART II

5.

Market for Registrant’s Common Equity, Related Stockholder Matters and

Issuer Purchases of Equity Securities ............................................................................

31

6.

Selected Financial Data ......................................................................................................

34

7.

Management’s Discussion and Analysis of Financial Condition and

Results of Operations .....................................................................................................

35

7A.

Quantitative and Qualitative Disclosures About Market Risk ............................................

72

8.

Financial Statements and Supplementary Data ...................................................................

75

9.

Changes in and Disagreements with Accountants on Accounting and

Financial Disclosure .......................................................................................................

185

9A.

Controls and Procedures .....................................................................................................

185

9B.

Other Information ...............................................................................................................

185

PART III

10.

Directors, Executive Officers and Corporate Governance ..................................................

186

11.

Executive Compensation ....................................................................................................

186

12.

Security Ownership of Certain Beneficial Owners and Management and

Related Stockholder Matters ..........................................................................................

186

13.

Certain Relationships and Related Transactions, and Director Independence....................

186

14.

Principal Accounting Fees and Services .............................................................................

186

PART IV

15.

Exhibits, Financial Statement Schedules ............................................................................

187

Signatures ...........................................................................................................................

197

1

Commonly Used Abbreviations

The following industry-specific, accounting and other terms, and abbreviations may be commonly used in this

report.

Currencies

Accounting

$ or USD

U.S. dollar

ARO

asset retirement obligation

CAD

Canadian dollar

ASC

accounting standards codification

GBP

British pound

ASU

accounting standards update

DD&A

depreciation, depletion and

Units of Measurement

amortization

BBL

barrel

FASB

Financial Accounting Standards

BCF

billion cubic feet

Board

BOE

barrels of oil equivalent

FIFO

first-in, first-out

MBD

thousands of barrels per day

G&A

general and administrative

MCF

thousand cubic feet

GAAP

generally accepted accounting

MMBOE

million barrels of oil equivalent

principles

MBOED

thousands of barrels of oil

LIFO

last-in, first-out

equivalent per day

NPNS

normal purchase normal sale

MMBTU

million British thermal units

PP&E

properties, plants and equipment

MMCFD

million cubic feet per day

SAB

staff accounting bulletin

VIE

variable interest entity

Industry

CBM

coalbed methane

Miscellaneous

E&P

exploration and production

EPA

Environmental Protection Agency

FEED

front-end engineering and design

EU

European Union

FPS

floating production system

FERC

Federal Energy Regulatory

FPSO

floating production, storage and

Commission

offloading

GHG

greenhouse gas

JOA

joint operating agreement

HSE

health, safety and environment

LNG

liquefied natural gas

ICC

International Chamber of

NGLs

natural gas liquids

Commerce

OPEC

Organization of Petroleum

ICSID

World Bank’s International

Exporting Countries

Centre for Settlement of

PSC

production sharing contract

Investment Disputes

PUDs

proved undeveloped reserves

IRS

Internal Revenue Service

SAGD

steam-assisted gravity drainage

OTC

over-the-counter

WCS

Western Canada Select

NYSE

New York Stock Exchange

WTI

West Texas Intermediate

SEC

U.S. Securities and Exchange

Commission

TSR

total shareholder return

U.K.

United Kingdom

U.S.

United States of America

2

PART I

Unless otherwise indicated, “the company,” “we,” “our,” “us” and “ConocoPhillips” are used in this report to

refer to the businesses of ConocoPhillips and its consolidated subsidiaries. Items 1 and 2—Business and

Properties, contain forward-looking statements including, without limitation, statements relating to our plans,

strategies, objectives, expectations and intentions that are made pursuant to the “safe harbor” provisions of the

Private Securities Litigation Reform Act of 1995. The words “anticipate,” “estimate,” “believe,” “budget,”

“continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “seek,” “should,” “will,” “would,”

“expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target” and similar

expressions identify forward-looking statements. The company does not undertake to update, revise or correct

any forward-looking information unless required to do so under the federal securities laws. Readers are

cautioned that such forward-looking statements should be read in conjunction with the company’s disclosures

under the headings “Risk Factors” beginning on page 21 and “CAUTIONARY STATEMENT FOR THE

PURPOSES OF THE ‘SAFE HARBOR’ PROVISIONS OF THE PRIVATE SECURITIES LITIGATION

REFORM ACT OF 1995,” beginning on page

Items 1 and 2. BUSINESS AND PROPERTIES

CORPORATE STRUCTURE

ConocoPhillips is an independent E&P company with operations and activities in 17 countries. Our diverse,

low cost of supply portfolio includes resource-rich unconventional plays in North America; conventional

assets in North America, Europe, Asia and Australia; LNG developments; oil sands assets in Canada; and an

inventory of global conventional and unconventional exploration prospects. Headquartered in Houston, Texas,

at December 31, 2019, we employed approximately 10,400 people worldwide and had total assets of $71

billion.

ConocoPhillips was incorporated in the state of Delaware on November 16, 2001, in connection with, and in

anticipation of, the merger between Conoco Inc. and Phillips Petroleum Company. The merger between

Conoco and Phillips was consummated on August 30, 2002.

SEGMENT AND GEOGRAPHIC INFORMATION

For operating segment and geographic information, see Note 25—Segment Disclosures and Related

Information, in the Notes to Consolidated Financial Statements, which is incorporated herein by reference.

We explore for, produce, transport and market crude oil, bitumen, natural gas, LNG and NGLs on a worldwide

basis. At December 31, 2019, our operations were producing in the U.S., Norway, Canada, Australia, Timor-

Leste, Indonesia, Malaysia, Libya, China and Qatar.

The information listed below appears in the “Oil and Gas Operations” disclosures following the Notes to

Consolidated Financial Statements and is incorporated herein by reference:

●

Proved worldwide crude oil, NGLs, natural gas and bitumen reserves.

●

Net production of crude oil, NGLs, natural gas and bitumen.

●

Average sales prices of crude oil, NGLs, natural gas and bitumen.

●

Average production costs per BOE.

●

Net wells completed, wells in progress and productive wells.

●

Developed and undeveloped acreage.

3

The following table is a summary of the proved reserves information included in the “Oil and Gas Operations”

disclosures following the Notes to Consolidated Financial Statements. Approximately 80 percent of our

proved reserves are located in politically stable countries that belong to the Organization for Economic

Cooperation and Development. Natural gas reserves are converted to BOE based on a 6:1 ratio: six MCF of

natural gas converts to one BOE. See Management’s Discussion and Analysis of Financial Condition and

Results of Operations for a discussion of factors that will enhance the understanding of the following summary

reserves table.

Millions of Barrels of Oil Equivalent

Net Proved Reserves at December 31

2019

2018

2017

Crude oil

Consolidated operations

2,562

2,533

2,322

Equity affiliates

73

78

83

Total Crude Oil

2,635

2,611

2,405

Natural gas liquids

Consolidated operations

361

349

354

Equity affiliates

39

42

45

Total Natural Gas Liquids

400

391

399

Natural gas

Consolidated operations

1,209

1,265

1,267

Equity affiliates

736

760

717

Total Natural Gas

1,945

2,025

1,984

Bitumen

Consolidated operations

282

236

250

Total Bitumen

282

236

250

Total consolidated operations

4,414

4,383

4,193

Total equity affiliates

848

880

845

Total company

5,262

5,263

5,038

Total production of 1,348 MBOED increased 5 percent in 2019 compared with 2018.

average production primarily resulted from new wells online in the Lower 48; an increased interest in the

Western North Slope (WNS) and Greater Kuparuk Area (GKA) of Alaska following acquisitions closed in

2018; and higher production in Norway due to drilling activity and the startup of Aasta Hansteen in December

2018. The increase in production was partly offset by normal field decline and disposition impacts, primarily

from the U.K. asset sale in 2019 and non-core asset sales in the Lower 48 during 2018.

4

Production excluding Libya was 1,305 MBOED in 2019 compared with 1,242 MBOED in 2018, an increase of

63 MBOED or 5 percent. Underlying production, which excludes Libya and the net volume impact from

closed dispositions and acquisitions of 51 MBOED in 2019 and 47 MBOED in 2018, is used to measure our

ability to grow production organically. Our underlying production grew 5 percent to 1,254 MBOED in 2019

from 1,195 MBOED in 2018.

Our worldwide annual average realized price was $48.78 per BOE in 2019, a decrease of 9 percent compared

with $53.88 per BOE in 2018, reflecting weaker marker prices as a result of macroeconomic demand concerns.

Our worldwide annual average crude oil price decreased 10 percent, from $68.13 per barrel in 2018 to $60.99

per barrel in 2019. Additionally, our worldwide annual average NGL prices decreased 34 percent, from

$30.48 per barrel in 2018 to $20.09 per barrel in 2019. Our worldwide annual average natural gas price

decreased 11 percent, from $5.65 per MCF in 2018 to $5.03 per MCF in 2019. Average annual bitumen prices

increased 42 percent, from $22.29 per barrel in 2018 to $31.72 per barrel in 2019.

ALASKA

The Alaska segment primarily explores for, produces, transports and markets crude oil, natural gas and NGLs.

We are the largest crude oil producer in Alaska and have major ownership interests in two of North America’s

largest oil fields located on Alaska’s North Slope: Prudhoe Bay and Kuparuk. We also have a 100 percent

interest in the Alpine Field, located on the Western North Slope. Additionally, we are one of Alaska’s largest

owners of state, federal and fee exploration leases, with approximately 1.32 million net undeveloped acres at

year-end 2019. Alaska operations contributed 25 percent of our worldwide liquids production and less than 1

percent of our natural gas production.

2019

Interest

Operator

Liquids

MBD

Natural Gas

MMCFD

Total

MBOED

Average Daily Net Production

Greater Prudhoe Area

36.1

%

BP

81

4

81

Greater Kuparuk Area

91.4-94.7

ConocoPhillips

86

2

86

Western North Slope

100.0

ConocoPhillips

50

1

51

Total Alaska

217

7

218

Greater Prudhoe Area

The Greater Prudhoe Area includes the Prudhoe Bay Field and five satellite fields, as well as the Greater Point

McIntyre Area fields. Prudhoe Bay, the largest oil field on Alaska’s North Slope, is the site of a large

waterflood and enhanced oil recovery operation, as well as a gas plant which processes natural gas to recover

NGLs before reinjection into the reservoir. Prudhoe Bay’s satellites are Aurora, Borealis, Polaris, Midnight

Sun and Orion, while the Point McIntyre, Niakuk, Raven, Lisburne and North Prudhoe Bay State fields are

part of the Greater Point McIntyre Area.

Greater Kuparuk Area

We operate the Greater Kuparuk Area, which consists of the Kuparuk Field and four satellite fields: Tarn,

Tabasco, Meltwater and West Sak. Kuparuk is located 40 miles west of Prudhoe Bay. Field installations

include three central production facilities which separate oil, natural gas and water, as well as a separate

seawater treatment plant. Development drilling at Kuparuk consists of rotary-drilled wells and horizontal

multi-laterals from existing well bores utilizing coiled-tubing drilling.

5

Western North Slope

On the Western North Slope, we operate the Colville River Unit, which includes the Alpine Field and three

satellite fields: Nanuq, Fiord and Qannik. Alpine is located 34 miles west of Kuparuk. In 2015, first oil was

achieved at Alpine West CD5, a drill site which extends the Alpine reservoir west into the National Petroleum

Reserve-Alaska (NPR-A). In 2019, we continued drilling additional wells using the available well slots on this

pad.

The Greater Mooses Tooth Unit, the first unit established entirely within the NPR-A, was formed in 2008. In

2017, we began construction in the unit with two drill sites; Greater Mooses Tooth #1 (GMT-1) and Greater

Mooses Tooth #2 (GMT-2). GMT-1 achieved first oil in the fourth quarter of 2018 and completed drilling in

2019. We expect first oil from GMT-2 in 2021.

Alaska North Slope Gas

In 2016, we, along with affiliates of Exxon Mobil Corporation, BP p.l.c. and Alaska Gasline Development

Corporation (AGDC), a state-owned corporation, completed preliminary FEED technical work for a potential

LNG project which would liquefy and export natural gas from Alaska’s North Slope and deliver it to

market. In 2016, we, along with the affiliates of ExxonMobil and BP, indicated our intention not to progress

into the next phase of the project due to changes in the economic environment. AGDC decided to continue on

its own. In 2019, affiliates of ExxonMobil and BP agreed to each contribute up to $5 million or approximately

one third of AGDC’s anticipated costs for full-year 2020. In 2020, AGDC will be focused on permitting

efforts, the most important of which is the National Environmental Protection Act process before the FERC.

FERC’s final milestones are the Publication of Notice of Availability of Final Environmental Impact

Statement, which is scheduled for March 6, 2020, and the Issuance of Final Order, which is scheduled for June

4, 2020. AGDC has recently contracted with Fluor Corporation to evaluate cost reduction opportunities in

preparation for soliciting partners for the project. We continue to be willing to sell our North Slope gas to the

project but do not plan to take an equity position.

Exploration

Appraisal of the Willow Discovery, located in the northeast portion of the NPR-A, continued throughout 2019

with five appraisal wells. In 2020, we will continue appraisal of the Willow Discovery and explore the

Harpoon Prospect, located southwest of Willow.

In 2019, we drilled the West Willow-2 well to appraise the 2018 West Willow oil discovery.

In late 2018, we commenced appraisal of the Putu Discovery with a long reach well from existing Alpine CD4

infrastructure. The CD4 appraisal well finished drilling and flow tested in 2019. A supporting injector well

was drilled in late 2019 for a 2020 injectivity test.

The Cairn 2S-315 Well was drilled in late 2018 from the 2S drill site on state leases in the Kuparuk River Unit.

A long-term flow test was commenced in 2019 and evaluations are ongoing.

A 3-D seismic survey was completed in 2018 over a 250-mile area on state lands. We are currently evaluating

this seismic data for future exploration opportunities.

We were successful in the federal lease sale on the North Slope in the fourth quarter of 2019, where we were

the high bidder on three tracts for a total of approximately 33,000 net acres.

Acquisitions

In the third quarter of 2019, we completed the Nuna discovery acreage acquisition, expanding the Kuparuk

River Unit by 21,000 acres and leveraging legacy infrastructure.

6

Transportation

We transport the petroleum liquids produced on the North Slope to south central Alaska through an 800-mile

pipeline that is part of Trans-Alaska Pipeline System (TAPS). We have a 29.1 percent ownership interest in

TAPS, and we also have ownership interests in the Alpine, Kuparuk and Oliktok pipelines on the North Slope.

Our wholly owned subsidiary, Polar Tankers, Inc., manages the marine transportation of our North Slope

production, using five company-owned, double-hulled tankers, and charters third-party vessels as necessary.

The tankers deliver oil from Valdez, Alaska, primarily to refineries on the west coast of the U.S.

LOWER 48

The Lower 48 segment consists of operations located in the contiguous U.S. and the Gulf of Mexico.

Organized into the Gulf Coast and Great Plains business units, we hold 10.4 million net onshore and offshore

acres, with a portfolio of conventional production from legacy assets as well as newer production from our low

cost of supply, shorter cycle time, resource-rich unconventional plays. Based on 2019 production volumes, the

Lower 48 is the company’s largest segment and contributed 39 percent of our worldwide liquids production

and 22 percent of our natural gas production.

2019

Interest

Operator

Liquids

MBD

Natural Gas

MMCFD

Total

MBOED

Average Daily Net Production

Eagle Ford

Various

%

Various

174

251

216

Gulf of Mexico

Various

Various

15

11

16

Gulf Coast—Other

Various

Various

3

9

5

192

271

237

Bakken

Various

Various

82

92

97

Permian Unconventional

Various

Various

40

94

56

Permian Conventional

Various

Various

20

59

30

Anadarko Basin

Various

Various

5

58

14

Wyoming/Uinta

Various

Various

-

36

6

Niobrara*

Various

Various

8

12

11

155

351

214

Total Lower 48

347

622

451

*Classified as held-for-sale as of December 31, 2019. See 'Dispositions' below for additional information.

Onshore

We hold 10.3 million net acres of onshore conventional and unconventional acreage in the Lower 48, the

majority of which is either held by production or owned by the company. Our unconventional holdings total

approximately 1.7 million net acres in the following areas:

●

610,000 net acres in the Bakken, located in North Dakota and eastern Montana.

●

234,000 net acres in Central Louisiana, where we recently announced our intention to discontinue

exploration activities.

●

201,000 net acres in the Eagle Ford, located in South Texas.

●

167,000 net acres in the Permian, located in West Texas and southeastern New Mexico.

●

98,000 net acres in the Niobrara, located in northeastern Colorado.

●

363,000 net acres in other areas with unconventional potential.

7

The majority of our 2019 onshore production originated from the Big 3—Eagle Ford, Bakken and Permian

Unconventional. Onshore activities in 2019 were centered mostly on continued development of assets, with an

emphasis on areas with low cost of supply, particularly in growing unconventional plays. Our major focus

areas in 2019 included the following:

●

Eagle Ford—The Eagle Ford continued full-field development in 2019. We operated seven rigs on

average in 2019, resulting in 155 operated wells drilled and 166 operated wells brought online.

Production increased 16 percent in 2019 compared with 2018, averaging 216 MBOED and 186

MBOED, respectively.

●

Bakken—We operated an average of three rigs during the year in the Bakken and participated in

additional development activities operated by co-venturers. We continued our pad drilling with 62

operated wells drilled during the year and 44 operated wells brought online. Production increased 15

percent in 2019 compared with 2018, averaging 97 MBOED and 84 MBOED, respectively.

●

Permian Basin—The Permian Basin is a combination of legacy conventional and unconventional

assets. We operated an average of three rigs during the year in the Permian Basin, resulting in 29

operated wells drilled and 35 operated wells brought online. The Permian Basin produced 86

MBOED in 2019, increasing 30 percent compared with 2018, including 56 MBOED of

unconventional production.

Gulf of Mexico

At year-end 2019, our portfolio of producing properties in the Gulf of Mexico totaled approximately 60,000

net acres. A majority of the production consists of three fields operated by co-venturers:

●

15.9 percent nonoperated working interest in the unitized Ursa Field located in the Mississippi Canyon

Area.

●

15.9 percent nonoperated working interest in the Princess Field, a northern subsalt extension of the

Ursa Field.

●

12.4 percent nonoperated working interest in the unitized K2 Field, comprised of seven blocks in the

Green Canyon Area.

Dispositions

We have terminal and pipeline use agreements with Golden Pass LNG Terminal and affiliated Golden Pass

Pipeline near Sabine Pass, Texas, intended to provide us with terminal and pipeline capacity for the receipt,

storage and regasification of LNG purchased from Qatar Liquefied Gas Company Limited (3) (QG3). We

previously held a 12.4 percent interest in Golden Pass LNG Terminal and Golden Pass Pipeline, but we sold

those interests in the second quarter of 2019 while retaining the basic use agreements.

In the fourth quarter of 2019, we completed the sale of our interests in the Magnolia Field in the Gulf of

Mexico. Production from this disposed asset was less than one MBOED in 2019.

In the fourth quarter of 2019, we entered into an agreement to sell our interests in the Niobrara, with an

anticipated closing date in the first quarter of 2020. Production from the interests to be disposed was

approximately 11 MBOED in 2019.

In January 2020, we entered into an agreement to sell our interests in certain non-core properties for $186

million, plus customary adjustments. The assets met the held for sale criteria in January 2020 and the

transaction is expected to be completed in the first quarter of 2020. This disposition will not have a significant

impact on Lower 48 production.

For additional information on these transactions, see Note 5—Asset Acquisitions and Dispositions, in the

Notes to Consolidated Financial Statements.

8

Exploration

Our exploration focus is on onshore unconventional plays, which in 2019 included the Delaware in the

Permian Basin, and the Eagle Ford in south Texas. In the third quarter of 2019, we announced our decision to

discontinue exploration activities in the Central Louisiana Austin Chalk.

Facilities

●

Lost Cabin Gas Plant—We operate and own a 46 percent interest in the Lost Cabin Gas Plant, a 246

MMCFD capacity natural gas processing facility in Lysite, Wyoming. The plant is currently operating at

less than capacity due to a fire in December 2018. Restoration efforts are ongoing and anticipated to be

completed in the second half of 2020. The expected production loss in 2020 is immaterial to the segment.

●

Helena Condensate Processing Facility—We operate and own the Helena Condensate Processing Facility,

a 110 MBD condensate processing plant located in Kenedy, Texas.

●

Sugarloaf Condensate Processing Facility—We operate and own an 87.5 percent interest in the Sugarloaf

Condensate Processing Facility, a 30 MBD condensate processing plant located near Pawnee, Texas.

●

Bordovsky Condensate Processing Facility—We operate and own the Bordovsky Condensate Processing

Facility, a 15 MBD condensate processing plant located in Kenedy, Texas.

9

CANADA

Our Canadian operations mainly consist of the Surmont oil sands development in Alberta and the liquids-rich

Montney unconventional play in British Columbia. In 2019, operations in Canada contributed 7 percent of our

worldwide liquids production and less than 1 percent of our natural gas production.

2019

Natural

Liquids

Gas

Bitumen

Total

Interest

Operator

MBD

MMCFD

MBD

MBOED

Average Daily Net Production

Surmont

50.0

%

ConocoPhillips

-

-

60

60

Montney

100.0

ConocoPhillips

1

9

-

3

Total Canada

1

9

60

63

Surmont

Our bitumen resources in Canada are produced via an enhanced thermal oil recovery method called SAGD,

whereby steam is injected into the reservoir, effectively liquefying the heavy bitumen, which is recovered and

pumped to the surface for further processing. We hold approximately 0.6 million net acres of land in the

Athabasca Region of northeastern Alberta.

The Surmont oil sands leases are located approximately 35 miles south of Fort McMurray, Alberta. Surmont

is a 50/50 joint venture with Total S.A. The second phase of the Surmont Project achieved first production in

2015 and reached peak production in 2018. We are focused on structurally lowering costs, reducing GHG

intensity and optimizing asset performance.

The Alberta government imposed a production curtailment impacting the industry beginning in January 2019.

The curtailment measure, which impacted our annualized average production by 3 MBOED in 2019, is

intended to strengthen the WCS differential to WTI at Hardisty. The curtailment program is established and

administered by the Alberta Energy Regulator under the

Curtailment Rules

expire on December 31, 2020.

Montney

We hold approximately 151,000 net acres in the emerging unconventional Montney play in northeast British

Columbia. Our Montney activity in 2019 included drilling 16 horizontal wells, completing 14 horizontal wells

and acquiring approximately 6,000 additional net acres. Production from our 2019 drilling program

commenced in February 2020 following the completion of third-party offtake facilities.

Appraisal drilling and completions activity will continue in 2020 to further explore the area’s resource

potential.

Exploration

Our primary exploration focus is assessing our Montney onshore unconventional acreage in Western Canada.

Additionally, we have exploration acreage in the Mackenzie Delta/Beaufort Sea Region and the Arctic Islands.

10

EUROPE AND NORTH AFRICA

The Europe and North Africa segment consisted of operations in Norway, Libya and the U.K. and exploration

activities in Norway and Libya. In 2019, operations in Europe and North Africa contributed 16 percent of our

worldwide liquids production and 17 percent of natural gas production.

Norway

2019

Liquids

Natural Gas

Total

Interest

Operator

MBD

MMCFD

MBOED

Average Daily Net Production

Greater Ekofisk Area

35.1

%

ConocoPhillips

50

44

57

Heidrun

24.0

Equinor

14

29

19

Alvheim

20.0

Aker BP

10

12

12

Visund

9.1

Equinor

4

46

12

Aasta Hansteen

10.0

Equinor

-

64

11

Troll

1.6

Equinor

2

49

10

Other

Various

Equinor

8

10

10

Total Norway

88

254

131

The Greater Ekofisk Area is located approximately 200 miles offshore Stavanger, Norway, in the North Sea,

and comprises three producing fields: Ekofisk, Eldfisk and Embla. Crude oil is exported to Teesside, England,

and the natural gas is exported to Emden, Germany. The Ekofisk and Eldfisk fields consist of several

production platforms and facilities, including the Ekofisk South and Eldfisk II developments. Continued

development drilling in the Greater Ekofisk Area is expected to contribute additional production over the

coming years, as additional wells come online.

The Heidrun Field is located in the Norwegian Sea. Produced crude oil is stored in a floating storage unit and

exported via shuttle tankers. Part of the natural gas is currently injected into the reservoir for optimization of

crude oil production, some gas is transported for use as feedstock in a methanol plant in Norway, in which we

own an 18 percent interest, and the remainder is transported to Europe via gas processing terminals in Norway.

The Alvheim Field is located in the northern part of the North Sea near the border with the U.K. sector, and

consists of a FPSO vessel and subsea installations. Produced crude oil is exported via shuttle tankers, and

natural gas is transported to the Scottish Area Gas Evacuation (SAGE) Terminal at St. Fergus, Scotland,

through the SAGE Pipeline.

Visund is an oil and gas field located in the North Sea and consists of a floating drilling, production and

processing unit, and subsea installations. Crude oil is transported by pipeline to a nearby third-party field for

storage and export via tankers. The natural gas is transported to a gas processing plant at Kollsnes, Norway,

through the Gassled transportation system.

Aasta Hansteen is located in the Norwegian Sea and achieved first production in December 2018. Produced

condensate is loaded onto shuttle tankers and transported to market. Gas is transported through the Polarled

gas pipeline to the onshore Nyhamna processing plant for final processing prior to export to market.

The Troll Field lies in the northern part of the North Sea and consists of the Troll A, B and C platforms. The

natural gas from Troll A is transported to Kollsnes, Norway. Crude oil from floating platforms Troll B and

Troll C is transported to Mongstad, Norway, for storage and export.

We also have varying ownership interests in two other producing fields in the Norway sector of the North Sea.

11

Exploration

In 2019, we operated the Busta and Enniberg exploration wells in Block 25/7 in the North Sea. The Busta well

encountered hydrocarbons and will be evaluated for future appraisal consideration. The Enniberg well

encountered insufficient hydrocarbons and was expensed as a dry hole in 2019. We also participated in the

Canela exploration well in the Heidrun area of the Norwegian Sea. The well encountered hydrocarbons and

will be further evaluated to determine commerciality. In 2019, we were awarded two new exploration

licenses; PL1001 and PL1009; and one acreage addition, PL782SD.

Transportation

We own a 35.1 percent interest in the Norpipe Oil Pipeline System, a 220-mile pipeline which carries crude oil

from Ekofisk to a crude oil stabilization and NGLs processing facility in Teesside, England.

United Kingdom

2019

Natural

Liquids

Total

Interest

Operator

MBD

MMCFD

MBOED

Average Daily Net Production

Britannia Satellites*

26.3–93.8

%

ConocoPhillips

7

55

16

J-Area

32.5–36.5

ConocoPhillips

6

38

12

Britannia

58.7

ConocoPhillips

2

49

10

East Irish Sea

100.0

Spirit Energy

-

48

8

Clair

7.5

BP

4

1

4

Other

Various

Various

-

2

-

Total United Kingdom

19

193

50

*Includes the Chevron-operated Alder Field, ConocoPhillips equity interest was 26.3 percent.

On September 30, 2019, we completed the sale of two ConocoPhillips U.K. subsidiaries to Chrysaor E&P

Limited, including all of our producing assets in the U.K. Annualized average production from the assets sold

was 50 MBOED in 2019. For additional information on this transaction, see Note 5—Asset Acquisitions and

Dispositions, in the Notes to Consolidated Financial Statements.

We retained our Teesside, England oil terminal, where we are the operator and have a 40.25 percent ownership

interest, to support our Norway operations.

Libya

2019

Natural

Liquids

Gas

Total

Interest

Operator

MBD

MMCFD

MBOED

Average Daily Net Production

Waha Concession

16.3

%

Waha Oil Co.

38

31

43

Total Libya

38

31

43

The Waha Concession consists of multiple concessions and encompasses nearly 13 million gross acres in the

Sirte Basin. Our production operations in Libya and related oil exports have periodically been interrupted over

the last several years due to the shutdown of the Es Sider crude oil export terminal. In 2019, we had 19 crude

liftings from Es Sider. The number of crude liftings from the Es Sider crude oil export terminal in 2020 is

uncertain due to civil unrest. In January 2020, we declared Force Majeure to our crude shippers following the

12

blockade of the Es Sider crude oil export terminal and the declaration of Force Majeure by the National Oil

Corporation of Libya.

ASIA PACIFIC AND MIDDLE EAST

The Asia Pacific and Middle East segment has exploration and production operations in China, Indonesia,

Malaysia and Australia and producing operations in Qatar and Timor-Leste. In 2019, operations in the Asia

Pacific and Middle East segment contributed 13 percent of our worldwide liquids production and 60 percent of

natural gas production.

Australia and Timor-Leste

2019

Natural

Liquids

Total

Interest

Operator

MBD

MMCFD

MBOED

Average Daily Net Production

ConocoPhillips/

Australia Pacific LNG

37.5

%

Origin Energy

-

679

113

Bayu-Undan*

56.9

ConocoPhillips

10

194

43

Athena/Perseus*

50.0

ExxonMobil

-

31

5

Total Australia and Timor-Leste

10

904

161

*This asset is held-for-sale as of December 31, 2019. See Note 5—Asset Acquisitions and Dispositions, in the Notes to Consolidated Financial

Statements, for additional information.

Australia Pacific LNG

Australia Pacific LNG Pty Ltd (APLNG), our joint venture with Origin Energy Limited and China

Petrochemical Corporation (Sinopec), is focused on producing CBM from the Bowen and Surat basins in

Queensland, Australia, to supply the domestic gas market and convert the CBM into LNG for export. Origin

operates APLNG’s upstream production and pipeline system, and we operate the downstream LNG facility,

located on Curtis Island near Gladstone, Queensland, as well as the LNG export sales business.

We operate two fully subscribed 4.5-million-metric-tonnes-per-year LNG trains. Approximately 3,900 net

wells are ultimately expected to supply both the LNG sales contracts and domestic gas market. The wells are

supported by gathering systems, central gas processing and compression stations, water treatment facilities,

and an export pipeline connecting the gas fields to the LNG facilities. The LNG is being sold to Sinopec under

20-year sales agreements for 7.6 million metric tonnes of LNG per year, and Japan-based Kansai Electric

Power Co., Inc. under a 20-year sales agreement for approximately 1 million metric tonnes of LNG per year.

As of December 31, 2019, APLNG has an outstanding balance of $6.7 billion on a $8.5 billion project finance

facility. In late 2018 and early 2019, APLNG successfully refinanced $4.6 billion of the project finance

facility through three separate transactions, which added lower cost United States Private Placement (USPP)

bond and commercial bank facilities. In conjunction with these transactions, APLNG made voluntary

repayments of $2.2 billion to a syndicate of Australian and international commercial banks and fully

extinguished $2.4 billion of financing from the Export-Import Bank of China. Project finance interest

payments are bi-annual, concluding September 2030.

For additional information, see Note 3—Variable Interest Entities, Note 6—Investments, Loans and Long-

Term Receivables and Note 12—Guarantees, in the Notes to Consolidated Financial Statements.

13

Bayu-Undan

The Bayu-Undan gas condensate field is located in the Timor Sea Joint Petroleum Development Area between

Timor-Leste and Australia. We also operate and own a 56.9 percent interest in the associated Darwin LNG

Facility, located at Wickham Point, Darwin.

The Bayu-Undan natural gas recycle facility processes wet gas; separates, stores and offloads condensate,

propane and butane; and re-injects dry gas back into the reservoir. In addition, a 310-mile natural gas pipeline

connects the facility to the 3.5-million-metric-tonnes-per-year capacity Darwin LNG Facility. Produced

natural gas is piped to the Darwin LNG Plant, where it is converted into LNG before being transported to

international markets. In 2019, we sold 133 billion gross cubic feet of LNG primarily to utility customers in

Japan.

Athena/Perseus

The Athena production license (WA-17-L) in which we had a 50 percent working interest is located offshore

Western Australia and our entitlement to production ended in the fourth quarter of 2019. Annualized average

production from this license was five MBOED in 2019.

Exploration

We operate three exploration permits in the Browse Basin, offshore northwest Australia, in which we own a 40

percent interest in permits WA-315-P, WA-398-P and TP 28, of the Greater Poseidon Area. Phase I of the

Browse Basin drilling campaign resulted in three discoveries in the Greater Poseidon Area and Phase II

resulted in five additional discoveries. All wells have been plugged and abandoned.

We operate two retention leases in the Bonaparte Basin, offshore northern Australia, where we own a 37.5

percent interest in the Barossa and Caldita discoveries. In April 2018, Barossa entered the FEED phase of

development which continued through 2019. During the FEED phase, costs and the technical definition for the

project will be finalized, gas and condensate sales agreements progressed, and access arrangements negotiated

with the owners of the Darwin LNG Facility and Bayu-Darwin Pipeline.

In December 2019, we entered into an agreement with 3D Oil to acquire a 75 percent interest and operatorship

of an offshore Tasmanian Permit located in the Otway Basin. The farm-in agreement is conditional upon the

agreement and signing of a JOA by both parties and required government approvals. We plan to conduct a 3D

seismic survey in the second half of 2020. This activity is excluded from the dispositions discussed below.

Dispositions

In the second quarter of 2019, we completed the sale of our 30 percent interest in the Greater Sunrise Fields to

the government of Timor-Leste.

In October 2019, we entered into an agreement to sell the subsidiaries that hold our Australia-West assets and

operations to Santos with an expected completion date in the first quarter of 2020, subject to regulatory

approvals and other specific conditions precedent. These subsidiaries hold our 37.5 percent interest in the

Barossa Project and Caldita Field, our 56.9 percent interest in the Darwin LNG Facility and Bayu-Undan

Field, our 40 percent interest in the Greater Poseidon Fields, and our 50 percent interest in the Athena Field.

Production associated with the Australia-West assets to be sold was 48 MBOED in 2019.

For additional information on these transactions, see Note 5—Asset Acquisitions and Dispositions, in the

Notes to Consolidated Financial Statements.

14

Indonesia

2019

Natural

Liquids

Total

Interest

Operator

MBD

MMCFD

MBOED

Average Daily Net Production

South Sumatra

54

%

ConocoPhillips

2

321

56

Total Indonesia

2

321

56

During 2019, we operated three PSCs in Indonesia: the Corridor Block and South Jambi “B,” both located in

South Sumatra, and Kualakurun in Central Kalimantan. Currently, we have production from the Corridor

Block.

South Sumatra

The Corridor PSC consists of two oil fields and seven producing natural gas fields. Natural gas is supplied

from the Grissik and Suban gas processing plants to the Duri steamflood in central Sumatra and to markets in

Singapore, Batam and West Java. In 2019, we were awarded a 20-year extension, with new terms, of the

Corridor PSC. Under these terms, we retain a majority interest and continue as operator for at least three years

after 2023 and retain a participating interest until 2043.

Production from the South Jambi “B” PSC has reached depletion and field development has been suspended.

This PSC expired on January 26, 2020 and has been returned to the Government of Indonesia.

Exploration

We hold a 60 percent working interest in the Kualakurun PSC. After completion of prospect evaluation, we

and the other joint venture partners decided to relinquish all of the remaining acreage to the Government of

Indonesia.

Transportation

We are a 35 percent owner of a consortium company that has a 40 percent ownership in PT Transportasi Gas

Indonesia, which owns and operates the Grissik to Duri and Grissik to Singapore natural gas pipelines.

China

2019

Natural

Liquids

Gas

Total

Interest

Operator

MBD

MMCFD

MBOED

Average Daily Net Production

Penglai

49.0

%

CNOOC

29

-

29

Panyu

24.5

CNOOC

6

-

6

Total China

35

-

35

Penglai

The Penglai 19-3, 19-9 and 25-6 fields are located in Bohai Bay Block 11/05 and are in various stages of

development.

As part of further development of the Penglai 19-9 Field, the wellhead platform J Project achieved first

production in 2016. This project will include 62 wells, 57 of which have been completed and brought online

through December 2019.

15

The Penglai 19-3/19-9 Phase 3 Project consists of three new wellhead platforms and a central processing

platform. First oil from Phase 3 was achieved in 2018 for two of the platforms, with the third platform planned

to come online in the second quarter of 2020. This project could include up to 186 wells, 42 of which have

been completed and brought online through December 2019.

In December 2018, we sanctioned the Penglai 25-6 Phase 4A Project. This project consists of one new

wellhead platform and anticipates 62 new wells. First production is expected in 2021.

Panyu

Our production license for Panyu 4-2, 5-1 and 11-6 located in Block 15/34 in the South China Sea expired in

September 2019. Annualized average production from these licenses were six MBOED in 2019.

We still have a license for Panyu 4-1 in Block 15/34 and are evaluating this area for potential development.

Exploration

Exploration activities in the Bohai Penglai Field during 2019 consisted of two successful appraisal wells, a

full-field 3-D seismic program covering existing and future development opportunities, and an infill

compressive seismic imaging (CSI) survey to improve imaging beneath the gas cloud in support of future

development projects. In Block 15/34, one exploration well was drilled in the Panyu 4-1E prospect and was

expensed as a dry hole.

Malaysia

2019

Natural

Liquids

Gas

Total

Interest

Operator

MBD

MMCFD

MBOED

Average Daily Net Production

Gumusut

29.0

%

Shell

23

-

23

Kebabangan (KBB)

30.0

KPOC

3

91

18

Malikai

35.0

Shell

15

-

15

Siakap North-Petai

21.0

PTTEP

1

-

1

Total Malaysia

42

91

57

We have varying stages of exploration, development and production activities across 2.2 million net acres in

Malaysia, with working interests in six PSCs. Three of these PSCs are located off the eastern Malaysian state

of Sabah: Block G, Block J and the Kebabangan Cluster (KBBC). We operated three exploration blocks,

Block SK304, Block SK313 and Block WL4-00, off the eastern Malaysian state of Sarawak.

Block J

Gumusut

First production from the Gumusut Field occurred from an early production system in 2012. Production from

a permanent, semi-submersible Floating Production System was achieved in 2014. We currently have a 29

percent working interest in the Gumusut Field following the redetermination of the Block J and Block K

Malaysia Unit in 2017. Gumusut Phase 2 first oil was achieved in 2019.

KBBC

The KBBC PSC grants us a 30 percent working interest in the KBB, Kamunsu East and Kamunsu East

Upthrown Canyon gas and condensate fields.

KBB

First production from the KBB gas field was achieved in 2014. During 2019, KBB tied-in to a nearby third-

party floating LNG vessel which provided increased gas offtake capacity. Production in 2020 is anticipated to

be impacted between 15 to 20 MBOED due to the rupture of a third-party pipeline, in January 2020, which

16

carries gas production from the KBB gas field to market. The extent of the required pipeline repairs, and the

amount of time required to return this pipeline to full service is still being evaluated.

Kamunsu East

Development options for the Kamunsu East gas field are being evaluated.

Block G

Malikai

We hold a 35 percent working interest in Malikai. This field achieved first production in December 2016 via

the Malikai Tension Leg Platform, ramping to peak production in 2018. The KMU-1 exploration well was

completed and started producing through the Malikai platform in 2018. Malikai Phase 2 development, a 6-

well drilling campaign that will commence in 2020, reached a final investment decision in late 2019.

Siakap North-Petai

We hold a 21 percent working interest in the unitized Siakap North-Petai oil field.

Exploration

In 2016, we entered into a farm-in agreement to acquire a 50 percent working interest in Block SK 313, a 1.4

million gross-acre exploration block offshore Sarawak, with an effective date of January 2017. Following

completion of the Sadok-1 exploration well in January 2017, we assumed operatorship of the block from

PETRONAS and completed a 3-D seismic survey. We have no plans for further exploration activity in this

block.

In 2017, we were awarded operatorship and a 50 percent working interest in Block WL4-00, which included

the existing Salam-1 oil discovery and encompassed 0.6 million gross acres. In 2018 and 2019, two

exploration and two appraisal wells were drilled, resulting in oil discoveries under evaluation at Salam and

Benum, while two Patawali wells were expensed as dry holes in 2019.

In 2018, we were awarded a 50 percent working interest and operatorship of Block SK304 encompassing 2.1

million gross acres offshore Sarawak. We acquired 3-D seismic over the acreage and completed processing of

this data in 2019.

The Gemilang-1 exploration well in Block J was completed in late 2018. Development options are being

evaluated.

Qatar

2019

Natural

Liquids

Gas

Total

Interest

Operator

MBD

MMCFD

MBOED

Average Daily Net Production

Qatargas Operating

QG3

30.0

%

Company Limited

21

373

83

Total Qatar

21

373

83

QG3 is an integrated development jointly owned by Qatar Petroleum (68.5 percent), ConocoPhillips

(30 percent) and Mitsui & Co., Ltd. (1.5 percent). QG3 consists of upstream natural gas production facilities,

which produce approximately 1.4 billion gross cubic feet per day of natural gas from Qatar’s North Field over

a 25-year life, in addition to a 7.8 million gross tonnes-per-year LNG facility. LNG is shipped in leased LNG

carriers destined for sale globally.

17

QG3 executed the development of the onshore and offshore assets as a single integrated development with

Qatargas 4 (QG4), a joint venture between Qatar Petroleum and Royal Dutch Shell plc. This included the joint

development of offshore facilities situated in a common offshore block in the North Field, as well as the

construction of two identical LNG process trains and associated gas treating facilities for both the QG3 and

QG4 joint ventures. Production from the LNG trains and associated facilities is combined and shared.

OTHER INTERNATIONAL

The Other International segment includes exploration activities in Colombia, Chile and Argentina and

contingencies associated with prior operations.

Colombia

We have an 80 percent operated interest in the Middle Magdalena Basin Block VMM-3. The block extends

over approximately 67,000 net acres and contains the Picoplata-1 Well, which completed drilling in 2015 and

testing in 2017. Plug and abandonment activity started during 2018 and completed in 2019. In addition, we

have an 80 percent working interest in the VMM-2 Block which extends over approximately 58,000 net acres

and is contiguous to the VMM-3 Block. As part of a case brought forward by environmental groups, the

Highest Administrative Court granted a preliminary injunction temporarily suspending hydraulic fracturing

activities until the substance of the case is decided. As a result, ConocoPhillips filed two separate Force

Majeure requests before the competent authority for both blocks, which were granted.

Chile

We have a 49 percent interest in the Coiron Block located in the Magallanes Basin in southern Chile.

Argentina

In January 2019, we secured a 50 percent nonoperated interest in the El Turbio Este Block, within the Austral

Basin in southern Argentina. In 2019, we acquired and processed 3-D seismic covering approximately 500

square miles, with evaluation of the data ongoing.

In November 2019, we acquired interests in two nonoperated blocks in the Neuquén Basin targeting the Vaca

Muerta play. We have a 50 percent interest in the Bandurria Norte Block and a 45 percent interest in the

Aguada Federal Block. In Bandurria Norte, one vertical and four horizontal wells were tested and shut-in

during 2019. In Aguada Federal, two horizontal wells were being tested at the end of the year.

Venezuela and Ecuador

For discussion of our contingencies in Venezuela and Ecuador, see Note 13—Contingencies and

Commitments, in the Notes to Consolidated Financial Statements.

OTHER

Marketing Activities

Our Commercial organization manages our worldwide commodity portfolio, which mainly includes natural

gas, crude oil, bitumen, NGLs and LNG. Marketing activities are performed through offices in the U.S.,

Canada, Europe and Asia. In marketing our production, we attempt to minimize flow disruptions, maximize

realized prices and manage credit-risk exposure. Commodity sales are generally made at prevailing market

prices at the time of sale. We also purchase and sell third-party volumes to better position the company to

satisfy customer demand while fully utilizing transportation and storage capacity.

Natural Gas

Our natural gas production, along with third-party purchased gas, is primarily marketed in the U.S., Canada,

Europe and Asia. Our natural gas is sold to a diverse client portfolio which includes local distribution

companies; gas and power utilities; large industrials; independent, integrated or state-owned oil and gas

18

companies; as well as marketing companies. To reduce our market exposure and credit risk, we also transport

natural gas via firm and interruptible transportation agreements to major market hubs.

Crude Oil, Bitumen and Natural Gas Liquids

Our crude oil, bitumen and NGL revenues are derived from production in the U.S., Canada, Australia, Asia,

Africa and Europe. These commodities are primarily sold under contracts with prices based on market indices,

adjusted for location, quality and transportation.

LNG

LNG marketing efforts are focused on equity LNG production facilities located in Australia and Qatar. LNG

is primarily sold under long-term contracts with prices based on market indices.

Energy Partnerships

Marine Well Containment Company (MWCC)

We are a founding member of the MWCC, a non-profit organization formed in 2010, which provides well

containment equipment and technology in the deepwater U.S. Gulf of Mexico. MWCC’s containment system

meets the U.S. Bureau of Safety and Environmental Enforcement requirements for a subsea well containment

system that can respond to a deepwater well control incident in the U.S. Gulf of Mexico. For additional

information, see Note 3—Variable Interest Entities, in the Notes to Consolidated Financial Statements.

Subsea Well Response Project (SWRP)

In 2011, we, along with several leading oil and gas companies, launched the SWRP, a non-profit organization

based in Stavanger, Norway, which was created to enhance the industry’s capability to respond to international

subsea well control incidents. Through collaboration with Oil Spill Response Limited, a non-profit

organization in the U.K., subsea well intervention equipment is available for the industry to use in the event of

a subsea well incident. This complements the work being undertaken in the U.S. by MWCC and provides well

capping and containment capability outside the U.S.

Oil Spill Response Removal Organizations (OSROs)

We maintain memberships in several OSROs across the globe as a key element of our preparedness program in

addition to internal response resources. Many of the OSROs are not-for-profit cooperatives owned by the

member companies wherein we may actively participate as a member of the board of directors, steering

committee, work group or other supporting role. Globally, our primary OSRO is Oil Spill Response Ltd.

based in the U.K., with facilities in several other countries and the ability to respond anywhere in the world. In

North America, our primary OSROs include the Marine Spill Response Corporation for the continental United

States and Alaska Clean Seas and Ship Escort/Response Vessel System for the Alaska North Slope and Prince

William Sound, respectively. Internationally, we maintain memberships in various regional OSROs including

the Norwegian Clean Seas Association for Operating Companies, Australian Marine Oil Spill Center and

Petroleum Industry of Malaysia Mutual Aid Group.

Technology

We have several technology programs that improve our ability to develop unconventional reservoirs, produce

heavy oil economically with less emissions, improve the efficiency of our exploration program, increase

recoveries from our legacy fields, and implement sustainability measures.

Our Optimized Cascade

®

for new LNG plants. The technology has been licensed for use in 26 LNG trains around the world, with

feasibility studies ongoing for additional trains.

19

RESERVES

We have not filed any information with any other federal authority or agency with respect to our estimated

total proved reserves at December 31, 2019. No difference exists between our estimated total proved reserves

for year-end 2018 and year-end 2017, which are shown in this filing, and estimates of these reserves shown in

a filing with another federal agency in 2019.

DELIVERY COMMITMENTS

We sell crude oil and natural gas from our producing operations under a variety of contractual arrangements,

some of which specify the delivery of a fixed and determinable quantity. Our commercial organization also

enters into natural gas sales contracts where the source of the natural gas used to fulfill the contract can be the

spot market or a combination of our reserves and the spot market. Worldwide, we are contractually committed

to deliver approximately 1.1 trillion cubic feet of natural gas, including approximately 75 billion cubic feet

related to the noncontrolling interests of consolidated subsidiaries, and 172 million barrels of crude oil in the

future. These contracts have various expiration dates through the year 2030. We expect to fulfill the majority

of these delivery commitments with proved developed reserves. In addition, we anticipate using PUDs and

spot market purchases to fulfill any remaining commitments. See the disclosure on “Proved Undeveloped

Reserves” in the “Oil and Gas Operations” section following the Notes to Consolidated Financial Statements,

for information on the development of PUDs.

COMPETITION

We compete with private, public and state-owned companies in all facets of the E&P business. Some of our

competitors are larger and have greater resources. Each of our segments is highly competitive, with no single

competitor, or small group of competitors, dominating.

We compete with numerous other companies in the industry, including state-owned companies, to locate and

obtain new sources of supply and to produce oil, bitumen, NGLs and natural gas in an efficient, cost-effective

manner. Based on statistics published in the September 2, 2019, issue of the

Oil and Gas Journal

, we were the

third-largest U.S.-based oil and gas company in worldwide natural gas and liquids production and worldwide

liquids reserves in 2018. We deliver our production into the worldwide commodity markets. Principal

methods of competing include geological, geophysical and engineering research and technology; experience

and expertise; economic analysis in connection with portfolio management; and safely operating oil and gas

producing properties.

GENERAL

At the end of 2019, we held a total of 942 active patents in 50 countries worldwide, including 371 active U.S.

patents. During 2019, we received 64 patents in the U.S. and 90 foreign patents. Our products and processes

generated licensing revenues of $69 million related to activity in 2019. The overall profitability of any

business segment is not dependent on any single patent, trademark, license, franchise or concession.

20

Health, Safety and Environment

Our HSE organization provides tools and support to our business units and staff groups to help them ensure

world class HSE performance. The framework through which we safely manage our operations, the HSE

Management System Standard, emphasizes process safety, risk management, emergency preparedness and

environmental performance, with an intense focus on process and occupational safety. In support of the goal

of zero incidents, HSE milestones and criteria are established annually to drive strong safety and

environmental performance. Progress toward these milestones and criteria are measured and reported. HSE

audits are conducted on business functions periodically, and improvement actions are established and tracked

to completion. We have designed processes relating to sustainable development in our economic,

environmental and social performance. Our processes, related tools and requirements focus on water,

biodiversity and climate change, as well as social and stakeholder issues.

The environmental information contained in Management’s Discussion and Analysis of Financial Condition

and Results of Operations on pages 60 through 65 under the captions “Environmental” and “Climate Change”

is incorporated herein by reference. It includes information on expensed and capitalized environmental costs

for 2019 and those expected for 2020 and 2021.

Website Access to SEC Reports

Our internet website address is

www.conocophillips.com

. Information contained on our internet website is not

part of this report on Form 10-K.

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any

amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange

Act of 1934 are available on our website, free of charge, as soon as reasonably practicable after such reports

are filed with, or furnished to, the SEC. Alternatively, you may access these reports at the SEC’s website at

www.sec.gov

.

21

Item 1A. RISK FACTORS

You should carefully consider the following risk factors in addition to the other information included in this

Annual Report on Form 10-K. These risk factors are not the only risks we face. Our business could also be

affected by additional risks and uncertainties not currently known to us or that we currently consider to be

immaterial. If any of these risks were to occur, our business, operating results and financial condition, as well

as the value of an investment in our common stock could be adversely affected.

Our operating results, our future rate of growth and the carrying value of our assets are exposed to the

effects of changing commodity prices.

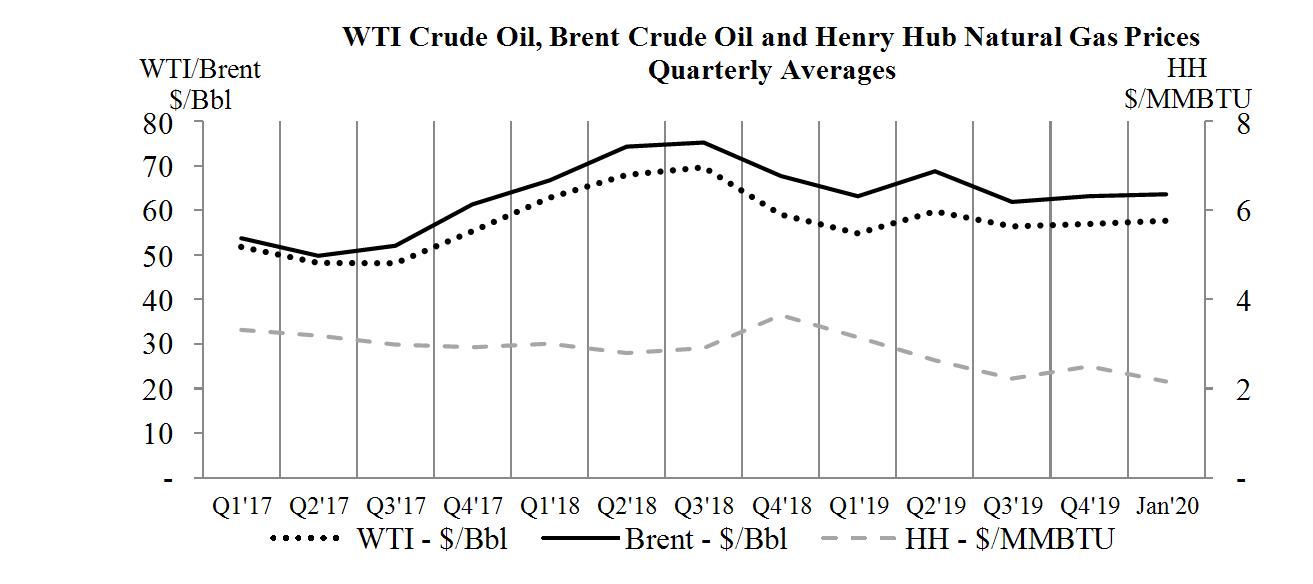

Prices for crude oil, bitumen, natural gas, NGLs and LNG can fluctuate widely. Brent crude oil prices

averaged $64 per barrel in 2019, ranging from a low of $53 per barrel in January to a high of almost $75 per

barrel in April. Given volatility in commodity price drivers and the worldwide political and economic

environment generally, as well as increased uncertainty generated by recent (and potential future) armed

hostilities in various oil-producing regions around the globe, price trends may continue to be volatile. Our

revenues, operating results and future rate of growth are highly dependent on the prices we receive for our

crude oil, bitumen, natural gas, NGLs and LNG. The factors influencing these prices are beyond our control.

Lower crude oil, bitumen, natural gas, NGL and LNG prices may have a material adverse effect on our

revenues, operating income, cash flows and liquidity, and may also affect the amount of dividends we elect to

declare and pay on our common stock and the amount of shares we elect to acquire as part of the share

repurchase program and the timing of such acquisitions. Lower prices may also limit the amount of reserves

we can produce economically, adversely affecting our proved reserves, reserve replacement ratio and

accelerating the reduction in our existing reserve levels as we continue production from upstream fields.

Significant reductions in crude oil, bitumen, natural gas, NGLs and LNG prices could also require us to reduce

our capital expenditures, impair the carrying value of our assets or discontinue the classification of certain

assets as proved reserves. In the past three years, we recognized several impairments, which are described in

Note 9—Impairments and the “APLNG” section of Note 6—Investments, Loans and Long-Term Receivables,

in the Notes to Consolidated Financial Statements. If commodity prices remain low relative to their historic

levels, and as we continue to optimize our investments and exercise capital flexibility, it is reasonably likely

we will incur future impairments to long-lived assets used in operations, investments in nonconsolidated

entities accounted for under the equity method and unproved properties. Although it is not reasonably

practicable to quantify the impact of any future impairments at this time, our results of operations could be

adversely affected as a result.

Our ability to declare and pay dividends and repurchase shares is subject to certain considerations.

Dividends are authorized and determined by our Board of Directors in its sole discretion and depend upon a

number of factors, including:

●

Cash available for distribution.

●

Our results of operations and anticipated future results of operations.

●

Our financial condition, especially in relation to the anticipated future capital needs of our properties.

●

The level of distributions paid by comparable companies.

●

Our operating expenses.

●

Other factors our Board of Directors deems relevant.

We expect to continue to pay quarterly dividends to our stockholders; however, our Board of Directors may

reduce our dividend or cease declaring dividends at any time, including if it determines that our net cash

provided by operating activities, after deducting capital expenditures and investments, are not sufficient to pay

our desired levels of dividends to our stockholders or to pay dividends to our stockholders at all.

22

Additionally, as of December 31, 2019, $5.4 billion of repurchase authority remained of the $15 billion share

repurchase program our Board of Directors had authorized. In February, 2020, our Board of Directors

approved an increase to our repurchase authorization from $15 billion to $25 billion, to support our plan for

future share repurchases. Our share repurchase program does not obligate us to acquire a specific number of

shares during any period, and our decision to commence, discontinue or resume repurchases in any period will

depend on the same factors that our Board of Directors may consider when declaring dividends, among others.

Any downward revision in the amount of dividends we pay to stockholders or the number of shares we

purchase under our share repurchase program could have an adverse effect on the market price of our common

stock.

We may need additional capital in the future, and it may not be available on acceptable terms.

We have historically relied primarily upon cash generated by our operations to fund our operations and

strategy; however, we have also relied from time to time on access to the debt and equity capital markets for

funding. There can be no assurance that additional debt or equity financing will be available in the future on

acceptable terms, or at all. In addition, although we anticipate we will be able to repay our existing

indebtedness when it matures or in accordance with our stated plans, there can be no assurance we will be able

to do so. Our ability to obtain additional financing, or refinance our existing indebtedness when it matures or

in accordance with our plans, will be subject to a number of factors, including market conditions, our operating

performance, investor sentiment and our ability to incur additional debt in compliance with agreements

governing our then-outstanding debt. If we are unable to generate sufficient funds from operations or raise

additional capital for any reason, our business could be adversely affected.

In addition, we are regularly evaluated by the major rating agencies based on a number of factors, including

our financial strength and conditions affecting the oil and gas industry generally. We and other industry

companies have had their ratings reduced in the past due to negative commodity price outlooks. Any

downgrade in our credit rating or announcement that our credit rating is under review for possible downgrade

could increase the cost associated with any additional indebtedness we incur.

Our business may be adversely affected by deterioration in the credit quality of, or defaults under our

contracts with, third parties with whom we do business.

The operation of our business requires us to engage in transactions with numerous counterparties operating in a

variety of industries, including other companies operating in the oil and gas industry. These counterparties

may default on their obligations to us as a result of operational failures or a lack of liquidity, or for other

reasons, including bankruptcy. Market speculation about the credit quality of these counterparties, or their

ability to continue performing on their existing obligations, may also exacerbate any operational difficulties or

liquidity issues they are experiencing, particularly as it relates to other companies in the oil and gas industry as

a result of the volatility in commodity prices. Any default by any of our counterparties may result in our

inability to perform our obligations under agreements we have made with third parties or may otherwise

adversely affect our business or results of operations. In addition, our rights against any of our counterparties

as a result of a default may not be adequate to compensate us for the resulting harm caused or may not be

enforceable at all in some circumstances. We may also be forced to incur additional costs as we attempt to

enforce any rights we have against a defaulting counterparty, which could further adversely impact our results

of operations.

In particular, in August 2018, we entered into a settlement agreement with Petróleos de Venezuela, S.A.

(PDVSA) providing for the payment of approximately $2 billion over a five-year period in connection with an

arbitration award issued by the International Chamber of Commerce (ICC) Tribunal in favor of ConocoPhillips

on a contractual dispute arising from Venezuela’s expropriation of our interests in the Petrozuata and Hamaca

heavy oil ventures and other pre-expropriation fiscal measures. We collected approximately $0.8 billion of the

$2.0 billion settlement in 2018 and 2019. PDVSA has defaulted on its remaining payment obligations under