UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________

Form 10-K

____________________

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2019

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from _____ to _____

Commission file no. 001-16337

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification No.) |

(Address of principal executive offices and zip code)

Registrant's telephone number, including area code is (713 ) 652-0582

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol(s) | Name of Exchange on Which Registered | ||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files.) Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

☒ | Accelerated filer | ☐ | ||

Non-accelerated filer | ☐ | Smaller reporting company | ||

Emerging growth company | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of June 30, 2019, the aggregate market value of the voting and non-voting common stock of the registrant held by non-affiliates of the registrant was $1,060,682,700 .

As of February 17, 2020, the number of shares of common stock outstanding was 60,402,022 .

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Definitive Proxy Statement for the 2020 Annual Meeting of Stockholders, which the registrant intends to file with the Securities and Exchange Commission not later than 120 days after the end of the fiscal year covered by this Annual Report on Form 10‑K, are incorporated by reference into Part III of this Annual Report on Form 10‑K.

-1-

TABLE OF CONTENTS

Page | |||

PART I | |||

Cautionary Statement Regarding Forward-Looking Statements | |||

Item 1. | Business | ||

Item 1A. | Risk Factors | ||

Item 1B. | Unresolved Staff Comments | ||

Item 2. | Properties | ||

Item 3. | Legal Proceedings | ||

Item 4. | Mine Safety Disclosures | ||

PART II | |||

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||

Item 6. | Selected Financial Data | ||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | ||

Item 8. | Financial Statements and Supplementary Data | ||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||

Item 9A. | Controls and Procedures | ||

Item 9B. | Other Information | ||

PART III | |||

Item 10. | Directors, Executive Officers and Corporate Governance | ||

Item 11. | Executive Compensation | ||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | ||

Item 14. | Principal Accounting Fees and Services | ||

PART IV | |||

Item 15. | Exhibits, Financial Statement Schedules | ||

Item 16. | Form 10-K Summary | ||

SIGNATURES | |||

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | |||

-2-

PART I

Cautionary Statement Regarding Forward-Looking Statements

This Annual Report on Form 10-K and other statements we make contain certain "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 (the "Securities Act") and Section 21E of the Securities Exchange Act of 1934 (the "Exchange Act"). Actual results could differ materially from those projected in the forward-looking statements as a result of a number of important factors, including incorrect or changed assumptions. For a discussion of known material factors that could affect our results, please refer to "Part I, Item 1. Business," "Part I, Item 1A. Risk Factors," "Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Part II, Item 7A. Quantitative and Qualitative Disclosures about Market Risk" below.

You can typically identify "forward-looking statements" by the use of forward-looking words such as "may," "will," "could," "project," "believe," "anticipate," "expect," "estimate," "potential," "plan," "forecast," "proposed," "should," "seek," and other similar words. Such statements may relate to our future financial position, budgets, capital expenditures, projected costs, plans and objectives of management for future operations and possible future strategic transactions. Actual results frequently differ from assumed facts and such differences can be material, depending upon the circumstances.

While we believe we are providing forward-looking statements expressed in good faith and on a reasonable basis, there can be no assurance that actual results will not differ from such forward-looking statements. The following are important factors that could cause actual results to differ materially from those expressed in any forward-looking statement made by, or on behalf of, our Company:

• | the level of supply of and demand for oil and natural gas; |

• | fluctuations in the current and future prices of oil and natural gas; |

• | the cyclical nature of the oil and natural gas industry; |

• | the level of exploration, drilling and completion activity; |

• | the financial health of our customers; |

• | political, economic and litigation efforts to restrict or eliminate certain oil and natural gas exploration, development and production activities due to concerns over the threat of climate change; |

• | the availability of and access to attractive oil and natural gas field prospects, which may be affected by governmental actions or actions of other parties which may restrict drilling and completion activities; |

• | the level of offshore oil and natural gas developmental activities; |

• | general global economic conditions; |

• | the ability of the Organization of Petroleum Exporting Countries ("OPEC") to set and maintain production levels and pricing; |

• | global weather conditions and natural disasters; |

• | public health crises, such as the coronavirus outbreak at the beginning of 2020, which could impact the global economy; |

• | changes in tax laws and regulations; |

• | the impact of tariffs and duties on imported materials and exported finished goods; |

• | impact of environmental matters, including future regulatory efforts to adopt environmental or climate change regulations that may result in increased operating costs or reduced commodity demand globally; |

• | our ability to timely obtain critical permits for constructing or operating facilities and find and retain skilled personnel; |

• | negative outcome of litigation, threatened litigation or government proceedings; |

• | our ability to develop new competitive technologies and products; |

• | fluctuations in currency exchange rates; |

• | physical, digital, cyber, internal and external security breaches; |

• | the availability and cost of capital; |

• | our ability to protect our intellectual property rights; |

• | our ability to complete the integration of acquired businesses and achieve the expected accretion in earnings; and |

• | the other factors identified in "Part I, Item 1A. Risk Factors." |

Should one or more of these risks or uncertainties materialize, or should the assumptions on which our forward-looking statements are based prove incorrect or change, actual results may differ materially from those expected, estimated or projected. In addition, the factors identified above may not necessarily be all of the important factors that could cause actual results to differ materially from those expressed in any forward-looking statement made by us, or on our behalf. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof. We undertake no responsibility to publicly release the result of any revision of our forward-looking statements after the date they are made.

-3-

In addition, in certain places in this Annual Report on Form 10-K, we refer to information and reports published by third parties that purport to describe trends or developments in the energy industry. The Company does so for the convenience of our stockholders and in an effort to provide information available in the market that will assist the Company's investors in better understanding the market environment in which the Company operates. However, the Company specifically disclaims any responsibility for the accuracy and completeness of such information and undertakes no obligation to update such information.

Item 1. Business

Our Company

Oil States International, Inc., through its subsidiaries, is a global oilfield products and services company serving the drilling, completion, subsea, production and infrastructure sectors of the oil and natural gas industry. Our manufactured products include highly engineered capital equipment as well as products consumed in the drilling, well construction and production of oil and natural gas. Through our acquisition of GEODynamics, Inc. ("GEODynamics") in 2018, we are a leading researcher, developer and manufacturer of engineered solutions to connect the wellbore with the formation in oil and natural gas well completions. Oil States is headquartered in Houston, Texas with manufacturing and service facilities strategically located across the globe. Our customers include many national oil and natural gas companies, major and independent oil and natural gas companies, onshore and offshore drilling companies and other oilfield service companies. We operate through three business segments – Well Site Services, Downhole Technologies and Offshore/Manufactured Products – and maintain a leadership position with certain of our product and service offerings in each segment. In this Annual Report on Form 10‑K, references to the "Company" or "Oil States," or to "we," "us," "our," and similar terms are to Oil States International, Inc. and its consolidated subsidiaries.

Available Information

The Company's website can be found at www.oilstatesintl.com. The Company makes available, free of charge through its website, its Annual Report on Form 10‑K, Quarterly Reports on Form 10‑Q, Current Reports on Form 8‑K, its proxy statement, Forms 3, 4 and 5 filed on behalf of directors and executive officers, and amendments to these reports, as soon as reasonably practicable after the Company electronically files such material with, or furnishes such material to, the Securities and Exchange Commission (the "SEC"). The Company is not including the information contained on the Company's website or any other website as a part of, or incorporating it by reference into, this Annual Report on Form 10‑K or any other filing the Company makes with the SEC. The filings are also available through the SEC's website at www.sec.gov. The Board of Directors of the Company (the "Board") has documented its governance practices by adopting several corporate governance policies. These governance policies, including the Company's Corporate Governance Guidelines, Corporate Code of Business Conduct and Ethics and Financial Code of Ethics for Senior Officers, as well as the charters for the committees of the Board (Audit Committee, Compensation Committee and Nominating & Corporate Governance Committee) may also be viewed at the Company's website. The financial code of ethics applies to our principal executive officer, principal financial officer, principal accounting officer and other senior officers. Copies of such documents will be provided to stockholders without charge upon written request to the corporate secretary at the address shown on the cover page of this Annual Report on Form 10‑K.

Our Business Strategy

We have historically grown our product and service offerings organically, through capital spending and strategic acquisitions. Our investments are focused in growth areas and on areas where we expect to be able to expand market share through our technology offerings and where we believe we can achieve an attractive return on our investment. As part of our long-term strategy, we continue to review complementary acquisitions, invest in research and development and make organic capital expenditures to enhance our cash flows, leverage our cost structure and increase our stockholders' returns. For additional discussion of our business strategy, please read "Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations."

Recent Developments

In addition to capital spending, we have invested in acquisitions of businesses complementary to our growth strategy. Our acquisition strategy has allowed us to leverage our existing and acquired products and services into new geographic locations and has expanded the breadth of our technology and product offerings while allowing us to leverage our cost structure. We have made strategic and complementary acquisitions in each of our business segments in recent years.

On December 12, 2017 we entered into an agreement to acquire GEODynamics, which provides oil and gas perforation systems and downhole tools in support of completion, intervention, wireline and well abandonment operations. On January 12, 2018, we closed the acquisition of GEODynamics for total consideration of approximately $615 million (the "GEODynamics Acquisition"), consisting of (i) $295 million in cash (net of cash acquired), (ii) approximately 8.66 million shares of our common stock (valued at $34.05 per share on the date of closing) and (iii) an unsecured $25 million promissory note.

-4-

In connection with the GEODynamics Acquisition, we completed several financing transactions in 2018 to extend the maturity of our debt and to provide flexibility in repaying outstanding borrowings under our revolving credit facility (the "Revolving Credit Facility") with anticipated future cash flows from operations.

On January 30, 2018, we sold $200 million aggregate principal amount of our 1.50% convertible senior notes due February 2023 (the "Notes") through a private placement to qualified institutional buyers. We received net proceeds from the offering of the Notes of approximately $194 million, after deducting issuance costs. We used the net proceeds to repay a portion of the borrowings outstanding under our Revolving Credit Facility, substantially all of which were drawn to fund the cash portion of the purchase price paid for GEODynamics.

Concurrently with the Notes offering, we amended our Revolving Credit Facility to extend the maturity date to January 2022, permit the issuance of the Notes and provide for up to $350 million in borrowing capacity, subject to certain limitations.

On February 28, 2018, we acquired Falcon Flowback Services, LLC ("Falcon"), a full-service provider of flowback and well testing services for the separation and recovery of fluids, solid debris and proppant used during hydraulic fracturing operations. Falcon provides additional scale and diversity to our Completion Services operations in key shale plays in the United States. The acquisition price was $84.2 million in cash, funded with borrowings under our Revolving Credit Facility.

During the third quarter of 2019, we made the strategic decision to reduce the scope of our Drilling Services business (adjusting from 34 rigs to 9 rigs) due to the ongoing weakness in customer demand for vertical drilling rigs in the U.S. land market. As a result of this decision, our Drilling Services business recorded a non-cash impairment charge of $33.7 million to decrease the carrying value of the business' fixed assets to their estimated fair value. Substantially all of the decommissioned rigs were sold in the fourth quarter of 2019.

During the fourth quarter of 2019, our Downhole Technologies segment recorded a non-cash goodwill impairment charge of $165.0 million due to, among other factors, a reduction in our near-term outlook for demand related to our short-cycle products and services in the U.S. shale play regions.

See Note 4, "Details of Selected Balance Sheet Accounts," Note 5, "Business Acquisitions" and Note 7, "Long-term Debt" to the Consolidated Financial Statements included in this Annual Report on Form 10‑K for further discussion of these recent developments.

Our Industry

We principally operate in the oilfield services industry and provide a broad range of products and services to our customers through each of our business segments. See Note 15, "Segments and Related Information," to the Consolidated Financial Statements included in this Annual Report on Form 10‑K for financial information by segment along with a geographical breakout of revenues and long-lived assets for each of the three years in the period ended December 31, 2019. Demand for our products and services is cyclical and substantially dependent upon activity levels in the oil and natural gas industry, particularly our customers' willingness to invest capital in the exploration for and development of crude oil and natural gas reserves. Our customers' capital spending programs are generally based on their outlook for near-term and long-term commodity prices, economic growth, commodity demand and estimates of resource production. As a result, demand for our products and services is largely sensitive to expectations with respect to future crude oil and natural gas prices.

Our consolidated results of operations include contributions from the GEODynamics and Falcon acquisitions completed in the first quarter of 2018. Our reported results of operations reflect the impact of current industry trends and customer spending activities with investments weighted toward U.S. shale play regions. However, in 2019, we began to see a general improvement in the level of planned investments in deepwater markets globally.

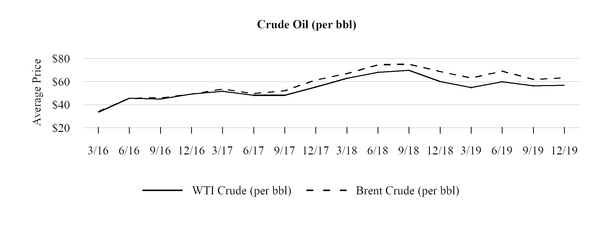

Our historical financial results reflect the cyclical nature of the oilfield services industry – witnessed by periods of increasing and decreasing activity in each of our operating segments. Lower oil and natural gas prices since 2014 have caused a reduction in most of our customers' drilling, completion and other production activities and related spending on our products and services. The reduction in demand from our customers has resulted in an oversupply of many of the services and products we provide. Such oversupply has substantially reduced the prices we can charge our customers for many of our products and services. Although oil prices have improved since the trough in 2016, these price improvements have not resulted in significant, sustained global improvements in the demand for our products and services or the prices we are able to charge. Following material price declines in the fourth quarter of 2018, Brent and West Texas Intermediate ("WTI") crude oil prices averaged $64 and $57 per barrel, respectively, in 2019 - down 10% and 13%, respectively, compared to 2018 average prices. While the commodity price environment improved in 2019 relative to December of 2018, the crude oil price outlook and associated volatility continues to have a moderating impact on our customers' operating results and capital spending plans, particularly those operating in the U.S. shale play regions. The U.S.

-5-

rig count at December 31, 2019 totaled 805 rigs, which was down 26% since the most recent peak of 1,083 rigs in December of 2018. We expect further customer-driven activity declines in early 2020 given crude oil price declines since the end of 2019 as our customers strive for financial discipline and spending levels that are within their capital budgets and generated cash flow ranges. This may cause additional declines in the demand for, and prices of, our products and services, which would adversely affect our future results of operations, cash flows and financial position. For additional information about activities in each of our segments, see "Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations."

Our Well Site Services segment is primarily affected by drilling and completion activity in the United States, including the Gulf of Mexico, and, to a lesser extent, the rest of the world. U.S. drilling and completion activity and, in turn, our Well Site Services segment results, are sensitive to near-term fluctuations in commodity prices, particularly WTI crude oil prices, given the call-out nature of our operations in the segment.

Similarly, demand for our Downhole Technologies segment products is predominantly tied to land-based oil and natural gas exploration and production activity levels in the United States. The primary driver for this activity is the price of crude oil and, to a lesser extent, natural gas. Activity levels have been, and we expect will continue to be, highly correlated with hydrocarbon commodity prices. Over recent years, our industry experienced increased customer spending in crude oil and liquids-rich exploration and development in the U.S. shale plays utilizing enhanced horizontal drilling and completion techniques.

Demand for the products and services supplied by our Offshore/Manufactured Products segment is generally driven by both the longer-term outlook for commodity prices and changes in land-based drilling and completion activity. Over recent years, lower crude oil prices, coupled with a relatively uncertain outlook around shorter-term and possibly longer-term commodity price improvements, caused exploration and production companies to reevaluate their future capital expenditures in regards to deepwater projects since they are expensive to drill and complete, have long lead times to first production and may be considered uneconomical relative to the risk involved. This resulted in reduced bidding and quoting activity, as well as reduced orders from customers, for our Offshore/Manufactured Products segment in 2017 and 2018 relative to the peak in 2014. Bidding and quoting activity, along with orders from customers, for deepwater projects improved in 2019 from 2018 levels and the potential for future awards appears to be improving.

See "Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations – Macroeconomic Environment" for further discussion on our industry.

Well Site Services

Overview

For the years ended December 31, 2019, 2018 and 2017, our Well Site Services segment generated approximately 42%, 44% and 43%, respectively, of our consolidated revenue. Our Well Site Services segment includes a broad range of equipment and services that are used to drill for, establish and maintain the flow of oil and natural gas from a well throughout its life cycle. In this segment, our operations primarily include completion-focused equipment and services and, to a much lesser extent, land drilling services in the United States. We use our fleet of completion tools and drilling rigs to serve our customers at well sites and project development locations. Our equipment and services are used in both onshore and offshore applications throughout the drilling, completion and production phases of a well's life cycle.

Well Site Services Market

Demand for our completion and drilling services is predominantly tied to the level of oil and natural gas exploration and production activity on land in the United States. The primary driver for this activity is the price of crude oil and, to a lesser extent, natural gas. Activity levels have been, and we expect will continue to be, highly correlated with hydrocarbon commodity prices.

Completion Services

Our Completion Services business, which is primarily marketed through the brand names Oil States Energy Services, Falcon and Tempress, provides a wide range of services used in the onshore and offshore oil and gas industry, including:

• | wellhead isolation services; |

• | flowback and frac valve services; |

• | wireline and coiled tubing support services; |

• | well testing, including separators and line heaters; |

• | downhole extended-reach technology; |

• | pipe recovery systems; |

-6-

• | thru-tubing milling and fishing services; |

• | hydraulic chokes and manifolds; |

• | blowout preventers; and |

• | gravel pack and sand control operations on wellbores. |

Employees in our Completion Services business typically rig up and operate our equipment on the well site for our customers. Our Completion Services equipment is primarily used during the completion and production stages of a well. As of December 31, 2019, we provided completion services through approximately 35 distribution locations serving our customers in the United States, including the Gulf of Mexico, and international markets. We typically provide our services and equipment based on daily rates which vary depending on the type of equipment and the length of the job. Billings to our customers typically separate charges for our equipment from charges for our field technicians. We own patents or have patents pending covering some of our technology, particularly in our wellhead isolation equipment and downhole extended-reach technology product lines. Our customers in the Completion Services business include major, independent and private oil and gas companies and other large oilfield service companies. No customer in Completion Services represented more than 10% of our total consolidated revenue in any period presented. Competition in the Completion Services business is widespread and includes many smaller companies, although we also compete with the larger oilfield service companies for certain equipment and services.

Drilling Services

Our Drilling Services business, which is marketed to oil and gas companies under the brand name Capstar Drilling, provides vertical land drilling services in the United States for shallow to medium depth wells generally of less than 15,000 feet. We historically served two primary markets with our Drilling Services business: the Permian Basin in West Texas and the U.S. Rocky Mountain area. During the third quarter of 2019, we made the strategic decision to reduce the scope of our Drilling Services business (adjusting from 34 rigs to 9 rigs) due to the ongoing weakness in customer demand for vertical drilling rigs in the U.S. land market. Since September 2019, the operations are primarily focused on serving operators in the U.S. Rocky Mountain region. See Note 4, "Details of Selected Balance Sheet Accounts," to the Consolidated Financial Statements included in this Annual Report on Form 10‑K for additional discussion.

Downhole Technologies

Overview

Our Downhole Technologies segment is comprised of the GEODynamics business we acquired in January 2018. GEODynamics was founded in 2004 as a researcher, developer and manufacturer of consumable engineered products used in completion applications. For the years ended December 31, 2019 and 2018, our Downhole Technologies segment contributed approximately 18% and 20%, respectively, of our consolidated revenue. This segment provides oil and gas perforation systems, downhole tools and services in support of completion, intervention, wireline and well abandonment operations. This segment designs, manufactures and markets its consumable engineered products to oilfield service as well as exploration and production companies.

Downhole Technologies Market

Similar to our Well Site Services segment, demand for our Downhole Technologies segment products is predominantly tied to the level of oil and natural gas exploration and production activity on land in the United States. The primary driver for this activity is the price of crude oil and, to a lesser extent, natural gas. Activity levels have been, and we expect will continue to be, highly correlated with hydrocarbon commodity prices. Demand for this segment's products is also influenced by continued trends toward longer lateral lengths, increased frac stages and more perforation clusters to target increased unconventional well productivity, which requires ongoing technological and product developments.

Products

Product and service offerings for this segment include advanced perforation technology achieved through patented and proprietary systems combined with advanced modeling and analysis tools. This expertise has led to the optimization of perforation hole size, depth, and quality of tunnels, which are key factors for maximizing the effectiveness of hydraulic fracturing. Additional offerings include proprietary toe valve and frac plug products, which are focused on zonal isolation for hydraulic fracturing of horizontal wells, and a broad range of consumable products, such as setting tools and bridge plugs, that are used in completion, intervention and decommissioning applications.

-7-

Customers and Competitors

Our customers in the Downhole Technologies segment include other oilfield services companies as well as major, independent and private oil and gas companies. No customer in this segment represented more than 10% of our total consolidated revenue in any period presented. Competition in the Downhole Technologies business is widespread and includes many smaller companies, although we also compete with the larger oilfield service companies for certain products and services.

Offshore/Manufactured Products

Overview

For the years ended December 31, 2019, 2018 and 2017, our Offshore/Manufactured Products segment generated approximately 40%, 36% and 57%, respectively, of our consolidated revenue. Through this segment, we provide technology-driven, highly-engineered products and services for offshore oil and natural gas production systems and facilities, as well as certain products and services to the offshore and land-based drilling and completion markets. Our products and services used primarily in deepwater producing regions include our FlexJoint® technology, advanced connector systems, high-pressure riser systems, compact valves, deepwater mooring systems, cranes, subsea pipeline products, specialty welding, fabrication, cladding and machining services, offshore installation services and inspection and repair services. In addition, we design, manufacture and market numerous other products and services used in both land and offshore drilling and completion activities and by non-oil and gas customers, including consumable downhole elastomer products used in onshore completion activities, valves and sound and vibration dampening products used in military applications. We have facilities that support our Offshore/Manufactured Products segment in Arlington, Houston and Lampasas, Texas; Houma, Louisiana; Oklahoma City and Tulsa, Oklahoma; the United Kingdom; Brazil; Singapore; Spain; Thailand; Vietnam; China; the United Arab Emirates; and India.

Offshore/Manufactured Products Market

The market for products and services offered by our Offshore/Manufactured Products segment centers primarily on the development of infrastructure for offshore production facilities and their subsequent operations, exploration and drilling activities, and to a lesser extent, new rig and vessel construction, refurbishments or upgrades. Demand for oil and natural gas, and the related drilling and production in offshore areas throughout the world, particularly in deeper water, drive spending for these activities. Sales of our shorter-cycle products to land-based drilling and completion markets are driven by the level and complexity of drilling, completion and workover activity, particularly in North America.

Products and Services

In operation for more than 75 years, our Offshore/Manufactured Products segment provides a broad range of products and services for use in offshore development and drilling activities. This segment also provides products for onshore oil and natural gas, defense and general industries. Our Offshore/Manufactured Products segment is dependent in part on the industry's continuing innovation and creative applications of existing technologies. We own various patents covering some of our technology, particularly in our connector and valve product lines.

Offshore Development and Drilling Activities. We design, manufacture, inspect, assemble, repair, test and market equipment for mooring, pipeline, production and drilling risers, and subsea applications along with equipment for offshore vessel and rig construction. Our products are components of equipment used for the drilling and production of oil and natural gas wells on offshore fixed platforms and mobile production units, including floating platforms, such as tension leg platforms, floating production, storage and offloading ("FPSO") vessels, Spars, and other marine vessels and offshore rigs. Our products and services include:

• | flexible bearings and advanced connection systems; |

• | casing and conductor connections and joints; |

• | subsea pipeline products; |

• | compact ball valves, manifold system components and diverter valves; |

• | marine winches, mooring systems, cranes and other heavy-lift rig equipment; |

• | production, workover, completion and drilling riser systems and their related repair services; |

• | blowout preventer ("BOP") stack assembly, integration, testing and repair services; |

• | consumable downhole products; and |

• | other products and services, including welding, cladding and other metallurgical technologies. |

-8-

Flexible Bearings and Advanced Connection Systems. We are the key supplier of flexible bearings, or FlexJoint® connectors, to the offshore oil and natural gas industry as well as weld-on connectors and fittings that join lengths of large diameter conductors or casing used in offshore drilling and production operations. A FlexJoint® is a flexible bearing that allows for rotational movement of a riser or tension leg platform tether while under high tension and/or pressure. When positioned at the top, bottom, or, in some cases, middle of a deepwater riser, it reduces the stress and loads on the riser while compensating for the pitch and rotational forces on the riser as the production facility or drilling rig moves with ocean forces. FlexJoint® connectors are used on drilling, production and export risers and are used increasingly as offshore production moves to deeper water.

Drilling riser systems provide the vertical conduit between the floating drilling vessel and the subsea wellhead. Through the drilling riser, the drill string is guided into the well and drilling fluids are returned to the surface. Production riser systems provide the vertical conduit for the hydrocarbons from the subsea wellhead to the floating production facility. Oil and natural gas flows to the surface for processing through the production riser. Export risers provide the vertical conduit from the floating production facility to the subsea export pipelines. Our FlexJoint® connectors are a critical element in the construction and operation of production and export risers on floating production systems in deepwater.

Floating production systems, including tension leg platforms, FPSO facilities and Spars (defined below), are a significant means of producing oil and natural gas, particularly in deepwater environments. We provide many important products for the construction of these facilities. A tension leg platform ("TLP") is a floating platform that is moored by vertical pipes, or tethers, attached to both the platform and the sea floor. Our FlexJoint® tether bearings are used at the top and bottom connections of each of the tethers, and our Merlin™ connectors are used to efficiently assemble the tether joints during offshore installation. An FPSO is a floating vessel, typically ship shaped, used to produce and process oil and natural gas from subsea wells. A Spar is a floating vertical cylindrical structure which is approximately six to seven times longer than its diameter and is anchored in place. Our FlexJoint® connectors are used to attach the various production, injection, import or export risers to all of these floating production systems.

Casing and Conductor Connections and Joints. Our advanced connection systems provide connectors used in various drilling and production applications offshore. These connectors are welded onto pipe to provide more efficient joint to joint connections with enhanced tensile and burst capabilities that exceed those of connections machined onto plain-end-pipe. Our connectors are reusable and pliable and, depending on the application, are equipped with metal-to-metal seals. We offer a suite of connectors offering differing specifications depending on the application. Our Merlin™ connectors are our premier connectors combining superior static strength and fatigue life with fast, non-rotational make-up and a slim profile. Merlin™ connectors have been used in sizes up to 60 inches (outside diameter) for applications including open-hole and tie-back casing, offshore conductor casing, pipeline risers and TLP tendons which moor the TLP to the sea floor.

Subsea Pipeline Products. We design and manufacture a variety of equipment used in the construction, maintenance, expansion and repair of offshore oil and natural gas pipelines. New construction equipment includes:

• | pipeline end manifolds and pipeline end terminals; |

• | deep and shallow water pipeline connectors; |

• | midline tie-in sleds; |

• | forged steel Y-shaped connectors for joining two pipelines into one; |

• | pressure-balanced safety joints for protecting pipelines and related equipment from anchor snags or a shifting sea-bottom; |

• | electrical isolation joints; and |

• | hot-tap clamps that allow new pipelines to be joined into existing lines without interrupting the flow of petroleum products. |

We provide diverless connection systems for subsea flowlines and pipelines. Our HydroTech® collet connectors provide a high-integrity, proprietary metal-to-metal sealing system for the final hook-up of deep offshore pipelines and production systems. They also are used in diverless pipeline repair systems and future pipeline tie-in systems. Our lateral tie-in sled, which is installed with the original pipeline, allows a subsea tie-in to be made quickly and efficiently using proven HydroTech® connectors without costly offshore equipment mobilization and without shutting off product flow.

We provide pipeline repair hardware, including deepwater applications beyond the depth of diver intervention. Our products include:

• | repair clamps used to seal leaks and restore the structural integrity of a pipeline; |

• | mechanical connectors used in repairing subsea pipelines without having to weld; |

• | misalignment and swivel ring flanges; and |

• | pipe recovery tools for recovering dropped or damaged pipelines. |

-9-

Compact Ball Valves, Manifold System Components and Diverter Valves. Our Piper Valve division designs and manufactures compact high-pressure valves and manifold system components for all environments of the oil and gas industry including onshore, offshore, drilling and subsea applications. Our valve and manifold bores are designed to closely match the inside diameter of the required pipe schedule for the system working pressure. The result is elimination of piping transition areas that minimize erosion and system friction pressure loss, resulting in a more efficient flow path. Our floating ball valve design with its large ball/seat interface has over 30 years of field service experience in upstream unprocessed produced liquids and gasses, assuring reliable service. Oil States Piper Valve Optimum Flow Technology is our way of helping end users maximize space, minimize weight and increase production.

Marine Winches, Mooring Systems, Cranes and other Heavy-Lift Rig Equipment. We design, engineer and manufacture marine winches, mooring systems, cranes and certain rig equipment. Our Skagit® winches are engineered for mooring floating and semi-submersible drilling rigs as well as positioning pipelay and derrick barges, anchor handling boats and jack-ups. Our Nautilus® marine cranes are used on production platforms throughout the world. We also design and fabricate rig equipment such as automatic pipe racking, blowout preventer handling equipment, as well as handling equipment used in the installation of offshore wind turbine platforms. Our engineering teams, manufacturing capability and service technicians, who install and service our products, provide our customers with a broad range of equipment and services to support their operations. Aftermarket service and support of our installed base of equipment to our customers is also an important source of revenue to us.

Production, Workover, Completion and Drilling Riser Systems and their related repair services. Utilizing the expertise of our welding technology group, we have extended the boundaries of our Merlin™ connector technology with the design and manufacture of multiple riser systems. The unique Merlin™ connection has proven to be a robust solution for even the most demanding high-pressure (up to 20,000 psi) riser systems used in high-fatigue, deepwater applications. Our riser systems are designed to meet a range of static and fatigue stresses on par with those of our Tension Leg Element connectors. The connector can be welded or machined directly onto upset riser pipe and provide sufficient material to perform "re-cuts" after extended service. We believe that our marine riser offers superior tension capabilities together with one of the fastest run times in the industry. Auxiliary riser system components and running tools can be provided along with full-service inspection and repair of these riser systems.

BOP Stack Assembly, Integration, Testing and Repair Services. While not typically a manufacturer of BOP components, we design and fabricate lifting and protection frames for BOP stacks and offer the complete system integration of BOP stacks and subsea production trees. We can provide complete turnkey and design fabrication services. We also design and manufacture a variety of custom subsea equipment, such as riser flotation tank systems, guide bases, running tools and manifolds. In addition, we also offer blowout preventer and drilling riser testing and repair services.

Consumable Downhole Products. North American shale play development has expanded the need for more advanced completion tools. In order to reduce well completion costs, minimizing the time to drill out tools is very important. Our Offshore/Manufactured Products segment has leveraged its knowledge of molded thermoset composites and elastomers to help meet this demand. For example, we have had success in developing and producing composite drillable zonal isolation tools (i.e., bridge/frac plugs) utilizing design and production techniques that reduce cost while still delivering high-quality performance. Time to drill out has been reduced significantly in comparison to other filament wound products in the market. Our products also include:

• | Swab Cups - used primarily in well servicing work; |

• | Rod Guides/Centralizers - used in both drilling and production for pipe protection; |

• | Gate Valve and Butterfly Valve Seats – we service many markets in the valve industry including well completion, refining, and distribution; |

• | Casing and Cementing Products – we are a custom manufacturer of cementing plugs, wellbore wipers, valve assemblies, combination plugs, specialty seals and gaskets; and |

• | Service Tools – our products include frac balls, packer elements, zonal isolation tools, as well as many custom molded products used in the well servicing industry. |

Other Products & Services. Our Offshore/Manufactured Products segment also produces a variety of products for use in industrial, military and other applications outside the oil and gas industry. For example, we provide:

• | sound and vibration isolation equipment for marine vessels; |

• | metal-elastomeric FlexJoint® bearings used in a variety of naval and marine applications; |

• | products used in the construction and maintenance of offshore wind projects; and |

• | drum-clutches and brakes for heavy-duty power transmission in the mining, paper, logging and marine industries. |

-10-

Backlog

Offshore/Manufactured Products' backlog consists of firm customer purchase orders for which contractual commitments exist and delivery is scheduled. Backlog in our Offshore/Manufactured Products segment was $280 million at December 31, 2019, compared to $179 million at December 31, 2018 and $168 million at December 31, 2017. We expect approximately 75% of our backlog at December 31, 2019 to be recognized as revenue during 2020. In some instances, these purchase orders are cancelable by the customer, subject to the payment of termination fees and/or the reimbursement of our costs incurred. While backlog cancellations have historically been insignificant, we incurred cancellations totaling $5.0 million during 2019 and $6.5 million during 2018, which we believe is attributable to lower commodity prices, the resultant decrease in capital spending by our customers and, in some cases, the financial condition of our customers. Additional cancellations may occur in the future, which would reduce our backlog. Our backlog is an important indicator of future Offshore/Manufactured Products' shipments and major project revenues; however, backlog as of any particular date may not be indicative of our actual operating results for any future period. We believe that the offshore construction and development business is characterized by lengthy projects and a "long lead-time" order cycle. The change in backlog levels from one period to the next does not necessarily evidence a long-term trend.

Regions of Operations

Our Offshore/Manufactured Products segment provides products and services to customers in the major offshore crude oil and natural gas producing regions of the world, including the U.S. Gulf of Mexico, Brazil, West Africa, the North Sea, Azerbaijan, Russia, India, Southeast Asia, China, the United Arab Emirates and Australia. In addition, we provide shorter-cycle products to customers in the land-based drilling and completion markets in the United States and, to a lesser extent, outside the United States.

Customers and Competitors

We market our products and services to a broad customer base, including direct end-users, engineering and design companies, prime contractors, and at times, our competitors through outsourcing arrangements. While no customer accounted for more than 10% of our consolidated revenues in 2019, Halliburton Company individually accounted for 10% and 16% of our total consolidated revenues in the years ended December 31, 2018 and 2017, respectively. Our main competitors in this segment include Cameron (a division of Schlumberger Limited), Dril-Quip, Inc., National Oilwell Varco, Inc., Baker Hughes Company, Hutchinson Group (a subsidiary of Total S.A.), Sparrows Offshore Group LTD, Oceaneering International, Inc. and Raina Engineers.

Seasonality of Operations

Our operations are directly affected by seasonal weather differences in certain areas in which we operate, most notably in the Rocky Mountain region, and the Gulf of Mexico. Severe winter weather conditions in the Rocky Mountain region can restrict access to work areas for our Well Site Services and Downhole Technologies segment operations. Our operations in the Gulf of Mexico are also affected by weather patterns. Seasonal weather trends in the Gulf Coast region generally result in higher drilling activity in the spring, summer and fall months with the lowest levels of activity in the winter months. Summer and fall drilling activity can be interrupted by hurricanes and other storms prevalent in the Gulf of Mexico and along the Gulf Coast. As a result of these seasonal differences, full-year results are not likely to be a direct multiple of any particular quarter or combination of quarters.

Employees

As of December 31, 2019, the Company employed 3,428 full-time employees on a consolidated basis, 42% of whom are in our Well Site Services segment, 14% of whom are in our Downhole Technologies segment, 41% of whom are in our Offshore/Manufactured Products segment, and 2% of whom are in our corporate headquarters. During 2019, company-wide headcount was reduced 13% from a total of 3,926 full-time employees as of December 31, 2018. We were party to collective bargaining agreements covering fewer than 100 employees located in the United Kingdom and Argentina as of December 31, 2019. We believe we have good labor relations with our employees.

-11-

Environmental and Occupational Health and Safety Matters

Our business operations are subject to numerous environmental and occupational health and safety laws and regulations that may be imposed domestically at the federal, regional, state, tribal and local levels or by foreign governments. These laws and regulations impose stringent environmental and/or worker safety regulation. Numerous governmental entities, including domestically the U.S. Environmental Protection Agency ("EPA"), the federal Bureau of Alcohol, Tobacco, Firearms and Explosives ("ATF"), the U.S. Occupational Safety and Health Administration ("OSHA") and analogous state agencies, have the power to enforce compliance with these laws and regulations and the permits issued under them, often requiring difficult and costly actions. These laws and regulations may, among other things, (i) require the acquisition of permits to conduct drilling and other regulated activities; (ii) restrict the types, quantities and concentration of various substances that can be released into the environment or injected into subsurface formations in connection with oil and natural gas drilling and production activities and wellsite support services; (iii) limit or prohibit drilling activities on certain lands lying within wilderness, wetlands and other protected areas; (iv) impose stringent regulations on the licensing or storage and use of explosives; (v) require remedial measures to mitigate pollution from former and ongoing operations, such as requirements to close pits and plug abandoned wells or decommission offshore facilities; (vi) impose specific safety and health criteria addressing worker protection; and (vii) impose substantial liabilities for pollution resulting from drilling operations and well site support services.

The more significant of these existing environmental and occupational health and safety laws and regulations include the following U.S. legal standards, as amended from time to time:

• | the Clean Air Act ("CAA"), which restricts the emission of air pollutants from many sources and imposes various pre-construction, operational, monitoring and reporting requirements, and that the EPA has relied upon as authority for adopting climate change regulatory initiatives relating to greenhouse gas ("GHG") emissions; |

• | the Federal Water Pollution Control Act, also known as the Clean Water Act, which regulates discharges of pollutants from facilities to state and federal waters and establishes the extent to which waterways are subject to federal jurisdiction and rulemaking as protected waters of the United States; |

• | the Oil Pollution Act of 1990, which subjects owners and operators of vessels, onshore facilities, and pipelines, as well as lessees or permittees of areas in which offshore facilities are located, to liability for removal costs and damages arising from an oil spill in waters of the United States; |

• | U.S. Department of the Interior regulations, which govern oil and natural gas operations on federal lands and waters and impose obligations for establishing financial assurances for decommissioning activities, liabilities for pollution cleanup costs resulting from operations, and potential liabilities for pollution damages; |

• | the Comprehensive Environmental Response, Compensation and Liability Act of 1980, which imposes liability on generators, transporters, and arrangers of hazardous substances at sites where hazardous substance releases have occurred or are threatening to occur; |

• | the Resource Conservation and Recovery Act ("RCRA"), which governs the generation, treatment, storage, transport, and disposal of solid wastes, including oil and natural gas exploration and production wastes and hazardous wastes; |

• | the Safe Drinking Water Act ("SDWA"), which ensures the quality of the nation's public drinking water through adoption of drinking water standards and controlling the injection of waste fluids into below-ground formations that may adversely affect drinking water sources; |

• | the Emergency Planning and Community Right-to-Know Act, which requires facilities to implement a safety hazard communication program and disseminate information to employees, local emergency planning committees, and response departments on toxic chemical uses and inventories; |

• | the Occupational Safety and Health Act, which establishes workplace standards for the protection of the health and safety of employees, including the implementation of hazard communications programs designed to inform employees about hazardous substances in the workplace, potential harmful effects of these substances, and appropriate control measures; |

• | the Endangered Species Act, which restricts activities that may affect federally identified endangered and threatened species or their habitats through the implementation of operating restrictions or a temporary, seasonal, or permanent ban in affected areas; |

• | the National Environmental Policy Act, which requires federal agencies, including the Department of the Interior, to evaluate major agency actions having the potential to impact the environment and that may require the preparation of environmental assessments and more detailed environmental impact statements that may be made available for public review and comment; |

-12-

• | the Department of Transportation regulations, which relate to advancing the safe transportation of energy and hazardous materials, including explosives, and emergency response preparedness; and |

• | regulations adopted by the ATF, a law enforcement agency under the U.S. Department of Justice, that impose stringent licensing conditions with respect to the acquisition, storage and use of explosives for well site support services in the oil and natural gas sector. |

These federal environmental and occupational health and safety laws and regulations generally restrict the level of substances generated as a result of our operations that may be emitted to ambient air, discharged to surface water, and disposed or otherwise released to surface and below-ground soils and groundwater. Additionally, there exist regional, state, tribal and local jurisdictions in the United States where we operate that also have, are developing or considering developing, similar environmental and occupational health and safety laws and regulations governing many of these same types of activities. Outside of the United States, there are countries and provincial, regional, tribal or local jurisdictions therein where we are conducting business that also have, or may be developing, regulatory initiatives or analogous controls that regulate our environmental-related activities. While the legal requirements imposed in foreign countries or jurisdictions therein may be similar in form to U.S. laws and regulations, in some cases, the actual implementation of these requirements may impose additional, or more stringent, conditions or controls that can significantly restrict, delay or cancel the permitting, development or expansion of a project or significantly increase the cost of doing business. Any failure by us to comply with these laws, regulations and regulatory initiatives or controls may result in the assessment of sanctions, including administrative, civil, and criminal penalties; the imposition of investigatory, remedial, and corrective action obligations or the incurrence of capital expenditures; the occurrence of restrictions, delays or cancellations in the permitting, development or expansion of projects; and the issuance of injunctions restricting or prohibiting some or all of our activities in a particular area. Certain environmental laws also provide for citizen suits, which allow environmental organizations to act in place of the government and sue operators for alleged violations of environmental laws. We have incurred and will continue to incur operating and capital expenditures, some of which may be material, to comply with environmental and occupational health and safety laws and regulations. Historically, our environmental and worker safety compliance costs have not had a material adverse effect on our results of operations. However, there can be no assurance that such costs will not be material in the future or that such future compliance will not have a material adverse effect on our business and operational results.

We own, lease or operate numerous properties that have been used for crude oil and natural gas wellsite support services for many years. We also have acquired certain properties supportive of oil and natural gas activities from third parties whose actions with respect to the management and disposal or release of hydrocarbons, hazardous substances or wastes at or from such properties were not under our control prior to acquiring them. Under environmental laws and regulations, we could incur strict joint and several liability for remediating hydrocarbons, hazardous substances or wastes disposed of or released by prior owners or operators. We also could incur costs related to the clean-up of third-party sites to which we sent regulated substances for disposal or to which we sent equipment for cleaning, and for damages to natural resources or other claims related to releases of regulated substances at or from such third-party sites.

Over time, both in the United States and in foreign countries, the trend in environmental and occupational health and safety laws and regulations is to typically place more restrictions and limitations on activities that may adversely affect the environment or expose workers to injury. Consequently, any new or amended legal requirement that may arise in the future to address potential environmental, health or safety-related concerns including, for example, as a result of oil and natural gas development in close proximity to occupied structures or environmentally-sensitive lands or recreational areas, could have a material adverse effect on our business, results of operations and financial position. While we maintain insurance coverage for certain environmental and occupational health and safety risks that we believe is consistent with insurance coverage held by other similarly situated industry participants, our insurance does not cover any penalties or fines that may be issued by a government authority. In addition, it is possible that other developments, such as stricter and more comprehensive environmental and occupational health and safety laws and regulations, claims for damages to property or persons or disruption of our customers' operations resulting from our actions or omissions, and imposition of penalties due to our operations could have a material adverse effect on us and our results of operations. See Risk Factors under Part I, Item 1A of this Form 10‑K for further discussion on environmental laws and regulations, including with respect to hydraulic fracturing; ozone standards, induced seismicity regulatory developments; climate change, including methane or other GHG emissions; storage and use of explosives; offshore drilling and related regulatory developments, including with respect to decommissioning obligations; and other risks or regulations relating to environmental protection.

-13-

Item 1A. Risk Factors

The risks described in this Annual Report on Form 10‑K are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition or future results.

Demand for the majority of our products and services is substantially dependent on the levels of expenditures by companies in the oil and natural gas industry. Lower oil and natural gas prices since 2014 have significantly reduced the demand for our products and services and the prices we are able to charge. This has had and may continue to have a material adverse effect on our financial condition and results of operations.

Demand for most of our products and services depends substantially on the level of expenditures by companies in the oil and natural gas industry. Lower oil and natural gas prices since 2014 have caused a reduction in most of our customers' drilling, completion and other production activities and related spending on our products and services. The reduction in demand from our customers has resulted in an oversupply of many of the services and products we provide, and such oversupply has substantially reduced the prices we can charge our customers for many of our products and services. Although oil prices improved since the trough in 2016, these price improvements have not resulted in significant global improvements in the demand for our products and services or the prices we are able to charge. If oil prices remain persistently low or decline further, our customers' activity levels and spending, along with the prices we charge, could worsen. In addition, a continuation or worsening of these conditions may result in a material adverse impact on certain of our customers' liquidity and financial position, resulting in further spending reductions, delays in the collection of amounts owing to us and similar impacts. These conditions have had, and may continue to have, an adverse impact on our financial condition, results of operations and cash flows, and it is difficult to predict how long the current depressed commodity price environment will continue.

While conditions in our industry improved in 2018, particularly in the shale resource plays in the United States, crude oil prices again declined significantly beginning in the fourth quarter of 2018. Given the historical volatility of crude oil prices, there remains a degree of risk that prices could remain highly volatile due to increases in global inventory levels, increasing domestic or international crude oil production, trade tensions with China, sanctions on Iranian production and tensions with Iran, civil unrest in Libya and Venezuela, increasing price differentials between markets, slowing growth rates in China and other global regions, use of alternative fuels, improved vehicle fuel efficiency, a more sustained movement to electric vehicles and/or the potential for ongoing supply/demand imbalances. If oil prices remain low or decline further, we could encounter difficulties such as an inability to access needed capital on attractive terms or at all, the incurrence of asset impairment charges, the inability to meet financial ratios contained in our debt agreements, the need to reduce our capital spending and other similar impacts. For example, our reduced EBITDA during recent periods resulted in our inability to access the full borrowing capacity available under our Revolving Credit Facility as a result of the maximum leverage ratio covenant. As more fully disclosed in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations under the heading "Liquidity, Capital Resources and Other Matters," we discuss our expectations regarding liquidity and covenant compliance for 2020.

Many factors affect the supply of and demand for oil and natural gas and, therefore, influence product prices, including:

• | the level of drilling and completion activity; |

• | the level of oil and natural gas production; |

• | the levels of oil and natural gas inventories; |

• | depletion rates; |

• | worldwide demand for oil and natural gas; |

• | the expected cost of finding, developing and producing new reserves; |

• | delays in major offshore and onshore oil and natural gas field permitting or development timetables; |

• | the availability of attractive offshore and onshore oil and natural gas field prospects that may be affected by governmental actions or environmental activists that may restrict development; |

• | the availability of transportation infrastructure for oil and natural gas, refining capacity and shifts in end-customer preferences toward fuel efficiency and the use of natural gas; |

• | public health crises, such as the coronavirus outbreak at the beginning of 2020, which could impact the global economy; |

• | global weather conditions and natural disasters; |

• | worldwide economic activity including growth in developing countries; |

-14-

• | national government political requirements, including the ability and willingness of OPEC to set and maintain production levels and prices for oil and government policies which could nationalize or expropriate oil and natural gas exploration, production, refining or transportation assets; |

• | shareholder activism or activities by non-governmental organizations to limit or cease certain sources of funding for the energy sector or restrict the exploration, development and production of oil and natural gas; |

• | the impact of armed hostilities involving one or more oil producing nations; |

• | rapid technological change and the timing and extent of development of energy sources, including liquefied natural gas or alternative fuels; |

• | environmental and other governmental laws and regulations; and |

• | domestic and foreign tax policies, including those regarding tariffs and duties. |

In response to lower oil prices, many of our customers have reduced or delayed their capital spending, which reduced the demand for our products and services and exerted downward pressure on the prices paid for our products and services. Although some of our customers increased their 2019 capital expenditure budgets, these customers are still spending significantly less than their pre-2015 levels. Additionally, if oil prices remain at current levels or decline further, these customers may further reduce their spending levels. We expect that we will continue to encounter weakness in the demand for, and prices of, our products and services until commodity prices stabilize at higher levels and our customers' capital spending increases. Any prolonged reduction in the overall level of exploration and production activities, whether resulting from changes in oil and natural gas prices or otherwise, could materially adversely affect our financial condition, results of operations and cash flows in many ways including by negatively affecting:

• | our equipment utilization, revenues, cash flows and profitability; |

• | our ability to obtain additional capital to finance our business and the cost of that capital; and |

• | our ability to attract and retain skilled personnel. |

Given the cyclical nature of our business, a severe prolonged downturn could negatively affect the value of our goodwill and other intangible assets.

As of December 31, 2019, goodwill and other intangible assets represented 28% and 13%, respectively, of our total assets. We record goodwill when the consideration we pay in acquiring a business exceeds the fair market value of the tangible and separately measurable intangible net assets of that business. We are required to at least annually review the goodwill and other intangible assets of our applicable reporting units (Completion Services, Downhole Technologies and Offshore/Manufactured Products) for impairment in value and to recognize a non-cash charge against earnings causing a corresponding decrease in stockholders' equity if circumstances, some of which are beyond our control, indicate that the carrying amounts will not be recoverable. In the fourth quarter of 2019, for example, we recognized a goodwill impairment charge of $165 million in our Downhole Technologies reporting unit due to, among other factors, a reduction in our near-term outlook for demand related to our short-cycle products and services in the U.S. shale play regions. It is possible that we could recognize goodwill or other intangible assets impairment losses in the future if, among other factors:

• | global economic and industry conditions deteriorate; |

• | the outlook for future profits and cash flow for any of our reporting units deteriorate further as the result of many possible factors, including, but not limited to, increased or unanticipated competition, lack of technological development, further reductions in customer capital spending plans, loss of key personnel, adverse legal or regulatory judgment(s), future operating losses at a reporting unit, downward forecast revisions, or restructuring plans; |

• | domestic and/or foreign income tax rates increase, or regulations change; |

• | costs of equity or debt capital increase; |

• | valuations for comparable public companies or comparable acquisition valuations deteriorate; or |

• | our stock price experiences a sustained decline. |

Laws, regulations and other regulatory initiatives regarding hydraulic fracturing could increase our costs of doing business and result in additional operating restrictions, delays or cancellations in the completion of oil and natural gas wells, or possible bans on the performance of hydraulic fracturing that may reduce demand for our products and services and could have a material adverse effect on our business, results of operations and financial condition.

Although we do not directly engage in hydraulic fracturing, a material portion of our Completion Services, Downhole Technologies and Offshore/Manufactured Products operations support many of our oil and natural gas exploration and production customers in such activities. Hydraulic fracturing is an important and commonly used process for the completion of oil and natural

-15-

gas wells in targeted subsurface formations with low permeability, such as shale formations, and involves the pressurized injection of water, sand or other proppants and chemical additives into rock formations to stimulate oil and natural gas production.

Hydraulic fracturing onshore in the United States is typically regulated by state oil and natural gas commissions and similar agencies. However, the practice continues to attract considerable public, scientific and governmental attention in certain parts of the country, resulting in increased scrutiny and regulation, including by federal agencies.

For example, in 2016, the EPA released its final report on the potential impacts of hydraulic fracturing on drinking water resources, concluding that "water cycle" activities associated with hydraulic fracturing may impact drinking water resources under certain circumstances. Additionally, Congress has from time to time considered legislation to provide for federal regulation of hydraulic fracturing in the United States and to require disclosure of the chemicals used in the hydraulic fracturing process. Due primarily to the threat of climate change arising from GHG emissions, certain candidates seeking the office of President of the United States in 2020 have pledged to take actions banning hydraulic fracturing of oil and natural gas.

At the state level, some states have adopted, and other states are considering adopting, legal requirements that could impose new or more stringent permitting, public disclosure or well construction requirements on hydraulic fracturing activities, including states where we or our customers operate, in addition to assessing more taxes, fees or royalties on production, or otherwise limiting the use of the technique. For example, in April 2019, the Governor of Colorado signed Senate Bill 19-181 into law, which legislation, among other things, revises the mission of the state oil and gas agency from fostering energy development in the state to instead focusing on regulating the oil and natural gas industry, in a manner that is protective of public health and safety and the environment, as well as authorizing cities and counties to regulate oil and natural gas operations within their jurisdiction as they do other developments. Among other things, the state oil and gas agency will consider enhanced safety and environmental protections during well development operations, including drilling and hydraulic fracturing activities. States could also elect to place prohibitions on hydraulic fracturing, following the approach taken by the States of Vermont, Maryland and New York. Local governments may seek to adopt ordinances within their jurisdictions regulating the time, place or manner of drilling activities in general or hydraulic fracturing activities in particular.

In the event that new or more stringent federal, state or local legal restrictions relating to use of the hydraulic fracturing process in the United States are adopted in areas where our oil and natural gas exploration and production customers operate, those customers could incur potentially significant added costs to comply with requirements relating to permitting, construction, financial assurance, monitoring, recordkeeping, and/or plugging and abandonment, as well as could experience delays or cancellations in the pursuit of production or development activities, any of which could reduce demand for the products and services of each of our business segments and have a material adverse effect on our business, financial condition, and results of operations.

In countries outside of the United States, including provincial, regional, tribal or local jurisdictions therein where we conduct operations, there may exist similar governmental restrictions or controls on our customers' hydraulic fracturing activities, which, if such restrictions or controls exist or are adopted in the future, our customers may incur significant costs to comply with such requirements or may experience delays or cancellations in the permitting or pursuit of their operations, which could have a material adverse effect on our business, results of operations and financial condition.

Explosive incidents arising out of dangerous materials used in our business could disrupt operations and result in bodily injuries and property damages, which occurrences could have a material adverse effect our business, results of operations and financial conditions.

Our Downhole Technologies business operations include the licensing, storage and handling of explosive materials. Despite our use of specialized facilities to store and handle dangerous materials and our performance of employee training programs, the storage and handling of explosive materials could result in explosive incidents that temporarily shut down or otherwise disrupt our or our customers' operations or could cause restrictions, delays or cancellations in the delivery of our services. It is possible that such incidents could result in death or significant injuries to employees and other persons. Material property damage to us, our customers and third parties arising from an explosion or resulting fire could also occur. Any explosion could expose us to adverse publicity and liability for damages or cause production restrictions, delays or cancellations, any of which occurrences could have a material adverse effect on our operating results, financial condition and cash flows. Moreover, failure to comply with applicable requirements or the occurrence of an explosive incident may also result in the loss of our license to store and handle explosives, which would have a material adverse effect on our business, results of operations and financial conditions.

-16-

Legislative and regulatory initiatives related to induced seismicity could result in operating restrictions or delays in the drilling and completion of oil and natural gas wells that may reduce demand for our products and services and could have a material adverse effect on our business, results of operations and financial condition.