UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

(Mark One)

|

|

|

þ

|

ANNUAL REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

FOR THE FISCAL YEAR ENDED: DECEMBER 31, 2013

|

|

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from _____________ to _____________

Commission File Number: 0-31198

TRIBUTE PHARMACEUTICALS CANADA INC.

(Exact name of registrant as specified in its charter)

|

Ontario, Canada

|

Not Applicable

|

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

(I.R.S. Employer Identification No.)

|

151 Steeles Avenue East, Milton, Ontario, Canada, L9T 1Y1

(Address of principal executive offices) (Zip Code)

(519) 434-1540

(Registrant's telephone number)

_______________________________________________________________

(Former Name, Former Address and Former Fiscal Year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to section 12(g) of the Act: Common Shares, no par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 (the "Exchange Act") during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes o No þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer o

|

Accelerated filer o

|

Non-accelerated filer o

(Do not check if a smaller reporting company)

|

Smaller reporting company þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates was US$8,261,917, computed by reference to the closing price of the common stock on June 30, 2013. For purposes of the above statement only, all directors, executive officers and 10% shareholders are assumed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for any other purpose.

As of March 14, 2014 the registrant had 51,581,238 shares of Common Stock outstanding.

FORM 10-K

TABLE OF CONTENTS

| 4 | |||||

| 17 | |||||

| 29 | |||||

| 29 | |||||

| 29 | |||||

| 29 | |||||

| 30 | |||||

| 32 | |||||

| 32 | |||||

| 39 | |||||

| 39 | |||||

| 39 | |||||

| 39 | |||||

| 40 | |||||

| 41 | |||||

| 45 | |||||

| 52 | |||||

| 54 | |||||

| 55 | |||||

| 56 | |||||

| 60 | |||||

General

In this annual report, “we”, “us”, “our”, “Tribute” and the “Company” refer to Tribute Pharmaceuticals Canada Inc., an Ontario, Canada corporation. All dollar amounts in this annual report are stated in Canadian Dollars unless stated otherwise. Certain terms used in this annual report are defined below in the section entitled “Glossary”. NeoVisc®, Uracyst® and Uropol® are trademarks owned by Tribute and are the subject of trademark registrations in certain jurisdictions. References to other products in this annual report are owned by third parties and certain of such other products have been trademarked and are the subject of trademark registrations in certain jurisdictions.

Forward-Looking Statements

This Report on Form 10-K for Tribute Pharmaceuticals Canada Inc. may contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Such forward-looking statements are characterized by future or conditional verbs such as "may," "will," "expect," "intend," "anticipate," believe," "estimate" and "continue" or similar words. You should read statements that contain these words carefully because they discuss future expectations and plans, which contain projections of future results of operations or financial condition or state other forward-looking information. Such statements are only predictions and our actual results may differ materially from those anticipated in these forward-looking statements. We believe that it is important to communicate future expectations to investors. However, there may be events in the future that we are not able to accurately predict or control. Factors that may cause such differences include, but are not limited to, those discussed under Item 1A. Risk Factors and elsewhere in this Form 10-K for the year ended December 31, 2013, as filed with the Securities and Exchange Commission, including the uncertainties associated with product development, the risk that we will not obtain approval to market our products, the risks associated with dependence upon key personnel and the need for additional financing. We do not assume any obligation to update forward-looking statements as circumstances change.

Exchange Rate for Canadian Dollar

The accounts for Tribute are maintained in Canadian dollars which is the Company’s functional currency. All dollar amounts contained herein are expressed in Canadian dollars, except as otherwise indicated. As at March 14, 2013, the exchange rate for Canadian dollars/United States dollars was $1.00 (Cdn.) = $0.9020 (U.S.).

Set forth below are the exchange rates based on the Bank of Canada noon rates for the Canadian dollar equivalent expressed in United States currency during 2013 and 2012.

|

Years ended December 31,

|

||||||||

|

2013

|

2012

|

|||||||

|

At End of Year

|

0.9402 | 1.0051 | ||||||

|

Average

|

0.9710 | 0.9995 | ||||||

|

High

|

1.0164 | 1.0285 | ||||||

|

Low

|

0.9348 | 0.9599 | ||||||

OVERVIEW

Tribute Pharmaceuticals Canada Inc. is an emerging Canadian specialty pharmaceutical company engaged in the acquisition, licensing, development and promotion of healthcare products in the Canadian and U.S. markets. The Company targets several therapeutic areas in Canada with a particular interest in products for the treatment of neurology, pain, urology, dermatology and endocrinology/cardiology.

Tribute’s current portfolio consists of six marketed products in Canada, including: NeoVisc® and NeoVisc® Single Dose, Uracyst®, Bezalip® SR, Soriatane®, Cambia® and Collatamp G. NeoVisc and Uracyst are also sold in several countries globally through strategic partners of the Company. Tribute also has an exclusive license for the development and commercialization of Bezalip SR (bezafibrate) for the U.S. market.

Tribute markets its products in Canada through its own sales force and currently has licensing agreements for the distribution of NeoVisc and Uracyst in over 20 countries, and continues to expand this footprint. The Company’s focus on business development is twofold: utilizing in-licensing and out-licensing for immediate impact on its revenue stream, as well as product development for future growth and stability.

Tribute’s management team has a strong track record in senior management positions from companies such as Wyeth, Syntex/Roche, Astra-Zeneca, Amgen, Bayer, Novartis and Biovail. The team has extensive operational and business development experience with the Canadian market.

The Company was incorporated under the Business Corporations Act (Ontario) on November 14, 1994 under the name “Stellar International Inc.” On January 1, 2005 the Company changed its name from Stellar International Inc. to Stellar Pharmaceuticals Inc. and on January 1, 2013 the Company changed its name from Stellar Pharmaceuticals Inc. to Tribute Pharmaceuticals Canada Inc. On December 1, 2011, Stellar Pharmaceuticals Inc. acquired 100% of the outstanding shares of the then privately held Tribute Pharmaceuticals Canada Ltd. and Tribute Pharma Canada Inc.. The Company maintains two facilities including its head office located at 151 Steeles Ave. East, Milton, Ontario, Canada L9T 1Y1 and the Company’s operations facility at 544 Egerton Street, London, Ontario, Canada N5W 3Z8. The Company’s telephone number is (519) 434-1540, its facsimile number is (519) 434-4382 and its e-mail address is info@tributepharma.com.

2013 Highlights

In February 2013, Cambia was officially launched by the Company to primary care physicians in Canada. Cambia is also commercially available in the United States and marketed by Tribute’s licensor, Depomed, Inc. Cambia was first introduced in the United States in June of 2010. Depomed acquired the North American rights to Cambia from Nautilus Neurosciences in December 2013.

The prescription market for migraine medications in Canada is valued at more than $140 million dollars annually based on IMS data.

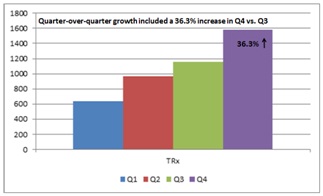

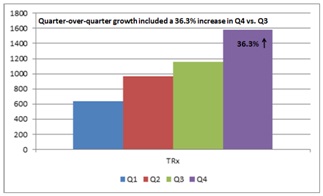

During the first year of commercial launch, Cambia has achieved quarter-over-quarter growth throughout 2013 including a 36.3% increase in total prescriptions written Q4 versus Q3 as illustrated below in Table 1. Furthermore, Cambia has obtained coverage of many private insurance payor open plans in Canada. Cambia is now widely available to Canadian patients.

Table 1 – Total Prescriptions for Cambia in 2013 by Quarter

Source: IMS

In 2013 we continued to expand our Canadian sales force, which enabled us to increase our revenues over 2012 levels. We are actively looking to add more products to our domestic sales portfolio in Canada, which will be supported by our expanded sales force. We are also looking for further growth from our internally developed proprietary products NeoVisc and Uracyst in countries where we do not yet have distribution agreements.

On September 27, 2013 an Investigational New Drug application ("IND") was submitted to the U.S. Food and Drug Administration ("FDA") setting out the proposed development program for Bezalip SR (bezafibrate) tablets in patients with severe hypertriglyceridemia (SHTG). This IND was cleared by the FDA on November 11, 2013. Bezalip SR is a well‐established medicine used to treat cholesterol and triglycerides and has been approved in over 40 countries globally. Tribute's development program has been based on guidance provided by the FDA during the end of a Phase II meeting held in March 2012. The Company intends to submit a Special Protocol Assessment to the FDA at its earliest convenience that incorporates all substantial scientific issues currently available to establish safety and efficacy as part of the development program. As part of the IND clearance for Bezalip SR, Tribute has initiated partnering activities related to securing a development and commercialization partner for Bezalip SR in the US. In March 2014, the Company entered into an agreement with JSB-Partners ("JSB"), a global life sciences advisor, to support Tribute in finding a co-development and commercial partner for the Company’s Bezalip SR (bezafibrate) in the U.S.

On August 8, 2013, SWK Funding LLC ("SWK"), a wholly-owned subsidiary of SWK Holdings Corporation entered into a credit agreement (the "Credit Agreement") pursuant to which the lenders party thereto provided to Tribute a term loan in the principal amount of US$6,000,000 (the "Loan") which may be increased by an additional US$2,000,000 at the Company's request on or before December 31, 2014. In connection with this loan, Tribute exercised its rights under its loan and security agreement with MidCap to prepay the outstanding balance of the Company’s term loan with MidCap. On February 4, 2014, pursuant to the terms of the Credit Agreement, SWK advanced the Company the remaining US$2,000,000 in available funds. All terms under the Credit Agreement apply to the additional loan.

Products

Approved & Marketed Products

Cambia®

Cambia (diclofenac potassium for oral solution) was licensed from Nautilus Neurosciences, Inc. (“Nautilus”) in November 2010. Cambia was approved by the FDA in June 2009 and is currently marketed by Depomed in the US. Cambia was approved by Health Canada in March 2012 and was commercially launched to specialists in Canada in October 2012 and broadly to all primary care physicians in February 2013. The market for prescription migraine products in Canada is valued at approximately $140 million dollars based on IMS data.

Cambia is a non-steroidal anti-inflammatory drug (NSAID) and the only prescription NSAID available and approved for the acute treatment of migraine attacks with or without aura in adults 18 years of age or older. Cambia is available as an oral solution in individual sachets each designed to deliver a 50mg dose when mixed in water. According to the 2011 U.S. guidelines published by the International Headache Society, Cambia is the only approved prescription NSAID available that was studied and proven to be an effective treatment for migraine that reached statistically significant results for all four co-primary endpoints including: pain free response at two hours; nausea free; photophobia free (sensitivity to light); and phonophobia free (sensitivity to sound). In addition, Cambia provides fast migraine pain relief within 30 minutes of dosing due in part to the significant benefits of the proprietary Dynamic Buffering TechnologyTM (“DBT”). DBT provides for enhanced drug absorption and bioavailability. In fasting volunteers, measurable plasma levels were observed within five minutes of dosing with Cambia. Peak plasma levels were achieved at approximately 15 minutes, with a range of approximately 10 to 40 minutes. The use of some NSAIDs has been associated with an increased incidence of cardiovascular adverse events such as myocardial infarction, stroke or thrombotic events. The risk may increase with duration of use and patients should only take this medication as prescribed by a physician.

Migraine Treatment Options: There are a number of different treatment options for migraine in Canada. Acute migraine treatment options can be broken down to three main categories: (i) triptans or 5-HT1 receptor agonists (e.g. sumatriptan, rizatriptan); (ii) ergot alkaloids (e.g. ergotamine, dihydroergotamine); and (iii) NSAIDs (Cambia). Triptans may cause dizziness, nausea, weakness and chest discomfort and should not be used by patients with heart disease, uncontrolled high blood pressure, blood vessel disease or who have a history of stroke. Ergots may cause chest pain, tingling or burning sensations, nausea, vomiting, and cramps. Furthermore, ergots may reduce blood flow to the extremities (hands and feet) and may lead to tissue damage. Ergots should also not be used by anyone with heart disease, uncontrolled high blood pressure or blood vessel disease. NSAIDs such as Cambia may increase the incidence of cardiovascular adverse events such as myocardial infarction, stroke or thrombotic events, gastrointestinal adverse events such as peptic/duodenal ulceration, perforation and gastrointestinal bleeding and are contraindicated in the third trimester of pregnancy.

In September of 2013 the Canadian Neurological Sciences Federations issued revised Canadian Headache Society Guidelines for Acute Drug Therapy for Migraine Headaches through the Canadian Journal of Neurological Sciences. Cambia (diclofenac potassium for oral solution) was acknowledged as potential first line therapy, fast onset of action and having a strong recommendation, high quality evidence and recommended for the acute treatment of migraine.

Migraine in Canada: The annual prescription migraine market in Canada is valued at approximately $140 million dollars. Management estimates that four million women and one million men suffer from migraine headaches in Canada and that 60 percent of those with migraine have one or more attacks per month while 25 percent of those with migraine have at least one attack per week. One Canadian study found that those with migraine lose 6.5 days of work each year resulting from their migraine. According to a study conducted by Pryse Phillip, et al, published by the Canadian Journal of Neurological Sciences in 1992, they estimate that 7,000,000 working days are lost annually in Canada due to migraine and that direct and indirect cost in the workplace due to migraine is estimated at $500 million annually. It was also found that 48 percent of all women suffering from migraine have never consulted a physician for their headaches.

Competitive Analysis: It is estimated that half of all people suffering from migraine in Canada never seek help from a physician but rather self-treat their condition with over-the-counter (“OTC”) medications such as aspirin (Bayer®), acetaminophen (Tylenol®) and OTC NSAID’s such as ibuprofen (Advil®) and naproxen sodium (Aleve®). The main prescription pharmacological agents used to treat acute migraine includes the triptan class of drugs or 5-HT1 receptor agonists as they are known and these products include sumatriptan (Imitrex®), rizatriptan (Maxalt®), zolmitriptan (Zomig®), almotriptan (Axert®), naratriptan (Amerge®), eletriptan (Relpax*) and frovatriptan (Frova®). There are also the ergot alkaloids such as ergotamine (Cafergot®) and dihydroergotamine (Migrinal®) used in some cases as are narcotics such as meperidine (Demerol) and the combination drug of aspirin, butalbital, and caffeine (Fiorinal®). In spite of a number of possible treatment options for treating migraines, many of these treatments are without a formal indication from Health Canada. The Company considers the competitive market as the triptans class, which currently sells approximately $140 million annually in Canada.

Bezalip® SR

Bezalip SR (bezafibrate) is a well-established pan-peroxisome proliferator-activated receptor (pan-PPAR) activator. Bezalip SR, used to treat hyperlipidemia, has over 25 years of therapeutic use globally with a good safety profile. Bezalip SR helps lower low-density lipoprotein cholesterol (LDL-C) and triglycerides while raising high-density lipoprotein cholesterol (HDL-C) levels. It also improves insulin sensitivity and reduces blood glucose levels, which in combination with the cholesterol effects may significantly lower the incidence of cardiovascular events and development of diabetes in patients with features of metabolic syndrome. Bezalip SR is under license from Actavis Group PTC ehf and is sold exclusively in Canada by Tribute. Tribute also has the exclusive development and licensing rights to Bezalip SR in the U.S. and recently filed an IND that received clearance from the FDA in the US. The initial target indication being pursued in the U.S. is for severe hypertriglyceridemia. Bezalip SR is contraindicated in patients with hepatic and renal impairment, pre-existing gallbladder disease, hypersensitivity to bezafibrate, or pregnancy or lactation.

Bezalip SR is currently approved in more than 40 countries worldwide. According to third party data from IMS, the U.S. fibrate market is estimated at nearly $2.5 billion dollars in 2013. Upon approval, should such an approval be obtained, Tribute would enjoy a five year market exclusivity period from the FDA extended to all new chemical entities.

Hyperlipidemia Treatment Options: Hyperlipidemia, or high cholesterol, is a very common chronic condition and is characterized by an excess of fatty substances called lipids, mainly cholesterol and triglycerides, in the blood. It is also called hyperlipoproteinemia because these fatty substances travel in the blood attached to proteins. This is the only way that these fatty substances can remain dissolved while in circulation. Hyperlipidemia, in general, can be divided into two subcategories:

|

●

|

Hypercholesterolemia, in which there is a high level of cholesterol; and

|

|

●

|

Hypertriglyceridemia, in which there is a high level of triglycerides, the most common form of fat.

|

Competitive Analysis: Cholesterol-lowering drugs in Canada include: statins, niacin, bile-acid resins, fibric acid derivatives (fibrates), and cholesterol absorption inhibitors. All classes of cholesterol-lowering medicines are most effective when combined with increased exercise and a low-fat, high-fiber diet. The statin class includes some of the largest-selling prescription products in the world (Lipitor®, Zocor®, Crestor®, etc.). Statins dominate single-agent prescribing for the treatment of lipid disorders. The niacin (nicotinic acid – vitamin B3) class includes brands such as Niaspan®, which work primarily on increasing HDL cholesterol. The fibrates class of cholesterol lowering treatments, and is composed of three competing molecules: gemfibrozil (Lopid®), bezafibrate (Bezalip SR), and fenofibrate (Lipidil® in Canada or Tricor® in the U.S.). Clinical studies have demonstrated that bezafibrate, the active ingredient in Bezalip SR was shown to be very effective in lowering high levels of triglycerides, raising HDL cholesterol and lowering LDL cholesterol. As of the end of 2013, IMS estimates the annual fibrate market in Canada to be approximately $50 million.

Soriatane®

Soriatane is chemically known as acitretin, and is indicated for the treatment of severe psoriasis (including erythrodermic and pustular types) and other disorders of keratinization. Soriatane is a retinoid, an aromatic analog of vitamin A.

Soriatane was approved in Canada in 1994 and is the first and only oral retinoid indicated for psoriasis. Soriatane is often used when milder forms of psoriasis treatments like topical steroids, emollients and topical tar-based therapies have failed.

Soriatane should be reserved for patients unresponsive to, or intolerant of standard treatment. In addition, Soriatane should only be prescribed by physicians knowledgeable in the use of systemic retinoids. Soriatane is teratogenic (can cause birth defects) and should not be used by women who are pregnant or who are planning to become pregnant during or within three years after stopping treatment of Soriatane.

Psoriasis Treatment Options: There are a number of different treatment options for psoriasis. Typically, topical agents are used for mild disease, phototherapy for moderate disease and oral systemic agents and biologicals for more severe disease.

The three main traditional systemic treatments are methotrexate, cyclosporine and Soriatane. Unlike Soriatane, methotrexate and cyclosporine are immunosuppressant drugs. Methotrexate may cause a decrease in the number of blood cells made by bone marrow, may cause liver damage, lung damage, damage to the lining of the mouth, stomach or intestines and may increase the risk of developing lymphoma (cancer that begins in the cells of the immune system), among other serious side effects. Methotrexate may also cause serious or life-threatening skin reactions. Cyclosporines may cause side effects that could be very serious, such as high blood pressure and kidney and liver problems. It may also reduce the body's ability to fight infections.

Competitive Analysis: Severe psoriasis is a condition that involves more than 10% of the body area or is physically, occupationally or psychologically disabling. Soriatane will typically be used in combination with other drugs such as topical steroids, emollients or tar-based therapies. Soriatane is most effective for treating psoriasis when it is used with phototherapy. Soriatane is sometimes used with the biologic agents such as etanercept (Enbrel®), adalimumab (Humira®) or infliximab (Remicade®) and may also be prescribed in rotation with cyclosporine or methotrexate. Biologic therapies such as Enbrel® Humira® and Remicade® are effective in treating severe forms of the disease, but are very expensive and sometimes not reimbursed by government or other private drug plans. Cyclosporine and methotrexate are also oral agents that are often used for severe forms of psoriasis. The market for moderate to severe psoriasis in Canada is estimated by management to be greater than $200 million dollars for 2013.

Collatamp G®

Tribute acquired the exclusive Canadian licensing rights for Collatamp G (restorable gentamicin-collagen haemostat) from Theramed Corporation in June 2012. EUSA Pharma ("EUSA") owns the worldwide rights (except US) to Collatamp G and licensed the product to Theramed in 2008. Collatamp G, approved by Health Canada on August 1, 2007 and launched in Canada in 2008, is a fully resorbable gentamicin-collagen haemostat, used as a surgical implant for haemostasis and local delivery of high doses of gentamicin. The market in which Collatamp G competes in Canada is estimated at $20 million dollars based on best estimates from management.

Collatamp G is indicated for the local haemostasis of capillary, parenchymatous and seeping haemorrhages in areas with a high risk of infection and has been shown to reduce post-operative infections across a range of surgical disciplines, including a reduction of 53% in a large randomized controlled study in cardiac surgery. Based on internal data, Collatamp G is currently used in over 100 hospitals and surgical centers across Canada and is approved or used in over 50 countries throughout the world.

Collatamp G contains gentamicin sulphate at a locally effective dose and has been shown to be efficacious in the treatment and prevention of post-operative acquired infection across many surgical interventions including: cardiac surgery, gastro-intestinal surgery, vascular surgery and orthopaedic surgery.

Collatamp G is a unique product within the surgical field as it is the only product in Canada which combines a hemostatic device with a locally acting antibiotic.

Competitive Analysis: There are a number of haemostatic agents on the market in Canada and gentamycin is available as an intravenous drug but Collatamp G is unique in that it combines a haemostat with the antibiotic gentamycin in a topical, collagen matrix.

NeoVisc® and NeoVisc® Single Dose

NeoVisc, is a proprietary product, developed by the Company and is used for the temporary replacement of synovial fluid in osteoarthritic joints. It is available as a triple-dosed, 2 mL pre-filled syringe of sterile 1.0% sodium hyaluronate solution and a single dose 6 mL pre-filled syringe of sterile 1.0% sodium hyaluronate solution. NeoVisc is classified in Canada by the Therapeutic Products Directorate (“TPD”) as a “medical device” under the Medical Devices Regulations of the Food and Drugs Act (Canada). NeoVisc is administered by intra-articular injection, by injecting the product directly into the affected joint and may be administered either as a single 6 mL injection or three 2 mL injections given over a two week period. Injections are typically repeated every 6 to 8 months thereafter and dependent on the patients response. The market for NeoVisc in Canada is estimated at $25 million dollars based on management estimates.

This type of treatment, referred to as viscosupplementation, is a well-established treatment for osteoarthritis of the knee, having gained Canadian approval in 1992 and United States approval in 1997. Viscosupplementation has also been used since the mid-1980s in many European markets. Replacing or supplementing the joint fluid provides symptomatic relief from the pain of osteoarthritis of the knee for up to 4 to 12 months before repeated injections are required. In late 2003, the first single dose product was launched in Canada and by 2009 there were four single dose therapies available in the Canadian market, including NeoVisc single dose. Single dose products like NeoVisc offer convenience of a single injection but the clinical effect typically is shorter in duration than the triple dose administration.

Osteoarthritis and Treatment Options: Osteoarthritis (“OA”) is the most common form of chronic arthritis worldwide and is a key cause of pain and disability in older adults. According to the Arthritis Society of Canada, OA affects about 10% of the adult population. OA of the knee, about twice as common as OA of the hip, is becoming an increasingly important condition with the aging population. OA risk factors include injury, prior joint inflammation, abnormalities of joint shape, and obesity. OA is a degenerative and sometimes painful disease that is associated with long term wear on weight-bearing joints. The market for OA is expected to grow significantly in future years as the average age of the population increases.

Current OA strategies and treatment goals include:

1. Patient education

2. Physical therapy

3. Over the Counter (“OTC”) analgesics

4. Non-steroidal anti-inflammatory drugs (“NSAID”), such as diclofenac, naproxen and COX2 inhibitors such as Celebrex®

5. Intra-articular viscosupplements, such as NeoVisc

6. Intra-articular steroids – corticosteroids are also used to treat inflammation associated with OA

7. Opioids

8. Joint replacement – surgical replacement with artificial joints

Products such as NeoVisc provide a non-pharmacological option in obtaining symptomatic improvements by supplementing the synovial fluid in the affected joint. NeoVisc can also be used in conjunction with other treatment strategies like physical therapy, OTC medications and NSAIDs, and as a result may reduce the amount of medication required and potentially delay joint replacement.

Competitive Analysis: There are a number of competitive viscosupplements to NeoVisc in Canada for both NeoVisc and NeoVisc Single Dose, including Sanofi’s products Synvisc® and Synvisc® One. The competitive landscape in the United States and other international markets is now very similar to the Canadian market. NeoVisc is an effective, technically engineered, highly purified, high molecular weight linear format, free of any avian peptides and available in a single or triple dose presentation. Furthermore, NeoVisc is the only marketed viscosupplement manufactured and packaged in Canada and marketed by a Canadian company.

Uracyst® (Uropol®)

Uracyst, developed by the Company, is used in the treatment of certain forms of interstitial cystitis (“IC”) and non-common cystitis. Uracyst is a sterile 2.0% sodium chondroitin sulfate solution available in a 20 mL vial. This product is instilled by catheter directly into a patient’s bladder. According to the Global Data: Interstitial Cystitis Therapeutics – Pipeline Assessment and Market Forecasts to 2019, the global interstitial market size is estimated to be valued at approximately US$150 million dollars.

Uracyst provides symptomatic relief for patients suffering from glycosaminoglycan (“GAG”) deficient cystitis such as IC and non-common cystitis (including radiation-induced cystitis and hemorrhagic cystitis) by supplementing and replenishing deficiencies in the glycosaminoglycan lining of the bladder wall. This GAG lining acts as a protective barrier between urine and the bladder wall. It protects the bladder wall against irritants and toxins (e.g., micro crystals, carcinogens and acid) in the urine and serves as an important defense mechanism against bacterial adherence. Many researchers believe that a large number of IC patients (over 70%) have “leaky” or deficient GAG layers in their bladder.

Uracyst is typically instilled weekly for six weeks, then once a month until symptoms resolve. Because these types of cystitis are typically chronic diseases of no known cause, patients will usually require re-treatment after a variable period of time when symptoms recur.

The Company has been issued a patent(s) for Uracyst in the United States, China, Japan, Australia and Canada and has international patents pending. Uracyst is classified in Canada by TPD as a medical device under the Medical Devices Regulations of the Food and Drugs Act (Canada).

Interstitial Cystitis and Treatment Options: Interstitial cystitis is a chronic inflammation of the bladder wall and is often associated with painful symptoms of the lower abdomen. Unlike common cystitis, IC is not caused by bacteria and does not respond to conventional antibiotic therapy. IC can affect people of any age, race or sex, but is more frequently diagnosed in women.

IC causes some or all of the following symptoms:

|

●

|

Frequency: Day and/or night frequency of urination (up to 60 times a day in severe cases). In early or very mild cases, frequency is sometimes the only symptom;

|

|

●

|

Urgency: Pain, pressure or spasms may also accompany the sensation of having to urinate immediately;

|

|

●

|

Pain: Can be abdominal, urethral or vaginal. Pain is also frequently associated with sexual intercourse; and

|

|

●

|

Other: Some patients also report experiencing symptoms such as muscle and joint pain, migraines, allergic reactions, colon and stomach problems, as well as the more common symptoms of IC described above.

|

At present, there is neither a cure for IC nor is there an effective treatment which works for everyone. The following treatments have been used to relieve the symptoms of IC in some people: (i) diet, (ii) bladder distention, (iii) instilled dimethyl sulfoxide (“DMSO”), heparin or hyaluronic acid, (iv) anti-inflammatory drugs, (v) antispasmodic drugs, (vi) antihistamines and (vii) muscle relaxants.

In severe cases, several types of surgery have been performed including bladder augmentation and urinary diversion. Products available for treating IC vary in their effectiveness. Most work for short periods of time and generally, are effective in about 30% to 40% of patients. Some therapies can take up to six months of active treatment before patients start to show symptomatic improvement.

Competitive Analysis: The treatment of IC is a relatively small niche market. Because of low efficacy rates and relatively expensive treatment costs for competitive products, management believes the treatment of IC remains an unsatisfied market with no dominant competitive product. Ortho McNeil Pharmaceutical, Inc. a competitor in the IC market has marketed Elmiron® (pentosan polysulfate sodium) in Canada since 1993. Elmiron® is used as an oral GAG replenishment therapy. Side effects reported from the use of Elmiron® include hair loss, diarrhea and mild to extreme gastrointestinal discomfort.

Development Strategy

Tribute is an emerging specialty pharmaceutical company engaged in the acquisition, licensing, development and promotion of healthcare products in the Canadian and U.S. markets. In addition to growing the business in Canada, the Company is also building revenues through out-licensing its current products to international markets and continues to explore new, life-cycle development opportunities for its proprietary products Uracyst and NeoVisc.

Tribute’s future product development efforts will be focused initially on developing strategic partners to assist Tribute in gaining regulatory approval in the U.S. and other key international markets for NeoVisc and Uracyst.

Tribute obtained FDA clearance for an IND related to Bezalip SR in October 2013. The fibrate market in which Bezalip SR will compete is estimated at approximately $2.5 billion annually in the U.S. and the Omega 3 fatty acid (fish oil) product category that are also used to treat SHTG are estimated to have annual sales in excess of $1.3 billion. The Company will explore all possibilities to obtain a market authorization for Bezalip SR in the US. In March 2014, the Company entered into an agreement with JSB-Partners ("JSB"), a global life sciences advisor, to support Tribute in finding a co-development and commercial partner for the Company's Bezalip® SR (bezafibrate) in the US.

Sales and Marketing

Tribute’s sales and marketing strategy is focused on the organic growth of existing marketed products through several key activities. First, our sales force ensures that it targets known prescribers of our medications or medications that compete with our products. We create demand by providing customers with reliable and trustworthy information from credible sources and by coordinating and facilitating continuing health education events in targeted areas. Second, we support our products by providing physicians and other healthcare practitioners with quality patient care materials. And third, we ensure that our products are easy to purchase through all major wholesalers and distributors in Canada and we manage our supply chain efficiently to ensure that we can always meet demand.

We consider our sales force to be very experienced and well trained. All of our representatives have experience from other pharmaceutical companies including many of the largest companies in the industry. Additionally, Tribute offers its representatives a competitive incentive plan based on the achievement of results.

Manufacturing

Tribute currently outsources the manufacturing of its proprietary products to special sterile facilities operated by third party contractors. These facilities are in compliance with applicable Health Canada, TPD division medical device guidelines and current Good Manufacturing Practice ("cGMP") regulations. The Company believes these facilities have sufficient excess capacity at present to meet the Company’s short and long term objectives. A significant interruption in the supply of any of the Company’s products could impair the successful marketing of such products.

Our licensed products are manufactured by authorized, third-party, contract manufacturing organizations in various places throughout the world. Our manufacturers are all cGMP compliant and approved fabricators of pharmaceutical or medical device products according to Health Canada.

During 2013 and 2012, the Company’s NeoVisc® product was manufactured at Therapure Biopharma Inc. in Mississauga, Ontario, Canada and Uracyst® was manufactured by Jubilant HollisterStier, Inc. (formerly Draxis Pharma, Inc.) in Kirkland, Quebec, Canada. Bezalip® SR and Soriatane® are provided by Tribute’s licensor, Actavis. Under the terms of these agreements the Company is obligated to make payments for batches to be manufactured within the one year termination notification period.

The manufacture of the Company’s products involves the handling and use of substances that are subject to various environmental laws and regulations that impose limitations on the discharge of pollutants into the soil, air and water, and establish standards for their storage and disposal. The Company believes that the manufacturers of its products are in material compliance with such environmental laws and regulations.

The sale and use of the Company’s products entails risk of product liability and the Company presently carries product liability insurance. There can be no assurance that, despite testing by the Company, as well as testing by regulatory agencies, defects will not be found in new products after commencement of commercial shipments. The occurrence of such defects could result in the loss of, or delay in, market acceptance of the Company’s products, which could have a material adverse effect on the Company. Furthermore, litigation, regardless of its outcome, could result in substantial costs to the Company, divert management’s attention and resources from the Company’s operations, and result in negative publicity that might impair the Company’s on-going marketing efforts.

Tribute is responsible for secondary packaging of its proprietary products at its London, Ontario facility. The Company’s licensed products are packaged by its third party contract manufactures.

The Company’s products are distributed in Canada by a third-party logistics provider, which provides warehousing, distribution, customer service and accounts receivable directly to the Company.

The Company, as a common practice for all of its products, maintains several months of inventory (including raw materials and finished goods) at any given time to mitigate against any risks of potential manufacturing disruptions. The Company did not experience any product disruptions of any significance in 2013.

The Industry

The pharmaceutical industry is highly competitive and is characterized by rapidly changing technology. Tribute believes that competition in its markets is based on, among other things, product safety, efficacy, convenience of dosing, reliability, availability and price. The market is dominated by a small number of highly-concentrated global competitors, many of which boast substantially greater resources than the Company. Given the size and scope of the competition, there can be no assurance that the Company will maintain or grow its current market position in its therapeutic areas, or that developments by others will not render the Company’s products or technologies non-competitive or obsolete. Also, many current and potential competitors of the Company may have greater name and brand recognition, or may enjoy more extensive customer relationships that could be leveraged to gain market share to the Company’s detriment. Although the Company is unaware of any competitors who may be able to complete the regulatory approval process more rapidly than the Company, and therefore may achieve market entry ahead of the Company’s products.

In order to maintain and improve its position in the industry, the Company is dedicated to enhancing its current products, developing or acquiring new products and product extensions, and implementing a comprehensive domestic and international sales and distribution marketing strategy. If the Company is not able to compete effectively against current and future competitors, such failure may result in fewer customer orders, reduced gross margins and profitability and loss of market share, any of which would materially adversely affect the Company.

Competition

Tribute faces product competition from companies marketing competing pharmaceutical products and medical devices in Canada and potentially on new products that could be launched in the future. The introduction of generic products of Tribute’s products as well as lower priced, similar competing products could have a profound impact on the Company’s existing business.

Competitive Strengths

Management believes that Tribute maintains a high level of competitive advantage within its chosen therapeutic areas over other Canadian companies or multi-national subsidiaries seeking to license or acquire products in Canada. These include:

|

●

|

A well trained and skilled sales force and employees;

|

|

●

|

Expertise in marketing new and existing products;

|

|

●

|

Its ability to obtain regulatory approvals for new and existing products in Canada and abroad;

|

|

●

|

Expertise in business development including sourcing, evaluation, negotiation and ability to complete business transactions to acquire or license new products for Canada;

|

|

●

|

The ability to offer cost-effective pricing while maintaining acceptable gross profit margins with many of its products;

|

|

●

|

The implementation and development of lifecycle management strategies;

|

|

●

|

Clear and defendable patents for certain of its products; and

|

|

●

|

The ability to obtain reasonable reimbursement and good pricing in Canada

|

REGULATORY, QUALITY ASSURANCES, SAFETY AND MEDICAL INFORMATION

Tribute currently utilizes a combination of internal and outsourced resources to address all of its quality assurance, regulatory affairs, pharmacovigilance and medical information needs. Tribute’s London, Ontario facility maintains a Health Canada Drug Establishment License and is ISO 13485 approved. The Company remains compliant with all regulatory guidelines and reporting obligations.

Canadian Regulatory Overview

The Canadian Therapeutic Products Directorate (“TPD”) is the Canadian federal authority that regulates, evaluates and monitors the safety, effectiveness, and quality of drugs, medical devices, biologics and other therapeutic products available to Canadians. The TPD is part of Health Canada. The TPD’s regulatory process for review, approval and regulatory oversight of products is similar to the regulatory process conducted by the Food and Drug Administration (“FDA”) in the United States.

Prior to being given market authorization for a product, a manufacturer must present substantive scientific evidence of a product’s safety, efficacy and quality as required by the Food and Drugs Act (Canada) and associated regulations. This information is submitted in the form of a New Drug Submission (“NDS”) in Canada.

The TPD performs a thorough review of the submitted information, sometimes using external consultants and advisory committees, to evaluate the potential benefits and risks of a drug. If, at the completion of the review, the conclusion is that the patient benefits outweigh the risks associated with the drug, the drug is issued a Notice of Compliance (“NOC”) and a Drug Identification Number (“DIN”), which permits the manufacturer to market the drug in Canada.

Currently, the process for the review of a drug typically takes an average of one to two years from the time that a manufacturer submits an NDS until the TPD approves a drug. The average time to approval varies but on average takes about fifteen to eighteen months.

All establishments engaged in the fabrication, packaging/labeling, importation, distribution, wholesale and operation of a testing laboratory relating to drugs are required to hold a Drug Establishment License unless expressly exempted under the Food and Drugs Regulations. The basis for the issuance of an Establishment License is compliance with current GMP as determined by inspection. Foreign sites whose products are being imported into Canada are also required to demonstrate GMP compliance.

Regulatory obligations and oversight continue following the initial market approval. The manufacturer must report any new information received concerning serious side effects, including the failure of a drug to produce the desired effect. The manufacturer must also notify the TPD of any new safety issues that it becomes aware of after the launch of a product.

Canadian Reimbursement Overview

After regulatory approval is received for a prescription drug, it can be sold to the public in accordance with prescription pharmaceutical regulations. Revenues are generated from prescription drug sales in Canada through one of three sources:

|

●

|

Cash: Patients will pay “out of pocket” at their sole expense. It is estimated that 10% of all prescription dollars spent in Canada come from cash purchases.

|

|

●

|

Private Insurance: Approximately 45% of prescription dollars spent in Canada is reimbursed via third-party private insurers, under plans generally provided by patients’ employers. Patients may be reimbursed a percentage of the cost of covered drugs minus deductibles or co-pays. The availability for reimbursement of drugs varies according to the type of reimbursement plan designed by the insurance company. There are a number of private insurers operating in Canada that provide employee plans to private and public sector employers.

|

|

●

|

Government Drug Plans: Government drug plans cover the cost of nearly 45% of prescription dollars spent in Canada, and generally serve patients over the age of 65 or patients for whom the cost of medications represents a significant financial burden such as families receiving social assistance. Each provincial government pays the cost of drugs that are listed on their own provincial formulary.

|

After regulatory approval of a drug is granted, approval for reimbursement is typically sought from provincial governments and private insurance companies. Until provincial and private reimbursement is approved, the product is sold only via cash purchases. Decisions to list drugs for reimbursement on private and government formularies vary widely depending on the drug, indications, competitive products and price.

Hospital products or products dispensed in the hospital are treated differently in Canada. All medications taken while in a hospital are fully reimbursed by the provincial governments. If a patient leaves the hospital and is prescribed a drug to be taken at home, this prescription product would be reimbursed either by cash, private insurance or public insurance plans.

Common Drug Review (CDR)

The CDR was implemented in 2003 to provide formulary listing recommendations for new drugs to participating publicly-funded federal, provincial and territorial drug benefit plans in Canada.

The CDR consists of:

|

●

|

A systematic review of the available clinical evidence and a review of the pharmacoeconomic data for the drug; and

|

|

●

|

A listing recommendation made by the Canadian Expert Drug Advisory Committee.

|

Based on the targeted timeframes of the CDR, a review should be completed approximately 20 to 26 weeks following receipt of a manufacturer’s submission, after which recommendations are made to participating drug plans.

At the provincial and territorial level, products are reviewed on the basis of their cost-effectiveness, comparable utility to other similar products, projected utilization and cost implications to the publicly-funded drug budget. Each submission is reviewed but there is wide variance in the formulary decisions and the time taken to make such decisions. Provinces and territories may utilize the recommendations of the CDR or perform their own analysis.

Presently, all provinces and territories except Quebec use the CDR recommendations in their assessment, but make their formulary decisions independently from the CDR. In many provinces, the formulary committee may grant “restricted or limited use approvals” for a drug as a means of regulating the size of the patient population eligible for reimbursement for the cost of the drug and by encouraging physicians to use older generation products first before prescribing newer, sometimes more costly medications.

Patent and Proprietary Protection

We are able to protect our technology from unauthorized use by third parties only to the extent that it is covered by valid and enforceable patents or is effectively maintained as a trade secret or is protected by confidentiality agreements. Accordingly, patents or other proprietary rights are an essential element of our business.

The Company currently has patents issued for Uracyst that include a low dose patent in both the United States (Patent No. 6,083,933 –- issued 07/04/2000) and Canada (Patent No. 2,269,260 – issued 12/31/2002). In addition, the Company has approved patents for its high dose product in Australia (Patent No. AU 2004212650 – issued 11/05/2009), Canada (Patent No. 2515512 – issued 07/10/2012), China (Patent No. ZL200480006467.1 – issued 05/26/2010), the United States (Patent No. US 7772210 – issued 08/10/2010, Patent No. US 8084441 – issued 12/27/2011 and Patent No. 833`4276 – issued 12/18/2012), and Japan (Patent JP 4778888 – issued 07/08/2011). Jurisdictions with patents pending related to the high dose Uracyst include: the United States, Europe, India, and Israel. Uracyst is classified as a medical device in all countries in which it currently has approval. The Company currently has one pending United States patent application and three pending foreign patent applications covering Uracyst/Uropol high dose patents.

The Company also has rights to patents on Cambia through its licensing agreement with Depomed, Inc. (previously Nautilus Neuroscience) (Patent No. 2,254, 144) and there is also one patent pending for Cambia in Canada. In addition, the Company also has rights to a Canadian patent on Bezalip SR through its licensing agreement with Actavis.

While trade secret protection is an essential element of our business and we have taken security measures to protect our proprietary information and trade secrets, we cannot give assurance that our unpatented proprietary technology will afford us significant commercial protection. We seek to protect our trade secrets by entering into confidentiality agreements with third parties, employees and consultants. Our employees and consultants also sign agreements requiring that they assign to us their interests in intellectual property arising from their work for us. All employees sign an agreement not to engage in any conflicting employment or activity during their employment with us and not to disclose or misuse our confidential information. However, it is possible that these agreements may be breached or invalidated, and if so, there may not be an adequate corrective remedy available. Accordingly, we cannot ensure that employees, consultants or third parties will not breach the confidentiality provisions in our contracts, infringe or misappropriate our trade secrets and other proprietary rights or that measures we are taking to protect our proprietary rights will be adequate.

Where deemed appropriate, Tribute files patent applications for products or technologies which it owns or in respect of which it has acquired a license and, if necessary, then further developed to make such technologies marketable. Licensed products often include rights to the intellectual property (“IP”) of the licensor. Such applications may cover composition of matter, the production of active ingredients and their novel applications and may be filed globally or in select territories that the Company may intend to commercialize its products.

The Company retains independent patent counsel where appropriate. Management of the Company believes that the use of outside patent specialists ensures prompt filing of patent applications, as well as the ability to access specialists in various areas of patents and patent law to ensure complete patent filings.

The patent position relating to medical devices and drug development is uncertain and involves many complex legal, scientific and factual questions. While the Company intends to protect its valuable proprietary information and believes that certain of its information is novel and patentable, there can be no assurance that: (i) any patent application owned by, or licensed to, the Company will issue to patent in all or any countries; (ii) proceedings will not be commenced seeking to challenge the Company’s patent rights or that such challenges will not be successful; (iii) proceedings taken against a third party for infringement of patent rights will be successful; (iv) processes or products of the Company will not infringe upon the patents of third parties; or (v) the scope of patents issued to, or licensed by, the Company will successfully prevent third parties from developing similar and competitive products. The cost of litigation to uphold the validity and prevent infringement of the patents owned by, or licensed to, the Company may be significant.

Issues may arise with respect to claims of others to rights in the patents or patent applications owned by or licensed to the Company. As the industry expands and more patents are issued, the risk increases that the Company’s processes and products may give rise to claims that they infringe the patents of others. Actions could be brought against the Company or its commercial partners claiming damages or an accounting of profits and seeking to enjoin them from clinically testing, manufacturing and marketing the affected product or process. If any such action were successful, in addition to any potential liability for damages, the Company or its commercial partners could be required to obtain a license in order to continue to manufacture or market the affected product or use the affected process. There can be no assurance that the Company or its commercial partners could prevail in any such action or that any license required under any such patent would be made available or, if available, would be available on acceptable terms. If no license is available, the Company’s ability to commercialize its products may be negatively affected or withdrawn. There may be significant litigation in the industry regarding patents and other intellectual property rights and such litigation could consume substantial resources. If required, the Company may seek to negotiate licenses under competitive or blocking patents, which it believes are required for it to commercialize its products.

Although the scope of patent protection ultimately afforded by the patents and patent applications owned by or licensed to the Company is difficult to quantify, management of the Company believes that such patents will afford adequate protection for it to ensure exclusivity in the conduct of its business operations as described in this Form 10-K. The Company also intends to rely upon trade secrets, confidential and unpatented proprietary know-how, and continuing technological innovation to develop and maintain its competitive position. To protect these rights, the Company whenever possible requires all employees and consultants to enter into confidentiality agreements with the Company. There can be no assurance, however, that these agreements will provide meaningful protection for the Company’s trade secrets, know-how or other proprietary information in the event of any unauthorized use or disclosure. Further, in the absence of patent protection, the Company’s business may be adversely affected by competitors who independently develop substantially equivalent or superior technology.

The existence, scope and duration of patent protection vary among the Company’s products and among the different countries where the Company’s products may be sold. They may also change over the course of time as patents are granted or expire, or become extended, modified or revoked.

Pricing and Reimbursement

As pressures for cost containment increase, particularly in Canada, the United States and the European Union, there can be no assurance that the prices the Company can charge for its products will be as favorable as historical pharmaceutical product prices. Reimbursement by government, private insurance organizations, and other healthcare payers has become increasingly important, as has the listing of new products on large formularies, such as those of benefit providers and group buying organizations. The failure of one or more products to be included on formulary lists, or to be reimbursed by government or private insurance organizations, could have a negative impact on the Company’s results of operation and financial condition.

Product Pricing Regulation on Certain Patented Drug Products

Patented drug products in Canada are subjected to the regulation of the Patented Medicine Prices Review Board (“PMPRB”). The PMPRB’s objective is to ensure that prices of patented products in Canada are not excessive. For new patented products, the price in Canada is limited to either the cost of existing drugs sold in Canada or the median of prices for the same drug sold in other specified industrial countries. For existing patented products, prices cannot increase by more than the Consumer Price Index. The PMPRB monitors compliance through a review of the average transaction price of each patented drug product as reported by the Company over a recurring six-month reporting period.

The PMPRB does not approve prices for drug products in advance of their introduction to the market. The PMPRB provides guidelines from which companies like Tribute set their prices at the time they launch their products. All patented pharmaceutical products introduced in Canada are subject to the post-approval, post launch scrutiny of the PMPRB. Since the PMPRB does not pre-approve prices for a patented drug product in Canada, there may be risk involved in the determination of an allowable price selected for a patented drug product at the time of introduction to the market by the company launching such products in Canada. If the PMPRB does not agree with the pricing assumptions chosen by such company introducing a new drug product, the price chosen could be challenged by the PMPRB and, if it is determined that the price charged is excessive, the price of the product may be reduced and a fine may be levied against the company for any amount deemed to be in excess of the allowable price determined. Drug products that have no valid patents are not subject to review by the PMPRB.

License Agreements

On December 1, 2011, the Company acquired 100% of the outstanding shares of Tribute Pharmaceuticals Canada Ltd. and Tribute Pharma Canada Inc. Included in this transaction were the following license agreements:

On June 30, 2008, Tribute signed a Sales, Marketing and Distribution Agreement with Actavis Group PTC ehf (“Actavis”) to perform certain sales, marketing, distribution, finance and other general management services in Canada in connection with the importation, marketing, sales and distribution of Bezalip® SR and Soriatane® (the “Products”). On January 1, 2010, a first amendment was signed with Actavis to grant the Company the right and obligation to more actively market and promote the Products in Canada. On March 31, 2011, a second amendment was signed with Actavis that extended the term of the agreement, modified the terms of the agreement and increased the Company’s responsibilities to include the day-to-day management of regulatory affairs, pharmacovigilance and medical information relating to the Products. The Company pays Actavis a sales and distribution fee up to an annual base-line net sales forecast plus an incremental fee for incremental net sales above the base-line. On May 4, 2011, the Company signed a Product Development and Profit Share Agreement with Actavis to develop, obtain regulatory approval of and market Bezalip SR in the USA. The Company shall pay US$5,000,000 to Actavis within 30 days of receipt of the regulatory approval to market Bezalip SR in the USA.

On November 9, 2010, the Company signed a license agreement (the "License Agreement") with Nautilus Neurosciences, Inc. (“Nautilus”) for the exclusive rights to develop, register, promote, manufacture, use, market, distribute and sell Cambia® in Canada. On August 11, 2011, the Company and Nautilus executed the first amendment to the License Agreement and on September 30, 2012 executed the second amendment to the License Agreement. The payments under this agreement include: a) US$250,000 ($255,820) upfront payment to Nautilus upon the execution of this agreement - paid; and b) the following milestone payments; i) US$750,000 ($746,175) to be paid upon the earlier of the first commercial sale of the product or six months after all regulatory approvals. As per the second amendment of the License Agreement, a payment of US$250,000 ($245,200) was paid in October 2012, while the remaining US$500,000 ($497,450) was made on March 1, 2013. Additional one-time performance based sales milestones are due as follows: i) US$250,000 ($265,900) the first year in which annual net sales exceed US$2,500,000 ($2,659,000), ii) US$500,000 ($531,800) the first year in which the annual net sales exceed US$5,000,000 ($5,318,000), iii) US$750,000 ($797,700) the first year in which the annual net sales exceed US$7,500,000 ($7,977,000), iv) US$1,000,000 ($1,063,600) the first year in which the annual net sales exceed US$10,000,000 ($10,636,000), v) US$1,500,000 ($1,595,400) the first year the annual net sales exceed US$15,000,000 ($15,954,000), and vi) US$2,000,000 ($2,127,200) the first year in which the annual net sales exceed US$20,000,000 ($21,272,000). Royalty rates are tiered and payable at rates ranging from 22.5-25.0% of net sales. The initial term of the agreement expires on September 30, 2025 but is subject to automatic renewals under certain circumstances.

Other Laws and Regulations

Tribute’s operations are or may be subject to various federal, provincial, state and local laws, regulations and recommendations relating to the marketing of products and relationships with treating physicians, data protection, safe working conditions, laboratory and manufacturing practices, patient safety, the export of products to certain countries and the purchase, storage, movement, use and disposal of hazardous or potentially hazardous substances. Although the Company believes its safety procedures comply with the standards prescribed by federal, provincial, state and local regulations, the risk of contamination, injury or other accidental harm cannot be eliminated completely. In the event of an accident, the Company could be held liable for any damages that result. The amount of such damages could have a materially adverse effect on the Company’s results of operations and financial condition.

Employees

The Company currently employs forty employees including full-time, part-time and contract employees. Twenty-seven of these employees are in sales and marketing and the remainder are in management and administration positions. The Company may add additional staff in areas that its management may feel is necessary for the successful operation of the Company.

The Company is substantially dependent on the services of its key senior management personnel. The Company has entered into employment agreements with certain of its key officers, (see “Item 11 – Executive Compensation”). The loss of the services of any key management employee could have a materially adverse effect on the Company. The Company does not maintain key man life insurance on the life of its officers. In addition, the Company’s future success will depend in part upon its continuing ability to hire, train, motivate and retain key senior management and skilled technical and marketing personnel. The market for qualified personnel has historically been and the Company expects that it will continue to be very competitive.

Customers

During the year ended December 31, 2013, the Company had two significant pharmaceutical wholesale customers that account for 58.2% (McKesson Pharmaceutical - 42.5% and Shoppers Drug Mart Inc. - 15.7%) of the Company’s sales. This is normal and customary in the Canadian pharmaceutical business. These are well known and highly respected customers that have a solid track record of paying all outstanding amounts owing on time and the Company does not anticipate that this will materially change in 2014.

Our Website

Our website address is www.tributepharma.com. Information found on our website is not incorporated by reference into this report. We make available free of charge through our website our Securities and Exchange Commission (“SEC”), filings furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The Company will also make available all financial reports filed in accordance with US GAAP with SEDAR through its website. The Company invites investors and interested parties to sign up for “Email Alerts” on the Company’s website to receive information such as press releases as they become available.

You should carefully consider the risks described below together with all of the other information included in this annual report on Form 10-K before making an investment decision with regard to our securities. The statements contained in or incorporated into this annual report on Form 10-K that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business

We have incurred significant losses since inception of the Company. If we are unable to achieve and then maintain profitability, the market value of our common stock will likely decline.

As of December 31, 2013 we had an accumulated deficit of $14,295,911. Because of the numerous risks and uncertainties associated with our products, we are unable to predict with any certainty the extent of any future losses or when we will become profitable. If we are unable to achieve and then maintain profitability, the market value of our common stock will likely decline.

We will require additional financing to expand our operations.

Management is seeking various alternatives to ensure that we can meet some of our operating cash flow requirements through financing activities, such as private placements of our common stock, preferred stock offerings and offerings of debt and convertible debt instruments as well as through merger or acquisition opportunities. In addition, management is actively seeking strategic alternatives, including strategic investments and divestitures.

We cannot provide any assurance that we will obtain the required funding. Our inability to obtain required funding in the near future or our inability to obtain funding on favorable terms will have a material adverse effect on our operations and our strategic development plan for future growth.

As a result of the weakened global economic situation, Tribute, along with all other pharmaceutical research and development entities, may have restricted access to capital, bank debt and equity, and is likely to face increased borrowing costs. The lending capacity of all financial institutions has diminished and risk premiums have increased. As future operations will be financed out of funds generated from financing activities, our ability to do so is dependent on, among other factors, the overall state of capital markets and investor appetite for investments in the pharmaceutical industry and our securities in particular.

Should we elect to satisfy our cash commitments through the issuance of securities, by way of either private placements or public offerings or otherwise, there can be no assurance that our efforts to raise such funding will be successful, or achieved on terms favorable to us or our existing shareholders. If adequate funds are not available on terms favorable to us, we may have to reduce substantially or eliminate expenditures, production and marketing of our proposed products or obtain funds through arrangements with corporate partners that require us to relinquish rights to certain of our technologies or products. There can be no assurance that we will be able to raise additional capital if our current capital resources are exhausted.

Our quarterly operating results may fluctuate significantly.

We expect our operating results to be subject to quarterly fluctuations. Our net loss and other operating results will be affected by numerous factors, including:

|

●

|

variations in the level of expenses related to our products;

|

|

●

|

regulatory developments affecting our product candidates;

|

|

●

|

our execution of any collaborative, licensing or similar arrangements, and the timing of payments we may make or receive under these arrangements; and

|

|

●

|

the level of underlying demand for our products and wholesalers’ buying patterns.

|

If our quarterly operating results fall below the expectations of investors or securities analysts, the price of our common stock could decline substantially. Furthermore, any quarterly fluctuations in our operating results may, in turn, cause the price of our common stock to fluctuate substantially.

If we make strategic acquisitions, we will incur a variety of costs and might never realize the anticipated benefits.

There are accretive and non-accretive acquisitions of pharmaceutical products. Since the valuations of product acquisitions are based on a forecast over a specified time-period, there is some risk inherent with all acquisitions. When appropriate opportunities become available, we might attempt to acquire approved products, additional drug candidates, technologies or businesses that we believe are a strategic fit with our business. If we pursue any transaction of that sort, the process of negotiating the acquisition and integrating an acquired product, drug candidate, technology or business might result in operating difficulties and expenditures and might require significant management attention that would otherwise be available for ongoing development of our business, whether or not any such transaction is ever consummated. Moreover, we might never realize the anticipated benefits of any acquisition or forecasted sales may not materialize. Future acquisitions could result in potentially dilutive issuances of equity securities, the incurrence of debt, contingent liabilities, or impairment expenses related to goodwill, and impairment or amortization expenses related to other intangible assets, which could harm our financial condition. However, some acquisitions are accretive in nature and for the completion of a successful accretive transaction the benefits may outweigh the risks.

We may not be able to compete with treatments now being marketed and developed, or which may be developed and marketed in the future by other companies.

Our products will compete with existing and new therapies and treatments and numerous pharmaceutical, biotechnology and drug delivery companies, hospitals, research organizations, individual scientists and nonprofit organizations are engaged in the development of alternatives to our technologies. Some of these companies have greater research and development capabilities, experience, manufacturing, marketing, financial and managerial resources than we do. Collaborations or mergers between large pharmaceutical or biotechnology companies with competing drug delivery technologies could enhance our competitors’ financial, marketing and other resources. Developments by other drug delivery companies could make our products or technologies uncompetitive or obsolete. Accordingly, our competitors may succeed in developing competing technologies, obtaining regulatory approval for products or gaining market acceptance more rapidly than we can.

If government programs and insurance companies do not agree to pay for or reimburse patients for our pharmaceutical products, our success will be impacted.

Sales of our products will depend in part on the availability of reimbursement by third-party payers such as government health administration authorities, private health insurers and other organizations. Third-party payers often challenge the price and cost-effectiveness of medical products and services. Governmental approval of health care products does not guarantee that these third-party payers will pay for the products. Even if third-party payers do accept our products, the amounts they pay may not be adequate to enable us to realize a profit. Legislation and regulations affecting the pricing of pharmaceuticals may change before our products are approved for marketing and any such changes could further limit reimbursement.

Even if regulatory approvals are obtained for our products, such products will be subject to ongoing regulatory review. If we or a partner fail to comply with continuing Canadian, U.S. and foreign regulations, the approvals to market drugs could be lost and our business would be materially adversely affected.

Following any initial Health Canada, FDA or foreign regulatory approval of any drugs or medical devices we or a partner may develop, such products will continue to be subject to regulatory review, including the review of adverse drug experiences, safety reports and clinical results that are reported after such products are made available to patients. This would include results from any post marketing tests or vigilance required as a condition of approval. The manufacturer and manufacturing facilities used to make any product candidates will also be subject to periodic review and inspection by regulatory authorities (“Regulatory Authorities”), including Health Canada and/or the FDA. The discovery of any new or previously unknown problems with the product, manufacturer or facility may result in restrictions on the products or manufacturer or facility, including withdrawal of the products from the market. Marketing, advertising and labeling also will be subject to regulatory requirements and continuing regulatory review. The failure to comply with applicable continuing regulatory requirements may result in fines, suspension or withdrawal of regulatory approval, product recalls and seizures, operating restrictions and other adverse consequences.

We and our partners are subject to extensive Canadian, U.S. and foreign government regulation, including the requirement of approval before products may be manufactured or marketed.