Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 000-27517

GAIAM, INC.

(Exact name of registrant as specified in its charter)

| COLORADO | 84-1113527 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

833 WEST SOUTH BOULDER ROAD

LOUISVILLE, CO 80027

(Address of principal executive offices, including zip code)

(303) 222-3600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Class A Common Stock, $.0001 par value | NASDAQ Stock Market LLC |

Securities registered pursuant to section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) YES ¨ NO x

The aggregate market value of the voting common equity held by non-affiliates of the registrant was approximately $98,969,728 as of June 30, 2015, based upon the closing price on the NASDAQ Global Market on that date. The registrant does not have non-voting common equity.

As of March 9, 2016, 19,130,681 shares of the registrant’s Class A common stock and 5,400,000 shares of the registrant’s Class B common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents (or portions thereof) are incorporated by reference into the Parts of this Form 10-K noted:

Part III incorporates by reference from the definitive proxy statement for the registrant’s 2016 Annual Meeting of Shareholders to be filed with the Commission pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this Form.

Table of Contents

Annual Report on Form 10-K

For the Fiscal Year Ended December 31, 2015

INDEX

| Page Number |

||||||

| 1 | ||||||

| Item 1. |

1 | |||||

| Item 1A. |

7 | |||||

| Item 1B. |

11 | |||||

| Item 2. |

11 | |||||

| Item 3. |

11 | |||||

| Item 4. |

12 | |||||

| 12 | ||||||

| Item 5. |

12 | |||||

| Item 6. |

13 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

16 | ||||

| Item 7A. |

24 | |||||

| Item 8. |

25 | |||||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

52 | ||||

| Item 9A. |

52 | |||||

| Item 9B. |

52 | |||||

| 53 | ||||||

| Item 10. |

53 | |||||

| Item 11. |

53 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

53 | ||||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

53 | ||||

| Item 14. |

53 | |||||

| 54 | ||||||

| Item 15. |

54 | |||||

| 57 | ||||||

Table of Contents

| Item 1. | Business |

Our Business

Since its start in 1996, Gaiam has grown to become a leader in the markets for yoga, fitness and wellness products and conscious content. Gaiam brands include Gaiam, focused on yoga and fitness; Gaiam Restore, focused on wellness; SPRI by Gaiam, focused on fitness; and Gaia, our global digital video subscription service.

We develop and market yoga and fitness accessories, apparel, and media under Gaiam’s brands. These products are sold primarily through major national retailers in the United States, Canada, Europe, and other countries, with placement in over 38,000 retail doors worldwide. We also sell our products through our digital partners, websites and e-commerce channels. Our products and services are targeted to all levels of yoga and fitness enthusiasts, including professionals. We believe that consumers are attracted to our products because of their design, functional characteristics, and our unique brand heritage. Our accessories include yoga mats, bags, straps and blocks, media content including digital media and apps, restorative and massage accessories such as rollers, resistance cords and balance balls, and various other offerings. Our comprehensive line of apparel includes pants, shorts, tops and jackets designed around yoga.

Gaia (formerly Gaiam TV), our digital subscription service, provides our members access to approximately 7,000 video titles, 90% of which are available exclusively to subscribers for digital streaming on most Internet-connected devices anytime, anywhere.

Recent Developments

Our wholly-owned subsidiary Gaia, Inc. (“Gaia”) filed a registration statement on Form 10 in connection with the previously announced proposed separation of the Gaia segment from the Gaiam Brand segment into two separate publicly traded companies. The proposed tax-free spin-off is expected to occur through a distribution to Gaiam, Inc.’s shareholders of all the stock of Gaia. Gaia will hold all of the assets and liabilities of the Gaia segment, provided the spin-off happens. The Gaiam Brand segment will remain with Gaiam, Inc. after the distribution. The completion of the separation is subject to satisfaction of several conditions. Furthermore, our board of directors has the right and ability, in its sole discretion, to abandon the proposed separation at any time before the distribution date. As a result, there can be no assurance that the separation will occur. Gaia filed the final amendment to its Form 10 on February 17, 2016. Prior to consummating the proposed tax-free spin-off of the subscription business, our board of directors believes it is appropriate to review possible funding structures, enhancements and alternatives for its two primary business units and its eco-travel subsidiary, to maximize shareholder value. The board of directors expects to complete the review process by the end of March, while Gaia finalizes its NASDAQ trading arrangements. The Company does not plan to comment further regarding the review process unless disclosure is legally required.

Our Heritage

Our heritage dates back to 1984 when our founder and Chairman, Jirka Rysavy, emigrated from Czechoslovakia to Boulder, CO and founded natural-food store concept Crystal Market (later Wild Oats), recycled-office products company Corporate Express (which was sold with $4.5 billion in revenues, and is now Staples), and Gaiam.

Gaiam has developed a reputation for quality and innovation that has helped elevate the practice and visibility of yoga, fitness and wellness and positively changed the way consumers interact and look at the world. Our long history and experience gives us a unique authenticity in the market.

Our Values

Gaiam adheres to values that are aligned with our customers. This creates loyalty to our brands, above and beyond their appreciation for the quality, design and effectiveness of our products. Authenticity and commitment to our core values are at the center of what we strive to achieve.

We also have a strong sense of corporate citizenship and contribution to our communities. We strive to respect our environment, to promote diversity and fulfillment among our employees, to coach talent and support those in need when and where we are able to.

1

Table of Contents

Our Brands

Our brands reflect our commitment to designing innovative, high quality and affordable products that enhance our customers’ enjoyment of their yoga, fitness and wellness practices.

Gaiam is our main brand for yoga, fitness and wellness accessories, apparel, and media. Launched with our company’s founding, Gaiam started with yoga videos in the late 1990s, and has since expanded to include a full line of apparel, yoga mats, yoga mat bags, yoga blocks and straps, yoga and fitness props, balance balls, bags, and various other accessories. The brand addresses the needs of all levels of yoga practitioners with a high-quality and stylish product assortment. We have successfully leveraged the brand’s authenticity and heritage into wellness and active sitting products, including our balance ball chair, and fitness kits. We actively research and test new product concepts under the Gaiam brand, and have the ability to create new sub-brands like Gaiam Restore when the opportunity is significant.

Gaiam Restore is about empowering tools to get our customers back to their healthiest, most flexible selves. We launched the Restore sub-brand in 2012 when we recognized growing consumer interest in self-care. The Restore line helps enhance athletic performance, improve flexibility, boost range of motion and combat muscle soreness. The product line consists of foam rollers, foot rollers, massage kits, stretch cords and straps, pressure point massagers, hand and grip therapy accessories, trigger point massagers and various other products and accessories. Our substantial Restore product set enables us to provide a complete store-within-store experience to our retail partners, giving their customers a trusted source for both general and condition-specific wellness products.

SPRI by Gaiam is a leading manufacturer and distributor of professional fitness accessories, which we acquired in 2008. Founded over 30 years ago, SPRI first pioneered rubber resistance exercise products and has since expanded into many other categories of fitness equipment. Through its network of fitness professionals and advisors, SPRI has remained on the cutting edge of today’s exercise trends including our recent release of SPRI CrossTrain, a line of accessories for functional cross training. We are expanding our educational content through the recently redesigned website SPRI.com, in addition to growing live course programming. These efforts support and educate the market on the effective use of our products, in addition to influencing new trends. Historically, we marketed SPRI products through professional channels, trainers and gyms, and through specialty fitness retail stores. In 2012, we began to market the products through our extensive network of sporting goods and select mass market retailers.

Gaia is a global subscription video streaming service with approximately 7,000 titles focused on yoga, health and longevity, seeking truth, spiritual growth and conscious films & series. Its content caters to a unique and underserved subscriber base and is available to our subscribers across most Internet connected devices anytime, anywhere, commercial free. The subscription also allows downloading and viewing of files from the library without being actively connected to the internet. Subscribers have unlimited access to a vast library of inspiring films, personal growth related content, cutting edge documentaries, interviews, yoga classes, and more – 90% of which is available exclusively for streaming to our subscribers.

Our Products

We have a long history of technical innovation and product development, with over 22 patents and 2 patents pending and hundreds of new product introductions since our start in 1996. Our employees’ passion and intimacy with yoga, fitness and wellness provides a significant advantage that we believe will help drive our Company to new levels.

2

Table of Contents

Examples of our products include:

3

Table of Contents

Our Strategy

We seek to generate sustainable and profitable growth by leveraging our leadership position and brand awareness to expand our business in the following ways:

Streamline and Focus Our Business – During 2013, we sold our non-Gaiam branded entertainment media distribution operations, discontinued our direct response television marketing operations, and sold virtually all our investment in Real Goods Solar, Inc. (“RGSE”) in order to restructure our business around our yoga, fitness, and wellness products as well as Gaia. We believe that maintaining focus and discipline will be critical as we seek to grow our leadership position and brands within these markets.

Extend Our Brand Into New Categories – Gaiam enjoys strong national brand awareness, and we believe that we have successfully demonstrated our ability to move into complementary and adjacent product categories. For example, our Gaiam Restore product line represented a step toward wellness, and has grown considerably since its launch in 2012. Similarly, our SPRI CrossTrain product line was a natural evolution of the SPRI brand, and is now carried in major retailers in the US.

In 2015, we launched a line of Gaiam branded yoga apparel that has provided access to the large and growing athletic apparel market. We believe that our brand combined with a favorable competitive environment in this segment of the market will become a significant part of our growth in the coming years.

Additionally, we are increasing our presence in the home and office with active sitting products. The Gaiam balance ball chair is a widely recognized product and forms the base of our active sitting strategy. With the continued success of our balance ball chair and the recent news coverage on the health issues associated with sitting for extended periods of time, we are designing a line of active sitting products that will further extend our brand.

Attract New Demographics – We believe that the growing interest in yoga, fitness, and wellness has created an opportunity for us to use our core brand assets to attract men and youth to these disciplines. Historically underrepresented in our disciplines and our customer base, both demographics are now a focus for our marketing and product development efforts. We plan to utilize our expertise in product development, merchandising, and content creation to develop unified sets of product and media content that appeal to men and children, and to sell these products through our existing wide retail distribution network and website.

Extend Our International Distribution Footprint – We believe that Gaiam has the ability to be the global brand for yoga, fitness and wellness by actively pursuing international expansion. International sales represented approximately 4% of our revenues in 2015 and we believe there is significant opportunity to address the yoga, fitness, and wellness market abroad and to do so as successfully as we have addressed it in the United States.

Grow our Retail Footprint – We currently have 19,000 branded stores-within-store presentations and believe the product category and demographic expansion strategies above will help us to grow our sales with existing customers and to enter new retail channels including department stores, grocery and drug stores. We believe that many retailers recognize an opportunity in the health and wellness lifestyle market, and are expanding their product mix in order to capitalize on this trend. Additionally, we launched our SPRI brand in retail during 2012, and are continuing to expand its penetration. As of December 31, 2015, SPRI was represented in approximately 4,500 U.S. retail doors.

Connect With Our Customers – Our business and customers continue to evolve and so will the way we engage with them. We are evolving our e-commerce experience to focus on engaging our target consumers through digital content and social and mobile marketing. As part of this strategy, in 2014, we acquired the Yoga Studio app, a highly rated and successful yoga instruction app, which we will continue to develop and leverage as a point of brand engagement. As of the end of 2015, Yoga Studio was the leading yoga app with over 1 million downloads. Expanding our reach into wellness, we created and launched Meditation Studio, an iOS app offering original guided meditations in 2015.

We recently launched the GaiamPro.com website, which enables us to better connect with the yoga and fitness studio and practitioner market – a key step in growing our brand presence within these highly influential channels. We have also completely redesigned our Gaiam.com and SPRI.com websites to focus on brand engagement across various devices, including tablet and mobile.

These efforts are all grounded in our belief that consumers increasingly seek direct brand interactions, through engaging content and digital interactions. We will continue to develop and evolve better ways to connect with our consumers through our consumer channels and our retail partners.

Build Gaia – Our core Gaia strategy is to grow our subscriber base domestically and internationally by expanding our unique and exclusive content library, enhancing our user interface and extending our streaming service to new Internet-connected devices as they are developed.

4

Table of Contents

Our content is focused on yoga, health and longevity, seeking truth, spiritual growth and conscious films & series. This media content is specifically targeted to a unique customer base which is interested in alternatives to the content provided by mainstream media. We have been able to grow these content options both organically through our own productions and through strategic acquisitions. In addition, through our investments in our streaming video technology and our user interface, we have been able to expand the many ways our subscription customer base can access our unique library of media titles.

Complement our Existing Business with Selective Strategic Acquisitions – Our growth strategy is not dependent on acquisitions. However, we will consider acquiring complementary branded businesses that strengthen our market position by expanding our product offerings, geographical reach or channel distribution. We often retain acquired company’s management to drive front-end business functions, such as creative presentation and marketing, while consolidating operational functions under our existing infrastructure where we can realize economies of scale.

Our Operations

Sales Channels, Product Development and Sourcing

We sell our branded products across various sales channels. We use our direct-to-consumer channel to test products before we distribute them through our retail channel. Because we use a multi-channel approach to our business, we are able to leverage product development costs across all channels of our business.

Our proprietary offerings are designed by our development team and sourced both domestically and internationally. We utilize third- party suppliers that produce our products to our specifications. We design our products to promote and support our customers’ healthy lifestyles. We also screen the environmental and social responsibility of our suppliers. In order to minimize risk, we often identify an alternate supplier for our products in a separate location.

Established Infrastructure

We have a distribution center centrally located near Cincinnati, Ohio. This distribution center provides fulfillment for much of our current domestic business needs and has the capacity to support the growth of our business. The center’s central U.S. location allows us to achieve shipping cost efficiencies to most locations. The center is also located within 30 minutes of several major shipping company hubs. We use a supply chain management system that supports our entire operation, including fulfillment, inventory management, and customer service.

Our Reporting Segments

We have two reportable segments: the Gaiam Brand segment, and the Gaia segment. The Gaiam Brand segment includes all of our yoga, fitness, and wellness product and media distributed through our website, apps, retail network, and catalogs, and also includes our eco-travel business. The Gaia segment includes our global digital video subscription service. During 2015, the Gaiam Brand and the Gaia segments represented 92.8% and 7.2% of our net revenues, respectively.

Our Gaiam Brand segment is dependent upon a few major customers for a significant portion of its revenues. The following Gaiam Brand segment customers make up 10% or more of our total revenues. No other customer accounted for 10% or more of our total net revenue. The loss of either of these customers would have a material adverse effect on our business.

| 2015 | 2014 | 2013 | ||||||||||

| Target |

21.8 | % | 29.3 | % | 32.1 | % | ||||||

| Kohl’s |

18.1 | % | 4.0 | % | — | |||||||

See further information about our reporting segments in Note 16 to the Consolidated Financial Statements.

Our Competition

Our business and brands are benefiting from the convergence of function and fashion in the yoga and fitness apparel, and equipment space. We believe consumer purchase decisions are driven by a need for solution-oriented products and a desire to create a particular lifestyle perception through distinctive aesthetics. A number of highly successful brands including Lululemon, Under Armour, and Nike have recognized and capitalized on this convergence. Primary growth drivers in our business include products that provide a high level of performance or comfort, that exhibit consistent, attractive design characteristics, and are affordable.

5

Table of Contents

The markets for our products are highly competitive. In each of our geographic markets, we face significant competition from numerous competitors, some of which are larger than us and have greater financial, marketing and operational resources with which to compete, and others that are smaller with fewer resources, but that may be deeply entrenched in local markets or have established themselves as niche category leaders. Some of our large wholesale customers also market competitive yoga, fitness and wellness apparel, accessories and equipment under their own private labels. In addition, our direct-to-consumer channels expose us to branded competitors who operate retail stores, as well as competitors who sell product online.

In addition to competing for end-consumer and wholesale market share, we also compete for manufacturing capacity of independent factory groups, primarily in Asia; and for experienced management, staff and suppliers to lead, operate and support our global business processes. Each of these areas of competition requires distinct operational and relational capabilities and expertise in order to create and maintain long-term competitive advantages.

Competitive Advantage

We believe our primary competitive advantages are:

| • | Brand awareness |

| • | Product design and innovation |

| • | Product quality |

| • | Management experience |

| • | Exclusive content library |

| • | Technical platform for continuity |

| • | Full onsite content production facilities |

We believe our brand is recognized as a leader in our industry. With a long history in the yoga, fitness and wellness market, our reputation and longevity make us the first choice for many consumers. Our expertise enables us to produce and market unique and innovative products under our core brands using materials and designs that take advantage of the newest health trends. Our employees leverage their own expertise and that of an external network of experts and advisors to continually research the trends in all of our markets, allowing us to continuously address the evolving needs of our consumers.

Discontinued Operations

In the fourth quarter of 2013, we sold our non-Gaiam-branded entertainment media distribution operations (“GVE”) and discontinued our direct response television marketing operations (“DRTV”). We now report these businesses as discontinued operations, and, accordingly, we have reclassified their financial results for all periods presented to reflect them as such. Unless otherwise noted, discussions in this Form 10-K pertain to our continuing operations.

Our Employees

As of March 9, 2016, we employed approximately 286 full-time and 10 part-time or seasonal individuals. None of our employees are covered by a collective bargaining agreement.

Regulatory Matters

A number of existing and proposed laws restrict disclosure of consumers’ personal information, which may make it more difficult for us to generate additional names for our direct marketing, and restrict our ability to send unsolicited electronic mail or printed materials. Although we believe we are generally in compliance with current laws and regulations and that these laws and regulations have not had a significant impact on our business to date, it is possible that existing or future regulatory requirements will impose a significant burden on us.

We generally collect sales taxes only on sales to residents of states in which we have nexus. Currently, we collect sales taxes on certain sales to residents of California, Colorado, Illinois, New York, New Jersey, Ohio, and Texas. A number of legislative proposals have been made at the federal, state and local level, and by foreign governments, that would impose additional taxes on the sale of goods and services over the Internet, and certain states have taken measures to tax Internet-related activities. If legislation is enacted that requires us to collect sales taxes on sales to residents of other states or jurisdictions, our direct to consumer sales channels may be adversely affected. Our business is also subject to a number of other governmental regulations, including the Mail or Telephone Order Merchandise Rule and related regulations of the Federal Trade Commission. These regulations prohibit unfair methods of competition and unfair or deceptive acts or practices in connection with mail and telephone order sales and require sellers of mail and telephone order merchandise to conform to certain rules of conduct with respect to shipping dates and shipping delays. We are also subject to regulations of the U.S. Postal Service and various state and local consumer protection agencies relating to matters such as advertising, order solicitation, shipment deadlines and customer refunds and returns. In addition, merchandise that we import is subject to import and customs duties and, in some cases, import quotas.

6

Table of Contents

Seasonality

See the “Quarterly and Seasonal Fluctuations” section of Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, for information pertaining to the seasonal aspects of our business.

Website and Available Information

Our corporate website at gaiam.com provides information about us, our history, goals and philosophy, as well as certain financial reports and corporate press releases. Our gaiam.com website also features a library of information and articles on personal development and healthy lifestyles, along with an extensive offering of products, services and media. We believe our website provides us with an opportunity to deepen our relationships with our customers and investors, educate them on a variety of issues, and improve our service. As part of this commitment, we have a link on our corporate website to our Securities and Exchange Commission filings, including our reports on Form 10-K, 10-Q and 8-K and amendments thereto. We make those reports available through our website, free of charge, as soon as reasonably practicable after these reports are filed with the Securities and Exchange Commission.

Additional information about our products and services can be found at SPRI.com and Gaia.com. We have included our website addresses only as inactive textual reference, and the information contained on our website is not incorporated by reference into this Form 10-K.

| Item 1A. | Risk Factors |

We wish to caution you that there are risks and uncertainties that could cause our actual results to be materially different from those indicated by forward looking statements that we make from time to time in filings with the Securities and Exchange Commission, news releases, reports, proxy statements, registration statements and other written communications as well as oral forward looking statements made from time to time by our representatives. These risks and uncertainties include those risks described below of which we are presently aware. Historical results are not necessarily an indication of future results. The risk factors below discuss important factors that could cause our business, financial condition, operating results and cash flows to be materially adversely affected.

We may be subject to litigation which, if adversely determined, could cause us to incur substantial losses.

From time to time during the normal course of operating our businesses, we are subject to various litigation claims and legal disputes. Some of the litigation claims may not be covered under our insurance policies, or our insurance carriers may seek to deny coverage. As a result, we might also be required to incur significant legal fees, which may have a material adverse effect on our financial position. In addition, because we cannot accurately predict the outcome of any action, it is possible that, as a result of current and/or future litigation, we will be subject to adverse judgments or settlements that could significantly reduce our earnings or result in losses.

We have had losses, and we cannot assure future profitability

We have reported net losses of $11.7 million, $9.9 million and $22.8 million in 2015, 2014 and 2013, respectively. We cannot assure you that we will operate profitably in future periods and, if we do not, we may not be able to meet any future debt service requirements, working capital requirements, capital expenditure plans, production slate, acquisition and releasing plans or other cash needs. Our inability to meet those needs could have a material adverse effect on our business, financial condition, operating results, liquidity and prospects.

Changes in general economic conditions could have a material impact on our business

Changes in overall economic conditions that impact consumer spending could impact our results of operations. Future economic conditions affecting disposable income such as employment levels, consumer confidence, credit availability, business conditions, stock market volatility, inflation, acts of terrorism, threats of war, and interest and tax rates could reduce consumer spending or cause consumers to shift their spending away from our products. If the economic conditions and performance of the retail and media environment worsen, we may experience material adverse impacts on our business, operating results and financial condition.

Increased competition could impact our financial results

We believe that the healthy lifestyles market includes thousands of small, local and regional businesses. Some smaller businesses may be able to more effectively personalize their relationships with customers, thereby gaining a competitive advantage. Although we believe that we do not compete directly with any single company that offers our entire range of merchandise and services, within each category we have competitors and we may face competition from new entrants. Some of our competitors or our potential competitors may have greater financial and marketing resources and greater brand recognition. In addition, larger, well-established and well-financed entities may acquire, invest in or form joint ventures with our competitors. Increased competition from these or other competitors could negatively impact our business.

7

Table of Contents

Changing consumer preferences may have an adverse effect on our business

We target consumers who assign high value to personal development, healthy lifestyles, responsible media, and the environment. A decrease of consumer interest in purchasing goods and services that promote the values we espouse would materially and adversely affect our customer base and sales revenues and, accordingly, our financial prospects. Further, consumer preferences and product trends are difficult to predict. Our future success depends in part on our ability to anticipate and respond to changes in consumer preferences and we may not respond in a timely or commercially appropriate manner to such changes. Failure to anticipate and respond to changing consumer preferences and product trends could lead to, among other things, lower sales of our products, increased merchandise returns and lower margins, which could have a material adverse effect on our business.

Our strategy of offering branded products could lead to inventory risk and higher costs

An important part of our strategy is to feature branded products. These products are sold under our brand names and are manufactured to our specifications. We expect our reliance on branded merchandise to increase. The use of branded merchandise requires us to incur costs and risks relating to the design and purchase of products, including submitting orders earlier and making larger initial purchase commitments.

In addition, the use of branded merchandise limits our ability to return unsold products to vendors, which can result in higher markdowns in order to sell excess inventory. Our commitment to customer service typically results in our keeping a high level of merchandise in stock so we can fill orders quickly. Consequently, we run the risk of having excess inventory, which may also contribute to higher markdowns. Our failure to successfully execute a branded merchandise strategy or to achieve anticipated profit margins on these goods, or a higher than anticipated level of overstocks, may materially adversely affect our revenues.

We offer our customers liberal merchandise return policies. Our consolidated financial statements include a reserve for anticipated merchandise returns, which is based on historical return rates. It is possible that actual returns may increase as a result of factors such as the introduction of new merchandise, changes in merchandise mix or other factors. Any increase in our merchandise returns will correspondingly reduce our revenues and profits.

Acquisitions and new initiatives may harm our financial results

We have historically expanded our operations in part through strategic acquisitions and through new initiatives that we generate. We cannot accurately predict the timing, size and success of these efforts. Our acquisition and new initiative strategies involve significant risks that could inhibit our growth and negatively impact our operating results, including the following: our ability to identify suitable acquisition candidates or new initiatives at acceptable prices; our ability to complete the acquisitions of candidates that we identify or develop our new initiatives; our ability to compete effectively for available acquisition opportunities; increases in asking prices by acquisition candidates to levels beyond our financial capability or to levels that would not result in the returns required by our acquisition criteria; diversion of management’s attention to expansion efforts; unanticipated costs and contingent liabilities associated with acquisitions and new initiatives; failure of acquired businesses or new initiatives to achieve expected results; our failure to retain key customers or personnel of acquired businesses and difficulties entering markets in which we have no or limited experience. In addition, the size, timing and success of any future acquisitions and new initiatives may cause substantial fluctuations in our operating results from quarter to quarter. Consequently, our operating results for any quarter may not be indicative of the results that may be achieved for any subsequent quarter or for a full fiscal year. These fluctuations could adversely affect the market price of our Class A common stock.

The loss of the services of our key personnel could disrupt our business

We depend on the continued services and performance of our senior management and other key personnel, particularly Jirka Rysavy and Lynn Powers, who intends to retire once a replacement is identified and transitioned into Gaiam. A loss of one or more of the members of our senior management or key personnel, without suitable replacements, could severely and negatively impact our operations. Our strategy of allowing the management teams of some acquired companies to continue to exercise significant management responsibility for those companies makes it important that we retain key employees, particularly the sales and creative teams, of the companies we might acquire. Hiring qualified management is difficult due to the limited number of qualified professionals in the industry in which we operate. Failure to attract and retain personnel, particularly management personnel, could materially harm our business, financial condition, and results of operations.

Our founder and chairman Jirka Rysavy has voting control over our company

Mr. Rysavy holds 100% of our 5,400,000 outstanding shares of Class B common stock and also owns 348,682 shares of Class A common stock. The shares of Class B common stock are convertible into shares of Class A common stock at any time. Each share of Class B common stock has ten votes per share, and each share of Class A common stock has one vote per share. Consequently, Mr. Rysavy holds approximately 74% of our voting stock and, thus, is able to exert substantial influence over us and to control matters requiring approval by our shareholders, including the election of directors, increasing our authorized capital stock, or a merger or sale of substantially all of our assets. As a result of Mr. Rysavy’s control of us, no change of control can occur without Mr. Rysavy’s consent.

8

Table of Contents

Our success depends on the value of our brand

Because of our reliance on sales of proprietary products, our success depends on our brand. Building and maintaining recognition of our brand are important for attracting and expanding our customer base. If the value of our brand were adversely affected, we cannot be certain that we would be able to attract new customers, retain existing customers or encourage repeat purchases, and if the value of our brand were to diminish, our revenues, results of operations and prospects would be adversely affected.

Our future cash flows may not be sufficient to meet our obligations and we may have difficulty obtaining financing

Our cash balance at December 31, 2015 was $13.8 million. Our subsidiary Boulder Road LLC has access to a $5.5 million revolving line of credit with a bank. Other than that, we presently do not have any financing arrangement in place to assist us in meeting our obligations. There can be no assurance in the future whether we will generate sufficient cash flow from operations to meet our obligations or whether we would be able to secure financing or other sources of funds, such as from the sale of our shelf registration stock, should the need arise.

Product liability claims against us could result in adverse publicity and potentially significant monetary damages

As a seller of consumer products, we may face product liability claims in the event that use of our products results in injuries. If such injuries or claims of injuries were to occur, we could incur monetary damages and our business could be adversely affected by any resulting negative publicity. The successful assertion of product liability claims against us also could result in potentially significant monetary damages and, if our insurance protection is inadequate to cover these claims, could require us to make significant payments from our own resources.

We are dependent on third party suppliers for the success of our proprietary products

We are dependent on the success of our proprietary products, and we rely on a select group of manufacturers to provide us with sufficient quantities to meet our customers’ demands in a timely manner, produce these products in a humane and safe environment for both their workers and the planet, maintain quality standards consistent with our brand, and meet certain pricing guarantees. Our overseas sourcing arrangements carry risks associated with products manufactured outside of the U.S., including political unrest and trade restrictions, currency fluctuations, transportation difficulties, work stoppages, and other uncertainties. In addition, a number of our suppliers are small companies, and some of these vendors may not have sufficient capital, resources or personnel to maintain or increase their sales to us or to meet our needs for commitments from them. The failure of our suppliers to provide sufficient quantities of our proprietary products could decrease our revenues, increase our costs, and damage our customer service reputation.

We rely on communications and shipping networks to deliver our products

Given our emphasis on customer service, the efficient and uninterrupted operation of order-processing and fulfillment functions is critical to our business. To maintain a high level of customer service, we rely heavily on a number of different outside service providers, such as printers, telecommunications companies and delivery companies. Any interruption in services from our principal outside service providers, including delays or disruptions resulting from labor disputes, power outages, human error, adverse weather conditions or natural disasters, could materially adversely affect our business. In addition, freight carriers must ship products that we source overseas to our distribution center, and a work stoppage or political unrest could adversely affect our ability to fulfill our customer orders.

Information systems upgrades or integrations may disrupt our operations or financial reporting

We continually evaluate and upgrade our management information systems, which are critical to our business. These systems assist in processing orders, managing inventory, purchasing and shipping merchandise on a timely basis, responding to customer service inquiries, and gathering and analyzing operating data by business segment, customer, and stock keeping unit (a specific identifier for each different product). We are required to continually update these systems. Furthermore, if we acquire other companies, we will need to integrate the acquired companies’ systems with ours, a process that could be time-consuming and costly. If our systems cannot accommodate our growth or if they fail, we could incur substantial expenses and our business could be adversely affected.

Additionally, success in e-commerce depends upon our ability to provide a compelling and satisfying shopping experience. To remain competitive, we must continue to enhance and improve the responsiveness, functionality and features of our online technology, and if we are unable to do this, our business could be adversely affected.

A material security breach could cause us to lose sales, damage our reputation or result in liability to us

Our computer servers may be vulnerable to computer viruses, physical or electronic break-ins and similar disruptions. We may need to expend significant additional capital and other resources to protect against a security breach or to alleviate problems caused by any breaches. Our relationships with our customers may be adversely affected if the security measures that we use to protect personal information such as credit card numbers are ineffective. We currently rely on security and authentication technology that we license from third parties. We may not succeed in preventing all security breaches and our failure to do so could adversely affect our business.

9

Table of Contents

Our systems may fail or limit user traffic, which would cause us to lose sales

We support a portion of our business through our call center in Louisville, Colorado. Even though we have back up arrangements, we are dependent on our ability to maintain our computer and telecommunications equipment in this center in effective working order and to protect against damage from fire, natural disaster, power loss, telecommunications failure or similar events. In addition, growth of our customer base may strain or exceed the capacity of our computer and telecommunications systems and lead to degradations in performance or systems failure. We have experienced capacity constraints and failure of information systems in the past that have resulted in decreased levels of service delivery or interruptions in service to customers for limited periods of time. Although we continually review and consider upgrades to our technical infrastructure and provide for system redundancies and backup power to limit the likelihood of systems overload or failure, substantial damage to our systems or a systems failure that causes interruptions for a number of days could adversely affect our business. Additionally, if we are unsuccessful in updating and expanding our infrastructure, including our call center, our ability to grow may be constrained.

Government regulation of the Internet and E-commerce is evolving and unfavorable changes could harm our business

We are subject to general business regulations and laws, as well as regulations and laws specifically governing the Internet and e-commerce. Such existing and future laws and regulations may impede the growth of the Internet or other online services. These regulations and laws may cover taxation, user privacy, pricing, content, copyrights, distribution, consumer protection, the provision of online payment services and quality of products and services. Many of the fundamental statutes and regulations applicable to our business were established before the adoption and growth of the Internet and e-commerce. There is lack of clarity on how existing laws and regulations governing issues such as property ownership, sales and other taxes and personal privacy apply to the Internet and e-commerce. Unfavorable resolution of these issues may harm our business.

Specifically, the application of indirect taxes (such as sales and use tax, value-added tax (VAT), goods and services tax, business tax and gross receipt tax) to e-commerce businesses such as ours and our customers is a complex and evolving issue. In many cases, it is not clear how existing tax laws and regulations apply to the Internet and e-commerce. In addition, governments are increasingly looking for ways to increase revenues, which has resulted in discussions about tax reform and other legislative action to increase tax revenues, including through indirect taxes. We generally collect sales taxes only on sales to residents of states in which we have nexus. Currently, we collect sales taxes on certain sales to residents of California, Colorado, Illinois, New York, New Jersey, Ohio, and Texas. A number of legislative proposals have been made at the federal, state and local level, and by foreign governments, that would impose additional taxes on the sale of goods and services over the Internet and certain states and other jurisdictions have taken measures to tax Internet-related activities. If legislation is enacted that requires us to collect taxes on sales to residents of other states or jurisdictions, sales in our direct to consumer businesses may be adversely affected. Further, a successful assertion by one or more states or other jurisdictions requiring us to collect taxes where we do not do so could result in substantial tax liabilities, including for past sales, as well as penalties and interest.

We may face legal liability for the content contained on our websites

We could face legal liability for defamation, negligence, copyright, patent or trademark infringement, personal injury or other claims based on the nature and content of materials that we publish or distribute on our websites. If we are held liable for damages for the content on our websites, our business may suffer. Further, one of our goals is for our websites to be trustworthy and dependable providers of information and services. Allegations of impropriety, even if unfounded, could therefore have a material adverse effect on our reputation and our business.

Relying on our centralized fulfillment center could expose us to losing revenue

Prompt and efficient fulfillment of our customers’ orders is critical to our business. Our facility near Cincinnati, Ohio handles a majority of our fulfillment functions and some customer-service related operations, such as returns processing. Many of our orders are filled and shipped from the Cincinnati facility. The balance is shipped by third party fulfillment centers or directly from suppliers. Because we rely on a centralized fulfillment center, our fulfillment functions could be severely impaired in the event of fire, extended adverse weather conditions, transportation difficulties or natural disasters. Because we recognize revenue only when we ship orders, interruption of our shipping could diminish our revenues.

We may face quarterly and seasonal fluctuations that could harm our business

Our revenue and results of operations have fluctuated and will continue to fluctuate on a quarterly basis as a result of a number of factors, including the timing of catalog offerings, timing of orders from retailers, recognition of costs or net sales contributed by new merchandise, fluctuations in response rates, fluctuations in paper, production and postage costs and expenses, merchandise returns, adverse weather conditions that affect distribution or shipping, shifts in the timing of holidays and changes in our merchandise mix. In particular, our net sales and profits have historically been higher during the fourth quarter holiday season. We believe that this seasonality will continue in the future.

10

Table of Contents

Postage and shipping costs may increase and therefore increase our expenses

We ship our products to our consumers and the cost of shipping is a material expenditure. Postage and shipping prices increase periodically and can be expected to increase in the future. Any inability to secure suitable or commercially favorable prices or other terms for the delivery of our merchandise could have a material adverse effect on our financial condition and results of operations.

Our business is subject to reporting requirements that continue to evolve and change, which could continue to require significant compliance effort and resources

Because our Class A common stock is publicly traded, we are subject to certain rules and regulations of federal, state and financial market exchange entities charged with the protection of investors and the oversight of companies whose securities are publicly traded. These entities, including the Public Company Accounting Oversight Board, the Securities and Exchange Commission and the NASDAQ, periodically issue new requirements and regulations and legislative bodies also review and revise applicable laws. As interpretation and implementation of these laws and rules and promulgation of new regulations continues, we will continue to be required to commit significant financial and managerial resources and incur additional expenses.

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

Our principal executive offices are located in Louisville, Colorado. Our fulfillment center is located in the Cincinnati, Ohio area. The following table sets forth certain information relating to our primary facilities:

| Primary Locations |

Size | Use | Lease Expiration | |||||

| Louisville, CO | 150,262 sq. ft. | Headquarters and studios | Owned | |||||

| Cincinnati, OH | 208,120 sq. ft. | Fulfillment center | June 2019 | |||||

| Libertyville, IL | 7,691 sq. ft. | Office | December 2016 | |||||

We rent to third parties approximately 63,450 square feet of our building space located in Colorado. Our existing fulfillment center lease has renewal options permitting the extension of the lease for up to an additional four years. We believe our facilities are adequate to meet our current needs and that suitable additional facilities will be available for lease or purchase when, and as, we need them.

| Item 3. | Legal Proceedings |

On August 13, 2014, Cinedigm Corp. and Cinedigm Entertainment Holdings, LLC (together, “Cinedigm”) initiated an arbitration proceeding with the American Arbitration Association under the Membership Interest Purchase Agreement, dated October 17, 2013, by and among Cinedigm and Gaiam and one of its subsidiaries (the “MIPA”). Cinedigm’s arbitration demand alleged that Gaiam owed Cinedigm approximately $12.9 million under the working capital adjustment mechanism included in the MIPA. In addition, Cinedigm claimed that Gaiam materially breached its representations and warranties under the MIPA, that Gaiam engaged in fraudulent and tortious acts in connection with the sale, and that Gaiam breached the terms of other agreements related to the transaction. The aggregate relief requested by Cinedigm exceeded $30.0 million and included unspecified compensatory damages, attorneys’ fees, costs and interest, and other relief. In response to the disputes, the Company accrued a litigation-related reserve of $3.0 million in 2014.

In a settlement agreement entered into on September 30, 2015, Cinedigm and Gaiam agreed to the following: (1) a mutual release of all claims, with only one exception (described immediately below), that the parties held against each other; (2) the commencement of a further arbitration to resolve Cinedigm’s single preserved claim that it did not receive all of the cash collected by Gaiam on Cinedigm’s behalf during the transition period following the sale (the “Cash Reconciliation Claim”); and (3) Gaiam would pay Cinedigm $2.3 million. In a settlement agreement made effective as of December 31, 2015, Cinedigm and Gaiam agreed to resolve the Cash Reconciliation Claim in exchange for a further payment by Gaiam to Cinedigm in the amount of $1.6 million.

As a result, all legal disputes between the parties have now been finally and fully settled. The parties’ settlements do not constitute an admission by either party of any liability or wrongdoing whatsoever. Gaiam entered into the settlement agreements in order to (i) eliminate the uncertainty and risk inherent in any litigation, (ii) significantly reduce the professional fees and costs that the litigation would require, and (iii) significantly reduce the distraction imposed by the process on management.

11

Table of Contents

During 2015, Gaiam recorded charges of $12.1 million which include a non-cash charge of $7.3 million for the working capital receivable due from Cinedigm. The expenses associated with the settlements and arbitration have all been included in Loss from discontinued operations in the accompanying condensed consolidated statements of operations.

From time to time, we are involved in legal proceedings that we consider to be in the normal course of business. Claimed amounts against us may be substantial but may not bear any reasonable relationship to the merits of the claim or the extent of any real risk of court or arbitral awards. We record accruals for losses related to those matters against us that we consider to be probable and that can be reasonably estimated. Although it is not feasible to predict the outcome of these matters with certainty, it is reasonably possible that some legal proceedings may be disposed of or decided unfavorably to us and in excess of the amounts currently accrued. Based on available information, in the opinion of management, settlements, arbitration awards and final judgments, if any, which are considered probable of being rendered against us in litigation or arbitration in existence at December 31, 2015 and can be reasonably estimated are reserved against or would not have a material adverse effect on our financial condition, results of operations or cash flows.

| Item 4. | Mine Safety Disclosures |

Not applicable.

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Stock Price History

Our Class A common stock is listed on the NASDAQ Global Market under the symbol “GAIA”. On March 9, 2016, we had 4,571 shareholders of record and 19,130,681 shares of $.0001 par value Class A common stock outstanding, and we had 5,400,000 shares of $.0001 par value Class B common stock outstanding, held by one shareholder.

The following table sets forth certain sales price data for our Class A common stock for the period indicated:

| High | Low | |||||||

| 2015 |

||||||||

| Fourth Quarter |

$ | 7.15 | $ | 5.94 | ||||

| Third Quarter |

$ | 7.25 | $ | 5.00 | ||||

| Second Quarter |

$ | 7.65 | $ | 6.14 | ||||

| First Quarter |

$ | 7.80 | $ | 6.05 | ||||

| 2014 |

||||||||

| Fourth Quarter |

$ | 7.85 | $ | 6.31 | ||||

| Third Quarter |

$ | 7.99 | $ | 6.44 | ||||

| Second Quarter |

$ | 8.76 | $ | 6.09 | ||||

| First Quarter |

$ | 7.36 | $ | 6.05 | ||||

Issuer Purchases of Registered Equity Securities

None.

Dividend Policy

No dividends were declared or paid during the years ended December 31, 2015 and 2014.

Sales of Unregistered Securities

None.

12

Table of Contents

Equity Compensation Plan Information

The following table summarizes equity compensation plan information for our Class A common stock at December 31, 2015:

| Plan Category |

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

Weighted average exercise price of outstanding options, warrants and rights |

Number of securities remaining available for future issuance under equity compensation plans |

|||||||||

| Equity compensation plans approved by security holders |

1,478,724 | $ | 6.19 | 1,281,169 | ||||||||

| Equity compensation plans not approved by security holders |

— | — | — | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

1,478,724 | $ | 6.19 | 1,281,169 | ||||||||

|

|

|

|

|

|

|

|||||||

Item 6. Selected Financial Data

We derived the selected consolidated statement of operations data and consolidated cash flow data for the years ended December 31, 2015, 2014 and 2013, and consolidated balance sheet data as of December 31, 2015 and 2014 set forth below from our audited consolidated financial statements, which are included elsewhere in this Form 10-K. We derived the selected consolidated statement of operations data and consolidated cash flow data for the years ended December 31, 2012 and 2011 and consolidated balance sheet data as of December 31, 2013, 2012 and 2011 set forth below from our audited consolidated financial statements which are not included in this Form 10-K. During 2013, we sold our non-Gaiam branded entertainment media distribution operations and discontinued our DRTV operations. These business are reported as discontinued operations for all periods presented below. At the end of 2011, we deconsolidated our RGSE subsidiary.

13

Table of Contents

The historical operating results are not necessarily indicative of the results to be expected for any other period. You should read the data set forth below in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes, included elsewhere in this Form 10-K.

| Years ended December 31, | ||||||||||||||||||||

| (in thousands, except per share data) |

2015 (a) | 2014 (a) | 2013 (b)(c) | 2012 (c) | 2011 (c) | |||||||||||||||

| Consolidated Statement of Operations Data: |

||||||||||||||||||||

| Net revenues |

$ | 188,018 | $ | 166,694 | $ | 155,463 | $ | 127,242 | $ | 223,691 | ||||||||||

| Cost of goods sold |

103,249 | 91,189 | 90,155 | 70,723 | 144,835 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

84,769 | 75,505 | 65,308 | 56,519 | 78,856 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Expenses: |

||||||||||||||||||||

| Selling and operating |

64,160 | 68,470 | 64,657 | 56,292 | 73,525 | |||||||||||||||

| Corporate, general and administration |

16,428 | 12,121 | 11,325 | 10,400 | 14,221 | |||||||||||||||

| Other general income and expense |

— | — | 10,967 | — | 22,456 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total expenses |

80,588 | 80,591 | 86,949 | 66,692 | 110,202 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from operations |

4,181 | (5,086 | ) | (21,641 | ) | (10,173 | ) | (31,346 | ) | |||||||||||

| Interest and other (expense) income |

(1,406 | ) | (600 | ) | 2,421 | (86 | ) | (90 | ) | |||||||||||

| Gain on sale of investments |

— | 1,480 | 25,096 | — | — | |||||||||||||||

| Loss from equity method investment |

(465 | ) | (55 | ) | — | (18,410 | ) | — | ||||||||||||

| Loss from deconsolidation of subsidiary |

— | — | — | — | (4,550 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before income taxes |

2,310 | (4,261 | ) | 5,876 | (28,669 | ) | (35,986 | ) | ||||||||||||

| Income tax expense (benefit) |

1,219 | 1,369 | 25,974 | (9,444 | ) | (10,713 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) from continuing operations |

1,091 | (5,630 | ) | (20,098 | ) | (19,225 | ) | (25,273 | ) | |||||||||||

| (Loss) income from discontinued operations, net of tax |

(12,103 | ) | (3,327 | ) | (1,995 | ) | 6,648 | 3 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss |

(11,012 | ) | (8,957 | ) | (22,093 | ) | (12,577 | ) | (25,270 | ) | ||||||||||

| Net (income) loss attributable to noncontrolling interest |

(694 | ) | (959 | ) | (659 | ) | (305 | ) | 398 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss attributable to Gaiam, Inc. |

$ | (11,706 | ) | $ | (9,916 | ) | $ | (22,752 | ) | $ | (12,882 | ) | $ | (24,872 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) per share attributable to Gaiam, Inc. common shareholders—basic and diluted: |

||||||||||||||||||||

| From continuing operations |

$ | 0.01 | $ | (0.27 | ) | $ | (0.90 | ) | $ | (0.86 | ) | $ | (1.08 | ) | ||||||

| From discontinued operations |

(0.49 | ) | (0.14 | ) | (0.09 | ) | 0.29 | 0.00 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic and diluted net loss per share attributable to Gaiam, Inc. |

$ | (0.48 | ) | $ | (0.41 | ) | $ | (0.99 | ) | $ | (0.57 | ) | $ | (1.08 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted-average shares outstanding: |

||||||||||||||||||||

| Basic |

24,510 | 24,228 | 22,972 | 22,703 | 23,126 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted |

24,612 | 24,228 | 22,972 | 22,703 | 23,126 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| As of December 31, | ||||||||||||||||||||

| (in thousands) |

2015 | 2014 | 2013 (c) | 2012 (c) | 2011 (c) | |||||||||||||||

| Consolidated Balance Sheet Data: |

||||||||||||||||||||

| Cash |

$ | 13,772 | $ | 15,772 | $ | 32,229 | $ | 9,858 | $ | 14,545 | ||||||||||

| Working capital |

33,168 | 39,699 | 53,674 | 51,418 | 62,217 | |||||||||||||||

| Total assets |

128,542 | 138,632 | 141,686 | 197,231 | 163,290 | |||||||||||||||

| Total liabilities |

39,749 | 39,073 | 36,396 | 78,359 | 32,116 | |||||||||||||||

| Total equity |

88,793 | 99,559 | 105,290 | 118,872 | 131,174 | |||||||||||||||

| Consolidated Cash Flow Data: |

||||||||||||||||||||

| Net cash provided by (used in) operating activities |

$ | 8,156 | $ | (8,969 | ) | $ | (23,124 | ) | $ | 16,476 | $ | 5,240 | ||||||||

14

Table of Contents

| (a) | We recorded non-cash and cash charges of $12.1 million and $3.3 million during 2015 and 2014, respectively, associated with the legal dispute and settlement with Cinedigm. |

| (b) | During 2013, we recognized $11.0 million for certain impairments and restructuring costs, $2.0 million net loss from discontinued operations due to the closure of our DRTV business, and the sale of GVE and a $25.0 million gain on the sale of stock. We also recorded a $23.2 million charge to income tax expense to provide a valuation allowance against our deferred tax assets. |

| (c) | Until December 31, 2011, we accounted for our investment in Real Goods Solar, Inc. (“RGSE”) as a consolidated subsidiary. Total revenues for RGSE were $109.3 million in 2011 and $77.3 million in 2010. Operating loss was $2.3 million in 2011. Net loss for 2011 was $1.9 million. On December 31, 2011, as a result of a decrease in our voting ownership to 37.5%, we converted our accounting for RGSE from consolidated subsidiary to equity method investment. Thus, our consolidated balance sheet data at December 31, 2011 and beyond excludes RGSE’s consolidated balance sheet and our consolidated statement of operations data for 2012 presents RGSE on an equity method investment basis. During May 2013, as a result of the sale of the majority of our ownership to less than 20% and the resignation of our chairman from his position as Chairman of the board of directors for RGSE, we changed the accounting for our investment in RGSE from the equity to cost method. Thus, our consolidated balance sheet data at December 31, 2013 and our consolidated statement of operations data for 2013 reports RGSE as a cost method investment. |

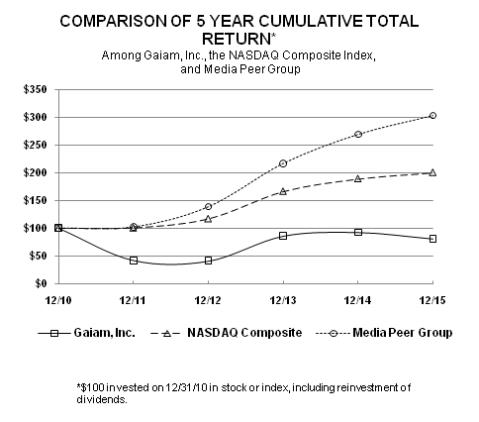

Stock Performance Graph

The graph below shows, for the five years ended December 31, 2015, the cumulative total return on an investment of $100 in our Class A common stock, assuming the investment was made on December 31, 2010. The graph compares such return with that of comparable investments assumed to have been made on the same date in (a) the NASDAQ Stock Market (U.S. Companies) Index and (b) a media peer group, comprised of Martha Stewart Living Omnimedia, Inc.; The Walt Disney Company; and Lions Gate Entertainment Corp. Our Class A common stock is quoted by The NASDAQ Stock Market’s Global Market under the trading symbol GAIA.

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

15

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Forward-Looking Statements

This report contains forward-looking statements that involve risks and uncertainties. When used in this discussion, we intend the words “anticipate,” “believe,” “plan,” “estimate,” “expect,” “strive,” “future,” “intend”, “will” and similar expressions as they relate to us to identify such forward-looking statements. Our actual results could differ materially from the results anticipated in these forward-looking statements as a result of certain factors set forth under “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Quantitative and Qualitative Disclosures About Market Risk” and elsewhere in this Form 10-K. Risks and uncertainties that could cause actual results to differ include, without limitation, general economic conditions, ongoing losses, competition, loss of key personnel, pricing, brand reputation, acquisitions, new initiatives we undertake, security and information systems, legal liability for website content, merchandise supply problems, failure of third parties to provide adequate service, reliance on centralized customer service, overstocks and merchandise returns, our reliance on a centralized fulfillment center, increases in postage and shipping costs, e-commerce trends, future Internet related taxes, our founder’s control of us, litigation, fluctuations in quarterly operating results, consumer trends, customer interest in our products, the effect of government regulation and programs and other risks and uncertainties included in our filings with the Securities and Exchange Commission. We caution you that no forward-looking statement is a guarantee of future performance, and you should not place undue reliance on these forward-looking statements which reflect our views only as of the date of this report. We undertake no obligation to update any forward-looking information.

You should read the following discussion and analysis of our financial condition and results of operations in conjunction with the consolidated financial statements and related notes included elsewhere in this document. This section is designed to provide information that will assist readers in understanding our consolidated financial statements, changes in certain items in those statements from year to year, the primary factors that caused those changes and how certain accounting principles, policies and estimates affect the consolidated financial statements.

Overview and Outlook

We have two reportable business segments which are aligned based on their products or services: Gaiam Brand and Gaia.

Gaiam Brand Segment

Gaiam is a leader in the markets for yoga, fitness and wellness products and media content. Gaiam brands include Gaiam, focused on yoga and fitness; Gaiam Restore, focused on wellness; SPRI focused on fitness; and our eco-travel business.

We develop and market fitness and yoga accessories, apparel, and media under Gaiam’s brands. These products are sold primarily through major national retailers in the United States, Canada, Europe, and other countries, with placement in over 38,000 retail doors worldwide and websites. Our products and services are targeted to all levels of yoga and fitness enthusiasts, including professionals. We believe that consumers are attracted to our products because of their design, functional characteristics, and our unique brand heritage. Our accessories include yoga mats, bags, straps and blocks, media content including digital media and apps, restorative and massage accessories such as rollers, resistance cords and balance balls, and various other offerings. Our comprehensive line of apparel includes pants, shorts, tops and jackets designed around yoga.

Through our business activities, we seek to position our brand as a trusted source for products that are relevant to our consumers’ active lifestyles. Our broad distribution network includes retail, online, and digital channels. Our business is vertically integrated from product design and content creation through product development and sourcing, to customer service and distribution. This efficient supply chain enables us to provide quality products at competitive prices for all of our brands.

We seek to drive sustainable and profitable growth in this segment by leveraging our brands’ leading market positions and heritage to expand our product offering and distribution channels. We believe that growth in yoga participation, greater awareness of health and wellness, and the success of our retail and online partners is increasing consumer interest in our brands and products, and creates new opportunities for us to expand our offering. Recent examples of our brand extension include the 2012 launch of Gaiam Restore and SPRI Dynamic Recovery brands, our at-home rehabilitative and restorative products, and the 2013 launch of our SPRI Cross Train line of high-intensity fitness accessories. In the spring of 2015, we launched a Gaiam branded yoga apparel line extending our brand to a new product segment.

16

Table of Contents

We recently launched or updated certain websites, evolving our e-commerce experience to focus on engaging customers through digital content, and social and mobile marketing across various devices. With the acquisition of Yoga Studio, the leading paid yoga app for mobile and tablet devices in the U.S. App Store, and the launch of our new Meditation Studio app, we will continue to develop and leverage our interactive digital strategy as a point of brand engagement. We plan to invest in our online branding and digital offerings, develop emerging talent, utilize social media, and sponsor local events. Additionally, during 2015 we curtailed the circulation of our consumer catalogs focusing our direct-to-consumer strategy to online channels.

Gaia Segment

Gaia is a global digital video subscription service with approximately 7,000 titles which caters to an underserved subscriber base. Gaia’s digital content is available to subscribers on most Internet connected devices anytime, anywhere commercial free. The subscription also allows subscribers to download and view files from the library without being actively connected to the internet. Through Gaia subscriptions, customers have unlimited access to a vast library of inspiring films, personal growth related content, cutting edge documentaries, interviews, yoga classes, and more – 90% of which is available exclusively to subscribers for digital streaming. More and more, people are augmenting their use of, or veering away from broadcast television and turning to, streaming video to watch their favorite content on services like Netflix, Amazon Prime, Hulu Plus, HBO Go and Gaia.

Gaia’s position in the streaming video landscape is firmly supported by a wide variety of exclusive and unique content, which provides a complementary offering to entertainment-based streaming video services. Gaia’s original content is developed and produced in our in-house production studios near Boulder, Colorado. By offering exclusive and unique content over a streaming service, we believe we will be able to significantly expand our target subscriber base.

In October 2013, Gaia acquired My Yoga Online, the largest on-line yoga video streaming subscription business in Canada. With this acquisition we grew our content library by approximately 1,300 video titles and expanded our international subscriber base. We plan to continue investing in international expansion, both in terms of subscribers and content.

Gaiam’s Board of Directors previously approved the separation of Gaia and Gaiam Brand into two separate publicly traded companies. We currently expect the separation to take the form of a tax-free spin-off to shareholders. Our board of directors has the right and ability, in its sole discretion, to abandon the proposed separation at any time before the distribution date. As a result, there can be no assurance that the separation will occur. Gaia filed the final amendment to its Form 10 on February 17, 2016. Prior to consummating the proposed tax-free spin-off of the subscription business, our board of directors believes it is appropriate to review possible funding structures, enhancements and alternatives for its two primary business units and its eco-travel subsidiary, to maximize shareholder value. The board of directors expects to complete the review process by the end of March, while Gaia finalizes its NASDAQ trading arrangements. The Company does not plan to comment further regarding the review process unless disclosure is legally required.

Results of Operations

Year Ended December 31, 2015 Compared to Year Ended December 31, 2014